Visaka Industries | Cement Products

November 18, 2014

Visaka Industries

BUY

CMP

`123

Initiating Coverage

Target Price

`174

Visaka Industries (VIL) is engaged in two businesses - building products (cement

Investment Period

12 Months

asbestos products and fibre cement flat products like V-boards and V-panels) and

synthetic yarn. It has an installed capacity of 7,52,000MT of cement asbestos

Stock Info

products with a strong network of 6000 plus stockists / dealers across India. In the

synthetic yarn segment it has an installed capacity of

31 MTS M/CS. With

Sector

Cement Products

consumer and business confidence improving in building products segment and

Market Cap (` cr)

196

sustainable performance of its synthetic yarn segment, we expect the company to

Net Debt

205

post a strong performance going ahead.

Beta

1.0

Utilization levels and EBIDTA margins to improve: VIL’s performance in FY2014

52 Week High / Low

143 / 67

was impacted on account of slowdown in economy and high competition, which

Avg. Daily Volume

10,593

were sector related issues. The company’s raw material cost as a percentage of

sales too increased sharply from 58% in FY2013 to 62.8% in FY2014 due to

Face Value (`)

10

increase in asbestos fibre (100% imported) which accounts for ~60% of the raw

BSE Sensex

28,178

material of the building products segment. However, with demand from housing

Nifty

8,431

and infrastructure sector picking up, we expect the utilization levels for its asbestos

Reuters Code

VSKI.BO

cement product business to improve coupled with strong growth momentum in its

Bloomberg Code

VSKI.IN

V-boards segment. Hence, we expect the company to post a 14.9% CAGR in its

top-line over FY2014-16E to `1,177cr. The EBIDTA margins are also expected to

Shareholding Pattern (%)

improve, as currency has stabilized at lower levels compared to FY2014 which

will keep the asbestos fibre cost under check.

Promoters

37.5

MF / Banks / Indian Fls

1.3

Lower depreciation cost in FY2016E to boost profitability: The company’s

FII / NRIs / OCBs

26.7

depreciation cost is expected to increase sharply in FY2015 due to changes made

in the Company’s Act 2013 which lays down the new rates for depreciation of

Indian Public / Others

34.5

fixed assets. However, in FY2016E, the depreciation cost is expected to decline by

~30% yoy which will significantly boost profits. We expect the net profit to grow at

Abs.(%)

3m 1yr

3yr

a CAGR of 81% over FY2014-16E to `39cr. At the current price of `123, the stock

Sensex

6.8

35.1

71.2

is trading at a valuation of 5x FY2016E EPS, which we believe is attractive. We

Visaka

2.8

60.7

70.4

initiate coverage on VIL with a Buy rating and a target price of `174, valuing the

stock at 7x on FY2016E earnings.

Key financials

Y/E March (` cr)

FY2012

FY2013

FY2014 FY2015E

FY2016E

Net sales

750

916

892

968

1177

% chg

15.4

22.0

(2.6)

8.5

21.6

Adj. net profit

34

51

12

17

39

% chg

(23.7)

47.6

(76.3)

38.1

137.1

EBITDA Margin (%)

10.4

11.7

6.4

8.4

8.6

EPS (`)

21.6

31.9

7.5

10.5

24.8

P/E (x)

5.7

3.9

16.3

11.8

5.0

P/BV (x)

0.7

0.6

0.6

0.6

0.5

RoE (%)

12.0

15.6

3.6

4.8

10.5

RoCE (%)

12.6

13.5

5.5

6.1

10.9

Bhavin Patadia

EV/Sales (x)

0.4

0.5

0.4

0.4

0.3

+91-22-3935 7800 Ext: 6868

EV/EBITDA (x)

3.6

3.9

7.0

4.8

3.8

Source: Company, Angel Research; Note: CMP as of November 17, 2014

Please refer to important disclosures at the end of this report

1

Visaka Industries | Initiating Coverage

Investment arguments

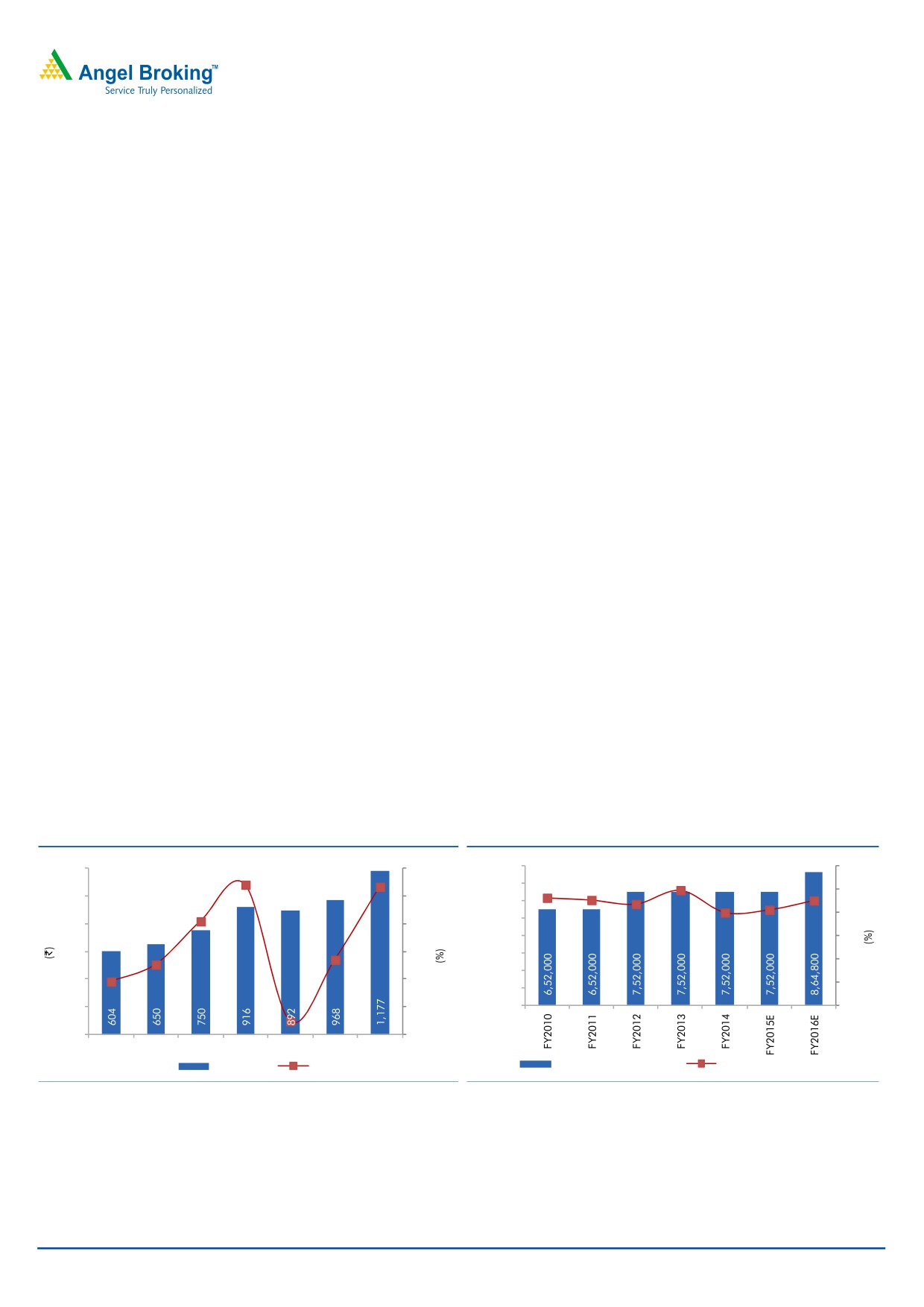

Improvement in utilization levels on revival in demand

VIL’s presence in the building products segment is dominated by cement asbestos

Revival in rural demand to drive future

products (71% of FY2014 revenue). The company has expanded its capacity from

top-line growth

6,52,000MT in FY2011 to 7,52,000MT in FY2012 to cater to the rising rural

demand. However, in FY2014 due to slow down in rural demand led by high food

inflation and lower disposable incomes, the utilization levels dropped sharply for

the cement asbestos products. Despite this, the company was able to retain its

position as the second largest cement asbestos products manufacturer in India with

a 17% market share supported by its outdoor advertising campaign and strong

dealer network. This shows the acceptance of the company’s products and its

ability to stay competitive during slowdowns. The overall de-growth in the segment

was limited by strong performance of its V-boards division (capacity of

1,20,000MT) which grew by a healthy 25.6% yoy. We expect the division to post a

robust performance going ahead as well on account of growing acceptance in

India due to cost advantages against substitute products and increasing

contribution of exports.

The company’s synthetic yarn segment has an installed capacity of 55,000 ring

spindles (31 MT M/CS). The utilization levels for this segment dipped marginally,

but due to strong growth in exports coupled with improvement in realizations due

to rupee depreciation, the company was able to post a revenue growth of 8% in

FY2014. As per the Federation of Indian Chamber of Commerce and Industry

(FICCI), India’s textile exports are expected to rise from US$21bn in 2012 to

US$145.6bn by 2023. This augurs well for the company as it is expected to

increase its focus on the export business which has higher margins.

With consumer and business confidence improving, the utilization levels are

expected to improve gradually which will enable the company to post a revenue

CAGR of 14.9% over FY2014-16E to `1,177cr.

Exhibit 1: Sales growth to rebound

Exhibit 2: Capacity Utilization to improve

1,200

21.6

25

9,00,000

90.0

120

22.0

98.9

8,00,000

87.0

82.0

92.3

90.4

79.7

100

1,000

20

7,00,000

15.4

80

6,00,000

800

15

7.6

5,00,000

60

600

10

4,00,000

8.5

40

3,00,000

400

5

20

4.5

2,00,000

200

0

1,00,000

0

(2.6)

0

-5

FY2010

FY2011

FY2012

FY2013

FY2014 FY2015E FY2016E

Net Sales

Sales growth

Installed Capacity (MT)

Utilization levels (%)

Source: Company, Angel Research

Source: Company, Angel Research

November 18, 2014

2

Visaka Industries | Initiating Coverage

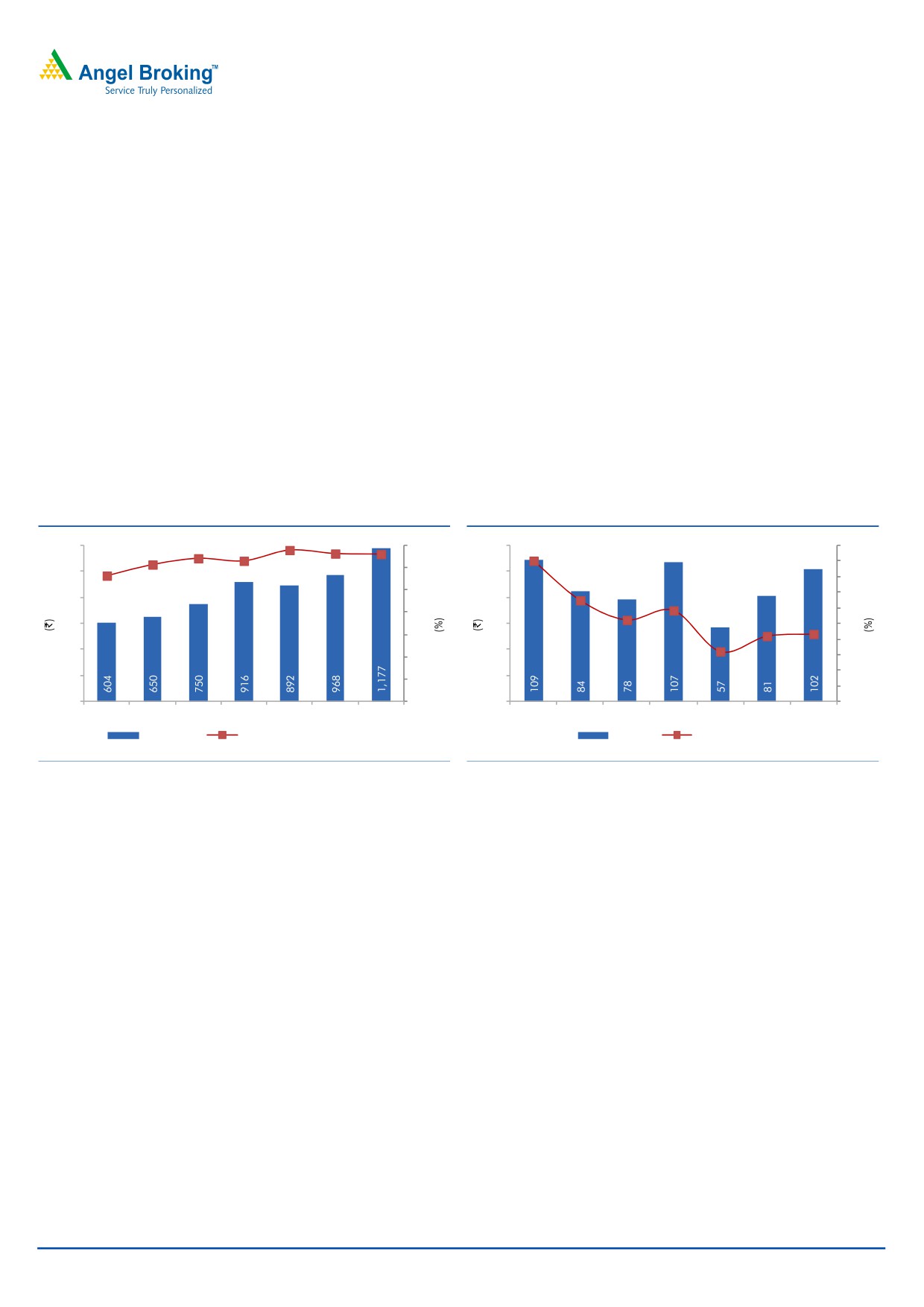

EBIDTA margin to witness an uptrend

The company’s net raw-material cost as a percentage of sales is expected to

Stability in key raw material prices and

decline to ~61% in FY2016E from 62.8% in FY2014 on account of stable prices of

higher exports to aid margin expansion

its key raw materials and stable currency rates. Asbestos fibre, the key raw material

for asbestos cement products is 100% imported and accounts for 60% of raw

material cost of building products segment. Sharp fall in rupee in FY2014 led to

increase in landed cost which impacted the segment margins. However, with rupee

stabilizing, the prices are expected to remain flat going ahead. Besides asbestos

fibre, cement and fly ash prices are also expected to remain flat. Freight costs too

are expected to remain stable as diesel prices have cooled down. The increase in

power costs due to power crisis in Andhra Pradesh and Tamilnadu would be offset

by the company’s newly commissioned 2.5MW solar power plant. The company is

expected to increase exports in its synthetic yarn business, which has higher

margins. As a result, the EBIDTA margin will witness a northward shift from 6.4%

in FY2014 to 8.6% in FY2016E.

Exhibit 3: Raw material cost to decline steadily

Exhibit 4: ...leading to higher EBIDTA margins

62.8

61.0

1200

59.1

61.2

65

120

20

56.3

58.0

18.0

18

51.4

55

1000

100

16

13.0

45

11.7

14

800

80

35

10.4

12

8.4

8.6

600

60

10

25

6.4

8

400

40

15

6

4

200

20

5

2

0

-5

0

0

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

Net Sales

Raw material as % of net sales

EBIDTA

EBIDTA margins

Source: Company, Angel Research

Source: Company, Angel Research

November 18, 2014

3

Visaka Industries | Initiating Coverage

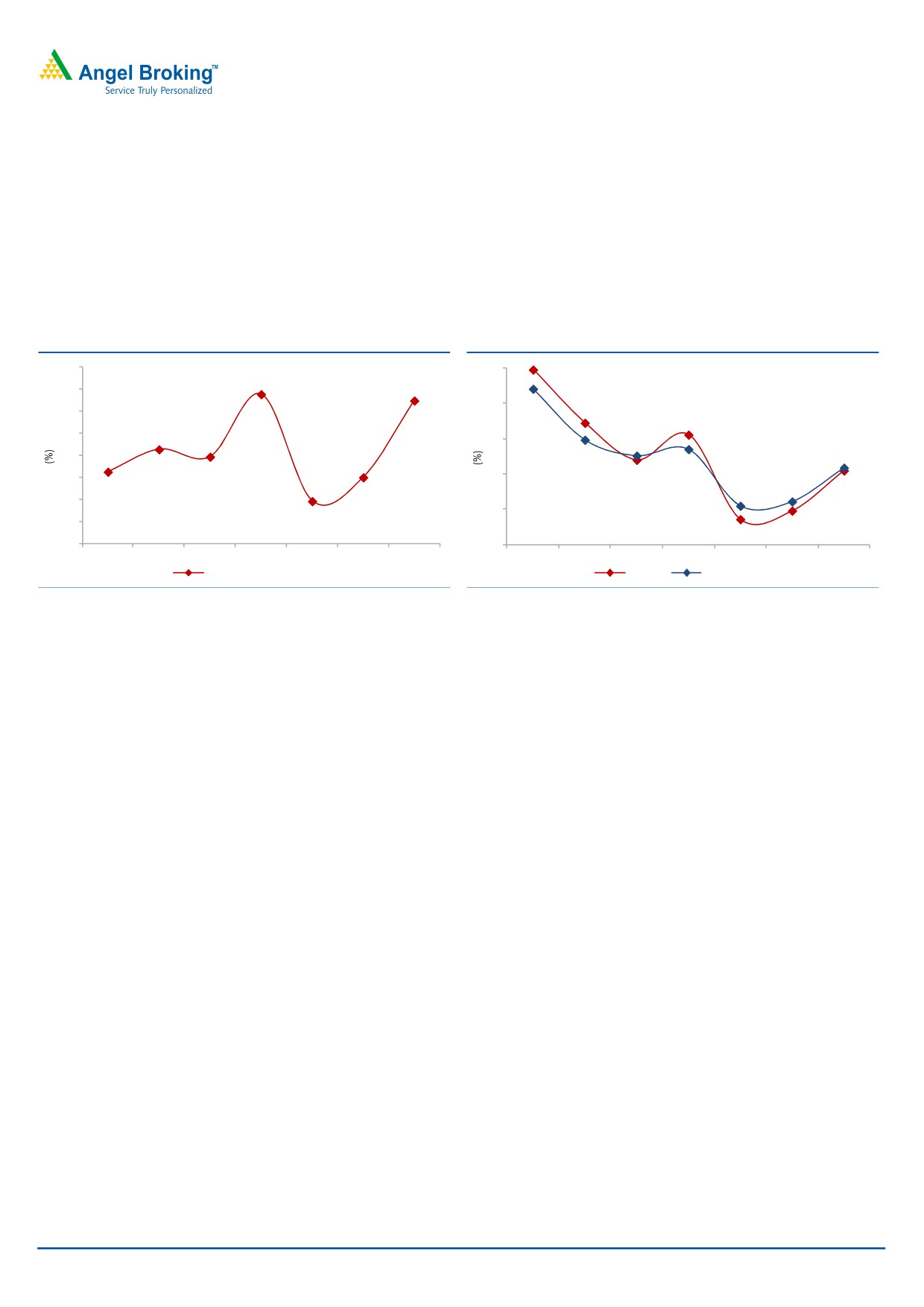

Asset turnover and return ratios to improve

With capacity in place to cater to the expected rise in overall demand, the

utilization levels are expected to improve. This will lead to higher sales, resulting in

higher asset turnover (Gross block) from 1.7x in FY2014 to 2.1x in FY2016E. The

ROCE is expected to improve from 5.5% in FY2014 to 10.9% in FY2016E. Also,

with improvement in profitability the ROE is expected to improve from 3.6% in

FY2014 to 10.5% in FY2016E.

Exhibit 5: Asset turnover to improve

Exhibit 6: Return ratios to see recovery

2.3

25

24.8

2.2

2.2

2.1

20

22.1

17.2

2.1

15.6

2.0

1.9

1.9

15

12.0

1.9

10.5

1.8

14.8

1.8

13.5

10

12.6

1.8

10.9

1.7

4.8

3.6

1.7

5

1.6

5.5

6.1

1.5

0

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

Asset Turnover (Gross Block)

ROE

ROCE (Pre-tax)

Source: Company, Angel Research

Source: Company, Angel Research

November 18, 2014

4

Visaka Industries | Initiating Coverage

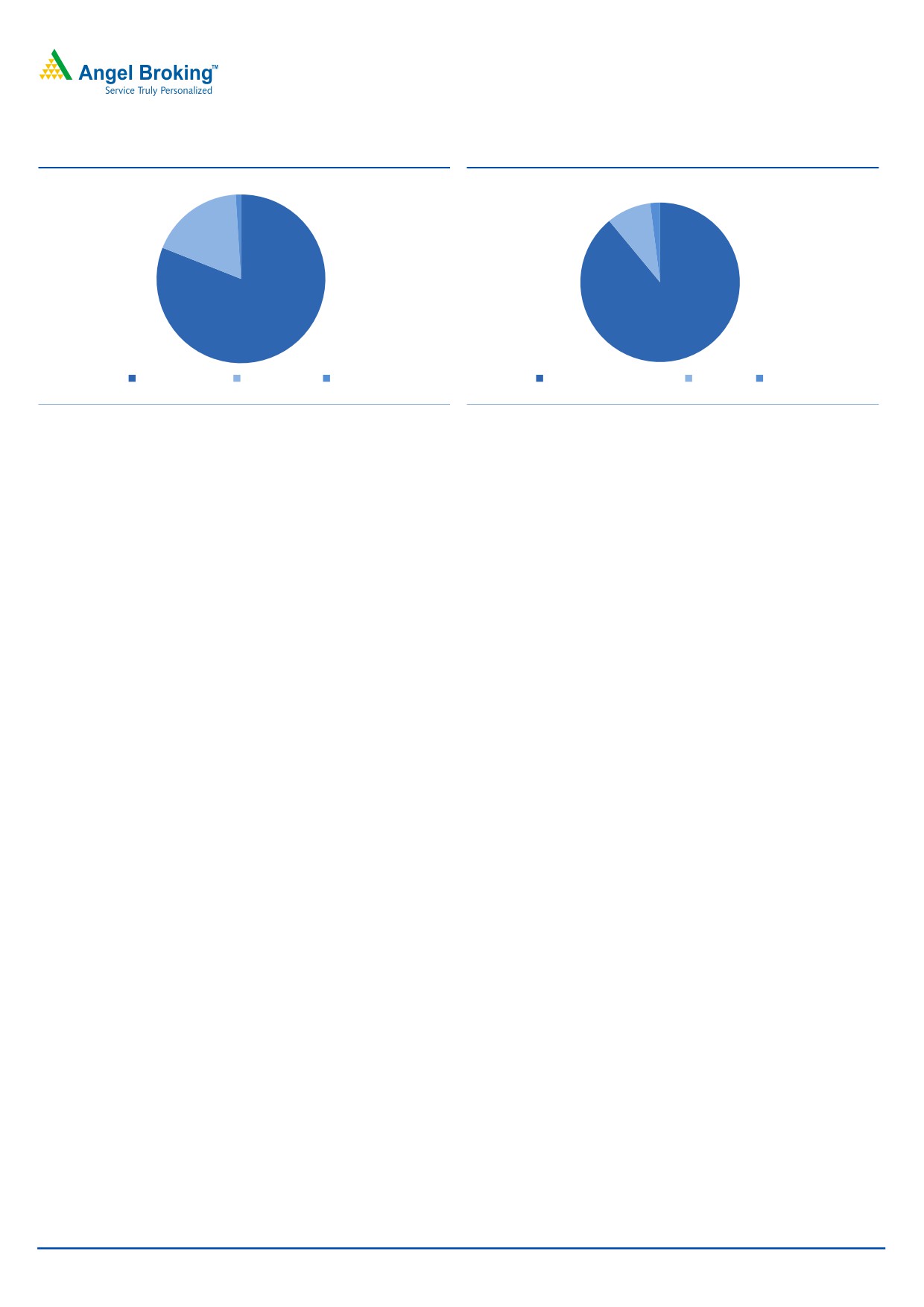

Exhibit 7: Segment wise revenue breakup

Exhibit 8: Building products’ revenue breakup

1%

2%

9%

18%

81%

89%

Building products

Synthetic Yarn

Others

Asbestos Cement Products

V- Boards

V - Pannel

Source: Company, Angel Research

Source: Company, Angel Research

Segment and Industry Outlook

Building Products

The company’s building products segment includes cement asbestos products,

V - boards (fibre cement sheets) and V - panels.

Cement asbestos products: Currently there are about 20 entities in the industry

with about 68 manufacturing plants throughout the country. Top five players

including VIL have a market share of 70-75%. Rural infrastructure is a key social

priority of the government. The huge housing deficit in rural India, with a majority

of houses being kaccha houses, offers tremendous opportunity of sustained growth

of new age construction practices as well as building products. Looking ahead,

with the ambitious 12th Five-year plan in place along with a stable government in

the country, the income of the under-privileged section is expected to go up. This

should translate into an increased demand for roofing products such as fibre

cement roofing sheets.

The industry is currently operating at lower utilization levels. Going ahead, if the

demand improves from here on, existing capacities are enough to cater through

higher utilization. Industry performance is directly linked to performance of

rural/semi-urban economies. Consumer inflation, food inflation and rural growth

are other driving factors for this segment. Cement asbestos sheets are popular as

they are inexpensive; they need no maintenance and last long when compared to

competing products such as thatched roofs, tiled roofs and galvanized iron sheets.

VIL has a total of 8 plants located in India with an installed capacity of

7,52,000MT. The company is the second largest cement asbestos products

manufacturer in India with a 17% market share. The company has a strong

distribution network comprising over 6,000 retailers (rural and the semi-urban

markets). The company derives 85% of its sales from these markets while the rest is

derived from institutional sales, governmental agencies, industries and poultry

farms.

November 18, 2014

5

Visaka Industries | Initiating Coverage

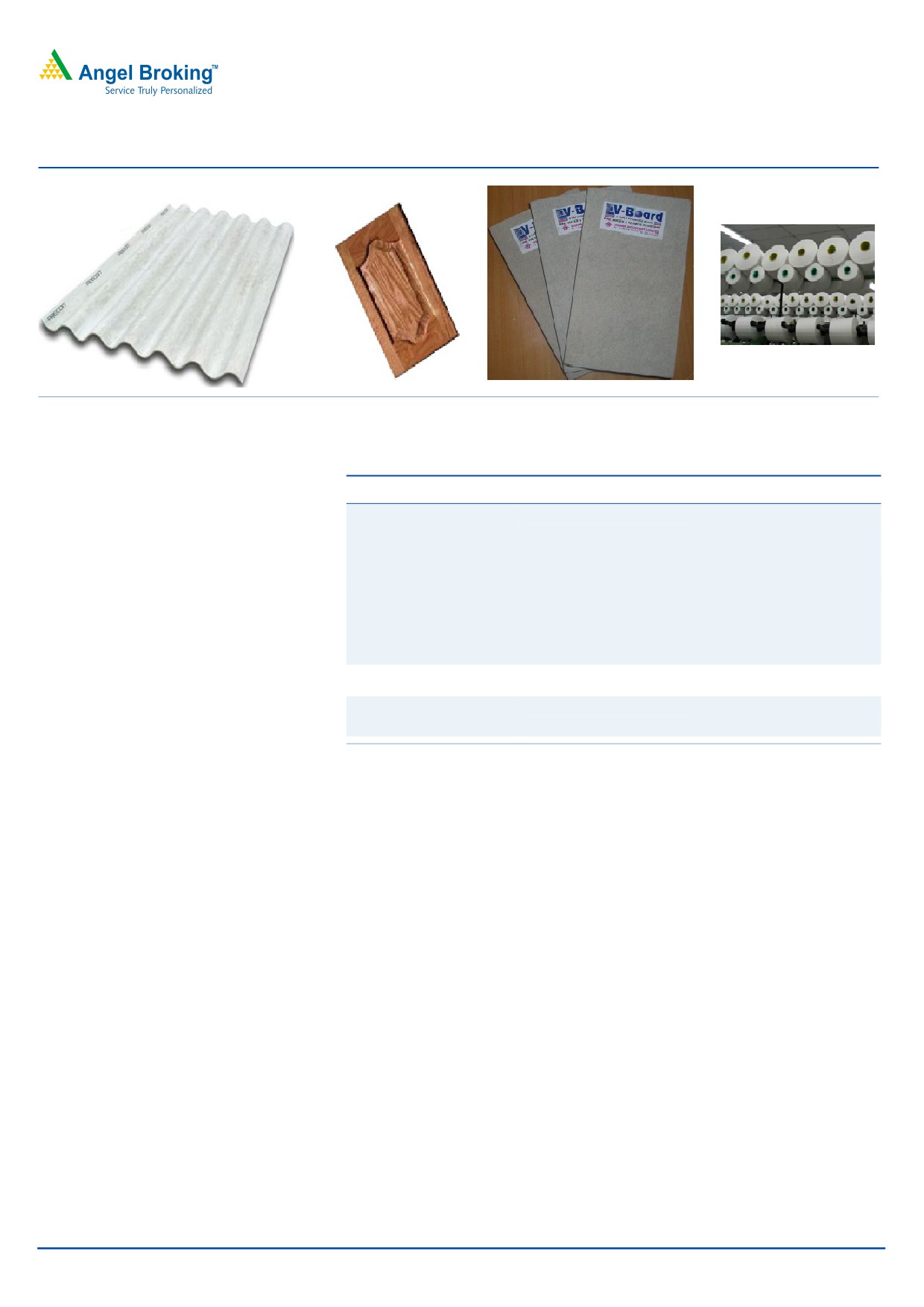

Exhibit 9: Product Profile

Source: Company

Exhibit 10: Products

Products

Manufacturing facility

Cumulative installed capacity

Patancheru (Andhra Pradesh)

Vijayawada (Andhra Pradesh)

Paramathi (Tamil Nadu)

Tumkur (Karnataka)

Cement Asbestos Facility

7,52,000 MT

Midnapur (West Bengal)

Rae Bareli (Uttar Pradesh)

Pune (Maharashtra)

Sambalpur (Odisha)

Fibre cement flat board

Miryalguda (Andhra Pradesh)

1,29,750 MT

products

Daund (Maharashtra)

Synthetic Yarn

31 MTS M/CS

Nagpur (Maharashtra)

Source: Company

Fibre Cement Sheets (Non-Asbestos) - V-BOARDS AND V-PANELS: The capacity of

the industry producing same or similar products is 396000MTPA with 8 players in

total. In the last few years, the use of flat products (V-boards and V-panels)

increased on account of a superior price-value proposition over alternatives. They

bring in the triple advantage of being fireproof, water-resistant and termite-resistant.

Also, they are easy to fix and take comparatively lesser time for installation.

The company possesses an installed capacity of 1,20,000MT of V-boards (fibre

cement flat sheets) and 9,750MT of V-panels. The company recently commissioned

a 72,000 TPA plant at Daund (Pune) to address growing product demand. The

company is continuously exploring new markets in various countries and has taken

initiatives to export V - boards, and has witnessed a fair amount of success.

Synthetic Yarn: VIL diversified into the manufacture of synthetic yarn in 1992. Its

textile division manufactures yarns using state-of-the-art twin air jet spinning

machines (Murata, Japan) with 31 MTS machines (equivalent to 55,000 ring

spindles) where yarn quality is superior to conventional ring frame yarn. The

company manufactures value-added yarn, enjoying some of the highest margins

in the segment. The company plans to increase its capacity by 10% in FY2016E.

The company gets better margins in the segment from export earnings. Hence, it

plans to increase exports from 25% to 40% by FY2016E.

November 18, 2014

6

Visaka Industries | Initiating Coverage

Financials

Exhibit 11: Key assumptions

Particulars (%)

FY2015E

FY2016E

Total revenue growth (yoy)

8.5

21.6

Asbestos Cement Products

Capacity Utilization (%)

82

90

Realization growth (%)

1

5

Revenue growth (yoy)

7

20.5

V-Boards

Capacity Utilization (%)

48

55

Realization growth (%)

1.5

2

Synthetic Yarn

Volume growth (yoy)

5.1

11.1

Realization growth (%)

3.0

2.0

Revenue growth (yoy)

8.2

13.3

Source: Angel Research

Top line to grow at a 14.9% CAGR over FY2014-16E

We expect the company’s net sales to grow at a CAGR of 14.9% over FY2014-

16E, from `892cr to `1,177cr due to higher capacity utilization on the back of

expected revival in rural demand and strong performance of its V-boards division.

The sales (gross) from the building products segment is expected to increase from

`792cr in FY2014 to `1,064cr by FY2016E, while the sales (gross) from V-board

are expected to increase from `68cr to `128cr, during the same period. Sales

(gross) from synthetic yarn segment are expected to increase from `178cr in

FY2014 to `218cr in FY2016E, led by improvement in realization due to higher

exports.

EBIDTA and EBITDA margins to improve

In FY2014, the EBIDTA and EBIDTA margins declined sharply due to increase in

raw material cost and higher advertisement & sales promotion expenses. EBIDTA

fell to `57cr in FY2014 from `107cr in FY2013 while the EBIDTA margins decline

to 6.4% in FY2014 from 11.7% in FY2013. With stable raw material cost in

building products segment due to stable rupee coupled with higher exports

contribution in synthetic yarn segment, the EBIDTA is expected to grow at a CAGR

of 33.3% to `102cr by FY2016E. As a result, EBIDTA margins are expected to

improve from 6.4% in FY2014 to 8.6% in FY2016E.

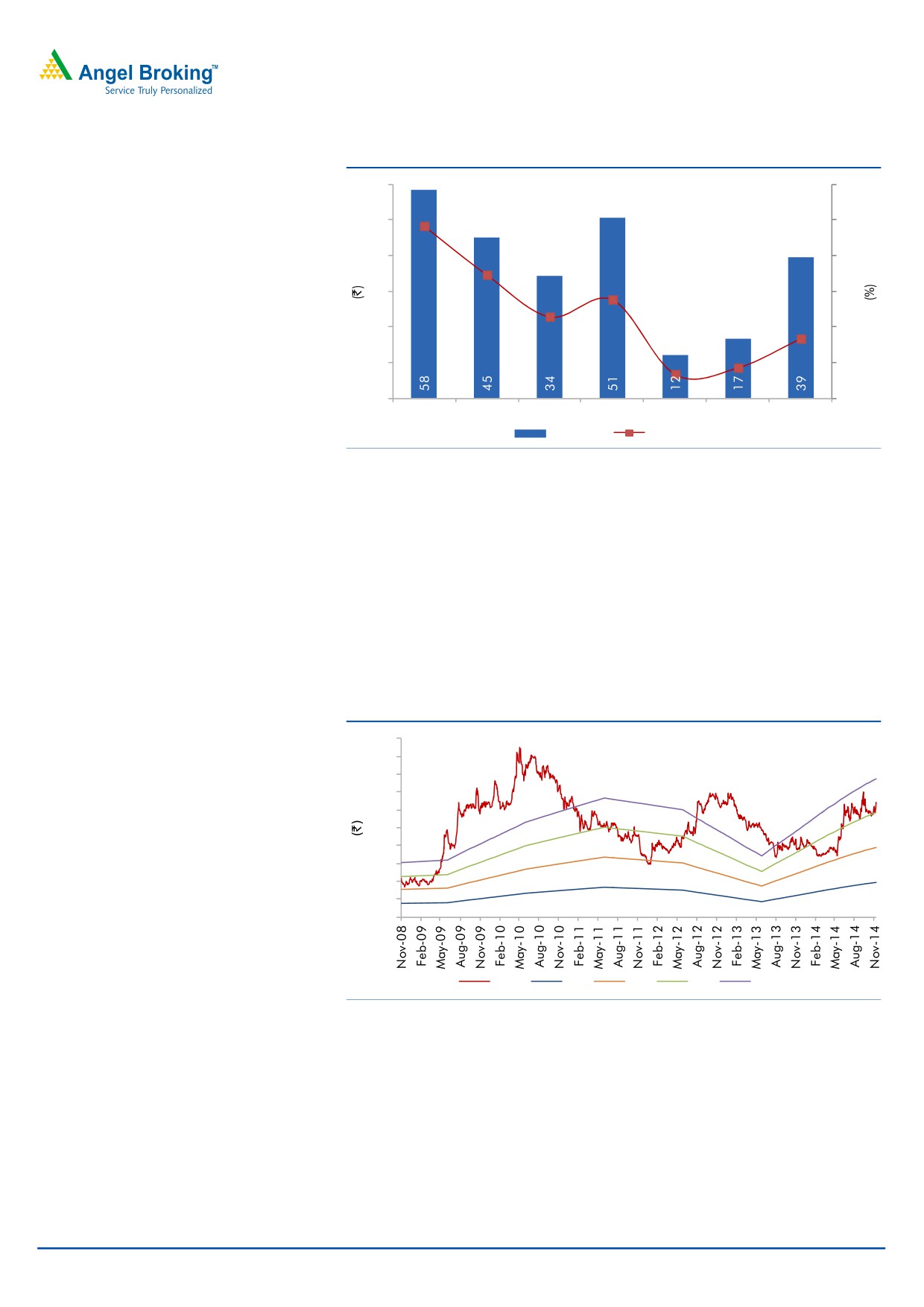

PAT to grow at a CAGR of 81% over FY2014-16E

With improvement in EBIDTA margins coupled with lower depreciation cost,

specifically in FY2016E, the PAT is expected to grow at a CAGR of 81% over

FY2014-16E to `39cr. As a result, the PAT margins are expected to improve from

1.3% in FY2014 to 3.3% in FY2016E.

November 18, 2014

7

Visaka Industries | Initiating Coverage

Exhibit 12: PAT and PAT margins to improve

60

12

50

10

9.7

40

8

6.9

30

6

5.5

4.6

20

4

3.3

10

2

1.7

1.3

0

0

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

ADJ. PAT

PAT margins

Source: Company, Angel Research

Outlook and valuation

We expect net sales and EBIDTA to register a CAGR of 14.9% and 33.3% to

`1177cr and `102cr respectively, over FY2014-16E. As a result, the net profit is

expected to grow at a CAGR of 81% over FY2014-16E to `39cr. At the current

market price the stock is trading at a P/E of 5x on FY2016E earnings.

On account of expected revival in rural demand aided by government’s focus on

low cost housing, we initiate coverage on the stock with a Buy rating and with a

target price of `174, valuing the stock at 7x on FY2016E earnings.

Exhibit 13: One-year forward PE band

200

180

160

140

120

100

80

60

40

20

0

Price

2 x

4 x

6 x

8 x

Source: Company, Angel Research

November 18, 2014

8

Visaka Industries | Initiating Coverage

Relative valuation

The leading players in the industry are Hyderabad Industries, Visaka Industries,

Everest Industries and Ramco Industries. These companies account for 70-75% of

industry capacity. VIL is trading at cheap valuations of 5x P/E and 0.5x P/BV on

FY2016E as compared to its peers which are trading at relatively high valuations.

Exhibit 14: Comparative analysis

EV/

EV/

Company

Year end

Mcap

Sales

OPM PAT

EPS

RoE

P/E

P/BV

Sales

EBIDTA

Visaka Industries

FY2015E

196

968

8.4

17

10.5

4.8

11.8

0.6

0.4

4.8

FY2016E

196

1,177

8.6

39

24.8

10.5

5.0

0.5

0.3

3.8

Everest Industries*

FY2015E

457

1,228

6.4

35

22.3

12.0

13.3

1.4

0.5

8.2

FY2016E

457

1,375

7.5

51

33.7

15.3

8.8

1.3

0.5

6.3

Hyderabad Industries* FY2015E

521

1,143

10.0

62

83.3

15.4

8.3

1.2

0.5

5.1

FY2016E

521

1,364

11.7

89

119.5

19.8

5.8

1.1

0.4

3.6

Source: Company, Angel Research, *Bloomberg

Key concerns

Increase in input costs due to rupee depreciation: The continuous increase in cost

of inputs is a matter of concern. Asbestos fibre, cement and fly ash and polyester

fibre are the key materials. Asbestos fibre is a key raw material and accounts for

60% of overall cost and is 100% imported. Since exports are limited and imports

are significant, the company is exposed to forex risk.

Dependence on rural growth: Rural demand for housing is the key growth driver

which depends upon increase in spending power and government schemes. High

inflation and lower spend could have adverse impact for roofing in rural India.

Activities of Ban Asbestos Lobby: Asbestos fibre has been included with other forms

of asbestos, in being considered to be a human carcinogen by the International

Agency for Research on Cancer (IARC) and by the U.S. Department of Health and

Human Services. Any government initiative to completely ban or restrict use of

asbestos fibre will be key negative.

Lack of entry barriers: Lack of entry barriers is attracting new entrants into this line

of business. Closure of Canadian and Zimbabwean asbestos mines are a matter

of concern.

November 18, 2014

9

Visaka Industries | Initiating Coverage

Company Background

Visaka Industries (established 1985) is engaged in two businesses - building

products (cement asbestos products and fibre cement flat products like V-Boards

and V-Panels) and textiles. Its manufacturing facilities are spread across

11

locations supported by nine marketing offices. The company is the second largest

cement asbestos products manufacturer in India with a 17% market share. The

spinning plant, with 31 MURATA Twinjet spinning machines and 112 Two-For-One

twisting machines, is the world's largest installation of its kind, producing about

9,000 tons of yarns per annum.

November 18, 2014

10

Visaka Industries | Initiating Coverage

Profit and Loss

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015E

FY2016E

Net Sales

750

916

892

968

1,177

Other operating income

-

-

-

-

-

Total operating income

750

916

892

968

1,177

% chg

15.4

22.0

(2.6)

8.5

21.6

Net Raw Materials

444

531

560

593

718

% chg

21.1

19.7

5.5

5.8

21.1

Power and Fuel costs

39

51

48

51

62

% chg

15.2

31.4

(6.4)

7.4

21.6

Personnel

42

47

52

56

69

% chg

25.1

12.2

10.6

8.5

21.6

Selling & Admin Expenses

71

80

86

92

112

% chg

2.7

11.9

8.7

6.4

21.6

Other

77

101

88

94

115

% chg

91.8

30.9

(12.1)

6.6

21.6

Total Expenditure

672

809

835

887

1,075

EBITDA

78

107

57

81

102

% chg

(7.0)

36.1

(46.3)

41.5

25.5

EBITDA Margin

10.4

11.7

6.4

8.4

8.6

Depreciation & Amortisation

18

20

22

43

30

EBIT

61

87

35

39

72

% chg

(10.5)

43.4

(60.0)

10.6

86.7

(% of Net Sales)

8.1

9.5

3.9

4.0

6.1

Interest & other Charges

14

15

21

19

18

Other Income

5

3

5

5

5

(% of Net Sales)

0.6

0.3

0.6

0.6

0.5

Recurring PBT

47

72

13

19

53

% chg

(19.2)

54.8

(81.4)

44.6

174.9

PBT (reported)

51

75

19

25

59

Tax

17

24

7

8

19

(% of PBT)

33.0

32.1

36.3

33.0

33.0

PAT (reported)

34

51

12

17

39

Extraordinary Expense/(Inc.)

(0.1)

(0.1)

(0.1)

-

-

ADJ. PAT

34

51

12

17

39

% chg

(23.7)

47.6

(76.3)

38.1

137.1

(% of Net Sales)

4.6

5.5

1.3

1.7

3.3

Basic EPS (`)

21.6

31.9

7.5

10.5

24.8

Fully Diluted EPS (`)

21.6

31.9

7.5

10.5

24.8

% chg

(23.8)

47.6

(76.4)

38.8

137.1

November 18, 2014

11

Visaka Industries | Initiating Coverage

Balance Sheet

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015E

FY2016E

SOURCES OF FUNDS

Equity Share Capital

16

16

16

16

16

Preference Capital

-

-

-

-

-

Reserves& Surplus

271

310

317

329

360

Shareholders’ Funds

286

326

333

345

375

Minority Interest

-

-

-

-

-

Total Loans

152

270

246

231

231

Other long term liabilities

18

21

24

24

24

Net Deferred tax liability

25

26

30

30

30

Total Liabilities

482

644

633

630

660

APPLICATION OF FUNDS

Gross Block

396

421

527

537

548

Less: Acc. Depreciation

152

171

192

235

265

Net Block

244

250

334

302

283

Capital Work-in-Progress

4

16

21

16

12

Lease adjustment

-

-

-

-

-

Goodwill

-

-

-

-

-

Investments

15

15

15

15

15

Other non-current assets

0

0

0

0

0

Current Assets

300

419

341

378

453

Cash

54

34

26

24

22

Loans & Advances

16

26

30

39

47

Other current assets

-

-

-

-

-

Current liabilities

92

96

96

102

123

Net Current Assets

207

323

245

276

329

Mis. Exp. not written off

-

-

-

-

-

Total Assets

482

644

633

630

660

November 18, 2014

12

Visaka Industries | Initiating Coverage

Cash flow statement

Y/E March (` cr)

FY2012

FY2013 FY2014 FY2015E FY2016E

Profit Before Tax

51

75

19

25

59

Depreciation

18

20

22

43

30

Other Income

(5)

(3)

(5)

(5)

(5)

Change in Working Capital

(1)

(136)

71

(34)

(55)

Direct taxes paid

(17)

(24)

(7)

(8)

(19)

Cash Flow from Operations

46

(68)

100

20

9

(Incr)/ Decr in Fixed Assets

(55)

(37)

(111)

(5)

(7)

(Incr)/Decr In Investments

14

(29)

22

(3)

0

Other Income

5

3

5

5

5

Cash Flow from Investing

(35)

(63)

(83)

(3)

(1)

Issue of Equity/Preference

-

-

-

-

-

Incr/(Decr) in Debt

(0)

123

(18)

(15)

0

Dividend Paid (Incl. Tax)

(9)

(11)

(5)

(5)

(9)

Others

(1)

(1)

(1)

-

-

Cash Flow from Financing

(11)

111

(24)

(20)

(9)

Incr/(Decr) In Cash

0

(20)

(7)

(3)

(2)

Opening cash balance

54

54

34

26

24

Closing cash balance

54

34

26

24

22

Source: Company, Angel Research

November 18, 2014

13

Visaka Industries | Initiating Coverage

Key Ratios

Y/E March

FY2012

FY2013

FY2014

FY2015E

FY2016E

Valuation Ratio (x)

P/E (on FDEPS)

5.7

3.9

16.3

11.8

5.0

P/CEPS

3.8

2.8

5.7

3.3

2.8

P/BV

0.7

0.6

0.6

0.6

0.5

Dividend yield (%)

4.7

5.7

2.4

2.4

4.8

EV/Net sales

0.4

0.5

0.4

0.4

0.3

EV/EBITDA

3.6

3.9

7.0

4.8

3.8

EV / Total Assets

0.6

0.6

0.6

0.6

0.6

Per Share Data (`)

EPS (Basic)

21.6

31.9

7.5

10.5

24.8

EPS (fully diluted)

21.6

31.9

7.5

10.5

24.8

Cash EPS

32.8

44.3

21.7

37.3

43.6

DPS

5.0

6.0

2.5

2.5

5.0

Book Value

180.4

205.3

209.9

217.5

236.4

DuPont Analysis

EBIT margin

8.1

9.5

3.9

4.0

6.1

Tax retention ratio

0.7

0.7

0.6

0.7

0.7

Asset turnover (x)

1.8

1.6

1.6

1.7

1.9

ROIC (Post-tax)

10.0

10.2

3.9

4.5

7.9

Cost of Debt (Post Tax)

6.3

3.8

5.5

5.5

5.4

Leverage (x)

0.3

0.7

0.6

0.6

0.5

Operating ROE

11.0

14.6

2.9

3.9

9.2

Returns (%)

ROCE (Pre-tax)

12.6

13.5

5.5

6.1

10.9

Angel ROIC (Pre-tax)

14.9

15.0

6.1

6.7

11.8

ROE

12.0

15.6

3.6

4.8

10.5

Turnover ratios (x)

Asset TO (Gross Block)

1.9

2.2

1.7

1.8

2.1

Inventory / Net sales (days)

74

85

94

76

73

Receivables (days)

35

32

38

38

35

Payables (days)

45

38

39

38

38

WC cycle (ex-cash) (days)

74

88

104

89

87

Solvency ratios (x)

Net debt to equity

0.3

0.7

0.6

0.6

0.5

Net debt to EBITDA

1.1

2.1

3.6

2.4

1.9

Int. Coverage (EBIT/ Int.)

4.3

5.8

1.6

2.0

3.9

November 18, 2014

14

Visaka Industries | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important 'Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Visaka Industries

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to 15%)

Sell (< -15%)

November 18, 2014

15

Visaka Industries | Initiating Coverage

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Amarjeet Maurya

Analyst

Bharat Gianani

Analyst

Shrenik Gujrathi

Analyst

Umesh Matkar

Analyst

Twinkle Gosar

Analyst

Tejas Vahalia

Research Editor

Technicals and Derivatives:

Siddarth Bhamre

Head - Technical & Derivatives

Sameet Chavan

Technical Analyst

Sneha Seth

Associate (Derivatives)

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Assistant Manager

Production Team:

Dilip Patel

Production Incharge

CSO & Registered Office: G-1, Ackruti Trade Centre, Road No. 7, MIDC, Andheri (E), Mumbai - 93. Tel: (022) 3083 7700. Angel Broking Pvt. Ltd: BSE Cash: INB010996539 / BSE F&O: INF010996539, CDSL Regn. No.: IN - DP - CDSL - 234 - 2004, PMS Regn. Code: PM/INP000001546, NSE Cash: INB231279838 /

NSE F&O: INF231279838 / NSE Currency: INE231279838, MCX Stock Exchange Ltd: INE261279838 / Member ID: 10500. Angel Commodities Broking (P) Ltd.: MCX Member ID: 12685 / FMC Regn. No.: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn. No.: NCDEX / TCM / CORP / 0302.

November 18, 2014

16