Initiating Coverage | Lubricants

September 2, 2014

Tide Water Oil India

BUY

CMP

`12,076

On the path of growth

Target Price

`14,704

Stock trading at a discount to its peers; provides good investment opportunity: We

Investment Period

12 Months

like Tide Water Oil India Ltd (TWOIL) given its well established product portfolio in

Stock Info

the lubricants segment, strong brand recall and large distribution network. The

Sector

Lubricants

company is consistent gaining market share over the last several years. On the

Market Cap (` cr)

1,050

financials front, the company has a strong balance sheet with zero debt, healthy

net cash position and delivers healthy return ratios. On the valuation front, the

Net Debt (` cr)

119

company is trading at a discount compared to its close peers like Gulf Oil

Beta

0.5

Lubricants India and Castrol India. Currently the company is trading at a discount

52 Week High / Low

13,005 / 6,556

of more than 20% (one year forward PE) to its close peer Gulf Oil Lubricants India

Avg. Daily Volume

818

and at a discount of more than 50% to Castrol India’s PE valuation. Considering

Face Value (`)

10

the above factors, ie market share gains, healthy return ratios and attractive

BSE Sensex

26,868

valuation, we believe the company presents a good investment opportunity.

Nifty

8,028

Reuters Code

TIDE.BO

Consistently gaining market share despite subdued industry scenario: Over the

Bloomberg Code

TWO@IN

last 12 years, TWOIL has shown continuous improvement in market share (the

company’s market share has surged from 2.9% in FY2003 to 4.7% in FY2013)

owing to its strong brands (Veedol, Prima, Turbo etc), wide distribution network

Shareholding Pattern (%)

and good quality of products. On the other hand, other PSU players and private

Promoters

26.2

players like Castrol India have been losing market share. Going forward, we

MF / Banks / Indian Fls

11.3

believe that the lubricant industry will report an improvement in volume growth

FII / NRIs / OCBs

0.0

owing to improvement in Indian economy which will benefit TWOIL.

Indian Public / Others

62.5

Outlook and Valuation: We forecast TWOIL to report standalone net sales CAGR

of ~9% over FY2014-16E to ~`1,196cr and standalone net profit CAGR of ~7%

Abs. (%)

3m 1yr

3yr

during the same period to `78cr. At the current market price of `12,076, the

Sensex

10.9

44.3

59.7

stock trades at a PE of 14.6x and 13.1x its FY2015E and FY2016E EPS of `828.6

TWOIL

30.8

77.6

80.7

and

`919.0, respectively. We initiate coverage on the stock with a Buy

recommendation and target price of `14,704, based on 16x FY2016E EPS,

indicating an upside of ~22% from the current levels.

Key financials (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

Net sales

954

1,007

1,089

1,196

% chg

19.1

5.6

8.1

9.8

Net profit (Reported)

63

68

70

78

% chg

6.5

8.6

3.1

10.9

EBITDA margin (%)

9.8

9.1

9.4

9.4

EPS (`)

740.4

804.0

828.6

919.0

P/E (x)

16.3

15.0

14.6

13.1

P/BV (x)

3.0

2.7

2.3

2.1

RoE (%)

18.6

17.7

16.1

15.9

RoCE (%)

24.8

21.5

21.2

21.0

Amarjeet S Maurya

EV/Sales (x)

1.0

0.9

0.8

0.7

022-39357800 Ext: 6831

EV/EBITDA (x)

9.9

9.9

8.7

7.8

Source: Company, Angel Research, Note: CMP as of September 1, 2014

Please refer to important disclosures at the end of this report

1

Tide Water Oil India | Initiating Coverage

Investment arguments

Stock trading at discount to its close peers; provides good

investment opportunity

We expect the company to perform better on the top-line and the bottom-line

fronts, going forward. We like the company given its well established product

portfolio in the lubricants segment, strong brand recall and large distribution

network. The company is consistent gaining market share despite poor

performance of the industry. On the financials front, the company has a strong

Currently the company is trading at a

balance sheet with zero debt, healthy net cash position and delivers healthy return

discount of more than 20% (one year

ratios.

forward PE) to its close peer Gulf Oil

On the valuation front, the company is trading at a discount compared to its close

Lubricants India and at a discount of

peers like Gulf Oil Lubricants India and Castrol India. Currently the company is

more than 50% to Castrol India’s PE

trading at a discount of more than 20% (one year forward PE) to its close peer Gulf

valuation

Oil Lubricants India and at a discount of more than 50% to Castrol India’s PE

valuation. Considering the above factors, ie market share gains, healthy return

ratios and attractive valuation, we believe the company presents a good investment

opportunity.

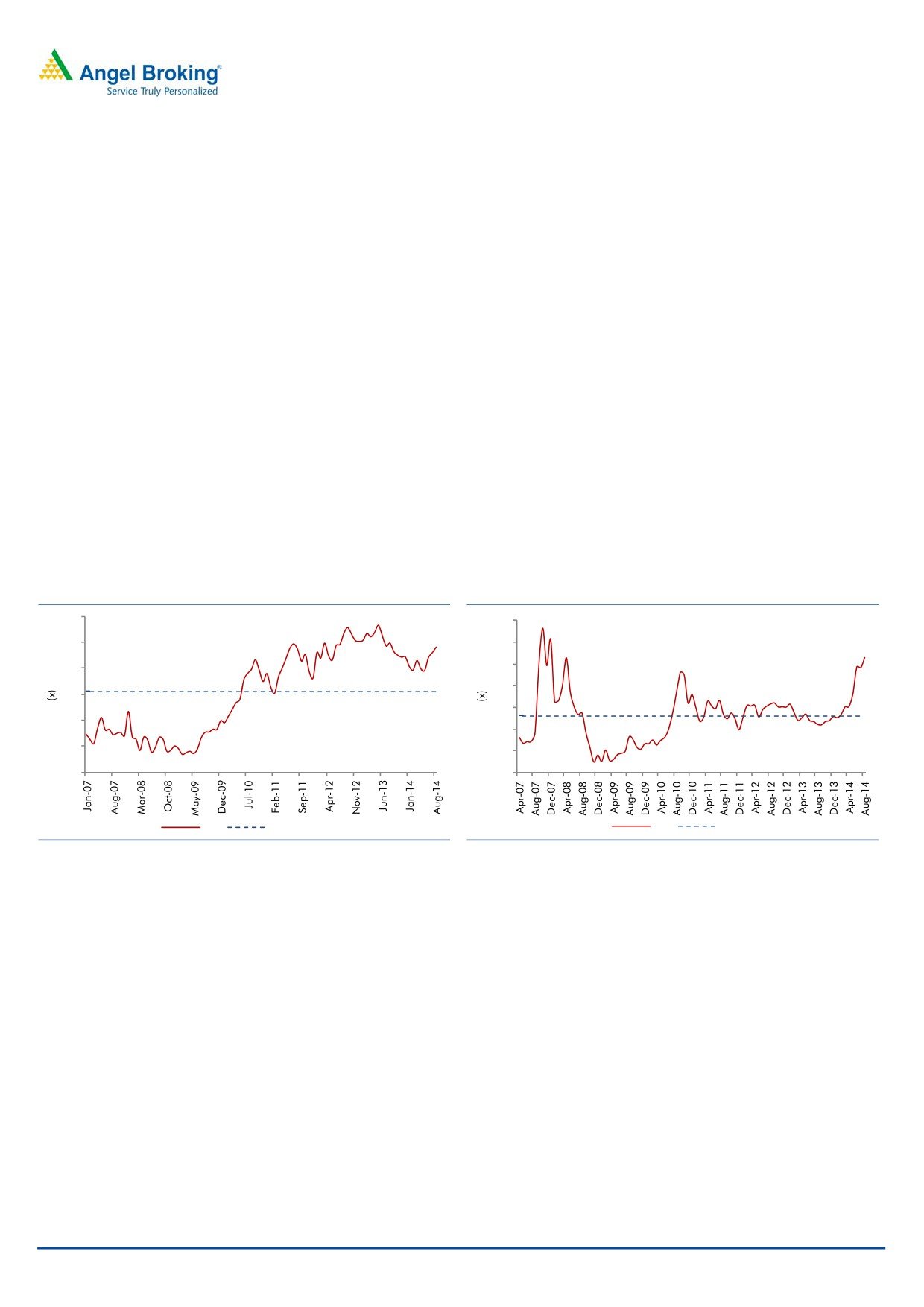

Exhibit 1: One year forward PE for Castrol India

Exhibit 2: One year forward PE for TWOIL

38

18

33

16

14

28

12

23

10

18

8

13

6

8

4

P/E

Average P/E

P/E

Average P/E

Source: Company, Angel Research

Source: Company, Angel Research

September 2, 2014

2

Tide Water Oil India | Initiating Coverage

Continuous gains in market share despite subdued industry

volumes

Over the last few years, the lubricant industry’s volume growth has contracted due

to improvement in motor vehicle technology leading to lower consumption of

Going forward, we expect the lubricant

lubricant oil and longer refill cycle. The quality of lubricant oil has also improved

industry to report improvement in

over the years due to development in its manufacturing technology leading to

volume growth, ie of 2-3% over the next

less-often refilling. Thus, the industry reported negative volume growth of ~1%

three year as per industry estimates)

CAGR over FY2010-13 (during the same period, TWOIL reported a volume growth

of ~2.3% CAGR). Going forward, we believe that the lubricant industry would

report an improvement in volume growth (of 2-3% over the next three years as per

industry estimates) owing to improvement in the Indian economic scenario. A

buoyant economy will lead to an improvement in automobile sales and growth in

the industrial sectors, which in turn will lead to higher lubricant oil consumption.

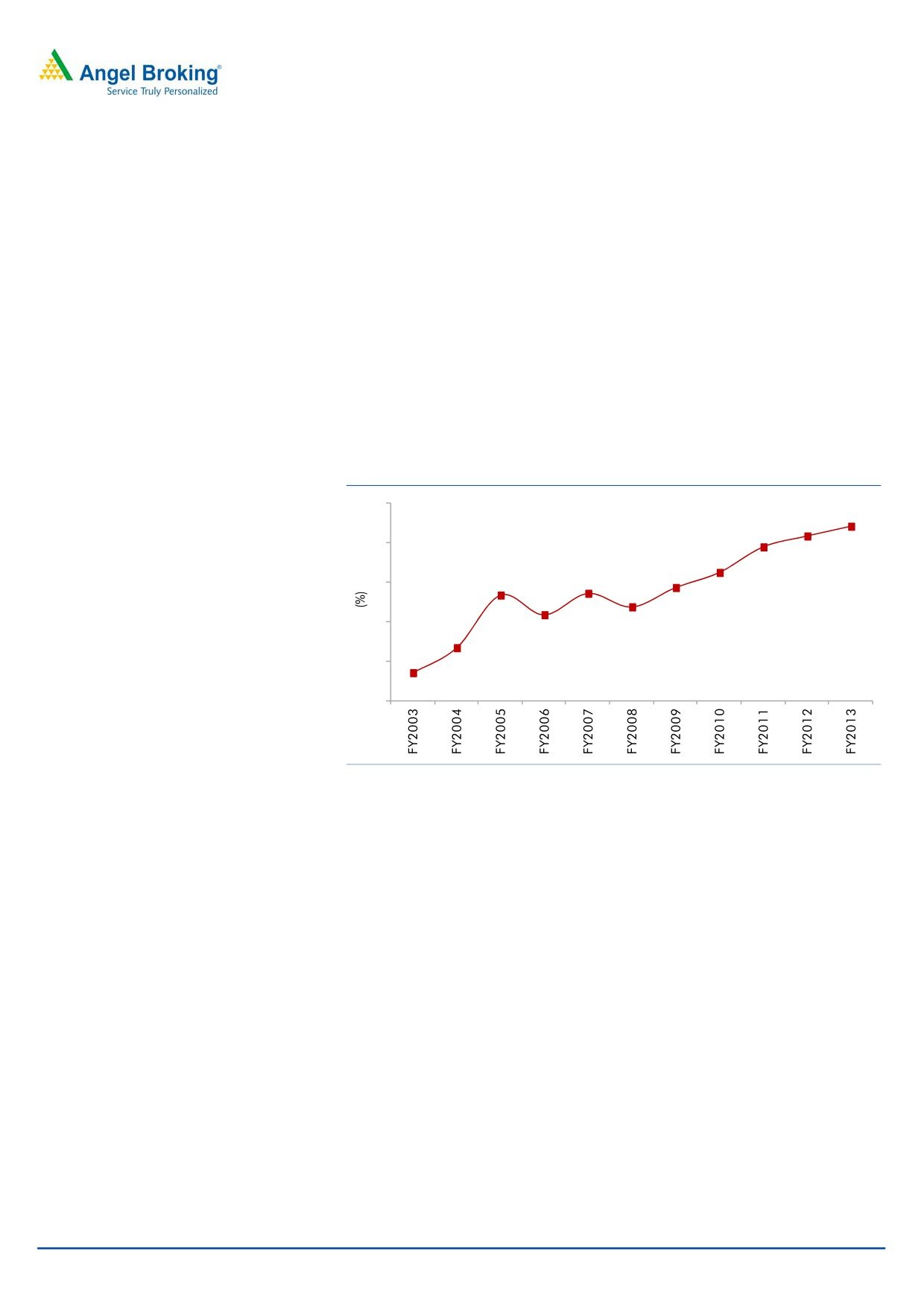

Exhibit 3: TWOIL is continuously gaining market share

5

4.7

4.6

4.4

5

4.1

3.9

3.8

3.9

4

3.7

3.6

4

3.2

2.9

3

3

Source: Company, Angel Research

Over the last 12 years, TWOIL has shown continuous improvement in market

share (the company’s market share has surged from 2.9% in FY2003 to 4.7% in

FY2013) owing to its strong brands (Veedol, Prima, Turbo etc), wide distribution

network and good quality of products. On the other hand, other PSU players and

private players like Castrol India have been losing market share.

TWOIL’s market share has risen from

Further, the company supplies its products to reputed companies such as Hero

2.9% in FY2013 to 4.7% in FY2013

MotoCorp (HMCL), Honda Motorcycle and Scooter India (HMSI), Honda Cars

India, Honda Siel Power Products, India Yamaha Motor, L& T Komatsu, Kobelco

Construction Equipment India, SML Isuzu, and Kubota Agricultural Machinery

among others, all of which have good growth prospects owing to anticipation of

improvement in Indian economy. This will result in an improvement in TWOIL’s

volumes.

September 2, 2014

3

Tide Water Oil India | Initiating Coverage

Healthy balance sheet with strong cash flow and zero debt

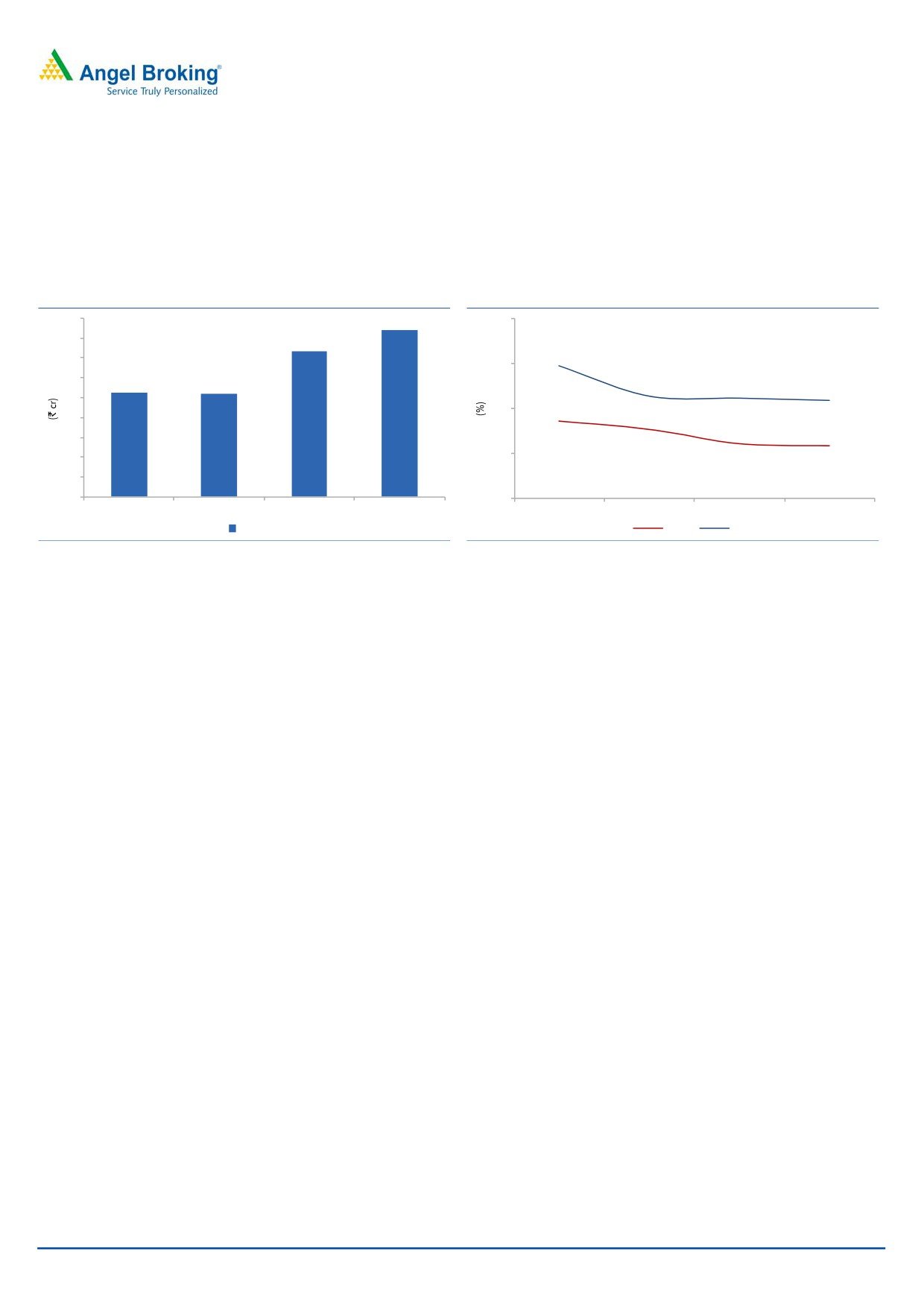

We expect the company to be able to generate free cash flow at a CAGR of ~27%

over FY2014-16E due to healthy sales and operating margins and lower capex.

Considering the above factors we expect a healthy ROE and ROCE. Further,

TWOIL has a strong balance sheet with zero debt.

Exhibit 4: Strong free cash flow generation

Exhibit 5: ROE and ROCE trend

45

42

30

40

37

35

25

30

26

26

25

20

20

15

15

10

5

0

10

FY2013

FY2014

FY2015E

FY2016E

FY2013

FY2014

FY2015E

FY2016E

Free cash flow

ROE

ROCE

Source: Company, Angel Research

Source: Company, Angel Research

Established brand and wide distribution network drive growth

The company is continuously marking efforts to enhance brand awareness by

The company’s pan-India distribution

adopting a more customer-centric approach, executing campaigns on the

network consists of 50 distributors and

electronic media and undertaking elaborate field level activities.

over 650 dealers servicing over 50,000

A pan-India distribution network, consisting of 50 distributors and over

650

retail outlets

dealers servicing over 50,000 retail outlets, has the spread and penetration to

deliver products in every nook and corner of the country. The company’s five

plants and 55 depots are located strategically across the country. Further, the

company is also implementing various loyalty programs with its dealers and

retailers which have strengthened the marketing and distribution network of the

company.

Going forward, we believe that the company’s strong brands and wide distribution

network (mainly in the “Bazaar” segment) would aid it to grow its business

substantially.

September 2, 2014

4

Tide Water Oil India | Initiating Coverage

Exhibit 6: Some reputed brands of TWOIL

Source: Company, Angel Research

Strong focus on R&D will ensure better product quality

The company is continuously focusing

The company has a wide range of products under the umbrella brand “Veedol” for

on maintaining and bettering the

the automotive and industrial segments. The company is continuously focusing on

quality of its products by spending

maintaining and bettering the quality of its products by spending adequately on

adequately

on

research

and

research and development. TWOIL is a pioneer in manufacturing engine oils

development

exceeding various performance standards in India. The manufacturing facilities are

backed by in-house R&D centres to ensure that the products match the most

stringent international standards as well as original equipment manufacturers’

requirement. Products are developed keeping in mind the high performance

requirement of modern engines, the extreme operating conditions and emerging

environmental regulations and new technologies.

The R&D centre for lube oils is located at Turbhe in Navi Mumbai and the R&D

centre for greases is at Oragadam near Chennai. These R&D centres are

approved by the Department of Scientific and Industrial Research, Ministry of

Science and Technology, and the Government of India.

Foray into global markets through subsidiaries

TWOIL is continuously making efforts to increase its global footprint by acquisition

and incorporation of new companies, entering into joint ventures and appointing

franchisees. The company acquired its first company - Veedol International Ltd

TWOIL is planning to expand its global

(100% subsidiary) - in FY2012 from Castrol and Lubricants UK, wholly owned

footprint in Latin American countries

subsidiaries of BP Plc. This acquisition brought with it global rights to a wide

like Cuba, Colombia and Mexico

portfolio of registered trademarks for the master brand, Veedol, as well as

through joint ventures or franchisees

associated product sub-brands and iconic logos. The acquisition also opened up

opportunities for exports and sale of lubricants under the Veedol brand to various

geographies around the world. To leverage the salience of the Veedol brand in the

international market, steps have been initiated for marketing products in the

Middle East, Asia, and Europe.

Apart from these regions, the company is also planning to market the Veedol

brand in parts of Latin America like in Cuba, Colombia and Mexico and also

through joint ventures or franchisees. Considering the increasing competition and

contracting volumes in the domestic lubricant market, we believe that TWOIL is

taking the right step by venturing into overseas markets for revenue growth and

profitability.

September 2, 2014

5

Tide Water Oil India | Initiating Coverage

Financial outlook

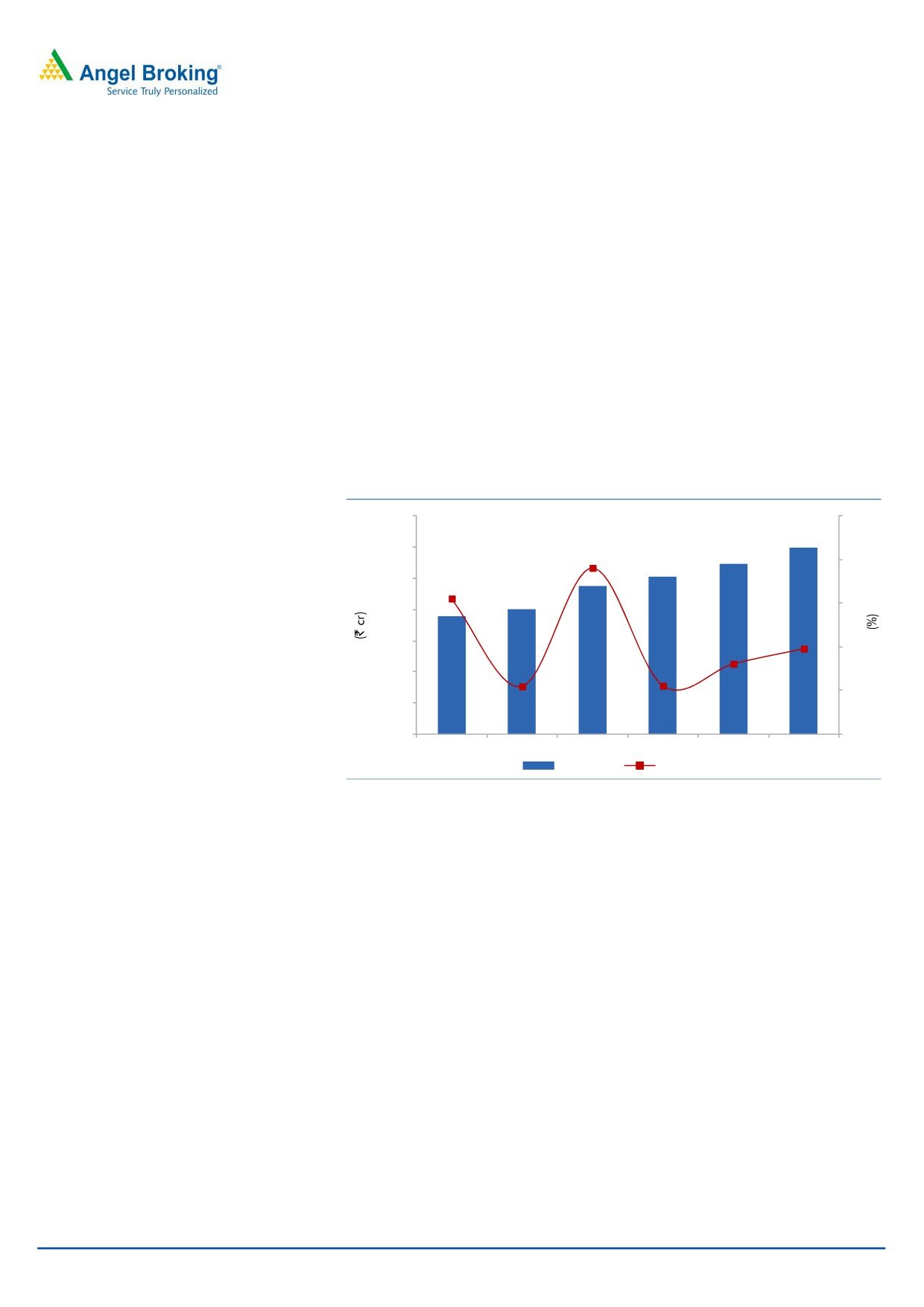

Top-line likely to clock a CAGR of ~9% over FY2014-16E

TWOIL has reported standalone sales CAGR of ~10% over FY2011-14. During

FY2014, the company was unable to perform well due to slowdown in Indian

economy and subdued automobile sales volumes, which affected OEM sales

volume of the company. Going forward, we expect TWOIL to register healthy

standalone sales CAGR of ~9% over FY2014-16E supported by healthy sales

volume in the automobile and industrial segments owing to recovery in the Indian

economy. Further, the company also has a strong brand equity and distribution

network. Moreover, the company’s subsidiaries in other international regions are

also expected to do well (we have not factored it in our numbers). Hence, we

expect TWOIL’s standalone revenue to grow by ~9% and ~10% in FY2015E and

FY2016E respectively.

Exhibit 7: Projected Net Sales growth trend

1,400

25

1,196

1,200

19.1

1,089

1,007

20

1,000

15.6

801

954

15

800

760

9.8

600

8.1

10

400

5.5

5.6

5

200

-

0

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

Net Sales

yoy growth (%)

Source: Company, Angel Research

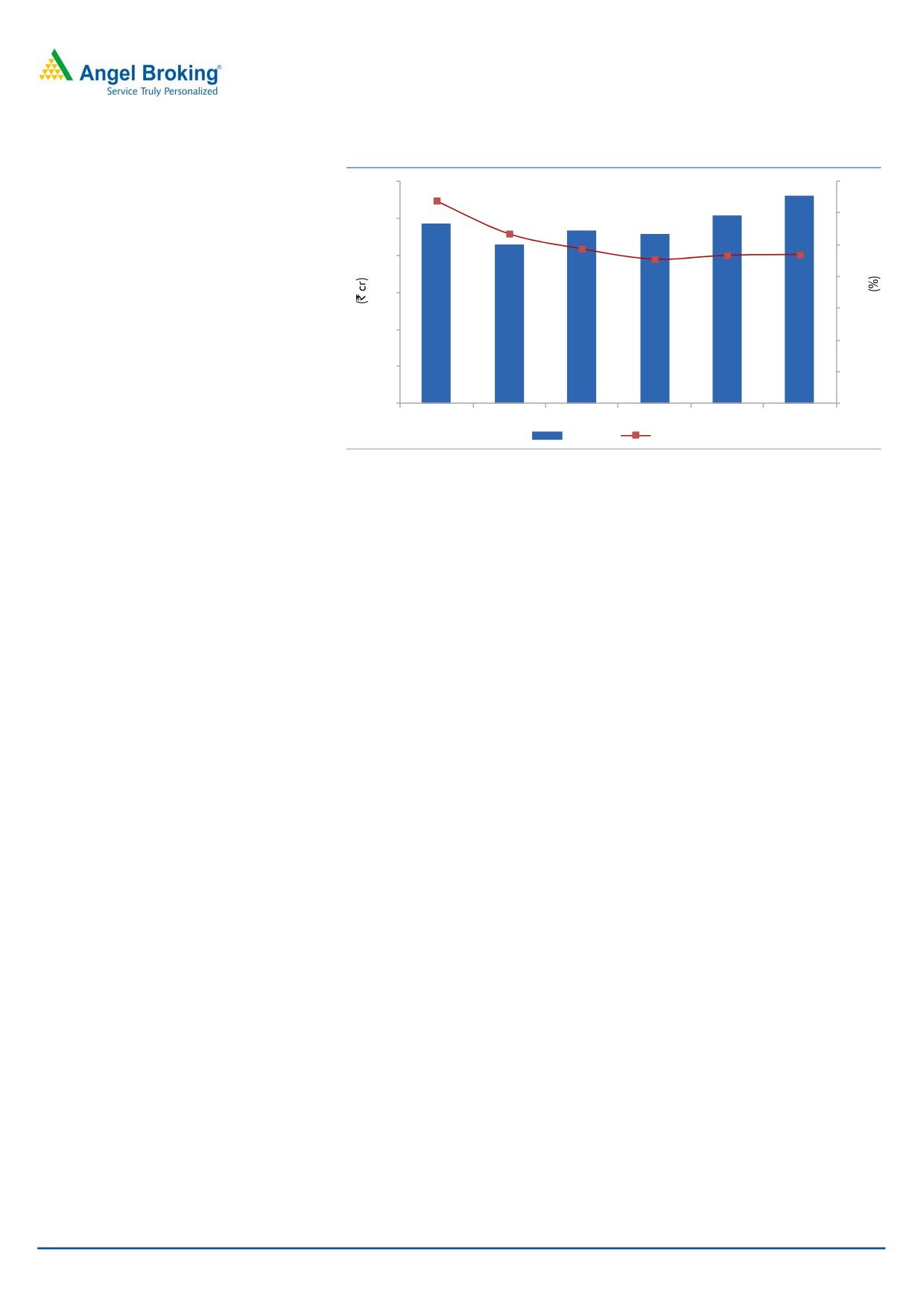

EBITDA to witness a CAGR of ~11% over FY2014-16E

Going forward, we expect the company’s operating margin to be in the range of

9-9.5% owing to falling crude oil prices (we however have not factored any

correction in crude prices in our model) and cost effective management strategy.

September 2, 2014

6

Tide Water Oil India | Initiating Coverage

Exhibit 8: Projected EBITDA and margin trend

120

12.8

14

12

100

10.7

9.8

9.4

9.4

10

9.1

80

8

60

112

102

6

97

93

92

86

40

4

20

2

0

0

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

EBITDA

Margin (%)

Source: Company, Angel Research

September 2, 2014

7

Tide Water Oil India | Initiating Coverage

Outlook and Valuation

Going ahead, we expect TWOIL to report standalone net sales CAGR of ~9% over

FY2014-16E to ~`1,196cr owing to some improvement in sales volume and

possible price hikes (the company would be able to take price hikes due to its

strong brands and better quality of products). We believe that the company would

perform better in the “Bazaar” segment owing to strong distribution network and

tie-ups with leading OEMs. Further, the company is expanding its footprint in

international markets through acquisitions, incorporation of new companies, joint

ventures or franchisees; which would aid the revenue growth for TWOIL in the

coming years. On the profitability front, we forecast TWOIL to report a standalone

net profit CAGR of ~7% over FY2014-16E to `78cr owing to healthy sales and

better operating margin due to cost effective management strategy.

At the current market price of `12,076, the stock trades at a PE of 14.6x and

13.1x its FY2015E and FY2016E EPS of `828.6 and `919.0, respectively. We

initiate coverage on the stock with a Buy recommendation and target price of

`14,704, based on 16x FY2016E EPS, indicating an upside of ~22% from the

current levels.

Exhibit 9: One-year forward P/E band

14,000

7x

9x

11x

13x

15x

12,000

10,000

8,000

6,000

4,000

2,000

0

Source: Company, Angel Research

The downside risks to our estimates include 1) any increase in crude oil (key raw

material) prices could negatively impact profitability,

2) downturn in the

automobile and industrial segments could affect business growth.

September 2, 2014

8

Tide Water Oil India | Initiating Coverage

Company Background

Tide Water Oil India Ltd (TWOIL) is a part of the multi divisional Andrew Yule

group that has diverse interests in Engineering, Electrical, Tea Cultivation, Power

Generation, Digital Communication Systems and Lubricants. TWOIL operates in

two segments: lubricants and wind power. The company’s products include

automotive oils, industrial oils, industrial grease, automotive grease and genuine

oils. Its repertoire of automotive products includes engine oils for trucks, tractors,

commercial vehicles, passenger cars and two/three wheelers. It also produces gear

oils, transmission oils, coolants and greases for automobiles. For industrial

application it manufactures industrial oils, greases and specialty products, such as

metal working fluids, quenching oils and heat transfer oils. The company’s plants

are located in Dadra & Nagar Haveli, Maharashtra, Haryana and West Bengal.

In October

2011, the company acquired Veedol International Ltd. On

January

15,

2012, the company incorporated Veedol International DMCC.

Recently, July 21, 2014, the company has entered into 50:50 JV with Japanese

company JX Nippon Oil.

Exhibit 10: Segment wise sales break up

0%

11%

89%

Lubricant oils

Greases

Wind Power Generation

Source: Company, Angel Research

September 2, 2014

9

Tide Water Oil India | Initiating Coverage

Standalone Profit & Loss Statement

Y/E March (` cr)

FY2011

FY2012

FY2013

FY2014

FY2015E

FY2016E

Net Sales

760

801

954

1,007

1,089

1,196

% chg

15.6

5.5

19.1

5.6

8.1

9.8

Total Expenditure

662

715

861

916

987

1,084

Cost of Materials

422

548

585

597

660

730

Personnel

31

31

40

42

47

53

Others

209

137

237

277

280

301

EBITDA

97

86

93

92

102

112

% chg

2.9

(11.6)

8.5

(1.5)

10.9

10.4

(% of Net Sales)

12.8

10.7

9.8

9.1

9.4

9.4

Depreciation& Amortisation

10

9

9

9

9

9

EBIT

87

77

84

83

93

103

% chg

(0.9)

(12.4)

9.7

(1.3)

11.9

11.2

(% of Net Sales)

11.5

9.6

8.8

8.2

8.5

8.6

Interest & other Charges

0

1

-

-

-

-

Other Income

7

11

10

21

14

15

(% of PBT)

7.4

12.4

10.8

20.0

13.0

12.7

Share in profit of Associates

-

-

-

-

-

-

Recurring PBT

94

86

94

104

107

118

% chg

5.7

(8.8)

9.3

10.1

2.8

10.9

Prior Period & Extord. Exp./(Inc.)

-

-

-

-

-

-

PBT (reported)

94

86

94

104

107

118

Tax

30

27

31

35

36

40

(% of PBT)

32.1

31.5

33.2

34.1

34.0

34.0

PAT (reported)

64

59

63

68

70

78

Add: Share of earnings of asso.

-

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

-

PAT after MI (reported)

64

59

63

68

70

78

ADJ. PAT

64

59

63

68

70

78

% chg

11.0

(7.9)

6.5

8.6

3.1

10.9

(% of Net Sales)

8.4

7.4

6.6

6.8

6.5

6.5

Basic EPS (`)

754.8

695.1

740.4

804.0

828.6

919.0

Fully Diluted EPS (`)

754.8

695.1

740.4

804.0

828.6

919.0

% chg

11.0

(7.9)

6.5

8.6

3.1

10.9

September 2, 2014

10

Tide Water Oil India | Initiating Coverage

Standalone Balance Sheet

Y/E March (` cr)

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

SOURCES OF FUNDS

Equity Share Capital

1

1

1

1

1

1

Reserves& Surplus

261

308

338

386

436

491

Shareholders Funds

262

308

339

387

437

492

Minority Interest

-

-

-

-

-

-

Total Loans

-

-

-

-

-

-

Deferred Tax Liability

6

6

5

5

5

5

Total Liabilities

268

314

344

392

442

497

APPLICATION OF FUNDS

Gross Block

117

127

133

138

147

157

Less: Acc. Depreciation

45

54

63

70

79

88

Net Block

72

73

70

69

69

70

Capital Work-in-Progress

1

2

1

1

1

1

Investments

1

52

54

57

65

70

Current Assets

318

337

377

451

508

581

Inventories

168

166

157

198

224

256

Sundry Debtors

76

83

129

149

167

190

Cash

16

34

49

62

72

85

Loans & Advances

57

53

42

42

46

50

Other Assets

-

-

-

-

-

-

Current liabilities

128

154

162

190

206

229

Net Current Assets

191

183

215

260

303

352

Deferred Tax Asset

3

4

4

5

5

5

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

268

314

344

392

442

497

September 2, 2014

11

Tide Water Oil India | Initiating Coverage

Standalone Cash Flow Statement

Y/E March (` cr)

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

Profit before tax

94

86

94

104

107

118

Depreciation

10

9

9

9

9

9

Change in Working Capital

(66)

26

(36)

(31)

(33)

(36)

Interest / Dividend (Net)

(2)

(2)

(4)

(8)

0

0

Direct taxes paid

(29)

(30)

(29)

(36)

(36)

(40)

Others

(2)

(4)

(3)

(5)

0

0

Cash Flow from Operations

5

86

32

33

46

52

(Inc.)/ Dec. in Fixed Assets

(3)

(8)

(2)

(0)

(9)

(10)

(Inc.)/ Dec. in Investments

-

(51)

(2)

(3)

(8)

(5)

Cash Flow from Investing

(3)

(59)

(4)

(3)

(17)

(15)

Issue of Equity

0

0

0

0

0

0

Inc./(Dec.) in loans

0

0

0

0

0

0

Dividend Paid (Incl. Tax)

(5)

(6)

(12)

(15)

(20)

(23)

Interest / Dividend (Net)

(1)

(2)

(1)

(1)

0

0

Cash Flow from Financing

(6)

(8)

(13)

(16)

(20)

(23)

Inc./(Dec.) in Cash

(4)

18

14

14

10

13

Opening Cash balances

20

16

34

49

62

72

Closing Cash balances

16

34

49

62

72

85

September 2, 2014

12

Tide Water Oil India | Initiating Coverage

Key Ratios

Y/E March

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

Valuation Ratio (x)

P/E (on FDEPS)

16.0

17.4

16.3

15.0

14.6

13.1

P/CEPS

13.9

15.0

14.3

13.3

12.9

11.8

P/BV

3.9

3.3

3.0

2.7

2.3

2.1

Dividend yield (%)

0.4

0.5

1.0

1.2

1.7

1.9

EV/Sales

1.3

1.2

1.0

0.9

0.8

0.7

EV/EBITDA

10.4

11.0

9.9

9.9

8.7

7.8

EV / Total Assets

2.6

2.0

1.8

1.6

1.4

1.2

Per Share Data (`)

EPS (Basic)

754.8

695.1

740.4

804.0

828.6

919.0

EPS (fully diluted)

754.8

695.1

740.4

804.0

828.6

919.0

Cash EPS

869.1

804.0

847.3

907.6

933.9

1,026.7

DPS

50.0

60.0

120.0

150.0

200.0

232.0

Book Value

3,077.3

3,627.9

3,987.3

4,548.6

5,145.2

5,788.4

Returns (%)

ROCE

33.4

24.8

24.8

21.5

21.2

21.0

Angel ROIC (Pre-tax)

35.7

34.4

35.6

31.0

30.9

30.6

ROE

24.5

19.2

18.6

17.7

16.1

15.9

Turnover ratios (x)

Asset Turnover (Gross Block)

6.5

6.3

7.2

7.3

7.4

7.6

Inventory / Sales (days)

81

76

60

72

75

78

Receivables (days)

37

38

49

54

56

58

Payables (days)

42

46

37

40

42

44

WC cycle (ex-cash) (days)

75

67

72

86

89

92

September 2, 2014

13

Tide Water Oil India | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Angel Broking Pvt. Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Pvt. Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking

or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or

in the past.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Tide Water Oil India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to -15%)

Sell (< -15%)

September 2, 2014

14

Tide Water Oil India | Initiating Coverage

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Amarjeet Maurya

Analyst

Denil Savla

Analyst

Shrenik Gujrathi

Analyst

Umesh Matkar

Analyst

Twinkle Gosar

Analyst

Bharat Gianani

Analyst

Tejas Vahalia

Research Editor

Technicals and Derivatives:

Siddarth Bhamre

Head - Technical & Derivatives

Sameet Chavan

Technical Analyst

Nagesh Arekar

Executive

Sneha Seth

Associate (Derivatives)

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Production Team:

Dilip Patel

Production Incharge

CSO & Registered Office: G-1, Ackruti Trade Centre, Road No. 7, MIDC, Andheri (E), Mumbai - 93. Tel: (022) 3083 7700. Angel Broking Pvt. Ltd: BSE Cash: INB010996539 / BSE F&O: INF010996539, CDSL Regn. No.: IN - DP - CDSL - 234 - 2004, PMS Regn. Code: PM/INP000001546, NSE Cash: INB231279838 /

NSE F&O: INF231279838 / NSE Currency: INE231279838, MCX Stock Exchange Ltd: INE261279838 / Member ID: 10500. Angel Commodities Broking (P) Ltd.: MCX Member ID: 12685 / FMC Regn. No.: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn. No.: NCDEX / TCM / CORP / 0302.

September 2, 2014

15