Advisory Desk

TVS Srichakra Ltd.

BUY

CMP

`355

Target Price

`468

TVS Srichakra Ltd. (TVSSL), a part of TVS Group, is a leading manufacturer of two

Investment Period

12 Months

and three-wheeler tyres with a 25% market share. Two-wheeler demand growth

(~16% yoy YTD) continues to be insulated from the current slowdown in the

automobile sector. Given this growth and increased installed capacity of

automotive tyres by 170% to 3.3cr units over FY2009-11, TVSSL’s volume is

expected to grow at a CAGR of 11% over FY2011-13E. Also, the promoters have

increased their stake in the company from 39.5% in June 2007 to 44.4% in June

2011, demonstrating their confidence in the company’s future growth outlook.

We recommend Buy on TVSSL with a target price of `468, based on a target PE of

5x for FY2013E.

Investment rationale

Better performance of two-wheeler sales to drive the company’s volume

Two-wheeler domestic sales have witnessed growth of ~16% yoy YTD. Being into

the manufacturing of two and three-wheeler tyres, TVSSL is not much exposed to

the risks of demand slowdown, as the two-wheeler segment continues to be

insulated from the current slowdown in the automobile sector and is expected to

grow at a CAGR of 13% over FY2011-13E. Backed by this and increased capacity

utilisation, we expect the company’s volume to grow at a CAGR of 11% over

FY2011-13.

Increase in capacity utilisation to drive operating leverage

TVSSL has increased its installed capacity of automotive tyres by 170% to 3.3cr

units over FY2009-11. This capacity increase is expected to drive the operating

leverage for the company. However, capacity utilisation is only 48% (as of March

2011), which is expected to increase to 59% over FY2011-13E.

Increase in promoters’ stake - A positive for the company

The company’s promoters have increased their share from 39.5% in June 2007 to

44.4% in June 2011. This consistent increase in their share in the company is a

good signal for investors, as it demonstrates the confidence of promoters in the

company’s future growth outlook.

Outlook and valuation

At `355, the stock is trading at 4.8x and 3.8x its FY2012E and FY2013E earnings,

respectively. We expect the company’s revenue and profit to witness CAGRs of

22% and 35%, respectively, on the back of the expected increase in capacity

utilisation, which will result in an 11% CAGR in volumes over FY2011-13E.

We recommend Buy on TVSSL with a target PE of 5x for FY2013E and a target

price of `468 for an investment period of 12 months.

Key financials

Sales

OPM PAT EPS RoE P/E P/BV

EV/

EV/

Year

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

EBITDA (x) Sales (x)

FY2011

1,085

8.4

39

51.2

34.4

6.9

2.4

5.7

0.5

FY2012E

1,430

8.6

56

73.7

35.1

4.8

1.7

4.5

0.4

FY2013E

1,607

9.2

72

93.5

32.2

3.8

1.2

3.6

0.3

Source: Company

Please refer to important disclosures at the end of this report

1

Advisory Desk

TVS Srichakra

Investment arguments

Better performance of two-wheeler sales to drive volumes

Two-wheeler domestic sales have witnessed growth of ~16% yoy YTD, whereas

M&HCVs grew by 7.1% and passenger vehicles grew only by 1.9% for the same

period. As TVSSL is largely into the two and three-wheeler tyres segments, it has

not been exposed to demand slowdown. The two-wheeler segment continues to be

insulated from the current slowdown in the automobile sector and is expected to

grow at a CAGR of 13% over FY2011-13E. Based on this growth and increased

capacity utilisation, we expect the company’s volume to grow at a CAGR of 11%

over FY2011-13.

Exhibit 1: Domestic sales of automobiles (April-August) (in’000)

FY2011

FY2012

% Change

Passenger vehicles

959

977

1.9

M&HCVs

121

130

7.1

Three-wheelers

200

200

(0.3)

Two-wheelers

4,621

5,358

15.9

Total

5,901

6,664

12.9

Source: SIAM

TVSSL is in a position to pass on any increase in rubber prices to consumers as it is

the second largest manufacturer in the segment and is considered to be a

premium brand.

Increase in capacity utilisation to drive operating leverage

TVSSL has set up a new plant at Pantnagar, Uttarakhand, (production started in

July 2009) and has increased the capacity at its Madurai plant. This led to a

significant increase of 170% in its installed capacity of automotive tyres to 3.3cr

units over FY2009-11.

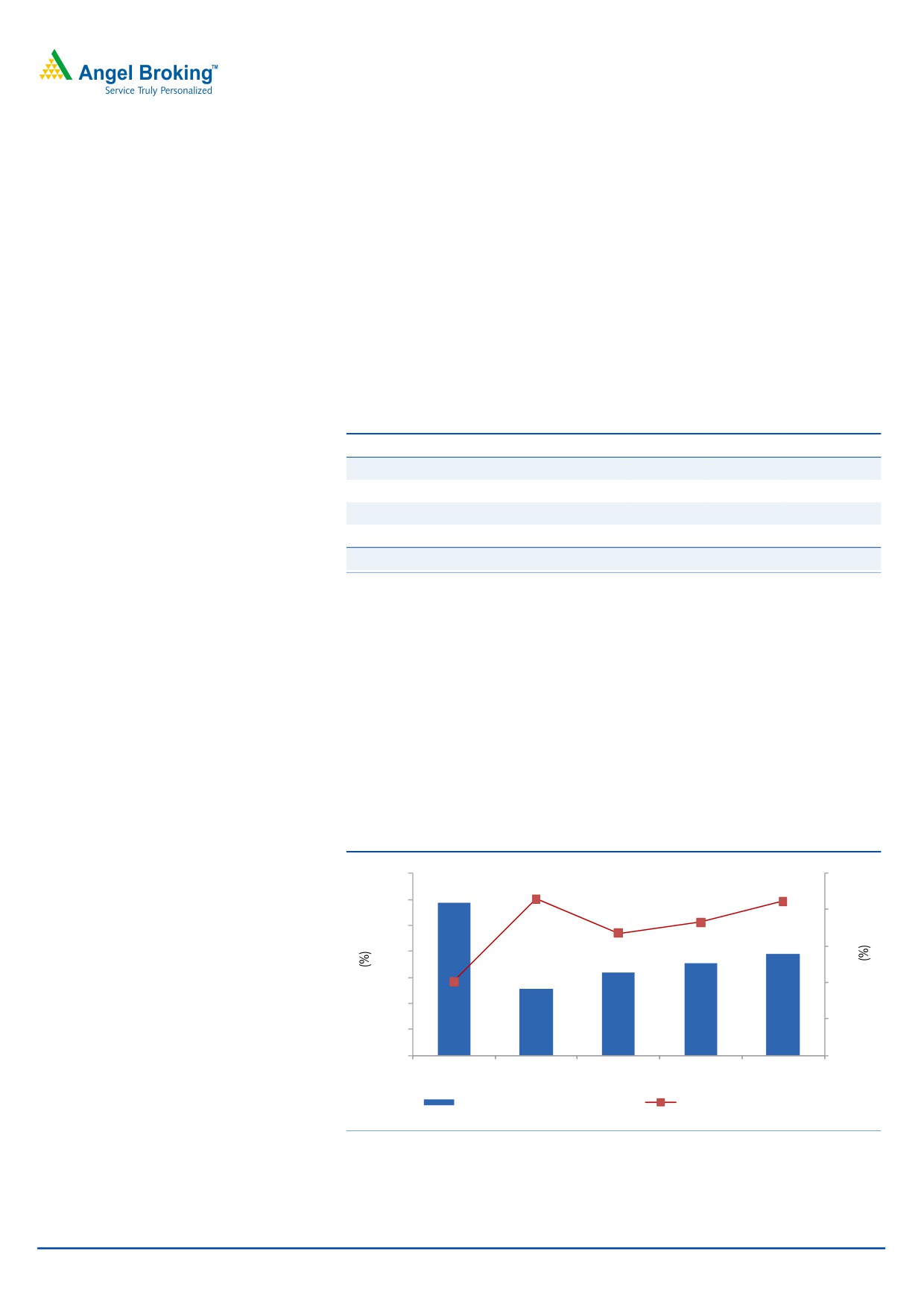

Exhibit 2: Operating leverage to drive margin

105

10

90

9

75

8

60

45

7

30

6

15

0

5

FY2009

FY2010

FY2011

FY2012E

FY2013E

Capacity utilization (LHS)

Operating margin (RHS)

Source: Company, Angel Research

September 21, 2011

2

Advisory Desk

TVS Srichakra

However, capacity utilisation is only 48% for tyres (as of March 2011). The

company has a significant opportunity in terms of increasing its capacity utilisation

to historical levels. We expect capacity utilisation to increase to

59% over

FY2011-13E and improve the company’s operating leverage. This will increase the

operating margin by 87bp to 9.2% in FY2013 from 8.4% in 2011.

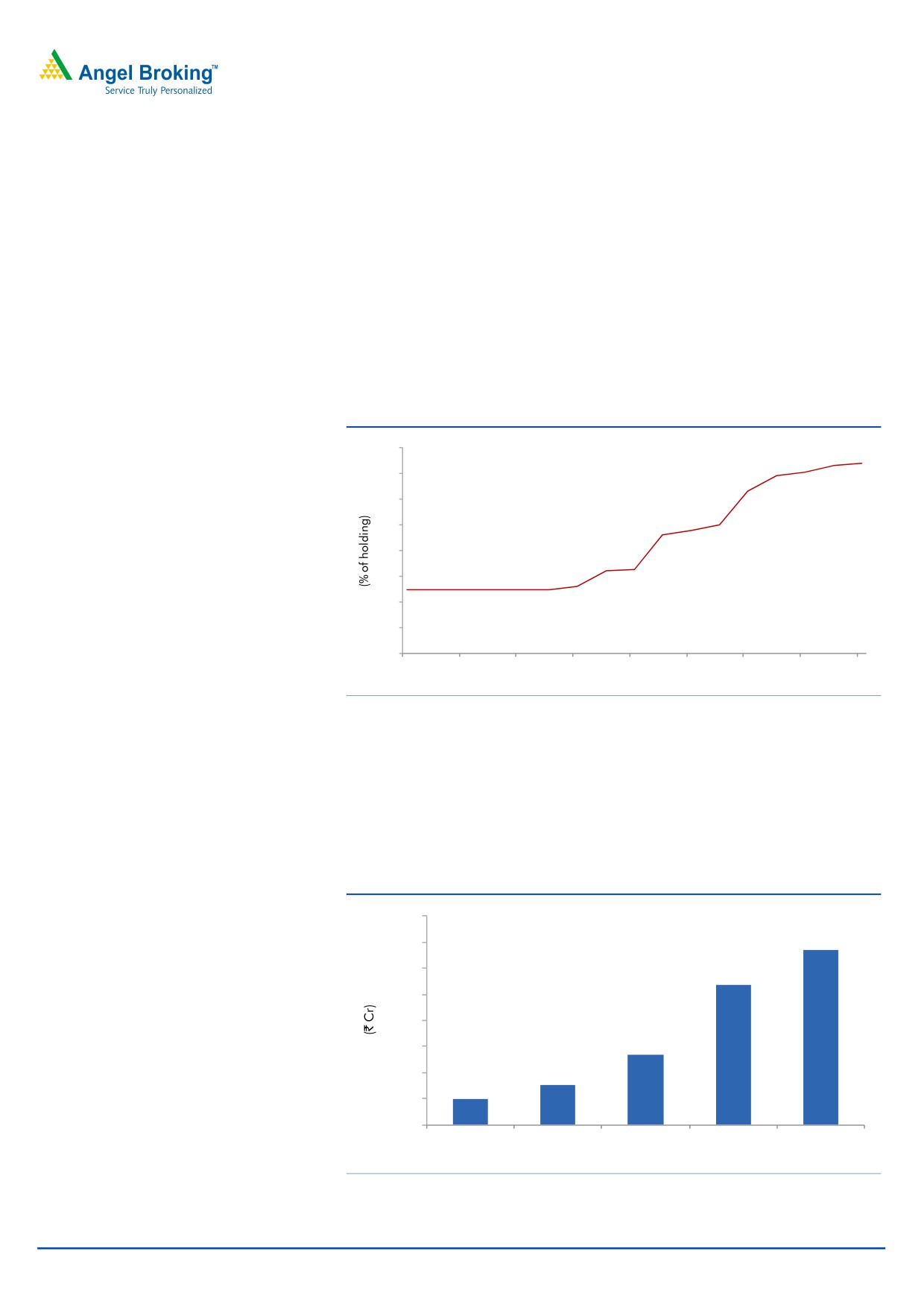

Increase in promoters’ stake - A positive for the company

The company’s promoters have increased their share from 39.5% in June 2007 to

44.4% in June 2011. This consistent increase in their share in the company is a

good signal for investors, as it demonstrates the confidence of promoters in the

company’s future growth outlook.

Exhibit 3: Promoters’ stake

45

44

44.4

43

42

41

40

39

39.5

38

37

Jun-07

Dec-07

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Source: Company

Branding

TVSSL is aggressively focusing on brand-building exercises to strengthen the quality

of its dealer network and improve its market share in the after sales business. The

company doubled its advertisement cost in FY2010; and in FY2011, the company

further increased it by 25% to `13.4cr.

Exhibit 4: Advertisement cost

16.0

13.4

14.0

12.0

10.7

10.0

8.0

5.4

6.0

4.0

3.0

2.0

2.0

0.0

FY2007

FY2008

FY2009

FY2010

FY2011

Source: Company

September 21, 2011

3

Advisory Desk

TVS Srichakra

Competition

TVSSL has a market share of 25% (in FY2011) in the two and three-wheeler tyre

segments, next to MRF - who is the leader with a 28% market share. Other players

in the same segment include CEAT and Falcon Tyres.

On the valuation front, TVSSL enjoys the highest RoE among other players in the

tyre manufacturing industry. With a PE of 4.8x and 3.8x for FY2012E and

FY2013E, respectively, TVSSL looks very attractive among its peers.

Exhibit 5: Relative valuation

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/

EV/

Company

Year

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

EBITDA (x)

Sales (x)

TVSSL

2012E

1,430

8.6

56

73.7

35.1

4.8

1.7

4.5

0.4

TVSSL

2013E

1,607

9.2

72

93.5

32.2

3.8

1.2

3.6

0.3

Goodyear

CY2011E

1,510

8.0

75

32.5

23.0

9.9

2.3

3.9

0.3

Goodyear

CY2012E

1,744

10.9

123

53.3

28.8

6.0

1.7

2.0

0.2

MRF

SY2011E

10,026

8.1

292

688.0

14.9

10.2

1.5

6.3

0.5

MRF

SY2012E

11,743

10.1

462

1088.8

19.3

6.5

1.2

4.4

0.4

Apollo Tyres

2012E

11,112

9.5

342

7.0

11.6

8.8

1.1

5.1

0.9

Apollo Tyres

2013E

12,710

10

469

9.0

15.0

6.4

1.0

4.3

0.9

Source: Company, Angel Research

September 21, 2011

4

Advisory Desk

TVS Srichakra

Financials

Exhibit 6: Key assumptions

2012E

2013E

Volume growth (%)

10.6

11.1

Average realisation growth (%)

16.0

1.0

Change in raw-material prices (%)

25.0

(4.0)

Source: Company, Angel Research

Volume growth at an 11% CAGR over FY2011-13E

TVSSL significantly increased its installed capacity of automotive tyres by 170% to

3.3cr units over FY2009-11 to meet up with the increasing demand of two and

three-wheeler tyres. We expect sales of two-wheelers and three-wheelers in the

industry to grow at a CAGR of 13% over FY2011-13E. Further, we expect the

company’s volume to grow at a CAGR of 11% over the same period on the back

of the above-mentioned factors and considering replacement demand.

Exhibit 7: TVSSL's volume growth

FY2008 FY2009 FY2010 FY2011 FY2012E FY2013E

Vehicle population growth (%)

10.1

9.8

11.3

12.9

12.8

12.7

Volume growth for TVSSL (%)

1.0

9.6

15.5

27.1

10.6

11.1

Source: Company, Angel Research

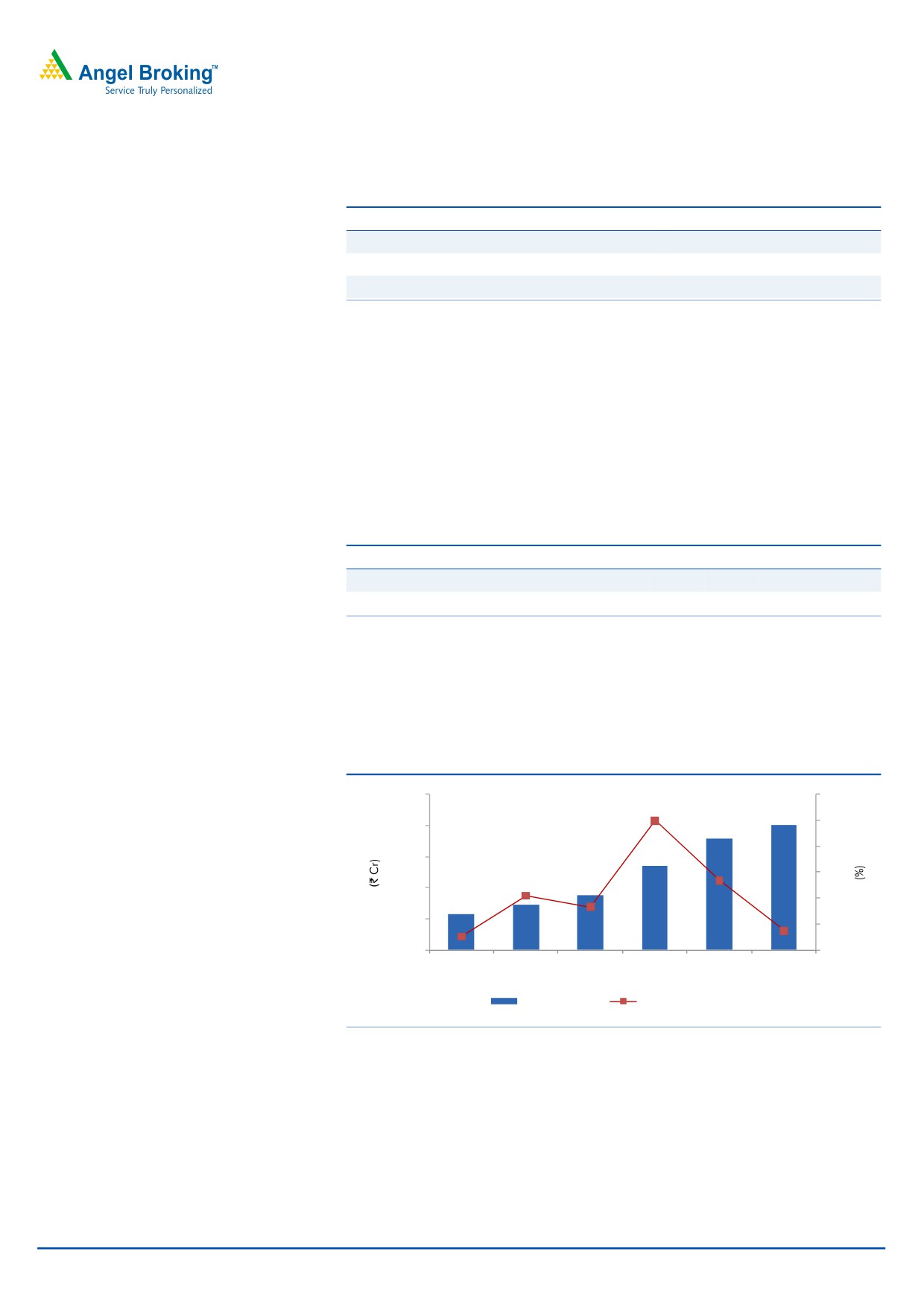

Revenue to grow at a 22% CAGR over FY2011-13E

TVSSL’s revenue is expected to grow at a 22% CAGR over FY2011-13E to

`1,607cr as volume is expected to post an 11% CAGR over the same period.

Exhibit 8: Revenue and revenue growth

2000

65

55

1600

45

1200

35

800

25

400

15

0

5

FY2008

FY2009

FY2010

FY2011

FY2012E FY2013E

Revenue (LHS)

Revenue growth (RHS)

Source: Company, Angel Research

September 21, 2011

5

Advisory Desk

TVS Srichakra

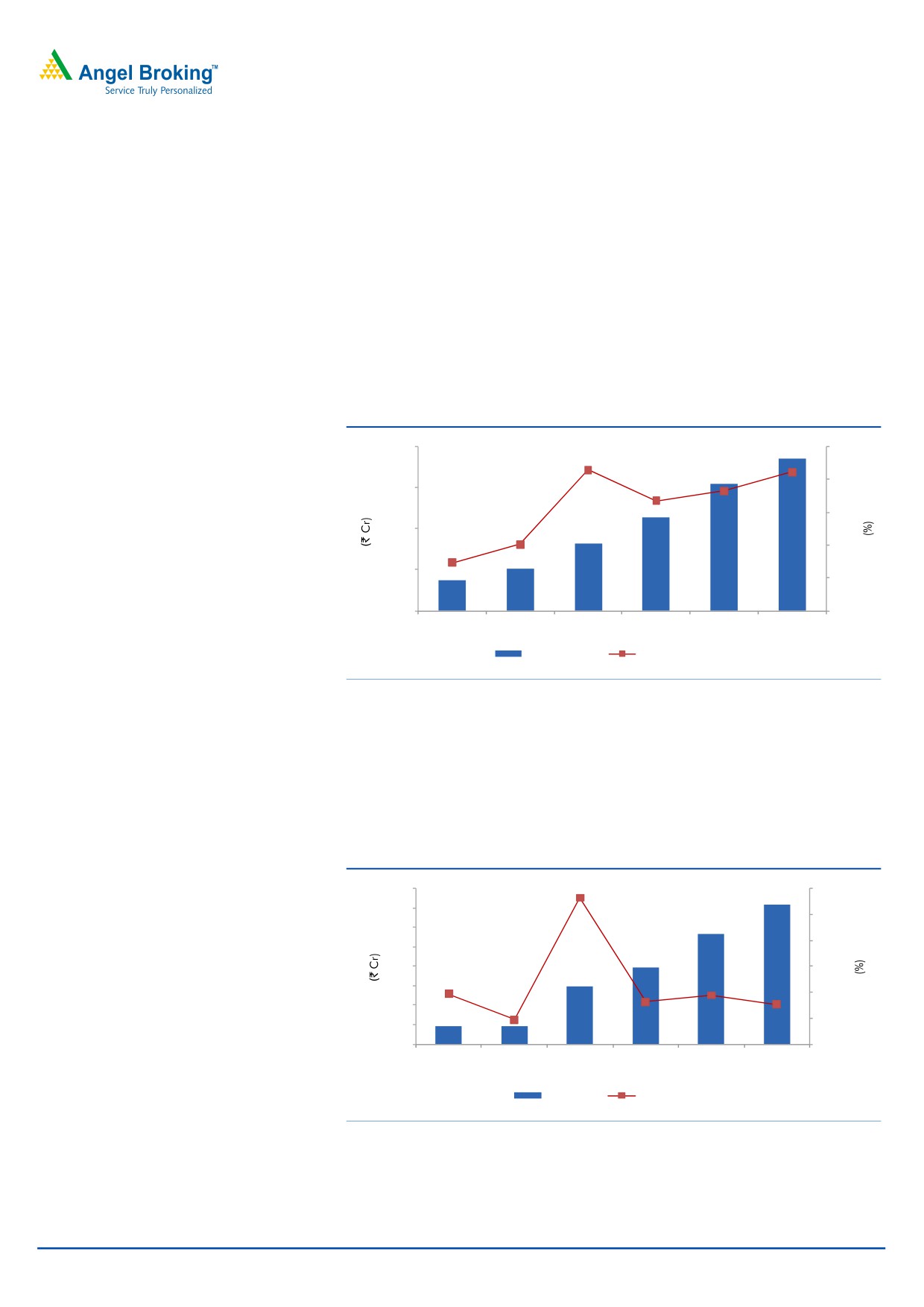

Profit to grow at a 35% CAGR for FY2011-13E

The company’s operating profit margin is expected to improve by 87bp to 9.2% in

FY2013E from 8.4% in FY2011, mainly on the back of increased capacity

utilisation from 48% to 59% over FY2011-13E.

The company’s rubber consumption is lower vis-à-vis the industry’s average rubber

consumption i.e., 57% of sales vis-à-vis industry average of 61%, which gives the

company an edge over its peers in terms of getting affected by any increase in

rubber prices. Also, TVSSL is in a position to pass on any increase in rubber prices

to consumers and maintain its operating margin as it is the second largest

manufacturer in the segment and is considered to be a premium brand.

Exhibit 9: EBITDA and EBITDA margin

160

10

9

120

8

80

7

40

6

0

5

FY2008

FY2009

FY2010

FY2011

FY2012E FY2013E

EBITDA (LHS)

EBITDA Margin (RHS)

Source: Company, Angel Research

The interest cost of for the company stood at `30cr at a rate of 11.6% for FY2011.

Considering the increase in the interest rates for the past 18 months, we have

assumed an interest rate of 13.5% for FY2013E on a conservative basis. Given the

company’s revenue growth and improved operating margin, we expect TVSSL’s

profit to grow at a 35% CAGR to `72cr over FY2011-13E.

Exhibit 10: PAT and PAT growth

80

250

70

200

60

150

50

40

100

30

50

20

0

10

0

-50

FY2008

FY2009

FY2010

FY2011

FY2012E FY2013E

PAT (LHS)

PAT growth (RHS)

Source: Company, Angel Research

September 21, 2011

6

Advisory Desk

TVS Srichakra

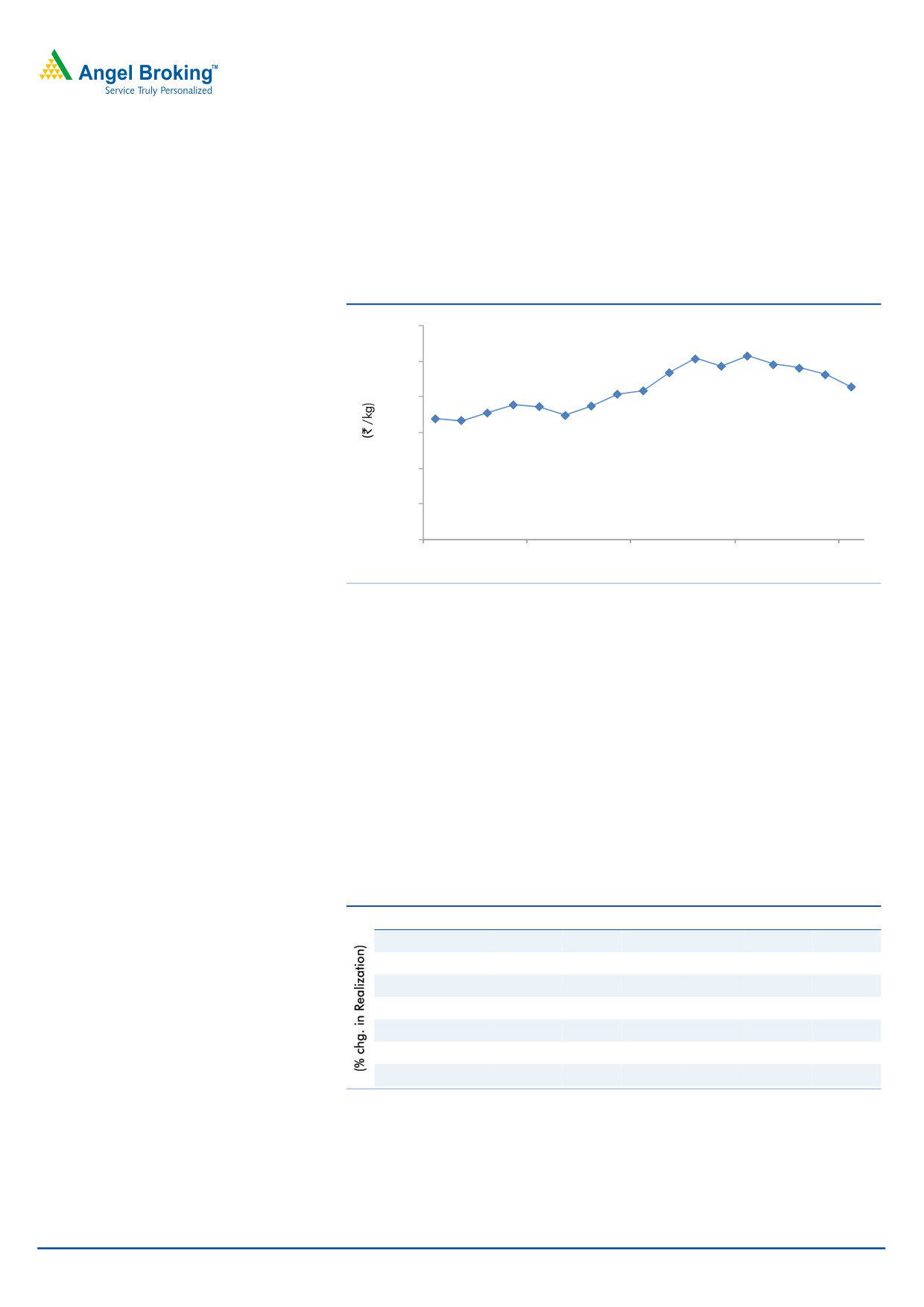

Risks

Further rise in raw-material prices

Rubber, the key raw material of the company, witnessed a price rise of 59% from

`169/kg in April 2010 to `244/kg in March 2011.

Exhibit 11: Rubber prices

300

250

214

200

150

169

100

50

0

Apr-10

Aug-10

Dec-10

Apr-11

Aug-11

Source: Rubber Board

Though rubber prices are witnessing a downtrend from April 2011, any further

price rise may pressurise the company’s operating margin. Due to a difference in

mix, rubber cost is typically 30% lower for TVSSL than other tyre companies.

Sensitivity analysis of EPS

The sensitivity analysis reflects the changes in EPS w.r.t. the percentage change in

rubber price and realisation. On our assumption of 4% decrease in rubber price

and 1% increase in realisation, the EPS for FY2013E stands at `93.5. However, if

rubber price goes down by 10% and realisation increases by 10%, EPS can grow to

`223; but if rubber price goes up by 10% with the same increase in realisation,

EPS will be `97.

Exhibit 12: Impact on EPS w.r.t. % chg. in realisation and rubber price

(% chg. in Rubber prices)

-10%

-4%

0%

10%

20%

30%

-10%

19.4

-18.5

-43.7

-106.7

-169.7

-232.8

0%

121.2

83.4

58.2

-4.9

-67.9

-130.9

1%

131.4

93.5

68.3

5.3

-57.7

-120.7

10%

223.0

185.2

160.0

97.0

33.9

-29.1

20%

324.8

287.0

261.8

198.8

135.8

72.7

30%

426.7

388.8

363.6

300.6

237.6

174.6

Source: Company, Angel Research

September 21, 2011

7

Advisory Desk

TVS Srichakra

Slowdown in the two-wheeler automobile segment

Any slowdown in the domestic sales of two wheelers may pose a risk to the

company as tyre demand (OE segment) is directly dependent on automobile

demand.

September 21, 2011

8

Advisory Desk

TVS Srichakra

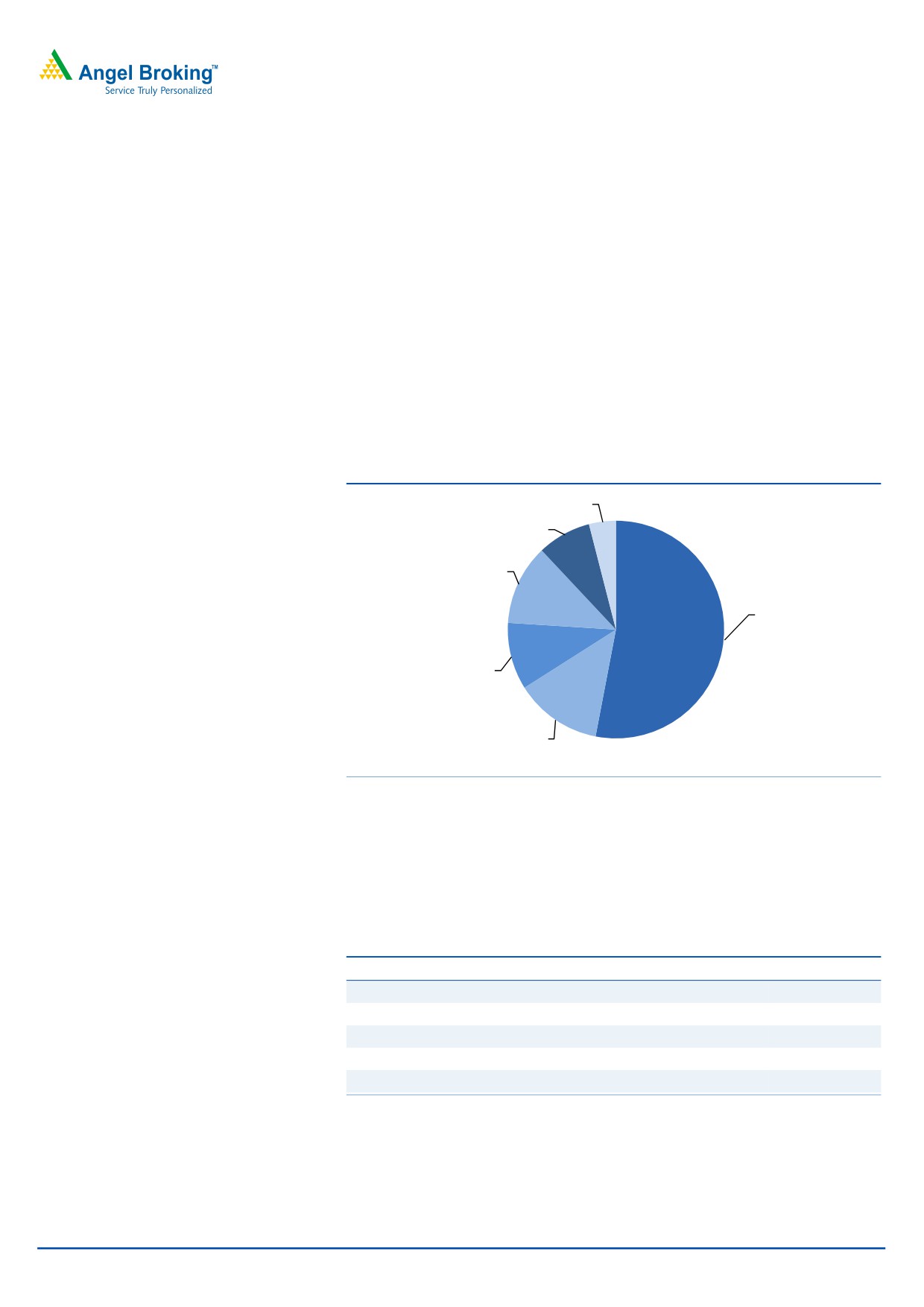

Tyre industry in India

According to Crisil Research, the Indian tyre industry is estimated at `29,000cr (as

of June 2011), registering a CAGR of 16% over FY2007-11. The industry has an

aggregate installed capacity of 13.7cr units and production of 9.7cr units of tyres

(FY2009-10). The industry has three segments: original equipment (OE) (26%),

replacement (63%) and exports (11%).

The industry’s margins are directly linked to raw-material cost, as it constitutes 66%

of sales turnover and 70% of operational cost. In FY2011, the industry’s operating

margin declined by 450-480bp from 13.4% in FY2009-10 because of the sharp

increase of 66% in natural rubber prices in the domestic market. In contrast, price

realisation for the same period was 17-19%, which was insufficient to sustain

margins.

Exhibit 13: Industry segments (As of March 2011)

Others

4%

LCV

8%

2/3 wheelers

12%

Truck and bus

53%

Tractors

10%

Cars and UVs

13%

Source: Crisil Research

Two-wheeler and three-wheeler tyre industry

The two and three-wheeler tyre industry is expected to grow at a CAGR of 13%

over FY2011-13E. MRF is the leader in this segment, with a market share of 28%

followed by TVSSL (25%).

Exhibit 14: Market share of two and three-wheeler tyres (FY2011)

Company

Market share (%)

MRF Ltd.

28

TVS Srichakra Ltd.

25

Falcon Tyres Ltd.

18

Ceat Ltd.

8

Others

21

Source: Crisil Research

September 21, 2011

9

Advisory Desk

TVS Srichakra

The company

TVSSL is part of the TVS Group. The company is a leading manufacturer of two

and three-wheeler tyres and enjoys a market share of

25% (FY2011).

The company manufactures a complete range of two and three-wheeler tyres for

the domestic market. For the export market, the company manufactures industrial

pneumatic tyres, farm and implements tyres, skid steer tyres, multipurpose tyres

and floatation tyres, among others. TVSSL’s manufacturing units are located at

Madurai, Tamil Nadu and Pantnagar (Uttarakhand). The company has a total

installed capacity of 330lakh units of tyres (as of March 2011).

In FY2010, TVSSL setup a new plant at Pantnagar, Uttarakhand, (production

started in July 2009) and increased the capacity at its Madurai plant. This resulted

in a significant increase of 170% in its installed capacity of automotive tyres to

3.3cr units in FY2011 from FY2009.

With a network of over 2,050 dealers and 20 warehouses across the country, the

company is a major supplier to TVS Motors, Hero MotoCorp, Bajaj Auto and India

Yamaha Motor. Exports constitute 11% of the company’s net sales, which includes

exports to the US, Europe, Africa, South America and Southeast Asia.

September 21, 2011

10

Advisory Desk

TVS Srichakra

Standalone profit and loss account

Y/E March (` cr)

FY2008

FY2009

FY2010

FY2011

FY2012E

FY2013E

Gross sales

520

643

753

1,181

1,557

1,749

Less: Excise duty

62

67

53

96

126

142

Net Sales

458

576

701

1,085

1,430

1,607

Other operating income

-

-

-

-

-

-

Total operating income

458

576

701

1,085

1,430

1,607

% chg

-

25.8

21.6

54.9

31.8

12.3

Net Raw Materials

304

390

432

691

940

1,047

% chg

28.2

10.6

60.0

36.2

11.4

Other Mfg costs

28

37

56

89

106

119

% chg

32.2

48.9

60.0

18.6

12.3

Personnel

35

42

54

84

103

116

% chg

20.8

26.9

57.7

22.0

12.3

Other

61

66

95

130

157

177

% chg

8.1

43.9

37.7

20.6

12.3

Total Expenditure

429

536

636

995

1,306

1,459

EBITDA

30

40

65

91

124

148

% chg

-

36.6

60.8

39.3

36.4

19.9

(% of Net Sales)

6.5

7.0

9.3

8.4

8.6

9.2

Depreciation& Amort.

9

10

12

16

22

24

EBIT

21

31

53

75

102

124

% chg

-

49.0

74.2

40.5

36.4

21.8

(% of Net Sales)

4.5

5.3

7.6

6.9

7.1

7.7

Interest & other Charges

11

19

16

30

36

38

Other Income

4

1

6

12

14

16

(% of sales)

0.9

0.2

0.8

1.1

1.0

1.0

Recurring PBT

9

12

38

45

66

86

% chg

-

25.3

221.6

20.0

46.8

30.0

Extraordinary Exps./(Inc.)

0

(0)

-

(0)

-

-

PBT (reported)

14

13

43

57

81

102

Tax

4

4

14

18

24

31

(% of PBT)

32.3

31.9

31.2

31.5

30.0

30.0

PAT (reported)

9

9

30

39

56

72

ADJ. PAT

9

9

30

39

56

72

% chg

-

(3.0)

232.4

31.4

44.1

26.9

(% of Net Sales)

2.0

1.6

4.3

3.6

3.9

4.5

Basic EPS (`)

12

12

39

51

74

94

Fully Diluted EPS (`)

12

12

39

51

74

94

% chg

-

(3.0)

232.4

31.4

44.1

26.9

Dividend

3

3

8

10

10

10

Retained Earning

7

6

22

30

47

62

September 21, 2011

11

Advisory Desk

TVS Srichakra

Standalone balance sheet

Y/E March (` cr)

FY2008

FY2009

FY2010

FY2011

FY2012E

FY2013E

SOURCES OF FUNDS

Equity Share Capital

8

8

8

8

8

8

Preference Capital

-

-

-

-

-

-

Reserves& Surplus

51

57

78

106

153

215

Shareholders’ Funds

59

65

86

114

161

223

Minority Interest

-

-

-

-

-

-

Total Loans

159

157

174

256

294

271

Deferred Tax Liability

8

8

8

10

10

10

Total Liabilities

225

230

268

380

465

504

APPLICATION OF FUNDS

Gross Block

127

146

192

250

270

291

Less: Acc. Depreciation

64

74

80

95

117

141

Net Block

63

72

112

155

153

151

Capital Work-in-Progress

1

1

3

10

10

10

Lease adjustment

-

-

-

-

-

-

Goodwill

-

-

-

-

-

-

Investments

1

1

3

3

3

3

Current Assets

219

213

315

481

650

732

Cash

4

13

9

5

9

12

Loans & Advances

37

27

32

37

49

55

Inventory

94

65

155

264

348

391

Debtors

85

107

119

174

243

273

Current liabilities

59

57

166

269

351

392

Net Current Assets

160

156

150

212

299

341

Misc. Exp. not written off

-

-

-

-

-

-

Deferred tax assets

-

-

-

-

-

-

Total Assets

225

230

268

380

465

504

September 21, 2011

12

Advisory Desk

TVS Srichakra

Key ratios

Y/E March

FY2008

FY2009

FY2010

FY2011

FY2012E

FY2013E

Valuation Ratio (x)

P/E (on FDEPS)

29.3

30.2

9.1

6.9

4.8

3.8

P/CEPS

14.8

14.4

6.5

4.9

3.5

2.8

P/BV

4.6

4.2

3.2

2.4

1.7

1.2

Dividend yield (%)

1.0

1.0

2.8

3.5

3.5

3.5

EV/Sales

0.9

0.7

0.6

0.5

0.4

0.3

EV/EBITDA

14.3

10.2

6.7

5.7

4.5

3.6

EV / Total Assets

1.9

1.8

1.6

1.4

1.2

1.0

Per Share Data (`)

EPS (Basic)

12.1

11.7

38.9

51.2

73.7

93.5

EPS (fully diluted)

12.1

11.7

38.9

51.2

73.7

93.5

Cash EPS

24.0

24.6

54.3

71.8

101.9

124.7

DPS

3.5

3.5

10.0

12.5

12.5

12.5

Book Value

77.2

84.8

112.1

148.7

209.9

291.0

DuPont Analysis

-

-

-

-

EBIT margin

4.5

5.3

7.6

6.9

7.1

7.7

Tax retention ratio

0.7

0.7

0.7

0.7

0.7

0.7

Asset turnover (x)

2.1

2.7

2.8

3.0

3.2

3.4

ROIC (Post-tax)

6.4

9.7

14.4

14.2

16.1

18.2

Cost of Debt (Post Tax)

4.8

8.2

6.2

7.9

8.5

9.9

Leverage (x)

2.6

2.2

1.9

2.2

1.8

1.1

Operating ROE

10.4

13.1

30.2

27.8

29.5

27.7

Returns (%)

ROCE (Pre-tax)

9.1

13.3

19.9

19.7

21.9

24.7

Angel ROIC (Pre-tax)

9.4

14.3

21.0

20.7

23.1

26.0

ROE

15.6

13.8

34.7

34.4

35.1

32.2

Turnover ratios (x)

Asset TO (Gross Block)

3.6

4.0

3.6

4.3

5.3

5.5

Inventory / Sales (days)

75

41

81

89

89

89

Receivables (days)

67

68

62

59

62

62

Payables (days)

50

39

95

99

98

98

WC cycle (ex-cash) (days)

124

90

74

70

74

75

Solvency ratios (x)

Net debt to equity

2.6

2.2

1.9

2.2

1.8

1.1

Net debt to EBITDA

5.2

3.5

2.5

2.7

2.3

1.7

Int. Coverage (EBIT/ Int.)

1.8

1.6

3.4

2.5

2.9

3.3

September 21, 2011

13

Advisory Desk

TVS Srichakra

Advisory Team Tel: (91) (022) 39500777

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

TVS Srichakra

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to 15%)

Sell (< -15%)

September 21, 2011

14