IPO Note | HFCs

March 11, 2013

Repco Home Finance (RHFL)

SUBSCRIBE

Issue Open: March 13, 2013

Attractive Priority

Issue Close: March 15, 2013

Operates in attractive loan segment - Priority sector home loans: RHFL is largely

Issue Details

focused on providing home loans in tier-II and tier-III cities (with a sub-`10lakh

average loan ticket size), due to which a large part of its book qualifies as priority

Face Value: `10

sector lending (PSL) for banks. In our view, NBFCs operating in PSL segments

Present Eq. Paid-up Capital: `46.4cr

enjoy competitive advantages, as most banks (especially in the private sector)

have a perennial shortage in meeting their PSL targets, creating favorable

Offer Size: 1.57cr Shares

demand-supply dynamics for those NBFCs that can source higher-yielding PSL

Post Eq. Paid-up Capital: `62.2cr

loans at reasonable asset quality.

Issue size (amount):* `259-270cr

REPCO’s loan book profile also allows it to procure 44% of its total borrowing via

low-cost NHB refinance averaging about 7.5-8% (NHB refinance is available

Price Band: `165-172

under various schemes, primarily for rural loans upto `15lakh and also for low

Post-issue implied mkt. cap*: `1,026cr-

1,069cr

cost urban housing loans up to `10lakhs). Moreover, the funding that it gets from

banks in turn largely qualifies as PSL for the banks (loans by banks to NBFCs,

Promoters holding Pre-Issue: 50.0%

which are on-lent as home loans less than `10lakhs qualify as PSL). This makes it

Promoters holding Post-Issue: 37.4%

attractive for banks to lend to RHFL at a reasonable cost (about 100bps above

Note:*At the lower and upper price band,

base rate), as against alternatives such as parking funds under RIDF at extremely

respectively

low yields, to meet their PSL targets. Relatively low-cost NHB and bank funding

enables it to maintain healthy margins and return ratios (NIMs at 3.8% and RoE

Book Building

at 22.2% in 1HFY2013, calculated on an annualized basis)

QIBs

Up to 50%

In terms of borrower profile, around 53% of RHFL’s outstanding loan book

Non-Institutional

At least 15%

constituted loans to relatively higher-yielding higher-risk non-salaried segment. To

mitigate risks, the company, lends at a low LTV of about 65%, as per the

Retail

At least 35%

management. In terms of geographical presence, 67% and 98% of its business is

concentrated in Tamil Nadu and South India, respectively, largely in tier-II and

tier-III cities.

Post Issue Shareholding Pattern

Management expects strong growth to continue: Over FY2008-12, the company

Promoters Group

37.4

grew its loan book at a CAGR of 43.8% (albeit on a small base) to `2,802cr,

MF/Banks/Indian

63.6

driving PAT CAGR of 43.3%. As of September 30, 2012, its CRAR stood at a

FIs/FIIs/Public & Others

comfortable 15.9% (entirely tier-I). Further, IPO proceeds would increase its

capital base by nearly 0.9x, providing enough headroom for maintaining strong

loan growth for the next few years as well. Funding mix is also expected to remain

stable (In FY2014 NHB refinance facility for Rural housing fund increased by 50%

to `6,000cr; bank demand for PSL opportunities is also expected to remain strong

and future outlook is favorable, in our view, given government’s priority sector

focus).

Outlook & Valuation: RHFL generated 22.2% RoE in 1HFY2013E and would trade

at 1.8x FY2013E ABV (at the upper end of its price band, based on post-issue

networth). Closest comparable peer - Gruh HF (mainly western India, rural and

semi-urban focus, largely PSL qualifying home loans) appears extremely

expensive at valuations of 7.3x FY2013E BV, notwithstanding its ~30% earnings

growth trajectory and ~35% ROEs (FY2013E). Other NBFCs like Mahindra

Vaibhav Agrawal

Finance and Shriram Transport Finance operating in different priority sector

022 - 39357800 Ext: 6808

segments to a varying degree and generating similar return ratios, are trading at

2.6x and 2.3x FY2013E ABV, respectively (but they have larger, relatively more

seasoned loan books and longer proven track record). Overall, keeping in mind

Sourabh Taparia

RHFL’s attractive niche loan segment, strong growth prospects and reasonable

022 - 39357800 Ext: 6872

valuations, we recommend subscribe to the issue at the upper band.

Please refer to important disclosures at the end of this report

1

RHFL | IPO Note

Key Financials

Particulars (Rs cr)

FY2009

FY2010

FY2011

FY2012

1HFY13

NII

43

73

98

117

63

% chg

63.6

69.4

33.8

19.3

18.4*

Net Profit

25

44

57

68

36

% chg

66.6

74.9

28.7

19.4

10.2*

RoA (%)

2.9

3.5

3.2

2.7

2.4

RoE (%)

17.7

25.7

26.2

24.8

22.2

P/ABV (x) Lower End

5.5

4.5

3.6

2.9

-

P/ABV (x) Upper End

5.2

4.2

3.4

2.7

-

Source: Company, Angel Research, Note: *yoy growth

Company background

RHFL, a south based housing finance company, was established in April 2000 as a

wholly owned subsidiary of Repco Bank. The company is primarily engaged in the

business of individual home loans and loans against property, which as of

1HFY2013 accounts for 85.6% and 14.4% of its loan book respectively. As of

December 31, 2012, it had a total of 73 branches and 19 satellite centers located

in Tamil Nadu, Karnataka, Andhra Pradesh, Kerala, Maharashtra, Odisha, West

Bengal, Gujarat and the Union Territory of Pondicherry.

In December 2007, the company raised funds to the tune of `76cr from Carlyle

group, a global alternative asset manager and by virtue of which Carlyle group

acquired 49.9% stake in the company. Recently, Carlyle group has transferred

26.2% of the total equity shares to Creador 1 LLC, WCP Holdings III and certain

other entities; and hence Carlyle currently hold a 23.7% stake in the company.

Repco Bank, the promoter of the company, is a Government of India owned co-

operative bank, which was established to help and promote the rehabilitation of

repatriates from Sri Lanka, Myanmar, Vietnam and other countries. Its operations

are largely confined in the four South Indian states and the Union Territory of

Puducherry. During FY2012, Repco Bank reported a net profit growth of 30.3%

yoy to `73cr, on a total asset base of `4,875cr, which grew by 33.4% yoy.

Mr. R. Varadarajan is the Managing Director of the company as well as the

promoter and has 35 years of experience in banking industry. He is responsible for

the overall strategy and direction of the company. Most of the key management

personnel have healthy experience in the housing finance and the banking industry

and have been associated with the company for anywhere between 4-9 years.

Details of the issue

The IPO comprises an issue of fresh equity shares of 1.57cr of face value `10 each

to the public, with a reservation of 0.02cr equity shares for subscription by eligible

employees. The issue constitutes 25.3% of the post-issue paid-up capital. The price

band for the issue has been fixed at `165-172/ share, valuing the company at

`1,026cr - `1,069cr. REPCO HF intends to utilize the proceeds to augment its

capital base, so as to meet future capital adequacy requirements. As of September

30, 2012, its CRAR stood at 15.9%, much above the regulatory minimum of 12%.

Post-issue, the shareholding of the promoters in the company will fall to 37.4%

from the current holding of 50.0%.

March 11, 2013

2

RHFL | IPO Note

Investment arguments

Operates in attractive loan segment - Priority sector home loans

RHFL is largely focused on providing home loans in tier-II and tier-III cities (with a

sub-`10lakh average loan ticket size), due to which a large part of its book

qualifies as priority sector lending (PSL) for banks. In our view, NBFCs operating in

PSL segments enjoy competitive advantages, as most banks (especially in the

private sector) have a perennial shortage in meeting their PSL targets, creating

favorable demand-supply dynamics for those NBFCs that can source higher-

yielding PSL loans at reasonable asset quality.

REPCO’s loan book profile also allows it to procure 44% of its total borrowing via

low-cost NHB refinance averaging about 7.5-8%. NHB refinance is available

under various schemes, primarily for rural loans upto `15lakh and also for low

cost urban housing loans up to `10lakhs. As per the management, of its total NHB

refinance roughly two-third pertained to rural schemes and balance pertained to

urban schemes. Moreover, the funding that it gets from banks in turn largely

qualifies as PSL for the banks (loans by banks to NBFCs, which are on-lent as

home loans less than `10lakhs qualify as PSL). This makes it attractive for banks to

lend to RHFL at a reasonable cost (about 100bps above base rate), as against

alternatives such as parking funds under RIDF at extremely low yields, to meet their

PSL targets. Relatively low-cost NHB and bank funding enables it to maintain

healthy margins and return ratios (NIMs at 3.8% and RoE at 22.2% in 1HFY2013,

calculated on an annualized basis).

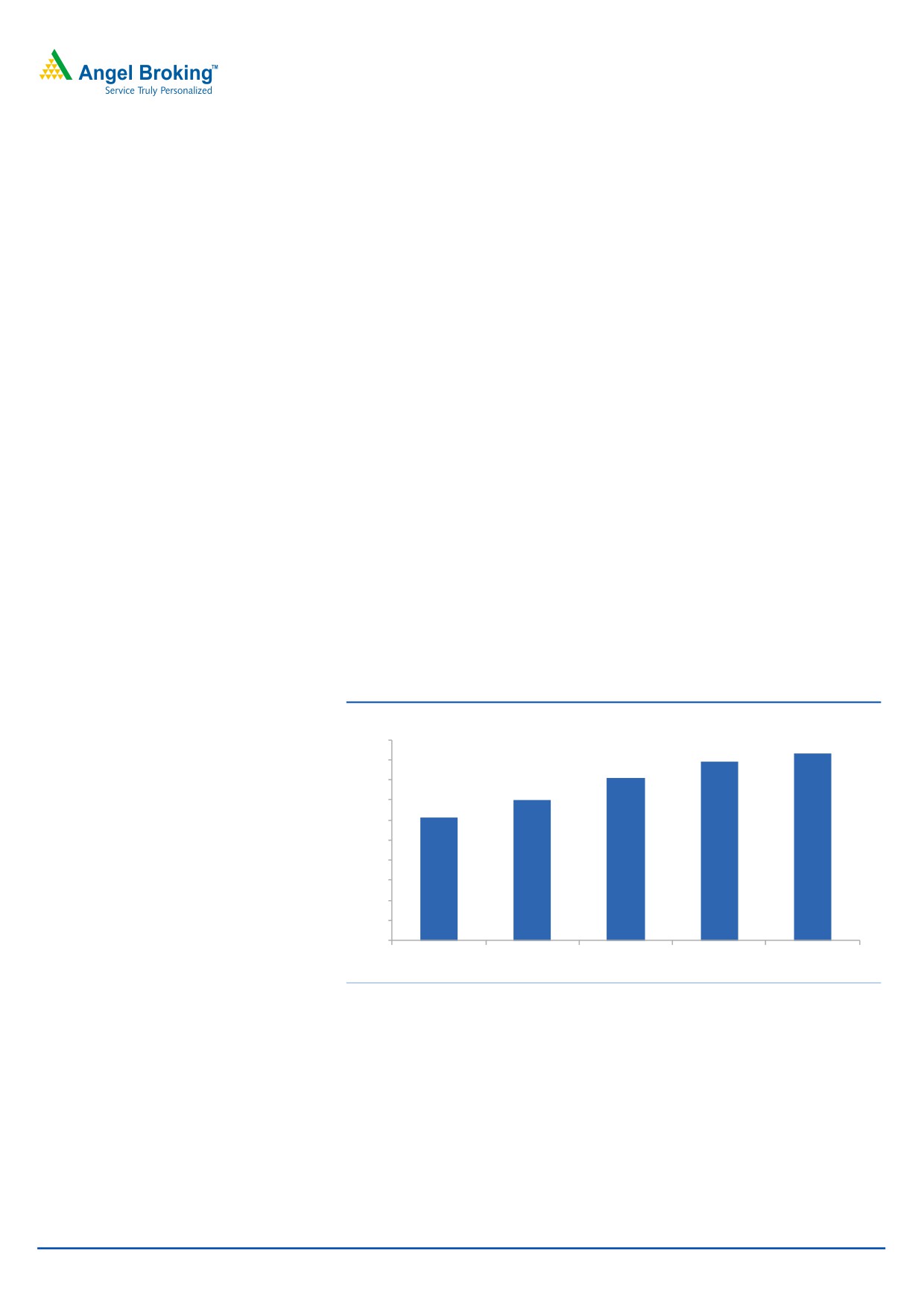

Exhibit 1: Average loan ticket size for the company

(` lakh)

10

9

9.3

8

8.9

8.1

7

7.0

6

6.1

5

4

3

2

1

0

FY2009

FY2010

FY2011

FY2012

1HFY13

Source: Company, Angel Research

March 11, 2013

3

RHFL | IPO Note

Exhibit 2: Salient features of some NHB refinance schemes

Scheme Name

Loan size

Location

Tenure (yrs) Ultimate borrower

Interest Rate

Golden Jubilee Rural Housing Refinance Scheme upto `15lakh Rural

1 -15 Any

Floating/fixed

Rural Housing Fund

upto `15lakh Rural

3 - 7 Weaker section

Fixed

Special Refinance Scheme for Urban Low

Persons having annual household

upto `10lakh

Urban

5 -15

Fixed

Income Housing

income below `2lakh

Liberalized Refinance Scheme

Any

Rural/Urban

1 -15 Any

Floating/fixed

Energy Efficient Housing Refinance Scheme

Any

Urban

1 -15 Any

Fixed

Source: NHB, Angel Research

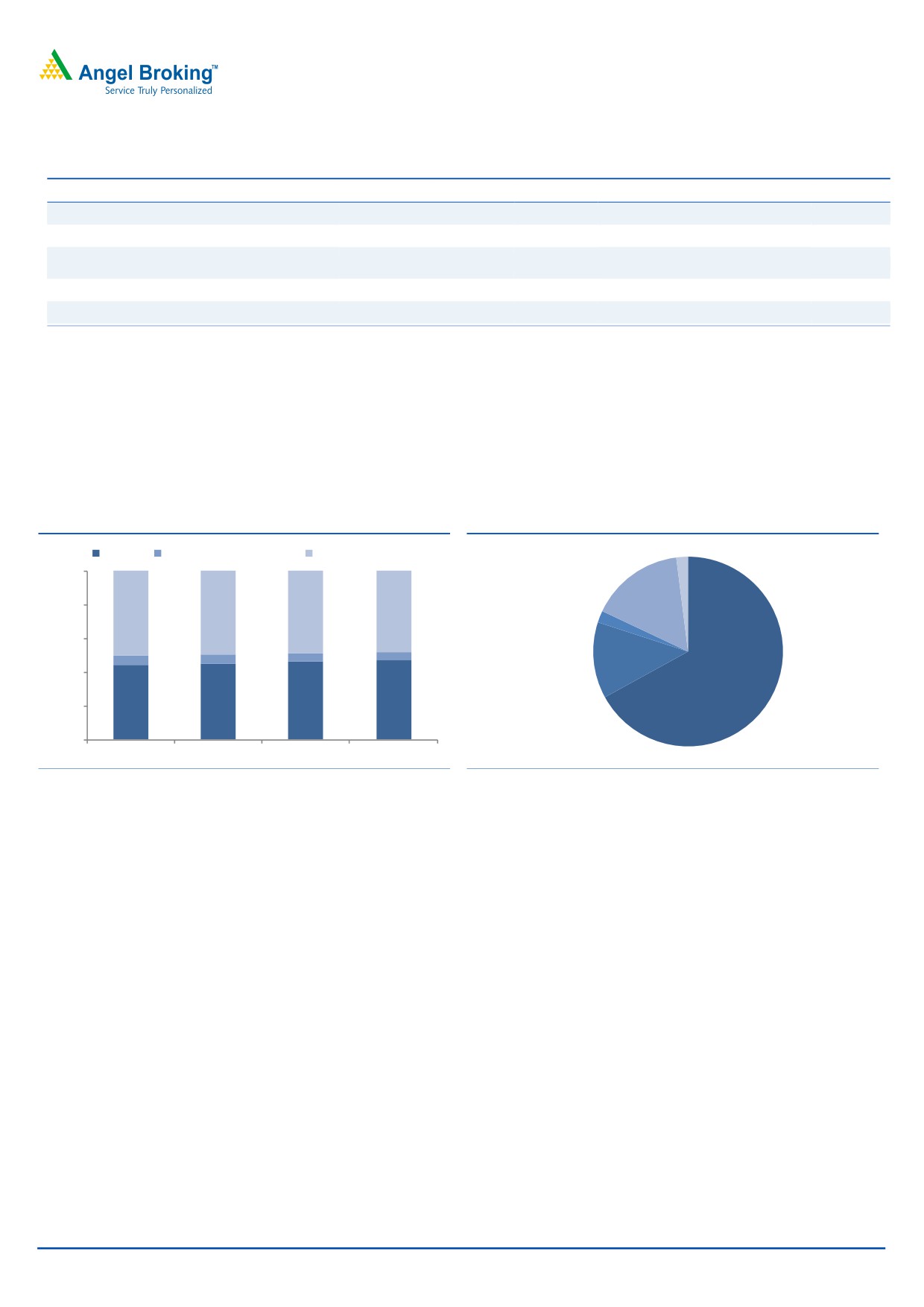

In terms of borrower profile, around 53% of REPCO’s outstanding loan book

constituted loans to relatively higher-yielding higher-risk non-salaried segment. To

mitigate risks, the company, lends at a low LTV of about 65%, as per the

management. In terms of geographical presence, 67% and 98% of its business is

concentrated in Tamil Nadu and South India, respectively, largely in tier-II and tier-

III cities.

Exhibit 3: Borrower profile wise loan book

Exhibit 4: Region-wise loan book, as of FY2012

Salaried

Professionals/Self employed

Loan to Businessmen

100%

Maharashtra

2%

Andhra Pradesh

16%

80%

50.0

49.3

48.9

48.2

Kerala

2%

60%

Karnataka

5.8

4.6

4.5

5.8

13%

40%

Tamil Nadu

67%

44.1

44.9

46.5

47.3

20%

0%

FY2010

FY2011

FY2012

1HFY13

Source: Company, Angel Research

Source: Company, Angel Research

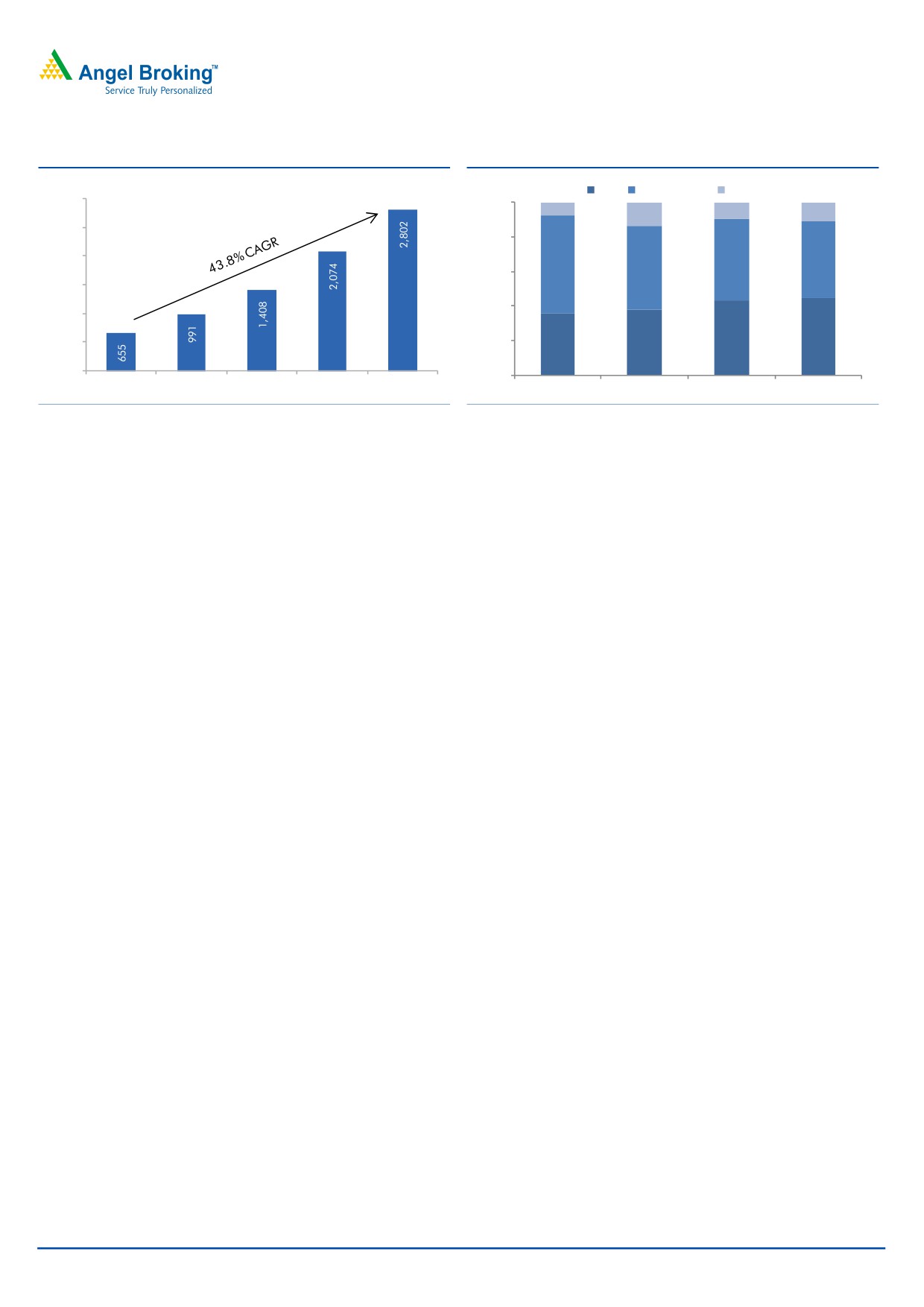

Management expects strong growth to continue

Over FY2008-12, the company grew its loan book at a CAGR of 43.8% (albeit on

a small base) to `2,802cr, driving PAT CAGR of 43.3%. As of September 30,

2012, its CRAR stood at a comfortable 15.94% (entirely tier-I). Further, IPO

proceeds would increase its capital base to nearly 1.9x, providing enough

headroom for maintaining strong loan growth for the next few years as well.

RHFL’s funding mix, which primarily comprises of loans from bank and NHB, is

also expected to remain stable, going ahead, given the government’s priority

sector focus, which is evident in 50% yoy increase in its allocation of funds to NHB

refinance facility for Rural Housing Fund during FY2014 (from `4,000cr to

`6,000cr) and strong demand from banks for PSL opportunities, considering a

perennial shortage in meeting their PSL targets, in case of most banks (especially

in the private sector).

March 11, 2013

4

RHFL | IPO Note

Exhibit 5: Strong loan book growth (on a low base)

Exhibit 6: RHFL’s funding profile

(` cr)

SCBs

NHB - refinance

Promoter

3,000

100%

7.8

9.8

13.6

11.3

2,500

80%

2,000

47.2

44.3

56.4

48.3

60%

1,500

40%

1,000

43.0

44.4

500

20%

35.8

38.0

0

0%

FY2008

FY2009

FY2010

FY2011

FY2012

FY2010

FY2011

FY2012

1HFY13

Source: Company, Angel Research

Source: Company, Angel Research

Key risks/concerns

Relatively unseasoned, fast growing loan book, focus on non -

salaried segment could pose asset quality concerns

RHFL grew its loan book at a CAGR of 43.8% over FY2008-12, much higher than

industry levels, owing to a small base. From `655cr in FY2008, its loan book has

grown more than 3x to `2,802cr in FY2012, and hence a large part of its loan

book appears unseasoned. Further, a sizeable proportion of its loan book

constitutes loans to non-salaried borrowers (53% as of 1HFY13), which is generally

regarded as a more vulnerable segment from an asset quality point-of-view, given

the inherently more uncertain income stream of the borrowers, which could be

exacerbated by low ticket size.

GNPA ratio for the company has increased consistently over the last three years,

from 1.0% in FY2010 to 1.4% in FY2012. Segment-wise, while GNPA ratio in the

loans against property segment declined from 1.4% in FY2010 to 1.1% in FY2012,

it grew from 1.2% to 1.4% over the same period for its individual home loan

portfolio. On an absolute basis, while GNPA levels for the company grew at a

CAGR of 59.3% over FY2009-12, doubtful and loss assets as a proportion to total

Gross NPAs increased from 27.9% in FY2010 to 47.6% in FY2012. PCR ratio for

the company stood at 31% as of FY2012.

Even during 1HFY2013, subdued economic environment has resulted in a further

increase in the GNPA ratio for the company to 2.1%. Though, HFCs generally face

higher delinquencies during the year, which get normalize at the end, however,

considering continued weakness in the economy and unseasoned nature of its loan

book, in our view, the asset quality of the company is likely to remain a concern.

Funding dependent on banks and NHB refinance

As of 1HFY2013, around 44% of its total funding constituted borrowings from

NHB, while the remaining came from banks (44%) and its parent company (12%).

NHB has been extending refinance at an average rate of around 7.5-8% to HFCs

under various schemes, primarily for rural loans upto `15lakh, while, banks also

extend loans to HFCs at a reasonable cost to meet their PSL targets, as on-lending

as home loans less than `10lakhs qualify as PSL for banks.

March 11, 2013

5

RHFL | IPO Note

If some or all of these low cost funding alternatives, cease to be entirely

available/are available in a reduced extent to HFCs, being a small housing

finance company and considering its funding profile, the cost of funding and

business growth would get severely impacted for the company. However, given the

strong focus of the Government on priority sector, in our view, such an adverse

event is highly unlikely to take place. Even in FY2014, the Government has

increased the allocation for NHB refinance facility for Rural housing fund by 50%

to `6,000cr and bank demand for PSL opportunities also continues to remain

strong.

Regional concentration risk

RHFL’s business is geographically confined to four south Indian states (98% of total

business, as of FY2012), of which, Tamil Nadu constitutes the largest pie (67% of

total business, as of FY2012). The company has expansion plans in place to

improve the proportion of its non-south loan-book (2% currently, only from

Maharashtra), and has opened new branches in West Bengal, Orissa and Gujarat

during the previous year. Hence, its business is likely to remain concentrated in

South India and particularly in Tamil Nadu and would remain vulnerable to

regional concentration risks, more so, as a large part of its loan book comes from

non-salaried segment. As of 1HFY2013, around 53% of its loan book constituted

loans to non-salaried segment, of which, loans to businessmen constituted 48% of

the total loan book, balance being loans to professionals.

Outlook and valuation

RHFL generated RoEs of 22.2% in 1HFY2013E and would trade at 1.8x FY2013E

ABV (at the upper end of its price band, based on post-issue networth). Closest

comparable peer - Gruh HF (mainly western India, rural and semi-urban focus,

largely PSL qualifying home loans) appears extremely expensive at valuations of

7.3x FY2013E BV, notwithstanding its ~30% earnings growth trajectory and ~35%

ROEs (FY2013E). Other NBFCs like Mahindra Finance and Shriram Transport

Finance operating in different priority sector segments to a varying degree and

generating similar return ratios, are trading at 2.6x and 2.3x FY2013E ABV

respectively (but they have larger, relatively more seasoned loan books and longer

proven track record). Overall, keeping in mind RHFL’s attractive niche loan

segment, strong growth prospects and reasonable valuations, we recommend

subscribe to the issue at the upper band.

Exhibit 7: Comparative profile of select HFCs

Loan Avg. ticket

Funding (%)

Company

Gross NPANet NPA

book (` cr) size(` lakh) NHB ref. Banks NCD Others

CANFIN$

3,592

NA

25.9

67.9

0.0

6.3

0.90%

0.00%

GIC$

3,872

NA

15.3

78.1

0.0

6.6

2.08%

0.41%

DEWAN*

24,340

8.4

7.2

67.9

11.8

13.0

0.73%

0.00%

GRUH*

5,003

4.6

49.4

34.0

3.7

12.8

0.53%

0.00%

REPCO#

3,098

8.9

44.3

44.4

0.0

11.3

2.12%

1.59%

Source: Company, Angel Research, Note: *as of Dec 31, 2012, however, for GRUH, funding and

average ticket size as of FY2012, #as of Sept 30, 2012, $as of March 31, 2012

March 11, 2013

6

RHFL | IPO Note

Exhibit 8: Comparative DuPont analysis

GIC

CANFIN

GRUH

REPCO

Parameter

FY2011

FY2012

1HFY13* FY2011 FY2012 1HFY13* FY2011 FY2012 1HFY13* FY2011 FY2012 1HFY13*

Yield

9.8

10.9

12.1

10.1

11.2

11.8

12.3

13.7

13.5

12.0

12.4

12.2

Prov.#

1.1

0.5

0.3

0.1

0.3

0.2

0.1

0.1

0.5

0.3

0.4

0.4

Risk adj. yields

8.7

10.4

11.8

10.1

10.9

11.6

12.2

13.6

13.0

11.7

12.0

11.8

Cost

6.3

7.8

8.3

6.9

7.8

8.6

6.8

8.2

8.6

7.1

8.2

8.4

Adj. NII

2.4

2.6

3.5

3.2

3.1

3.1

5.4

5.4

4.4

4.5

3.8

3.4

Other Income

2.7

0.1

0.0

0.2

0.3

0.0

0.0

0.0

0.0

0.7

0.5

0.4

Operating Income

5.1

2.7

3.5

3.4

3.4

3.1

5.4

5.4

4.4

5.2

4.3

3.8

Operating Exp#

0.8

0.8

0.8

0.8

0.9

0.9

1.1

1.0

1.0

0.8

0.8

0.7

PBT

4.2

2.0

2.7

2.6

2.4

2.2

4.3

4.3

3.4

4.3

3.5

3.2

Taxes

0.9

0.5

0.7

0.7

0.7

0.5

1.2

1.1

1.0

1.2

0.8

0.8

RoA

3.3

1.5

2.0

1.9

1.8

1.7

3.1

3.2

2.4

3.2

2.7

2.4

Leverage

8.1

8.3

8.5

7.6

7.6

8.3

10.1

10.7

10.8

8.3

9.1

9.3

RoE

26.7

12.3

17.4

14.3

13.3

14.4

31.4

34.2

25.9

26.2

24.8

22.2

Source: Company, Angel Research, Note:*on an annualized basis, #for CANFIN and GIC, as the data regarding provisioning expenses in total operating

expense was unavailable for 1HFY13, assumed similar run-rate for operating expenses (excl. provisions) for 1HFY13 as was in FY2012

Exhibit 9: Valuation Summary

Trailing* RoA

Trailing* RoE Trailing* P/ABV (x)

FY13E P/ABV (x)

CANFIN

1.8

14.5

0.9

0.8

GICHF

1.9

14.9

1.2

1.1

DEWAN

1.7

17.5

1.0

0.9

GRUH

3.2

33.1

8.3

7.3

REPCO

2.5

25.9

2.6

1.8

SHRIRAM TRAN.

3.1

20.8

2.5

2.3

M&MFIN

3.5

24.2

3.8

2.6

Source: Company, Angel Research, Note: *as of 1HFY2013

March 11, 2013

7

RHFL | IPO Note

Income statement (standalone)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012

1HFY13*

NII

43

73

98

117

63

- YoY Growth (%)

63.6

69.4

33.8

19.3

18.4

Other Income

2

1

0

0

0

- YoY Growth (%)

(17.9)

(66.9)

(39.7)

(82.9)

-

Operating Income

45

74

98

117

63

- YoY Growth (%)

56.5

63.1

33.1

18.9

18.4

Operating Expenses

7

9

15

19

10

- YoY Growth (%)

1.3

31.9

59.5

29.7

21.3

Pre - Provision Profit

38

64

83

97

54

- YoY Growth (%)

74.2

69.0

29.2

16.9

17.9

Prov. & Cont.

3

4

5

9

6

- YoY Growth (%)

209.4

29.8

53.3

74.2

7.1

Profit Before Tax

35

61

78

88

48

- YoY Growth (%)

68.5

72.0

27.9

12.9

19.4

Prov. for Taxation

10

17

21

20

12

- as a % of PBT

28.8

27.7

27.2

23.0

25

PAT

25

44

57

68

36

- YoY Growth (%)

66.6

74.9

28.7

19.4

10.2

Note:*growth is on a yoy basis, i.e. 1HFY13 over 1HFY12

Balance sheet (standalone)

Y/E March (` cr)

FY2009 FY2010

FY2011

FY2012

1HFY13*

Share Capital

79

46

46

46

46

Reserve & Surplus

73

144

195

257

292

Loan Funds

849

1,258

1,810

2,486

2,735

- Growth (%)

47.6

48.1

43.9

37.4

28.4

Other Liabilities & Provisions

30

35

46

61

75

Total Liabilities

1,032

1,483

2,097

2,851

3,149

Investments

1

2

2

8

8

Advances

991

1,409

2,076

2,807

3,103

- Growth (%)

51.3

42.2

47.3

35.2

10.5

Fixed Assets

1

2

3

3

3

Cash & Bank

35

64

8

18

17

Other Assets

4

5

8

15

18

Total Assets

1,032

1,483

2,097

2,851

3,149

Note:*growth is on a yoy basis, i.e. 1HFY13 over 1HFY12

March 11, 2013

8

RHFL | IPO Note

Ratio analysis (standalone)

Y/E March

FY2009

FY2010

FY2011

FY2012

1HFY13

Profitability ratios (%)

NIMs

4.6

5.2

4.8

4.2

3.8

Cost to Income Ratio

15.7

12.7

15.3

16.7

15.4

RoA

2.9

3.5

3.2

2.7

2.4

RoE

17.7

25.7

26.2

24.8

22.2

Asset Quality (%)

Gross NPAs

0.96

1.24

1.21

1.37

2.12

Net NPAs

0.69

0.96

0.95

0.95

1.58

Provision Coverage

27.9

22.1

21.7

30.8

25.3

Per Share Data (`)

EPS

5.4

9.5

12.2

14.5

7.7

ABVPS (100% cover.)

31.2

38.1

47.8

59.6

62.4

DPS

0.4

1.0

1.0

1.1

-

Valuation Ratios

PER (x) at upper band

31.8

18.2

14.1

11.8

-

PER (x) at lower band

30.5

17.4

13.5

11.3

-

P/ABVPS (x) at upper band

5.5

4.5

3.6

2.9

-

P/ABVPS (x) at lower band

5.2

4.2

3.4

2.7

-

DuPont Analysis

NII

4.6

5.2

4.8

4.2

3.8

(-) Prov. Exp.

0.3

0.3

0.3

0.4

0.4

Adj. NII

4.3

4.9

4.5

3.8

3.4

Other Inc.

0.6

0.6

0.7

0.5

0.4

Op. Inc.

4.8

5.6

5.2

4.3

3.8

Opex

0.8

0.7

0.8

0.8

0.7

PBT

4.0

4.8

4.3

3.5

3.2

Taxes

1.2

1.3

1.2

0.8

0.8

RoA

2.9

3.5

3.2

2.7

2.4

Leverage

6.2

7.3

8.3

9.1

9.3

RoE

17.7

25.7

26.2

24.8

22.2

March 11, 2013

9

RHFL | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

March 11, 2013

10

RHFL | IPO Note

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Bhavesh Chauhan

Sr. Analyst (Metals & Mining)

Viral Shah

Sr. Analyst (Infrastructure)

Sharan Lillaney

Analyst (Mid-cap)

V Srinivasan

Analyst (Cement, FMCG)

Yaresh Kothari

Analyst (Automobile)

Ankita Somani

Analyst (IT, Telecom)

Sourabh Taparia

Analyst (Banking)

Bhupali Gursale

Economist

Vinay Rachh

Research Associate

Amit Patil

Research Associate

Shareen Batatawala

Research Associate

Twinkle Gosar

Research Associate

Tejashwini Kumari

Research Associate

Technicals:

Shardul Kulkarni

Sr. Technical Analyst

Sameet Chavan

Technical Analyst

Sacchitanand Uttekar

Technical Analyst

Derivatives:

Siddarth Bhamre

Head - Derivatives

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Hiten Sampat

Sr. A.V.P- Institution sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Akshay Shah

Sr. Executive

Production Team:

Tejas Vahalia

Research Editor

Dilip Patel

Production

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE: INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

March 11, 2013

11