Initiating Coverage | Power

March 16, 2015

Power Grid Corporation of India

BUY

CMP

`147

Healthy capitalisation provides earnings visibility

Target Price

`170

Power Grid Corporation of India (PGCIL) is among the largest transmission

Investment Period

12 Months

utilities in the world and is one of the best plays on the power sector in India

Stock Info

owing to its assured ROE model and strong earnings visibility.

Sector

Power

Huge investments lined up for augmenting power generation and transmission

Market Cap (` cr)

76,695

capacities: Power generation capacity in the country is expected to increase to

Net Debt (` cr)

66,343

~318GW by the end of the XII plan and a further addition of ~110GW has been

Beta

1.0

planned during the XIII plan. The transmission sector is also expected to see huge

52 Week High / Low

98 / 159

investments of ~`1,80,000cr and ~`2,00,000cr during the XII and XIII plan,

Avg. Daily Volume

2,73,051

respectively. A majority of these investments are expected to be towards

Face Value (`)

10

inter-regional transmission.

BSE Sensex

28,503

Regulated ROE model assures steady earnings growth: PGCIL receives a fixed

Nifty

8,648

return on equity (ROE) of 15.5%, with an additional 0.5% for timely completion of

Reuters Code

PGRD.BO

projects, as per norms laid out by the Central Electricity Regulatory Commission

Bloomberg Code

PWGR IN

(CERC). The fixed ROE model implies that earnings growth is directly linked to the

growth in assets capitalised. We estimate PGCIL’s current projects under

Shareholding Pattern (%)

implementation to be upwards of `1,00,000cr, providing strong earnings visibility.

Promoters

57.9

Strong capex plans to drive growth: PGCIL has incurred a capex of ~`60,000cr

MF / Banks / Indian Fls

7.7

since the beginning of FY2013 and remains well on track to achieve the XII plan

FII / NRIs / OCBs

27.6

capex target of `110,000cr. Further, we expect ~60-65% of XIII plan investments

Indian Public / Others

6.8

in the transmission sector toward inter-state transmissions, implying a capex

outlay of ~`1,20,000-1,30,000cr by PGCIL. The pace of capitalisation has also

Abs. (%)

3m 1yr

3yr

picked up in recent years, with FY2015 expected to have a capitalisation to capex

Sensex

4.2

30.9

60.0

ratio of >1.

Power Grid

8.8

48.5

32.0

Outlook and Valuation: Led by the strong capex plans and a healthy

capitalisation rate, we expect PGCIL to report a top-line and bottom-line CAGR of

3-Year Daily price chart

~15% and ~17% over FY2014-17E. At the current market price of `147, the

stock trades at a P/B of 1.8x and 1.7x its FY2016E and FY2017E BV of `79.7 and

180

160

`88.7, respectively. We initiate coverage on the stock with a Buy recommendation

140

and a target price of `170, based on ~1.9x FY2017E book value, implying a

120

16% upside from the current levels.

100

80

Key financials

60

Y/E March (` cr)

FY2014

FY2015E

FY2016E

FY2017E

Net sales

15,230

17,177

20,085

22,938

% chg

19.4

12.8

16.9

14.2

Source: Capitaline

Net profit

4,497

4,991

6,127

7,277

% chg

7.3

12.4

20.5

18.8

EBITDA margin (%)

85.1

86.4

86.5

86.7

EPS (`)

9.4

9.5

11.7

13.9

P/E (x)

15.6

15.4

12.5

10.5

P/BV (x)

2.2

2.0

1.8

1.7

RoE (%)

14.9

14.1

15.4

16.5

RoCE (%)

8.3

7.7

8.1

8.4

Rahul Dholam

EV/Sales (x)

10.2

9.7

8.9

8.2

022-39357800 Ext: 6847

EV/EBITDA (x)

12.0

11.3

10.2

9.5

Source: Company, Angel Research, Note: CMP as of March 13, 2015

Please refer to important disclosures at the end of this report

1

Power Grid Corporation of India | Initiating Coverage

Investment Arguments

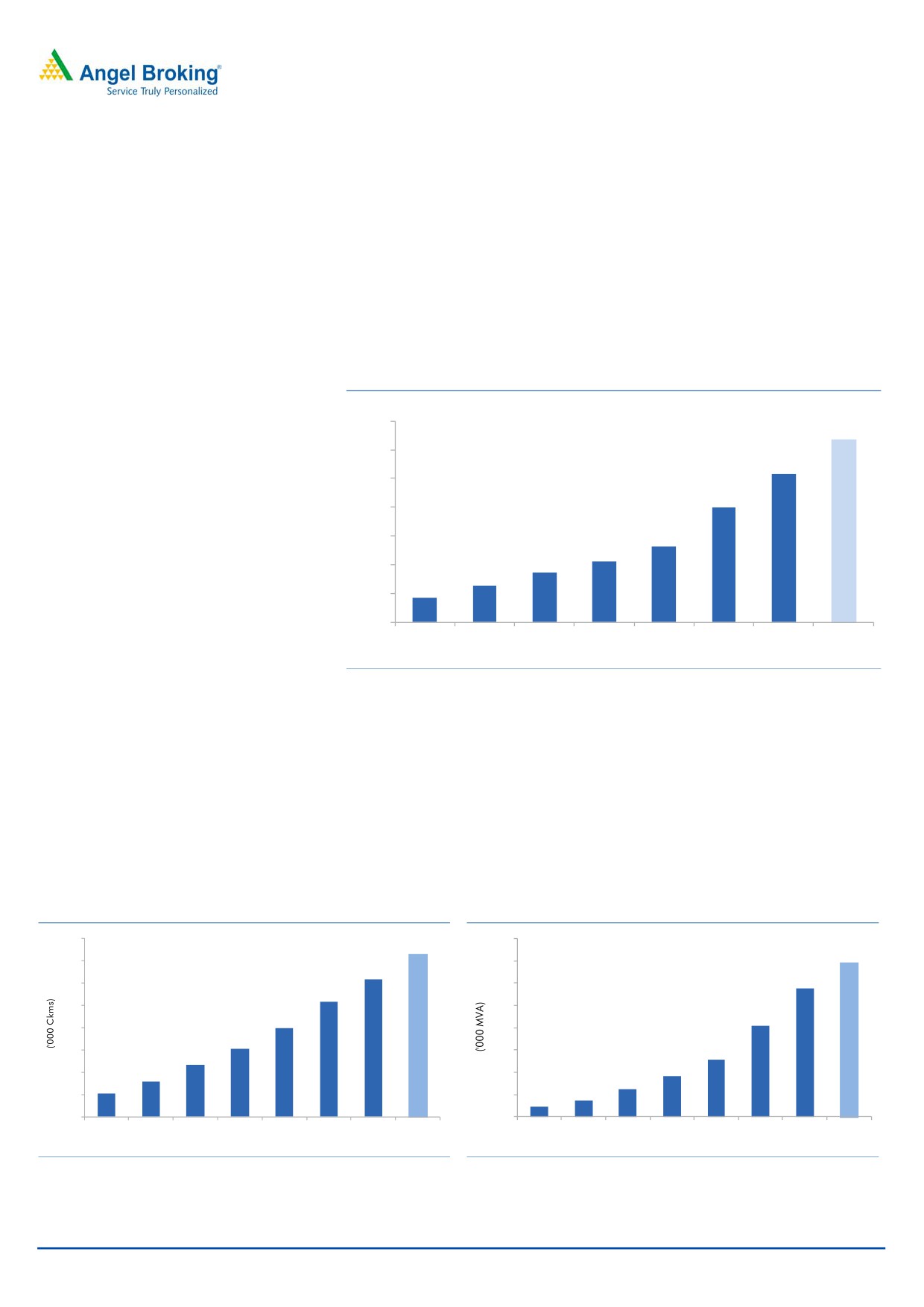

Huge investments lined up for augmenting power generation

and transmission capacities

Power generation capacity in the country has increased at a CAGR of 7.2% since

the end of the IX plan to ~259GW as of January 1, 2015 as against ~105GW at

the end of FY2001-02. Generation capacity is expected to reach ~318GW by the

end of the XII plan. A further capacity addition of ~110GW is currently planned

during the XIII plan.

Exhibit 1: Power generation capacity

(GW)

350

318

300

259

250

200

200

132

150

105

86

100

64

43

50

-

6th Plan 7th Plan 8th Plan 9th Plan

10th plan

11th plan Jan-15

12th plan

(Target)

Source: CEA, Planning Commission

Transmission capacity has also increased at a rapid clip, keeping pace with rise in

generation capacity. India added 1,55,715 circuit kilometers (ckm) of transmission

lines since the end of the IX plan to take the total length of transmission lines to

3,07,984ckm. Transformation capacity increased even faster, i.e. by 3,84,232MVA

and 8,300MW (HVDC sub-stations) to 5,60,975MVA and 13,500MW, respectively.

Transmission line length is expected to increase to 364,921ckm by the end of the

XII plan to expand the total transformation capacity to

6,69,801MVA and

22,500MW for HVDC sub-stations.

Exhibit 2: Transmission Lines (Length)

Exhibit 3: Transformation capacity

800

400

365

692

350

700

308

574

300

600

257

250

500

198

410

200

400

152

150

300

258

117

182

100

79

200

125

52

75

50

100

47

-

-

6th Plan 7th Plan 8th Plan 9th Plan

10th plan 11th plan Jan-15

12th plan

6th Plan 7th Plan 8th Plan 9th Plan 10th plan11th plan Jan-15 12th plan

(Target)

(Target)

Source: CEA, Planning Commission

Source: CEA, Planning Commission

March 16, 2015

2

Power Grid Corporation of India | Initiating Coverage

PGCIL is responsible for planning, implementation, operation and maintenance of

inter-state transmission system and operation of National & Regional Power Grids.

Inter-regional transmission capacity increased at a CAGR of 16% to 46,450MW as

on January 31, 2015 from 14,050MW on March 31, 2007. The inter-regional

transmission capacity is expected to reach 72,250MW by the end of the XII plan,

implying a CAGR of 24%.

Exhibit 4: Inter-regional transmission capacity

80

72

70

60

50

46

38

40

30

28

30

24

21

21

17

20

14

10

0

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

Jan-15

FY17

Source: Company, Angel Research

Total investment required during the XII plan was envisaged at `1,80,000cr to add

1,09,440ckm and transformation capacity of 2,70,000MVA. Under the XIII plan, a

further addition of 1,30,000ckm of transmission lines and 3,00,000MVA of

transformation capacity is foreseen. This will require an investment of more than

~`2,00,000cr. The power minister envisages an investment of `3,00,000cr over

the next five years to tackle the power shortages.

Majority of these investments would be towards inter-regional transmission

systems, which would directly benefit PGCIL. The company has planned a capital

outlay of `1,10,000cr during the XII plan. Further, we expect ~60-65% of XIII plan

investments in the transmission sector toward inter-state transmissions, implying a

capex outlay of ~`1,20,000-1,30,000cr by PGCIL.

Regulated ROE model assures steady earnings growth

PGCIL operates on a fixed ROE model

PGCIL receives its tariffs as per norms laid out by the CERC. CERC Regulations,

with an assured return of 15.5% on

2014 came into effect for a tariff block of five years starting from April 01, 2014.

projects.

The new regulations maintained the existing rate of return on equity (ROE) of

15.5%, with an additional 0.5% for timely completion of projects. The debt to

equity split for the transmission projects has also been maintained at 70:30.

The fixed ROE model implies that earnings growth is directly linked to the growth

in assets capitalised. The capitalisation rate in turn is directly linked to the rate of

capex and timely completion of projects. The company has outlined a strong capex

plan and has also demonstrated an excellent track record of execution and

management of transmission projects.

March 16, 2015

3

Power Grid Corporation of India | Initiating Coverage

We estimate PGCIL’s current projects under implementation to be upwards of

`100,000cr. The strong order pipeline and the amount of investments required in

the power transmission sector provide strong visibility for future earnings growth.

Strong capex plans to drive growth

After successfully achieving, its XI plan capex target of `55,000cr, PGCIL plans to

further invest `1,10,000cr during the XII plan, mainly towards development of

transmission infrastructure for implementation of various inter-state transmission

PGCIL has incurred a capex of

systems. The company plans to add

40,000ckm of transmission lines and

~`60,000cr till February 11, 2015 and

~1,00,000MVA of transformation capacity during the XII Plan. Of this, PGCIL has

remains well on track to achieve the XII

already commissioned about 23,479ckm (59%) of EHV transmission lines and

plan capex target

~95,861MVA (96%) of transformation capacity as on February 11, 2015.

PGCIL has incurred a capex of `20,037cr and `22,324cr in FY2013 and FY2014,

respectively. Capex till February 11, 2015 was ~`17,700cr, taking the total capex

under the XII plan, to ~`60,000cr. The company remains well on track to achieve

the XII plan capex target.

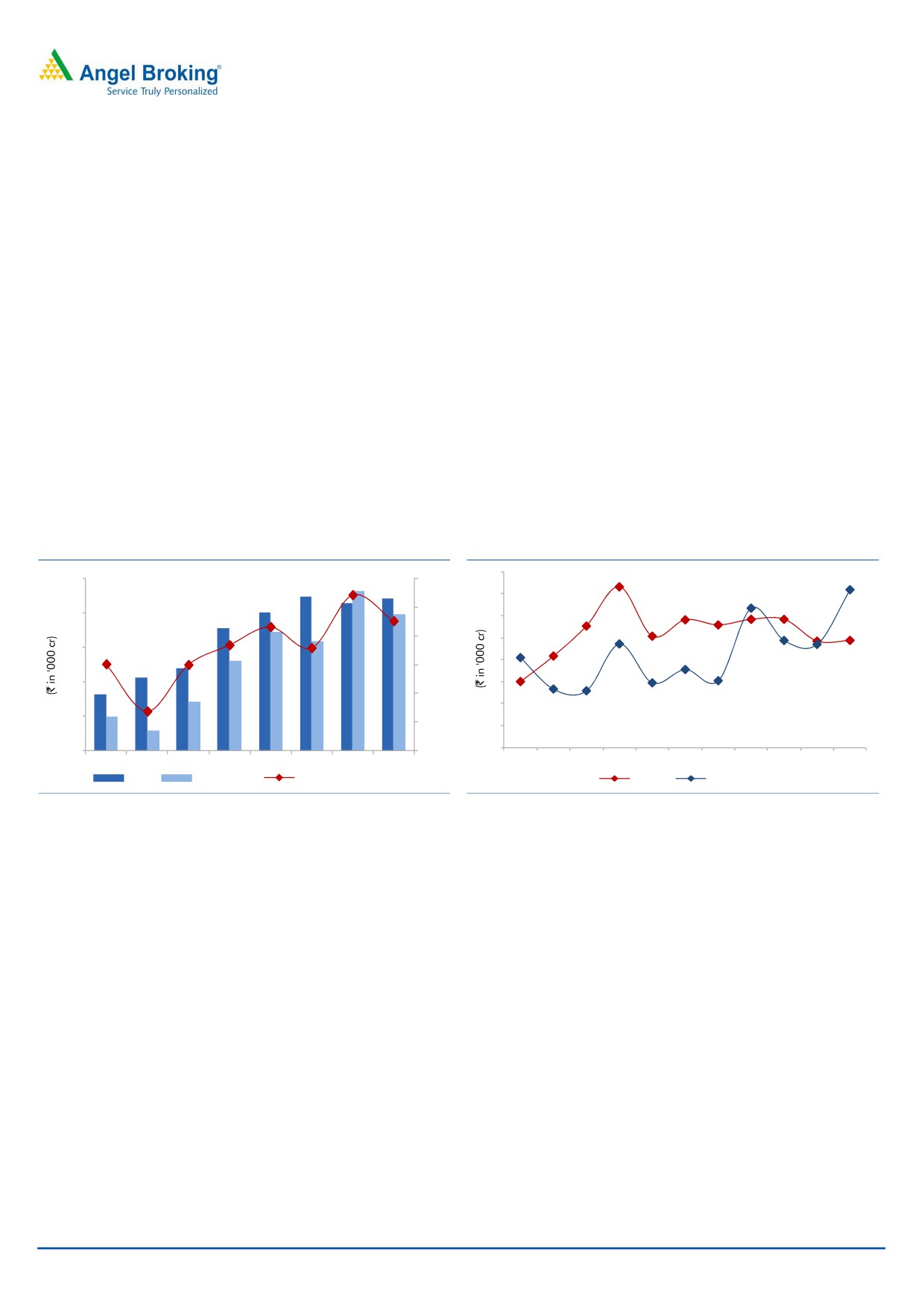

Exhibit 5: Capex / Capitalisation Trends

Exhibit 6: Recent quarterly Capex vs. Capitalisation

23

8

25

22

1.2

22

21

7

20

20

1.0

20

18

6

17

16

0.8

5

15

13

12

4

11

0.6

10

8

3

7

0.4

5

2

5

3

0.2

1

0

-

-

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

FY09

FY10

FY11

FY12

FY13

FY14

FY15E FY16E

Capex

Capitalisation

Capitlisation/Capex (%)

Capex

Capitalisation

Source: Company, Angel Research

Source: Company, Angel Research

The pace of capitalisation has also increased in recent years, with FY2015

expected to have a capitalisation to capex ratio of

108%. The cumulative

capitalisation rate for the company has been ~90% over the FY2007-14 period.

We expect capitalisation rate to remain healthy over FY2016 and FY2017 at 90%

and 85% respectively led by the strong order pipeline, efficient operations and

execution track record.

Regulated projects to remain the significant portion of capex mix

Tariff-based competitive bidding (TBCB) has been made mandatory since January

2011, for all transmission projects, barring a few cases such as the experimental

1,200kv HVDC line and projects which are required urgently or in a compressed

time schedule as decided by Central Government as a case to case basis. At the

end of FY2014, Power Grid had won 6 (40%) out of the 15 projects put up for

bidding via the TBCB route. Aggregate levelised tariff for these projects won

through competitive bidding was is ~`565cr. The company has won two more

projects in FY2015

-

1) Transmission system strengthening associated with

Vindhyachal-V and 2) Transmission System Associated with Gadarwara (Part A&B).

The aggregate levelised tariff for these projects is ~`758cr.

March 16, 2015

4

Power Grid Corporation of India | Initiating Coverage

PGCIL is expected to incur a total capex of ~`12,000cr to execute these projects.

Based on the debt to equity ratio of 70:30, the company will require a total equity

of ~`3,600cr over the life of these projects. The current equity invested in these

projects stands at ~`800cr. We expect this to increase to ~`1500cr (3% of total

equity) by FY2017. Thus, projects assigned to PGCIL on cost plus basis would

continue to dominate the project mix over the next few years.

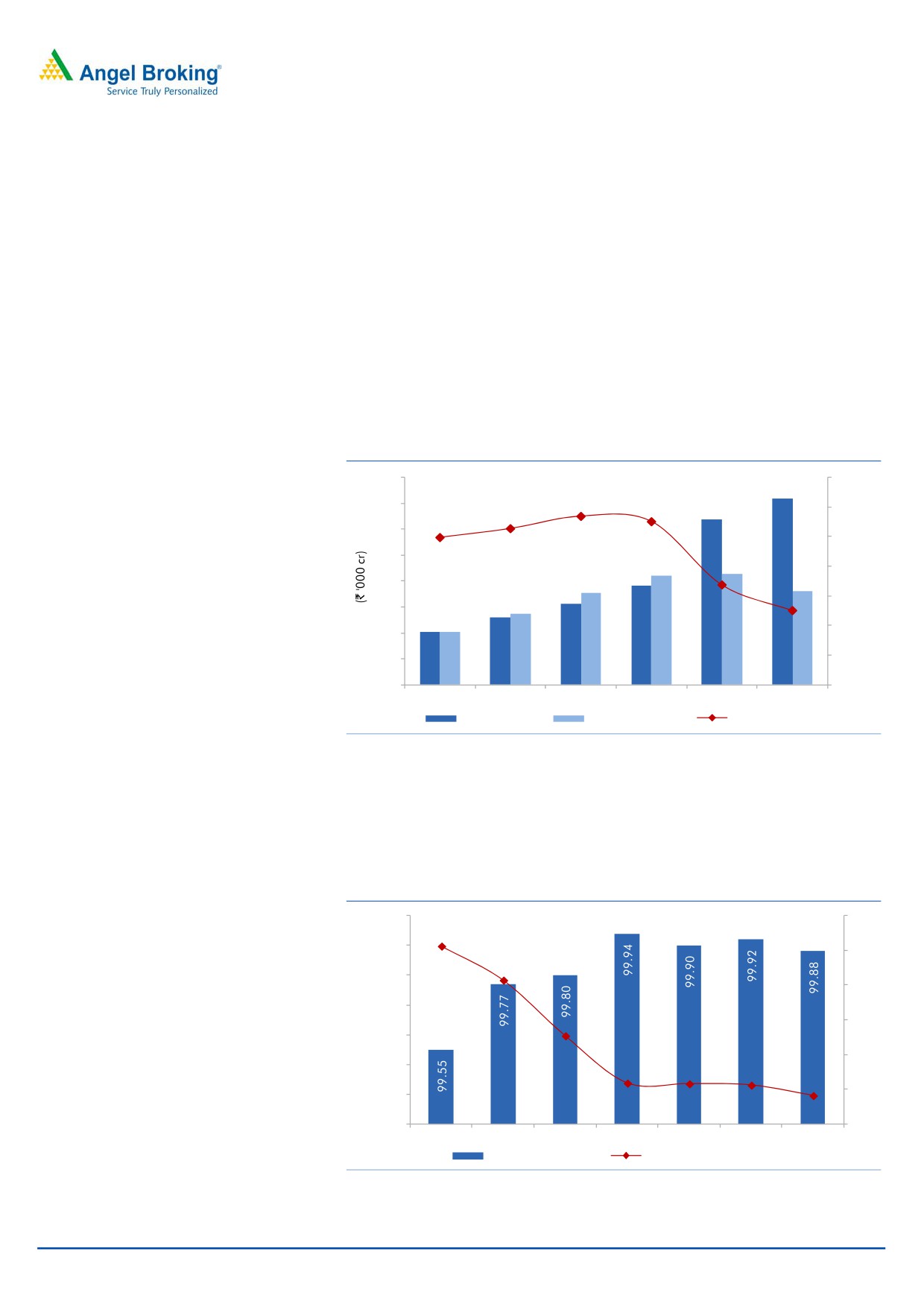

Efficient operations

PGCIL earns its tariff only on assets which are capitalised and not on the entire

capex it incurs. All the capital expenditure related to erection charges are shown as

capital work-in-progress (CWIP) till the date of capitalisation. A higher CWIP acts

as a drag on earnings and the company has over the last couple of years focused

on reducing CWIP, to increase the efficiency of operations.

Exhibit 7: CWIP & Construction Stores

40

140.0

36

35

113.7

32

120.0

110.1

105.4

99.4

30

100.0

25

21

21

80.0

19

67.4

20

18

18

16

14

50.1

60.0

15

13

10

10

40.0

10

20.0

5

-

-

FY10

FY11

FY12

FY13

FY14

FY15E

CWIP (installed)

Construction stores

Stores (% of CWIP)

Source: Company, Angel Research

The company has worked along with its suppliers to reduce the inventory of

materials, by ensuring payments are made only on actual erection at sites.

Material inventory as a % of CWIP has reduced to 50% at the end of 9MFY2015 as

against 114% in FY2012 and 110% in FY2013.

Exhibit 8: Availability and reliability

100.00

3.0

2.6

99.90

2.5

99.80

2.1

2.0

99.70

1.5

99.60

1.3

1.0

99.50

0.6

0.6

0.6

0.4

0.5

99.40

99.30

0.0

FY09

FY10

FY11

FY12

FY13

FY14

9M15

System Availability

Reliability (Trippings per line)

Source: Company, Angel Research

March 16, 2015

5

Power Grid Corporation of India | Initiating Coverage

PGCIL is one of the world’s largest transmission utility, managing over

928

transmission lines with a network length of 113,838ckm and 189 sub-stations with

a transformation capacity of 2,20,394MVA. Despite its size, the company has

consistently operated its transmission systems at high levels of efficiency, with a

system availability rate of >99% and trippings per line at <1%.

PGCIL has also pioneered the implementation of state-of-the-art smart grid

technologies in transmission, which makes existing infrastructure more robust,

reliable and efficient by using intelligent tools and technologies. Almost all the

attributes of a smart grid, viz. advance metering infrastructure, outage

management system, demand response, power quality management, etc. have

been successfully integrated at Smart Grid control centre at Puducherry.

Power Grid has also focused on indigenously developing smart products such as

smart meter, data concentrator unit, home energy management system, micro grid

controller, smart cap utilising solar energy, active filter etc. for varied applications.

March 16, 2015

6

Power Grid Corporation of India | Initiating Coverage

Outlook and Valuation

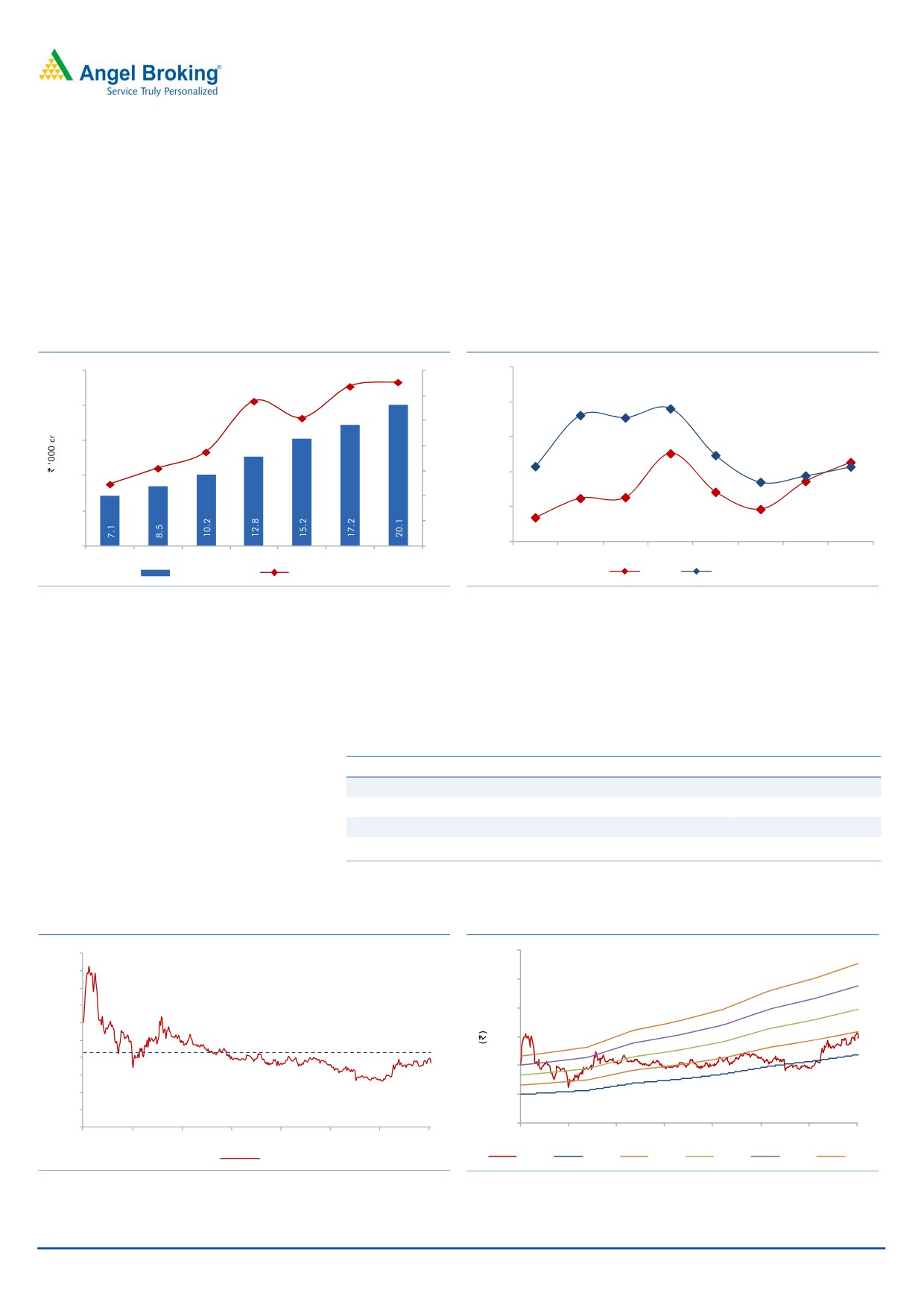

We like PGCIL for the high quality earnings and growth offered by the regulated

Going ahead, we expect Power Grid to

equity model, huge investments that are required in the transmission sector and

report a top-line CAGR of ~17% over

the execution track record of the company. We expect PGCIL to report a top-line

FY2014-17E to ~`7,277cr

CAGR of ~15% over FY2014-17E to ~`22,938cr led by the strong capex plans

and capitalisation rate. We expect the bottom-line to grow at a CAGR of 17% over

the same period.

Exhibit 9: Revenue & EBITDA margin

Exhibit 10: Return on Equity

25

86.5

87

22.0

86.4

85.8

86

19.6

20

85.1

20.0

19.2

19.1

85

83.8

18.0

15

16.9

83.1

84

16.3

16.3

15.8

82.5

83

16.0

17.0

15.4

10

16.5

82

15.4

14.0

14.8

5

14.5

14.5

81

13.8

13.4

-

80

12.0

FY10

FY11

FY12

FY13

FY14

FY15E

FY16E

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

Revenue (` cr)

EBITDA Margin (%)

ROE

Regulated ROE

Source: Company, Angel Research

Source: Company, Angel Research

At the current market price of `147, the stock trades at a P/B of 1.8x and 1.7x its

FY2016E and FY2017E BV of `79.7 and `88.7, respectively. We initiate coverage

on the stock with a Buy recommendation and target price of `170, based on

~1.9x FY2017E book value, implying a 16% upside from current levels.

Exhibit 11: Valuation (FY2017E)

(` cr)

Equity

46,398

P/B (x)

1.9

Equity Value

89,005

Target price (`)

170

Source: Company, Angel Research

Exhibit 12: Average P/B

Exhibit 13: P/B Band

5.00

300

4.50

250

4.00

3.50

200

3.00

2.50

150

2.00

100

1.50

1.00

50

0.50

-

0

Oct-07

Oct-08

Nov-09

Dec-10

Dec-11

Jan-13

Feb-14

Mar-15

Oct-07

Oct-08

Nov-09

Dec-10

Dec-11

Jan-13

Feb-14

Mar-15

P/B

Price

1.5X

2.0X

2.5X

3.0X

3.5X

Source: Bloombert

Source: Bloomberg

March 16, 2015

7

Power Grid Corporation of India | Initiating Coverage

Risks to our target price

We are currently expecting an outlay of ~`1,20,000-1,30,000cr during the

XIII plan. A lower than expected capex outlay would be a negative for the

stock.

Increase in the rate of projects allocated through the tariff-based competitive

bidding (TBCB). Tariff bids under TBCB require an accurate assessment of

future costs, project execution timelines and operational complexities. The bids

under TBCB could end up being aggressive, posing risks to the financial

viability of these projects or affecting their execution.

We expect capitalisation to remain healthy at 90% and 85% in FY2016 and

FY2017, respectively. A higher than expected rate of capitalisation would be

positive for the stock.

March 16, 2015

8

Power Grid Corporation of India | Initiating Coverage

Company Background

Power Grid Corporation of India Ltd is the Central Transmission Utility (CTU) of the

country and a 'Navratna' company operating under the Ministry of Power. The

company is engaged in the power transmission business with the responsibility for

planning, implementation, operation and maintenance of inter-state

transmission system and operation of National & Regional Power Grids. As of

January 31, 2015, the company owns and operates a transmission network of

about 1,13,688ckm of transmission lines and 189 EHVAC & HVDC substations

with transformation capacity of about 2,20,394MVA. The company continues to

wheel ~50% of total power generated in the country through its transmission

network with a consistently high availability of over 99%.

Exhibit 13: Key Statistics (as on January 31, 2015)

Transmission

Consultancy

Telecom

1,13,688ckm transmission lines

Transmission related consultancy to

Owns and operates ~29,641kms of

189 sub-stations

more than 150 domestic clients

telecom network

>99% system availability

Global foot prints in

18 countries

Points of presence in ~317 locations

2,20,394MVA transformation capacity

catering to more than 20 clients

Intra-city network in

68 cities across

~45850MW inter-regional capacity

India

Source: Company

March 16, 2015

9

Power Grid Corporation of India | Initiating Coverage

Profit & Loss Statement (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Transmission Charges

11,754

14,046

16,512

19,390

22,212

Telecom & Consultancy

547

903

636

660

686

Net Sales

12,300

14,949

17,148

20,050

22,898

Other operating income

457

281

30

35

40

Total operating income

12,758

15,230

17,177

20,085

22,938

% chg

25.5

19.4

12.8

16.9

14.2

Transmission Expenses

368

456

561

659

755

Employee Expenses

886

942

1,016

1,168

1,311

Other Mfg costs

558

849

755

863

962

Provisions

3

22

10

15

17

EBITDA

10,943

12,961

14,835

17,380

19,892

% chg

28.6

18.4

14.5

17.2

14.5

(% of Net Sales)

85.8

85.1

86.4

86.5

86.7

Depreciation & Amortisation

3,352

3,996

5,034

5,906

6,646

EBIT

7,591

8,965

9,800

11,473

13,246

% chg

27.8

18.1

9.3

17.1

15.4

(% of Net Sales)

59.5

58.9

57.1

57.1

57.7

Interest & other Charges

2,535

3,168

3,965

4,357

4,744

Other Income

571

491

533

585

645

(% of PBT)

10.1

7.8

8.4

7.6

7.1

Share in profit of Associates

-

-

-

-

-

Recurring PBT

5,627

6,289

6,368

7,701

9,147

% chg

21.9

11.8

1.3

20.9

18.8

Extraordinary Inc/(Expense)

18

(25)

(95)

-

-

PBT (reported)

5,645

6,264

6,273

7,701

9,147

Tax

1,410

1,766

1,282

1,574

1,870

(% of PBT)

25.0

28.2

20.4

20.4

20.4

PAT (reported)

4,235

4,497

4,991

6,127

7,277

ADJ. PAT

4,216

4,523

5,086

6,127

7,277

% chg

28.7

7.3

12.4

20.5

18.8

(% of Net Sales)

33.0

29.7

29.6

30.5

31.7

Basic EPS (`)

9.1

9.4

9.5

11.7

13.9

Adj. fully Diluted EPS (`)

9.1

9.4

9.7

11.7

13.9

% chg

28.7

3.4

3.3

20.5

18.8

March 16, 2015

10

Power Grid Corporation of India | Initiating Coverage

Balance Sheet (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

SOURCES OF FUNDS

Equity Share Capital

4,630

5,232

5,232

5,232

5,232

Reserves & Surplus

21,610

29,228

32,467

36,443

41,166

Shareholders Funds

26,239

34,460

37,699

41,675

46,398

Share Warrants

-

-

-

-

-

Total Loans

68,188

83,170

95,221

1,05,304

1,15,562

Deferred Tax Liability

1,959

2,443

2,432

2,421

2,411

Other Long term liabilities

4,708

5,855

5,998

6,431

6,527

Long term provisions

443

524

591

692

790

Total Liabilities

1,01,537

1,26,452

1,41,941

1,56,522

1,71,687

APPLICATION OF FUNDS

Gross Block

80,600

96,504

1,19,661

1,39,506

1,58,673

Less: Acc. Depreciation

19,199

23,350

28,384

34,290

40,937

Net Block

61,401

73,154

91,277

1,05,215

1,17,736

Capital Work-in-Progress

19,115

31,851

31,374

33,040

35,460

Construction Stores

21,038

21,479

20,218

20,756

21,719

Investments

964

814

900

900

900

Non-current Loans & Adv.

2,351

3,190

3,435

4,017

4,588

Current Assets

6,265

9,100

9,505

9,857

10,995

Cash

1,662

4,418

4,205

3,606

3,755

Loans & Advances

429

472

532

623

711

Other

4,175

4,211

4,768

5,629

6,529

Current liabilities

9,597

13,138

14,767

17,263

19,711

Net Current Assets

(3,331)

(4,037)

(5,262)

(7,406)

(8,716)

Mis. Exp. not written off

-

-

-

-

-

Total Assets

1,01,537

1,26,452

1,41,941

1,56,522

1,71,687

March 16, 2015

11

Power Grid Corporation of India | Initiating Coverage

Cashflow Statement (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015E FY2016E FY2017E

Profit before tax

5,645

6,264

6,273

7,701

9,147

Depreciation

3,380

4,011

5,034

5,906

6,646

Change in Working Capital

1,241

3,333

1,002

1,941

1,848

Others

2,091

2,809

4,175

4,483

4,539

Direct taxes paid

(1,072)

(1,157)

(1,282)

(1,574)

(1,870)

Cash Flow from Operations

11,284

15,259

15,202

18,457

20,310

(Inc.)/ Dec. in Fixed Assets

(22,389)

(26,735)

(21,418)

(22,050)

(22,550)

(Inc.)/ Dec. in Investments

137.0

148.8

(85.8)

-

-

Others

303

209

(246)

(581)

(571)

Cash Flow from Investing

(21,948)

(26,378)

(21,749)

(22,631)

(23,121)

Issue of Equity

0

5,297

0

0

0

Inc./(Dec.) in loans

13,795

12,720

12,051

10,083

10,258

Dividend Paid (Incl. Tax)

(1,569)

(1,391)

(1,752)

(2,150)

(2,554)

Others

(2,236)

(2,752)

(3,965)

(4,357)

(4,744)

Cash Flow from Financing

9,990

13,874

6,334

3,575

2,960

Inc./(Dec.) in Cash

(675)

2,756

(213)

(599)

150

Opening Cash balances

2,337

1,662

4,418

4,205

3,606

Closing Cash balances

1,662

4,418

4,205

3,606

3,755

March 16, 2015

12

Power Grid Corporation of India | Initiating Coverage

Key Ratios

Y/E March

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

16.0

15.6

15.4

12.5

10.5

P/CEPS

9.0

8.3

7.6

6.4

5.5

P/BV

2.6

2.2

2.0

1.8

1.7

Dividend yield (%)

1.9

1.8

2.0

2.4

2.8

EV/Sales

10.5

10.2

9.7

8.9

8.2

EV/EBITDA

12.3

12.0

11.3

10.2

9.5

EV/Total Assets

1.3

1.2

1.2

1.1

1.1

Per Share Data (`)

Adjusted EPS (Basic)

9.1

9.4

9.7

11.7

13.9

Adjusted EPS (fully diluted)

9.1

9.4

9.7

11.7

13.9

Cash EPS

16.3

17.7

19.3

23.0

26.6

DPS

2.8

2.6

2.9

3.5

4.2

Book Value

56.7

65.9

72.1

79.7

88.7

Dupont Analysis

EBIT margin

59.5

58.9

57.1

57.1

57.7

Tax retention ratio (%)

75.0

71.8

79.6

79.6

79.6

Asset turnover (x)

0.1

0.1

0.1

0.1

0.1

ROIC (Post-tax)

6.7

6.1

6.3

6.6

6.9

Cost of Debt (Post Tax)

3.1

3.0

3.5

3.5

3.4

Leverage (x)

2.4

2.4

2.3

2.4

2.4

Operating RoE

15.1

13.6

12.9

14.2

15.3

Returns (%)

RoCE (Pre-tax)

8.7

8.3

7.7

8.1

8.4

Angel RoIC (Pre-tax)

15.6

15.4

13.9

13.4

13.6

RoE

17.0

14.9

14.1

15.4

16.5

Turnover ratios (x)

Asset Turnover (Gross Block)

0.2

0.2

0.2

0.2

0.2

Inventory (days)

14

15

16

17

18

Receivables (days)

42

36

36

36

37

Payables (days)

44

45

51

47

47

WC cycle (ex-cash) (days)

(116)

(161)

(190)

(186)

(187)

Solvency ratios (x)

Net debt to equity

2.5

2.3

2.4

2.4

2.4

Net debt to EBITDA

6.1

6.1

6.1

5.8

5.6

Interest Coverage

3.0

2.8

2.5

2.6

2.8

March 16, 2015

13

Power Grid Corporation of India | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel has received in-principal approval

from SEBI for registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its associates

including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company covered by

Analyst. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of securities of

the company covered by Analyst during the past twelve months. Angel/analyst has not served as an officer, director or employee of

company covered by Analyst and has not been engaged in market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Power Grid Corporation of India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

Yes

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15

March 16, 2015

14