FPO Note | Oil & Gas

January 31, 2013

OIL INDIA

SUBSCRIBE

Issue Open: February 01, 2013

Attractively priced

Issue Close: February 01, 2013

Oil India is a government-owned company that explores, develops and produces

Issue Details

oil and gas. It is India’s second-largest E&P company in terms of production and

Face Value: `10

reserves. Currently, Oil India has 2P reserves of 941mnboe, indicating a reserve

life of 22 years.

Present Eq. Paid-up Capital: `240cr

Offer Size: 6.01cr Shares

One of the lowest cost producers: During FY2012, Oil India’s cost of oil

production stood at US$8.3/bbl, which is one of the lowest in our view. Its cost of

Post Eq. Paid-up Capital: `240cr

natural gas production stood at US$1.4/mmbtu. Due to lower cost of production,

Issue size (amount):* `3,065cr

Oil India enjoys robust operating margins (~30%) despite lower net realizations,

Floor Price: `510

on the back of subsidy sharing with Oil Marketing Companies (OMCs).

Post-issue implied mkt cap: `32,413cr

Rise in fuel prices could pave way for re-rating: Upstream oil PSU companies

Promoters holding Pre-Issue: 78.4%

have been sharing under-recoveries by the downstream companies who sell

Promoters holding Post-Issue: 68.4%

diesel, kerosene and LPG cylinders at subsidized rates. As there is no concrete

formula or methodology to determine the annual subsidy of any of these

companies, investors have remained concerned over the lack of visibility on

profitability of downstream and upstream companies. During FY2012, subsidy

Post Issue Shareholding Pattern

shared by Oil India rose by 123.3% yoy to `7,352cr. However, given the rising

Promoters Group

68.4

under-recoveries, government has hinted at diesel price de-regulation (diesel

MF/Banks/Indian

contributes 60% to total under-recoveries). Hence, going forward, diesel price de-

FIs/FIIs/Public &

regulation is likely to result in lower subsidy burden on upstream companies

Others

31.6

including Oil India and thus higher realizations. Oil India’s Management also

expects the subsidy amount to decline significantly during FY2014.

Strong balance sheet paves way for acquisition of energy assets: As on

September 30, 2012, Oil India had net cash of `252/share on the balance sheet.

Considering the operating cash flow and the company’s capex requirements over

the coming few years, we believe the company will maintain high cash balance,

which could pave way for acquisition of oil and gas assets. The company aims to

acquire shale gas assets in the US.

Outlook and valuation: Historically, Oil India stock has traded at a lower EV/1P

Reserves compared to its global peers on account of lower realizations on crude

oil (subsidy sharing with downstream companies’ results in lower net realizations).

However, we believe that the government’s initiatives to raise (de-regulate) the

price of diesel gradually should lead to lower subsidy sharing by upstream

companies from FY2014 and hence, result in higher realizations. Consequently,

we expect Oil India’s valuation gap to narrow gradually with global peers. We

derive a SOTP-based target price of `600 and recommend investors with

Bhavesh Chauhan

long-term horizon to Subscribe to the shares of Oil India.

Tel: 022- 39357600 Ext: 6821

Vinay Rachh

Tel: 022- 39357600 Ext: 6841

Please refer to important disclosures at the end of this report

1

Oil India | FPO Note

Company background

Oil India is a Navratna company that is into exploration, development and

production of oil and gas. It is India’s second-largest E&P company in terms of

production and reserves. Approximately 95% of Oil India’s production comes from

its Upper Assam basin. The company holds several NELP blocks as an operator

and some with joint ventures. Currently, Oil India has 2P reserves of 941mnboe,

indicating a reserve life of 22 years.

Exhibit 1: Reserves break-up

Exhibit 2: Reserve Replacement ratio

2.5

1000

878

900

2.0

2.0

800

2.0

1.7

1.7

700

1.6

600

1.4

600

1.5

486

1.2

500

400

341

1.0

274

300

199

200

0.5

100

0

0.0

1P

2P

3P

FY2006

FY2007

FY2008

FY2009

FY2010

FY2011

FY2012

Oil Gas

Source: Company, Angel Research

Source: Company, Angel Research

Issue details

The issue comprises an offer for sale of 6.01cr equity shares of face value `10

each. There is no fresh issue of equity. Oil India has fixed the floor price of the

issue at `510 per share.

Exhibit 3: Shareholding Pattern

Pre-Issue

Post-Issue

Particulars

No. of shares

(%)

No. of shares

(%)

Promoter and promoter group

47,14,98,900

78.4

41,11,76,993

68.4

Total public holding

12,96,37,055

21.6

18,99,58,962

31.6

Total

60,11,35,955

100

60,11,35,955

100

Source: Source: RHP, Angel Research

January 31, 2013

2

Oil India | FPO Note

Investment arguments

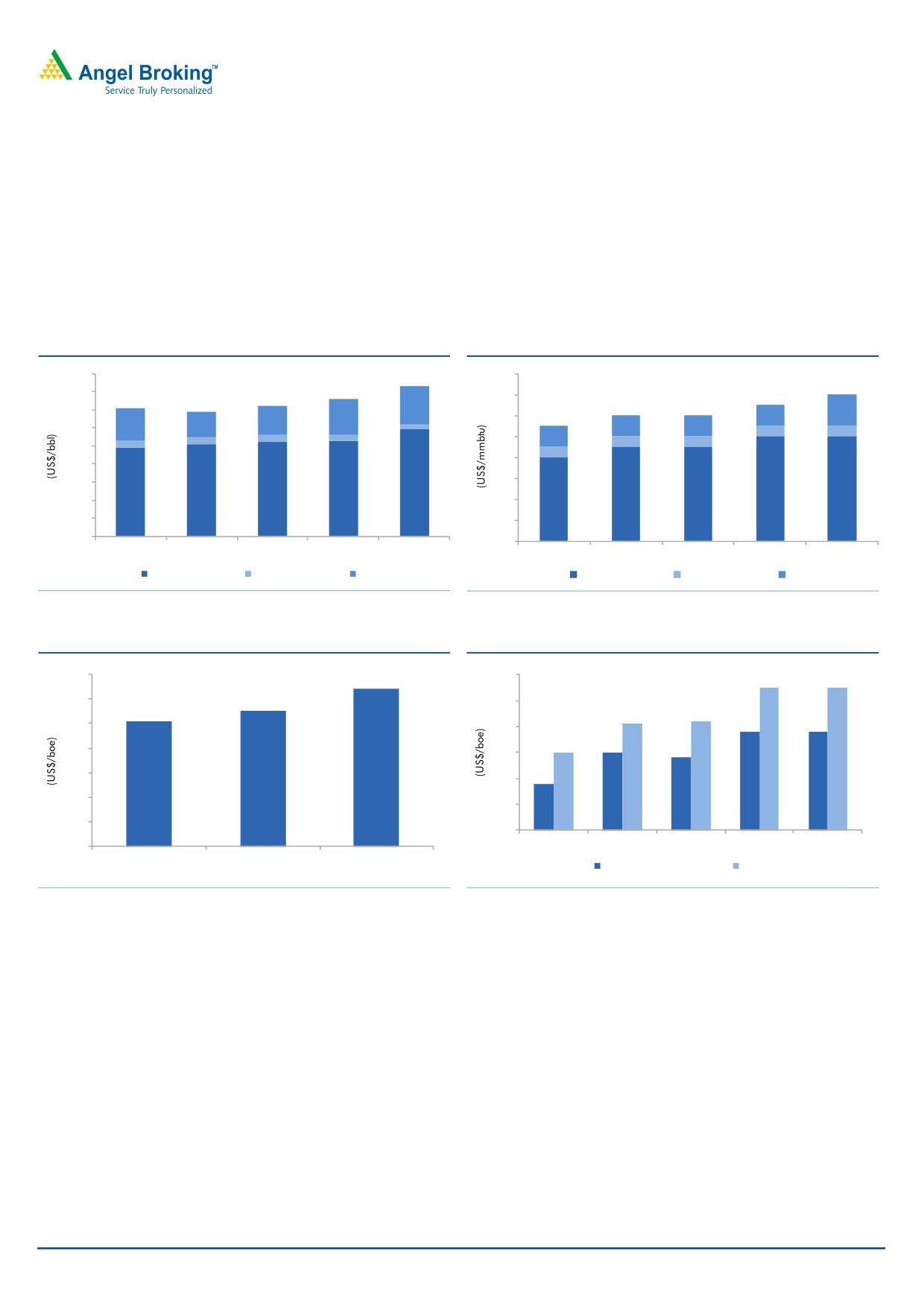

One of the lowest cost producers

During FY2012, Oil India’s cost of oil production stood at US$8.3/bbl, which is

one of the lowest in our view. Its cost of natural gas production stood at

US$1.4/mmbtu. Due to lower cost of production, Oil India enjoys robust operating

margins (~30%) despite lower net realizations, on the back of subsidy sharing with

Oil Marketing Companies (OMCs).

Exhibit 4: Crude oil production cost trend

Exhibit 5: Natural gas production cost trend

9.0

1.6

8.0

1.4

7.0

1.2

6.0

1.0

5.0

0.8

4.0

0.6

3.0

2.0

0.4

1.0

0.2

0.0

0.0

FY2008

FY2009

FY2010

FY2011

FY2012

FY2008

FY2009

FY2010

FY2011

FY2012

Raising Cost

Depreciation

Depletion

Raising Cost

Depreciation

Depletion

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 6: Lowest cost operator (FY2012)

Exhibit 7: Finding and development costs trend

7.0

6.4

6.0

5.5

5.5

6.0

5.5

5.0

5.1

4.1

4.2

3.8

3.8

5.0

4.0

3.0

3.0

4.0

2.8

3.0

3.0

1.8

2.0

2.0

1.0

1.0

0.0

0.0

FY2008

FY2009

FY2010

FY2011

FY2012

Lifting/Prod'n Costs

Finding & Dev. costs

Opex

Finding Costs

F&D Costs

Source: Company, Angel Research

Source: Company, Angel Research

Rise in fuel prices could pave way for re-rating

Upstream oil PSU companies have been sharing under-recoveries by the

downstream companies who sell diesel, kerosene and LPG cylinders at subsidized

rates. As there is no concrete formula or methodology to determine the annual

subsidy of any of these companies, investors have remained concerned over the

lack of visibility on profitability of downstream and upstream companies. During

FY2012, subsidy shared by Oil India rose by 123.3% yoy to `7,352cr. However,

given the rising under-recoveries, government has hinted at diesel price

de-regulation (diesel contributes 60% to total under-recoveries). Hence, going

forward, diesel price de-regulation is likely to result in lower subsidy burden on

upstream companies including Oil India and thus higher realizations. Oil India’s

Management also expects the subsidy amount to decline significantly

during FY2014.

January 31, 2013

3

Oil India | FPO Note

Exhibit 8: Subsidy sharing by upstream companies (` cr)

FY2008

FY2009

FY2010

FY2011

FY2012

ONGC

22,001

28,226

11,550

24,786

44,500

Oil India

2,305

3,023

1,549

3,293

7,352

GAIL

1,314

1,781

1,327

2,111

3,183

Source: Company, Angel Research

Strong balance sheet paves way for acquisition of energy assets

As on September 30, 2012, Oil India had net cash of `252/share on the balance

sheet. Considering the operating cash flow and the company’s capex requirements

over the coming few years, we believe the company will maintain high cash

balance, which could pave way for acquisition of oil and gas assets. The company

aims to acquire shale gas assets in the US.

Oil India vs ONGC

ONGC is the largest explorer and crude oil producer in India with reserves which

are more than 10x Oil India’s reserves. ONGC shares subsidy-burden similar to

Oil India. Hence, we compare Oil India vis-à-vis ONGC on several parameters.

We find that Oil India scores over ONGC on most of these parameters. Even on

valuations front, Oil India is currently trading at 3.5x EV/2P Reserves compared to

ONGC which is trading at 4.7x.

January 31, 2013

4

Oil India | FPO Note

Exhibit 9: ONGC vs Oil India - Reserve Life (Stand.)

Exhibit 10: ONGC vs Oil India - Realizations (Stand.)

70

35

31

58.1

59

60

56

56

56

55

30

27

60

52.9

53.8

49

25

22

21

50

40

20

16

15

30

10

10

20

5

10

0

0

1P

2P

3P

FY2008

FY2009

FY2010

FY2011

FY2012

OIL

ONGC

OIL INDIA ONGC

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 11: ONGC vs Oil India - Oil production (mmt)

Exhibit 12: ONGC vs Oil India - Gas production (bcm)

28.2

2.7

35.0

4.5

2.6

4.0

28.0

34.5

2.6

3.5

27.8

2.5

34.0

3.0

27.6

2.5

2.5

27.4

2.4

33.5

2.0

2.4

27.2

33.0

1.5

2.3

27.0

1.0

2.3

32.5

26.8

0.5

2.2

32.0

0.0

26.6

2.2

FY2008

FY2009

FY2010

FY2011

FY2012

FY2008

FY2009

FY2010

FY2011

FY2012

ONGC

Oil India -(RHS)

ONGC

Oil India -(RHS)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 13: ONGC vs Oil India - ROE

Exhibit 14: ONGC vs Oil India EV/2P reserves valuation

30

5.0

25

4.7

23

23

23

4.8

25

21

21

20

20

4.6

20

4.4

15

4.2

4.0

10

3.8

5

3.5

3.6

0

3.4

FY2009

FY2010

FY2011

FY2012

3.2

3.0

ONGC

OIL

ONGC

Oil India

Source: Company, Angel Research

Source: Company, Angel Research

January 31, 2013

5

Oil India | FPO Note

Outlook and valuation

Historically, Oil India stock has traded at a lower EV/1P Reserves compared to its

global peers on account of lower realizations on crude oil (subsidy sharing with

downstream companies’ results in lower net realizations). However, we believe that

the government’s initiatives to raise (de-regulate) the price of diesel gradually

should lead to lower subsidy sharing by upstream companies from FY2014 and

hence, result in higher realizations. Consequently, we expect Oil India’s valuation

gap to narrow gradually with global peers. We derive a SOTP-based target price

of `600 and recommend investors with long-term horizon to Subscribe to the

shares of Oil India.

Exhibit 15: SOTP valuation

mm/bbl

US$/boe

US$ mn

`/share

2P oil reserves

600

5.2

3,120

285

2P gas reserves

341

2.0

682

62

Net cash

252

Target price

600

Source: Company, Angel Research

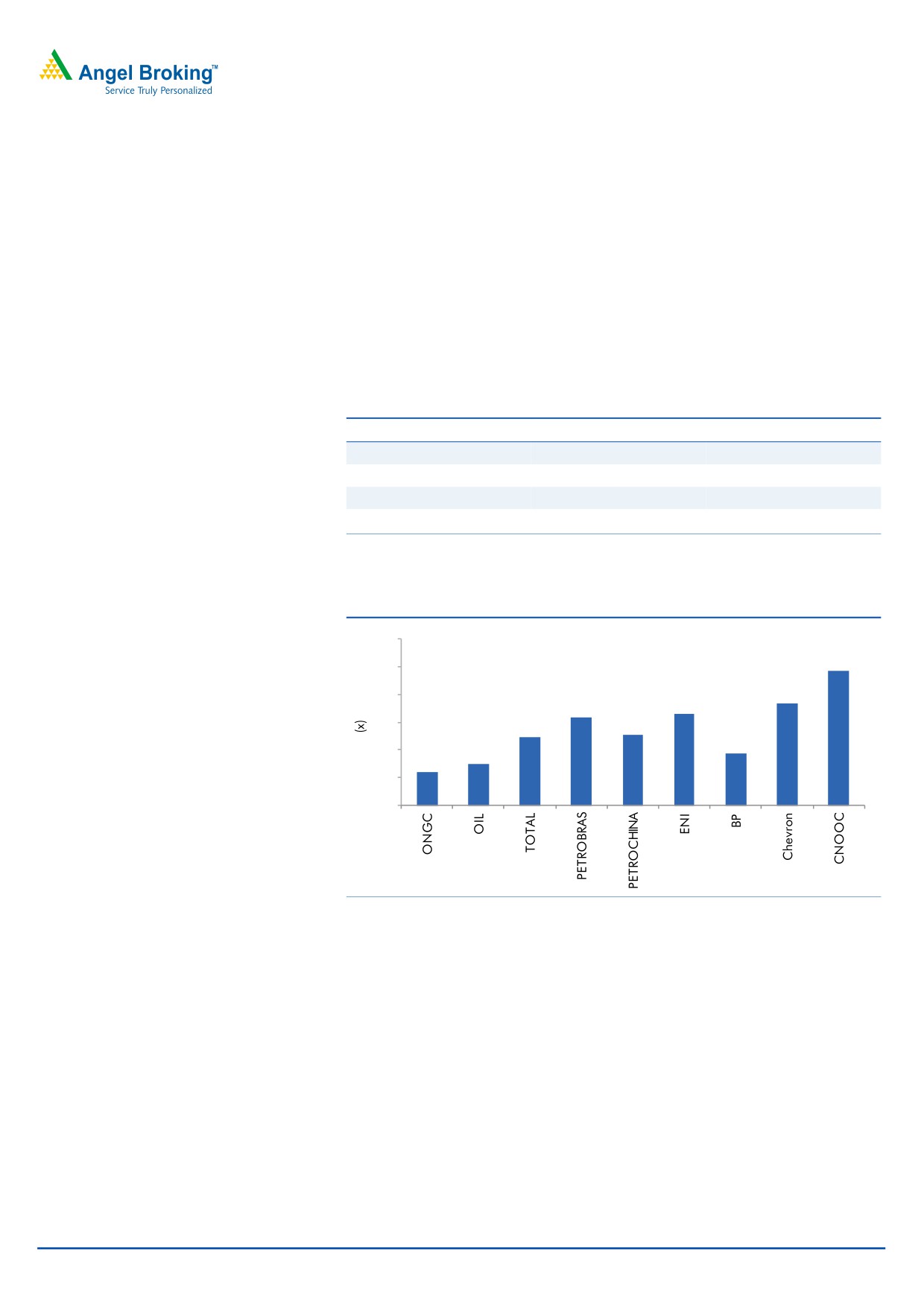

Exhibit 16: EV/1P Reserves matrix

30

24.3

25

18.3

20

16.5

15.8

15

12.2

12.6

9.4

10

7.4

6.1

5

-

Source: Angel Research, Bloomberg

Key concerns

High dependence on one region

Currently, 95% of Oil India’s production comes from its Upper Assam basin. Any

adverse event or security concerns in this region can potentially affect Oil India’s

operations.

Risk of higher subsidy sharing

Over the past five years, Oil India’s subsidy sharing has remained volatile as there

is no concrete formula for calculating subsidy. Although we anticipate government

to gradually de-regulate diesel prices, the risk of higher subsidy sharing by Oil

India remains in the near-term.

January 31, 2013

6

Oil India | FPO Note

Profit & Loss Statement (Standalone)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012

Net Sales

7,241

9,454

11,614

17,215

% chg

-

30.6

22.8

48.2

Total Expenditure

4,635

6,290

7,346

12,518

EBIDTA

3,564

4,119

5,142

6,142

(%of Net Sales)

49.2

43.6

44.3

35.7

Other Income

957

954

874

1,445

Depreciation & Amortization

168

220

820

1,009

Interest

9

4

13

9

PBT

3,387

3,895

4,309

5,124

(% of Net Sales)

46.8

41.2

37.1

29.8

Extraordinary Expense/(Inc.)

-

-

-

-

Tax

1,225

1,285

1,425

1,655

(% of PBT)

36.2

33.0

33.1

32.3

PAT

2,162

2,610

2,884

3,469

% chg

-

20.8

10.5

20.3

Ad. PAT

2,162

2,610

2,884

3,469

% chg

-

20.8

10.5

20.3

Balance Sheet (Standalone)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012

SOURCES OF FUNDS

Equity Share Capital

214

240

240

240

Reserves & Surplus

9,118

13,525

15,357

17,499

Shareholders’ Funds

9,332

13,766

15,598

17,740

Share warrants

-

-

-

-

Minority Interest

-

-

-

-

Total Loans

56

38

1,027

19

Other Liabilities

-

-

325

404

Deferred Tax Liability (net)

900

1,021

1,149

1,077

Total Liabilities

10,289

14,824

18,099

19,239

APPLICATION OF FUNDS

Gross Block

2,972

3,211

3,320

3,534

Less: Acc. Depreciation

1,838

2,136

2,331

2,476

Net Block

1,134

1,075

990

1,058

Capital Work-in-Progress

3,402

3,871

4,477

4,567

Goodwill

-

-

-

-

Investments

489

859

885

2,632

Current Assets

8,413

12,307

14,553

14,166

Current liabilities

3,149

3,306

3,184

3,509

Net Current Assets

5,264

9,000

11,369

10,657

Other assets

-

-

379

325

Misc Expenditure

-

18

-

-

Total Assets

10,289

14,824

18,099

19,239

January 31, 2013

7

Oil India | FPO Note

Cash Flow Statement (Standalone)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012

Profit before tax

3,387

3,895

4,313

5,102

Depreciation

173

222

178

151

(Inc)/Dec in Working Capital

386

(500)

402

313

Direct taxes paid

(517)

(1,248)

(1,382)

(1,897)

Others

(259)

(405)

(458)

(571)

Cash Flow from Operations

3,170

1,964

3,052

3,097

(Inc.)/Dec. in Fixed Assets

-

-

(952)

(860)

Free Cash Flow

3,170

1,964

2,100

2,237

(Inc)/Dec in Investments

-

(371)

(31)

(1,724)

Others

(124)

210

(120)

1,504

Issue of Equity

-

2,777

-

-

Inc./(Dec.) in loans

(118)

(16)

989

(1,004)

Dividend Paid (Incl.Tax)

(642)

(765)

(818)

(1,310)

Cash Flow from Financing

(884)

1,836

21

(2,534)

Inc./(Dec.) in Cash

1,789

2,473

3,225

(832)

Opening Cash balances

4,281

6,070

8,543

11,767

Closing Cash balances

6,070

8,543

11,767

10,935

Key Ratios

Y/E March

FY2009

FY2010

FY2011

FY2012

Per Share Data (`)

EPS (diluted)

50.5

54.3

60.0

72.1

Book Value

218.0

286.2

324.3

368.9

Ratios

EBITDA margin (%)

49.2

43.6

44.3

35.7

Adj. Net margin (%)

29.9

27.6

24.8

20.2

Net Debt/Equity (x)

(0.6)

(0.6)

(0.7)

(0.6)

Returns (%)

RoE

230

23.0

20.0

21.0

RoCE

36.2

33.7

28.1

29.2

RoIC

52.4

61.5

69.5

70.7

Valuation Ratio (x)

P/E

10.0

10.1

9.2

7.0

P/BV

2.4

1.8

1.6

1.4

EV/Sales

2.2

1.7

1.2

0.7

EV/EBITDA

4.4

3.8

2.6

1.9

January 31, 2013

8

Oil India | FPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

January 31, 2013

9

Oil India | FPO Note

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Bhavesh Chauhan

Sr. Analyst (Metals & Mining)

Viral Shah

Sr. Analyst (Infrastructure)

Sharan Lillaney

Analyst (Mid-cap)

V Srinivasan

Analyst (Cement, FMCG)

Yaresh Kothari

Analyst (Automobile)

Ankita Somani

Analyst (IT, Telecom)

Sourabh Taparia

Analyst (Banking)

Bhupali Gursale

Economist

Vinay Rachh

Research Associate

Amit Patil

Research Associate

Shareen Batatawala

Research Associate

Twinkle Gosar

Research Associate

Tejashwini Kumari

Research Associate

Technicals:

Shardul Kulkarni

Sr. Technical Analyst

Sameet Chavan

Technical Analyst

Sacchitanand Uttekar

Technical Analyst

Derivatives:

Siddarth Bhamre

Head - Derivatives

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Hiten Sampat

Sr. A.V.P- Institution sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Akshay Shah

Sr. Executive

Production Team:

Tejas Vahalia

Research Editor

Dilip Patel

Production

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE: INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

January 31, 2013

10