Nagarjuna Agrichem | Agrichemical

December 22, 2014

Nagarjuna Agrichem

BUY

CMP

`12

Initiating Coverage

Target Price

`18

Nagarjuna Agrichem Ltd (NACL) is one of the largest pesticide agrichemical

Investment Period

12 Months

companies in the country with a market share of ~4% and belongs to the

Nagarjuna Group of Hyderabad. NACL manufactures a comprehensive range of

Stock Info

pesticide technicals, formulations and custom manufactured fine chemicals

Sector

Agrochemical

through its three plants situated at Srikakulam, Ethakota and Shadnagar in

Market Cap (` cr)

193

Andhra Pradesh. Pesticides account for more than 95% of the company's total

Net debt (` cr)

202

revenues. Historically, the domestic business has been contributing by around

Beta

0.8

70% to the company’s overall revenues, while exports have been accounting for

52 Week High / Low

17 / 4

the balance. However, in the recent past, the contribution of exports has come

Avg. Daily Volume

83,067

down, ie to ~20% in FY2014.

Face Value (`)

1

Profitability to improve: NACL’s performance since FY2011-14 has been

BSE Sensex

27,372

impacted on account of a slew of industry and company specific issues. Raw

Nifty

8,225

material constraints and raw material price hikes have diluted the gross margin of

Reuters Code

NAGA.BO

the company, which has now stabilized at around ~30% from a high of ~39%

Bloomberg Code

CGI@IN

(Avg. FY2000-10). Also, in FY2013, exports were significantly impacted due to the

closure of the Srikakulam Plant for about five months and the incapacitation of

Block 5 which was affected by a fire. Block 5 is one of the largest blocks in the

Shareholding Pattern (%)

plant and accounting for around 40% of the total capacity of the plant (FY2013);

Promoters

74.8

its closure impacted the operating profitability of the company. These factors led

MF / Banks / Indian Fls

4.9

the company to post an EBIDTA profit of a mere `4cr in FY2014. However, with

FII / NRIs / OCBs

0.3

the block operational again and raw material prices stabilizing, the company is

Indian Public / Others

20.0

poised to be back on the path of recovery. Hence, we expect the company to post

a 16.1% CAGR in its top-line over FY2014-16E to `849cr and EBDITA margins

bouncing back to around 10.3% levels (in FY2016).

Abs. (%)

3m 1yr 3yr

Outlook & Valuation: With the Srikakulam plant’s Block 5 back into operation, the

Sensex

1.1

29.6

72.9

company is expected to witness improved profitability, going forward. Thus, we

Nag. Agrichem

(18.3)

219.2

90.0

expect the company to post a sales CAGR of 16.1% over FY2014-16E and a net

profit of `39cr in FY2016E V/s a loss of `12.6cr in FY2013. At the CMP, the stock

trades at a P/E of 5.0x FY2016E EPS, which we believe is attractive in comparison

to its peers. Thus we recommend a Buy on the stock with a target price of `18.

Key financials (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015E

FY2016E

Net sales

626

596

630

739

849

% chg

12.9

(4.9)

5.7

17.4

14.9

Adj. net profit

7

(13)

(18)

10

39

% chg

61.5

-

40.3

-

298.3

EBITDA Margin (%)

8.6

2.1

0.7

5.8

10.3

EPS (`)

0.5

(0.8)

(1.1)

0.6

2.5

P/E (x)

25.1

(14.6)

(10.9)

20.0

5.0

P/BV (x)

0.9

0.9

1.1

1.1

0.9

RoE (%)

3.6

(6.3)

(9.6)

5.4

19.3

RoCE (%)

9.6

2.1

1.8

9.3

16.2

Sarabjit kour Nangra

EV/Sales (x)

0.6

0.6

0.6

0.6

0.6

+91-22-3935 7800 Ext: 6806

EV/EBITDA (x)

7.1

26.9

92.9

10.3

5.5

Source: Company, Angel Research; Note: CMP as of December 19, 2014

Please refer to important disclosures at the end of this report

1

Nagarjuna Agrichem | Initiating Coverage

Investment arguments

Pick up in exports to drive growth momentum

Revival in exports to drive future top-line

Over the last one decade (FY2000-2010) NACL has emerged as one of the fastest

growth

growing agrochemical companies, posting a sales CAGR of 29.2%. The sales

growth during the period was mainly driven by exports which posted a CAGR of

54.8%, albeit on a lower base, to end the period at `225cr (FY2010). The

domestic markets segment posted a CAGR of around 24.5% (FY2010) during the

period, leading the company to emerge among the top 10 players in the domestic

market. However, since FY2011, the company’s performance has moderated, with

it posting sales CAGR of only 4.3% over the FY2011-14 period. The main cause

for the same has been gyration in exports and institutional sales. Revenues from

these segments were impacted due to lower demand in export markets and owing

to other operational reasons.

Also, in FY2013, exports were significantly impacted due to the closure of

Srikakulam plant for about five months and due to the incapacitation of Block 5

which was affected by a fire. Block 5 is one of the largest blocks in the plant and

accounted for around 40% of the total capacity of the plant (FY2013). Export sales

accordingly decreased to `120cr in FY2013 V/s `197cr in FY2012. Rough

calculations put the overall sales attributable to the plant at ~`200cr. The

incapacitation of the plant has also severely impacted export sales of the company

in FY2014, which dipped by 23.3% to end the period at `92cr. As a result, the

contribution of exports to total revenue dipped to around 20% in FY2014 from

35% in FY2010.

However, the company has finished its rebuilding work of the fire affected Block-5

and it was re-commissioned in March 2014; the first output of the plant was

received on 30th March, 2014. As a part of risk mitigation and in order to prevent

any such untoward event in future, the company has taken various initiatives and

additional safety measures.

Thus the export and institutional sales of the company have resumed and the same

are reflected in the company’s net sales growth of 19.2% for 1HFY2015. During

FY2015, the company expects to clock export sales of `200cr and should reach its

earlier export sales levels of around `250cr by FY2016.

On the domestic markets front, the company has been growing at a rate higher

than the industry. Going forward, with domestic markets expected to grow at a

CAGR of 12%, on a conservative basis, we easily expect the company to post a

CAGR of 13% over FY2014-16E, while exports are expected to post a CAGR of

61.5% during the same period. This would enable the company to post a CAGR of

16.1% in sales over FY2014-16E to `849cr.

December 22, 2014

2

Nagarjuna Agrichem | Initiating Coverage

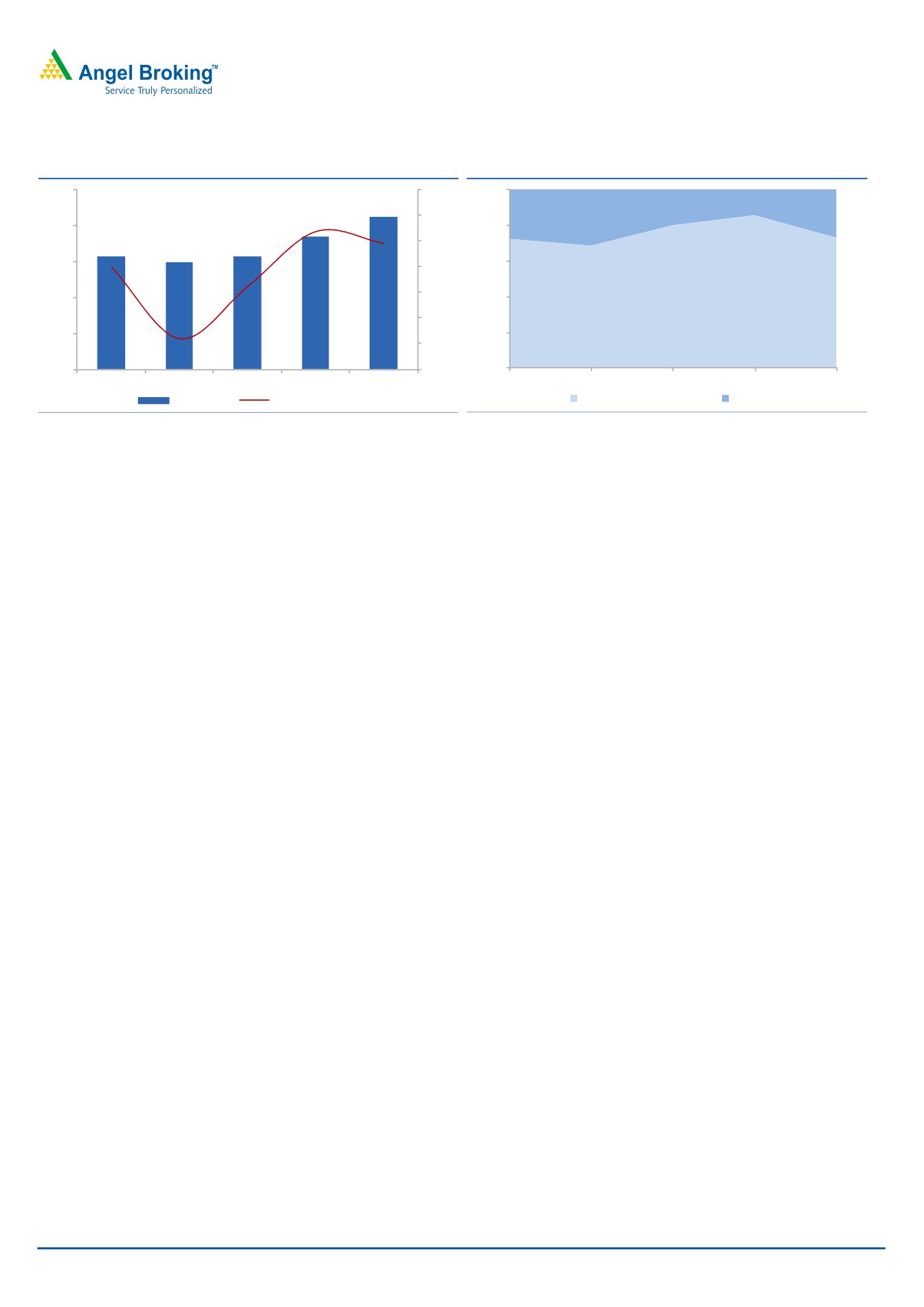

Exhibit 1: Sales growth to rebound

Exhibit 2: Exports to regain prominence

1000

25

100.0

849

14.6

739

20.2

20

27.7

31.4

27.1

800

80.0

626

630

15

596

600

60.0

10

5

72.3

85.4

400

40.0

79.8

68.6

72.9

0

200

20.0

(5)

0

(10)

0.0

FY2012

FY2013

FY2014

FY2015E

FY2016E

FY2012

FY2013

FY2014

FY2015E

FY2016E

Sales (` cr)

Sales growth(%)

Domestic Sales & others (%)

Exports (%)

Source: Company, Angel Research

Source: Company, Angel Research

EBIDTA margin to witness an uptrend

Stability in key raw material prices and

On the operating profitability front, the company’s gross margins have averaged a

higher exports to aid margin expansion

healthy 39.0% during FY2000-10 with EBITDA margin at 16.6%. However after

FY2010, the gross margins along with operating margins came under pressure.

During FY2011-14, the gross margins and operating margins averaged around

34.4% and 6.0%, respectively. While the company is backward integrated and

uses almost

65% of its raw material manufactured indigenously, capacity

constraints internally along with rising input costs and raw material supply

constraints have impacted its gross margins. Along with this, the erratic and

irregular power supply from the electricity board, manpower shortage issues etc.

continue to be causes of concerns for the company. However, the major drain on

the operating margins has been the lower capacity utilization of the Srikakulam

plant due to fire at Block 5. Block 5 is one of the largest blocks in the plant; the

block accounted for around 40% of the total capacity of the plant (FY2013). Thus,

both external and internal factors have constrained the overall profitability of the

company, with the company posting EBITDA margins of a meager 0.7% in

FY2014.

With the company now having resolved its problem at the Srikakulam plant, the

operating margins of the company have moved up to 5.2% in 1HFY2015 V/s 2.1%

in 1HFY2014. The gross margins have stabilized at around 30.6% in 1HFY2015

V/s 25.9% in 1HFY2014.

December 22, 2014

3

Nagarjuna Agrichem | Initiating Coverage

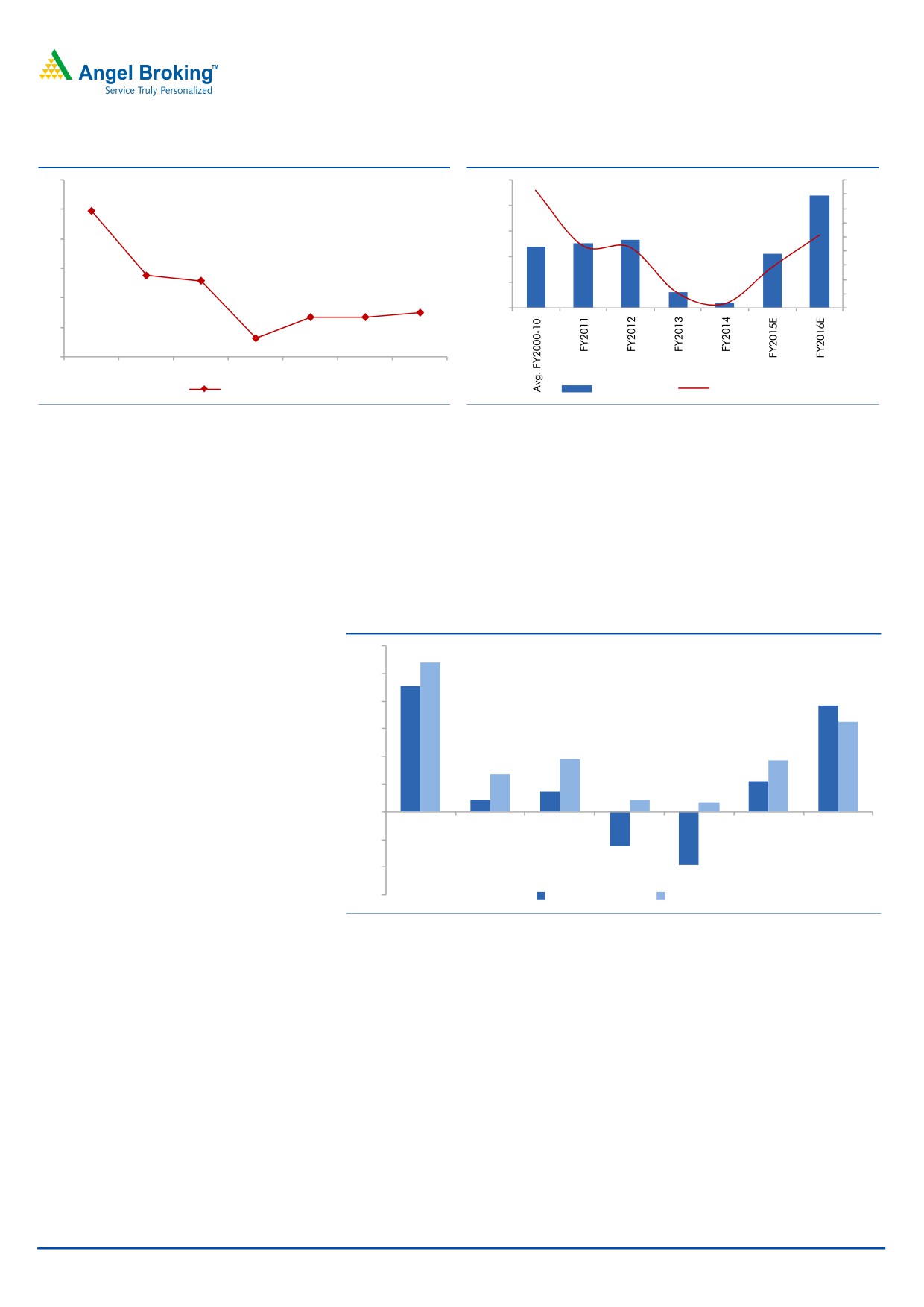

Exhibit 3: Gross Margins to stabilise

Exhibit 4: EBIDTA margins to inch higher

42

100.0

16.6

18.0

39.9

16.0

40

80.0

14.0

10.3

12.0

60.0

8.8

8.6

38

10.0

5.8

8.0

40.0

35.5

6.0

35.2

36

2.1

4.0

20.0

0.7

2.0

34

33.0

32.7

32.7

0.0

0.0

32

31.3

30

Avg.

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

FY2000-10

Gross Margins(%)

EBDITA( ` Cr)

EBDITA Margins(%)

Source: Company, Angel Research

Source: Company, Angel Research

Return ratios to improve

With the company having resolved its problem at the Srikakulam capacity, the

overall capacity utilization levels are expected to improve. This will lead to higher

sales, resulting in improved operational profitability and higher ROCE and ROE.

The ROCE is expected to turn positive to 16.2% in FY2016E, while the ROE is

expected to be 19.3% in FY2016E, broadly in line with the industry averages.

Exhibit 5: Return ratios to see recovery

30

26.9

22.8

25

19.3

20

16.2

15

9.3

9.6

10

6.8

5.4

3.6

5

2.2

2.1

1.8

0

Avg.

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E

(5)

FY2000-10

(6.3)

(10)

(9.6)

(15)

ROE(%)

ROCE(%)

Source: Company, Angel Research

Industry Outlook

Agrochemical Industry- Drivers for growth in place

Domestic Market— Under-penetration to drive growth

The Indian agrochemical sector, with a market size of around ~`13,200cr

(FY2014), has been growing by

~8-10% annually, in comparison to the

3-4% growth rate globally. India is one of the largest consumers of agrochemicals.

The usage of pesticides in India is less than 2% of the global consumption and is

confined to one-fourth of the total arable land of about 180mn hectares. Overall,

India’s consumption of pesticides at around 0.6Kg/ha is lower compared to US

(7Kg/ha) and Japan (12Kg/ha), thus leaving a huge scope for the organized

players to grow.

December 22, 2014

4

Nagarjuna Agrichem | Initiating Coverage

The crop protection market in India is largely dominated by insecticides which

account for 65% of the total crop protection chemicals market. Herbicides are the

largest growing segment and currently account for 16% of the total and rest is

attributed to fungicides. Paddy and cotton are the major consumers of crop

protection chemicals, accounting for

28% and 20% of overall consumption

respectively. In terms of states, the top three - Andhra Pradesh, Maharashtra and

Punjab - account for ~50% of the total pesticide consumption in India.

Challenges in the domestic market include seasonality and higher dependence on

monsoon. As much as 60% to 70% of demand is in the Kharif (June to November)

season and companies have to stock inventories well before. The business is long

on credit and agrochemicals are the last thing farmers buy, well after seeds and

fertilizers and offtake depends on a lot of things, including the weather going right.

Also around 64% of Indian cultivated land is monsoon dependent. In terms of

competition, the industry is highly fragmented at both levels, with around

125 technical producers and more than 800 formulators, serving millions of

farmers through thousands of dealers

/ distributors. The top five players

cumulatively capture only 57% of the total market and no single player among

these has over 20% share.

These factors would continue to keep the profitability, especially of the medium

and small players, in check. Hence, companies with large market shares and the

ones being backward integrated will be able to make most of the opportunity.

Overall, the growing populations, shrinking farmland and scarcity of water would

continue to increase pressure on improving farm productivity. In this respect,

pesticides play an important role in trying to minimise the loss due to insects,

weeds and diseases, given that about 35% to 45% of crop production is lost on this

account. This will continue to drive growth of the Indian agrochemical industry. The

apex industry body Assocham said that the agrochemicals sector in India is likely to

cross the `17,600cr mark by 2017, with it currently growing at a CAGR of about

12%.

Exports- Generic along with Contract Manufacturing lucrative

Exports on the other hand, standing at `16,800cr (FY2014), are expected to post a

CAGR of 10% over the next three years, mainly driven by generics. The global

agrichem industry, valued at ~US$53bn (CY2014E), is dominated by the top six

innovators, viz Bayer, Syngenta, Monsanto, BASF, DuPont and Dow, which enjoy a

large market share of the patented (28%) and off-patent (32%) market. The top six

innovators enjoy a large share of the off-patent market due to high entry barriers

for pure generic players. Thus, one-third of the total pie worth ~US$18bn, which is

controlled by the top six innovators through proprietary off-patent products,

provides a high-growth opportunity for larger integrated generic players.

The market share of generic players increased from 32% levels in 1998 to 40%

levels by 2006-end. The industry registered a CAGR of 3% over 1998-2014, while

generic players outpaced the industry, posting a CAGR of 6%. Going ahead, given

the opportunities and a drop in the rate of new molecule introduction by

innovators, we expect generic players to continue to outpace the industry’s growth

and increase their market share in the overall pie. Historically, global agrichem

players have been logging in-line growth with global GDP. Going ahead, over

December 22, 2014

5

Nagarjuna Agrichem | Initiating Coverage

CY2014-15, the global economy is expected to grow by 3-4%. Assuming this trend

plays out in terms of growth for the agrichem industry and given that the same rate

of genericisation occurs, the agrichemical generic industry could log in 6-8% yoy

growth during the period and garner a market share of 50--55%.

Apart from this, toll manufacturing is also an important segment, mainly in

technicals. Many leading MNCs are getting their technicals manufactured in

countries like India on toll basis in view of the cost advantage that it offers. Tolling

as a business is expected to grow as products come out of the patent protection

periods. India, which is the fourth largest producer of agro-chemicals in the world

after the United States, Japan and China can easily make its mark in the

international generic markets, given its low cost of production.

Financials

Top-line to grow at a CAGR of 16.1% over FY2014-16E

We expect the company’s net sales to grow at a CAGR of

16.1% over

FY2014-16E, from `630cr to `849cr, mainly driven by a bounce back in exports.

The company’s net domestic sale is expected to increase from `477cr in FY2014 to

`609cr by FY2016E, while its exports are expected to increase from `92cr to

`240cr, during the same period. The company’s exports growth during the period

would be driven by the full operation of its Srikakulam plant. Growth in the

domestic markets however would be restricted owing to capacity constraints.

EBIDTA and EBIDTA margins to improve

The EBIDTA and the EBIDTA margins of the company have been under pressure on

back of high input costs and closure of one of the main blocks of its Srikakulam

plant, which constitutes around 40% of its capacity. With the block resuming its

production, the EBDITA margins have bounced back to ~5% levels in 1HFY2015.

With stable raw material cost and capacity utilization improving, the company’s

EBIDTA is expected to grow at a CAGR of 359.1% to `87cr by FY2016E. As a

result, EBIDTA margins are expected to improve from 0.7% in FY2014 to 10.3% in

FY2016E.

PAT to witness a significant improvement over FY2014-16E

With improvement in EBIDTA margins specifically in FY2016E, the PAT is expected

to come in at `39cr in FY2016E from a loss of `18cr in FY2014. As a result, the

PAT margins are expected to improve from 0.8% in FY2011 to 4.5% in FY2016E.

December 22, 2014

6

Nagarjuna Agrichem | Initiating Coverage

Exhibit 6: PAT and PAT margins to improve

50.0

8.0

7.4

4.5

40.0

6.0

30.0

4.0

20.0

1.2

1.3

10.0

0.8

2.0

0.0

0.0

(10.0)

(2.0)

(20.0)

(2.1)

(2.8)

(30.0)

(4.0)

PAT (` cr)

PAT Margins(%)

Source: Company, Angel Research

Outlook and valuation

We expect net sales and EBIDTA to register a CAGR of 16.1% and 359.1% to

`849cr and `87cr, respectively, over FY2014-16E. As a result, the net profit is

expected to come in at `39cr in FY2014-16E. At the current market price the stock

is trading at a P/E of 5.0x its FY2016E earnings. On account of expected revival in

profitability of the company, we initiate coverage on the stock with a Buy rating

and target price of `18, valuing the stock at ~7x its FY2016E earnings.

Exhibit 7: EV/Sales band

700

600

500

400

300

200

0.4x

0.6x

0.7x

0.9x

Source: Company, Angel Research

Relative valuation

The leading players in the industry are United Phosphorus, Rallis India, and

Insecticides. NACL is trading at cheap valuations of 5.0x P/E and 0.9x P/BV on

FY2016E as compared to its peers which are trading at relatively higher

valuations.

December 22, 2014

7

Nagarjuna Agrichem | Initiating Coverage

Exhibit 8: Comparative analysis

EV/

EV/

Company

Year end

Mcap

Sales

OPM

PAT

EPS

RoE

P/E

P/BV

Sales

EBIDTA

Nagarajuna Agri.

FY2015E

187

739

5.8

10

0.6

5.4

20.0

1.1

0.6

10.3

FY2016E

187

849

10.3

39

2.5

19.3

5.0

0.9

0.6

5.5

UPL

FY2015E

13,788

11,850

17.3

1,282

29.9

22.2

10.8

2.0

1.3

7.4

FY2016E

13,788

13,627

17.3

1,515

35.3

21.7

9.1

1.7

1.1

6.1

Rallis

FY2015E

4,062

2,020

13.9

176

9.0

22.6

23.3

4.9

2.0

14.7

FY2016E

4,062

2,365

13.9

204

10.5

22.3

19.9

4.1

1.7

12.4

Source: Company, Angel Research,

Key concerns

Growth challenge in exports: In FY2010, NACL derived 35% of its revenues

from exports, which came down to 27% in FY2011, also on back of the lower

demand from its toll manufacturing business. These exports primarily constitute the

contract manufacturing job that the company does for the MNC players. Hence

any drop in demand of final products of these MNCs will negatively impact the

company’s performance.

Vagaries of monsoon: Most of the agricultural production in India is rain fed

and hence highly dependent on monsoons. Hence, vagaries in monsoon could

affect the demand for agrichemicals and in turn impact the company.

Company Background

NACL is one of the largest pesticide agrichemical companies in the country with a

market share of ~4% and belongs to the Nagarjuna Group of Hyderabad. The

company also has a credible presence in the international market. NACL

manufactures a comprehensive range of pesticide technicals, formulations and

custom manufactured fine chemicals. Pesticides account for 95% of the company's

total revenues. Historically, the domestic business has been contributing around

70% of the company’s overall revenues, while exports accounted for the balance.

However, in the recent past, decline in exports has lead to its contribution coming

down to 20% in FY2014. NACL has three plants situated at Srikakulam, Ethakota

and Shadnagar in Andhra Pradesh.

December 22, 2014

8

Nagarjuna Agrichem | Initiating Coverage

Profit and Loss

Y/E March (` Cr)

FY11

FY12

FY13

FY14E

FY15E

FY16E

Net Sales

554

626

596

630

739

849

Other operating income

16

17

22

25

25

25

Total operating income

570

643

617

655

764

874

% chg

(11.9)

12.8

(4.0)

6.1

16.7

14.4

Total Expenditure

517

572

583

625

696

762

Net Raw Materials

368

406

409

424

497

569

Other Mfg costs

45

52

53

57

61

51

Personnel

40

35

40

43

35

40

Other

64

80

80

101

103

102

EBITDA

38

54

13

4

43

87

% chg

(68.8)

43.2

(76.2)

(67.6)

931.8

104.2

(% of Net Sales)

6.8

8.6

2.1

0.7

5.8

10.3

Depreciation& Amortisation

23

27

25

22

26

30

EBIT

30

44

9

8

42

83

% chg

(70.0)

45.0

(79.1)

(17.3)

451.8

98.7

(% of Net Sales)

5.3

6.8

1.5

1.2

5.5

9.5

Interest & other Charges

26

33

31

28

31

36

Other Income

5

4

2

1

1

1

(% of PBT)

56

27

(8)

(3)

5

1

Recurring PBT

9

14

(20)

(20)

11

47

% chg

(90.0)

51.5

-

-

-

324.5

Extraordinary (Expense )/Inc.

(3)

(0)

(0)

(3)

-

-

PBT (reported)

6

14

(20)

(23)

11

47

Tax

3

7

-

-

2

9

(% of PBT)

52.1

48.7

36.5

9.3

20.0

20.0

PAT (reported)

3

7

(13)

(21)

9

38

Add: Share of earnings of asso.

-

-

-

1

1

1

Less: Minority interest (MI)

-

-

-

-

-

-

Prior period items

-

-

-

-

-

-

PAT after MI (reported)

3

7

(13)

(21)

10

39

ADJ. PAT

5

7

(13)

(18)

10

39

% chg

(92.0)

61.5

298.3

(% of Net Sales)

0.8

1.2

(2.1)

(2.8)

1.3

4.5

Basic EPS (`)

0.3

0.5

(0.8)

(1.1)

0.6

2.5

Fully Diluted EPS (`)

0.3

0.5

(0.8)

(1.1)

0.6

2.5

% chg

(92.0)

61.5

298.3

December 22, 2014

9

Nagarjuna Agrichem | Initiating Coverage

Balance Sheet

Y/E March (` Cr)

FY11

FY12

FY13

FY14E FY15E FY16E

SOURCES OF FUNDS

Equity Share Capital

15

15

15

16

16

16

Preference Capital

-

-

-

-

-

-

Reserves& Surplus

188

192

180

159

166

202

Shareholders Funds

203

207

195

174

182

218

Minority Interest

-

-

-

-

-

-

Total Loans

204

220

177

219

260

300

Other Long term liabilities

11

11

10

12

12

12

Long Term Provisions

0

1

1

1

1

1

Deferred Tax Liability

25

29

22

19

19

19

Total Liabilities

443

467

405

426

474

550

APPLICATION OF FUNDS

Gross Block

324

334

325

353

403

453

Less: Acc. Depreciation

117

144

154

172

198

228

Net Block

207

190

171

181

205

225

Capital Work-in-Progress

7

16

11

18

18

18

Goodwill / Intangilbles

1

1

1

1

1

1

Investments

0

4

4

9

9

9

Long Term Loan & Adv.

12

17

14

12

17

19

Current Assets

325

403

400

399

452

540

Cash

23

25

22

17

4

6

Loans & Advances

19

19

41

46

54

80

Other

283

359

337

336

395

454

Current liabilities

109

164

195

195

229

263

Net Current Assets

216

239

204

204

224

277

Others

-

-

-

-

-

-

Total Assets

443

467

405

426

474

550

December 22, 2014

10

Nagarjuna Agrichem | Initiating Coverage

Cash flow statement

Y/E March (` Cr)

FY11

FY12

FY13

FY14E

FY15E

FY16E

Profit before tax

6

14

(20)

(23)

11

47

Depreciation

23

27

25

22

26

30

Change in Working Capital

20

(26)

35

(4)

(37)

(54)

Less: Other income

(5)

(4)

(2)

(1)

(1)

(1)

Direct taxes paid

(3)

(7)

7

2

(2)

(9)

Cash Flow from Operations

41

4

46

(4)

(2)

13

(Inc.)/ Dec. in Fixed Assets

(54)

11

15

(35)

(50)

(50)

(Inc.)/ Dec. in Investments

-

(4)

-

-

-

-

Inc./ (Dec.) in loans and adv.

-

-

-

-

-

-

Other income

(5)

(4)

(2)

(1)

(1)

(1)

Cash Flow from Investing

(49)

12

16

(34)

(49)

(49)

Issue of Equity

-

-

-

1

-

-

Inc./(Dec.) in loans

30

24

43

(44)

(41)

(40)

Dividend Paid (Incl. Tax)

(7)

(2)

-

-

(2)

(2)

Others

(14)

(26)

(106)

76

82

81

Cash Flow from Financing

9

(4)

(63)

33

39

39

Inc./(Dec.) in Cash

1

12

(3)

(5)

(13)

2

Opening Cash balances

22

13

25

22

17

4

Closing Cash balances

23

25

22

17

4

6

December 22, 2014

11

Nagarjuna Agrichem | Initiating Coverage

Key Ratios

Y/E March

FY11

FY12

FY13

FY14E

FY15E

FY16E

Valuation Ratio (x)

P/E (on FDEPS)

40.6

25.1

-

-

20.0

5.0

P/CEPS

3.6

3.0

4.9

7.4

3.1

2.0

P/BV

0.9

0.9

0.9

1.1

1.1

0.9

Dividend yield (%)

3.6

1.1

-

-

1.2

1.2

EV/Sales

0.7

0.6

0.6

0.6

0.6

0.6

EV/EBITDA

9.9

7.1

26.9

92.9

10.3

5.5

EV / Total Assets

0.8

0.8

0.8

0.9

0.9

0.9

Per Share Data (`)

EPS (Basic)

0.3

0.5

(0.8)

(1.1)

0.6

2.5

EPS (fully diluted)

0.3

0.5

(0.8)

(1.1)

0.6

2.5

Cash EPS

3.4

4.1

2.5

1.7

4.0

6.3

DPS

0.4

0.1

-

-

0.1

0.1

Book Value

13.6

13.9

13.1

11.2

11.7

14.0

Dupont Analysis

EBIT margin

5.3

6.8

1.5

1.2

5.5

9.5

Tax retention ratio

47.9

51.3

63.5

90.7

80.0

80.0

Asset turnover (x)

0.3

1.4

1.5

1.6

1.7

1.7

ROIC (Post-tax)

0.8

5.0

1.4

1.7

7.5

12.9

Cost of Debt (Post Tax)

0.9

8.1

9.8

12.8

10.4

10.4

Leverage (x)

0.9

0.9

0.9

1.0

1.3

1.4

Operating ROE

0.7

2.2

(6.0)

(9.2)

3.8

16.4

Returns (%)

ROCE (Pre-tax)

6.8

9.6

2.1

1.8

9.3

16.2

Angel ROIC (Pre-tax)

7.2

10.2

2.2

1.9

9.7

16.6

ROE

2.2

3.6

(6.3)

(9.6)

5.4

19.3

Turnover ratios (x)

Asset Turnover (Gross Block)

1.8

2.0

1.9

1.9

2.0

2.0

Inventory / Sales (days)

93

88

100

97

90

91

Receivables (days)

88

94

106

90

83

85

Payables (days)

76

86

98

89

86

92

WC cycle (ex-cash) (days)

127

125

121

107

100

105

Solvency ratios (x)

Net debt to equity

0.9

0.9

0.9

1.0

1.3

1.4

Net debt to EBITDA

4.8

4.2

7.9

30.4

27.4

4.7

Interest Coverage (EBIT / Int.)

1.2

1.3

0.3

0.3

1.3

2.3

December 22, 2014

12

Nagarjuna Agrichem | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important 'Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Nagarjuna Agrichem

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to 15%)

Sell (< -15%)

December 22, 2014

13

Nagarjuna Agrichem | Initiating Coverage

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research (Banking)

Amarjeet Maurya

Analyst (FMCG, Media, Mid-Cap)

Bharat Gianani

Analyst (Automobile)

Shrenik Gujrathi

Analyst (Cap Goods, Cement)

Umesh Matkar

Analyst (Banking)

Twinkle Gosar

Analyst (Mid-Cap)

Tejas Vahalia

Research Editor

Technicals and Derivatives:

Siddarth Bhamre

Head - Technical & Derivatives

Sameet Chavan

Technical Analyst

Sneha Seth

Associate (Derivatives)

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Assistant Manager

Production Team:

Dilip Patel

Production Incharge

CSO & Registered Office: G-1, Ackruti Trade Centre, Road No. 7, MIDC, Andheri (E), Mumbai - 93. Tel: (022) 3083 7700. Angel Broking Pvt. Ltd: BSE Cash: INB010996539 / BSE F&O: INF010996539, CDSL Regn. No.: IN - DP - CDSL - 234 - 2004, PMS Regn. Code: PM/INP000001546, NSE Cash: INB231279838 /

NSE F&O: INF231279838 / NSE Currency: INE231279838, MCX Stock Exchange Ltd: INE261279838 / Member ID: 10500. Angel Commodities Broking (P) Ltd.: MCX Member ID: 12685 / FMC Regn. No.: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn. No.: NCDEX / TCM / CORP / 0302.

December 22, 2014

14