Offer for Sale | Power Sector

February 6, 2013

NTPC

SUBSCRIBE

CMP

`152

Valuation commands Subscribe

OFS floor price

`145

The government is coming out with an Offer For Sale (OFS) of 78.3cr equity

Stock Info

shares of NTPC. The OFS is expected to raise close to `11,350cr at the floor price

Sector

Power

of `145/share. After this OFS, the government’s stake in the company would

Market Cap (` cr)

125,578

come down from 84.5% to 75%. The OFS will be held on February 07, 2013.

Net Debt (` cr)

30,365

Beta

0.8

Investment Arguments

52 Week High / Low

190/139

Capacity addition to drive future growth: Going forward, NTPC’s growth is

Avg. Daily Volume

239,341

expected to be driven by the huge capacity addition planned by it. The company

Face Value (`)

10

envisions having 51,000MW of capacity by FY2017. In all, the company targets

BSE Sensex

19,640

to add ~14,038MW of capacity in the Twelfth Plan (FY2012-17), of which

Nifty

5,959

4,170MW and 2,718MW of capacity is planned for addition during FY2013 and

Reuters Code

NTPC.BO

FY2014 respectively. The robust capacity addition is expected to result in

Bloomberg Code

NTPC@IN

15% CAGR in regulated equity to `36,003cr over FY2012-14E.

Earnings protected by the regulated return model: NTPC, being a central public

Shareholding Pattern (%)

utility, is governed by the regulated return model. The CERC’s regulations for

Promoters

84.5

FY2010-14 provide RoE of 15.5% on regulated equity. As per regulations, fuel

MF / Banks / Indian Fls

7.5

costs are a pass-through, which protect the company from cost pressures due to

FII / NRIs / OCBs

4.4

increased fuel costs. NTPC has 85% of its overall output tied up under the

Indian Public / Others

3.6

long-term power purchase agreement (PPA) route (regulated returns), which

ensures power off-take and stable cash flows thereof.

Abs. (%)

3m 1yr

3yr

Outlook and Valuation: We expect NTPC to register a CAGR of 12.3% and 8.5%

Sensex

4.4

10.9

23.4

in its top-line and bottom-line over FY2012-14E, respectively. At the offer price

NTPC

(9.6)

(14.3)

(25.7)

(which is at a 4.6% discount to the price as on February 06, 2013), the stock

would trade at 1.3x FY2014E P/BV. Given the attractive valuation (stock trading at

1.3x FY2014E P/BV compared to its three year trading range of 1.5x to 2.3x and

median of 1.8x), we recommend Subscribe on the issue. We have assigned a

multiple of 1.5x to arrive at a target price of `163.

Key financials (Consolidated)

Y/E March (` cr)

FY2011

FY2012 FY2013E

FY2014E

Net Sales

57,607

64,958

72,809

81,951

% chg

19.4

12.8

12.1

12.6

Net Profit

7,691

9,497

10,048

11,187

% chg

(13.0)

23.5

5.8

11.3

EBITDA (%)

22.2

21.8

23.4

24.1

EPS (`)

9.3

11.5

12.2

13.6

P/E (x)

15.5

12.6

11.9

10.7

V Srinivasan

P/BV (x)

1.7

1.6

1.5

1.3

022-39357800 Ext: 6831

RoE (%)

11.5

13.1

12.7

13.0

RoCE (%)

8.8

8.7

9.3

9.6

EV/Sales (x)

2.4

2.3

2.3

2.2

Amit Patil

022-39357800 Ext: 6839

EV/EBITDA (x)

11.0

10.6

9.7

9.0

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Offer for Sale | Power sector

Company Background

Established in 1975, NTPC is India's largest power generation company. NTPC

Group has an installed capacity of 39,674MW. The company enjoys healthy

operational efficiency and has consistently reported high PLF of ~85% compared

to all-India PLF of ~73%.

Investment Rationale

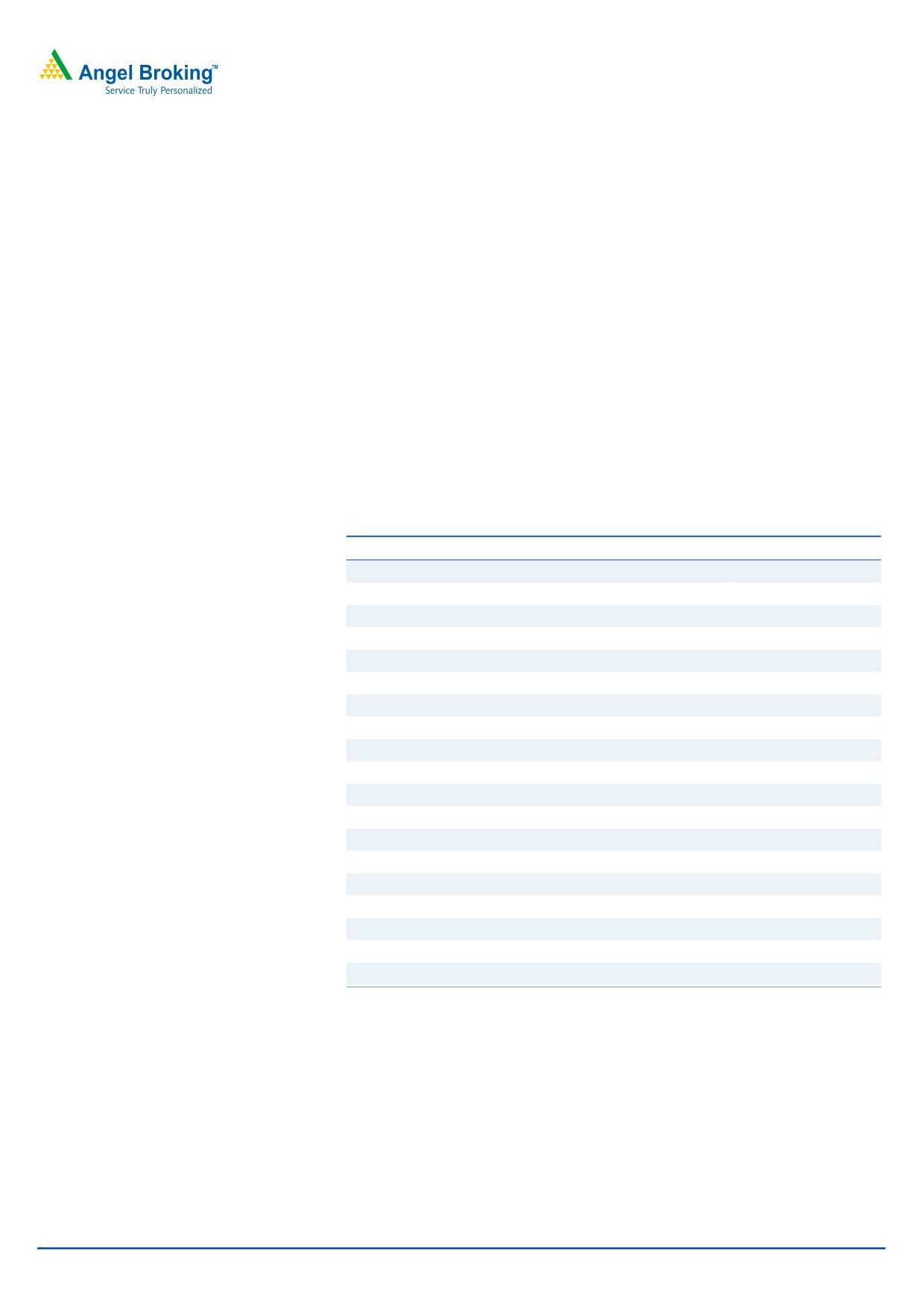

Capacity addition to drive future growth: Going forward, NTPC’s growth is

expected to be driven by the huge capacity addition planned by it. The company

envisions having 51,000MW of capacity by FY2017. In all, the company targets to

add ~14,038MW of capacity in the Twelfth Plan (FY2012-17), of which 4,170MW

and 2,718MW of capacity is planned for addition during FY2013 and FY2014

respectively. NTPC has already commissioned 2,660MW capacity in 1HFY2013

and is likely to meet its targeted capacity for FY2013. The robust capacity addition

is expected to result in 15% CAGR in regulated equity to `36,003cr by FY2014.

Exhibit 1: Upcoming Projects

Projects

Capacity (MW)

Vallur - I, Phase - I & II JV

500

Solar PV (A&N, Dadri)

10

Rihand - III

500

Bongaigaon

250

Barh-II

660

Koldam

800

Singrauli Hydel

8

Vallur - I, Phase - I & II JV

500

Bongaigaon

500

Barh-II

660

Barh-I

660

Tapovan Vishnugarh Hydel

520

Nabinagar JV

500

Kanti - Subsidiary

390

Barh-I

1320

Vindhyachal

500

Kudgi

800

Nabinagar JV

500

Kudgi

800

Source: Company, Angel Research

February 6, 2013

2

Offer for Sale | Power sector

Exhibit 2: Capacity ramp up

50,000

45,000

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

-

FY2011

FY2012

FY2013E

FY2014E

FY15E

Source: Company, Angel Research

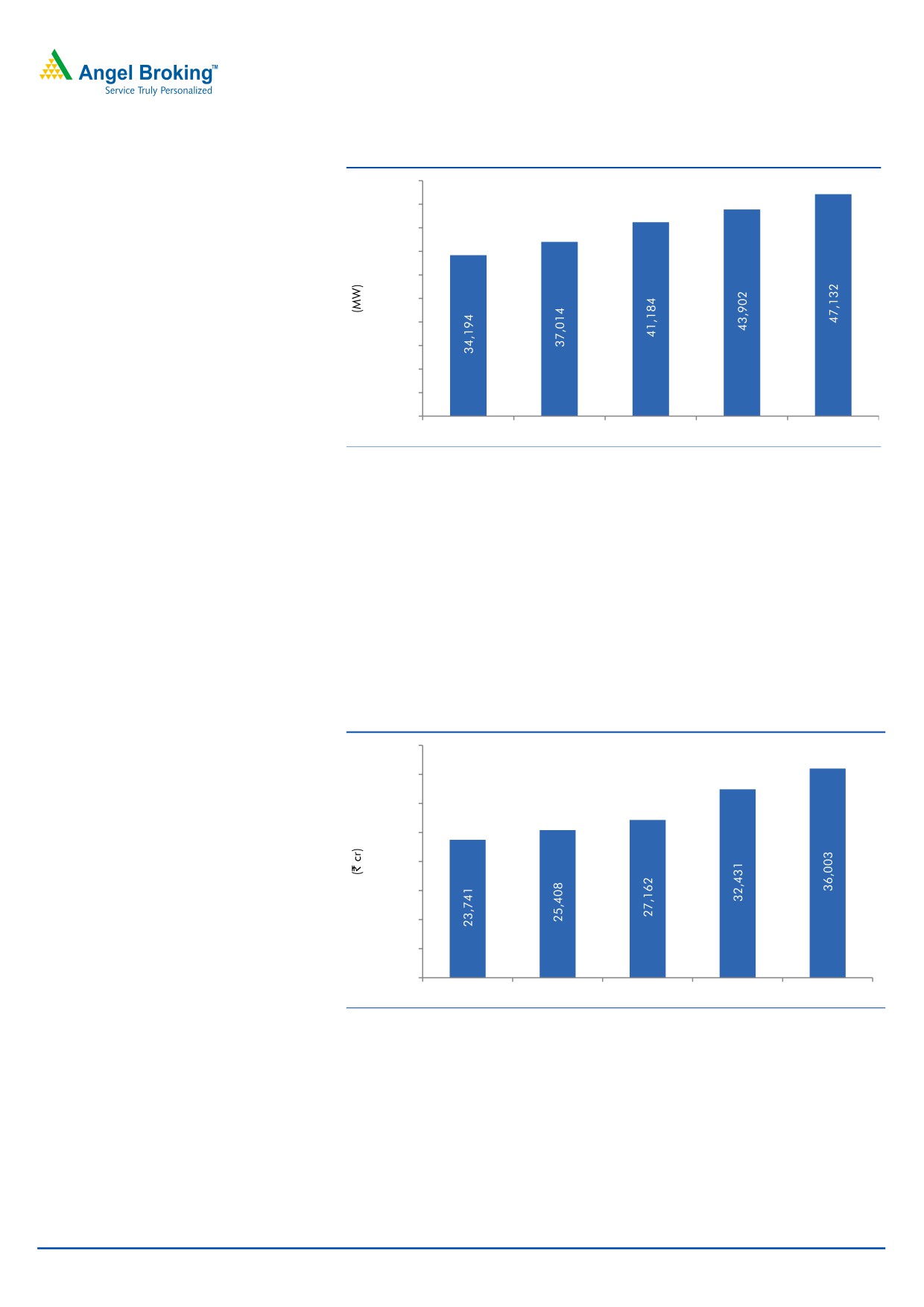

Earnings protected by the regulated return model: NTPC, being a central public

utility, is governed by the regulated return model. CERC’s regulations for

FY2010-14 provide RoE of 15.5% on regulated equity. As per regulations, fuel

costs are a pass-through, which protect the company from cost pressures due to

increased fuel costs. NTPC has 85% of its overall output tied up under the

long-term power purchase agreement (PPA) route (regulated returns), which

ensures power off-take and stable cash flows thereof. Further, recent tariff hikes

carried out by almost all SEBs across India is expected to improve their financial

position, resulting in higher power off-take, which will benefit NTPC.

Exhibit 3: Regulated Equity

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

-

FY2010

FY2011

FY2012

FY2013E

FY2014E

Source: Company, Angel Research

February 6, 2013

3

Offer for Sale | Power sector

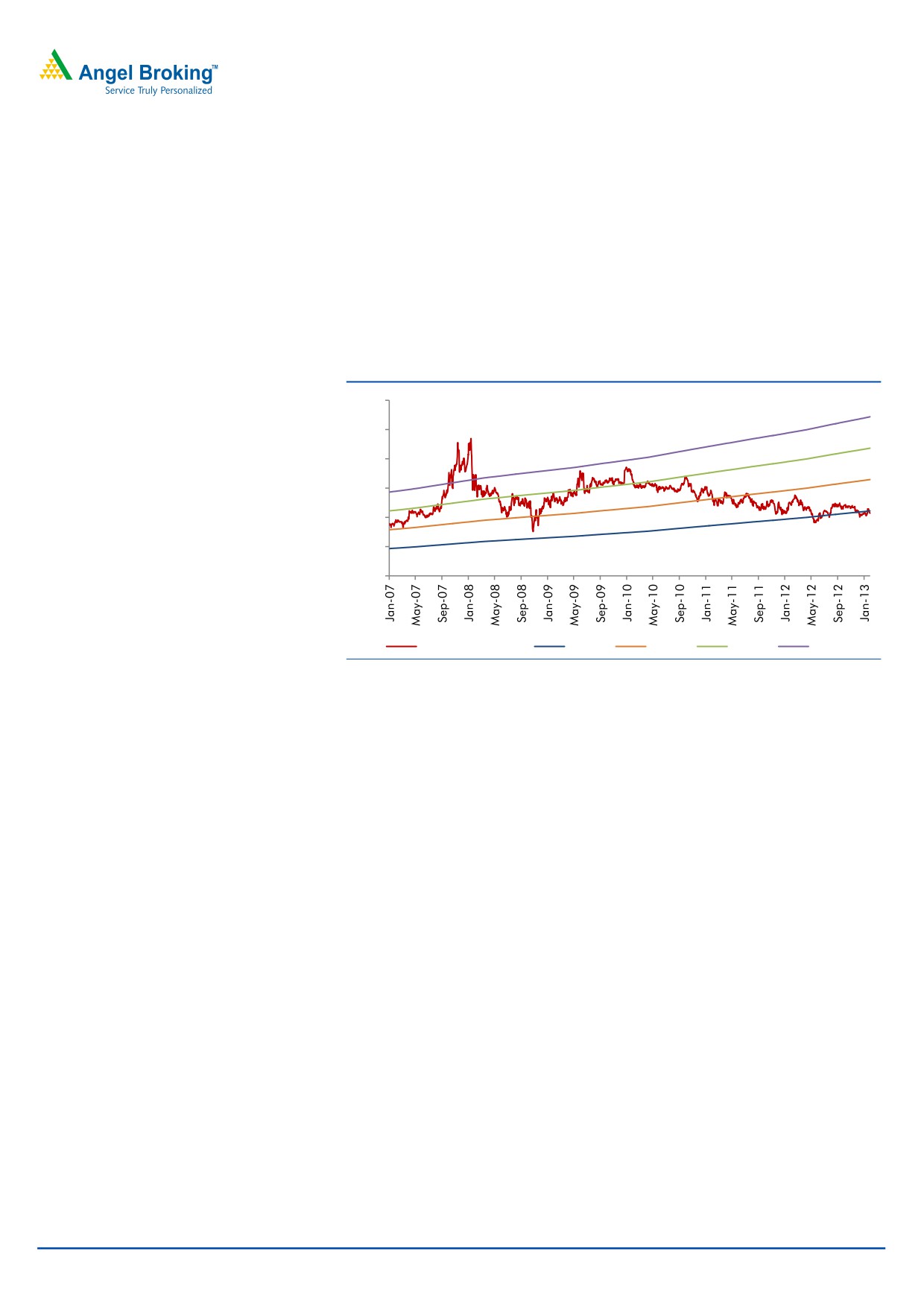

Outlook and Valuation

We expect NTPC to register a CAGR of 12.3% and 8.5% in its top-line and bottom-

line over FY2012-14E, respectively. At the offer price (which is at a 4.6% discount

to the price as on February 06, 2013), the stock would trade at 1.3x FY2014E

P/BV. Given the attractive valuation (stock trading at

1.3x FY2014E

P/BV compared to its three year trading range of 1.5x to 2.3x and median of

1.8x), we recommend Subscribe on the issue. We have assigned a multiple of

1.5x to arrive at a target price of `163.

Exhibit 4: One-year forward P/BV

350

300

250

200

150

100

50

Share Price (`)

1.5x

2.0x

2.5x

3.0x

Source: BSE, Company, Angel Research

Company Background

Established in 1975, NTPC is India's largest power generation company. NTPC has

an installed capacity of 39,674MW (including 4,864MW under JVs), spread across

28 power stations. The company's capacity has grown by

9,610MW over

FY2007-12. The company envisions being a 75,000MW company by FY2017.

NTPC enjoys healthy operational efficiency and has consistently reported high PLF

of ~90% compared to all-India PLF of ~75%.

February 6, 2013

4

Offer for Sale | Power sector

Profit and loss statement (Consolidated)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012

FY2013E

FY2014E

Total Operating Income

44,245

48,231

57,607

64,958

72,809

81,951

% chg

14.5

9.0

19.4

12.8

12

13

Total Expenditure

33,702

35,156

44,833

50,768

55,793

62,183

Net Raw Materials

27,347

30,188

36,422

43,312

47,763

53,268

Other Mfg costs

3,823

2,446

5,488

4,207

4,570

5,143

Personnel

2,533

2,523

2,922

3,250

3,460

3,772

EBITDA

10,544

13,075

12,775

14,190

17,016

19,767

% chg

(7.6)

24.0

(2.3)

11.1

19.9

16

(% of Net Sales)

23.8

27.1

22.2

21.8

23.4

24.1

Depreciation& Amortisation

2,495

2,894

2,720

3,107

3,736

4,366

EBIT

8,049

10,180

10,055

11,083

13,280

15,402

% chg

(12.6)

26.5

(1.2)

10.2

20

16

(% of Net Sales)

18

21

17

17

18

19

Interest & other Charges

2,144

2,078

1,726

2,135

2,935

3,496

Other Income

3,402

2,947

2,401

3,873

2,984

2,934

Share in profit of Associates

-

-

-

-

-

-

Recurring PBT

9,307

11,049

10,730

12,821

13,329

14,840

Extraordinary Expense/(Inc.)

-

-

-

-

-

PBT (reported)

9,307

11,049

10,730

12,821

13,329

14,840

Tax

1,215

2,211

3,044

3,323

3,279

3,651

(% of PBT)

13.1

20.0

28.4

25.9

25

25

PAT (reported)

8,092

8,838

7,686

9,499

10,050

11,189

Less Minority Interest

-

(0.0)

(5.2)

1.9

2

2

PAT After Minority Interest

8,092

8,838

7,691

9,497

10,048

11,187

% chg

8.3

9.2

(13.0)

23.5

5.8

11.3

(% of Net Sales)

18.3

18.3

13.4

14.6

13.8

13.7

Basic EPS (`)

9.8

10.7

9.3

11.5

12.2

13.6

Fully Diluted EPS (`)

9.8

10.7

9.3

11.5

12.2

13.6

% chg

8.3

9.2

(13.0)

23.5

5.8

11.3

Note: Some of the figures from FY2011 onwards are reclassified; hence not comparable with

previous year numbers

February 6, 2013

5

Offer for Sale | Power sector

Balance Sheet (Consolidated)

Y/E March

FY2009 FY2010E FY2011 FY2012 FY2013E FY2014E

SOURCES OF FUNDS

Equity Share Capital

8,246

8,246

8,246

8,246

8,246

8,246

Reserves& Surplus

51,706

55,993

61,053

67,587

73,968

81,488

Shareholders Funds

59,951

64,239

69,298

75,833

82,214

89,734

Minority Interest

166

279

485

596

596

596

Total Loans

38,823

43,844

47,099

55,002

66,002

76,002

Deferred Tax Liability

0

230

672

764

764

764

Other long term liablities

2,469

1,792

1,792

1,792

Total Liabilities

98,940

108,592

120,023

133,987

151,368

168,888

APPLICATION OF FUNDS

Gross Block

64,741

71,527

79,210

88,882

106,882

124,882

Less: Acc. Depreciation

29,776

32,723

34,346

37,749

41,485

45,850

Net Block

34,966

38,804

44,863

51,133

65,397

79,031

Capital Work-in-Progress

30,929

37,682

41,092

50,397

54,397

57,397

Goodwill

1

1

1

1

1

1

Investments

11,696

11,778

8,357

6,545

5,545

4,545

Current Assets

33,486

33,215

41,836

45,811

46,791

49,583

Cash

17,250

16,053

17,860

18,092

15,649

14,448

Loans & Advances

9,006

6,549

18,319

16,861

18,971

21,435

Other

7,230

10,614

5,657

10,859

12,171

13,700

Current liabilities

12,137

12,908

16,590

21,275

22,138

23,044

Net Current Assets

21,349

20,307

25,246

24,536

24,653

26,539

Other non CA

-

20

463

1,375

1,375

1,375

Total Assets

98,940

108,592

120,023

133,987

151,368

168,888

Note: Some of the figures from FY2011 onwards are reclassified; hence not comparable with

previous year numbers

February 6, 2013

6

Offer for Sale | Power sector

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2009 FY2010 FY2011 FY2012 FY2013E FY2014E

Profit before tax

9,307

11,049

12,392

13,137

13,329

14,840

Depreciation

2,495

2,894

2,720

3,107

3,736

4,366

Chg in WC & other adj.

(2,782)

408

(3,132)

941

(2,560)

(3,088)

Less: Other income

3,402

2,947

503

3,873

2,984

2,934

Direct taxes paid

2,566

2,799

3,044

3,323

3,279

3,651

Cash Flow from Operations

3,052

8,606

8,433

9,989

8,242

9,533

(Inc)/ Decin Fixed Assets

(11,344)

(14,009)

(10,550)

(19,477)

(22,000)

(21,000)

(Inc)/ Dec in Investments

1,751

(82)

3,820

1,612

1,000

1,000

Other income

3,402

2,947

503

3,873

2,984

2,934

Cash Flow from Investing

(6,192)

(11,144)

(6,226)

(13,992)

(18,016)

(17,066)

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

8,508

5,022

3,255

7,903

11,000

10,000

Dividend Paid (Incl. Tax)

3,478

3,682

3,654

3,669

3,669

3,669

Others

-

-

-

-

-

-

Cash Flow from Financing

5,030

1,340

(400)

4,234

7,331

6,331

Inc./(Dec.) in Cash

1,890

(1,198)

1,807

231

(2,443)

(1,202)

Opening Cash balances

15,361

17,250

16,053

17,860

18,092

15,649

Closing Cash balances

17,250

16,053

17,860

18,092

15,649

14,448

Note: Some of the figures from FY2011 onwards are reclassified; hence not comparable with

previous year numbers

February 6, 2013

7

Offer for Sale | Power sector

Key ratios

Y/E March

FY2009

FY2010

FY2011

FY2012

FY2013E

FY2014E

Valuation Ratio (x)

P/E (on FDEPS)

14.8

13.5

15.5

12.6

11.9

10.7

P/CEPS

11.3

10.2

11.5

9.5

8.7

7.7

P/BV

2.0

1.9

1.7

1.6

1.5

1.3

Dividend yield (%)

2.9

3.1

3.1

3.1

3.1

3.1

EV/Sales

2.9

2.8

2.4

2.3

2.3

2.2

EV/EBITDA

12.3

10.4

11.0

10.6

9.7

9.0

EV / Total Assets

1.3

1.3

1.2

1.1

1.1

1.1

Per Share Data (`)

EPS (Basic)

9.8

10.7

9.3

11.5

12.2

13.6

EPS (fully diluted)

9.8

10.7

9.3

11.5

12.2

13.6

Cash EPS

12.8

14.2

12.6

15.3

16.7

18.9

DPS

4.2

4.5

4.4

4.4

4.4

4.4

Book Value

72.7

77.9

84.0

92.0

99.7

108.8

DuPont Analysis

EBIT margin

18.2

21.1

17.5

17.1

18.2

18.8

Tax retention ratio

86.9

80.0

71.6

74.1

75.4

75.4

Asset turnover (x)

0.6

0.6

0.6

0.6

0.6

0.6

ROIC (Post-tax)

9.3

9.4

7.4

7.5

8.0

8.0

Cost of Debt (Post Tax)

5.4

4.0

2.7

3.1

3.7

3.7

Leverage (x)

0.6

0.7

0.7

0.7

0.8

0.8

Operating ROE

11.7

12.9

10.6

10.7

11.3

11.6

Returns (%)

ROCE (Pre-tax)

8.8

9.8

8.8

8.7

9.3

9.6

Angel ROIC (Pre-tax)

17.1

19.3

17.4

17.5

18.1

17.3

ROE

14.2

14.2

11.5

13.1

12.7

13.0

Turnover ratios (x)

Asset Turnover (Gross Block)

0.7

0.7

0.8

0.8

0.7

0.7

Inventory / Sales (days)

26

26

24

23

22

22

Receivables (days)

29

41

28

24

36

35

Payables (days)

114

130

120

136

142

133

WC cycle (ex-cash) (days)

25

32

37

39

39

47

Solvency ratios (x)

Net debt to equity

0.4

0.4

0.4

0.5

0.6

0.7

Net debt to EBITDA

2.0

2.1

2.3

2.6

3.0

3.1

Interest Coverage (EBIT / Int.)

3.8

4.9

5.8

5.2

4.5

4.4

Note: Some of the figures from FY2011 onwards are reclassified; hence not comparable with

previous year numbers

February 6, 2013

8

Offer for Sale | Power sector

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

NTPC

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to -15%)

Sell (< -15%)

February 6, 2013

9

Offer for Sale | Power sector

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Bhavesh Chauhan

Sr. Analyst (Metals & Mining)

Viral Shah

Sr. Analyst (Infrastructure)

Sharan Lillaney

Analyst (Mid-cap)

V Srinivasan

Analyst (Cement, FMCG)

Yaresh Kothari

Analyst (Automobile)

Ankita Somani

Analyst (IT, Telecom)

Sourabh Taparia

Analyst (Banking)

Bhupali Gursale

Economist

Vinay Rachh

Research Associate

Amit Patil

Research Associate

Shareen Batatawala

Research Associate

Twinkle Gosar

Research Associate

Tejashwini Kumari

Research Associate

Technicals:

Shardul Kulkarni

Sr. Technical Analyst

Sameet Chavan

Technical Analyst

Sacchitanand Uttekar

Technical Analyst

Derivatives:

Siddarth Bhamre

Head - Derivatives

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Hiten Sampat

Sr. A.V.P- Institution sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Akshay Shah

Sr. Executive

Production Team:

Tejas Vahalia

Research Editor

Dilip Patel

Production

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE: INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

February 6, 2013

10