1QFY2012 Result Update | Education

July 22, 2011

NIIT

BUY

CMP

`56

Performance Highlights

Target Price

`69

(` cr)

1QFY12 4QFY10

% chg (qoq) 1QFY11

% chg (yoy)

Investment Period

12 Months

Net revenue

321.2

323.8

(0.8)

278.0

15.5

EBITDA

30.7

40.4

(23.9)

28.7

7.1

Stock Info

EBITDA margin (%)

9.6

12.5

(290)bp

10.3

(75)bp

Sector

Education

PAT

13.1

37.7

(65.1)

13.0

1.1

Market Cap (` cr)

922

Source: Company, Angel Research

Beta

0.8

52 Week High / Low

75/43

For 1QFY2012, NIIT reported a decent performance, which was in-line with our

expectations. Revenue growth was driven by all businesses, but operational

Avg. Daily Volume

147606

performance was dented due to the SLS business, which posted a 472bp yoy dip

Face Value (`)

2

in EBITDA margin. We have valued NIIT on an SOTP basis, arriving at a target

BSE Sensex

18,722

EV/EBITDA of 4.3x on FY2013E consolidated EBITDA of `214.4cr, and have

Nifty

5,634

added the company’s stake in NIIT Technologies (with a holding discount of

Reuters Code

NIIT.BO

25%). We maintain Buy on the stock.

Bloomberg Code

NIIT@IN

Quarterly highlights: Consolidated revenue came in at `321cr, up 15.5% yoy.

Revenue from ILS, SLS and CLS businesses increased by 15.7%, 5.0% and 18.4%

Shareholding Pattern (%)

yoy to `177.8cr, `40.3cr and `163.0cr, respectively. Blended EBITDA margin

Promoters

34.0

declined by 75bp yoy to 10.3% due to a 162bp and 472bp yoy margin decline in

MF / Banks / Indian Fls

10.4

ILS and SLS businesses to 9.6% and 12.2%, respectively. However, the CLS

FII / NRIs / OCBs

28.4

segment posted a 102bp yoy increase in its EBITDA margin to 8.9%.

Indian Public / Others

27.3

Outlook and valuation: The hiring environment in the Indian IT sector is

strengthening, as indicated by Indian IT players such as Infosys and TCS aiming

to collectively hire ~1,05,000 people in FY2012. Thus, we expect ILS to record

Abs. (%)

3m 1yr 3yr

strong growth of

16% yoy in FY2012, with strengthening of the hiring

Sensex

(4.5)

3.4

32.7

environment expected to result in demand for vocational courses. With developed

NIIT Ltd.

(1.6)

(18.3)

(39.5)

economies such as the US returning to growth, we expect discretionary spend

related to training outsourcing, learning products and managed training services

to turn robust and expect 7% yoy growth in the CLS business. At the CMP, the

stock is trading at EV/EBITDA of 4.0x FY2013E EBITDA, but the stake in NIIT

Technologies provides for a strong upside. Hence, we maintain Buy on the stock

with a target price of `69.

Key financials (Consolidated)

Y/E March (` cr)

FY2009 FY2010

FY2011

FY2012E

FY2013E

Net sales

1149

1199

1248

1415

1556

% chg

14.1

4.4

4.1

13.3

10.0

Net profit

70

70

92

92

114

% chg

(7.7)

0.6

31.2

0.0

23.7

EBITDA margin (%)

10.3

13.1

12.8

13.1

13.8

EPS (`)

4.2

4.3

5.6

5.6

6.9

Srishti Anand

P/E (x)

13.2

13.1

10.0

10.0

8.1

022-3935 7800 Ext: 6820

P/BV (x)

1.9

1.8

1.7

1.5

1.3

RoE (%)

14.6

13.9

16.5

15.0

16.6

RoCE (%)

6.5

9.0

8.0

10.1

12.4

Ankita Somani

EV/Sales (x)

0.9

0.9

0.9

0.7

0.6

022-3935 7800 Ext: 6819

EV/EBITDA (x)

9.1

7.2

6.7

5.5

4.0

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

NIIT | 1QFY2012 Result Update

Exhibit 1: 1QFY2012 performance

(` cr)

1QFY12

4QFY11

% chg (qoq) 1QFY11

% chg (yoy) FY2011 FY2010

% chg (yoy)

Net revenue

321.2

323.8

(0.8)

278.0

15.5

1,248.2

1,199.3

4.1

Operating expenses

290.4

283.4

2.5

249.3

16.5

1,089.0

1,042.6

4.5

EBITDA

30.7

40.4

(23.9)

28.7

7.1

159.2

156.7

1.6

Depreciation

22.7

21.4

6.1

20.3

11.8

85.5

75.1

13.8

EBIT

8.0

19.0

(57.7)

8.4

(4.3)

73.7

81.6

(9.7)

Other income

(6.4)

7.5

(7.4)

(18.1)

(32.9)

PBT

1.6

26.5

(93.8)

1.0

64.0

55.6

48.7

14.2

Income tax

(1.3)

2.6

(150.0)

(1.5)

(13.3)

8.9

10.8

(17.6)

PAT

2.9

23.9

(87.7)

2.5

17.6

46.7

37.9

23.2

Share of associates' net profit

10.2

13.8

10.5

45.3

32.2

Adj. PAT

13.1

37.7

(65.1)

13.0

1.1

92.0

70.1

31.2

EPS (`)

0.8

2.3

(65.1)

0.8

1.1

5.6

4.3

31.2

EBITDA margin (%)

9.6

12.5

(290)bp

10.3

(75)bp

12.8

13.1

(31)bp

EBIT margin (%)

2.5

5.9

(336)bp

3.0

(52)bp

5.9

6.8

(90)bp

PAT margin (%)

4.2

11.4

(720)bp

4.8

(63)bp

7.5

6.0

147bp

Source: Company, Angel Research

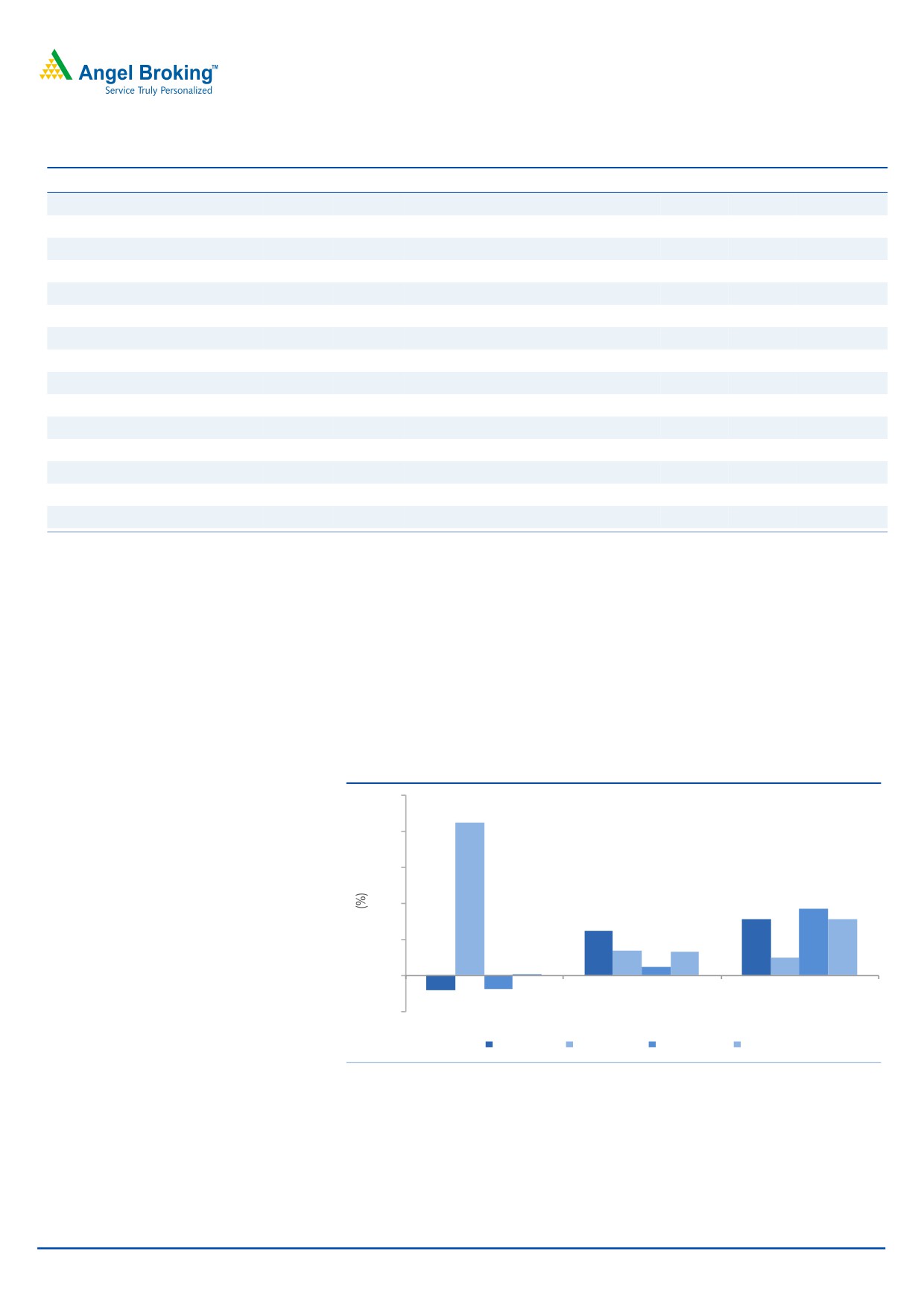

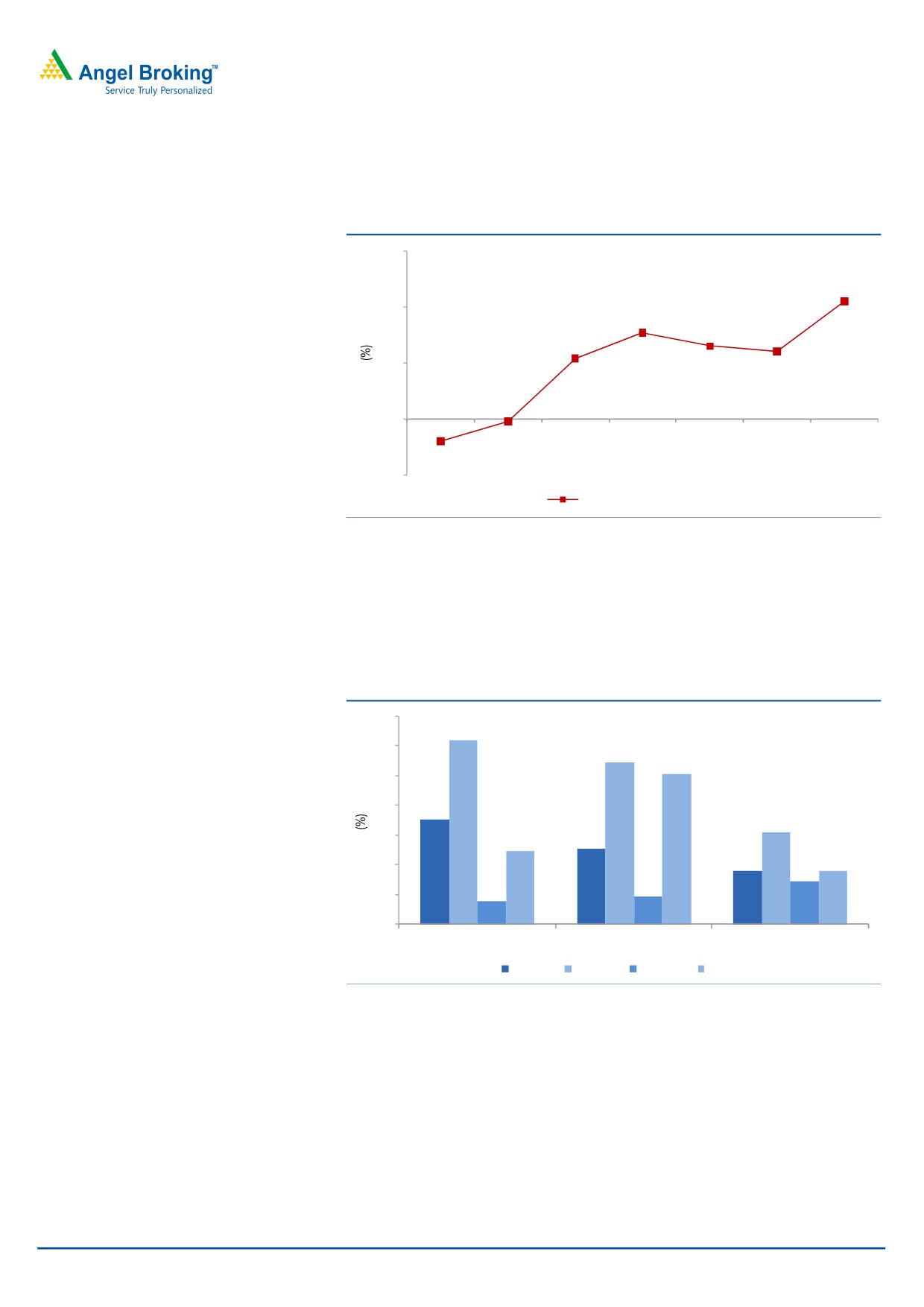

Modest revenue growth but margin declines

For 1QFY2012, NIIT reported revenue of `321.2cr (vs. our expectation of `305cr),

up 15.5% yoy. Corporate learning solutions (CLS) business emerged as the

primary growth driver for the company and reported 18.4% yoy growth in revenue,

which led to a 130bp yoy increase in its revenue share in NIIT’s overall revenue to

50.8%. Revenue from individual learning solution (ILS) and school learning

solutions (SLS) businesses grew by 15.7% and 5.0% yoy, respectively.

Exhibit 2: Revenue growth (Segment wise, yoy)

50

42.5

40

30

18.4

20

15.5

15.7

12.4

10

7.0

6.5

5.0

2.4

0.5

0

(4.0)

(3.9)

(10)

AMJ09

AMJ10

AMJ11

ILS

SLS

CLS

Consolidated

Source: Company, Angel Research

July 22, 2011

2

NIIT | 1QFY2012 Result Update

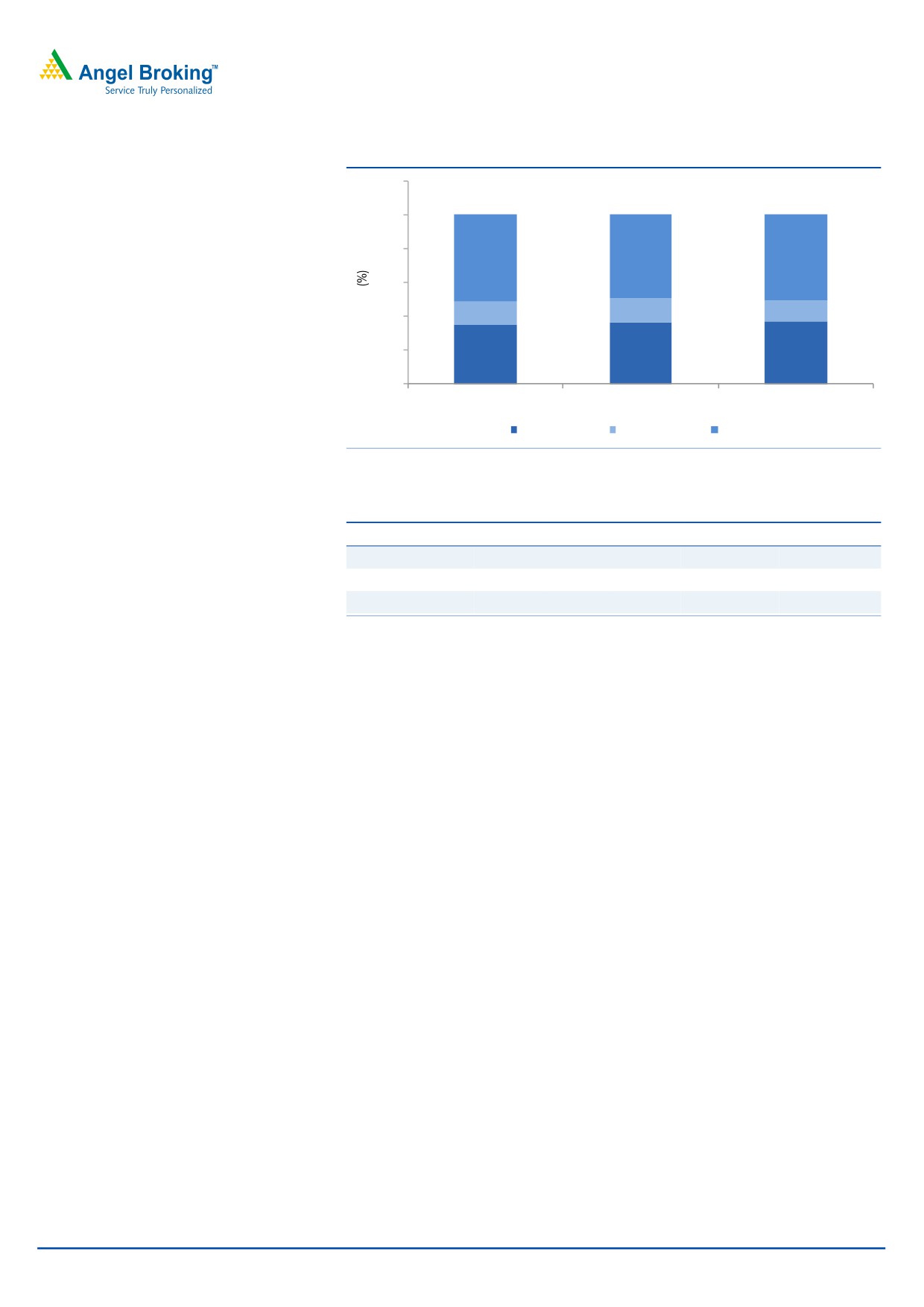

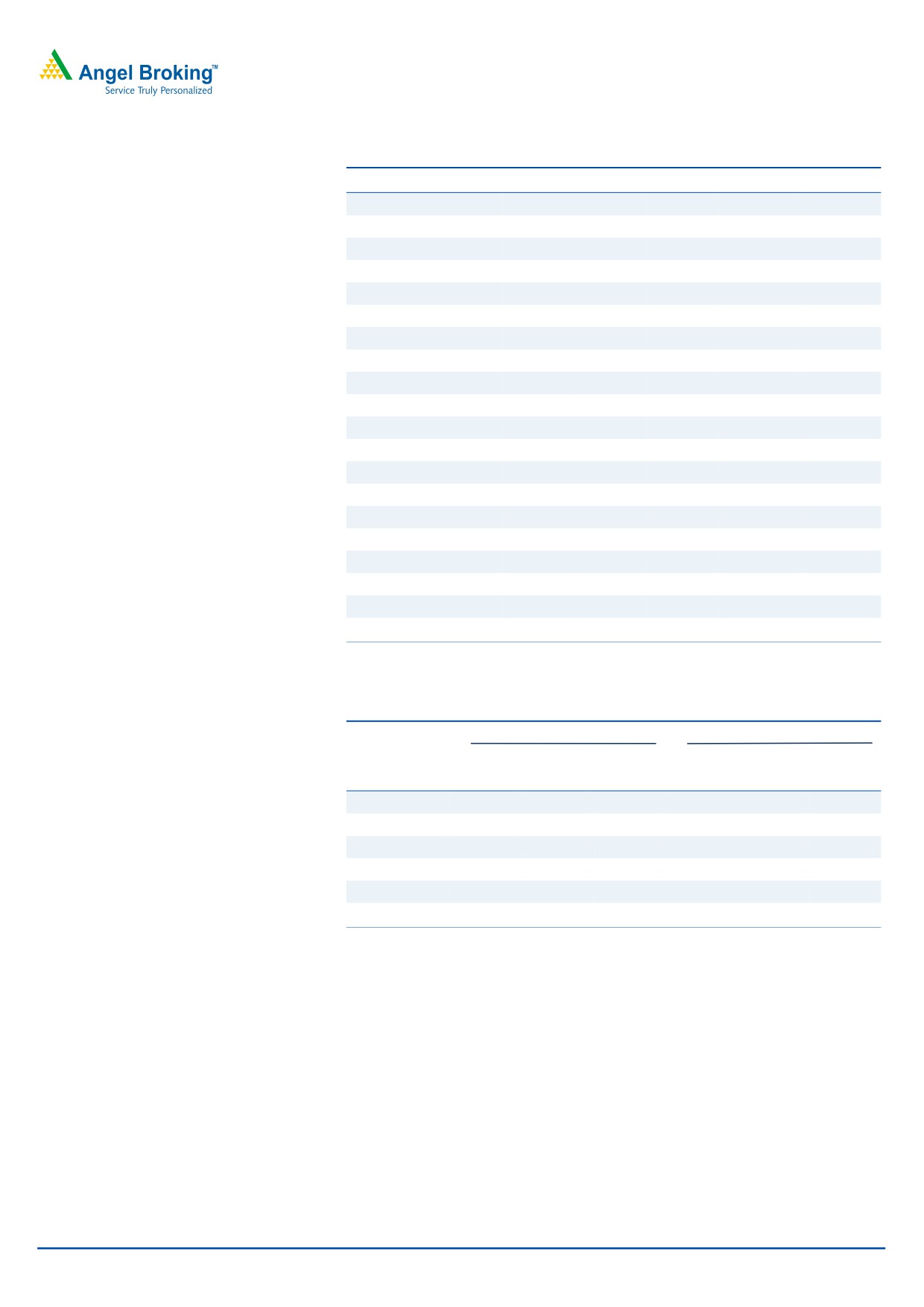

Exhibit 3: Revenue mix (Segment wise)

120

100

80

51.5

49.5

50.8

60

13.8

12.6

40

13.8

20

34.7

36.6

36.7

0

AMJ09

AMJ10

AMJ11

ILS

SLS

CLS

Source: Company, Angel Research

Exhibit 4: Revenue performance (Segment wise)

(` cr)

AMJ 11 AMJ 10 JFM 11

% chg (yoy)

% chg (qoq)

ILS

117.8

101.8

133.8

15.7

(11.9)

SLS

40.3

38.4

37.4

5.0

7.8

CLS

163.0

137.7

152.6

18.4

6.8

Source: Company, Angel Research

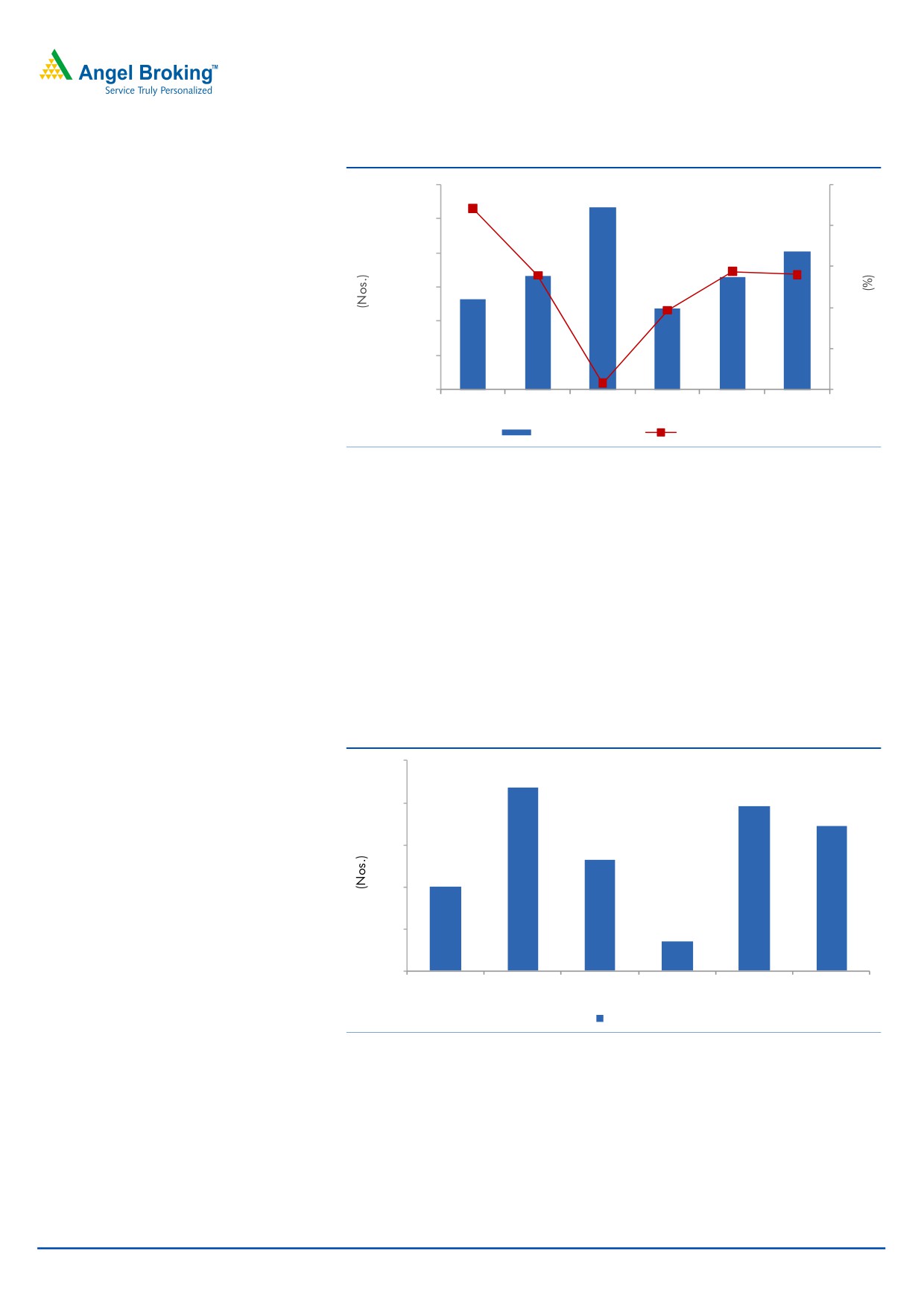

ILS: For 1QFY2012, revenue of the ILS business grew by 15.7% yoy to `177.8cr,

with global enrollments growing by 11% yoy to 1,40,455; career IT enrollments

increasing by 19% yoy; and strong surge witnessed in banking enrollments.

Also, placements continued to be robust, especially for the IT and banking sectors,

posting combined growth of 28% yoy. The pending order book of this segment

currently stands at

`138.4cr, with

70% of it being executable in the next

12 months. Also, cloud campus (new initiative by NIIT) was implemented in over

50 centres. EBITDA margin of the segment declined by 162bp yoy to 9.6% during

the quarter.

July 22, 2011

3

NIIT | 1QFY2012 Result Update

Exhibit 5: ILS - Enrolment growth

180,000

20

17.7

160,000

16

140,000

11.5

11.2

12

11.1

120,000

7.7

8

100,000

4

80,000

0.6

60,000

0

JFM10

AMJ10

JAS 10

OND 10

JFM 11

AMJ11

Enrollment

yoy growth (%)

Source: Company, Angel Research

SLS: Revenue of the SLS business grew by 5.0% yoy to `40.3 in 1QFY2012. During

the quarter, the company added 173 private schools with order intake of `97.6cr.

Revenue from non-government schools grew by 24% yoy and now contribute 41%

to the total SLS revenue. The pending order book of this segment stands at

`497.5cr, with 30% being executable in the next 12 months.

For 1QFY2012, EBITDA margin of the business declined ferociously by 472bp yoy

to 12.2% due to reorganisation going on in this segment as well as the company

gearing up for strategies adopted earlier. Management has indicated that the

margin of this business will witness an uptick in the coming quarters.

Exhibit 6: Trend in private school addition in the SLS segment

250

218

196

200

173

150

132

101

100

50

35

0

JFM10

AMJ10

JAS 10

OND 10

JFM 11

AMJ 11

Private schools

Source: Company, Angel Research

CLS: Revenue of the CLS business grew by 18.4% yoy to `163.0cr on the back of

robust volume growth of 21.0% yoy, driven by growth in managed training

services (56% yoy) and online learning products (22% yoy). Order intake for the

quarter stood at US$25.4mn, with the pending order book standing at

US$87.0mn, of which 61% is executable over the next 12 months.

July 22, 2011

4

NIIT | 1QFY2012 Result Update

EBITDA margin of this segment increased by 102bp yoy to 8.9% on account of

strong traction from managed services contacts.

Exhibit 7: Volume growth trend in CLS

30

21.0

20

15.3

13.0

12.0

10.8

10

(4.0)

(0.5)

0

OND09

JFM10

AMJ10

JAS 10

OND 10

JFM 11

AMJ 11

(10)

Volume growth (%)

Source: Company, Angel Research

Consolidated margin declines: Blended EBITDA margin declined by 75bp yoy to

10.3% (vs. our expectation of 9.8%) due to margin decline in ILS and SLS

businesses as well as increased business development expenses, as the company

expanded its sales force from 873 in 4QFY2011 to 985 in 1QFY2012.

Exhibit 8: EBITDA margin (Segment wise)

20

18.4

18

16.9

16.1

16

14

13.0

12.2

12

11.0

11.1

9.6

9.6

10

8.9

7.8

7.6

8

6

AMJ09

AMJ10

AMJ11

ILS

SLS

CLS

Consolidated

Source: Company, Angel Research

July 22, 2011

5

NIIT | 1QFY2012 Result Update

Outlook and valuation

The ILS and CLS businesses are emerging to be the company’s growth drivers.

We expect enrollment growth for ILS-IT to be stronger in FY2012, with strong

recruitment plans announced by Indian IT majors (including Infosys and TCS) and

initial gross hiring targets of

45,000 and

60,000 in FY2012, respectively.

We expect ILS to return to its strong growth momentum of 16% yoy in FY2012, with

strengthening of the hiring environment by the Indian IT players resulting in

demand for vocational courses. CLS, which was heavily impacted by the downturn,

has rebounded with respect to growth and has managed to bag a strong order

book. Demand for discretionary services, including training outsourcing, learning

products and managed training services, is gaining traction. Also, demand for new

business courses such as IFBI, Imperia and Uniqua is expected to strengthen with

the hiring environment turning positive in the management, commercial banking

and BPO space. In the SLS business, the company is witnessing strong traction

from non-GSA schools and has added 754 schools since 1QFY2011. Hence,

we expect the company to post a revenue CAGR of 11.6% over FY2011-13E,

whereas EBITDA growth is expected to outpace the same, reporting a 16.0% CAGR

due to improving business mix in CLS as well as growth in ILS enrollments.

NIIT is strategically moving towards turning asset-light by targeting more

annuity-based revenue. Management aims to do so by being selective in

government SLS contracts, which are highly capital-intensive and have long debtor

cycles (thus impacting returns), targeting more private schools in the SLS business.

Also, annuity contracts bagged in CLS (related to learning products and MTS) are

expected to accelerate revenue growth and improve margins. With the realignment

of its focus, management expects to improve the company’s profitability, reduce

debtor cycle and repay debt by `80cr-90cr in FY2012 itself.

July 22, 2011

6

NIIT | 1QFY2012 Result Update

Exhibit 9: Segmental expectations

(` cr)

FY2009

FY2010

FY2011

FY2012E

FY2013E

ILS

Revenue

432

457

517

601

675

yoy growth (%)

22.9

7.4

9.5

16.3

12.3

EBITDA

79

83

95

113

139

EBITDA margin (%)

18.3

18.2

18.4

18.8

20.6

SLS

Revenue

138

200

148

172

197

yoy growth (%)

36.7

44.6

(26.0)

16.4

14.0

EBITDA

21

30

17

17

18

EBITDA margin (%)

15.5

14.8

11.4

10.1

9.3

CLS

Revenue

579

542

584

641

684

yoy growth (%)

5.0

(6.3)

7.6

9.9

6.7

EBITDA

18

44

47

55

57

EBITDA margin (%)

3.2

8.1

8.1

8.5

8.3

Consolidated

Revenue

1,149

1,199

1,248

1,415

1,556

yoy growth (%)

14.1

4.4

4.1

13.3

10.0

EBITDA

119

157

159

185

214

EBITDA margin (%)

10.3

13.1

12.8

13.1

13.8

Source: Company, Angel Research

Exhibit 10: Change in estimates

FY2012E

FY2013E

Parameter

Earlier

Revised

Variation

Earlier

Revised

Variation

(` cr)

estimates estimates

(%)

estimates

estimates

(%)

Net revenue

1,401

1,415

1.0

1,545

1,556

0.7

EBITDA

185

185

(0.1)

213

214

0.4

Other income

(25)

(24)

(3.3)

(14)

(13)

(1.9)

PBT

66

67

0.5

96

97

0.4

Tax

20

18

(8.3)

30

30

(0.7)

PAT

91

92

1.3

113

114

0.5

Source: Company, Angel Research

July 22, 2011

7

NIIT | 1QFY2012 Result Update

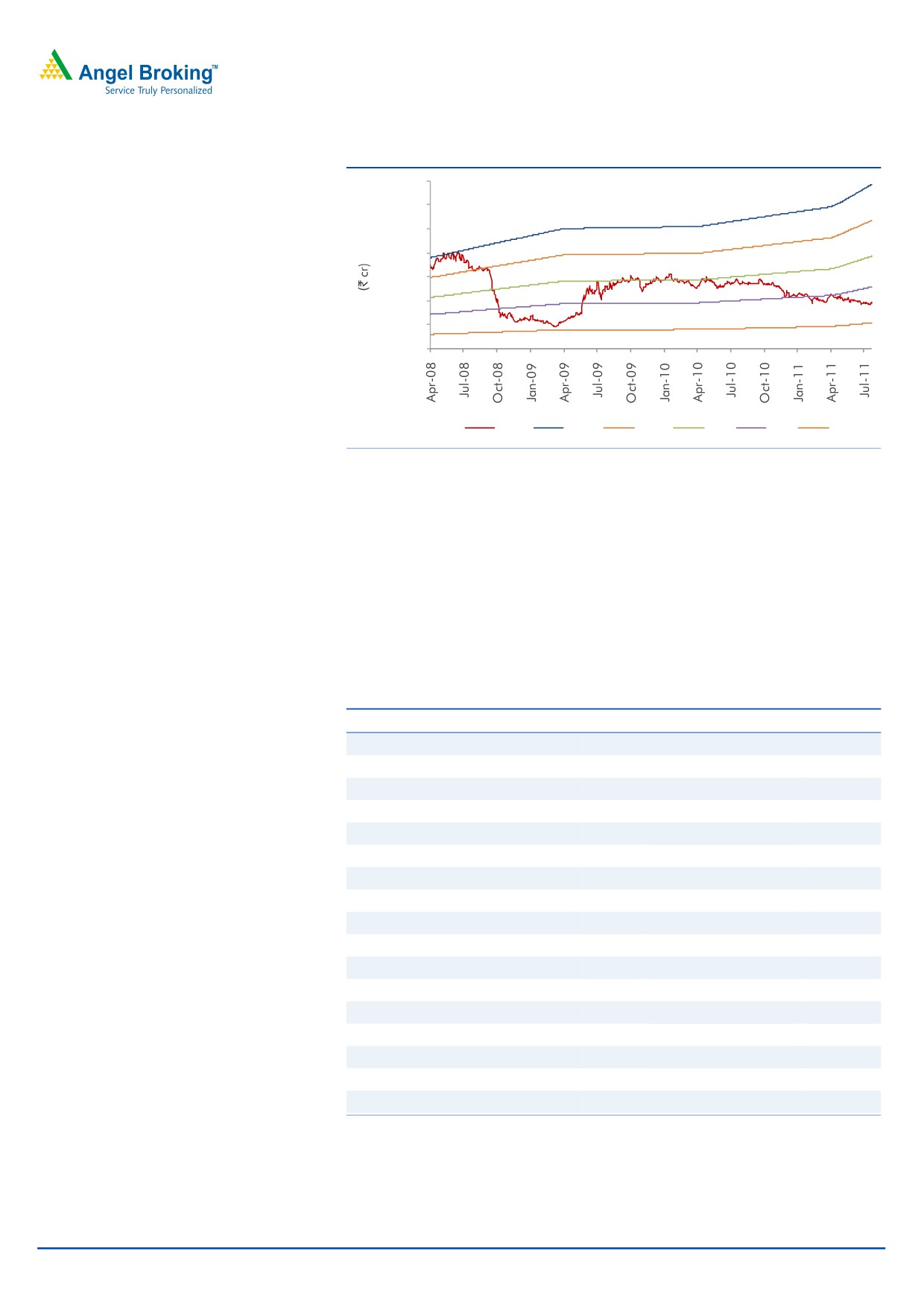

Exhibit 11: One-year forward EV/EBITDA

3,500

3,000

2,500

2,000

1,500

1,000

500

0

EV

16

13

9

6

3

Source: Company, Angel Research

Also, the company’s subsidiary, NIIT Technologies is witnessing a strong growth

momentum. At the CMP, the stock is trading at EV/EBITDA of 4.0x FY2013E

EBITDA, but the stake in NIIT Technologies provides for a strong upside. Hence,

we have valued NIIT on an SOTP basis, arriving at a target EV/EBITDA of 4.3x on

FY2013E consolidated EBITDA of `214.4cr, and have added the company’s stake

in NIIT Technologies (with a holding discount of 25%), arriving at a target price of

`69. We maintain Buy on the stock.

Exhibit 12: Valuation metric for NIIT (Based on FY2013E)

FY2013E (` cr)

EBITDA

Target EV/EBITDA (X)

Target EV

ILS

139.2

5.0

696.2

SLS

18.3

3.0

55.0

CLS

56.8

3.0

170.3

Target EV for NIIT

921.5

Debt

201.0

Cash & Cash equivalent

183.6

Target Mcap for NIIT

904.1

Value per share for NIIT (`)

55.0

Value due to NIIT Technologies

Current price (`)

222.4

Holding discount

25.0

No. of shares held by NIIT (cr)

1.5

Value of held equity

225.7

Value per share of held equity

13.7

Target price for NIIT Ltd.

68.7

Source: Company, Angel Research

July 22, 2011

8

NIIT | 1QFY2012 Result Update

Exhibit 13: Recommendation summary

Company

Reco.

CMP Tgt. price Upside Target

FY2013 FY2013E

FY2011-13E FY2013E FY2013E

(`)

(`)

(%) P/E (x)

EBITDA (%)

P/E (x)

EPS CAGR (%) RoCE (%)

RoE (%)

3iInfotech

Neutral

43

-

-

-

21.5

3.6

(4.3)

12.0

15.1

Educomp

Buy

376

522

39.0

10

46.7

7.3

17.7

16.4

17.0

Everonn

Neutral

555

-

-

-

33.5

13.1

27.7

15.5

16.7

HCL Tech

Buy

504

591

17.2

14

18.5

11.9

30.8

18.9

26.9

Infosys

Accumulate

2,825

3,200

13.3

20

30.6

17.7

15.7

24.7

22.7

Infotech Entp.

Neutral

137

-

-

-

16.1

8.4

13.9

15.2

13.4

KPIT Cummins

Accumulate

192

206

7.3

12

16.1

11.4

21.8

20.6

17.7

MindTree

Accumulate

400

445

11.4

11

13.3

9.9

27.5

16.9

15.4

Mphasis

Accumulate

444

499

12.3

11

17.2

10.0

9.2

16.8

16.8

NIIT^

Buy

56

69

23.5

-

13.8

8.1

11.2

12.4

16.6

Persistent

Buy

367

424

15.6

11

19.5

9.5

5.1

16.6

15.4

TCS

Buy

1,133

1,368

20.8

22

28.9

18.2

18.4

30.2

31.3

Tech Mahindra

Accumulate

748

790

5.6

9*

18.3

13.3

6.8

14.9

15.6

Wipro

Neutral

406

-

-

-

18.7

15.5

9.9

13.8

19.8

Source: Company, Angel Research; Note:*Standalone basis (excluding Mahindra Satyam, ^ Valued on SOTP basis

July 22, 2011

9

NIIT | 1QFY2012 Result Update

Profit and loss statement (consolidated)

Y/E March (` cr)

FY2009 FY2010 FY2011 FY2012E FY2013E

Net sales

1,149

1,199

1,248

1,415

1,556

Operating expenses

1,030

1,043

1,089

1,230

1,341

EBITDA

119

157

159

185

214

% of net sales

10.3

13.1

12.8

13.1

13.8

Dep. and amortization

65

75

86

94

104

% of net sales

5.6

6.3

6.8

6.7

6.7

EBIT

54

82

74

91

110

% of net sales

4.7

6.8

5.9

6.4

7.1

Other income

(5)

(33)

(18)

(24)

(13)

Profit before tax

49

49

56

67

97

Provision for tax

10

11

9

18

30

% of PBT

21.1

22.2

16.0

26.9

30.8

PAT

39

38

47

49

67

Share in profit of associates

31

32

45

43

47

Profit after minority interest

70

70

92

92

114

EPS (`)

4.2

4.3

5.6

5.6

6.9

July 22, 2011

10

NIIT | 1QFY2012 Result Update

Balance sheet (consolidated)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012E

FY2013E

Capital employed

Equity capital

33

33

33

33

33

ESOP outstanding

0

-

-

-

-

Reserves and surplus

416

463

517

573

643

Currency translation reserve

28

8

7

8

8

Net worth

477

504

557

614

684

Secured loans

252

254

265

285

201

Unsecured loans

96

151

101

-

-

Total debt

348

405

366

285

201

Minority interest

1

2

3

3

3

Total capital employed

826

911

925

902

888

Capital deployed

Gross block

784

814

877

937

997

Accumulated depreciation

273

322

397

491

596

Net block

511

492

480

446

401

Capital WIP

62

45

62

40

40

Total fixed assets

573

536

542

486

441

Investments

107

127

164

80

75

Inventories

10

13

15

10

10

Sundry debtors

290

340

390

399

413

Cash at bank

75

62

53

109

184

Loans and advances

150

154

135

170

199

Other current assets

44

70

117

70

66

Sundry creditors

241

211

234

236

257

Other liabilities

171

168

243

177

206

Provisions

45

42

45

42

54

Net deferred tax assets

35

30

31

34

17

Miscellaneous expense

-

-

-

-

-

Total capital deployed

826

911

925

902

888

July 22, 2011

11

NIIT | 1QFY2012 Result Update

Cash flow statement (consolidated)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012E

FY2013E

Pre tax profit from oper.

29

45

39

57

76

Depreciation

65

75

86

94

104

Pre tax cash from oper.

94

120

125

151

180

Other inc./prior period ad

20

4

2

10

21

Net cash from operations

114

124

126

161

201

Tax

10

11

9

18

30

Share of profit from ass.

31

32

45

43

47

Cash profits

135

145

163

186

218

(Inc)/dec in sundry debtors

(86)

(50)

(49)

(9)

(14)

(Inc)/dec in current assets

(14)

(26)

(48)

48

3

(Inc)/dec in inventories

3

(3)

(3)

5

-

(Inc)/dec in loans and adv.

(20)

(4)

19

(34)

(29)

Inc/(dec) in sundry creditors

56

(31)

24

1

21

Inc/(dec) in other current liab.

40

(5)

78

(68)

41

Net trade working capital

(20)

(118)

20

(58)

22

Cash flow from oper. actv.

114

27

183

128

240

(Inc)/dec in fixed assets

(240)

(38)

(91)

(38)

(60)

(Inc)/dec in investments

(17)

(21)

(37)

84

5

(Inc)/dec in deferred tax asset

(10)

5

(1)

(3)

17

Cash flow from investing actv.

(267)

(55)

(129)

43

(38)

Inc/(dec) in debt

142

56

(39)

(81)

(84)

Inc/(dec) in equity/premium

31

(16)

5

2

-

Inc/(dec) in minority interest

(1)

2

1

-

-

Dividends

25

27

30

35

44

Cash flow from fin. activities

147

15

(63)

(115)

(128)

Cash generated/(utilised)

(5)

(13)

(9)

57

74

Cash at start of the year

80

75

62

53

109

Cash at end of the year

75

62

53

109

184

July 22, 2011

12

NIIT | 1QFY2012 Result Update

Key ratios

Y/E March

FY2009

FY2010

FY2011

FY2012E

FY2013E

Valuation ratio (x)

P/E (on FDEPS)

13.2

13.1

10.0

10.0

8.1

P/CEPS

6.8

6.3

5.2

4.9

4.2

P/BVPS

1.9

1.8

1.7

1.5

1.3

Dividend yield (%)

2.3

2.5

2.8

3.3

4.1

EV/Sales

0.9

0.9

0.9

0.7

0.6

EV/EBITDA

9.1

7.2

6.7

5.5

4.0

EV/Total assets

1.3

1.2

1.2

1.1

1.0

Per share data (`)

EPS

4.2

4.3

5.6

5.6

6.9

Cash EPS

8.2

8.8

10.8

11.3

13.3

Dividend

1.3

1.4

1.6

1.8

2.3

Book value

29.0

30.6

33.8

37.3

41.6

Dupont analysis

Tax retention ratio (PAT/PBT)

0.8

0.8

0.8

0.7

0.7

Cost of debt (PBT/EBIT)

0.9

0.6

0.8

0.7

0.9

EBIT margin (EBIT/sales)

0.0

0.1

0.1

0.1

0.1

Asset turnover ratio (sales/assets)

1.4

1.3

1.3

1.6

1.8

Leverage ratio (assets/equity)

1.7

1.8

1.7

1.5

1.3

Operating ROE

8.1

7.5

8.4

7.9

9.8

Return ratios (%)

RoCE (pre-tax)

6.5

9.0

8.0

10.1

12.4

Angel RoIC

9.2

12.1

11.4

13.5

18.6

RoE

14.6

13.9

16.5

15.0

16.6

Turnover ratios(x)

Asset turnover (fixed assets)

2.0

2.2

2.3

2.9

3.5

Receivables days

79

96

107

103

97

Payable days

76

79

75

70

70

July 22, 2011

13

NIIT | 1QFY2012 Result Update

Research Team Tel: 022 - 3935 7800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

NIIT Ltd

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below `lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to 15%)

Sell (< -15%)

July 22, 2011

14