Market Outlook

July 27, 2015

Dealer’s Diary

Domestic Indices

Chg (%)

(Pts)

(Close)

Indian markets are expected to open in red tracking SGX Nifty.

BSE Sensex

(0.9)

(259)

28,112

US markets corrected, on account of sell-off seen across materials and energy

Nifty

(0.8)

(68)

8,522

companies, which were impacted by continued fall in the oil and metal prices. On

MID CAP

(0.6)

(68)

11,148

Friday, Amazon surprised the street by reporting profit, and Biogen stock plunged

SMALL CAP

(0.6)

(68)

11,668

22%, after posting poor earnings and lowering of guidance numbers for 2015.

BSE HC

(0.3)

(57)

16,837

BSE PSU

(0.9)

(66)

7,740

U.K. stocks were slammed on Friday, with mining shares hit hard, and Diageo Plc

BANKEX

(1.2)

(259)

21,374

shares correcting on the news of U.S. regulatory investigation in to the liquor maker.

AUTO

(1.1)

(217)

18,953

Days top gainer on FTSE 100 was Vodafone Plc, after it said its seeing continued

METAL

(1.3)

(113)

8,772

recovery in its key European markets, even as quarterly revenue fell.

OIL & GAS

(0.9)

(88)

10,155

Markets continued their downward trend, with a loss of over half a percent on

BSE IT

(0.6)

(65)

11,005

Friday. Correction across Auto, Banking and Cap-good stocks pulled down the

Global Indices

Chg (%)

(Pts)

(Close)

broader indices.

Dow Jones

(0.9)

(163)

17,569

News & Result Analysis

NASDAQ

(1.1)

(58)

5,089

FTSE

(1.1)

(75)

6,580

Power Finance Corp. (PFC) OFS- SUBSCRIBE

Lupin Acquires Specialty Product Portfolio in Germany

Nikkei

(0.7)

(139)

20,545

Result Review: Hitachi Home, Relaxo Footwear, Visaka Industries

Hang Sang

(1.1)

(270)

25,129

Result Preview: Subros Ltd, Tech Mahindra

Straits Times

(0.1)

(4)

3,353

Refer detailed news & result analysis on the following page

Shanghai Com

(1.3)

(53)

4,071

Markets Today

The trend deciding level for the day is 28,200 / 8,541 levels. If NIFTY trades above

Indian ADR

Chg (%)

(Pts)

(Close)

this level during the first half-an-hour of trade then we may witness a further rally up

INFY

(0.5)

(0.1)

$17.2

to 28,315 - 28,518 / 8,569 - 8,617 levels. However, if NIFTY trades below

WIT

(2.6)

(0.3)

$12.3

28,200 / 8,541 levels for the first half-an-hour of trade then it may correct towards

IBN

(3.5)

(0.3)

$9.7

27,997 - 27,881 / 8,494 - 8,466 levels.

HDB

(0.9)

(0.5)

$61.5

Indices

S2

S1

PIVOT

R1

R2

Advances / Declines

BSE

NSE

SENSEX

27,881

27,997

28,200

28,315

28,518

Advances

1,254

573

NIFTY

8,466

8,494

8,541

8,569

8,617

Declines

1,622

947

Net Inflows (July 24, 2015)

Unchanged

97

60

` cr

Purch

Sales

Net

MTD

YTD

Volumes (` cr)

FII

3,860

3,554

306

7,757

143,137

MFs

805

984

(179)

1,634

55,244

BSE

3,422

NSE

17,808

FII Derivatives (July 25, 2015)

` cr

Purch

Sales

Net

Open Interest

Index Futures

1,663

1,698

(36)

21,041

Stock Futures

5,413

5,735

(322)

51,246

Gainers / Losers

Gainer

Loser

Company

Price (`)

chg (%)

Company

Price (`)

chg (%)

TATAELXSI

1,594

12.9

KAILASH

7

(10.0)

UNITDSPR

3,788

5.5

JPASSOCIAT

11

(9.3)

IBREALEST

58

5.2

RALLIS

235

(7.1)

RTNPOWER

8

4.5

INFRATEL

419

(7.0)

GRUH

244

4.0

PVR

803

(6.3)

Market Outlook

July 27, 2015

Power Finance Corp. (PFC) OFS- SUBSCRIBE

Power sector reforms to benefit PFC: Government is geared up to resolve

issues relating to power sector, which will directly benefit PFC, not just in the form

of better credit off-take, but also improved asset quality and profitability. Apart

from its focus on increasing generation and transmission capacities, the

government is also concentrating on addressing the bottleneck faced by power

producers due to shortage of coal. It is in the process of allocating coal mines

directly to state and central PSU and through e-auction to private players, which

would address coal supply issue. For PFC, it removes uncertainty, as 16 projects

with exposure of `36,237cr were linked to de-allocation of coal. Rationalization of

tariff by states and intent of government to reduce AT&C losses from 25% to 15%

by FY22 is positive development to improve health of SEB. We expect PFC to be

direct beneficiary of improving performance of power sector.

High visibility on Credit growth: Outstanding sanctions stand at `1.4lakhcr,

which is 3.2x of disbursement done during FY15. This alone provides loan growth

visibility in the next few years. Improvement in sector outlook will lead to further

improvement in loan book for the company. PFC is well capitalized with Tier I ratio

at 17.6%, which would enable the company to grow without diluting equity.

Moreover banks being cautious to lend to power sector and having to comply with

strict credit concentration norms, it creates even more space for specialized lenders

such as PFC to grow.

However RBI provisioning requirement for new loans restructured from April 2015

at 5% and for existing stock of restructured assets, gradual increase of provisions

from 2.75% to 5% in FY2018, will increase credit cost for the company.

Attractive valuations: At the offer-for-sale (OFS) price of `254, the stock is

trading at 0.77x the consensus FY2017E per book value of `329. Considering the

5% discount (`241), the stock is available at a P/B ratio of 0.73x consensus

FY2017E book, which is attractive. Hence, we recommend investors to apply for

PFC shares in the OFS.

Key financials

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015P

NII

3958

5,830

7,694

8,782

% chg

20.4

47.3

32.0

14.1

Net profit

3059

4,438

5,462

6,004

% chg

15.6

45.1

23.1

9.9

NIM (%)

3.5

4.0

4.4

4.4

EPS (`)

23.2

33.6

41.4

45.5

P/E (x)

12.1

8.3

6.8

6.1

P/ABV (x)

1.9

1.6

1.4

1.2

RoA (%)

2.5

2.9

3.0

2.8

RoE (%)

17.0

20.0

21.3

20.0

Company background

Incorporated in 1986, Power Finance Corporation (PFC) was formed as a part of

the government’s initiative to enhance funding of power projects in India. The

company plays a major role in channelizing investment into the power sector and

acts as a vehicle for development of this sector. Apart from funding, it works

closely with state governments & state power sector utilities and assists them to

undertake reforms within their organizations.

Market Outlook

July 27, 2015

PFC enjoys the highest credit rating in the Indian market; while in international

markets, the company is rated at par with the Indian Sovereign rating. The

company is registered as a non-banking financial company (NBFC) by the RBI and

was conferred with the status of Nav-Ratna PSU by the Government of India on

June 22, 2007. The company was conferred with the status of NBFCND-IFC (Non

Banking Finance Company-Non Deposit Taking-Infrastructure Finance Company)

on July 28, 2010.

Details of the issue

The Promoter (Government of India), proposes to sell 6,60,02,035 equity shares

of face value of `10 each representing 5% of the total paid up equity share capital

of the company. PFC has fixed the OFS floor price at `254 per share (at a ~2%

discount to its closing price as on July 24, 2015). Retail shareholders will get an

additional discount of 5% on cut-off price. 20% of the issue is reserved for retail

investors.

Pre-Issue

Post-Issue

Particulars

No. of shares

(%)

No. of shares

(%)

Promoter and promoter group

96,09,26,401

72.8

89,49,24,366

67.8

Total public holding

35,91,14,303

27.2

42,51,16,338

32.2

Total

1,32,00,40,704

100

1,32,00,40,704

100

Income statement

Y/E. March (` cr)

FY11

FY12

FY13

FY14

FY15P

Interest Earned

9,776

12,621

16,923

20,980

24,262

Interest Expended

6,490

8,663

11,093

13,286

15,480

Net Interest Income

3,287

3,958

5,830

7,694

8,782

- YoY Growth (%)

13.0

20.4

47.3

32.0

14.1

Other Income

437.8

475

395

649

750

- YoY Growth (%)

72.0

8.5

(16.9)

64.4

15.6

Operating Income

3,725

4,433

6,225

8,343

9,532

- YoY Growth (%)

17.8

19.0

40.4

34.0

14.3

Operating Expenses

107

144

150

249

242

- YoY Growth (%)

(9.3)

34.4

4.2

65.4

(2.5)

Pre - Provision Profit

3,617

4,289

6,074

8,094

9,290

- YoY Growth (%)

18.8

18.6

41.6

33.3

14.8

Provision and

32

143

81

470

844

Contingencies

- YoY Growth (%)

350

(43)

481

80

Profit Before Tax

3,586

4,146

5,994

7,624

8,446

- YoY Growth (%)

17.7

15.6

44.6

27.2

10.8

Provision for Taxation

938

1,087

1,556

2,163

2,441

- as a % of PBT

26.2

26.2

26.0

28.4

28.9

PAT

2,647

3,059

4,438

5,462

6,004

- YoY Growth (%)

11.3

15.6

45.1

23.1

9.9

Market Outlook

July 27, 2015

Balance sheet

Y/E. March (` cr)

FY11

FY12

FY13

FY14

FY15P

Share Capital

1,148

1,320

1,320

1,320

1,320

Res. & Surplus

14,093

19,473

22,360

26,202

31,091

Borrowings

85,599

1,10,126

1,39,473

1,59,215

1,87,795

- Growth (%)

26.3

28.7

26.6

14.2

18.0

Other Liab. & Prv.

3,803

4,676

5,968

7,309

8,517

Total Liabilities

104642

135595

1,69,121

1,94,047

2,28,723

Investments

27

27

27

27

24

Advances

97,622

1,24,556

1,58,380

1,87,098

2,14,244

- Growth (%)

22.2

27.6

27.2

18.1

14.5

Fixed Assets

77

77

75

72

104

Other Assets

6,917

10,934

10,639

6,849

14,351

Total Assets

104643

135594

1,69,121

1,94,047

2,28,723

Key Ratios

Year end March

FY11

FY12

FY13

FY14

FY15P

Per Share Data (`)

EPS

23.1

23.2

33.6

41.4

45.5

ABVPS ( 75% Coverage for NPAs)

131.6

150.9

173.9

203.4

235.7

DPS

5.2

6.0

7.0

9.0

9.3

Profitability ratios (%)

Yield on earning assets

10.8

11.1

11.7

12.0

12.1

Cost of funds

8.5

8.9

8.9

8.9

8.9

NIMs

3.6

3.5

4.0

4.4

4.4

ROA

2.8

2.5

2.9

3.0

2.8

ROE

18.5

17.0

20.0

21.3

20.0

Asset Quality (%)

Gross NPAs

0.24

1.09

0.72

0.66

1.10

Net NPAs

0.20

0.98

0.64

0.53

0.88

Valuation Ratios

PER (x)

12.1

12.1

8.3

6.8

6.1

P/ABVPS (x)

2.1

1.9

1.6

1.4

1.2

Dividend Yield

1.9

2.1

2.5

3.2

3.3

DuPont Analysis (%)

NII

3.5

3.3

3.8

4.2

4.2

(-) Prov. Exp.

0.0

0.1

0.1

0.3

0.4

Adj NII

3.4

3.2

3.8

4.0

3.8

Other Inc.

0.5

0.4

0.3

0.4

0.4

Op. Inc.

3.9

3.6

4.0

4.3

4.1

Opex

0.1

0.1

0.1

0.1

0.1

PBT

3.8

3.5

3.9

4.2

4.0

Taxes

1.0

0.9

1.0

1.2

1.2

ROA

2.8

2.5

2.9

3.0

2.8

Leverage

6.7

6.7

6.9

7.1

7.1

ROE

18.5

17.0

20.0

21.3

20.0

Market Outlook

July 27, 2015

Lupin Acquires Specialty Product Portfolio in Germany

Lupin announced it has entered into a strategic asset purchase agreement with

TEMMLER PHARMA GMBH & CO. KG (Temmler), a part of the Aenova Group, one

of the world’s largest pharmaceutical contract manufacturers, to acquire Temmler's

specialty product portfolio subject to certain closing conditions.

Based in Marburg (Germany), Temmler has a fast growing specialty portfolio of 13

products including key Central Nervous System (CNS) products and specialty

products that address rare disease areas like Myasthenia Gravis, Huntington

disease as well as fast-growing dermatology products for anti-wart treatment. This

adds to Lupin’s specialty business. Temmler’s business has a strong strategic fit

with Lupin’s business in Germany and enables Lupin to bring an enhanced

specialty CNS portfolio to the German market. While the cost of acquisition and

sales are not available, we don’t think the sales will be significant to contribute

significantly to the overall sales. We maintain our neutral rating on the stock.

Result Review

Hitachi Home (CMP: `1,518/ TP: -/ Upside: -)

For 1QFY2016, the company reported numbers that were in-line with our

estimates. The top-line grew by 18.1% yoy to `709cr against our estimate of

`704cr. Operating expenses as a percentage of sales were stable during the

quarter where - raw material cost (as a percentage of sales) declined by 13bp yoy

to 62.8%, employee expense de-grew by 67bp yoy to 4.0% and other expenses

grew by 2bp yoy to 21% of sales. This resulted in EBITDA increasing by 26.1% yoy

to `87cr and EBITDA margin improving by 78bp yoy to 12.2%. We had built in

slightly higher raw material cost of 63.8% of sales which resulted in EBITDA

margin coming above our estimate of 10.9%. Owing to higher foreign exchange

loss of `3cr (against `0.3cr in the same quarter of the previous year) and higher

depreciation, the net profit witnessed 8.1% yoy improvement to `47cr, which is

in-line with our estimate of `46cr.

At the current market price, the stock is trading at PE of 39.1x for FY2017E. We

maintain our Neutral recommendation on the stock owing to higher valuations.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

Mar

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,806

9.2

79

29.1

22.6

52.2

10.6

25.4

2.3

FY2017E

2,112

9.7

105

38.8

24.0

39.1

8.4

20.4

2.0

Relaxo Footwears (CMP: `569/ TP: -/ Upside: -)

For 1QFY2016, Relaxo footwears reported numbers that were mainly in-line with

our estimates. The top-line during the quarter witnessed 21.4% yoy improvement

to `452cr against our expectation of `442cr. Raw material cost as a percentage of

sales decline significantly by 509bp yoy to 40.8%. Employee expenses (% of sales)

remained stable at 9.0% of (vs. 8.9% in the same quarter of the previous year) and

other expenses as a percentage of sales increased by 256bp yoy to 35.3%. On the

back of decline in raw material cost, the EBITDA margin expanded by 237bp yoy

Market Outlook

July 27, 2015

to 14.8%. Consequently, the net profit grew by 55.5% yoy to `36cr vis-à-vis our

expectation of `34cr.

At the current market price, the stock is trading at PE of 45.8x for FY2017E. We

have a Neutral recommendation on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

Mar

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,796

12.3

115

19.1

27.3

59.5

14.4

31.5

3.9

FY2017E

2,169

12.5

149

24.8

27.5

45.8

11.2

25.2

3.2

Visaka Industries (CMP: `143/ TP: `161/ Upside: 13%)

For 1QFY2016, Visaka Industries posted decent set of numbers. The top-line

during the quarter grew by 2.9% yoy to `321cr. The raw material cost as a

percentage of sales remained the same on qoq basis but it declined by 319bp yoy

to 58.7%. Employee expense grew marginally by 29bp yoy to 5.8% of sales and

other expenses increased by 268bp yoy to 24.3% thus negating the positive impact

of lower raw material cost. As a result, the EBITDA margin improved marginally by

23bp yoy to 11.2% - against our expectation of 11.1%. Depreciation expense

declined by 30.3% to `9cr and consequently, the net profit for the quarter grew by

21.6% yoy to `14cr.

The top-line for the Building Products segment of the company grew marginally by

4.2% on yoy basis to `274cr. The EBIT margin for the segment reported 79bp yoy

expansion to 9.0% and segment ROCE improved marginally to 18.3% from 18.1%

in the same quarter of the previous year. The Synthetic Yarn segment witnessed

7.6% yoy decline in its top-line to `44cr with EBIT margin expanding significantly

by 723bp yoy to 17.4%. The ROCE for the segment improved to 55.9% from

35.4% in 1QFY2015.

At the current market price, the stock is trading at PE of 4.4x for FY2017E. We

maintain our Accumulate rating on the stock with a revised target price of `161

based on target PE of 5.0X for FY2017E.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

Mar

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,113

9.6

36

22.9

10.1

6.2

0.6

4.3

0.4

FY2017E

1,254

10.0

51

32.2

12.8

4.4

0.6

3.7

0.4

Result Preview

Subros Ltd (CMP: `80/ TP: /Upside: )

Subros Ltd is slated to announce its 1QFY2016 results today. Revenues are

estimated to grow 8% yoy to `309cr. Volumes are expected to grow 12% yoy on

back of strong double digit growth by major customer Maruti Suzuki. However

realization/kit is likely to decline 4% yoy on back of continued weakness in

Japanese Yen. Operating margins are likely to improve 220 bp yoy to 12.6% on

back of decline in raw material costs (due to Yen depreciation) and operating

leverage. We expect the Net Profit to come in at `7.9cr as against `3.3cr reported

in 1QFY2015. Currently we have Neutral rating on the stock.

Market Outlook

July 27, 2015

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,295

11.7

25

4.2

7.7

19.2

1.4

5.7

0.6

FY2017E

1,533

12.0

44

7.3

12.4

11.0

1.3

4.5

0.5

Tech Mahindra (CMP: `511/ TP: `646/Upside: 26.4%)

Tech Mahindra is expected to announce its 1QFY2016 results today. The company

is expected to post a dip of 0.1% qoq in USD revenues to US$983mn V/s

US$984mn in 4QFY2015. The, company has already guided for a weaker

1QFY2016, on back of the weakness in Telecom and Energy domain. In rupee

terms, the revenues are expected to come in at `6,242cr V/s `6,117cr in

4QFY2015, a qoq growth of 2.0%. The EBDITA is expected to come in at 14.9%

and EBIT is expected to be around 12.1%, registering a dip of 30bp and 24bps

qoq respectively. Consequently; the PAT is expected to come in at `556cr V/s

`472cr in 4QFY2015 a growth of 17.9% qoq. We maintain our buy rating on the

stock with a target price of `646.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

27,281

17.3

2,957

30.8

20.3

16.6

3.4

9.5

1.6

FY2017E

31,373

18.4

3,651

38.0

20.9

13.4

2.8

7.3

1.3

Quarterly Bloomberg Brokers Consensus Estimate

Tech Mahindra Ltd (Consol)- July 27, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

6,218

5,122

21.4

6,117

1.7

EBITDA

923

928

(0.6)

928

(0.6)

EBITDA margin (%)

14.8

18.1

15.2

Net profit

593

631

(6.0)

472

25.6

Ambuja Cements Ltd- July 27, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

2,505

2,706

(7.4)

2,425

3.3

EBITDA

390

588

(33.6)

510

(23.5)

EBITDA margin (%)

15.6

21.7

21.0

Net profit

251

409

(38.7)

318

(21.1)

Maruti Suzuki India Ltd- July 28, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

13,420

11,074

21.2

13,273

1.1

EBITDA

2,130

1,328

60.4

2,164

(1.6)

EBITDA margin (%)

15.9

12.0

16.3

Net profit

1,269

762

66.5

1,284

(1.2)

Market Outlook

July 27, 2015

Housing Development Finance Corp- July 28, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

2,154

6,447

(66.6)

7,448

(71.1)

EBITDA

1,874

6,234

(69.9)

7,241

(74.1)

EBITDA margin (%)

87.0

96.7

97.2

Net profit

1,365

1,345

1.5

1,862

(26.7)

Punjab National Bank- July 28, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

PAT

872

1,405

(38.0)

307

184.3

Bank of India- July 28, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

PAT

329

806

(59.1)

(56)

0.0

IDBI Bank Ltd- July 28, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

PAT

150

105

43.3

546

(72.5)

Union Bank of India- July 28, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

PAT

509

664

(23.3)

444

14.7

Yes Bank Ltd- July 29, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

PAT

550

439

25.1

551

(0.2)

Nestle India Ltd- July 29, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

2,361

2,419

(2.4)

2,507

(5.8)

EBITDA

400

500

(20.1)

612

(34.7)

EBITDA margin (%)

16.9

20.7

24.4

Net profit

272

288

(5.6)

320

(15.2)

Dabur India Ltd (Consol)- July 29, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

2,065

1,864

10.8

1,945

6.2

EBITDA

317

268

18.4

346

(8.2)

EBITDA margin (%)

15.4

14.4

17.8

Net profit

255

211

21.1

285

(10.3)

Godrej Consumer Products Ltd (Consol)- July 29, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

2,116

1,886

12.2

2,083

1.6

EBITDA

298

242

23.4

387

(22.9)

EBITDA margin (%)

14.1

12.8

18.6

Net profit

193

143

34.8

266

(27.2)

Market Outlook

July 27, 2015

JSW Steel Ltd (Consol)- July 29, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

11,583

13,067

(11.4)

12,364

(6.3)

EBITDA

1,540

2,612

(41.0)

1,683

(8.4)

EBITDA margin (%)

13.3

20.0

13.6

Net profit

(98)

656

0.0

62

0.0

Vedanta- July 29, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

17,403

17,056

2.0

17,732

(1.9)

EBITDA

4,300

5,673

(24.2)

4,014

7.1

EBITDA margin (%)

24.7

33.3

22.6

Net profit

544

1,341

(59.5)

491

10.6

NHPC Ltd- July 29, 2015

Particulars (` cr)

1QFY16E

1QFY15

y-o-y (%)

4QFY15

q-o-q (%)

Net sales

2,168

2,034

6.6

1,450

49.5

EBITDA

1,467

1,317

11.3

872

68.2

EBITDA margin (%)

67.7

64.8

60.2

Net profit

763

616

23.9

645

18.4

Economic and Political News

Modi sounds Bihar poll bugle, inaugurates slew of projects

Govt. may Issue `15,000cr Sovereign Gold Bonds in Fiscal Second Half

Disinvestment Department Wants PF Body to Invest `6,000cr: Report

Govt approves `1,000cr for India-Bangladesh rail link

Corporate News

ONGC to invest $8.8bn in KG oil and gas finds

Tata JLR planning new plant in Poland

Reliance Jio spending `1,00,000cr on 4G rollout

JSW Steel to seek shareholders' nod to raise `14,000cr

Market Outlook

July 27, 2015

Top Picks

Large Cap

Market Cap

CMP

Target

Upside

Company

Sector

Rating

(` Mn)

(`)

(`)

(%)

Axis Bank

Financials

1,38,010

Buy

581

716

23.2

ICICI Bank

Financials

1,74,426

Buy

301

392

30.4

Infosys

IT

2,50,218

Buy

1,089

1,306

19.9

Power Grid

Power

74,289

Buy

142

170

19.7

TCS

IT

4,90,417

Buy

2,504

3,168

26.5

Tech Mahindra

IT

49,134

Buy

511

646

26.4

Yes Bank

Financials

33,810

Buy

809

1,006

24.4

Ashok Leyland

Auto

22,938 Accumulate

81

88

9.2

LIC Housing Fin.

Financials

24,966 Accumulate

495

553

11.8

MRF

Others

16,340 Accumulate

38,528

43,439

12.7

Source: Angel Research, Bloomberg

Mid Cap

Market

CMP

Target

Upside

Company

Sector

Rating

Cap (` Mn)

(`)

(`)

(%)

Action Const. Equip. Capital Goods

428

Buy

43

54

24.9

Bajaj Electricals

Others

2,789

Buy

277

341

23.3

Hindustan Media Ven. Media

1,790

Buy

244

292

19.7

JK Tyre

Auto Ancillary

2,349

Buy

104

127

22.6

MBL Infrastructures

Construction

1,218

Buy

588

789

34.2

Mangalam Cements Cement

721

Buy

270

349

29.3

MT Educare

Others

447

Buy

112

141

25.5

Radico Khaitan

Others

1,222

Buy

92

112

21.9

Setco Automotive

Auto Ancillary

626

Buy

234

286

22.1

Source: Angel Research, Bloomberg

Market Outlook

July 27, 2015

Result Calendar

Date

Company

July 27, 2015

Subros, KEC International, Ambuja Cements, Tech Mahindra, Jagran Prakashan, MRF

Maruti, Thermax, Blue Star, HDFC, Punjab Natl.Bank, Bank of India, Union Bank, IDBI Bank, Syndicate Bank, Tide

July 28, 2015

Water Oil India

United Phosphorus, Yes Bank, Allahabad Bank, Nestle, Dabur India, Godrej Consumer, Mphasis, Sesa Goa, JSW Steel

July 29, 2015

, Essar Oil, NHPC

Exide Industries, Kotak Mah. Bank, Bank of Baroda, IDFC, Oriental Bank, Vijaya Bank, Dena Bank, ITC, Colgate,

July 30, 2015

Electrosteel Castings, Petronet LNG, Jyothy Laboratories, HSIL, L G Balakrishnan & Bros, Dr Reddy's, Glenmark

Pharma., Ipca labs, Indoco Remedies, NTPC

July 31, 2015

Suzlon Energy, ICICI Bank, Shriram Trans., Sun TV Network, GSK Pharma, Alembic Pharma, CESC

August 1, 2015

Transport Corporation of India

August 2, 2015

August 3, 2015

Hero Motocorp, Bharat Forge, BGR Energy , HCL Tech, Styrolution, Vesuvius India

August 4, 2015

Britannia, Hexaware, Sterling Tools

Tata Chemicals, Automotive Axle, Siemens, Ramco Cements, GlaxoSmith Con, Indraprasth Gas, ITD Cementation,

August 5, 2015

PTC India

August 6, 2015

Tata Global, Motherson Sumi, Cummins India, Bajaj Electrical

August 7, 2015

Tata Motors, M&M, Rural Elec.Corp., GSPL, Kirloskar Engines India Ltd

Source: Bloomberg, Angel Research

Global economic events release calendar

Date

Time

Country Event Description

Unit

Period

Bloomberg Data

Last Reported Estimated

July 28, 2015

2:00PM UK

GDP (YoY)

% Change

2Q A

2.90

2.60

7:30PM US

Consumer Confidence

S.A./ 1985=100

Jul

101.40

100.00

July 29, 2015

11:30PM US

FOMC rate decision

%

Jul 29

0.25

0.25

July 30, 2015

1:25PM Germany Unemployment change (000's)

Thousands

Jul

(1.00)

(5.50)

6:00PM US

GDP Qoq (Annualised)

% Change

2Q A

(0.20)

2.50

August 1, 2015

6:30AM China PMI Manufacturing

Value

Jul

50.20

--

August 3, 2015

2:00PM UK

PMI Manufacturing

Value

Jul

51.40

--

August 4, 2015

11:00AM India

RBI Reverse Repo rate

%

Aug 4

6.25

--

11:00AM India

RBI Repo rate

%

Aug 4

7.25

--

11:00AM India

RBI Cash Reserve ratio

%

Aug 4

4.00

--

August 6, 2015

4:30PM UK

BOE Announces rates

% Ratio

Aug 6

0.50

0.50

2:00PM UK

Industrial Production (YoY)

% Change

Jun

2.10

--

August 7, 2015

6:00PM US

Change in Nonfarm payrolls

Thousands

Jul

223.00

--

6:00PM US

Unnemployment rate

%

Jul

5.30

--

August 8, 2015

China

Exports YoY%

% Change

Jul

2.80

--

August 9, 2015

7:00AM China Consumer Price Index (YoY)

% Change

Jul

1.40

--

August 10, 2015

India

Imports YoY%

% Change

Jul

(13.40)

--

India

Exports YoY%

% Change

Jul

(15.80)

--

August 12, 2015

2:00PM UK

Jobless claims change

% Change

Jul

7.00

--

11:00AM China Industrial Production (YoY)

% Change

Jul

6.80

--

5:30PM India

Industrial Production YoY

% Change

Jun

2.70

--

Source: Bloomberg, Angel Research

Market Outlook

July 27, 2015

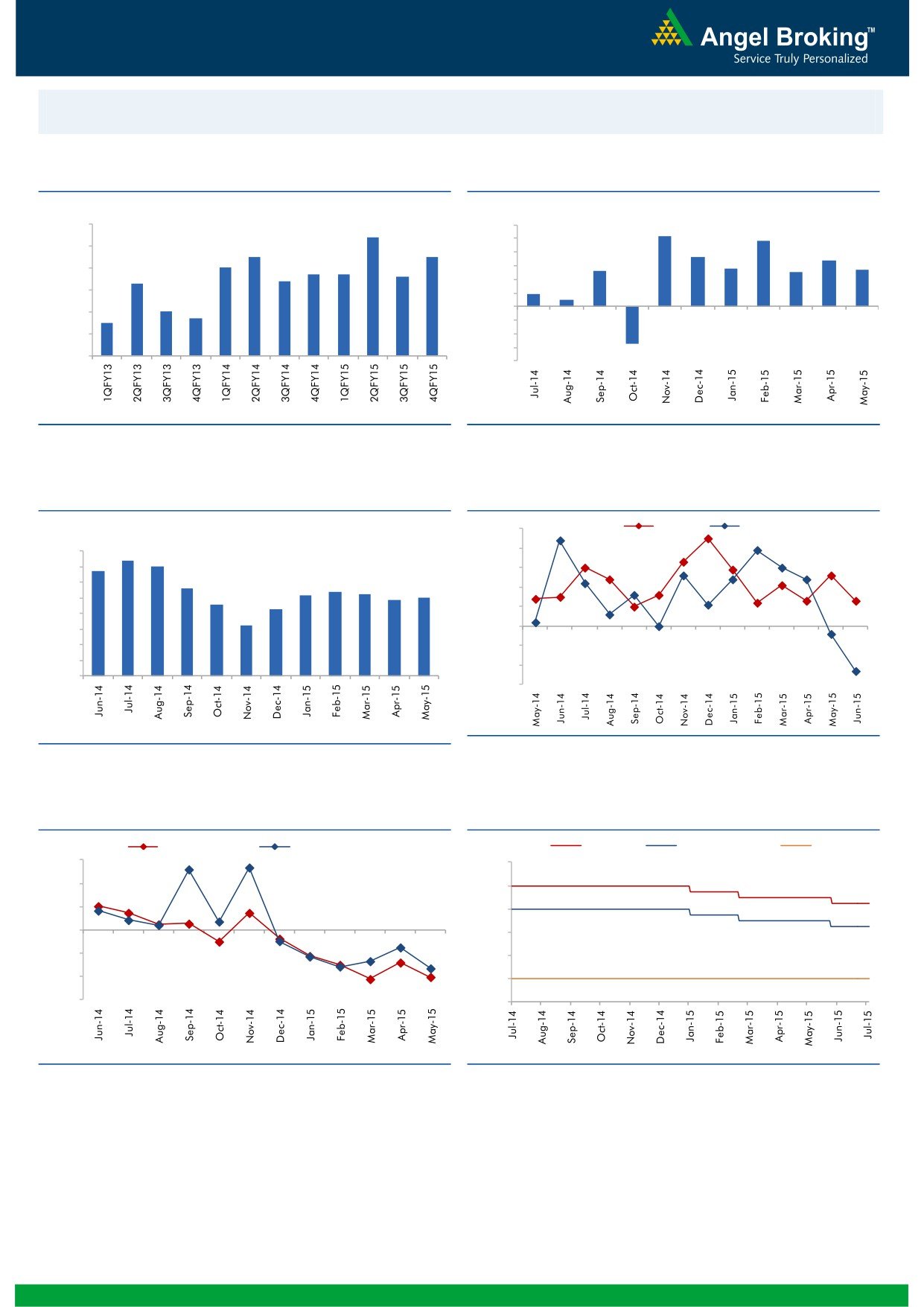

Macro watch

Exhibit 1: Quarterly GDP trends

Exhibit 2: IIP trends

(%)

(%)

9.0

8.4

6.0

5.2

4.8

5.0

8.0

7.5

7.5

3.6

3.4

7.0

4.0

2.8

2.7

6.7

6.7

2.6

2.5

6.6

3.0

7.0

6.3

6.4

2.0

0.9

6.0

0.5

1.0

5.0

4.7

-

5.0

4.5

(1.0)

4.0

(2.0)

(3.0)

3.0

(2.7)

(4.0)

Source: CSO, Angel Research

Source: MOSPI, Angel Research

Exhibit 3: Monthly CPI inflation trends

Exhibit 4: Manufacturing and services PMI

(%)

55.0

Mfg. PMI

Services PMI

8.0

7.4

54.0

6.8

7.0

7.0

53.0

5.6

5.4

6.0

5.2

5.3

4.9

5.0

52.0

4.6

5.0

4.3

51.0

4.0

3.3

50.0

3.0

2.0

49.0

1.0

48.0

-

47.0

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Source: MOSPI, Angel Research

Exhibit 5: Exports and imports growth trends

Exhibit 6: Key policy rates

(%)

Exports yoy growth

Imports yoy growth

(%)

Repo rate

Reverse Repo rate

CRR

30.0

9.00

20.0

8.00

10.0

7.00

0.0

6.00

(10.0)

5.00

(20.0)

4.00

(30.0)

3.00

Source: Bloomberg, Angel Research

Source: RBI, Angel Research

Market Outlook

July 27, 2015

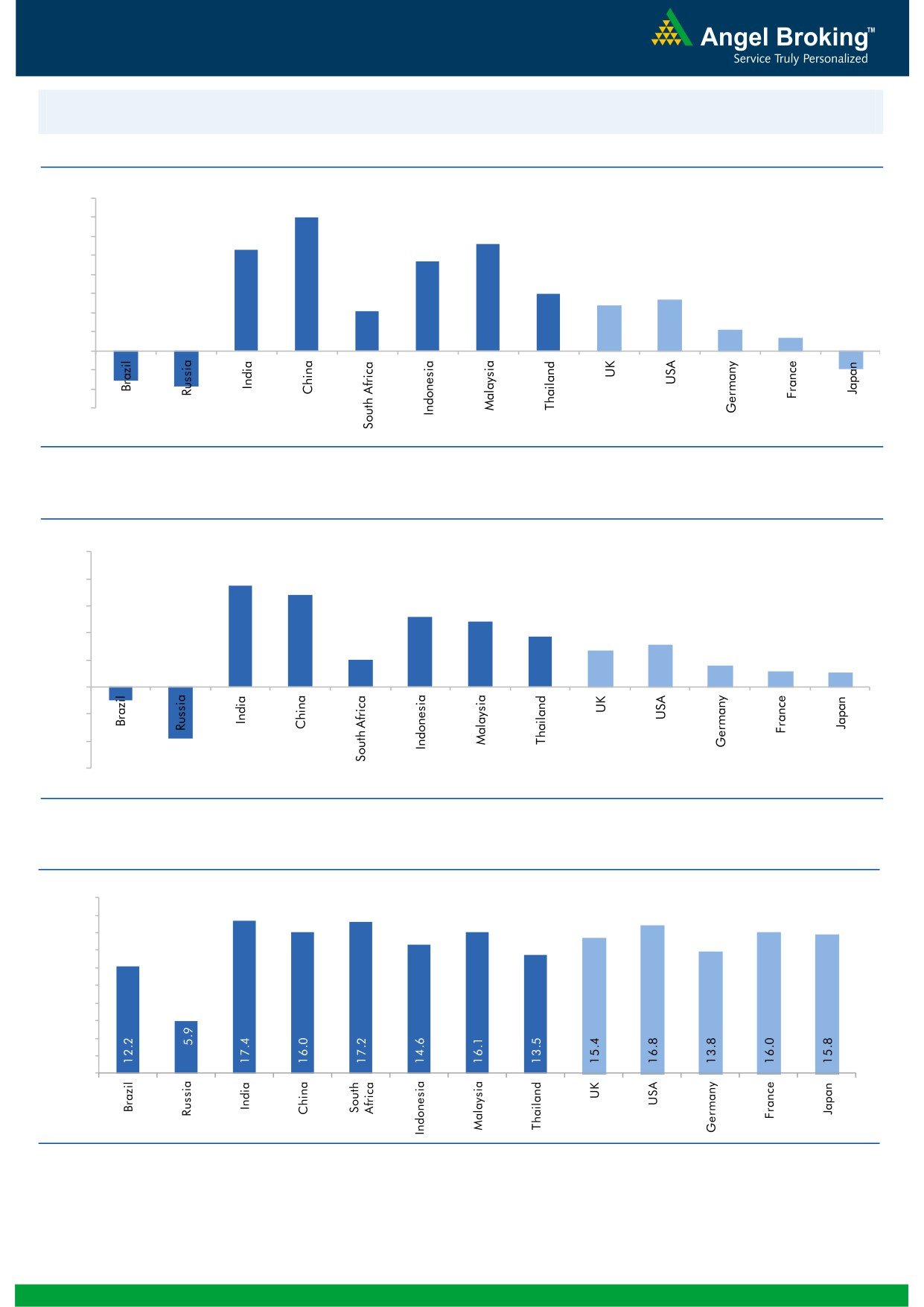

Global watch

Exhibit 1: Latest quarterly GDP Growth (%, yoy) across select developing and developed countries

(%)

8.0

7.0

7.0

5.6

6.0

5.3

4.7

5.0

4.0

3.0

2.7

3.0

2.4

2.1

2.0

1.1

0.7

1.0

(1.6)

(1.9)

(0.9)

-

(1.0)

(2.0)

(3.0)

Source: Bloomberg, Angel Research

Exhibit 2: 2015 GDP Growth projection by IMF (%, yoy) across select developing and developed countries

(%)

10.0

7.5

8.0

6.8

6.0

5.2

4.8

3.7

4.0

3.1

2.7

2.0

1.6

2.0

1.2

1.0

(1.0)

(3.8)

-

(2.0)

(4.0)

(6.0)

Source: IMF, Angel Research

Exhibit 3: One year forward P-E ratio across select developing and developed countries

(x)

20.0

18.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

Source: Bloomberg, Angel Research

Market Outlook

July 27, 2015

Exhibit 4: Relative performance of indices across globe

Returns (%)

C ountry

Name of index

Closing price

1M

3M

1YR

Brazil

Bovespa

49,246

(8.4)

(9.8)

(15.1)

Russia

Micex

1,596

(3.4)

(6.7)

13.4

India

Nifty

8,522

1.9

2.6

13.2

China

Shanghai Composite

4,071

(13.2)

(7.8)

96.9

South Africa

Top 40

45,858

(2.9)

(4.5)

(1.3)

Mexico

Mexbol

44,249

(2.6)

(3.3)

(0.4)

Indonesia

LQ45

828

(2.6)

(12.1)

(3.7)

Malaysia

KLCI

1,721

(0.4)

(7.2)

(8.6)

Thailand

SET 50

943

(4.6)

(8.8)

(8.4)

USA

Dow Jones

17,569

(3.2)

(2.7)

3.6

UK

FTSE

6,580

(3.9)

(6.7)

(3.1)

Japan

Nikkei

20,545

(1.3)

4.6

33.4

Germany

DAX

11,347

(1.1)

(3.2)

15.9

France

CAC

5,057

0.2

(2.8)

17.3

Source: Bloomberg, Angel Research

Market Outlook

July 27, 2015

Stock Watch

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Agri / Agri Chemical

Rallis

Neutral

235

-

4,564

2,075

2,394

14.4

14.4

9.5

11.0

24.7

21.3

4.9

4.2

21.1

21.3

2.2

1.9

United Phosphorus

Neutral

537

-

23,016

13,698

15,752

17.6

17.6

32.1

38.5

16.7

14.0

3.3

2.7

21.4

21.3

1.8

1.5

Auto & Auto Ancillary

Ashok Leyland

Accumulate

81

88

22,938

17,094

19,726

9.5

10.7

2.7

4.2

29.9

19.2

4.1

3.8

13.9

19.8

1.3

1.1

Bajaj Auto

Neutral

2,497

-

72,268

25,664

29,609

18.8

18.6

134.2

150.3

18.6

16.6

5.7

4.9

30.7

29.6

2.4

2.1

Eicher Motors

Accumulate

20,114

21,843

54,594

11,681

15,550

15.3

16.9

358.5

564.3

56.1

35.6

16.9

12.5

29.8

34.9

4.6

3.4

Hero Motocorp

Neutral

2,738

-

54,678

29,771

34,219

13.0

13.5

142.3

165.2

19.2

16.6

7.0

5.9

36.3

35.8

1.7

1.4

L G Balakrishnan & Bros Accumulate

498

541

781

1,254

1,394

11.6

11.8

35.9

41.7

13.9

12.0

1.9

1.7

13.5

13.8

0.7

0.7

Mahindra and Mahindra Neutral

1,328

-

82,506

41,078

46,473

11.5

12.0

51.4

62.7

25.8

21.2

3.8

3.4

14.7

15.9

1.7

1.5

Maruti

Neutral

4,234

-

127,890

57,615

68,166

15.6

15.5

180.2

220.0

23.5

19.2

4.6

4.0

19.7

20.6

2.0

1.6

Minda Industries

Buy

550

652

872

2,500

2,889

7.6

8.3

39.4

54.3

14.0

10.1

2.0

1.7

14.1

16.3

0.5

0.4

Rane Brake Lining

Accumulate

338

366

267

454

511

11.1

11.4

23.8

28.1

14.2

12.0

2.0

1.8

14.2

15.3

0.7

0.7

Setco Automotive

Buy

234

286

626

718

862

13.3

14.3

13.4

19.0

17.5

12.3

2.7

2.3

15.4

18.5

1.1

1.0

Tata Motors

Buy

391

489

112,933

260,543

278,575

13.3

13.7

31.7

38.0

12.3

10.3

1.4

1.3

12.2

13.0

0.6

0.7

TVS Motor

Neutral

251

-

11,946

11,839

13,985

7.0

8.1

10.8

16.2

23.3

15.5

5.9

4.7

25.5

30.1

1.0

0.8

Amara Raja Batteries

Neutral

858

-

14,663

5,355

6,641

17.4

17.8

31.8

40.9

27.0

21.0

6.8

5.4

25.2

25.5

2.7

2.1

Exide Industries

Accumulate

151

164

12,844

7,919

9,028

13.9

14.4

7.3

8.6

20.7

17.6

2.8

2.6

13.8

14.4

1.4

1.2

Apollo Tyres

Neutral

194

-

9,878

12,866

13,892

15.7

15.4

20.1

19.9

9.7

9.8

1.5

1.3

15.8

13.6

0.8

0.8

Ceat

Neutral

783

-

3,167

6,047

6,776

12.4

12.0

82.0

90.4

9.6

8.7

1.6

1.4

16.5

15.7

0.7

0.6

JK Tyres

Buy

104

127

2,349

7,774

8,456

13.3

12.9

17.3

18.1

6.0

5.7

1.4

1.1

22.8

19.7

0.6

0.6

Swaraj Engines

Neutral

872

-

1,083

604

689

14.3

14.5

51.4

60.7

17.0

14.4

4.0

3.6

23.4

24.7

1.7

1.4

Subros

Neutral

80

-

479

1,295

1,533

11.7

12.0

4.2

7.3

19.0

10.9

1.4

1.3

7.7

12.4

0.7

0.5

Indag Rubber

Buy

195

247

511

283

329

17.0

17.2

13.0

15.4

15.0

12.6

3.3

2.7

21.8

21.6

1.5

1.3

Capital Goods

ACE

Buy

43

54

428

660

839

4.7

8.2

1.0

3.9

43.3

11.1

1.4

1.2

3.2

11.3

0.8

0.6

BEML

Accumulate

1,482

1,607

6,171

3,277

4,006

6.0

8.9

29.2

64.3

50.8

23.1

5.7

11.7

2.0

1.6

BGR Energy

Neutral

126

-

911

3,615

3,181

9.5

9.4

16.7

12.4

7.6

10.2

0.7

0.7

10.0

7.0

0.7

0.8

BHEL

Neutral

280

-

68,618

33,722

35,272

10.8

11.7

10.5

14.2

26.7

19.7

2.0

1.9

7.0

9.0

2.1

2.0

Blue Star

Buy

333

391

2,998

3,649

4,209

4.8

5.7

8.5

14.0

39.4

23.8

6.3

5.4

16.3

24.4

0.9

0.8

Crompton Greaves

Buy

182

220

11,426

15,252

16,870

5.4

5.6

7.9

10.7

23.1

17.0

2.8

2.5

12.0

15.0

0.8

0.7

Inox Wind

Buy

422

505

9,373

4,980

5,943

17.0

17.5

26.6

31.6

15.9

13.4

35.0

30.0

2.0

1.7

Market Outlook

July 27, 2015

Stock Watch

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Capital Goods

KEC International

Neutral

151

-

3,869

8,791

9,716

6.1

6.8

5.4

8.2

27.9

18.4

2.8

2.6

10.0

14.0

0.7

0.6

Thermax

Neutral

1,059

-

12,622

6,413

7,525

7.4

8.5

30.5

39.3

34.7

27.0

5.4

4.7

15.0

17.0

1.9

1.6

Cement

ACC

Accumulate

1,407

1,548

26,406

11,856

14,092

14.5

17.8

47.6

76.2

29.6

18.5

3.0

2.8

10.6

15.7

2.1

1.7

Ambuja Cements

Neutral

240

-

37,300

10,930

12,022

22.2

23.2

9.7

11.2

24.7

21.4

3.4

3.1

14.3

15.2

3.0

2.7

India Cements

Buy

84

132

2,593

4,716

5,133

14.9

15.8

1.0

4.5

84.4

18.8

0.9

0.8

1.0

4.5

0.9

0.8

JK Cement

Buy

627

778

4,385

4,061

4,748

16.2

17.7

24.5

42.9

25.6

14.6

2.5

2.2

10.0

15.9

1.5

1.3

J K Lakshmi Cement

Buy

322

443

3,790

3,004

3,618

17.6

19.9

13.9

27.2

23.2

11.8

2.6

2.3

11.8

20.5

1.7

1.3

Mangalam Cements

Buy

270

349

721

1,111

1,336

12.2

15.1

16.3

34.6

16.6

7.8

1.3

1.2

8.2

16.0

0.9

0.7

Orient Cement

Neutral

186

-

3,813

2,039

2,573

22.7

24.5

9.3

13.3

20.0

14.0

3.4

2.9

18.3

22.6

2.5

1.9

Ramco Cements

Neutral

361

-

8,597

4,036

4,545

20.8

21.3

15.1

18.8

23.9

19.2

2.9

2.6

12.9

14.3

2.6

2.3

Shree Cement^

Neutral

10,914

-

38,021

7,150

8,742

26.7

28.6

228.0

345.5

47.9

31.6

7.1

5.9

15.7

20.3

5.1

4.1

UltraTech Cement

Neutral

3,209

-

88,050

27,562

31,548

20.3

22.0

111.0

145.0

28.9

22.1

4.1

3.5

15.1

17.0

3.3

2.8

Construction

ITNL

Buy

148

211

3,640

7,589

8,021

34.0

35.9

16.0

19.0

9.2

7.8

0.6

0.5

6.5

6.7

3.6

3.8

KNR Constructions

Neutral

585

-

1,645

915

1,479

14.3

13.9

20.3

37.2

28.8

15.7

2.7

2.3

9.6

15.6

1.9

1.2

Larsen & Toubro

Accumulate

1,803

2,013

167,719

68,920

82,446

10.9

11.5

57.0

73.0

31.6

24.7

2.9

2.7

13.6

15.5

2.7

2.2

Gujarat Pipavav Port

Neutral

220

-

10,628

793

694

53.0

50.9

9.0

8.0

24.4

27.5

5.3

4.3

25.9

18.4

13.0

14.8

MBL Infrastructures

Buy

588

789

1,218

2,507

2,986

12.4

14.4

43.0

41.0

13.7

14.3

1.6

1.5

12.6

12.7

1.3

1.1

PNC Infratech

Accumulate

431

445

2,210

1,719

2,003

13.0

13.5

21.0

28.0

20.5

15.4

1.8

1.6

11.0

10.9

1.4

1.2

Financials

Allahabad Bank

Neutral

88

-

5,022

8,859

9,817

3.0

3.0

23.7

30.1

3.7

2.9

0.4

0.4

10.6

12.3

-

-

Axis Bank

Buy

581

716

138,010

26,522

31,625

3.6

3.6

36.2

45.4

16.1

12.8

3.1

2.7

18.2

19.6

-

-

Bank of Baroda

Neutral

155

-

34,322

18,934

21,374

2.0

2.0

13.2

15.1

11.8

10.3

0.9

0.8

7.1

7.7

-

-

Bank of India

Neutral

171

-

11,387

17,402

20,003

2.0

2.1

40.3

50.7

4.3

3.4

0.4

0.4

9.0

10.4

-

-

Canara Bank

Accumulate

279

297

14,387

15,805

17,745

2.0

2.2

64.3

73.5

4.4

3.8

0.5

0.4

10.8

11.3

-

-

Dena Bank

Neutral

44

-

2,444

3,580

4,040

2.1

2.2

8.4

10.9

5.2

4.0

0.5

0.4

6.8

8.4

-

-

Federal Bank

Neutral

70

-

11,978

3,522

4,045

3.2

3.2

12.2

14.1

5.7

5.0

0.7

0.6

12.9

13.4

-

-

HDFC

Neutral

1,354

-

213,513

11,198

13,321

3.5

3.5

45.1

53.7

30.1

25.2

6.2

5.6

27.2

28.2

-

-

HDFC Bank

Accumulate

1,107

1,255

277,968

38,629

47,500

4.5

4.7

52.6

66.4

21.0

16.7

3.9

3.3

19.6

21.2

-

-

ICICI Bank

Buy

301

392

174,426

36,037

41,647

3.5

3.6

22.9

26.7

13.1

11.3

2.2

1.9

15.7

15.9

-

-

IDBI Bank

Neutral

63

-

10,049

9,806

11,371

1.7

1.9

10.0

16.3

6.3

3.9

0.5

0.4

6.8

10.4

-

-

Market Outlook

July 27, 2015

Stock Watch

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Financials

Indian Bank

Neutral

139

-

6,671

6,454

7,321

2.5

2.6

26.4

33.3

5.3

4.2

0.5

0.4

8.1

9.6

-

-

LIC Housing Finance

Accumulate

495

553

24,966

2,934

3,511

2.3

2.3

30.9

36.8

16.0

13.4

2.6

2.2

16.8

17.5

-

-

Oriental Bank

Neutral

170

-

5,085

7,930

8,852

2.5

2.5

51.8

57.1

3.3

3.0

0.4

0.3

9.3

9.5

-

-

Punjab Natl.Bank

Neutral

139

-

25,815

24,160

27,777

2.9

3.0

18.5

24.6

7.5

5.7

0.7

0.6

8.8

10.8

-

-

South Ind.Bank

Neutral

23

-

3,119

1,999

2,249

2.4

2.4

3.5

4.0

6.7

5.8

0.8

0.8

12.6

13.1

-

-

St Bk of India

Accumulate

264

297

199,370

86,900

100,550

3.1

3.1

22.1

27.7

12.0

9.5

1.5

1.3

12.7

14.3

-

-

Union Bank

Neutral

159

-

10,134

12,995

14,782

2.4

2.4

32.3

40.9

4.9

3.9

0.6

0.5

10.7

12.3

-

-

Vijaya Bank

Neutral

40

-

3,462

3,474

3,932

1.8

1.9

5.9

7.2

6.9

5.6

0.6

0.5

8.1

9.3

-

-

Yes Bank

Buy

809

1,006

33,810

7,006

8,825

3.1

3.3

61.4

77.1

13.2

10.5

2.5

2.1

20.1

21.3

-

-

FMCG

Asian Paints

Neutral

847

-

81,268

16,553

19,160

16.0

16.2

17.7

21.5

47.9

39.4

12.7

11.5

29.4

31.2

4.7

4.1

Britannia

Neutral

2,898

-

34,770

8,065

9,395

9.6

10.2

47.2

65.5

61.4

44.3

20.4

19.3

38.3

41.2

4.2

3.6

Colgate

Neutral

2,058

-

27,989

4,836

5,490

19.5

19.7

48.5

53.2

42.4

38.7

31.1

27.1

99.8

97.5

5.7

5.0

Dabur India

Neutral

297

-

52,107

9,370

10,265

17.1

17.2

7.3

8.1

40.4

36.6

12.2

9.9

33.7

30.6

5.5

5.0

GlaxoSmith Con*

Neutral

6,228

-

26,193

4,919

5,742

17.2

17.4

168.3

191.2

37.0

32.6

10.5

8.9

28.8

28.9

4.9

4.1

Godrej Consumer

Neutral

1,226

-

41,749

10,168

12,886

16.1

16.1

32.1

38.4

38.2

31.9

7.8

7.2

19.7

21.0

4.2

3.3

HUL

Neutral

907

-

196,236

34,940

38,957

17.5

17.7

20.8

24.7

43.6

36.7

48.5

38.8

110.5

114.2

5.4

4.8

ITC

Buy

314

409

252,028

41,068

45,068

37.8

37.4

13.9

15.9

22.6

19.8

7.6

6.7

34.1

33.8

5.8

5.2

Marico

Neutral

434

-

28,026

6,551

7,766

15.7

16.0

10.4

12.5

41.9

34.8

12.2

10.1

33.2

32.4

4.2

3.5

Nestle*

Accumulate

6,026

6,646

58,099

11,291

12,847

22.2

22.3

158.9

184.6

37.9

32.6

19.8

17.8

55.0

57.3

5.0

4.3

Tata Global

Buy

141

186

8,879

8,735

9,182

9.8

9.9

8.5

9.3

16.6

15.1

2.2

2.1

7.9

8.1

1.0

0.9

IT

HCL Tech^

Buy

954

1,100

134,172

41,535

46,519

24.0

23.4

56.6

61.1

16.9

15.6

3.5

2.8

20.8

17.7

3.1

2.7

Infosys

Buy

1,089

1,306

250,218

60,250

66,999

28.0

28.0

58.3

63.7

18.7

17.1

3.9

3.4

20.9

19.7

3.5

3.0

TCS

Buy

2,504

3,168

490,417

108,420

123,559

28.8

28.7

127.2

143.9

19.7

17.4

7.9

7.3

39.9

41.8

4.1

3.6

Tech Mahindra

Buy

511

646

49,134

27,281

31,373

17.3

18.4

30.8

38.0

16.6

13.4

3.4

2.8

20.3

20.9

1.6

1.3

Wipro

Buy

566

753

139,883

54,050

61,617

23.7

23.8

39.4

44.1

14.4

12.8

2.9

2.6

19.9

18.8

2.2

1.8

Media

D B Corp

Accumulate

318

356

5,839

2,241

2,495

27.8

27.9

21.8

25.6

14.6

12.4

3.8

3.4

26.7

28.5

2.5

2.3

HT Media

Buy

89

129

2,066

2,495

2,703

13.5

13.6

9.4

10.7

9.4

8.3

1.0

0.9

10.4

10.6

0.4

0.2

Jagran Prakashan

Buy

135

156

4,402

1,939

2,122

26.0

26.0

8.3

9.2

16.2

14.6

2.8

2.5

17.5

17.1

2.2

2.0

Sun TV Network

Neutral

280

-

11,021

2,779

3,196

70.2

70.5

22.8

27.3

12.3

10.2

3.0

2.7

26.7

28.3

3.7

3.2

Market Outlook

July 27, 2015

Stock Watch

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Media

Hindustan Media

Buy

244

292

1,790

920

1,031

20.0

20.0

19.2

20.9

12.7

11.7

2.1

1.8

16.4

15.3

1.5

1.3

Ventures

Metals & Mining

Coal India

Accumulate

426

450

269,014

77,595

89,628

22.9

24.4

27.6

30.0

15.4

14.2

6.7

6.7

33.9

33.2

2.8

2.4

Hind. Zinc

Neutral

164

-

69,274

15,546

16,821

47.5

49.0

19.7

20.3

8.3

8.1

1.4

1.2

17.2

16.6

2.2

1.7

Hindalco

Neutral

109

-

22,519

112,328

119,817

7.7

7.9

16.3

20.1

6.7

5.4

0.5

0.5

8.0

8.5

0.7

0.6

JSW Steel

Neutral

845

-

20,427

48,125

53,595

18.8

21.0

46.9

97.5

18.0

8.7

0.9

0.8

4.4

9.5

1.2

1.1

NMDC

Neutral

114

-

45,118

12,544

13,330

59.5

59.7

16.3

16.5

7.0

6.9

1.2

1.2

5.1

9.9

2.3

2.3

SAIL

Neutral

58

-

23,975

56,365

63,383

6.9

8.0

7.1

8.2

8.2

7.1

0.5

0.5

7.0

7.1

1.0

0.9

Vedanta

Neutral

132

-

39,267

81,842

88,430

30.6

32.8

20.2

25.7

6.6

5.2

0.5

0.4

7.5

8.5

0.9

0.6

Tata Steel

Neutral

265

-

25,747

136,805

149,228

11.3

11.9

26.4

36.8

10.0

7.2

0.8

0.7

6.0

8.0

0.7

0.7

Oil & Gas

Cairn India

Neutral

175

-

32,791

12,617

14,513

33.7

40.0

25.5

27.7

6.9

6.3

0.5

0.5

7.4

7.7

1.3

1.0

GAIL

Neutral

361

-

45,798

75,595

85,554

8.6

8.0

31.8

36.1

11.3

10.0

1.2

1.2

10.7

11.4

0.7

0.6

ONGC

Neutral

283

-

242,163

174,773

192,517

22.7

24.8

34.6

38.2

8.2

7.4

1.2

1.1

14.2

14.9

1.5

1.3

Petronet LNG

Neutral

196

-

14,708

45,759

49,386

3.7

4.0

12.6

14.9

15.6

13.2

2.4

2.1

16.1

16.7

0.4

0.3

Reliance Industries

Accumulate

1,025

1,100

331,880

339,083

384,014

7.8

9.5

75.7

94.5

13.6

10.9

1.3

1.3

10.7

12.2

1.3

1.2

Pharmaceuticals

Alembic Pharma

Neutral

751

-

14,158

2,405

2,859

19.9

20.4

17.7

22.0

42.4

34.1

12.2

9.3

32.6

30.9

5.9

4.9

Aurobindo Pharma

Accumulate

735

824

42,918

14,435

16,600

22.6

22.6

36.1

41.2

20.4

17.8

6.1

4.6

34.5

29.3

3.3

2.8

Aventis*

Neutral

3,736

-

8,603

2,156

2,455

15.1

16.8

109.7

133.9

34.1

27.9

4.7

3.8

18.4

22.5

3.7

3.1

Cadila Healthcare

Neutral

1,915

-

39,201

10,224

11,840

19.7

20.0

69.8

81.0

27.4

23.6

7.3

5.8

26.8

25.3

3.9

3.3

Cipla

Neutral

678

-

54,475

14,051

16,515

18.9

18.7

25.1

28.9

27.0

23.5

4.3

3.7

17.2

16.9

3.9

3.2

Dr Reddy's

Neutral

3,907

-

66,605

17,443

20,296

22.3

22.4

156.7

180.1

24.9

21.7

5.0

4.1

21.8

20.8

3.8

3.2

Dishman Pharma

Buy

178

250

1,438

1,716

1,888

20.2

20.2

16.3

21.6

10.9

8.3

1.0

0.9

9.7

11.7

1.0

0.8

GSK Pharma*

Neutral

3,390

-

28,711

2,818

3,044

18.9

18.9

56.2

58.6

60.3

57.8

17.1

18.5

27.1

30.7

9.7

9.1

Indoco Remedies

Neutral

363

-

3,346

1,088

1,262

18.2

18.2

13.1

15.5

27.7

23.4

5.4

4.5

21.2

21.1

3.1

2.7

Ipca labs

Accumulate

690

736

8,710

3,533

4,109

18.6

19.6

28.2

34.8

24.5

19.8

3.4

2.9

15.0

15.9

2.7

2.3

Lupin

Neutral

1,672

-

75,221

14,864

17,244

26.9

26.9

62.1

71.1

26.9

23.5

6.5

5.2

27.4

24.6

4.8

4.0

Sun Pharma

Accumulate

836

950

201,112

27,839

33,542

27.7

29.7

18.9

26.9

44.2

31.1

4.0

3.5

13.0

14.6

6.6

5.2

Power

Tata Power

Neutral

72

-

19,419

38,302

38,404

14.1

13.1

5.1

6.0

14.0

12.0

1.3

1.3

9.2

10.3

1.4

1.4

NTPC

Neutral

138

-

113,375

89,067

98,329

15.9

16.5

12.1

13.1

11.4

10.5

1.3

1.2

11.0

11.6

2.3

2.3

Power Grid

Buy

142

170

74,289

19,986

22,702

86.2

86.3

11.1

12.7

12.8

11.2

1.7

1.6

14.4

14.7

8.9

8.2

Market Outlook

July 27, 2015

Stock Watch

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Telecom

Bharti Airtel

Neutral

434

-

173,587

101,748

109,191

32.1

31.7

12.0

12.5

36.2

34.7

2.5

2.3

6.9

6.7

2.3

2.1

Idea Cellular

Neutral

179

-

64,273

34,282

36,941

32.0

31.5

5.9

6.2

30.3

28.8

2.8

2.5

9.9

9.3

2.5

2.3

zOthers

Abbott India

Neutral

4,245

-

9,020

2,713

3,141

13.7

13.5

127.8

145.7

33.2

29.1

7.8

6.3

25.9

23.9

3.0

2.6

Bajaj Electricals

Buy

277

341

2,789

4,719

5,287

5.2

5.8

8.6

12.7

32.3

21.9

3.7

3.2

11.4

14.8

0.6

0.5

Finolex Cables

Neutral

265

-

4,049

2,728

3,036

10.8

11.0

14.4

16.8

18.4

15.8

2.8

2.4

15.2

15.3

1.2

1.0

Goodyear India*

Neutral

573

-

1,321

1,536

1,683

9.6

10.0

41.8

48.0

13.7

11.9

2.3

2.0

18.2

18.3

0.6

0.5

Hitachi

Neutral

1,518

-

4,127

1,801

2,051

8.9

9.3

31.0

38.8

48.9

39.1

10.5

8.4

23.9

23.8

2.3

2.0

Jyothy Laboratories

Neutral

313

-

5,662

1,620

1,847

11.5

11.5

7.3

8.5

42.9

36.9

5.5

5.1

13.3

14.4

3.4

2.9

MRF

Accumulate

38,528

43,439

16,340

13,524

14,440

18.6

18.2

2,999.2

3,102.8

12.9

12.4

2.8

2.3

24.7

20.5

1.2

1.0

Page Industries

Neutral

14,641

-

16,330

1,929

2,450

19.8

20.1

229.9

299.0

63.7

49.0

28.1

19.5

52.1

47.1

8.5

6.7

Relaxo Footwears

Neutral

569

-

6,830

1,767

2,152

12.3

12.5

19.3

25.1

29.6

22.7

7.3

5.6

27.7

27.8

3.9

3.2

Siyaram Silk Mills

Neutral

1,218

-

1,142

1,653

1,873

11.7

12.2

99.3

122.1

12.3

10.0

2.2

1.9

19.5

20.2

0.9

0.7

Styrolution ABS India*

Neutral

723

-

1,271

1,271

1,440

8.6

9.2

32.0

41.1

22.6

17.6

2.3

2.1

10.7

12.4

1.0

0.8

Tree House

Neutral

425

-

1,798

259

324

56.8

56.8

17.0

21.7

25.0

19.6

2.5

2.3

10.1

11.5

6.9

5.6

TVS Srichakra

Neutral

2,417

-

1,850

2,112

2,389

11.9

12.1

168.5

202.5

14.3

11.9

4.9

3.7

39.6

35.5

1.0

0.8

HSIL

Buy

339

434

2,449

2,085

2,436

18.5

18.6

21.7

28.9

15.7

11.7

1.6

1.4

10.0

12.1

1.3

1.0

Kirloskar Engines India

Accumulate

283

298

4,097

2,779

3,314

10.3

11.9

12.0

17.5

23.7

16.2

2.9

2.6

12.5

16.7

1.1

0.9

Ltd

M M Forgings

Buy

669

783

807

586

671

22.3

22.9

53.4

65.2

12.5

10.3

2.7

2.2

24.1

23.5

1.5

1.3

Banco Products (India)

Neutral

112

-

804

1,196

1,370

9.7

11.8

9.4

14.3

12.0

7.9

1.2

1.1

10.4

14.5

0.6

0.6

Competent Automobiles Neutral

156

-

96

1,007

1,114

3.1

3.1

23.7

28.2

6.6

5.5

0.9

0.8

13.9

14.6

0.1

0.1

Nilkamal

Neutral

818

-

1,220

1,947

2,131

8.1

8.3

35.7

45.9

22.9

17.8

2.3

2.0

10.3

12.1

0.7

0.6

Visaka Industries

Buy

143

166

228

1,158

1,272

8.6

9.5

23.7

32.7

6.1

4.4

0.6

0.6

10.1

12.5

0.4

0.3

Transport Corporation of

Accumulate

263

293

1,989

2,830

3,350

8.8

9.0

14.4

18.3

18.3

14.4

2.8

2.5

15.4

17.1

0.8

0.7

India

Elecon Engineering

Neutral

87

-

952

1,452

1,596

13.7

14.7

4.2

6.2

21.1

14.0

1.7

1.5

8.1

11.2

1.0

0.8

Surya Roshni

Accumulate

139

152

610

2,992

3,223

8.4

8.7

15.2

19.3

9.2

7.2

0.9

0.8

10.1

11.5

0.5

0.5

MT Educare

Buy

112

141

447

275

355

18.3

17.3

7.4

8.8

15.2

12.7

3.1

2.7

20.2

21.1

1.5

1.2

Radico Khaitan

Buy

92

112

1,222

1,565

1,687

11.9

12.4

5.4

6.6

17.0

13.9

1.4

1.3

8.0

9.0

1.3

1.2

Garware Wall Ropes

Neutral

302

-

661

875

983

10.4

10.5

23.1

27.5

13.1

11.0

1.9

1.6

14.1

14.6

0.8

0.6

Source: Company, Angel Research; Note: *December year end; #September year end; &October year end; Price as on July 24, 2015

Market Outlook

July 27, 2015

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a registered

entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164.

Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities

Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in

the company covered by Analyst. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst has not served as an officer,

director or employee of company covered by Analyst and has not been engaged in market making activity of the company covered by

Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way responsible for any

loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Pvt.

Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any

representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking

Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance,

or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or

in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may have

investment positions in the stocks recommended in this report.