Market Outlook

November 2, 2015

Market Cues

Domestic Indices

Chg (%)

(Pts)

(Close)

Indian markets are expected to open in the red tracking the SGX Nifty and Asian

BSE Sensex

(0.7)

(181)

26,657

markets.

Nifty

(0.6)

(46)

8,066

US markets closed in the red due to some late selling pressure after choppy trading

Mid Cap

(0.1)

(14)

10,975

on account of mixed economic data. While US personal income and consumer

Small Cap

(0.8)

(89)

11,315

spending inched up marginally, both were lower than expected. US consumer

sentiment too inched up in October, but missed expectations.

Bankex

0.9

180

19,774

European markets also closed on a negative note led by weak economic data.

Despite the stimulus, Eurozone consumer prices remained flat in October. Eurozone

Global Indices

Chg (%)

(Pts)

(Close)

unemployment too remained high despite a marginal decline.

Dow Jones

(0.5)

(92)

17,664

The Indian markets fell for the fifth straight session led by uncertainty over the

Nasdaq

(0.4)

(21)

5,054

outcome of Bihar elections and disappointing earnings from majors L&T and ITC.

FTSE

(0.5)

(34)

6,361

Nikkei

0.8

147

19,083

News & Result Analysis

Hang Seng

(0.8)

(180)

22,640

Result Review: ICICI Bank, Larsen & Toubro, Indoco Remedies, GSK Pharma,

Shanghai Com

(0.1)

(5)

3,383

IPCA Labs, Relaxo Footwear

Detailed analysis on Pg2

Advances / Declines

BSE

NSE

Investor’s Ready Reckoner

Advances

964

479

Key Domestic & Global Indicators

Declines

1,652

1,024

Stock Watch: Latest investment recommendations on 150+ stocks

Unchanged

190

71

Refer P7 onwards

Top Picks

Volumes (` Cr)

CMP

Target

Upside

Company

Sector

Rating

BSE

3,187

(`)

(`)

(%)

Axis Bank

Financials

Buy

475

630

32.6

NSE

19,049

HCL Tech

IT

Buy

870

1,132

30.2

ICICI Bank

Financials

Buy

277

348

25.6

Net Inflows (` Cr)

Net

Mtd

Ytd

Power Grid

Power

Buy

129

170

32.0

FII

536

5,567

(13,457)

TCS

IT

Buy

2,497

3,165

26.7

MFs

(301)

1,307

48,719

More Top Picks on Pg5

Key Upcoming Events

Top Gainers

Price (`)

Chg (%)

Previous

Consensus

Date

Region

Event Description

Jet Airways

437

9.3

Reading

Expectations

Nov 1

China

PMI Manufacturing

49.8

50.0

Adani Ent.

1,669

6.7

Nov 2

US

ISM manufacturing PMI

50.2

50.0

Bharat Forge

859

5.4

Nov 2

China

Chinese Caixin Manufacturing PMI

47.2

47.6

Sun TV

396

5.2

Nov 2

UK

ISM manufacturing PMI

51.5

51.3

Glenmark

991

5.0

Top Losers

Price (`)

Chg (%)

Mphasis

478

(7.6)

Wockhardt Pharma

1,495

(6.5)

Vedanta

100

(6.4)

Apollo Tyre

171

(6.2)

Just Dial

806

(5.7)

As on October 30, 2015

Market Outlook

November 2, 2015

Result Review

ICICI Bank (CMP: `277/ TP: `348/ Upside: 25.6%)

ICICI Bank reported a decent set of number for 2QFY2016 results with PAT growth

of 11.9% yoy to `3,030cr in 2QFY2016 which was in-line with our expectations.

NII grew at steady pace of 12.8% yoy which was in-line with the expectations likely

due to growth in advances at 13.3% yoy as well as flat margins sequentially. The

bank managed to keep the operating expenses under check which grew 15.0%

yoy on a low base of the same quarter last year; below our estimates. The

provisions saw a decline of 1.4% qoq which was below our expectations.

The bank continues to grow its retail franchise and has seen healthy growth in

retail loan book at 25% yoy which now constituted about 44% of the loan portfolio

of the bank as of September 30, 2015. Also, the growing retail franchise is visible

in CASA ratio which came at 45.1% as against 43.7% in the year ago period.

The country's largest private sector lender today approved sale of 9.0% stake in

insurance company ICICI Lombard to Fairfax Financial Holdings Limited at a

valuation of `17,225cr which was higher than our estimates. Incorporating the

implied value from this stake sale, our SOTP based value for the non-life business

will increase by `10 per share.

Asset quality was in-line with our expectations since the management has guided

for more additions to stressed assets during the year. The Gross NPA ratio rose by

9bp qoq to 3.77% while the Net NPA ratio rose by 7bps qoq to 1.65% in

2QFY2016. However, we would wait for more clarity on the stress assets additions

during the year. At CMP, the bank’s core banking business (after adjusting

`58/share towards value of subsidiaries) is trading at 1.5x FY2017E ABV. We

recommend BUY rating on the stock.

Y/E

Op. Inc

NIM

PAT

EPS

ABV ROA ROE

P/E P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2016E

35,168

3.4

12,479

21.4

124.9

1.6

14.7

12.7

2.2

FY2017E

40,517

3.4

14,680

25.2

149.8

1.6

15.2

10.8

1.8

Larsen & Toubro (CMP: `1,414 / TP: `1,646 / Upside: 16.6%)

Larsen & Toubro (L&T; standalone entity) reported a poor set of numbers for

2QFY2016, both at the top-line and the bottom-line level. The company reported

a lower-than-expected top-line growth, i.e. of 4.1% YoY to INR 13,234cr. The

subtle revenue growth is owing to lower revenue booking across Infrastructure,

Metallurgical & Material Handling and Heavy Engineering segments. The

disappointment continued further towards the EBITDA level; the company reported

a 290bp YoY decline in the EBITDA margin to 7.6%. Revenue de-growth and

56.5% YoY increase in sales, administration and other expenses led to EBITDA

margin compression. During the quarter, L&T reported a gain from stake sale in a

subsidiary and an associate company to the tune of INR 546cr. Adjusting for the

same, the Adj. PAT of the company came in at INR 643cr (lower than our estimate

of INR 1,084cr). The Adj. PAT was impacted due to increase in interest expenses by

22.7% YoY.

Market Outlook

November 2, 2015

For 2QFY2016, L&T reported order inflows of INR 28,620cr. Due to lower order

inflows in two consecutive quarters (1QFY2016 & 2QFY2016), the Management

has revised down its order inflow guidance for FY2016E to 5-7% (from 15%

earlier).

Even though there have been delays on the awarding front, we believe in the

Indian Infra growth story. Given the company’s market positioning, we see L&T to

be well positioned to gain from an expected gradual recovery in the capex cycle,

given its exposure to a range of sectors, and better cash flow generating potential

vis-a-vis its peers. We maintain our positive view on L&T; we maintain our BUY

rating on the stock with price target of `1,646.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BVEV/EBITDAEV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

64,148

11.5

5,776

61.5

13.4

22.9

2.3

19.5

2.2

FY2017E

73,241

11.7

6,155

65.6

14.0

21.5

2.1

16.9

2.0

Indoco Remedies (CMP: `326 / TP: /Upside : )

For 2QFY2016, the company posted numbers lower than expected. The company

posted a 9.4% growth in sales to end the period at `248cr V/s `272cr expected

and `226cr in 2QFY2015, on back of domestic and exports posting a growth of

1.2% and 23.6% respectively. In domestic markets (`146cr), posted a growth of

1.2% yoy, mainly on back a tepid formulation sales (`138cr), a yoy growth of

0.5%, while API sales (`7.6cr), posted a 11.7% yoy growth. In exports (`101cr), a

yoy growth of 23.6%, on back of formulation exports (`92.8cr) a growth of 23.7%

yoy, while API exports (`6.9cr) posted a yoy growth of 3.6%.

On operating front, the EBITDA margins came in at 15.5% V/s 20.9% expected V/s

20.6% in 2QFY2015, on back of lower than expected sales and 28.3% yoy and

82.6% yoy rise in staff expenditure and R&D expenditure respectively. The R&D

expenditure during the quarter was 3.6% of sales V/s 2.2% of sales in 2QFY2015.

Thus, the Adj. net profit came in at `22.6cr V/s `33.4cr expected and `22.4cr in

2QFY2015, a yoy growth of 0.9%. The lower than expected net profit is on back of

lower than expected sales and OPM. On back of valuations, we maintain our

neutral stance on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,008

18.2

120

13.1

21.2

24.9

4.9

15.9

2.9

FY2017E

1,262

18.2

143

15.5

21.1

21.0

4.1

13.4

2.4

Market Outlook

November 2, 2015

GSK Pharma (CMP: `3,295 / TP: /Upside : )

For 2QFY2016, the company posted a disappointing numbers, on back of lower

than expected sales. For the quarter, the company posted sales of `692cr V/s

`720cr expected a dip of 6.4% yoy. The dip in sales is on back of the supply

constraints. On the operating profits, the company posted gross margins of

56.4% V/s 53.5% during the last corresponding period. Inspite of the same, the

OPM’s came in at 17.4% V/s 21.3% during the last corresponding period, mainly

on back of the lower sales during the quarter. This was against the expectations of

20.2%. Thus the reported net profit came in at `96cr V/s `129cr in during the last

corresponding period. However Adj. net profit came in at `101cr V/s `129cr, a

yoy dip of 21.4%. We remain neutral on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

2,870

20.0

504

59.5

28.5

63.0

18.6

52.3

10.5

FY2017E

3,158

22.1

574

68.3

34.3

54.8

19.1

43.3

9.6

IPCA Labs (CMP: `782 / TP: `900 / Upside: 15.0%)

For 2QFY2016, the company posted sales in line while, the net profit posted

numbers lower than estimates. The company, posted a 4.7% de-growth in sales to

end the period at `739cr V/s `750cr expected and `775cr in 2QFY2015, on back

of domestic and exports posting a dip of 2.3% and 6.9%, respectively. Domestic

markets (`364cr) posted a dip of 2.3% yoy, mainly on back of tepid formulation

sales (`331cr), a yoy growth of 0.9%, while API sales (`33cr), a 25.3% yoy dip.

Exports (`375cr) saw a yoy fall of 6.9%, on back of dip in formulation exports

(`227cr), a dip of 25.7% yoy, while API exports (`147cr) posted a yoy growth of

52.9%.

On operating front, the EBITDA margins came in at 10.6% V/s 11.4% expected V/s

10.0% in 2QFY2015, on back of lower than expected sales during the quarter,

while Gross margins , came in at 62.0% V/s 65.0% in 2QFY2015. Thus, the Adj.

net profit came in at `31cr V/s `41cr expected and `68cr in 2QFY2015, a yoy dip

of 54.3%.

However, on back of `24cr forex losses, the company posted a net profit of `12cr

V/s `61cr, a yoy dip of 80.9% yoy. While the current performance of the company

is impacted on back of its key plants being under the USFDA scanner, we believe

once out of it, the company can bounce back to its normalized ROE’s of 25%. Thus

we maintain our buy with a target price of `900.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

3,363

12.9

169

13.4

7.4

58.4

4.2

24.8

3.2

FY2017E

3,909

18.6

354

28.0

14.0

27.9

3.7

14.8

2.8

Market Outlook

November 2, 2015

Relaxo Footwears (CMP: `524 / TP: - / Upside: -)

For 2QFY2016, Relaxo reported numbers that were in-line with our estimates. The

top-line grew by 15.8% yoy to `384cr, the same was lower than our estimate of

`398cr. The gross margin expanded by 267bp yoy to 58.7% and net raw material

cost as a percentage sales came in at 41.3%. On the back of lower raw material

cost, the EBITDA margin expanded by 174bp yoy to 12.8% vis-à-vis our estimate

of 11.6%. The interest expense has increased by 39.6% yoy to `6cr (as the debt

quantum has increased) and the other income during the quarter was higher as it

included sale of Long Term investment for the amount of `4.2cr. Adjusting for the

sale of investment, the net profit grew by 34.6% yoy to `23cr, which same as our

estimate. At current market price, the stock trades at 35.3x its FY2017E earnings.

We have a Neutral view on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,760

14.3

135

11.2

31.3

46.6

12.7

25.6

3.7

FY2017E

2,120

15.0

178

14.9

30.9

35.3

9.5

19.9

3.0

Economic and Political News

Government unveils draft civil aviation policy to raise FDI limit beyond 50%,

make air travel cheaper

Rajasthan attracts investments of ~`1.5 lakh cr ahead of the Resurgent

Rajasthan Partnership Summit from solar, mining, textiles & petroleum sectors

India may need to import 10 MT of pulses to tame prices: Assocham Study

Corporate News

RCom to take over SSTL’s telecom business in ~`5,000cr cashless deal

IOC eyes 5-10% stake in Russia's Vankor oilfield

M&M October sales up by 20% led by festive season push

Market Outlook

November 2, 2015

Top Picks ★★★★★

Large Cap

Market Cap

CMP

Target

Upside

Company

Rationale

(` Cr)

(`)

(`)

(%)

Healthy pace of branch expansion, backed by distribution

Axis Bank

1,12,936

475

630

32.6

network, will be the driving force for the bank’s retail business

and overall earnings.

The stock is trading at attractive valuations and is factoring all

HCL Tech

1,22,281

870

1,132

30.2

the bad news.

Due to its robust franchise and capital adequacy position, the

bank is well positioned to grow by at least a few percentage

ICICI Bank

1,60,873

277

348

25.6

points higher than the average industry growth rate from a

structural point of view.

Back on the growth trend, expect a long term growth of 14% to

Infosys

2,60,944

1,136

1,306

15.0

be a US$20bn in FY2020.

Government thrust on Renewable sector and strong order book

Inox Wind

8,829

398

505

26.9

would drive future growth.

LICHF continues to grow its retail loan book at a healthy pace

with improvement in asset quality. We expect the company to

LIC HFL

24,229

480

571

18.9

post a healthy loan book which is likely to reflect in a strong

earnings growth.

Direct beneficiary of the huge investments lined up in the power

Power Grid

67,357

129

170

32.0

transmission sector.

Growth to pick up from 2HFY2017, attractive given the risk-

TCS

4,92,075

2,497

3,165

26.7

reward.

Tech Mahindra

51,865

539

646

19.9

Acquisitions, to drive growth, normalised valuations attractive.

An improving liability franchise, capital adequacy well above

Yes Bank

31,804

759

914

20.4

Basel-III requirements and lowest NPA ratio in the industry, will

help Yes Bank to deliver a stronger growth.

Source: Company, Angel Research

Mid Cap

Market Cap

CMP

Target

Upside

Company

Rationale

(` Cr)

(`)

(`)

(%)

Bajaj Electricals

2,481

246

341

38.7

Visible turnaround in E&P business to drive the earnings

Garware Wall Ropes

752

344

390

13.5

Higher exports & easing material prices to drive profitability

Comfortable balance sheet to support strong growth; this

MBL Infrastructures

866

209

285

36.4

coupled with attractive valuation to lead to rerating.

New product introductions and increased sourcing by clients to

Minda Industries

827

521

652

25.1

enable outpace industry growth

Strong brand & quality teaching with innovative technologies &

MT Educare

546

137

169

23.3

higher government educational spending to boost growth

Earnings boost on back of stable material prices and favourable

Radico Khaitan

1,346

101

119

17.6

pricing environment. Valuation discount to peers provides

additional comfort

Structural shift in the Lighting industry towards LED lighting will

Surya Roshni

585

134

183

37.1

drive growth.

Tree House

1,166

276

347

25.9

Robust expansion plan for pre-schools to drive growth

Source: Company, Angel Research

Market Outlook

November 2, 2015

Quarterly Bloomberg Brokers Consensus Estimate

Reliance Capital - November 02, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

PAT

224

217

3.0

229

(2.4)

Adani Ports and Special Economic Zone Ltd - November 02, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

1,773

1,415

25.3

1,723

2.9

EBITDA

1,210

1,074

12.7

1,164

4.0

EBITDA margin (%)

68.3

75.9

67.6

Net profit

670

574

16.8

641

4.6

United Spirit Limited- November 02, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

2,341

2,157

8.6

1,988

17.7

EBITDA

258

233

10.8

202

27.9

EBITDA margin (%)

11.0

10.8

10.2

Net profit

86

(28)

410.1

20

333.7

Market Outlook

November 02, 2015

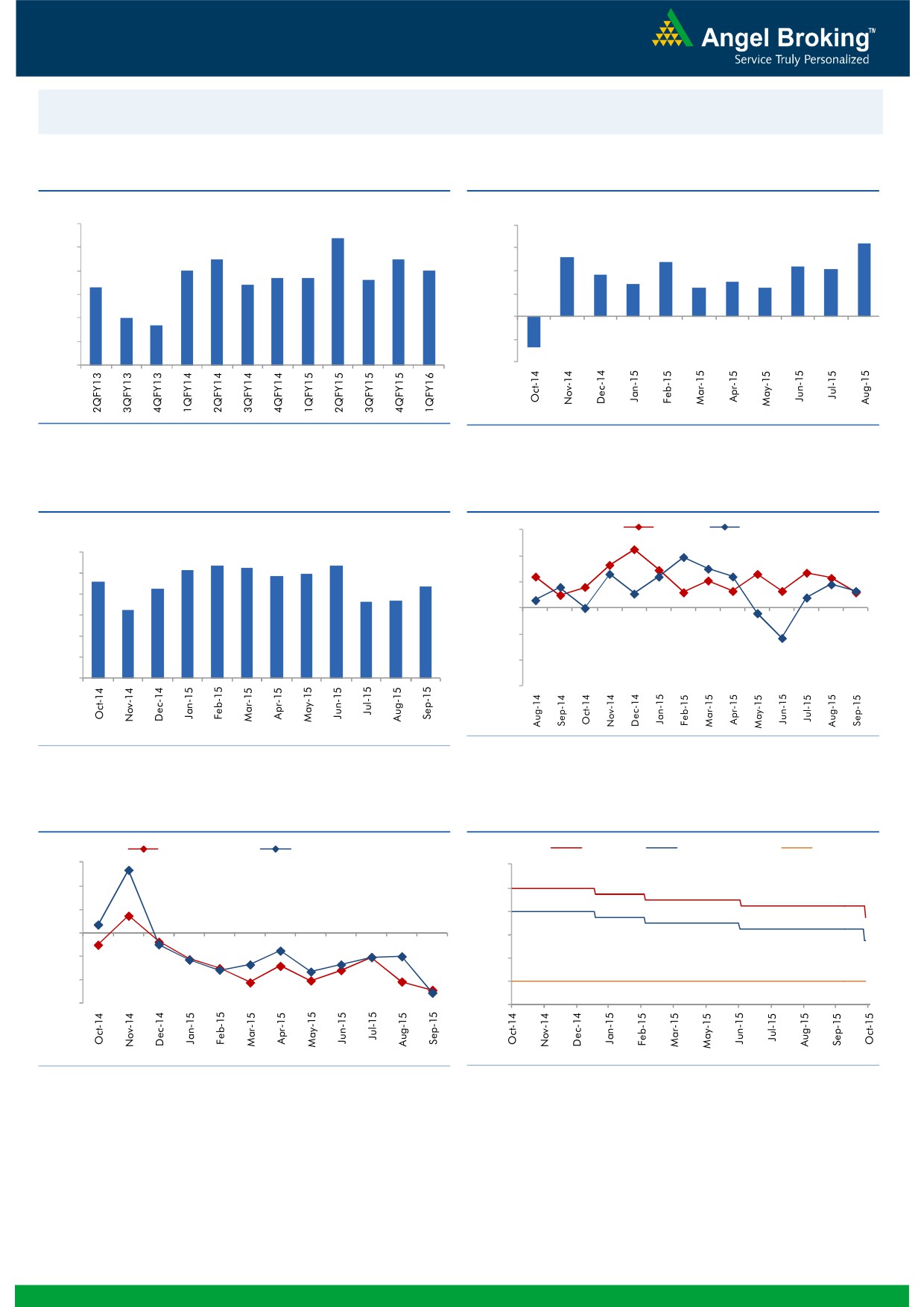

Macro watch

Exhibit 1: Quarterly GDP trends

Exhibit 2: IIP trends

(%)

(%)

9.0

8.4

8.0

6.4

7.5

7.5

5.2

8.0

6.0

4.8

7.0

7.0

4.4

4.1

6.7

6.7

6.6

3.6

7.0

6.4

4.0

2.8

3.0

6.3

2.5

2.5

6.0

2.0

5.0

4.7

5.0

-

4.0

(2.0)

3.0

(4.0)

(2.7)

Source: CSO, Angel Research

Source: MOSPI, Angel Research

Exhibit 3: Monthly CPI inflation trends

Exhibit 4: Manufacturing and services PMI

(%)

56.0

Mfg. PMI

Services PMI

6.0

5.4

5.3

5.4

54.0

5.2

5.0

4.9

4.6

5.0

4.3

4.4

52.0

3.7

3.7

4.0

3.3

50.0

3.0

2.0

48.0

1.0

46.0

-

44.0

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Source: MOSPI, Angel Research

Exhibit 5: Exports and imports growth trends

Exhibit 6: Key policy rates

(%)

Exports yoy growth

Imports yoy growth

(%)

Repo rate

Reverse Repo rate

CRR

30.0

9.00

20.0

8.00

10.0

7.00

0.0

6.00

(10.0)

5.00

(20.0)

4.00

(30.0)

3.00

Source: Bloomberg, Angel Research

Source: RBI, Angel Research

Market Outlook

November 02, 2015

Global watch

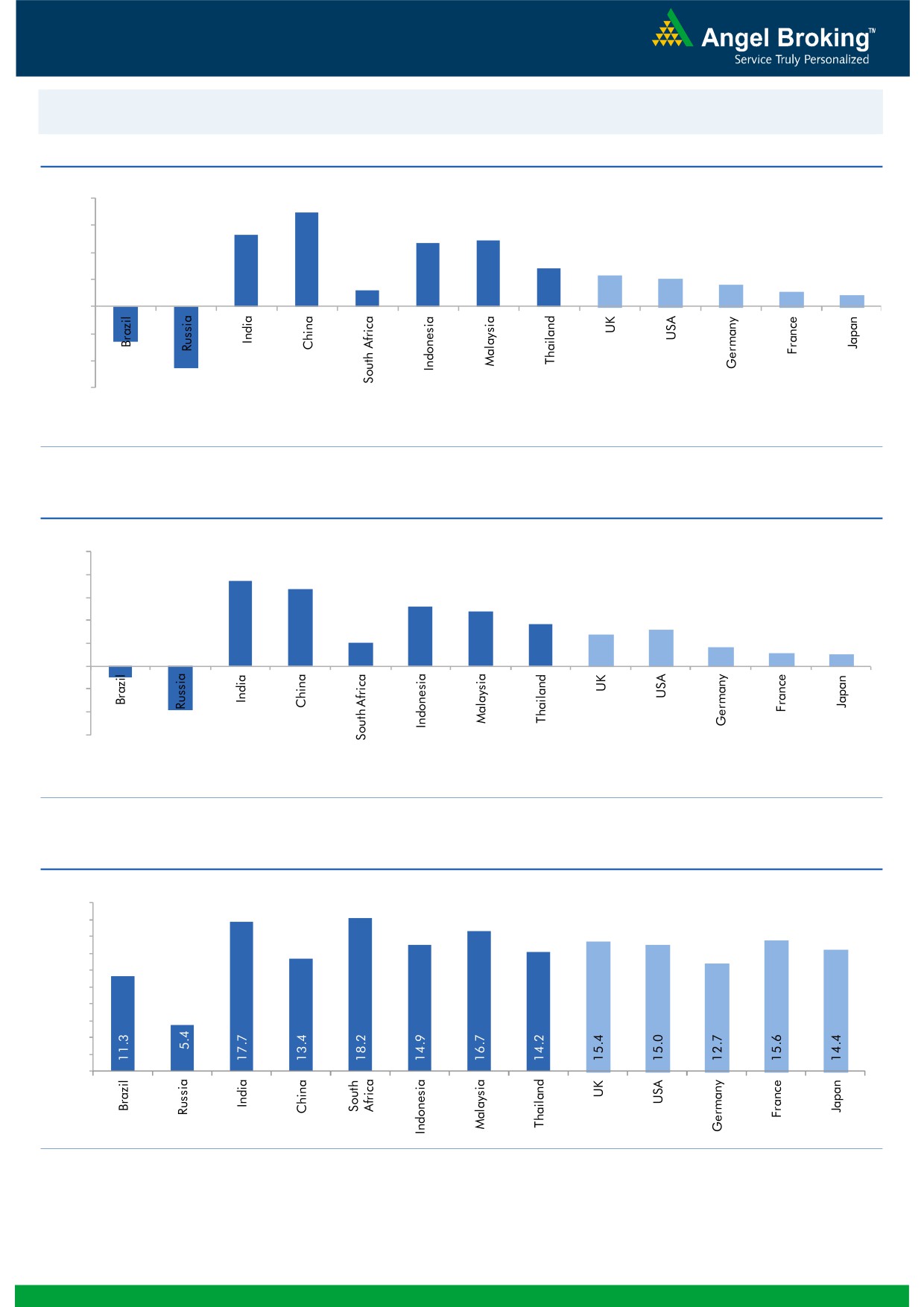

Exhibit 1: Latest quarterly GDP Growth (%, yoy) across select developing and developed countries

(%)

8.0

6.9

6.0

5.3

4.9

4.7

4.0

2.8

2.3

2.0

1.6

2.0

1.2

1.1

0.8

(2.6)

-

(2.0)

(4.0)

(4.6)

(6.0)

Source: Bloomberg, Angel Research

Exhibit 2: 2015 GDP Growth projection by IMF (%, yoy) across select developing and developed countries

(%)

10.0

7.5

8.0

6.8

5.2

6.0

4.8

3.7

3.1

4.0

2.7

2.0

1.6

1.2

1.0

2.0

-

(2.0)

(4.0)

(1.0)

(3.8)

(6.0)

Source: IMF, Angel Research

Exhibit 3: One year forward P-E ratio across select developing and developed countries

(x)

20.0

18.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

Source: IMF, Angel Research

Market Outlook

November 02, 2015

Exhibit 4: Relative performance of indices across globe

Returns (%)

Country

Name of index

Closing price

1M

3M

1YR

Brazil

Bovespa

45,869

(2.5)

(6.2)

(16.0)

Russia

Micex

1,712

2.9

7.3

15.0

India

Nifty

8,066

1.5

(4.2)

(3.1)

China

Shanghai Composite

3,383

10.8

(8.7)

39.8

South Africa

Top 40

48,317

5.8

3.1

8.9

Mexico

Mexbol

44,543

4.2

(0.5)

(1.1)

Indonesia

LQ45

760

8.3

(4.5)

(12.5)

Malaysia

KLCI

1,666

2.3

(1.1)

(10.2)

Thailand

SET 50

900

3.6

(4.1)

(14.6)

USA

Dow Jones

17,664

7.2

(1.4)

1.6

UK

FTSE

6,361

3.8

(4.2)

(2.8)

Japan

Nikkei

19,083

7.7

(10.7)

16.3

Germany

DAX

10,850

13.6

(7.5)

16.3

France

CAC

4,898

9.8

(5.0)

15.7

Source: Bloomberg, Angel Research

Stock Watch

November 02, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Agri / Agri Chemical

Rallis

Neutral

207

-

4,017

2,075

2,394

14.4

14.4

9.5

11.0

21.7

18.8

4.3

3.7

21.1

21.3

2.0

1.7

United Phosphorus

Accumulate

461

510

19,754

13,698

15,752

17.6

17.6

32.1

38.5

14.4

12.0

2.8

2.3

21.4

21.3

1.5

1.3

Auto & Auto Ancillary

Ashok Leyland

Buy

94

111

26,652

18,763

22,357

11.1

11.2

3.6

4.8

26.0

19.5

4.8

4.4

18.7

22.6

1.4

1.1

Bajaj Auto

Neutral

2,550

-

73,777

24,115

27,600

21.3

21.0

136.8

157.2

18.6

16.2

6.0

5.1

32.2

31.5

2.6

2.3

Eicher Motors

Buy

17,762

22,859

48,210

11,681

15,550

15.3

16.9

358.5

564.3

49.6

31.5

14.9

11.1

29.8

34.9

4.0

3.0

Hero Motocorp

Neutral

2,585

-

51,619

28,561

31,559

14.7

14.7

151.1

163.2

17.1

15.8

6.6

5.6

38.7

35.6

1.6

1.5

L G Balakrishnan & Bros Neutral

464

-

729

1,254

1,394

11.6

11.8

35.9

41.7

12.9

11.2

1.8

1.5

13.5

13.8

0.7

0.6

Mahindra and Mahindra Accumulate

1,183

1,357

73,444

37,986

42,660

12.8

13.2

51.6

61.9

22.9

19.1

3.4

3.0

14.6

15.6

1.6

1.3

Maruti

Accumulate

4,449

4,960

134,385

57,865

68,104

16.4

16.7

176.3

225.5

25.2

19.7

4.9

4.2

19.4

21.2

2.1

1.7

Minda Industries

Buy

521

652

827

2,567

2,965

7.3

8.0

38.8

54.3

13.4

9.6

1.9

1.6

14.4

16.8

0.4

0.4

Rane Brake Lining

Accumulate

322

366

255

454

511

11.1

11.4

23.8

28.1

13.5

11.4

1.9

1.7

14.2

15.3

0.7

0.6

Setco Automotive

Neutral

227

-

607

594

741

12.7

13.7

8.4

15.8

27.1

14.4

2.8

2.4

10.4

16.9

1.5

1.2

Tata Motors

Accumulate

384

424

110,999

264,038

297,882

13.8

13.9

34.5

38.9

11.1

9.9

1.9

1.6

17.6

16.8

0.6

0.6

TVS Motor

Accumulate

265

296

12,609

11,845

14,040

7.2

9.0

10.4

17.4

25.5

15.3

6.4

4.9

25.1

32.0

1.0

0.9

Amara Raja Batteries

Buy

903

1,040

15,427

4,892

5,871

17.4

17.6

28.8

37.1

31.4

24.3

7.3

5.9

23.4

24.1

3.1

2.5

Exide Industries

Accumulate

150

162

12,737

6,950

7,784

14.4

14.8

6.6

7.3

22.7

20.5

2.9

2.6

12.6

12.8

1.6

1.4

Apollo Tyres

Neutral

171

-

8,707

12,576

12,978

16.8

16.1

22.3

19.9

7.7

8.6

1.3

1.2

17.2

13.4

0.8

0.8

Ceat

Neutral

1,082

-

4,376

6,041

6,597

14.1

13.7

99.5

111.9

10.9

9.7

2.1

1.8

19.6

18.5

0.9

0.8

JK Tyres

Neutral

101

-

2,300

7,446

7,669

15.2

14.0

19.6

18.4

5.2

5.5

1.3

1.1

25.2

19.5

0.7

0.6

Swaraj Engines

Neutral

937

-

1,164

552

630

14.2

14.7

44.6

54.1

21.0

17.3

4.9

4.4

23.2

25.6

2.0

1.7

Subros

Neutral

89

-

534

1,268

1,488

11.6

11.9

3.7

6.6

24.1

13.5

1.6

1.5

6.8

11.4

0.7

0.6

Indag Rubber

Neutral

195

-

511

283

329

17.0

17.2

13.0

15.4

15.0

12.6

3.3

2.7

21.8

21.6

1.5

1.3

Capital Goods

ACE

Neutral

42

-

419

660

839

4.7

8.2

1.0

3.9

42.4

10.9

1.3

1.2

3.2

11.3

0.8

0.6

BEML

Neutral

1,167

-

4,859

3,277

4,006

6.0

8.9

29.2

64.3

40.0

18.2

2.2

2.0

5.7

11.7

1.6

1.2

BGR Energy

Neutral

110

-

790

3,615

3,181

9.5

9.4

16.7

12.4

6.6

8.8

0.6

0.6

10.0

7.0

0.6

0.8

BHEL

Neutral

199

-

48,671

33,722

35,272

10.8

11.7

10.5

14.2

18.9

14.0

1.4

1.3

7.0

9.0

1.5

1.5

Blue Star

Neutral

389

-

3,499

3,649

4,209

5.0

5.9

9.2

14.7

42.5

26.4

7.7

7.2

9.1

17.5

1.1

0.9

Crompton Greaves

Buy

174

204

10,902

13,484

14,687

4.9

6.2

4.5

7.1

38.7

24.5

2.7

2.6

7.2

10.8

0.9

0.9

Inox Wind

Buy

398

505

8,829

4,980

5,943

17.0

17.5

26.6

31.6

15.0

12.6

4.5

3.3

35.0

30.0

1.9

1.6

Stock Watch

November 02, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Capital Goods

KEC International

Neutral

134

-

3,449

8,791

9,716

6.1

6.8

5.4

8.2

24.8

16.4

2.5

2.3

10.0

14.0

0.6

0.6

Thermax

Neutral

848

-

10,104

6,413

7,525

7.4

8.5

30.5

39.3

27.8

21.6

4.3

3.7

15.0

17.0

1.6

1.3

Cement

ACC

Buy

1,376

1,630

25,836

13,151

14,757

16.4

18.3

63.9

83.4

21.5

16.5

2.8

2.5

13.3

16.1

1.8

1.5

Ambuja Cements

Accumulate

207

233

32,171

11,564

12,556

19.4

20.7

8.9

10.1

23.3

20.5

2.9

2.8

12.8

13.8

2.4

2.2

India Cements

Buy

78

112

2,405

4,716

5,133

15.9

16.9

3.7

7.5

21.2

10.4

0.8

0.7

3.8

7.3

0.8

0.7

JK Cement

Accumulate

678

767

4,738

4,056

4,748

14.5

17.0

22.6

41.1

30.0

16.5

2.7

2.4

9.3

15.3

1.6

1.3

J K Lakshmi Cement

Buy

372

430

4,376

2,947

3,616

16.7

19.9

11.5

27.2

32.3

13.7

3.1

2.7

9.8

20.8

1.9

1.5

Mangalam Cements

Neutral

227

-

607

1,053

1,347

10.5

13.3

8.4

26.0

27.1

8.7

1.1

1.1

4.3

12.5

1.0

0.7

Orient Cement

Accumulate

164

183

3,353

1,854

2,524

21.2

22.2

7.7

11.1

21.3

14.7

3.1

2.6

13.3

15.7

2.5

1.8

Ramco Cements

Neutral

362

-

8,612

4,036

4,545

20.8

21.3

15.1

18.8

24.0

19.2

2.9

2.6

12.9

14.3

2.6

2.3

Shree Cement^

Neutral

12,328

-

42,948

7,150

8,742

26.7

28.6

228.0

345.5

54.1

35.7

8.0

6.7

15.7

20.3

5.8

4.6

UltraTech Cement

Accumulate

2,884

3,282

79,132

25,021

30,023

19.1

21.6

89.0

132.0

32.4

21.9

3.8

3.3

12.2

15.9

3.2

2.7

Construction

ITNL

Neutral

94

-

3,084

7,360

8,825

34.0

35.9

1.0

5.0

93.8

18.8

0.4

0.4

0.3

1.4

3.9

3.7

KNR Constructions

Neutral

581

-

1,633

915

1,479

14.3

13.9

20.3

37.2

28.6

15.6

2.6

2.3

9.6

15.6

1.9

1.2

Larsen & Toubro

Buy

1,411

1,646

131,330

64,148

73,241

11.5

11.7

62.0

66.0

22.8

21.4

2.3

2.1

13.4

14.0

2.2

2.0

Gujarat Pipavav Port

Neutral

161

-

7,786

629

684

51.0

52.2

6.4

5.9

25.2

27.3

3.3

3.0

15.9

12.7

12.0

10.9

MBL Infrastructures

Buy

209

285

866

2,313

2,797

12.2

14.6

19.0

20.0

11.0

10.5

1.1

1.1

11.3

10.6

1.1

1.0

Nagarjuna Const.

Neutral

81

-

4,475

7,892

8,842

8.3

9.1

2.4

5.3

33.5

15.2

1.3

1.3

4.2

8.6

0.8

0.7

PNC Infratech

Neutral

513

-

2,631

1,798

2,132

13.2

13.5

22.0

30.0

23.3

17.1

2.1

1.9

11.5

11.4

1.6

1.3

Simplex Infra

Neutral

324

-

1,605

6,241

7,008

10.4

10.7

20.0

36.0

16.2

9.0

1.3

1.2

6.8

11.1

0.8

0.7

Financials

Allahabad Bank

Neutral

75

-

4,504

8,332

9,259

2.8

2.8

21.0

25.6

3.6

2.9

0.4

0.3

9.8

10.9

-

-

Axis Bank

Buy

475

630

112,936

26,473

31,527

3.5

3.6

35.7

43.5

13.3

10.9

2.6

2.2

17.9

18.9

-

-

Bank of Baroda

Neutral

160

-

36,936

19,105

21,474

2.0

2.0

19.1

24.8

8.4

6.5

0.9

0.8

10.2

12.1

-

-

Bank of India

Neutral

132

-

10,422

15,972

17,271

1.9

2.0

15.3

33.4

8.6

4.0

0.4

0.3

3.6

7.6

-

-

Canara Bank

Neutral

277

-

15,044

15,251

16,725

2.0

2.0

59.3

68.6

4.7

4.0

0.5

0.5

10.1

10.7

-

-

Dena Bank

Neutral

42

-

2,357

3,440

3,840

2.1

2.3

7.3

10.0

5.8

4.2

0.4

0.4

6.1

7.9

-

-

Federal Bank

Neutral

54

-

9,329

3,477

3,999

3.0

3.0

5.0

6.2

10.8

8.7

1.1

1.0

10.6

11.9

-

-

HDFC

Neutral

1,257

-

198,346

10,358

11,852

3.3

3.3

41.1

47.0

30.6

26.7

5.8

5.3

24.7

24.9

-

-

HDFC Bank

Buy

1,097

1,262

276,258

38,309

47,302

4.3

4.3

49.3

61.1

22.2

18.0

3.8

3.3

18.5

19.7

-

-

Stock Watch

November 02, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Financials

ICICI Bank

Buy

277

348

160,873

35,168

40,517

3.4

3.4

21.4

25.2

13.0

11.0

2.2

1.9

14.7

15.2

-

-

IDBI Bank

Neutral

86

-

13,778

9,625

10,455

1.8

1.8

8.5

14.2

10.1

6.0

0.6

0.6

5.9

9.3

-

-

Indian Bank

Neutral

125

-

6,008

6,160

6,858

2.5

2.5

24.5

29.8

5.1

4.2

0.4

0.4

7.7

8.6

-

-

LIC Housing Finance

Buy

480

571

24,229

3,101

3,745

2.5

2.5

33.0

40.2

14.6

12.0

2.7

2.3

19.7

20.5

-

-

Oriental Bank

Neutral

135

-

4,045

7,643

8,373

2.4

2.4

37.2

45.4

3.6

3.0

0.3

0.3

8.2

9.4

-

-

Punjab Natl.Bank

Neutral

128

-

25,213

23,638

26,557

2.8

2.8

17.9

27.2

7.2

4.7

0.7

0.6

8.5

12.0

-

-

South Ind.Bank

Neutral

21

-

2,768

1,965

2,185

2.5

2.5

2.5

3.3

8.2

6.2

0.8

0.7

9.5

11.7

-

-

St Bk of India

Buy

237

295

184,133

82,520

93,299

2.7

2.8

20.0

24.5

11.8

9.7

1.3

1.1

11.5

12.8

-

-

Union Bank

Neutral

157

-

10,793

12,646

14,129

2.3

2.4

31.0

39.1

5.1

4.0

0.5

0.5

9.8

11.4

-

-

Vijaya Bank

Neutral

37

-

3,157

3,536

3,827

1.9

1.9

5.5

6.7

6.7

5.5

0.6

0.5

7.8

8.8

-

-

Yes Bank

Buy

759

914

31,789

7,228

9,043

3.2

3.3

57.7

69.4

13.2

10.9

2.3

2.0

19.1

19.6

-

-

FMCG

Asian Paints

Neutral

829

-

79,489

16,553

19,160

16.0

16.2

17.7

21.5

46.9

38.5

12.4

11.2

29.4

31.2

4.6

4.0

Britannia

Neutral

3,227

-

38,717

8,065

9,395

9.6

10.2

47.2

65.5

68.4

49.3

22.7

21.5

38.3

41.2

4.7

4.0

Colgate

Neutral

956

-

26,011

4,836

5,490

19.5

19.7

48.5

53.2

19.7

18.0

14.5

12.6

99.8

97.5

5.3

4.6

Dabur India

Neutral

270

-

47,469

9,370

10,265

17.1

17.2

7.3

8.1

36.8

33.4

11.1

9.0

33.7

30.6

5.0

4.5

GlaxoSmith Con*

Neutral

5,976

-

25,133

4,919

5,742

17.2

17.4

168.3

191.2

35.5

31.3

10.1

8.6

28.8

28.9

4.7

4.0

Godrej Consumer

Neutral

1,264

-

43,040

10,168

12,886

16.1

16.1

32.1

38.4

39.4

32.9

8.0

7.4

19.7

21.0

4.3

3.4

HUL

Neutral

802

-

173,510

34,940

38,957

17.5

17.7

20.8

24.7

38.6

32.5

42.9

34.3

110.5

114.2

4.8

4.3

ITC

Buy

335

409

268,647

41,068

45,068

37.8

37.4

13.9

15.9

24.1

21.1

8.1

7.1

34.1

33.8

6.2

5.6

Marico

Neutral

387

-

24,978

6,551

7,766

15.7

16.0

10.4

12.5

37.3

31.0

10.8

9.0

33.2

32.4

3.7

3.2

Nestle*

Accumulate

6,180

6,646

59,580

11,291

12,847

22.2

22.3

158.9

184.6

38.9

33.5

20.3

18.3

55.0

57.3

5.1

4.5

Tata Global

Accumulate

133

144

8,394

8,635

9,072

9.8

9.9

6.5

7.6

20.5

17.5

2.0

2.0

6.8

7.4

0.9

0.9

IT

HCL Tech^

Buy

870

1,132

122,277

42,038

47,503

23.2

23.5

55.8

62.9

15.6

13.8

3.6

2.7

23.0

19.8

2.5

2.0

Infosys

Accumulate

1,136

1,306

260,944

60,250

66,999

28.0

28.0

58.3

63.7

19.5

17.8

4.1

3.5

20.9

19.7

3.6

3.1

TCS

Buy

2,497

3,165

492,075

111,274

126,852

28.4

28.7

125.4

143.9

19.9

17.4

7.9

7.3

39.9

42.2

4.0

3.5

Tech Mahindra

Buy

539

646

51,849

25,566

28,890

16.0

17.0

26.3

31.9

20.5

16.9

3.7

3.1

17.9

18.6

1.8

1.5

Wipro

Buy

573

719

141,599

52,414

58,704

23.7

23.8

38.4

42.3

14.9

13.6

2.9

2.6

19.5

18.0

2.3

1.9

Media

D B Corp

Accumulate

325

356

5,961

2,241

2,495

27.8

27.9

21.8

25.6

14.9

12.7

3.9

3.4

26.7

28.5

2.6

2.3

HT Media

Neutral

83

-

1,933

2,495

2,603

11.2

11.2

7.3

8.6

11.4

9.7

0.9

0.8

7.4

8.1

0.3

0.3

Stock Watch

November 02, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Media

Jagran Prakashan

Buy

140

164

4,569

2,170

2,355

27.0

27.6

12.8

10.3

10.9

13.6

3.0

2.9

21.8

19.4

1.9

1.6

Sun TV Network

Neutral

396

-

15,594

2,779

3,196

70.2

70.5

22.8

27.3

17.4

14.5

4.3

3.9

26.7

28.3

5.4

4.6

Hindustan Media

Neutral

270

-

1,985

920

1,031

20.0

20.0

19.2

20.9

14.1

13.0

2.3

2.0

16.4

15.3

1.7

1.5

Ventures

Metals & Mining

Coal India

Buy

320

400

202,060

77,508

85,330

21.4

23.7

24.8

27.6

12.9

11.6

5.0

4.7

38.6

41.6

1.9

1.7

Hind. Zinc

Accumulate

157

175

66,316

14,641

14,026

50.4

50.4

17.7

16.0

8.9

9.8

1.4

1.2

16.2

13.2

2.1

2.0

Hindalco

Neutral

84

-

17,356

104,356

111,186

8.7

9.5

6.7

11.1

12.5

7.6

0.5

0.4

3.5

5.9

0.7

0.6

JSW Steel

Neutral

912

-

22,038

42,308

45,147

16.4

20.7

(10.3)

49.5

18.4

1.0

1.0

(1.0)

5.6

1.6

1.5

NMDC

Neutral

100

-

39,627

8,237

10,893

46.6

44.5

10.0

11.7

10.1

8.6

1.1

1.0

12.5

13.0

4.6

3.5

SAIL

Neutral

53

-

22,034

45,915

53,954

7.2

10.5

1.5

4.4

35.4

12.2

0.5

0.5

2.3

4.1

1.1

1.0

Vedanta

Neutral

100

-

29,647

71,445

81,910

26.2

26.3

12.9

19.2

7.8

5.2

0.5

0.5

7.2

8.9

0.9

0.7

Tata Steel

Neutral

247

-

23,965

126,760

137,307

8.9

11.3

6.4

23.1

38.8

10.7

0.8

0.8

2.0

7.1

0.8

0.7

Oil & Gas

Cairn India

Neutral

154

-

28,798

11,323

12,490

49.4

51.0

20.7

20.7

7.4

7.4

0.5

0.5

6.4

6.1

1.6

1.0

GAIL

Neutral

309

-

39,158

64,856

70,933

9.1

9.6

24.0

28.9

12.9

10.7

1.1

1.0

8.8

9.6

0.8

0.7

ONGC

Neutral

248

-

212,048

154,564

167,321

36.8

37.4

28.6

32.5

8.7

7.6

1.1

1.0

12.7

13.5

1.6

1.5

Petronet LNG

Accumulate

193

210

14,498

29,691

31,188

5.8

6.2

12.8

13.4

15.1

14.4

2.3

2.0

15.8

14.8

0.6

0.5

Indian Oil Corp

Accumulate

399

455

96,900

359,607

402,760

5.9

6.1

42.5

48.7

9.4

8.2

1.3

1.1

14.1

14.4

0.4

0.3

Reliance Industries

Accumulate

948

1,050

306,954

304,775

344,392

12.6

13.4

91.3

102.6

10.4

9.2

1.2

1.1

11.8

12.0

0.9

0.8

Pharmaceuticals

Alembic Pharma

Neutral

678

-

12,789

2,601

3,115

21.2

20.2

20.8

23.9

32.6

28.4

10.5

7.9

37.2

31.8

4.9

4.1

Aurobindo Pharma

Neutral

835

-

48,755

14,923

17,162

23.0

23.0

38.2

43.6

21.9

19.2

6.7

5.1

36.0

30.2

3.6

3.1

Aventis*

Neutral

4,545

-

10,467

2,082

2,371

17.4

20.8

118.2

151.5

38.5

30.0

5.6

4.5

19.9

25.5

4.7

3.9

Cadila Healthcare

Neutral

416

-

42,629

10,224

11,840

21.0

22.0

14.6

17.6

28.5

23.7

7.8

6.1

30.8

29.0

4.2

3.6

Cipla

Neutral

690

-

55,402

14,359

16,884

21.3

19.7

28.4

30.5

24.3

22.6

4.3

3.7

19.3

17.5

3.8

3.2

Dr Reddy's

Neutral

4,270

-

72,802

18,213

21,214

22.6

22.7

163.0

192.5

26.2

22.2

5.4

4.4

22.5

20.0

4.0

3.3

Dishman Pharma

Neutral

362

-

2,921

1,716

1,888

20.2

20.2

16.3

21.6

22.2

16.8

2.1

1.9

9.7

11.7

1.9

1.6

GSK Pharma*

Neutral

3,295

-

27,908

2,870

3,158

20.0

22.1

59.5

68.3

55.4

48.2

16.3

16.8

28.5

34.3

9.2

8.4

Indoco Remedies

Neutral

326

-

3,000

1,088

1,262

18.2

18.2

13.1

15.5

24.9

21.0

4.9

4.1

21.2

21.1

2.8

2.4

Ipca labs

Buy

782

900

9,864

3,363

3,909

12.9

18.6

13.4

28.0

58.3

27.9

7.6

6.1

7.4

14.0

3.2

2.8

Lupin

Neutral

1,926

-

86,712

14,864

17,244

26.9

26.9

62.1

71.1

31.0

27.1

7.5

6.0

27.4

24.6

5.6

4.7

Sun Pharma

Accumulate

889

950

213,932

28,163

32,610

25.8

30.7

17.4

26.9

51.1

33.1

4.8

4.2

13.0

16.6

7.1

5.9

Stock Watch

November 02, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Power

Tata Power

Neutral

69

-

18,635

35,923

37,402

22.6

22.8

4.1

5.2

17.0

13.4

1.3

1.2

7.5

9.3

1.5

1.4

NTPC

Buy

133

157

109,417

87,064

98,846

23.5

23.5

11.7

13.2

11.3

10.1

1.3

1.2

11.4

12.1

2.3

2.0

Power Grid

Buy

129

170

67,357

20,702

23,361

86.7

86.4

12.1

13.2

10.7

9.8

1.6

1.4

15.6

15.1

8.2

7.6

Telecom

Bharti Airtel

Neutral

349

-

139,409

101,748

109,191

32.1

31.7

12.0

12.5

29.1

27.9

2.0

1.9

6.9

6.7

2.0

1.8

Idea Cellular

Neutral

140

-

50,305

34,282

36,941

32.0

31.5

5.9

6.2

23.7

22.5

2.2

2.0

9.9

9.3

2.0

1.9

zOthers

Abbott India

Neutral

5,570

-

11,835

2,715

3,153

14.5

14.1

134.3

152.2

41.5

36.6

10.4

8.5

27.4

25.6

4.1

3.4

Bajaj Electricals

Buy

246

341

2,481

4,719

5,287

5.2

5.8

8.6

12.7

28.7

19.4

3.3

2.9

11.4

14.8

0.5

0.5

Finolex Cables

Neutral

251

-

3,837

2,728

3,036

10.8

11.0

14.4

16.8

17.4

15.0

2.7

2.3

15.2

15.3

1.2

1.0

Goodyear India*

Buy

560

655

1,291

1,953

1,766

12.4

12.0

67.4

59.6

8.3

9.4

2.1

1.8

27.7

20.2

0.4

0.4

Hitachi

Neutral

1,345

-

3,657

1,779

2,081

7.8

8.8

21.8

33.4

61.7

40.2

10.0

8.1

17.4

22.1

2.1

1.8

Jyothy Laboratories

Neutral

308

-

5,581

1,620

1,847

11.5

11.5

7.3

8.5

42.3

36.4

5.5

5.1

13.3

14.4

3.3

2.8

MRF

Accumulate

39,692

45,575

16,834

20,316

14,488

21.4

21.1

5,488.0

3,798.0

7.2

10.5

2.5

2.0

41.1

21.2

0.8

1.0

Page Industries

Neutral

14,066

-

15,689

1,929

2,450

19.8

20.1

229.9

299.0

61.2

47.1

27.0

18.8

52.1

47.1

8.2

6.4

Relaxo Footwears

Neutral

524

-

6,288

1,767

2,152

12.3

12.5

19.3

25.1

27.2

20.9

6.7

5.1

27.7

27.8

3.6

2.9

Siyaram Silk Mills

Buy

933

1,145

875

1,636

1,815

11.5

11.5

89.9

104.1

10.4

9.0

1.7

1.5

17.9

17.8

0.7

0.6

Styrolution ABS India*

Neutral

790

-

1,390

1,271

1,440

8.6

9.2

32.0

41.1

24.7

19.3

2.5

2.3

10.7

12.4

1.1

0.9

Tree House

Buy

276

347

1,166

259

324

56.8

56.8

17.0

21.7

16.2

12.7

1.6

1.5

10.1

11.5

4.4

3.7

TVS Srichakra

Accumulate

2,902

3,210

2,222

2,127

2,388

15.2

14.9

237.7

267.5

12.2

10.9

5.2

3.7

51.7

39.8

1.1

0.9

HSIL

Accumulate

279

302

2,017

2,182

2,404

16.3

16.5

15.8

18.9

17.7

14.8

1.4

1.3

8.4

9.4

1.3

1.1

Kirloskar Engines India

Neutral

272

-

3,935

2,634

3,252

10.1

12.0

10.9

17.4

25.0

15.6

2.8

2.5

11.4

16.8

1.1

0.9

Ltd

M M Forgings

Buy

531

670

641

541

634

21.7

21.4

47.8

55.9

11.1

9.5

2.2

1.8

21.8

20.9

1.3

1.1

Banco Products (India)

Neutral

130

-

933

1,208

1,353

11.0

12.3

10.8

14.5

12.1

9.0

1.4

1.2

11.9

14.5

0.7

0.6

Competent Automobiles Neutral

146

-

90

1,007

1,114

3.1

3.1

23.7

28.2

6.2

5.2

0.9

0.8

13.9

14.6

0.1

0.1

Nilkamal

Neutral

997

-

1,487

1,948

2,147

10.6

10.3

60.0

67.0

16.6

14.9

2.6

2.2

16.8

16.1

0.8

0.7

Visaka Industries

Buy

132

166

210

1,158

1,272

8.6

9.5

23.7

32.7

5.6

4.0

0.6

0.5

10.1

12.5

0.4

0.3

Transport Corporation of

Neutral

281

-

2,134

2,830

3,350

8.8

9.0

14.4

18.3

19.5

15.3

3.0

2.6

15.4

17.1

0.9

0.8

India

Elecon Engineering

Neutral

77

-

838

1,452

1,596

14.0

14.7

4.4

6.2

17.4

12.4

1.5

1.3

8.6

11.2

0.9

0.7

Surya Roshni

Buy

134

183

585

2,992

3,223

8.3

8.5

14.7

18.3

9.1

7.3

0.9

0.8

9.7

11.0

0.5

0.4

MT Educare

Buy

137

169

546

286

366

18.3

17.7

7.7

9.4

17.8

14.6

3.7

3.3

20.2

21.1

1.8

1.4

Stock Watch

November 02, 2015

Company Name

Reco

CMP

Target Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E

zOthers

Radico Khaitan

Buy

101

119

1,346

1,565

1,687

11.9

12.4

5.4

6.6

18.7

15.4

1.5

1.4

8.0

9.0

1.4

1.3

Garware Wall Ropes

Accumulate

344

390

752

875

983

10.4

10.6

23.1

27.8

14.9

12.4

2.1

1.8

14.1

14.8

0.9

0.7

Wonderla Holidays

Neutral

324

-

1,833

206

308

44.0

43.6

9.0

12.9

36.0

25.1

4.9

4.5

13.7

17.8

8.8

5.9

Linc Pen & Plastics

Accumulate

163

185

240

340

371

8.3

8.9

10.8

13.2

15.1

12.3

2.4

2.1

16.0

17.1

0.7

0.7

The Byke Hospitality

Accumulate

159

181

636

222

287

20.5

20.5

5.6

7.6

28.1

21.0

5.3

4.4

18.9

20.8

2.9

2.2

Source: Company, Angel Research; Note: *December year end; #September year end; &October year end; Price as on October 30, 2015

Market Outlook

November 02, 2015

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitian Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial ownership

of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation / managed or co

-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst has not served as

an officer, director or employee of company covered by Analyst and has not been engaged in market making activity of the company

covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way responsible for any

loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Pvt.

Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any

representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking

Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance,

or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or

in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may have

investment positions in the stocks recommended in this report.