Market Outlook

February 1, 2016

Market Cues

Domestic Indices

Chg (%)

(Pts)

(Close)

Indian markets are expected to open in positive tracking the SGX Nifty.

BSE Sensex

1.6

401

24,871

Traders reacted positively to an unexpected monetary policy move by the Bank of

Nifty

1.9

139

7,564

Japan which led Dow Jones rose 2.5% on Friday. The gains on the day helped the

Mid Cap

2.0

206

10,417

major averages more than offset the steep drop seen on Wednesday. The rally on

Small Cap

1.1

115

10,870

Wall Street was partly in reaction to the Bank of Japan's surprise decision to

Bankex

0.7

123

17,604

introduce negative interest rates. Traders were also digesting the latest U.S.

economic news which included a Commerce Department report showing a

slowdown in GDP growth in the December quarter.

Global Indices

Chg (%)

(Pts)

(Close)

Dow Jones

2.5

397

16,466

The European markets ended in positive territory with the markets followed their

Asian peers higher after the Bank of Japan's negative interest rate move. Crude oil

Nasdaq

2.4

107

4,614

prices also continued their recent recovery Friday, rising back to around $34 a

FTSE

2.6

152

6,084

barrel.

Nikkei

2.8

477

17,518

Indian shares joined the global rally on Friday as oil extended overnight gains.

Hang Seng

2.5

487

19,683

Chinese shares steadied and investors reacted to the the Bank of Japan's negative

Shanghai Com

3.1

82

2,738

interest rate move. Yes Bank soared 10.9% after reporting a better-than-expected

25% increase in Q3 profit. Vedanta climbed 6.7% despite reporting a 99% fall in

Advances / Declines

BSE

NSE

quarterly profit. Maruti Suzuki India ended flat and ICICI Bank dropped 1.2% after

posting disappointing results for the December quarter.

Advances

1,558

1,021

Declines

1,047

541

News & Result Analysis

Unchanged

191

64

Result Review: Yes Bank, Blue Star, Larsen & Toubro, United Phosphorus,

Banco Products, Elecon Engineering, Relaxo Footwear, Indoco Remedies

Volumes (` Cr)

Result Preview: Tech Mahindra

Detailed analysis on Pg2

BSE

2,697

NSE

20,637

Investor’s Ready Reckoner

Key Domestic & Global Indicators

Net Inflows (` Cr)

Net

Mtd

Ytd

Stock Watch: Latest investment recommendations on 150+ stocks

FII

(761)

(8,251)

(7,584)

Refer P8 onwards

MFs

810

2,764

72,180

Top Picks

CMP

Target

Upside

Company

Sector

Rating

Top Gainers

Price (`)

Chg (%)

(`)

(`)

(%)

Amara Raja Batteries Auto & Auto Ancillary

Buy

837

1,040

24.2

Srtransfin

842

11.9

HCL Tech

IT

Buy

866

1,038

19.9

Yesbank

747

10.9

HDFC Bank

Financials

Buy

1,049

1,262

20.3

Suzlon

20

7.7

LIC Housing Finance Financials

Buy

476

592

24.3

Titan

364

7.3

Navkar Corporation Others

Buy

200

265

32.7

Suntv

379

7.0

More Top Picks on Pg7

Key Upcoming Events

Top Losers

Price (`)

Chg (%)

Previous

Consensus

Date

Region

Event Description

Justdial

609

(15.2)

Reading

Expectations

Syndibank

68

(3.8)

Feb 01

UK

PMI Manufacturing

51.90

51.60

Feb 02

India

RBI Repo Rate (%)

6.75

6.75

Jetairways

603

(3.8)

Feb 05

US

Change in Nonfarm payrolls (thousands)

292

190

Unitdspr

2,488

(3.6)

Feb 04

UK

BOE Announces rates

0.50

0.50

Bankbaroda

126

(3.3)

6.(

As on January 29, 2015

Market Outlook

February 1, 2016

Result Review

Yes Bank (CMP: `747/ TP: `767/ Upside: 2.7%)

Yes Bank reported a healthy performance during the quarter with PAT growth of

25.1% yoy to `675.7cr, above our expectations. NII for the bank grew at healthy

pace of 27.3% yoy, on account of strong growth in advances and Retail & CASA

deposits. Reported NIM inched up to 3.4% as compared to 3.3% in 2QFY16.

CASA Ratio improved to 26.6% from 22.6% a year ago on the back of savings

deposits robust growth of 64.1% y-o-y. Advances jumped 26.7% yoy to `84,396cr

which is a healthy number given the sluggish credit growth in the economy. Non

Interest Income continued to deliver healthy growth at 39.0% yoy while operating

expenses grew by 29.2% yoy led by growth in staff as well as other operating

expenses. On the asset quality front, Gross NPA and Net NPA ratios marginally

inched up to 0.66% and 0.22% respectively in 3QFY2016 as compared to 0.61%

and 0.20% in 2QFY2016 which remains comfortable. The bank indicated that

there has neither been any sale to ARC during the previous four quarters nor the

bank has refinanced any loan through 5-25 route.

The bank’s asset quality performance has held up well so far. Going forward, we

have factored higher provisions and slippages given the bank’s corporate

exposure to metals and EPC. Even after factoring the higher provisions and

slippages, we expect Yes Bank to deliver a CAGR of 20.5% in earnings for

FY2015-17E. Currently the stock trades at 1.9x FY2017E ABV. We recommend

NEUTRAL rating on the stock.

Y/E

Op. Inc NIM

PAT

EPS

ABV ROA ROE

P/E

P/ABV

Mar

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

7,190

3.2

2,433

58.2

326.1

1.6

19.2

12.8

2.3

FY2017E

9,011

3.3

2,910

69.7

383.7

1.6

19.6

10.7

1.9

Blue Star Ltd (CMP: `362/ TP: `439 / Upside: 21.5%)

Blue Star reported 3QFY2016 numbers that were broadly in line with our

estimates. The standalone top-line for the quarter reported an impressive 15.1%

yoy increase to `686cr. This is above our estimate of `641cr. Both Electro

Mechanical Projects and Packaged Air-conditioning Systems (EMPPAC) business

and Cooling Products business reported healthy growth of 21.5% yoy and 21.0%

yoy to `439cr and `238cr, respectively. The PEIS business top-line came in at `9cr

against `38cr in 3QFY2015. However yoy comparison for PEIS business is not

reasonable as the segment has been transferred to Blue Star’s subsidiary, BSEEL.

On operating front, the EBITDA margin expanded by 259bp yoy to 4.1% which is

in-line with our estimate of 4.0%. The raw material cost as a percentage of sales

increased by 175bp yoy to 68.9% but this was made up by 94bp yoy and 341bp

yoy decline in Employee and Other expenses to 9.7% and 17.4%, respectively. The

EBIT margins for EMPPAC, Cooling Products and PEIS were 5.8%, 7.1% and 18.7%

respectively. There was an exceptional loss of `2cr during the quarter due to bonus

expenses for earlier years pursuant to retrospective amendment in the statute.

Adjusting for exceptional item, the net profit came in at `7cr which is marginally

below our estimate of `8cr.

Market Outlook

February 1, 2016

We remain positive on the stock as its RAC business continues to outperform the

market by 10% points and continues to gain market share. Also, the performance

of the EMPPAC business is showing gradual improvement which should also aid

growth. We maintain our Buy rating on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

3,548

6.3

123

13.7

26.1

26.4

6.6

16.0

1.0

FY2017E

3,977

6.9

164

17.2

25.4

21.1

4.3

12.5

0.9

FY2018E

4,375

7.1

182

19.1

21.1

18.9

3.7

10.7

0.8

Larsen & Toubro (CMP: `1,102/ TP: ` Under Review )

Larsen & Toubro (L&T; standalone entity) reported bad set of numbers for

3QFY2016, both at the top-line and the bottom-line level. The company reported

YoY top-line de-growth at 1.5% YoY to `14,774cr (vs. our expectation of 6% YoY

growth). Revenue de-growth on YoY basis is owing to lower revenue booking

across Infrastructure and Metallurgical & Material Handling segments. The

disappointment continued further towards the EBITDA level; the company reported

a 368bp YoY decline in EBITDA margin to 6.8%. Revenue de-growth and 38.0%

YoY increase in sales, admin and other expenses, led to EBITDA margin

compression. During the quarter, L&T reported gain from stake sale in subsidiary

and associate company to the tune of `92cr. Adjusting for the same, Adj. PAT of

the company were at `791cr. Adj. PAT was also impacted due to muted other

income, which declined 0.8% YoY to `617cr.

For 3QFY2016 L&T reported consol, order inflows of `38,500cr. L&T in order to

attain its revised flattish Order inflow guidance for FY2016 needs to report ~

`61,900cr in 4QFY2016. This translates to asking rate of 30% order inflows

growth in 4QFY2016, which in our view is very challenging.

Even though there have been delays on the awarding front, we believe in the

Indian Infra growth story. Given the company’s market positioning, we expect L&T

to be well positioned and to gain from an expected gradual recovery in the capex

cycle, given its exposure to a range of sectors, and better cash flow generating

potential vis-a-vis its peers. We maintain our positive view on L&T; and maintain

our BUY rating on the stock.

United Phosphorus (CMP: `411/ TP: `510/ Upside: 24.1%)

United Phosphorus, posted sales of `3050cr, a yoy growth of 1.3% in 3QFY2016.

The sales were impacted as all the key markets during the quarter were under

pressure, while USA and Latin America, posted a 12% and 14% yoy growth in

3QFY2016. Other key markets like India, Europe and ROW posted a dip of 17%,

9% and 8% respectively. Overall, the growth was driven by price and volume

growth of 3% and 11% respectively, the exchange which was the main culprit was

dipped by 13%.

India (`498cr) posted a 17% dip on back of serious drought conditions affecting

agrochemical usage both in Kharif & Rabi crops. Europe ( `300cr) posted a 9%

dip due to devaluation of Euro which impacted growth in `terms. European

Market Outlook

February 1, 2016

markets likely to be reported flat to de-growth in Europe. Latin America (`1,279cr),

posted a yoy 14% growth on back of high demand of fungicide.

On operating front, the OPM’s came in at 19.0% V/s 17.9% in 3QFY2015, in spite

of the lower sales, as the GPM improved from 54.2% V/s 48.8% in 3QFY2015 on

back of healthy volume growth and price rise. This aided the Adj. net profit to

come in at `306cr V/s `264cr, a 15.8% yoy growth. We maintain our buy with a

price target of `510.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

13,698

17.6

1,376

32.1

21.4

13.6

2.7

10.3

1.8

FY2017E

15,752

17.6

1,651

38.5

21.3

11.3

2.2

8.6

1.5

Banco Products (CMP: `128/ TP: -/ Upside: -)

For 3QFY2016, Banco has posted numbers that are in-line with our estimates. The

Consolidated top-line has grown by 8.4% yoy to `264cr, against our expectation

of `270 cr. The operating performance has improved mainly due to 168bp yoy

decline in employee cost to 14.4% of sales. The EBITDA grew by 25.1% yoy to

`27cr (in-line with our estimate of `28cr) and EBITDA margin expanded by

137bp yoy to 10.3% which is also in-line with our estimate of 10.5%. Aided by

better operating performance, the consolidated net profit grew by 32.2% yoy to

`15cr.

The improvement company’s performance on the consolidated level is mainly on

the back of its strong performance by the standalone business where it posted a

top-line growth of 16.3% yoy to `112cr, EBITDA almost doubled to `20cr, and net

profit grew by 51.5% yoy to `14cr. This indicates that the Netherland subsidiary is

proving to be a drag on the overall performance while the standalone business

maintains its performance. Additionally, the company had recently filed an

application with the Directorate General of Anti-Dumping and Allied

Duties alleging that there are cheaper imports of Aluminium Radiators, Sub-

Assemblies and Aluminium Radiator Core coming in from China. Since the

company is a major player, levying of anti dumping duty on radiators from China

will definitely be crucial from company’s standpoint.

At the current market price, the stock is trading at PE of 8.2x its FY2017E earnings.

We maintain our Neutral view on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,191

11.9

85

11.9

13.1

10.7

1.3

6.0

0.7

FY2017E

1,334

13.3

111

15.5

15.3

8.2

1.2

4.6

0.6

Elecon Engineering (CMP: `65/ TP: -/ Upside: -)

For 3QFY2016, Elecon Engineering reported a disappointing set of numbers. The

consolidated top-line grew by 10.6% on yoy basis to `330cr mainly led by the

overseas business and MHE business. The standalone top-line grew by 6.0% yoy to

`120cr. On operating front, the consolidated EBITDA margins deteriorated sharply

by 872bp yoy to 2.8% mainly on the back of spike in raw material cost and other

expenses. Raw material cost and other expenses increased by 717bp yoy and

Market Outlook

February 1, 2016

189bp yoy to 69.0% and 16.6% of sales respectively. The standalone EBITDA

margins declined by 891bp yoy mainly on account of unfavorable revenue mix

involving bulk of the shipments of low margins. The other income was higher at

`30cr on account of profit from the sale of surplus land amounting to `21.6cr.

Adjusting for profit from sale of land and accounting for minority interest and

share of profits from associates, the company reported a consolidated loss of

`10cr.

The standalone (gear) business reported a 56.4% yoy decline in net profit to `3cr

while the MHE business reported a total loss of ~`19.5cr (as per our estimates).

Although the long term prospect of the company remains intact, we acknowledge

the cautious commentary provided by the management in the result update. Hence

we currently have a Neutral view on the stock and will update our rating and

numbers post management discussion.

Relaxo Footwears (CMP: `467/ TP: -/ Upside: -)

For 3QFY2016, Relaxo reported numbers that were in-line with our estimates. The

top-line grew by 16.9% yoy to `386cr, which is in line with our estimate of `387cr.

The gross margin expanded by 72bp yoy to 58.3% and net raw material cost as a

percentage sales came in at 41.7%. On the back of lower raw material cost, the

EBITDA margin expanded by 119bp yoy to 13.5% vis-à-vis our estimate of 13.4%.

The interest expense has increased by 44.6% yoy to `6cr while depreciation cost

increased by 24.1% yoy to `12cr. As a result, the net profit grew by 22.6% yoy to

`24cr, which slightly below our estimate of `26xr. At current market price, the

stock trades at 32.3x its FY2017E earnings. We have a Neutral view on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,741

13.8

129

10.7

30.0

43.6

11.5

23.9

3.3

FY2017E

2,097

14.9

174

14.5

30.6

32.3

8.7

18.2

2.7

Indoco Remedies (CMP: `323/ TP: / Upside: )

Indoco Remedies results were in line with expectations, on sales front, while net

profit was lower on back of the lower than expected OPM’s. On sales the company

posted sales of `255cr ( V/s 257cr estimated) , a yoy growth of 19.6%. The growth

during the quarter came in through exports (`112.1cr) a yoy growth of 34.6%,

while domestic markets posted sales of `141.9cr, a yoy growth of 9.8%. Exports

growth during the period was aided by the regulated markets (`90.4cr) a yoy

growth of 36.3% and emerging markets (`139.0cr) a yoy growth of 32.6%. The

domestic formulation (`135.7cr) posted a yoy growth of 10.5%.

On the operating front, the OPM’s have come in at 15.4% (V/s 16.5% expected)

and 18.3% in 3QFY2015. The margins have declined on back of 30.7% and

76.3% rise in employee expenditure and R&D expenditure respectively. Thus the,

net profit came in at `20.4cr V/s `21.6cr in 3QFY2015, a yoy dip of 5.6%. This is

against expectations of `25.4cr.

Also, during the quarter, USFDA audited Company’s finished dosage (Plant I) at

Goa. Establishment Inspection Reports (EIRs) for the Finished Dosage Plant I,

Sterile Plant II and Finished Dosage Plant III at Goa are awaited. Overall, we are

neutral on the stock.

Market Outlook

February 1, 2016

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,033

15.9

87

9.4

15.7

34.3

5.1

19.0

3.0

FY2017E

1,199

18.2

125

13.6

19.7

23.7

4.3

14.2

2.6

Result Preview

Tech Mahindra (CMP: `502/ TP: `646 / Upside: 28.7% )

Tech Mahindra for 3QFY2016 is expected to post a 1.0% QoQ growth in the sales

front to end the period at US$1,021mn V/s US$1,011mn in 2QFY2016. In rupee

terms, the company is expected to post sales of `6,729cr V/s `6,616cr, a QoQ

growth of 1.7%. On the operating front, the EBDITA is expected to come in at

17.2% V/s 16.6% in 2QFY2016, an QoQ expansion of 53bps, while the EBIT

would come in at 14.2% V/s 13.7% in 2QFY2016. On net profit, the company is

expected to post a net profit of `809cr V/s `786cr in 2QFY2016, a QoQ growth

of 3.0%. We remain positive on the stock with a price target of `646.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

Mar

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

25,566

16.0

2,528

26.3 17.9 19.1

3.4

10.9

1.7

FY2017E

28,890

17.0

3,066

31.9 18.6 15.7

2.9

8.7

1.5

Quarterly Bloomberg Brokers Consensus Estimate

Tech Mahindra Ltd - February 1, 2016

Particulars (` cr)

3QFY16E

3QFY15

y-o-y (%)

2QFY16

q-o-q (%)

Net sales

6,749

5,752

17.3

6,615

2.0

EBITDA

1,162

1,059

9.7

1,101

5.5

EBITDA margin (%)

17.2

18.4

16.6

Net profit

771

805

(4.2)

785

(1.8)

Economic and Political News

Coal Secretary appreciates MCL, eyes 250 mn ton output by 2020

Excise duty raised on petrol by `1/litre, on diesel by `1.5

Jaitley vows more reforms, eyes 8-9% growth

Corporate News

Grasim to spend over `4,000 crore on capex in FY17

Blue Star enters air cooler segment, eyes `150 cr sales

NBCC aims for `1 lakh crore order book by 2020-end

Market Outlook

February 1, 2016

Top Picks ★★★★★

Large Cap

Market Cap

CMP

Target

Upside

Company

Rationale

(` Cr)

(`)

(`)

(%)

To outpace battery industry growth due to better technological

Amara Raja Batteries

14,298

837

1,040

24.2

products leading to market share gains in both the automotive

OEM and replacement segments.

Earnings to grow strongly given the MHCV cyclical upturn.

Ashok Leyland

25,428

89

111

24.2

Focus on exports and LCV's provides additional growth

avenue.

The stock is trading at attractive valuations and is factoring all

HCL Tech

1,22,047

866

1,038

19.9

the bad news.

Strong visibility for a robust 20% earnings trajectory, coupled

HDFC Bank

2,64,869

1,049

1,262

20.3

with high quality of earnings on account of high quality retail

business and strategic focus on highly rated corporates.

Back on the growth trend, expect a long term growth of 14%

Infosys

2,67,560

1,165

1,347

15.6

to be a US$20bn in FY2020.

Well positioned to benefit from such expected gradual

recovery in the overall domestic capex cycle, given its presence

Larsen & Toubro

1,02,638

1,102

1,646

49.3

across various infrastructure segments, its execution

capabilities, and its strong balance sheet.

LICHF continues to grow its retail loan book at a healthy pace

with improvement in asset quality. We expect the company to

LIC Housing Finance

24,017

476

592

24.3

post a healthy loan book which is likely to reflect in a strong

earnings growth.

Source: Company, Angel Research

Mid Cap

Market Cap

CMP

Target

Upside

Company

Rationale

(` Cr)

(`)

(`)

(%)

Favourable outlook for the AC industry to augur well for

Cooling products business which is out pacing the market

Blue Star

3,253

362

439

21.4

growth. EMPPAC division's profitability to improve once

operating environment turns around.

Change in business focus towards high-margin chronic &

Garware Wall Ropes

778

355

473

33.1

lifestyle segments and increasing penetration in Europe and

US

Economic recovery to have favourable impact on advertising &

circulation revenue growth. Further, the acquisition of a radio

Jagran Prakashan

5,299

162

189

16.6

business (Radio City) would also boost the company's revenue

growth.

Massive capacity expansion along with rail advantage at ICD

Navkar Corporation

2,849

200

265

32.7

as well CFS augurs well for the company

Earnings boost on back of stable material prices and

Radico Khaitan

1,517

114

156

36.8

favourable pricing environment. Valuation discount to peers

provides additional comfort

Strong brands and distribution network would boost growth

Siyaram Silk Mills

1,018

1,086

1,354

24.7

going ahead. Stock currently trades at an inexpensive

valuation.

Structural shift in the Lighting industry towards LED lighting will

Surya Roshni

661

151

201

33.3

drive growth.

Source: Company, Angel Research

Market Outlook

February 01, 2016

Key Upcoming Events

Result Calendar

Date

Company

Feb 1, 2016

Tech Mahindra, Abbott India, Transport Corporation of India

Feb 2, 2016

Amara Raja Batteries, Cummins India, Crompton Greaves, HSIL, DLF

Feb 3, 2016

Mangalam Cement, Hexaware, IOC, The Byke Hospitality

Feb 4, 2016

Bajaj Auto, ABB, J K Lakshmi Cements, Mphasis, Tata Steel, GSPL, Styrolution, Visaka Industries, Aventis, MT Educare

Feb 5, 2016

Bosch India, Vijaya Bank, Goodyear, Lupin, Cadila Healthcare, Divi's Lab., Tata Power Co., PTC India, Radico Khaitan

Feb 6, 2016

Prakash Industries, TVS Srichakra

Feb 8, 2016

JK Tyre, GlaxoSmith Con, Hitachi, Sterling Tools, Ipca labs

Motherson Sumi, Apollo Tyres, Ramco Cements, Allahabad Bank, Britannia, SAIL, Hindalco, MOIL, GAIL, Petronet

Feb 9, 2016

LNG, Dr Reddy's, Aurobindo Pharma, CESC

Tata Chemicals, Tata Global, Automotive Axle, Ambuja Cements, ACC, India Cements, Rural Elec.Corp., Bank of

Feb 10, 2016

Maharashtra, Bajaj Electrical, Finolex Cables, GSK Pharma, NHPC

Tata Motors, Ashok Leyland, BHEL, BGR Energy , Indian Bank, ONGC, Indraprasth Gas, Page Industries, GIPCL,

Feb 11, 2016

Coffee Day Enterprises Ltd

Feb 12, 2016

M&M, FAG Bearings, Nestle, BPCL, HPCL, Sun Pharma

Source: Bloomberg, Angel Research

Global economic events release calendar

Date

Time

Country

Event Description

Unit

Period

Bloomberg Data

Last Reported Estimated

Feb 1, 2016

2:25PM

Germany

PMI Manufacturing

Value

Jan F

52.10

52.10

3:00PM

UK

PMI Manufacturing

Value

Jan

51.90

51.60

6:30AM

China

PMI Manufacturing

Value

Jan

49.70

49.60

Feb 2, 2016

2:25PM

Germany

Unemployment change (000's)

Thousands

Jan

(14.00)

(8.00)

11:00AM

India

RBI Reverse Repo rate

%

Feb 2

5.75

5.75

11:00AM

India

RBI Repo rate

%

Feb 2

6.75

6.75

11:00AM

India

RBI Cash Reserve ratio

%

Feb 2

4.00

4.00

Feb 3, 2016

2:25PM

Germany

PMI Services

Value

Jan F

55.40

55.40

Feb 4, 2016

7:00PM

US

Initial Jobless claims

Thousands

Jan 30

278.00

280.00

5:30PM

UK

BOE Announces rates

% Ratio

Feb 4

0.50

0.50

Feb 5, 2016

7:00PM

US

Change in Nonfarm payrolls

Thousands

Jan

292.00

190.00

7:00PM

US

Unnemployment rate

%

Jan

5.00

5.00

Feb 10, 2016

India

Imports YoY%

% Change

Jan

(3.90)

--

India

Exports YoY%

% Change

Jan

(14.70)

--

3:00PM

UK

Industrial Production (YoY)

% Change

Dec

0.90

--

Feb 12, 2016

7:30AM

India

Industrial Production YoY

% Change

Dec

(3.20)

--

3:30PM

Euro Zone

Euro-Zone GDP s.a. (QoQ)

% Change

4Q A

0.30

--

12:30PM

Germany

GDP nsa (YoY)

% Change

4Q P

1.80

--

Feb 15, 2016

12:00PM

India

Monthly Wholesale Prices YoY%

% Change

Jan

(0.73)

--

China

Exports YoY%

% Change

Jan

(1.40)

--

Feb 16, 2016

3:00PM

UK

CPI (YoY)

% Change

Jan

0.20

--

Feb 17, 2016

7:00PM

US

Housing Starts

Thousands

Jan

1,149.00

--

7:00PM

US

Building permits

Thousands

Jan

1,204.00

--

3:00PM

UK

Jobless claims change

% Change

Jan

(4.30)

--

7:45PM

US

Industrial Production

%

Jan

(0.36)

--

US

Producer Price Index (mom)

% Change

Jan

(0.70)

--

Feb 18, 2016

7:00AM

China

Consumer Price Index (YoY)

% Change

Jan

1.60

--

Feb 19, 2016

7:00PM

US

Consumer price index (mom)

% Change

Jan

(0.10)

--

8:30PM

Euro Zone

Euro-Zone Consumer Confidence

Value

Feb A

(6.30)

--

Feb 23, 2016

8:30PM

US

Existing home sales

Million

Jan

5.46

--

8:30PM

US

Consumer Confidence

S.A./ 1985=100

Feb

98.10

--

Market Outlook

February 01, 2016

Key Upcoming Events

Feb 24, 2016 8:30PM US

New home sales

Thousands

Jan

544.00

--

Feb 25, 2016 3:00PM UK

GDP (YoY)

% Change

4Q P

1.90

--

3:30PM Euro Zone

Euro-Zone CPI (YoY)

%

Jan F

0.40

--

Feb 26, 2016 7:00PM US

GDP Qoq (Annualised)

% Change

4Q S

0.70

--

Source: Bloomberg, Angel Research

Market Outlook

February 1, 2016

Macro watch

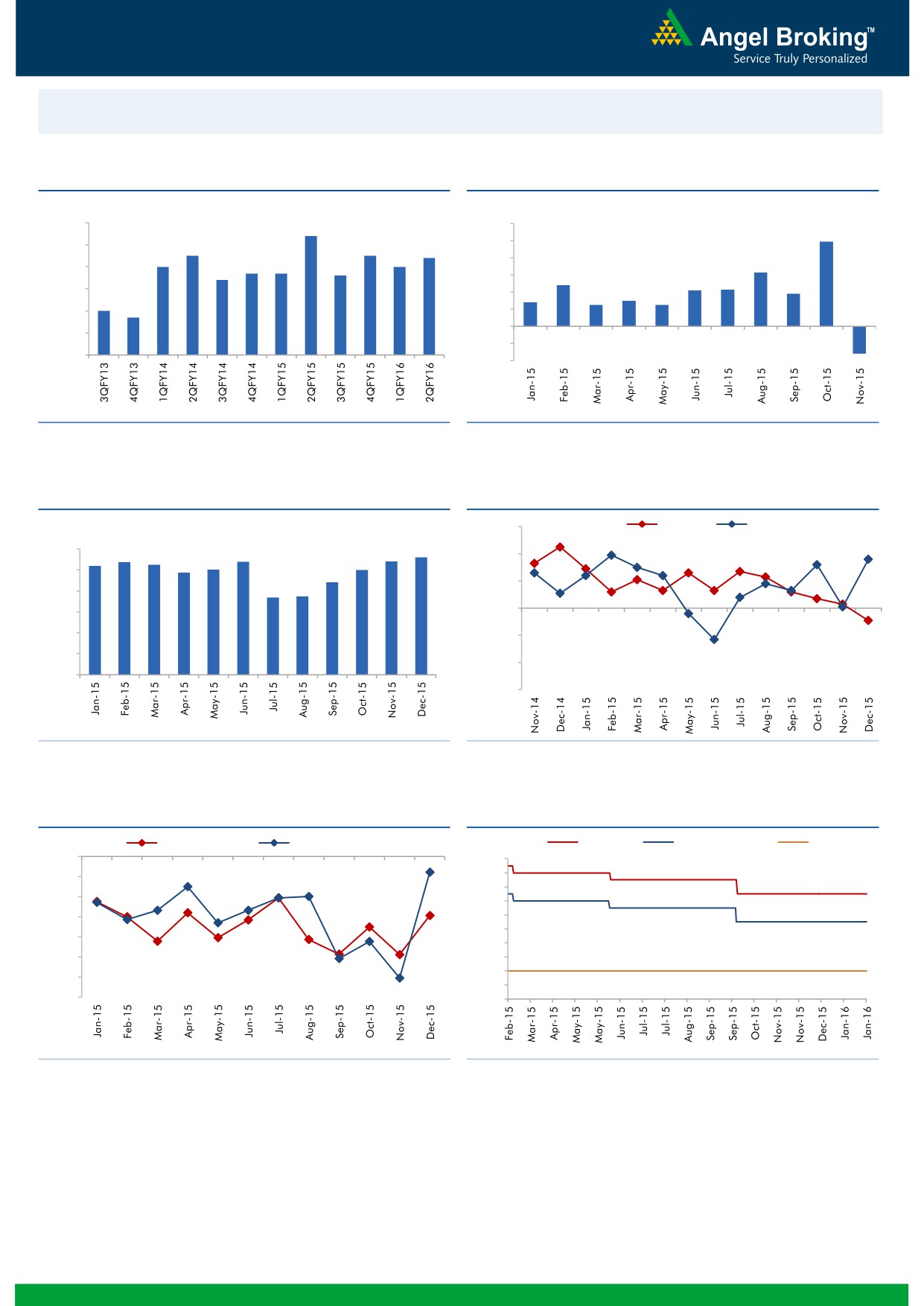

Exhibit 1: Quarterly GDP trends

Exhibit 2: IIP trends

(%)

(%)

9.0

8.4

12.0

9.9

7.5

7.5

10.0

8.0

7.4

7.0

7.0

6.7

6.7

6.6

8.0

6.3

7.0

6.4

6.0

4.8

4.3

4.2

3.8

6.0

2.8

3.0

4.0

2.5

2.5

5.0

4.7

5.0

2.0

(3.2)

-

4.0

(2.0)

3.0

(4.0)

Source: CSO, Angel Research

Source: MOSPI, Angel Research

Exhibit 3: Monthly CPI inflation trends

Exhibit 4: Manufacturing and services PMI

(%)

56.0

Mfg. PMI

Services PMI

5.4

5.4

5.6

6.0

5.2

5.4

5.3

54.0

4.9

5.0

5.0

5.0

4.4

3.7

3.7

52.0

4.0

3.0

50.0

2.0

48.0

1.0

46.0

-

44.0

Source: MOSPI, Angel Research

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Exhibit 5: Exports and imports growth trends

Exhibit 6: Key policy rates

(%)

Exports yoy growth

Imports yoy growth

(%)

Repo rate

Reverse Repo rate

CRR

0.0

8.00

(5.0)

7.50

7.00

(10.0)

6.50

(15.0)

6.00

5.50

(20.0)

5.00

(25.0)

4.50

4.00

(30.0)

3.50

(35.0)

3.00

Source: Bloomberg, Angel Research

Source: RBI, Angel Research

Market Outlook

February 1, 2016

Global watch

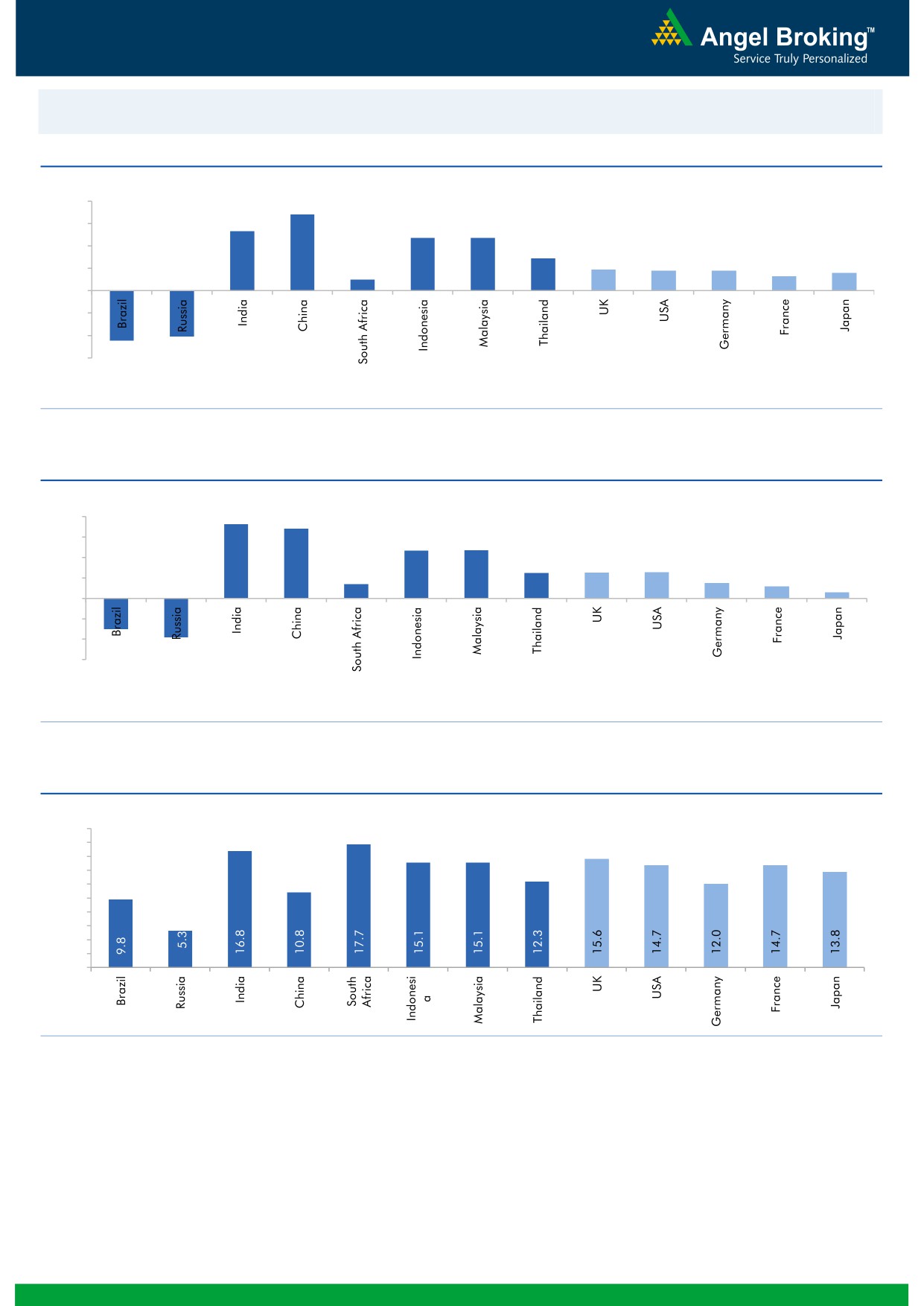

Exhibit 1: Latest quarterly GDP Growth (%, yoy) across select developing and developed countries

(%)

8.0

6.8

5.3

6.0

4.7

4.7

4.0

2.9

1.9

1.8

1.8

1.0

1.3

1.6

2.0

-

(2.0)

(4.0)

(4.1)

(4.5)

(6.0)

Source: Bloomberg, Angel Research

Exhibit 2: 2015 GDP Growth projection by IMF (%, yoy) across select developing and developed countries

(%)

7.3

8.0

6.8

6.0

4.7

4.7

4.0

2.5

2.5

2.6

1.4

1.5

1.2

2.0

(3.0)

0.6

(3.8)

-

(2.0)

(4.0)

(6.0)

Source: IMF, Angel Research

Exhibit 3: One year forward P-E ratio across select developing and developed countries

(x)

20.0

18.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

Source: IMF, Angel Research

Market Outlook

February 1, 2016

Exhibit 4: Relative performance of indices across globe

Returns (%)

Country

Name of index

Closing price

1M

3M

1YR

Brazil

Bovespa

40,406

(16.1)

(19.4)

(21.6)

Russia

Micex

1,785

(6.4)

(5.9)

3.4

India

Nifty

7,564

(5.8)

(11.3)

(13.9)

China

Shanghai Composite

2,738

(19.4)

(12.9)

(9.3)

South Africa

Top 40

44,066

(7.4)

(12.8)

(3.4)

Mexico

Mexbol

43,631

(6.1)

(7.9)

(2.2)

Indonesia

LQ45

800

1.7

(0.1)

(14.4)

Malaysia

KLCI

1,668

(0.2)

(2.3)

(5.8)

Thailand

SET 50

826

(7.3)

(16.0)

(23.8)

USA

Dow Jones

16,466

(11.2)

(8.4)

(10.2)

UK

FTSE

6,084

(3.7)

(5.5)

(10.3)

Japan

Nikkei

17,518

(6.7)

(6.9)

1.4

Germany

DAX

9,798

(10.1)

(7.1)

(10.0)

France

CAC

4,417

(11.8)

(11.7)

(10.8)

Source: Bloomberg, Angel Research

Stock Watch

February 01, 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Agri / Agri Chemical

Rallis

Neutral

165

-

3,212

2,097

2,415

14.4

14.4

9.5

11.0

17.4

15.0

3.5

3.0

21.1

21.3

1.6

1.4

United Phosphorus

Buy

437

510

18,726

13,698

15,752

17.6

17.6

32.1

38.5

13.6

11.4

2.7

2.2

21.4

21.3

1.5

1.2

Auto & Auto Ancillary

Ashok Leyland

Buy

89

111

25,428

17,995

21,544

11.4

11.6

3.4

4.7

26.3

19.0

4.6

4.2

17.7

22.2

1.4

1.1

Bajaj Auto

Buy

2,342

2,728

67,767

23,695

27,298

21.3

20.4

134.6

151.5

17.4

15.5

5.5

4.7

31.8

30.6

2.4

2.1

Bharat Forge

Accumulate

832

943

19,379

7,867

8,881

20.0

20.3

34.4

41.0

24.2

20.3

4.7

3.9

21.1

20.9

2.6

2.2

Eicher Motors

Buy

16,547

19,036

44,931

15,379

16,498

15.6

16.6

473.2

574.8

35.0

28.8

12.9

9.6

36.7

33.2

2.8

2.6

Gabriel India

Buy

87

101

1,251

1,415

1,544

8.7

9.0

4.6

5.4

18.9

16.1

3.4

3.1

18.1

18.9

0.9

0.8

Hero Motocorp

Accumulate

2,563

2,774

51,176

28,561

31,559

14.7

14.7

151.1

163.2

17.0

15.7

6.6

5.6

38.7

35.6

1.6

1.4

Jamna Auto Industries Neutral

146

-

1,164

1,292

1,486

9.3

9.8

6.0

7.5

24.3

19.4

5.0

4.3

20.7

21.8

1.0

0.9

L G Balakrishnan & Bros Neutral

473

-

742

1,254

1,394

11.6

11.8

35.9

41.7

13.2

11.4

1.8

1.6

13.5

13.8

0.7

0.6

Mahindra and Mahindra Buy

1,233

1,449

76,562

39,031

44,440

13.8

13.9

57.9

67.6

21.3

18.2

3.4

3.0

16.1

16.6

1.6

1.4

Maruti

Neutral

4,097

-

123,776

57,865

68,104

16.4

16.7

176.3

225.5

23.2

18.2

4.5

3.8

19.4

21.2

1.9

1.6

Minda Industries

Accumulate

810

867

1,285

2,567

2,965

8.0

8.3

46.1

57.8

17.6

14.0

2.9

2.4

16.7

17.3

0.6

0.5

Motherson Sumi

Buy

265

313

35,065

39,343

45,100

8.8

9.1

10.1

12.5

26.3

21.2

8.3

6.5

35.3

34.4

1.0

0.8

Rane Brake Lining

Buy

398

465

315

454

511

11.5

12.0

25.2

31.0

15.8

12.9

2.4

2.1

14.9

16.6

0.8

0.8

Setco Automotive

Neutral

34

-

452

594

741

12.7

13.7

1.7

3.2

19.9

10.6

2.1

1.8

10.4

16.9

1.2

1.0

Tata Motors

Buy

337

409

97,212

266,022

312,667

12.8

13.1

26.3

38.3

12.8

8.8

1.7

1.4

8.4

12.1

0.5

0.5

TVS Motor

Buy

292

338

13,849

11,569

13,648

7.3

8.7

10.3

16.1

28.3

18.1

7.0

5.5

24.8

30.5

1.2

1.0

Amara Raja Batteries

Buy

837

1,040

14,298

4,892

5,871

17.4

17.6

28.8

37.1

29.1

22.6

6.8

5.4

23.4

24.1

2.9

2.3

Exide Industries

Buy

120

162

10,221

6,950

7,784

14.4

14.8

6.6

7.3

18.2

16.5

2.3

2.1

12.6

12.8

1.2

1.1

Apollo Tyres

Buy

148

171

7,513

12,146

12,689

16.8

16.0

21.2

19.0

7.0

7.8

1.2

1.0

16.5

13.0

0.7

0.7

Ceat

Buy

940

1,119

3,804

6,041

6,597

14.1

13.7

99.5

111.9

9.5

8.4

1.9

1.6

19.6

18.5

0.8

0.7

JK Tyres

Neutral

91

-

2,063

7,446

7,669

15.2

14.0

19.6

18.4

4.6

4.9

1.2

1.0

25.2

19.5

0.7

0.6

Swaraj Engines

Accumulate

850

919

1,056

552

630

14.2

14.7

44.6

54.1

19.1

15.7

4.4

4.0

23.2

25.6

1.8

1.5

Subros

Neutral

93

-

557

1,293

1,527

11.8

11.9

4.2

6.7

22.1

13.9

1.7

1.5

7.7

11.5

0.7

0.6

Indag Rubber

Neutral

180

-

471

283

329

17.0

17.2

13.0

15.4

13.9

11.6

3.0

2.5

21.8

21.6

1.4

1.1

Capital Goods

ACE

Neutral

40

-

393

660

839

4.7

8.2

1.0

3.9

39.8

10.2

1.2

1.1

3.2

11.3

0.7

0.6

BEML

Neutral

1,047

-

4,359

3,277

4,006

6.0

8.9

29.2

64.3

35.8

16.3

2.0

1.8

5.7

11.7

1.4

1.1

Bharat Electronics

Accumulate

1,232

1,414

29,557

7,737

8,634

16.8

17.2

54.0

61.0

22.8

20.2

3.3

2.9

39.3

45.6

2.9

2.5

Stock Watch

February 01, 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Capital Goods

Voltas

Buy

286

353

9,472

5,363

5,963

8.0

9.1

11.0

13.8

26.0

20.7

4.0

3.5

16.2

17.9

1.7

1.5

BGR Energy

Neutral

114

-

824

3,615

3,181

9.5

9.4

16.7

12.4

6.8

9.2

0.6

0.6

10.0

7.0

0.6

0.8

BHEL

Neutral

139

-

33,985

33,722

35,272

10.8

11.7

10.5

14.2

13.2

9.8

1.0

0.9

7.0

9.0

1.1

1.0

Blue Star

Buy

362

439

3,253

3,548

3,977

6.3

6.9

13.7

17.2

26.4

21.1

6.6

4.3

26.1

25.4

1.0

0.9

Crompton Greaves

Buy

171

204

10,724

13,484

14,687

4.9

6.2

4.5

7.1

38.0

24.1

2.7

2.5

7.2

10.8

0.9

0.8

Greaves Cotton

Neutral

129

-

3,150

1,655

1,755

16.6

16.8

7.4

7.8

17.4

16.5

3.5

3.3

21.1

20.6

1.9

1.7

Inox Wind

Buy

317

458

7,033

4,980

5,943

17.0

17.5

26.6

31.6

11.9

10.0

3.6

2.6

35.0

30.0

1.6

1.3

KEC International

Neutral

123

-

3,167

8,791

9,716

6.1

6.8

5.4

8.2

22.8

15.0

2.3

2.1

10.0

14.0

0.6

0.5

Thermax

Neutral

837

-

9,969

6,413

7,525

7.4

8.5

30.5

39.3

27.4

21.3

4.2

3.7

15.0

17.0

1.5

1.3

Cement

ACC

Buy

1,240

1,630

23,288

13,151

14,757

16.4

18.3

63.9

83.4

19.4

14.9

2.5

2.3

13.3

16.1

1.6

1.4

Ambuja Cements

Buy

195

233

30,239

11,564

12,556

19.4

20.7

8.9

10.1

21.9

19.3

2.7

2.6

12.8

13.8

2.3

2.0

HeidelbergCement

Neutral

70

-

1,589

1,772

1,926

13.3

15.4

1.0

3.0

70.1

23.4

1.8

1.6

2.6

7.9

1.5

1.3

India Cements

Buy

94

112

2,883

4,216

4,840

18.0

19.5

4.0

9.9

23.5

9.5

0.9

0.9

4.0

9.5

1.0

0.8

JK Cement

Buy

497

744

3,477

3,661

4,742

10.1

15.8

18.0

61.0

27.6

8.2

2.0

1.8

7.5

22.9

1.4

1.1

J K Lakshmi Cement

Buy

301

430

3,542

2,947

3,616

16.7

19.9

11.5

27.2

26.2

11.1

2.5

2.1

9.8

20.8

1.6

1.3

Mangalam Cements

Neutral

178

-

475

1,053

1,347

10.5

13.3

8.4

26.0

21.2

6.9

0.9

0.8

4.3

12.5

0.8

0.6

Orient Cement

Buy

144

183

2,940

1,854

2,524

21.2

22.2

7.7

11.1

18.6

12.9

2.7

2.3

13.3

15.7

2.3

1.6

Ramco Cements

Neutral

387

-

9,218

4,036

4,545

20.8

21.3

15.1

18.8

25.6

20.6

3.1

2.8

12.9

14.3

2.8

2.4

Shree Cement^

Neutral

10,473

-

36,486

7,150

8,742

26.7

28.6

228.0

345.5

45.9

30.3

6.8

5.7

15.7

20.3

4.9

3.9

UltraTech Cement

Buy

2,826

3,282

77,552

25,021

30,023

19.1

21.6

89.0

132.0

31.8

21.4

3.7

3.2

12.2

15.9

3.2

2.7

Construction

ITNL

Neutral

80

-

2,625

7,360

8,825

34.0

35.9

7.0

9.0

11.4

8.9

0.4

0.4

3.2

3.7

3.7

3.6

KNR Constructions

Buy

494

673

1,388

937

1,470

14.3

14.0

33.5

38.6

14.7

12.8

2.2

1.9

15.4

15.4

1.6

1.0

Larsen & Toubro

Buy

1,102

1,646

102,638

65,065

77,009

11.5

11.7

61.5

65.6

17.9

16.8

1.8

1.7

13.4

14.0

1.8

1.5

Gujarat Pipavav Port

Neutral

162

-

7,824

629

684

51.0

52.2

6.4

5.9

25.3

27.4

3.3

3.1

15.9

12.7

12.1

10.9

MBL Infrastructures

Buy

162

285

672

2,313

2,797

12.2

14.6

19.0

20.0

8.5

8.1

0.9

0.8

11.3

10.6

1.0

0.9

Nagarjuna Const.

Neutral

64

-

3,577

7,892

8,842

8.8

9.1

3.0

5.3

21.5

12.1

1.1

1.0

5.0

8.5

0.7

0.6

PNC Infratech

Accumulate

509

558

2,610

1,873

2,288

13.2

13.5

24.0

32.0

21.2

15.9

2.1

1.8

12.1

12.3

1.5

1.2

Simplex Infra

Neutral

278

-

1,375

5,955

6,829

10.3

10.5

16.0

31.0

17.4

9.0

0.9

0.8

5.3

9.9

0.7

0.6

Power Mech Projects

Neutral

591

-

869

1,539

1,801

12.8

12.7

59.0

72.1

10.0

8.2

1.5

1.3

18.6

16.8

0.6

0.5

Stock Watch

February 01, 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Construction

Sadbhav Engineering

Neutral

309

-

5,300

3,481

4,219

10.7

10.8

8.0

12.0

38.6

25.8

3.6

3.2

10.3

13.5

1.8

1.5

NBCC

Accumulate

963

1,089

11,555

7,382

9,506

7.7

8.6

39.8

54.4

24.2

17.7

5.8

4.6

26.7

29.1

1.3

1.0

MEP Infra

Neutral

43

-

703

1,956

1,876

28.1

30.5

1.3

3.0

33.3

14.4

7.0

4.7

21.2

32.8

1.8

1.8

SIPL

Neutral

88

-

3,084

675

1,042

62.4

64.7

-

-

3.3

3.7

-

-

16.2

11.0

Financials

Allahabad Bank

Neutral

54

-

3,222

8,569

9,392

2.8

2.9

16.3

27.5

3.3

2.0

0.3

0.2

7.6

11.9

-

-

Axis Bank

Buy

408

494

97,134

26,473

31,527

3.5

3.6

35.7

43.5

11.4

9.4

1.9

1.7

17.9

18.9

-

-

Bank of Baroda

Neutral

126

-

28,986

18,485

21,025

1.9

2.0

13.5

21.1

9.4

6.0

0.7

0.7

7.3

10.6

-

-

Bank of India

Neutral

100

-

8,123

15,972

17,271

1.9

2.0

15.3

33.4

6.5

3.0

0.3

0.3

3.6

7.6

-

-

Canara Bank

Neutral

194

-

10,534

15,441

16,945

2.0

2.1

46.6

70.4

4.2

2.8

0.4

0.3

8.0

11.2

-

-

Dena Bank

Neutral

36

-

2,326

3,440

3,840

2.1

2.3

7.3

10.0

5.0

3.6

0.4

0.3

6.1

7.9

-

-

Federal Bank

Neutral

46

-

7,927

3,477

3,999

3.0

3.0

5.0

6.2

9.2

7.4

0.9

0.8

10.6

11.9

-

-

HDFC

Neutral

1,178

-

185,911

10,358

11,852

3.3

3.3

41.1

47.0

28.7

25.0

5.5

5.0

24.7

24.9

-

-

HDFC Bank

Buy

1,049

1,262

264,869

38,309

47,302

4.3

4.3

49.3

61.1

21.3

17.2

3.7

3.2

18.5

19.7

-

-

ICICI Bank

Accumulate

230

254

133,742

34,279

39,262

3.3

3.3

21.0

24.4

11.0

9.4

1.9

1.6

14.4

14.7

-

-

IDBI Bank

Neutral

59

-

11,191

9,625

10,455

1.8

1.8

8.5

14.2

6.9

4.1

0.4

0.4

5.9

9.3

-

-

Indian Bank

Neutral

91

-

4,373

6,160

6,858

2.5

2.5

24.5

29.8

3.7

3.1

0.3

0.3

7.7

8.6

-

-

LIC Housing Finance

Buy

476

592

24,017

3,101

3,745

2.5

2.5

33.0

40.2

14.4

11.9

2.7

2.3

19.7

20.5

-

-

Oriental Bank

Neutral

112

-

3,361

7,643

8,373

2.4

2.4

37.2

45.4

3.0

2.5

0.3

0.2

8.2

9.4

-

-

Punjab Natl.Bank

Neutral

91

-

17,898

23,638

26,557

2.8

2.8

17.9

27.2

5.1

3.4

0.5

0.4

8.5

12.0

-

-

South Ind.Bank

Neutral

19

-

2,498

1,965

2,185

2.5

2.5

2.5

3.3

7.4

5.6

0.7

0.7

9.5

11.7

-

-

St Bk of India

Accumulate

180

202

139,691

82,520

93,299

2.7

2.8

20.0

24.5

9.0

7.4

1.0

0.9

11.5

12.8

-

-

Union Bank

Neutral

130

-

8,968

12,646

14,129

2.3

2.4

31.0

39.1

4.2

3.3

0.5

0.4

9.8

11.4

-

-

Vijaya Bank

Neutral

31

-

2,676

3,536

3,827

1.9

1.9

5.5

6.7

5.6

4.7

0.5

0.4

7.8

8.8

-

-

Yes Bank

Neutral

747

-

31,349

7,190

9,011

3.2

3.3

58.2

69.7

12.8

10.7

2.3

2.0

19.2

19.6

-

-

FMCG

Asian Paints

Neutral

869

-

83,340

16,553

19,160

16.0

16.2

17.7

21.5

49.2

40.4

13.1

11.7

29.4

31.2

4.9

4.2

Britannia

Neutral

2,683

-

32,188

8,065

9,395

9.6

10.2

47.2

65.5

56.8

41.0

18.9

17.9

38.3

41.2

3.8

3.3

Colgate

Neutral

856

-

23,293

4,836

5,490

19.5

19.7

48.5

53.2

17.7

16.1

12.9

11.3

99.8

97.5

4.7

4.1

Dabur India

Accumulate

250

267

43,987

9,370

10,265

17.1

17.2

7.3

8.1

34.1

30.9

10.3

8.4

33.7

30.6

4.6

4.2

GlaxoSmith Con*

Neutral

5,835

-

24,539

4,919

5,742

17.2

17.4

168.3

191.2

34.7

30.5

9.8

8.4

28.8

28.9

4.6

3.9

Stock Watch

February 01, 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FMCG

Godrej Consumer

Neutral

1,224

-

41,690

10,168

12,886

16.1

16.1

32.1

38.4

38.2

31.9

7.8

7.2

19.7

21.0

4.2

3.3

HUL

Neutral

817

-

176,767

34,940

38,957

17.5

17.7

20.8

24.7

39.3

33.1

43.7

34.9

110.5

114.2

4.9

4.3

ITC

Buy

320

382

256,772

41,068

45,068

37.8

37.4

13.9

15.9

23.0

20.1

7.7

6.8

34.1

33.8

5.9

5.3

Marico

Neutral

222

-

28,655

6,551

7,766

15.7

16.0

10.4

12.5

21.4

17.8

6.2

5.2

33.2

32.4

4.3

3.6

Nestle*

Buy

5,491

6,646

52,938

11,291

12,847

22.2

22.3

158.9

184.6

34.6

29.7

18.1

16.2

55.0

57.3

4.5

3.9

Tata Global

Accumulate

127

144

7,984

8,635

9,072

9.8

9.9

6.5

7.6

19.5

16.6

1.9

1.9

6.8

7.4

0.9

0.8

IT

HCL Tech^

Buy

866

1,038

122,047

42,038

47,503

21.2

21.5

51.5

57.7

16.8

15.0

3.6

2.8

21.5

18.8

2.5

2.0

Infosys

Buy

1,165

1,347

267,560

61,850

69,981

27.5

27.5

59.4

65.7

19.6

17.7

4.2

3.6

21.2

20.1

3.6

3.0

TCS

Buy

2,391

2,854

471,169

108,487

122,590

28.3

28.5

122.8

138.4

19.5

17.3

7.4

6.7

38.0

38.9

3.9

3.4

Tech Mahindra

Buy

502

646

48,511

25,566

28,890

16.0

17.0

26.3

31.9

19.1

15.7

3.4

2.9

17.9

18.6

1.7

1.4

Wipro

Buy

561

719

138,644

50,808

58,713

23.7

23.8

37.3

42.3

15.1

13.3

2.9

2.5

19.0

17.9

2.3

1.8

Media

D B Corp

Accumulate

320

356

5,878

2,241

2,495

27.8

27.9

21.8

25.6

14.7

12.5

3.8

3.4

26.7

28.5

2.6

2.3

HT Media

Neutral

78

-

1,805

2,495

2,603

11.2

11.2

7.3

8.6

10.6

9.0

0.8

0.8

7.4

8.1

0.2

0.2

Jagran Prakashan

Buy

162

189

5,299

2,170

2,355

27.2

26.2

8.9

9.9

18.2

16.4

3.8

3.3

20.9

20.5

2.3

2.2

Sun TV Network

Neutral

379

-

14,924

2,779

3,196

70.2

70.5

22.8

27.3

16.6

13.9

4.1

3.7

26.7

28.3

5.1

4.4

Hindustan Media

Neutral

278

-

2,042

920

1,031

20.0

20.0

19.2

20.9

14.5

13.3

2.4

2.0

16.4

15.3

1.8

1.5

Ventures

Metals & Mining

Coal India

Buy

320

380

202,155

76,167

84,130

19.9

22.3

22.4

25.8

14.3

12.4

5.2

5.0

35.5

41.0

2.0

1.8

Hind. Zinc

Accumulate

161

175

67,880

14,641

14,026

50.4

50.4

17.7

16.0

9.1

10.0

1.4

1.3

16.2

13.2

2.3

2.1

Hindalco

Neutral

71

-

14,568

104,356

111,186

8.7

9.5

6.7

11.1

10.5

6.4

0.4

0.4

3.5

5.9

0.7

0.6

JSW Steel

Neutral

1,059

-

25,586

42,308

45,147

16.4

20.7

(10.3)

49.5

21.4

1.2

1.1

(1.0)

5.6

1.7

1.5

NMDC

Neutral

81

-

32,055

8,237

10,893

46.6

44.5

10.0

11.7

8.1

6.9

0.9

0.8

12.5

13.0

3.7

2.8

SAIL

Neutral

43

-

17,677

45,915

53,954

7.2

10.5

1.5

4.4

28.4

9.8

0.4

0.4

2.3

4.1

1.0

0.9

Vedanta

Neutral

72

-

21,272

71,445

81,910

26.2

26.3

12.9

19.2

5.6

3.7

0.4

0.4

7.2

8.9

0.7

0.6

Tata Steel

Neutral

250

-

24,285

126,760

137,307

8.9

11.3

6.4

23.1

39.3

10.8

0.8

0.8

2.0

7.1

0.8

0.7

Oil & Gas

Cairn India

Neutral

122

-

22,901

11,323

12,490

49.4

51.0

20.7

20.7

5.9

5.9

0.4

0.4

6.4

6.1

1.1

0.5

GAIL

Neutral

367

-

46,566

64,856

70,933

9.1

9.6

24.0

28.9

15.3

12.7

1.3

1.2

8.8

9.6

0.9

0.8

ONGC

Neutral

226

-

193,440

154,564

167,321

36.8

37.4

28.6

32.5

7.9

7.0

1.0

0.9

12.7

13.5

1.5

1.4

Petronet LNG

Neutral

245

-

18,401

29,691

31,188

5.8

6.2

12.8

13.4

19.2

18.3

2.9

2.6

15.8

14.8

0.7

0.7

Indian Oil Corp

Accumulate

402

455

97,677

359,607

402,760

5.9

6.1

42.5

48.7

9.5

8.3

1.3

1.1

14.1

14.4

0.4

0.3

Stock Watch

February 01, 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Oil & Gas

Reliance Industries

Accumulate

1,035

1,150

335,294

304,775

344,392

12.6

13.4

91.3

102.6

11.3

10.1

1.3

1.2

11.8

12.0

1.0

0.9

Pharmaceuticals

Alembic Pharma

Neutral

618

-

11,646

2,658

3,112

24.1

20.2

24.6

23.9

25.1

25.9

9.0

6.9

42.5

30.2

4.4

3.7

Aurobindo Pharma

Neutral

833

-

48,730

14,923

17,162

22.0

23.0

35.7

42.8

23.3

19.5

6.9

5.2

34.0

30.2

3.6

3.1

Aventis*

Neutral

4,242

-

9,769

2,082

2,371

17.4

20.8

118.2

151.5

35.9

28.0

5.3

4.2

19.9

25.5

4.4

3.6

Cadila Healthcare

Buy

305

352

31,193

10,224

11,840

21.0

22.0

14.6

17.6

20.9

17.3

5.7

4.5

30.8

29.0

3.1

2.6

Cipla

Accumulate

586

636

47,046

14,211

16,611

20.6

19.0

27.0

28.9

21.7

20.3

3.7

3.2

18.4

16.8

3.3

2.8

Dr Reddy's

Buy

3,104

3,933

52,927

16,838

19,575

25.0

23.1

167.5

178.8

18.5

17.4

3.9

3.3

23.1

20.4

3.1

2.6

Dishman Pharma

Neutral

331

-

2,667

1,733

1,906

21.5

21.5

17.0

19.9

19.4

16.6

2.0

1.8

10.5

11.2

2.1

1.8

GSK Pharma*

Neutral

3,224

-

27,309

2,870

3,158

20.0

22.1

59.5

68.3

54.2

47.2

16.0

16.4

28.5

34.3

9.0

8.2

Indoco Remedies

Neutral

323

-

2,977

1,033

1,199

15.9

18.2

9.4

13.6

34.4

23.8

5.1

4.3

15.7

19.7

3.0

2.6

Ipca labs

Buy

669

900

8,439

3,363

3,909

12.9

18.6

13.4

28.0

49.9

23.9

3.6

3.1

7.4

14.0

2.8

2.4

Lupin

Neutral

1,710

-

77,052

13,092

16,561

25.0

27.0

50.4

68.3

33.9

25.0

7.0

5.5

22.8

24.7

5.6

4.3

Sun Pharma

Accumulate

873

950

210,097

28,163

32,610

25.8

30.7

17.4

26.9

50.2

32.5

4.8

4.1

13.0

16.6

6.9

5.8

Power

Tata Power

Neutral

60

-

16,255

35,923

37,402

22.6

22.8

4.1

5.2

14.8

11.7

1.1

1.1

7.5

9.3

1.4

1.3

NTPC

Accumulate

142

157

117,251

87,064

98,846

23.5

23.5

11.7

13.2

12.2

10.8

1.4

1.3

11.4

12.1

2.4

2.1

Power Grid

Buy

148

170

77,218

20,702

23,361

86.7

86.4

12.1

13.2

12.2

11.2

1.8

1.6

15.6

15.1

8.7

8.0

Telecom

Bharti Airtel

Neutral

290

-

115,805

101,748

109,191

32.1

31.7

12.0

12.5

24.1

23.2

1.7

1.6

6.9

6.7

1.8

1.6

Idea Cellular

Neutral

103

-

37,120

34,282

36,941

32.0

31.5

5.9

6.2

17.5

16.6

1.6

1.5

9.9

9.3

1.7

1.6

zOthers

Abbott India

Neutral

5,048

-

10,727

2,715

3,153

14.5

14.1

134.3

152.2

37.6

33.2

9.4

7.7

27.4

25.6

3.7

3.1

Bajaj Electricals

Buy

183

290

1,845

4,719

5,287

5.2

5.8

8.6

12.7

21.4

14.4

2.4

2.1

11.4

14.8

0.4

0.4

Finolex Cables

Neutral

232

-

3,546

2,520

2,883

12.2

12.0

12.7

14.2

18.3

16.3

2.5

2.2

13.6

13.5

1.2

1.0

Goodyear India*

Buy

495

622

1,142

1,888

1,680

12.1

11.9

62.2

56.6

8.0

8.8

1.9

1.6

25.9

19.7

0.4

0.4

Hitachi

Neutral

1,191

-

3,240

1,779

2,081

7.8

8.8

21.8

33.4

54.7

35.6

8.8

7.1

17.4

22.1

1.9

1.6

Jyothy Laboratories

Neutral

285

-

5,167

1,620

1,847

11.5

11.5

7.3

8.5

39.1

33.7

5.1

4.7

13.3

14.4

3.1

2.6

MRF

Buy

35,607

45,575

15,101

20,316

14,488

21.4

21.1

5,488.0

3,798.0

6.5

9.4

2.2

1.8

41.1

21.2

0.7

0.9

Page Industries

Neutral

12,086

-

13,480

1,929

2,450

19.8

20.1

229.9

299.0

52.6

40.4

23.2

16.1

52.1

47.1

7.0

5.5

Relaxo Footwears

Neutral

467

-

5,609

1,767

2,152

12.3

12.5

19.3

25.1

24.3

18.6

6.0

4.6

27.7

27.8

3.2

2.6

Siyaram Silk Mills

Buy

1,086

1,354

1,018

1,636

1,815

11.5

11.5

89.9

104.1

12.1

10.4

2.0

1.7

17.9

17.8

0.8

0.7

Styrolution ABS India*

Neutral

697

-

1,225

1,271

1,440

8.6

9.2

32.0

41.1

21.8

17.0

2.2

2.0

10.7

12.4

0.9

0.8

Stock Watch

February 01, 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

zOthers

TVS Srichakra

Buy

2,557

3,240

1,958

2,101

2,338

15.7

15.0

248.6

270.0

10.3

9.5

4.5

3.2

43.6

34.0

1.0

0.8

HSIL

Accumulate

273

302

1,977

2,123

2,384

16.1

16.5

15.0

18.9

18.2

14.5

1.4

1.3

8.0

9.4

1.3

1.1

Kirloskar Engines India

Neutral

241

-

3,481

2,471

2,826

8.8

10.4

9.1

13.3

26.4

18.1

2.5

2.3

9.7

13.4

1.1

0.9

Ltd

M M Forgings

Buy

470

614

567

511

615

21.7

21.6

43.1

55.8

10.9

8.4

2.0

1.6

19.9

21.2

1.3

1.0

Banco Products (India) Neutral

128

-

915

1,208

1,353

11.0

12.3

10.8

14.5

11.9

8.8

1.4

1.2

11.9

14.5

0.7

0.6

Competent Automobiles Neutral

142

-

87

1,040

1,137

3.2

3.1

25.7

28.0

5.5

5.1

0.8

0.7

15.0

14.3

0.1

0.1

Nilkamal

Neutral

1,346

-

2,009

1,910

2,083

10.5

10.3

63.3

69.2

21.3

19.5

3.5

3.0

17.6

16.5

1.1

1.0

Visaka Industries

Buy

109

144

174

1,086

1,197

9.9

10.3

21.5

28.8

5.1

3.8

0.5

0.4

9.6

11.6

0.4

0.3

Transport Corporation of

Neutral

250

-

1,899

2,830

3,350

8.8

9.0

14.4

18.3

17.4

13.6

2.7

2.3

15.4

17.1

0.8

0.7

India

Elecon Engineering

Neutral

65

-

711

1,369

1,533

13.7

14.9

3.3

6.1

19.7

10.8

1.3

1.2

6.6

11.4

0.9

0.8

Surya Roshni

Buy

151

201

661

2,992

3,223

8.1

8.4

14.7

18.3

10.3

8.2

1.0

0.9

9.7

11.0

0.5

0.5

MT Educare

Neutral

165

-

656

286

366

18.3

17.7

7.7

9.4

21.3

17.6

4.5

3.9

20.2

21.1

2.2

1.7

Radico Khaitan

Buy

114

156

1,517

1,565

1,687

12.2

13.0

5.7

7.1

20.0

16.1

1.7

1.5

8.3

9.6

1.4

1.3

Garware Wall Ropes

Buy

355

473

778

862

974

11.2

11.2

24.9

29.6

14.3

12.0

2.2

1.9

15.1

15.4

0.9

0.8

Wonderla Holidays

Neutral

399

-

2,252

206

308

44.0

43.6

9.0

12.9

44.3

30.9

6.1

5.5

13.7

17.8

10.8

7.2

Linc Pen & Plastics

Neutral

211

-

312

340

371

8.3

8.9

10.8

13.2

19.5

16.0

3.1

2.7

16.0

17.1

1.0

0.9

The Byke Hospitality

Neutral

159

-

637

222

287

20.5

20.5

5.6

7.6

28.2

21.0

5.3

4.4

18.9

20.8

2.9

2.2

Interglobe Aviation

Neutral

875

-

31,520

17,022

21,122

20.7

14.5

63.9

53.7

13.7

16.3

20.5

16.8

149.9

103.2

1.9

1.5

Coffee Day Enterprises

Neutral

263

-

5,424

2,692

2,964

17.0

18.6

-

4.7

-

55.6

3.2

3.0

0.2

5.5

2.4

2.2

Ltd

Navneet Education

Neutral

91

-

2,170

998

1,062

24.1

24.0

5.8

6.1

15.8

15.0

3.5

3.1

22.0

20.6

2.3

2.1

Navkar Corporation

Buy

200

265

2,849

365

436

38.3

37.5

5.6

5.9

35.4

34.0

2.2

2.1

6.3

6.1

8.6

7.4

Source: Company, Angel Research; Note: *December year end; #September year end; &October year end; Price as on January 29, 2016

Market Outlook

February 01, 2016

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitian Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial ownership

of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation / managed or co

-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst has not served as

an officer, director or employee of company covered by Analyst and has not been engaged in market making activity of the company

covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way responsible for any

loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Pvt.

Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any

representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking

Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance,

or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or

in connection with the use of this information.