M M Forging | Others

March 18, 2013

MM Forgings

BUY

CMP

`98

Forging the future

Target Price

`131

MM Forgings (MMFL) is one of the largest exporters of forgings from India with a

Investment Period

12 months

capacity of 40,000MT (exports contributed ~70.0% to the revenue in FY2013). It

is engaged in the manufacturing of steel forgings, catering to the forging

Stock Info

requirements of almost all sections of industry including Automotive, Valve and

Sector

Others

Oil-field, Engineering and Off Highway segments, with a focus on commercial

vehicle (CV) industry which contributed ~76.0% to the total revenue in FY2013.

Market Cap (` cr)

118

The company is now focusing on improving its operational efficiencies and increasing

Net debt (` cr)

115

capacity utilization, providing the company an immense potential to grow.

Beta

0.8

Sufficient capacity to cater to improving demand across the globe

52 Week High / Low

114/ 60

The company has a capacity of 40,000MT (last reported in FY2011). It is now

focusing on optimum capacity utilisation to take advantage of the production

Avg. Daily Volume

3,754

capacities that it has created. The company mainly caters to the global market

Face Value (`)

10

with a focus on the commercial vehicle industry and export focus on America and

BSE Sensex

21,810

Europe. After the recession, the American economy is now seeing an upturn, and

thus we are witnessing a growth in CV sales as well. In addition, the production in

Nifty

6,504

domestic CV industry grew by a CAGR of 22% over FY2008-12 and is expected to

Reuters Code

MMFO.BO

grow as a CAGR of 11% over FY2012-21E to 23.5lakh units. We expect this to

Bloomberg Code

MMFG IN

provide enormous opportunities to the company.

Rupee depreciation against US$ to boost company’s growth

The contribution of exports to the company’s revenue has increased from 57.4%

Shareholding Pattern (%)

in FY2008 to 70.3% in FY2013. Given that USA and Europe are the major

markets to which the company exports, the depreciating rupee against the US$

Promoters

59.5

and Euro is a positive for the company. In addition, the Chinese currency, Yuan,

MF / Banks / Indian Fls

14.3

has appreciated by 2.7% against the US$ in the past one year, while the INR has

FII / NRIs / OCBs

0.4

depreciated by 12.4% in the same period against the US$. This is providing the

Indian players an added competitive advantage in the export markets.

Indian Public / Others

25.9

Outlook and valuation: We expect MMFL to register a revenue CAGR of 13.9%

over FY2013-16E to `534cr with an operating margin of 18.1% in FY2016E. The

profit is expected to grow at a CAGR of 17.4% over the same period to `40cr in

Abs.(%)

3m

1yr

3yr

FY2016E. At the CMP, the company is trading at a PE of 3.0x FY2016E earnings.

Sensex

5.6

11.4

18.3

On account of positive growth outlook and low valuation, we initiate coverage on

MMFL

13.1

28.6

(8.8)

the company with a Buy recommendation with a target price of `131 on a target

PE of 4.0x FY2016E earnings.

Key financials

Y/E March (` cr)

FY2012 FY2013 FY2014E

FY2015E

FY2016E

Net Sales

350

361

412

469

534

% chg

28.7

3.1

14.1

13.9

13.9

Adj. Net Profit

21

24

28

32

40

% chg

(4.1)

14.7

13.0

16.9

22.4

OPM (%)

17.3

16.0

18.1

18.1

18.1

EPS (`)

17.7

20.3

22.9

26.8

32.8

P/E (x)

5.5

4.8

4.3

3.7

3.0

P/BV (x)

0.8

0.7

0.6

0.5

0.5

RoE (%)

15.2

15.1

15.1

15.8

17.1

RoCE (%)

14.2

12.7

13.3

15.0

16.6

Tejashwini Kumari

EV/Sales (x)

0.7

0.6

0.6

0.5

0.4

022-39357800 Ext: 6856

EV/EBITDA (x)

4.1

4.0

3.0

2.6

2.3

Source: Company, Angel Research, Note: CMP as of March 14, 2014

Please refer to important disclosures at the end of this report

1

M M Forgings | Initiating Coverage

Investment arguments

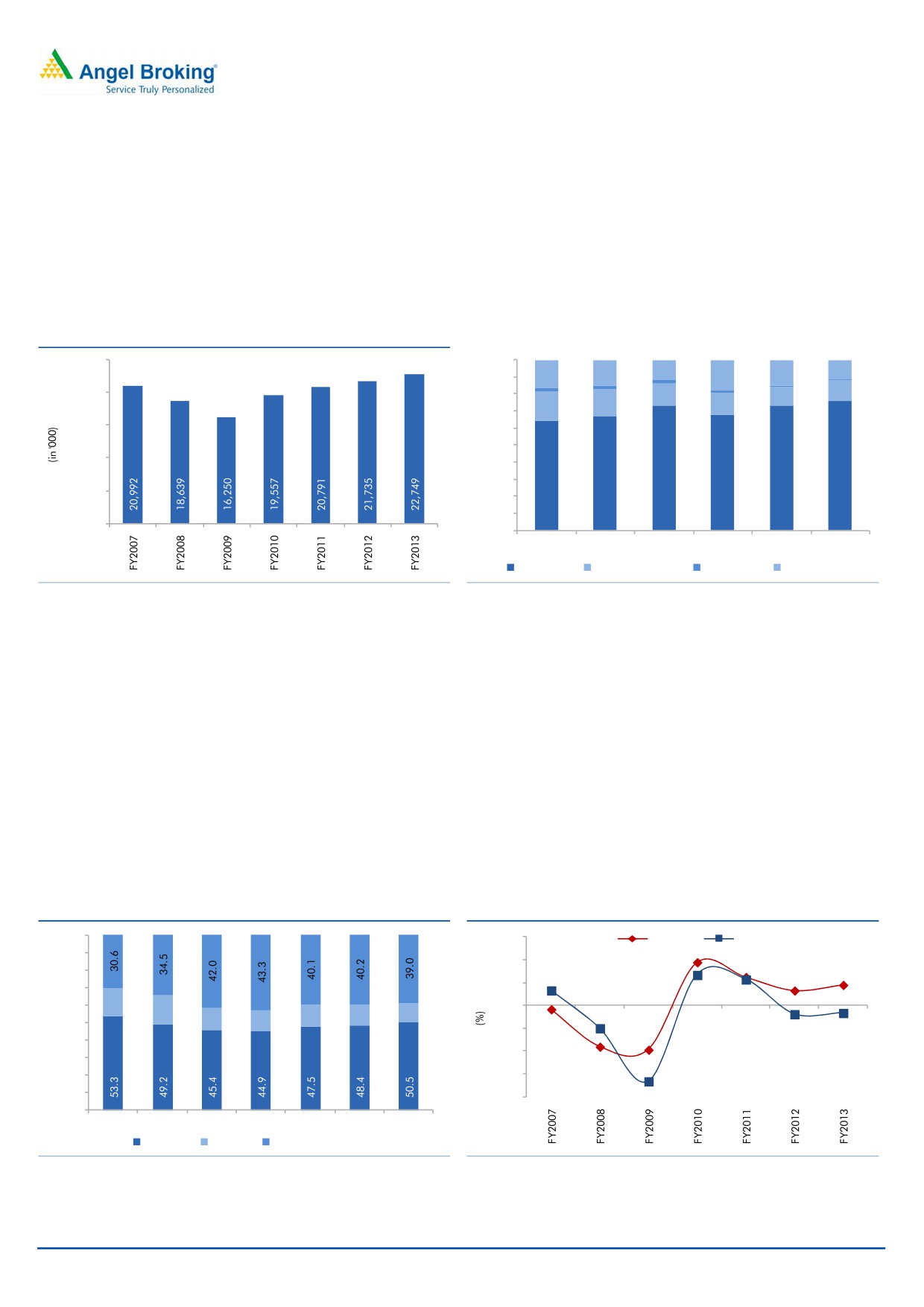

Sufficient capacity to cater to improving demand across the globe

The company has a capacity of 40,000MT (last reported in FY2011). It is now

focusing on optimum capacity utilisation to take advantage of the production

capacities created by it. The company mainly caters to the global market with a

focus on the CV industry.

Exhibit 1: Global CV sales

Exhibit 2: Automotive segment’s contribution increases in net sales

25,000

100%

15.0

12.0

15.0

11.0

90%

16.5

18.0

20,000

12.0

80%

13.0

11.0

17.0

16.1

13.0

70%

15,000

60%

50%

10,000

40%

30%

5,000

20%

10%

64.5

66.8

73.0

68.0

73.0

76.0

-

0%

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

Automotive

Valve and Oilfiled

Engineering

Off Highway

Source: OICA, Angel Research

Source: OICA, Angel Research

The CV industry contributed 76.0% to the company’s sales in FY2013. We expect

the demand to improve going forward as the economy recovers. The company

majorly exports to America and Europe. The American economy is now seeing an

upturn, and thus we are witnessing a growth in CV sales as well. In FY2013, the

CV sales grew by 9.0%. However, the scenario in Europe is still gloomy. The CV

sales in Europe are still sluggish; however, UK, one of the major markets has

shown some respite in the month of January and grew by 5.4% yoy.

According to Automotive Component Manufacturers Association (ACMA), the

production in domestic CV industry grew at a CAGR of 22% over FY2008-12 and

is expected to grow at a CAGR of 11% over FY2012-21E to 23.5lakh units. We

believe these factors provide MMFL a strong growth opportunity.

Exhibit 3: Geographical contribution in CV sales

Exhibit 4: CV sales pattern in America and Europe

100%

30.0

America

Europe

90%

20.0

19.0

12.5

80%

9.0

10.0

6.6

70%

6.6

13.4

11.4

60%

16.1

-

16.4

10.5

12.4

11.4

(10.0)

50%

12.5

11.8

(1.7)

(10.0)

(3.8)

(3.3)

40%

(19.4)

(20.0)

30%

(18.1)

20%

(30.0)

(33.3)

10%

(40.0)

0%

FY2007 FY2008 FY2009 FY2010 FY2011 FY2012 FY2013

America

Europe

Rest of the world

Source: Company, Angel Research

Source: Company, Angel Research

February 18, 2014

2

M M Forgings | Initiating Coverage

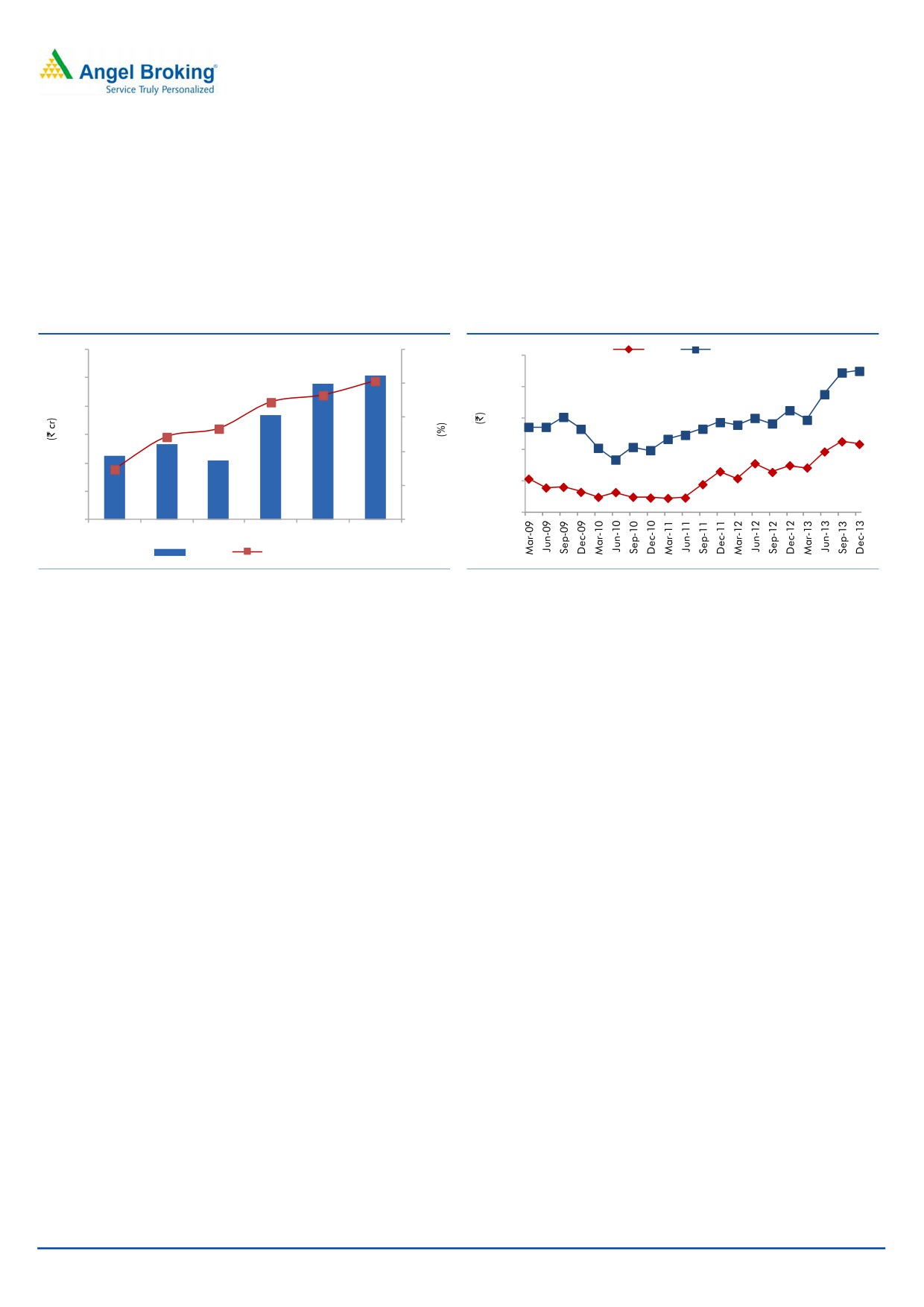

Rupee depreciation against US$ to boost company’s growth

The contribution of exports to the company’s revenue has increased from 57.4% in

FY2008 to 70.3% in FY2013. Given that USA and Europe are the major markets

to which the company exports, the depreciating rupee against the US$ and Euro is

a positive for the company. We do not expect any correction in the same in the

near term.

Exhibit 5: Increasing contribution of exports

Exhibit 6: Depreciating rupee - an advantage

300

75.0

USD

EURO

90.0

85.1

70.3

250

68.3

67.2

70.0

80.0

200

63.4

67.2

62.1

65.0

70.0

61.8

150

57.4

60.0

60.0

100

50.7

50.0

55.0

50

113

133

104

183

239

254

40.0

0

50.0

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

Export

% of total sales

Source: Company, Angel Research

Source: Company, Angel Research

Further, the appreciation of the Yuan is an additional advantage for Indian

exports. The Chinese currency, Yuan, has appreciated by 2.7% against the USD in

the past one year, however, the INR has depreciated by 12.4% in the same time

against US$ which is providing the Indian players an added advantage in the

export market.

February 18, 2014

3

M M Forgings | Initiating Coverage

Financials

Exhibit 7: Key assumptions

Y/E March

FY2014E

FY2015E

FY2016E

Global CV sales

23,886,810

25,200,585

26,586,617

yoy growth (%)

5.0

5.5

5.5

Total operating Income (` cr)

412

469

534

yoy growth (%)

14.1

13.9

13.9

Source: Company, Angel Research

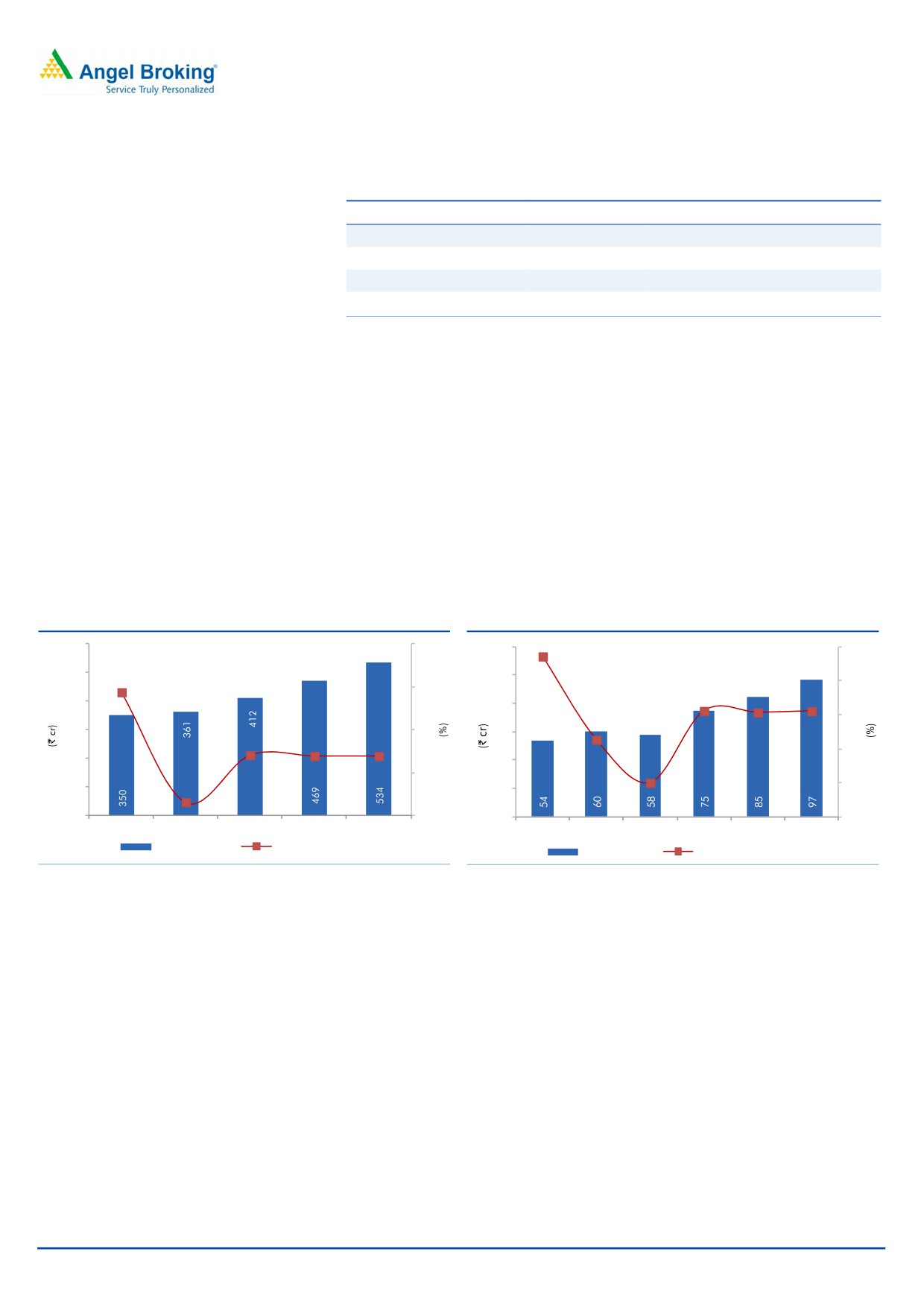

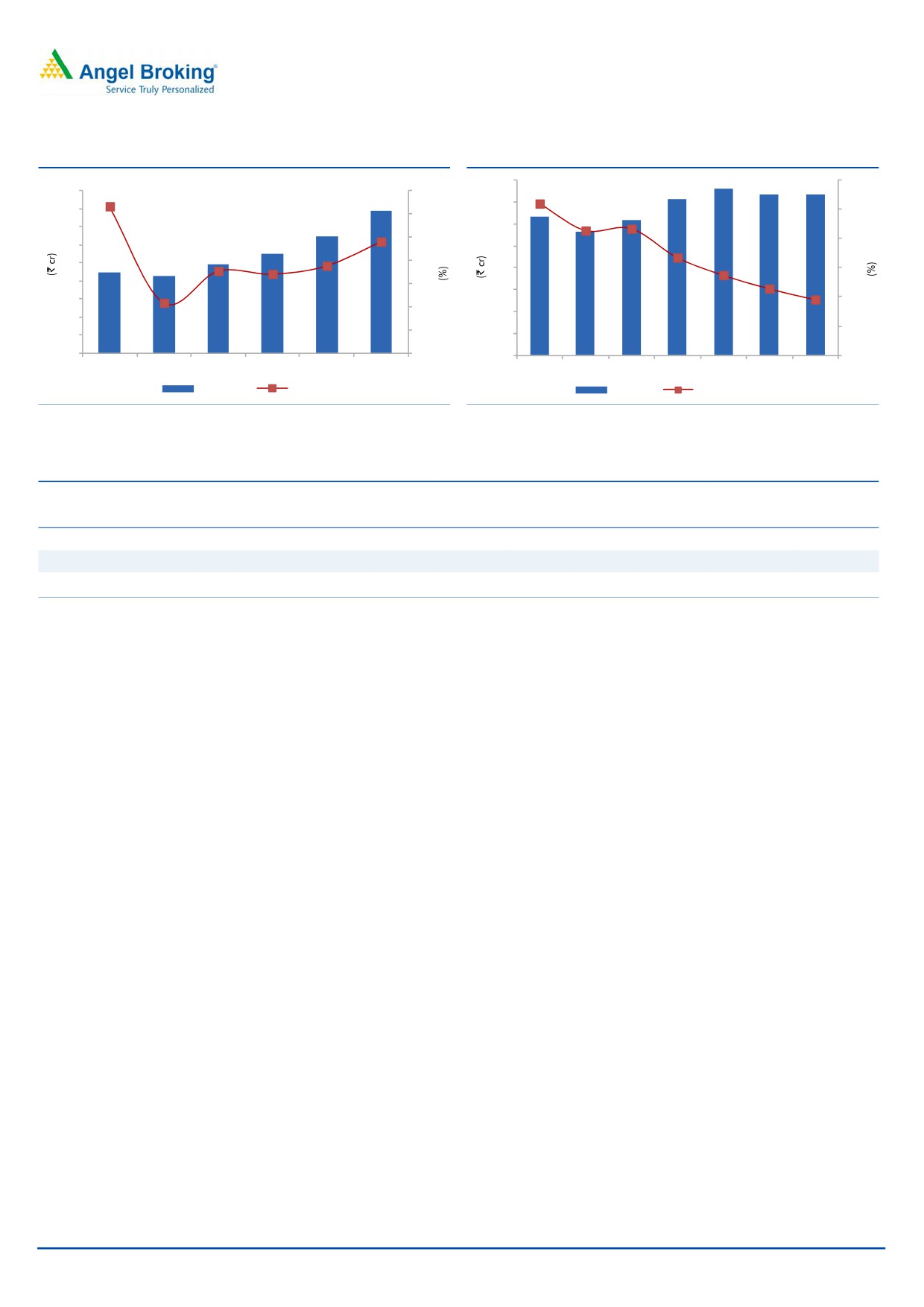

Revenue to grow on the back of global CV industry recovery

The company has witnessed a CAGR growth of 30.0% over FY2009-13 while the

global CV industry’s sales contracted by 38.8% during the same period. The

current capacity of the company is of 40,000MT and it is continuously focusing on

increasing capacity utilization level to take advantage of the production capacities

created by it. On the back of recovery trends visible in the CV industry across the

globe and the company’s strong relationship with its customers, we expect the

company to successfully ramp up capacity utilization and witness strong top-line

growth. We expect the revenue for the company to grow at a CAGR of 13.9% over

FY2013-16E to `534cr.

Exhibit 8: Improving CV sales to drive volume

Exhibit 9: Improving operational efficiencies to aid margin growth

600

40

120

19.7

20

500

28.7

100

19

30

18.1

18.1

18.1

400

80

18

17.3

300

20

60

13.9

13.9

17

200

40

16.0

10

14.1

16

100

3.1

20

0

0

0

15

FY2012

FY2013

FY2014E

FY2015E

FY2016E

FY2011

FY2012

FY2013

FY2014E FY2015E FY2016E

Revenue (LHS)

Revenue growth (RHS)

EBITDA (LHS)

EBITDA Margin (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

On the back of different energy conservation methods undertaken by the

company, its power and fuel costs are expected to reduce over FY2013-16E from

12.8% to 11.0% of net sales. In addition, continuous efforts are being made on

conservation of raw material by improving design and layout of dies leading to

reduction in raw material consumption. Also, the company is able to pass on the

changes in steel prices to the customers.

We believe that with improving operational efficiencies and increasing capacity

utilization, the operating margin will improve by 210bp over FY2013-16E at

18.1%. We expect the debt of the company to be offloaded marginally leading to

a lower interest cost going forward. Consequently, we expect the profit to grow at

a CAGR of 17.4% over FY2013-16E to `40cr.

February 18, 2014

4

M M Forgings | Initiating Coverage

Exhibit 10: PATM to improve

Exhibit 11: Net debt to equity to decrease

8

1.2

45

8.2

8.5

7

1.0

40

1.0

8.0

35

7.4

6

0.9

0.9

7.5

0.8

30

6.9

5

6.8

0.7

25

6.7

7.0

4

0.6

0.5

20

6.1

6.5

3

0.5

15

0.4

0.4

6.0

2

10

0.2

5

5.5

1

22

21

24

28

32

40

6

6

6

7

8

7

7

0

5.0

0

0.0

FY2011

FY2012

FY2013

FY2014E FY2015E FY2016E

FY2010

FY2011

FY2012

FY2013

FY2014E FY2015E FY2016E

PAT (LHS)

PATM (RHS)

Interest

Net debt to equity

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 12: Relative valuation (Trailing twelve months)

Mcap

Sales

OPM

PAT

EPS

RoE

P/E

P/BV

EV/Sales

EV/

Company

(` cr)

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

EBITDA (x)

M M Forgings

287

387

18.3

28

23.5

13.7

4.2

0.6

3.1

0.6

Ramkrishna Forgings

118

364

13.3

4

1.6

3.7

69.5

0.9

13.7

1.8

Ahmednagar Forgings

398

1,607

24.6

148

40.3

11.3

2.7

0.4

5.3

1.3

Source: Company, Angel Research; * Bloomberg estimates

February 18, 2014

5

M M Forgings | Initiating Coverage

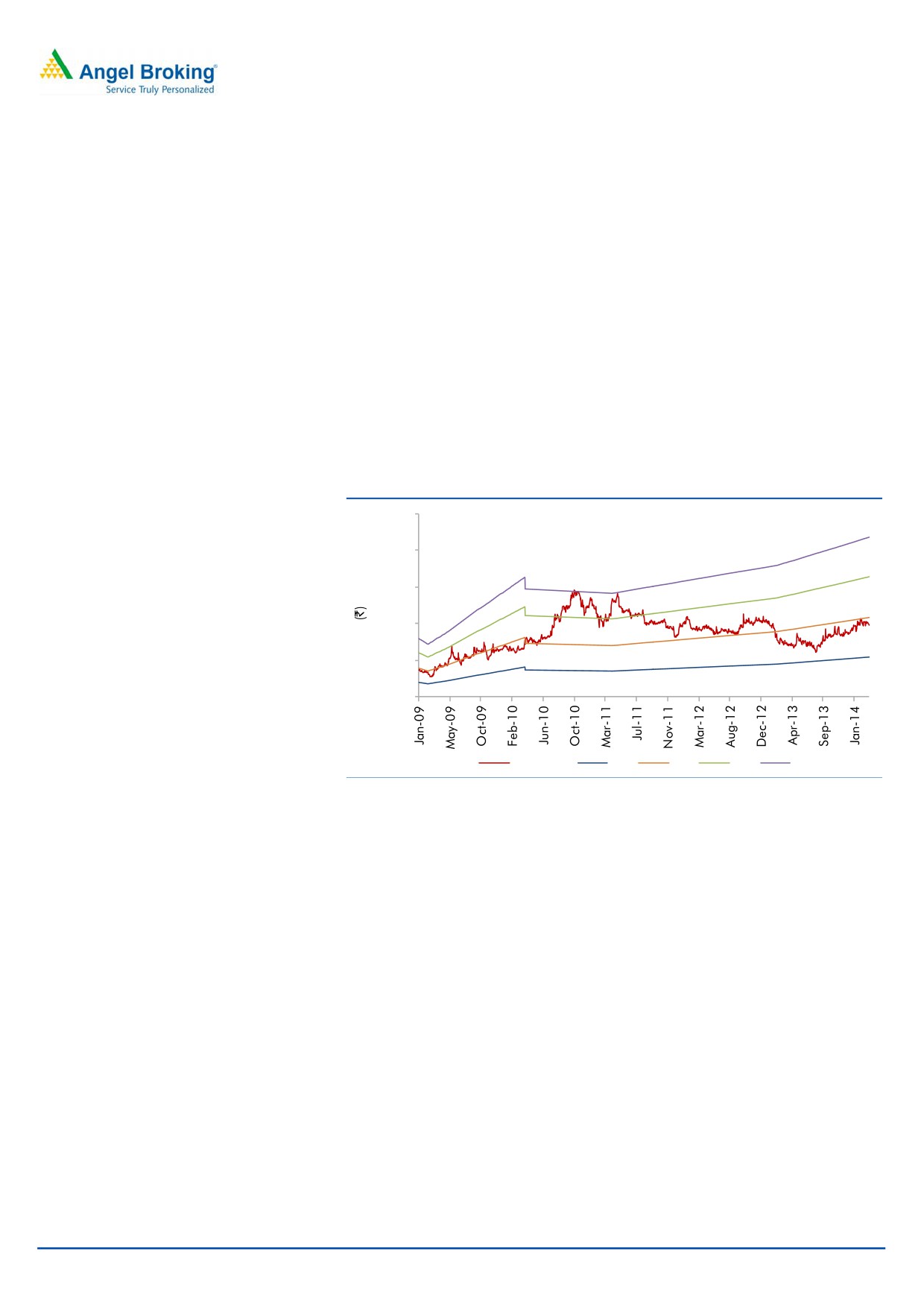

Outlook and valuation: We expect MMFL to register a revenue CAGR of 13.9%

over FY2013-16E to `534cr in FY2016E. On account of improving operational

efficiencies and increasing capacity utilization, we expect the operating margin for

the company to expand by 210bp over the same period to 18.1% for FY2016E.

Consequently the profit is expected to grow at a CAGR of 17.4% over FY2013-16E

to `40cr in FY2016E.

Given the company’s increased capacity from 35,000MT in FY2007 to 40,000MT

in FY2011 and improvement in the economy of its major export markets - America

and Europe, we are positive on the company from a long term perspective.

At the CMP, the company is trading at a PE of 3.0x FY2016E earnings. On account

of positive growth outlook and low valuation, we initiate coverage on the company

with a Buy recommendation with a target price of `131 at a target PE of 4.0x

FY2016E earnings.

Exhibit 13: One-year forward P/E band

250

200

150

100

50

0

Price (`)

2x

4x

6x

8x

Source: Company, Angel Research

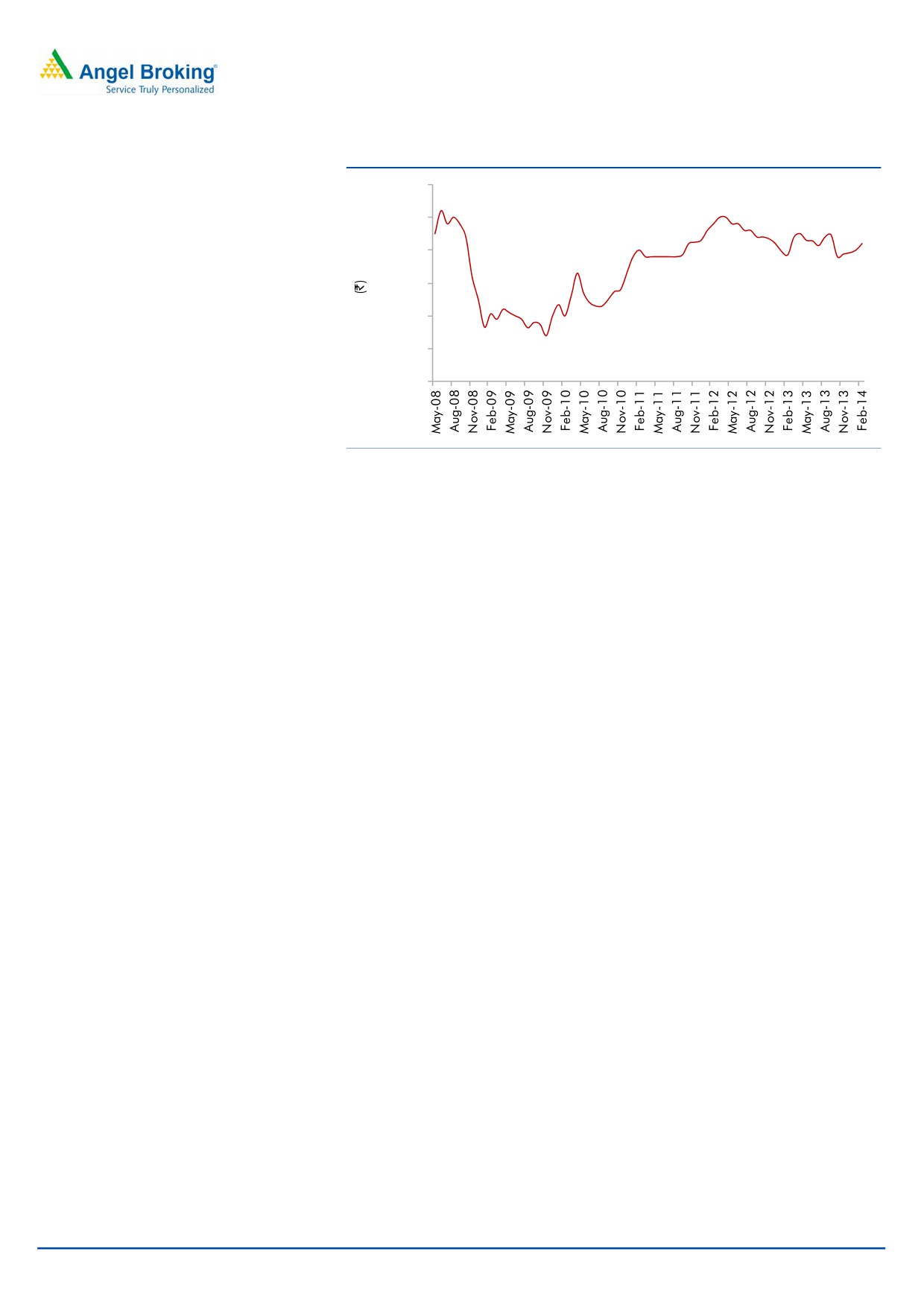

Concerns

Continued slowdown in CV industry: The company earns its major revenue from

the CV industry, mainly in the US and Europe. Any prolonged slowdown in these

economies can adversely affect the company’s performance.

Adverse movement in currency: Rupee depreciation is an added advantage for the

company. In case of any appreciation, the revenue of the company will be

adversely affected.

Fluctuations in Steel price: Any substantial fluctuation in the steel price can lead to

margin compression of the company.

February 18, 2014

6

M M Forgings | Initiating Coverage

Exhibit 14: Steel price

50,000

45,000

41,000

40,000

35,000

30,000

25,000

20,000

Source: Angel Research, Bloomberg

Company background

MM Forgings (MMFL) was incorporated in 1946 as Madras Motors Ltd. and was

renamed MM Forgings Ltd. in the year 1993. It is engaged in the manufacturing of

steel forgings, with a work force of 1,105 employees. It manufactures steel

forgings in raw, semi-machined and fully machined stages in various grades of

Carbon, Alloy, Micro-Alloy and Stainless Steels in the weight range of 0.20Kg to

60Kg. The Company caters to the forging requirements of almost all sections of

the industry - Automotive, Valve and Oil-filed, Engineering and Off Highway.

The company’s manufacturing plants are located at Singampunari-Pasumpon

Muthuramalingam District, Viralimalai-Pudukkottai District and Karainaithangal

Village- Kanchipuram District, all in Tamil Nadu. The company has its Wind Farm

at Panakudi Village- Tirunelveli District and at Meenakshipuram, Theni District and

the power generated is used for captive use.

Further the company earns ~70% of its sales from exports, mainly to the US and

Europe.

Industry

Global forging industry

According to a report by ResearchMoz, a New York based market research firm,

the global forging industry is expected to grow at a CAGR of 9.4% over FY2012-

16E, and the automotive industry is believed to be the major factor contributing in

this growth. It further states that the global forging industry is sourcing forged

products from countries where manufacturing costs are low.

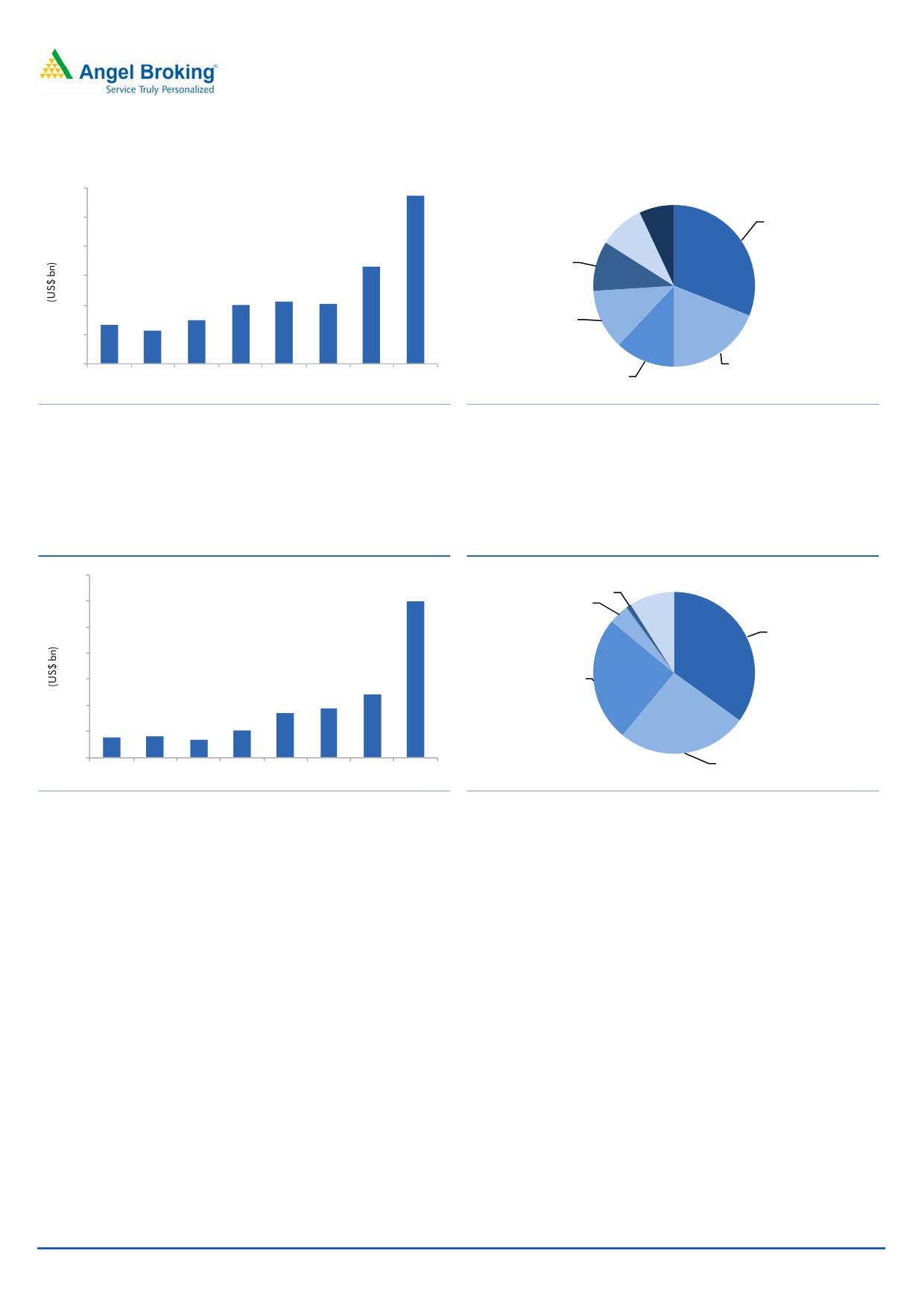

Domestic auto component and forging industry

According to ACMA estimates, the domestic auto component industry has grown at

a CAGR of 12% over FY2008-12 and is expected to grow at a CAGR of 14% over

FY2013-21E to US$115bn in FY2021E.

February 18, 2014

7

M M Forgings | Initiating Coverage

Exhibit 15: Auto Component Industry Profile - Turnover

Exhibit 16: Auto component industry product profile (2012)

Others

115

120

7%

Electrical parts

100

9%

Engine parts

31%

80

66

Equipments

10%

60

40

42

41

40

30

27

23

Suspension &

Braking parts

20

12%

Drive

0

transmission &

FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2016E FY2021E

Body & chasis

steering parts

12%

19%

Source: ACMA, Angel Research

Source: ACMA, Angel Research

Also, the export of auto components is expected to grow at a CAGR of 16% over

FY2013-21E. In value terms the export is expected to grow from US$9bn to

US$30bn over the same period.

Exhibit 17: Auto Component Industry Profile - Exports

Exhibit 18: Export destination

35.0

Australia

Africa

30.0

1%

9%

30.0

South America

4%

25.0

Europe

35%

20.0

Asia

15.0

12.0

25%

9.3

8.5

10.0

5.2

3.8

4.0

3.4

5.0

0.0

North America

FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2016E FY2021E

26%

Source: ACMA, Angel Research

Source: ACMA, Angel Research

The Indian forging industry was valued at `25,000cr (May, 2013) and looking at

the auto component industry’s future growth forecasts, it is expected that the

production of forgings will be at ~ `37,000cr by FY2015E. The forging industry

has installed capacity of 3.8mn tonne/year with a capacity utilisation rate of 75%.

February 18, 2014

8

M M Forgings | Initiating Coverage

Profit and loss statement

Y/E Mar. (` cr)

FY2012

FY2013

FY2014E

FY2015E

FY2016E

Net Sales

350

361

412

469

534

Other operating income

-

-

-

-

-

Total operating income

350

361

412

469

534

% chg

28.7

3.1

14.1

13.9

13.9

Net Raw Materials

147

154

176

201

229

% chg

49.6

4.9

14.0

14.2

14.0

Power and Fuel

45

46

46

52

59

% chg

30.5

2.7

0.1

12.8

12.8

Personnel

28

31

39

45

51

% chg

0.7

11.8

26.7

13.9

13.9

Other

70

72

76

87

99

% chg

20.2

2.6

5.6

13.9

13.9

Total Expenditure

290

303

337

384

437

EBITDA

60

58

75

85

97

% chg

12.7

(4.4)

29.1

13.6

14.1

(% of Net Sales)

17.3

16.0

18.1

18.1

18.1

Depreciation

23

21

35

37

40

EBIT

37

37

40

48

57

% chg

10.5

(1.9)

7.9

20.3

19.7

(% of Net Sales)

10.7

10.1

9.6

10.1

10.7

Interest & other Charges

6

7

8

7

7

Other Income

7

1

4

4

5

(% of Net Sales)

2.1

0.1

0.9

0.9

0.9

Recurring PBT

31

30

32

40

49

% chg

10.7

(5.5)

7.7

26.2

23.3

PBT (reported)

39

30

35

44

54

Tax

12

6

8

12

15

(% of PBT)

30.7

18.6

22.2

27.2

27.2

PAT (reported)

27

24

28

32

40

Extraordinary Expense/(Inc.)

5

0

0

0

0

ADJ. PAT

21

24

28

32

40

% chg

(4.1)

14.7

13.0

16.9

22.4

(% of Net Sales)

6.1

6.8

6.7

6.9

7.4

Basic EPS (`)

17.7

20.3

22.9

26.8

32.8

Fully Diluted EPS (`)

17.7

20.3

22.9

26.8

32.8

% chg

(4.1)

14.7

13.0

16.9

22.4

February 18, 2014

9

M M Forgings | Initiating Coverage

Balance sheet

Y/E Mar. (` cr)

FY2012

FY2013

FY2014E

FY2015E

FY2016E

SOURCES OF FUNDS

Equity Share Capital

12

12

12

12

12

Reserves& Surplus

140

160

181

205

233

Shareholders’ Funds

152

172

193

217

246

Total Loans

133

117

111

111

111

Other Long Term Liabilities

1

1

1

1

1

Long Term Provisions

0

0

0

0

0

Deferred Tax (Net)

10

11

11

11

11

Total liabilities

296

300

315

339

368

APPLICATION OF FUNDS

Gross Block

369

398

438

464

497

Less: Acc. Depreciation

181

202

237

275

314

Net Block

188

196

201

190

182

Capital Work-in-Progress

3

4

4

5

5

Goodwill

-

-

-

-

-

Investments

0

0

0

0

0

Long Term Loans and adv.

-

-

-

-

-

Other Non-current asset

12

17

20

23

32

Current Assets

137

146

155

195

232

Cash

1

1

2

5

10

Loans & Advances

27

39

38

56

72

Inventory

85

71

82

91

101

Debtors

23

34

33

42

48

Other current assets

-

-

-

-

-

Current liabilities

44

63

65

74

84

Net Current Assets

94

83

90

121

148

Misc. Exp. not written off

-

-

-

-

-

Total Assets

296

300

315

339

368

February 18, 2014

10

M M Forgings | Initiating Coverage

Cash flow statement

Y/E Mar. (` cr)

FY2012 FY2013 FY2014E FY2015E FY2016E

Profit before tax

39

30

35

44

54

Depreciation

23

21

35

37

40

Change in Working Capital

(1)

10

(6)

(28)

(22)

Direct taxes paid

(12)

(6)

(8)

(12)

(15)

Others

(1)

2

(4)

(4)

(5)

Cash Flow from Operations

48

57

53

37

53

(Inc.)/Dec. in Fixed Assets

(66)

(30)

(40)

(27)

(33)

(Inc.)/Dec. in Investments

-

(0)

-

-

-

(Incr)/Decr In LT loans & adv.

(2)

(5)

(3)

(4)

(9)

Others

9

6

4

4

5

Cash Flow from Investing

(59)

(30)

(39)

(26)

(37)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

21

(17)

(6)

-

-

Dividend Paid (Incl. Tax)

(4)

(4)

(4)

(4)

(4)

Others

(6)

(7)

(3)

(4)

(7)

Cash Flow from Financing

11

(28)

(13)

(8)

(11)

Inc./(Dec.) in Cash

0

(0)

1

2

5

Opening Cash balances

1

1

1

2

5

Closing Cash balances

1

1

2

5

10

February 18, 2014

11

M M Forgings | Initiating Coverage

Key ratios

Y/E Mar.

FY2012

FY2013

FY2014E

FY2015E

FY2016E

Valuation Ratio (x)

P/E (on FDEPS)

5.5

4.8

4.3

3.7

3.0

P/CEPS

2.7

2.6

1.9

1.7

1.5

P/BV

0.8

0.7

0.6

0.5

0.5

EV/Net sales

0.7

0.6

0.6

0.5

0.4

EV/EBITDA

4.1

4.0

3.0

2.6

2.3

EV / Total Assets

0.9

0.8

0.7

0.7

0.6

Per Share Data (`)

EPS (Basic)

17.7

20.3

22.9

26.8

32.8

EPS (fully diluted)

17.7

20.3

22.9

26.8

32.8

Cash EPS

36.8

37.8

51.9

57.5

65.7

DPS

3.0

3.0

3.0

3.0

3.0

Book Value

125.8

142.6

159.8

179.5

203.4

DuPont Analysis

EBIT margin

10.7

10.1

9.6

10.1

10.7

Tax retention ratio

0.7

0.8

0.8

0.7

0.7

Asset turnover (x)

1.3

1.3

1.4

1.5

1.6

ROIC (Post-tax)

10.0

10.5

10.6

11.3

12.6

Cost of Debt (Post Tax)

3.5

4.7

5.3

4.9

4.9

Leverage (x)

0.9

0.7

0.6

0.5

0.4

Operating ROE

15.6

14.5

13.5

14.3

15.7

Returns (%)

ROCE (Pre-tax)

14.2

12.7

13.3

15.0

16.6

Angel ROIC (Pre-tax)

14.4

13.0

13.6

15.4

17.2

ROE

15.2

15.1

15.1

15.8

17.1

Turnover ratios (x)

Asset TO (Gross Block)

1.0

0.9

1.0

1.0

1.1

Inventory / Net sales (days)

78

79

68

67

66

Receivables (days)

34

29

29

33

33

Payables (days)

50

64

70

70

70

WC cycle (ex-cash) (days)

96

88

75

79

87

Solvency ratios (x)

Net debt to equity

0.9

0.7

0.6

0.5

0.4

Net debt to EBITDA

2.2

2.0

1.5

1.3

1.0

Int. Coverage (EBIT/ Int.)

6.1

5.1

5.1

6.4

7.6

February 18, 2014

12

M M Forgings | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Angel Broking Pvt. Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Pvt. Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking

or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or

in the past.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

M M Forgings

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to -15%)

Sell (< -15%)

February 18, 2014

13

M M Forgings | Initiating Coverage

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Bhavesh Chauhan

Sr. Analyst (Metals & Mining)

V Srinivasan

Analyst (Cement, FMCG)

Yaresh Kothari

Analyst (Automobile)

Ankita Somani

Analyst (IT, Telecom)

Bhupali Gursale

Economist

Vinay Rachh

Research Associate

Amit Patil

Research Associate

Twinkle Gosar

Research Associate

Tejashwini Kumari

Research Associate

Akshay Narang

Research Associate

Harshal Patkar

Research Associate

Nishant Sharma

Research Associate

Technicals and Derivatives:

Siddarth Bhamre

Head - Technical & Derivatives

Sameet Chavan

Technical Analyst

Nagesh Arekar

Executive

Sneha Seth

Associates (Derivatives)

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Production Team:

Tejas Vahalia

Research Editor

Dilip Patel

Production Incharge

CSO & Registered Office: G-1, Ackruti Trade Centre, Road No. 7, MIDC, Andheri (E), Mumbai - 93. Tel: (022) 3083 7700. Angel Broking Pvt. Ltd: BSE Cash: INB010996539 / BSE F&O: INF010996539, CDSL Regn. No.: IN - DP - CDSL - 234 - 2004, PMS Regn. Code: PM/INP000001546, NSE Cash: INB231279838 /

NSE F&O: INF231279838 / NSE Currency: INE231279838, MCX Stock Exchange Ltd: INE261279838 / Member ID: 10500. Angel Commodities Broking (P) Ltd.: MCX Member ID: 12685 / FMC Regn. No.: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn. No.: NCDEX / TCM / CORP / 0302.

February 18, 2014

14