IPO Note | Commodity Exchange

February 22, 2012

Multi Commodity Exchange (MCX)

SUBSCRIBE

Issue Open: February 22, 2012

A Gold(en) Opportunity

Issue Close: February 24, 2012

Sustainable competitive position: Multi Commodity Exchange of India Ltd. (MCX)

Issue Details

is a leading commodities exchange, which received permanent recognition from

Government of India on September 26, 2003. The company reported a market

Face Value: `10

share of 87.3% as of December 2011. MCX is also the fifth largest commodity

Present Eq. Paid-up Capital: `51.0cr

futures exchange globally in terms of the number of contracts. As of June 2011,

Offer Size*: 0.64cr Shares

MCX was the largest silver exchange, the second largest gold, copper and natural

gas exchange and the third largest crude oil exchange for this period globally.

Post Eq. Paid-up Capital: `51.0cr

Growth strategy in place: MCX has introduced a variety of new commodity futures

Issue size (amount):** `553-663cr

contracts; and since inception, the number of products offered by the company

Price Band: `860-1,032

has grown from 15 to 49 as of December 31, 2011. MCX has 2,153 members

Post-issue implied mkt cap**: `4,386cr-

5,263cr

nationwide with over 296,000 terminals, including CTCL spread over 1,572 cities

Promoters holding Pre-Issue: 31.2%

and towns in India. The company intends to continue to increase the number of

participants by introducing new products on its exchange by expanding to more

Promoters holding Post-Issue: 26.0%

geographical areas, which is expected to drive growth going ahead. Regulatory

Note:* 250,000 reserved for employees;

**At the lower and upper price band, respectively

changes can also lent a fillip to MCX as currently option contracts are not allowed

to be traded in commodity. Any changes in favor of MCX can lead to a major

increase in revenue and profitability going ahead.

Book Building

QIBs

Up to 50%

Outlook and valuation: MCX currently has zero debt on its book, and major

capex to fuel growth has already been incurred by the company. Secondly, the

Non-Institutional

At least 15%

company reported investment and cash worth `1,324cr at the end of 9MFY2012,

Retail

At least 35%

which works out to `260/share. On an annualized basis, the stock will be trading

at 15.1x and 18.1x at the lower and upper band on FY2012E earnings,

respectively, which we believe is fair compared to global peers, which trade at

Post Issue Shareholding Pattern

18x-19x TTM earnings; further, the recent off-market deals value MCX’s Indian

Promoters Group

26.0

peers, NSE and BSE, at 22x-24x 9MFY2012 annualized earnings. We believe

MF/Banks/Indian

MCX being the only major commodity exchange in India and the world’s fifth

FIs/FIIs/Public & Others

74.0

largest exchange can witness strong growth in revenue and profitability going

ahead, which makes its valuation much more attractive than global peers. Hence,

we recommend Subscribe to the issue on account of its relatively fair valuations.

Key financials

Y/E March (` cr)

FY2009

FY2010

FY2011

9MFY2012

Net Sales

212

287

369

402

% chg

-

35.3

28.4

9.1

Net Profit

159

221

176

218

% chg

-

39.0

(20.2)

23.6

Adj. Net Profit

67

74

171

210

% chg

-

9.0

132.0

22.9

EBITDA Margin (%)

36.0

49.3

52.0

64.8

FDEPS (`)

38.9

54.1

34.6

42.7

P/E (x) Lower End

22.1

15.9

24.9

20.1

Sharan lillaney

P/E (x) Upper End

26.5

19.1

29.9

24.1

022 - 39357800 Ext: 6811

RoE (%)

32.2

31.7

20.8

20.3

Source: Company, Angel Research Note: Net profit adjusted for sale of investments.

Please refer to important disclosures at the end of this report

1

MCX | IPO Note

Company background

Multi Commodity Exchange of India Ltd. (MCX) is a leading commodities exchange

in India based on value of commodity futures contracts traded. A

de-mutualized exchange, MCX received permanent recognition from the

Government of India on September 26, 2003, to facilitate nationwide online

trading, clearing and settlement operations of commodities futures transactions.

The total value of commodity futures contracts traded on MCX in 9MFY2012 was

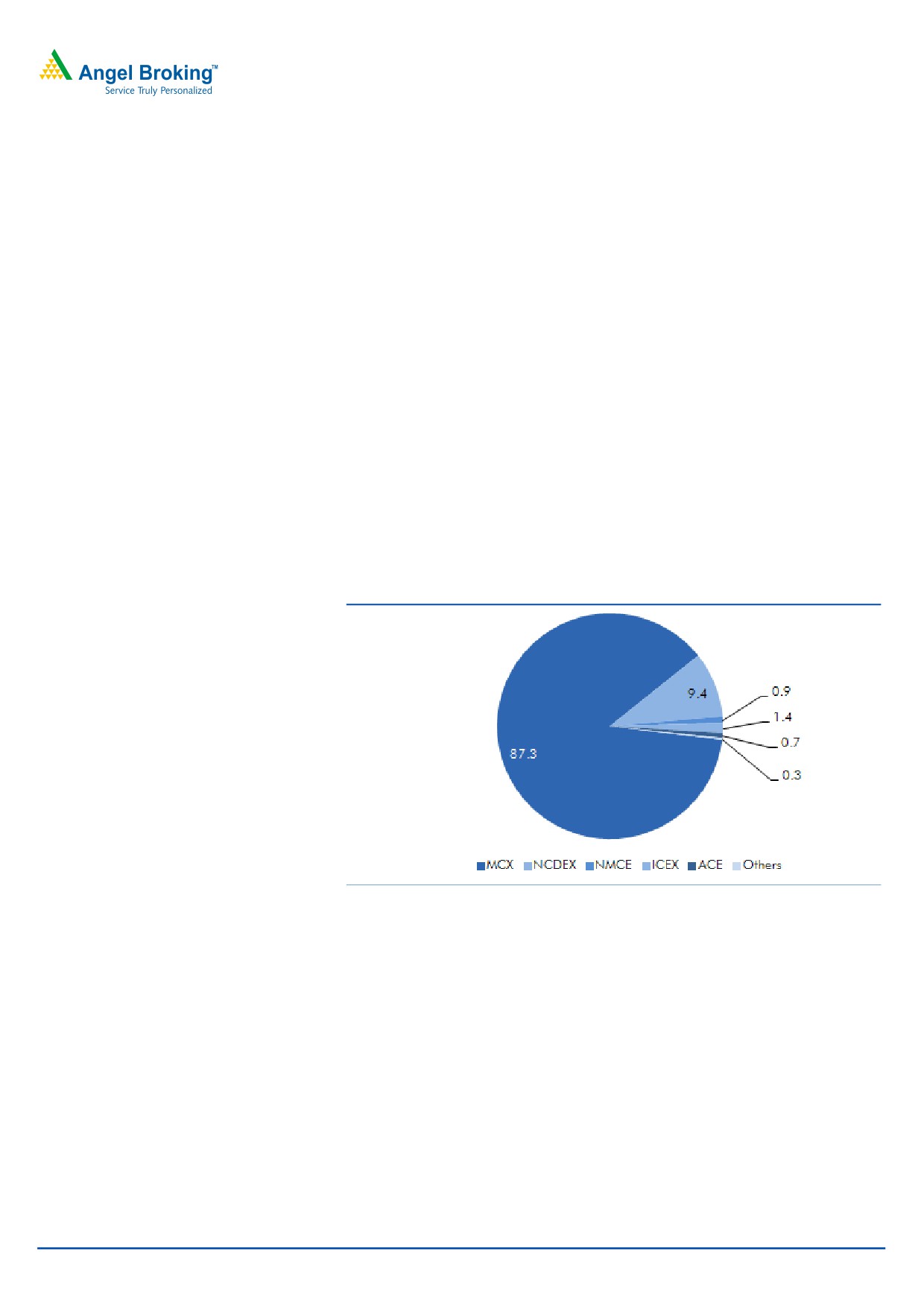

`119,807bn. Further, MCX has reported a 45% CAGR in the past four years.

According to data maintained by the FMC, these amounts represented 87.3%

(9MFY2012), 82.4% (FY2011), 82.3% (FY2010) and 87.4% (FY2009) of the Indian

commodity futures industry in terms of the value of commodity futures contracts

traded. Currently, MCX offers trading in 49 commodity futures, including bullion,

ferrous and non-ferrous metals, energy and agriculture. The same underlying

physical asset traded under different contract specifications is regarded as a

separate commodity future. As of December 31, 2011, MCX had 2,153 members,

with over 296,000 terminals, including CTCL spread over 1,572 cities and towns

across India. Silver, gold, crude oil and copper dominate the value with ~90% of

total value traded.

Exhibit 1: Highest market share amongst local peers

Source: Company, Angel Research

Details of the issue

The IPO comprises an issue of 6.4mn equity shares of face value `10 each to the

public, with a reservation of 0.25mn equity shares for subscription by eligible

employees. The issue shall constitute 12.6% of the post-issue paid-up capital. MCX

has fixed the issue price band at `860-1,032 per share, valuing the company at

US$877mn to US$1,052mn (`4,386cr to `5,263cr). The key shareholders who are

tendering their shares are Financial Technologies, promoter of MCX, with 2.6mn

shares, State Bank of India with 2.1mn shares, and GLG Financials Fund with

0.8mn shares. The remaining 0.9mn shares are being offered by Alexandra, Bank

of Baroda, ICICI Lombard and Corporation Bank. MCX will not get any money

from this IPO as it is an offer for sale.

February 22, 2012

2

MCX | IPO Note

Investment arguments

Market leader in the commodity futures industry

MCX is a leading commodity futures exchange in India in terms of value of

commodity futures contracts traded in metals, energy and certain agricultural

commodities. According to FMC, the total value of commodity futures contracts

traded on MCX for the nine months ended December 31, 2011, FY2011 and

FY2010 constituted

87.3%,

82.4% and

82.3%, respectively, of the Indian

commodity futures industry during those periods. Among national commodities

exchanges in India, MCX’s market share based on the total value of commodities

traded in futures markets for the nine months ended December 31, 2011, for

gold, crude oil, silver, copper and natural gas futures contracts was approximately

97.1%,

94.8%,

98.5%,

94.9% and 99.9%, respectively. (Source: Information

derived from FMC April - December 2011 data). MCX is the fifth largest commodity

futures exchange globally, among all commodity exchanges considered in the FIA

survey, in terms of the number of contracts traded and were among the leading

commodity exchanges in the world in terms of trading volumes of certain

commodities. Based on the comparison of the trading volumes of the exchange

with leading global commodity futures exchanges in the world, for CY2010 and

the six months ended June 30, 2011, MCX is the largest silver exchange, the

second largest gold, copper and natural gas exchange and the third largest crude

oil exchange for this period.

Exhibit 2: Top ranked contracts by volume in the world

Exhibit 3: 5th largest commodity exchange by volume

Commodity futures contracts

World Rank

Rank Particulars

1HCY2010

1HCY2011

Growth yoy

MCX Crude Oil Futures

6

1 CME Group

299

353

18.1

MCX Silver Mini Futures

7

2 Zhengzhou CX

227

218

(4.0)

MCX Copper Futures

9

3 ICE Group

134

159

18.4

MCX Silver Futures

10

4 Shanghai FE

300

129

(57.2)

MCX Silver Micro Futures

11

5 MCX

90

128

41.5

Source: Company, Angel Research

Source: Company, Angel Research

February 22, 2012

3

MCX | IPO Note

Growth strategy going ahead

New products and services to drive growth

MCX has introduced a variety of new commodity futures contracts since inception.

The number of products offered by MCX has grown from 15 as of March 31,

2004, to 49 as of December 31, 2011. The company is expected to continue to

focus on offering futures trading in commodities, which are significant in the Indian

and global contexts, and will continue to offer trading in commodities through

contracts that will be customized to meet the needs of Indian markets, such as

Gold Mini and Gold Petal contracts, which are aimed at local retail investors.

Exhibit 4: Strong volume growth in 9MFY2012

Commodity

FY2009

FY2010

FY2011

9MFY2012

Gold Guinea

3

4

4

8

Gold

15

11

11

10

Gold Mini

14

13

15

23

Source: Company, Angel Research

Increasing market presence and participants

As of December 31, 2011, MCX has 2,153 members nationwide with over

296,000 terminals including CTCL spread over 1,572 cities and towns in India. It

intends to continue to increase the number of participants by introducing new

products on its exchange by expanding to more geographical areas and by

continuing its efforts to disseminate knowledge and information about the

commodity futures industry. Along with its alliance partners, MCX plans to establish

and grow its presence in additional regions across India.

February 22, 2012

4

MCX | IPO Note

Capitalize on changes proposed in regulations

MCX also intends to capitalize on changes proposed in regulations governing the

Indian commodities derivatives industry, permitting trading in options and

intangibles, including indices. For example, it has already developed the software

technology infrastructure and other in-house expertise to launch trading in

commodities options when such trading is permitted to reduce the lead time to the

market. Similarly, if and when trading in commodity indices is permitted, investors

will be able to trade in MCX’s composite commodity index, MCX-COMDEX and

other indices that it has developed.

Increasing revenue from existing products

MCX intends to develop new revenue sources that are not transaction-driven.

We believe market data products and information offerings have the potential to

become a source of revenue for MCX, as is the case for various leading exchanges

in India and the rest of the world. MCX currently has such arrangements with

Bloomberg Finance L.P., NewsWire 18 Private Limited, IQN Data Solutions Private

Limited, Reuters India Private Limited, Interactive Data (Europe) Limited and

TickerPlant Limited. MCX aims to further develop its market data offerings by

integrating proprietary information generated by the exchange into new market

data products designed to meet the needs of a higher number of customers.

Scalable technology platform and business model

We believe the company’s technology platform and business model are highly

scalable and have the potential to generate better margins at greater volumes.

MCX plans to structure its business costs based on its historical and expected

growth. Consequently, the company has made significant investments in

developing fixed operating infrastructure, including technology systems, to support

anticipated growth and increased demand for its products. MCX’s current

technology infrastructure is sufficient to handle daily trading volumes of up to

10,000,000 trades a day. Increased trading activity on the exchange would result

in higher profitability. Further, the company intends to increase the use of data

generated from commodity futures contracts traded on the exchange to capitalize

on opportunities in market data products and information dissemination. We

believe the company’s overall business model is highly scalable and offers growth

potential with limited incremental costs.

February 22, 2012

5

MCX | IPO Note

Key concerns

Decline in volumes can lead to lower revenue

MCX’s business depends, in part, on its ability to maintain and increase

its members and turnover on the exchange and the resultant income from

transaction fees. Income from transaction fees depends on the average daily

turnover generated by members and is, therefore, correlated with the value of

commodity futures contracts. Any decline in the trading volume or the number of

members trading on the exchange could lead to a decline in the income from

transaction fees.

Decline in commodity prices can directly lead to lower revenue

Transaction fees charged by MCX is directly related to the value of commodity

futures contracts traded on the exchange; hence, income and results of operations

could be adversely affected by any decline in total value of commodity futures

contracts for these commodities traded on the exchange and their volumes. For the

nine months ended December

31,

2011, the value of contracts of four

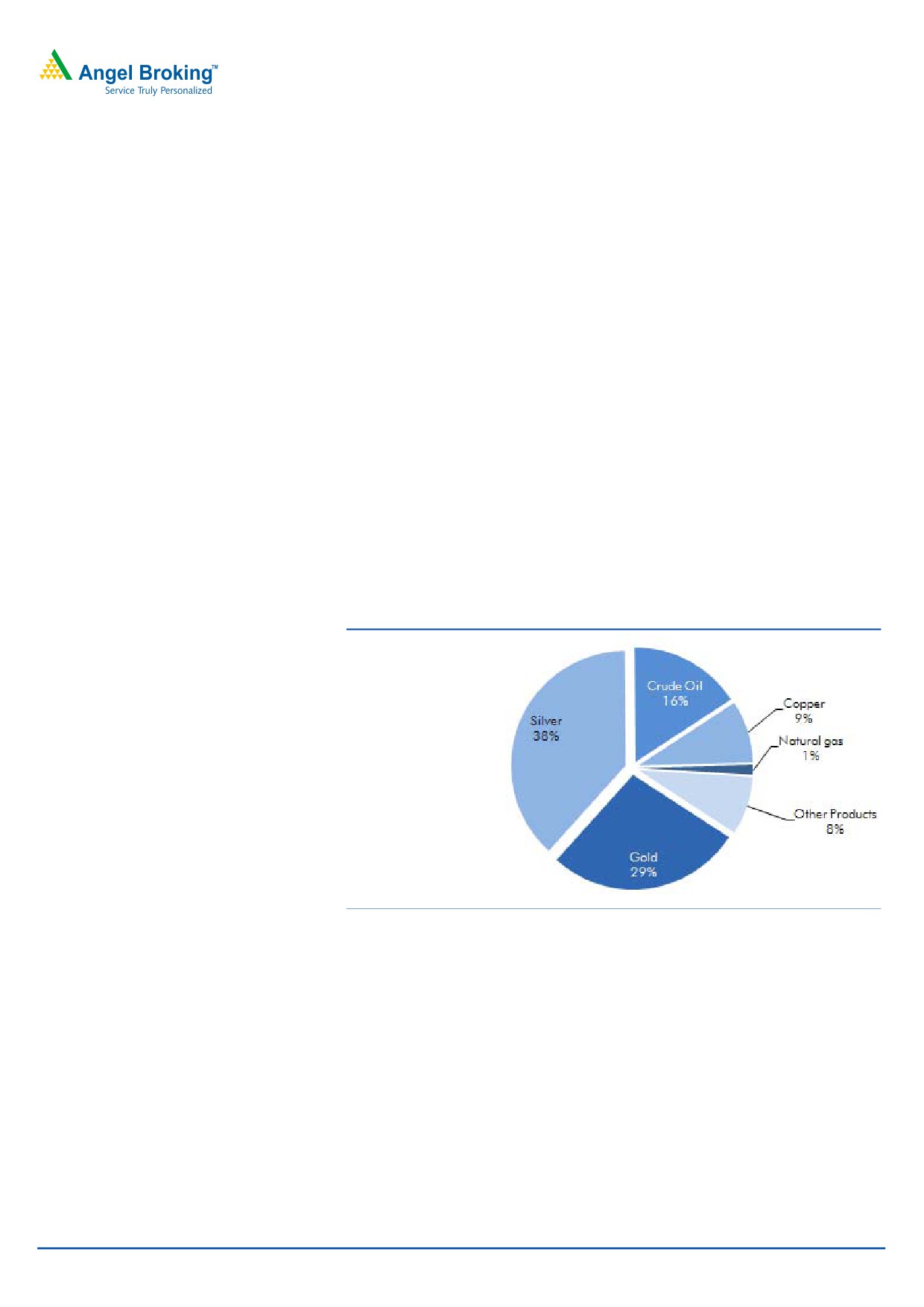

commodities traded on the exchange, namely silver, gold, crude oil and copper,

accounted for 38.2%, 27.5%, 15.9% and 8.8%, respectively, of the total value of

commodity futures contracts traded.

Exhibit 5: Revenue dependent on four major commodities (9MFY2012)

Source: Company, Angel Research; Note: Segment revenue of the total revenue

Competition may lead to margin compression

The derivatives exchange industry is generally highly competitive. MCX’s ability to

maintain and enhance its competitiveness will have a direct impact on its business,

financial condition and results of operations. There are currently 21 associations

recognized by Government of India that are authorized to organize and regulate

futures trading in various commodities. Of these, MCX faces competition mainly

from national commodity exchanges such as NCDEX, NMCE, ICEX and ACE,

which have a combined market share of only 12.4%.

February 22, 2012

6

MCX | IPO Note

Policy paralysis could hamper growth strategies

Under the current regulatory environment, foreign institutional investors, banks

and mutual funds cannot trade on commodity exchanges. Further, trading in

options in commodities futures is prohibited in India. If changes in policy are not

brought into force in a timely manner, or at all, MCX’s ability to introduce new

products on the exchange and implementation on new growth strategy could be

adversely affected.

Outlook and valuation

MCX currently has zero debt on its book, and major capex to fuel growth has

already been incurred by the company. Secondly, the company reported

investment and cash worth `1,324cr at the end of 9MFY2012, which works out to

`260/share. On an annualized basis, the stock will be trading at 15.1x and 18.1x

at the lower and upper band on FY2012E earnings, respectively, which we believe

is fair compared to global peers, which trade at 18x-19x TTM earnings; further,

the recent off-market deals value MCX’s Indian peers, NSE and BSE, at 22x-24x

9MFY2012 annualized earnings. We believe MCX being the only major

commodity exchange in India and the world’s fifth largest exchange can witness

strong growth in revenue and profitability going ahead, which makes its valuation

much more attractive than global peers. Hence, we recommend Subscribe to the

issue on account of its relatively fair valuations.

February 22, 2012

7

MCX | IPO Note

Industry Overview

The Global Commodity Futures Market

There are over 30 commodity futures and options exchanges worldwide that trade

commodities ranging from energy, metals, agriculture to livestock in many countries

including the United States, China, Japan, Malaysia and the United Kingdom.

(Source: Futures Industry Association (“FIA”), FI magazine September 2011 (“FIA

Report”)). According to the FIA Report, strong levels of growth were seen in the

trading volume of commodity futures and options, especially those relating to non-

precious metals, agricultural, energy and precious metals commodities.

Metals Futures

The metal futures contracts include a wide variety of metal commodities, which are

typically classified into precious and non-precious metals. Precious metals include

gold, silver and platinum. Non-precious metals include lead, aluminium, copper

and zinc. Gold is the most popular precious metal in metal futures contracts

trading. Trading in gold futures provides individual investors with an easy and

convenient alternative to the traditional means of investing in gold, such as bullion,

coins, and mining stocks.

Energy Futures

Energy futures contracts include energy commodities such as crude oil, natural

gas, heating oil, gasoline and coal. Over the past several years, the markets for

energy commodities trading have been characterised by rapid growth and high

liquidity, which we believe is due to several factors, including 1) increased market

acceptance of the value of commodity futures as risk management tools;2)

increased price fluctuation in crude oil, partially created by geopolitical conditions

in oil producing 3) increased price fluctuation in natural gas, partially created by

weather conditions and increased demand in emerging economies; 4) increased

awareness of the ability to obtain or hedge market exposure through the use of

futures and options contracts.

The Indian Commodities Market

India has over 7,000 regulated agricultural markets, or mandis, and the majority of the

nation‘s agricultural production is consumed domestically, according to the Agricultural

Marketing Information Network (Source: Agricultural Marketing Information Network

official website). There are currently 21 commodity exchanges recognised by FMC in

India offering trading in over 60 commodity futures with the approval of FMC. The

total value of commodities traded on commodity futures exchanges in India for the first

nine months ended December 31, 2011 was ` 137,228.55 billion.

Industry Growth in India

Commodity futures trading in India has grown since the Government of India

issued a notification on April 1, 2003 permitting futures trading in commodities.

The total value of commodities futures traded in India in the fiscal 2011 was `

119,489.42 billion, representing growth of approximately 90-fold from the value

of commodity futures contracts traded in the fiscal 2004, which was ` 1,293.67

billion. Commodity futures trading volumes have risen at a compound annual

growth rate of 90.9% between fiscal 2004 and fiscal 2011.

February 22, 2012

8

MCX | IPO Note

Income statement

Y/E March (` cr)

FY2009

FY2010

FY2011

9MFY2012

Income

Transaction fees

186.1

264.1

349.5

386.8

% chg

41.9

32.4

10.7

Membership Admission fees

10.5

7.0

3.5

4.1

% chg

(33.8)

(49.5)

17.7

Annual subscription fees

13.6

13.6

13.5

9.9

% chg

0.2

(1.1)

(26.7)

Terminal charges

2.2

2.7

2.4

1.5

% chg

21.5

(13.0)

(36.7)

Income from operations

212.4

287.4

368.9

402.3

% chg

35.3

28.4

9.1

Staff costs

25.4

21.8

26.4

20.1

% Net Sales

12.0

7.6

7.2

5.0

Administration and other operating exp.

110.6

124.1

150.7

121.7

% Net Sales

52.1

43.2

40.9

30.2

Total Expenditure

136.0

145.8

177.1

141.8

EBITDA

76.4

141.6

191.8

260.5

Margin

36.0

49.3

52.0

64.8

Depreciation/ Amortisation

20.0

24.7

24.7

20.4

EBIT

56.5

116.8

167.1

240.1

Interest

0.2

-

-

-

Other Income

153.4

206.3

78.7

72.2

Net profit before tax

209.7

323.1

245.8

312.2

Provision for tax

52.2

102.4

72.7

91.7

%PBT

24.9

31.7

29.6

29.4

Current tax

45.3

100.4

70.4

91.4

Prior period tax

-

-

0.2

(2.7)

Deferred tax

6.3

1.9

2.1

3.0

Wealth tax

-

-

-

-

Fringe benefit tax

0.6

-

-

-

Net profit after tax before share of profit of Asso.

157.4

220.7

173.1

220.5

Margin

74.1

76.8

46.9

54.8

Share of profit of Associate

0.0

0.3

0.3

0.1

Impact of prior period adjustments

1.4

(0.2)

2.9

(2.7)

Net profit

158.8

220.8

176.3

218.0

Margin

74.8

76.8

47.8

54.2

% chg

39.0

(20.2)

13.4

Exceptional Items

91.4

147.3

5.6

8.2

Adj. Net profit

67.5

73.6

170.6

209.8

% chg

9.0

132.0

22.9

Margin

31.8

25.6

46.3

52.1

Basic EPS

38.9

54.1

34.6

42.7

Source: Company, Angel Research; Note: Net profit adjusted

for sale

of property

which in

non- recurring in nature.

February 22, 2012

9

MCX | IPO Note

Balance sheet

Y/E March (` cr)

FY2009

FY2010

FY2011

9MFY2012

Gross block

259

268

292

310

Less : Accumulated depreciation/ amortisation

51

75

96

117

Net block

209

193

195

193

Add: Capital work-in-progress

-

-

-

-

Total Fixed Assets

209

193

195

193

Investments (B)(Refer Annexure X)

470

617

824

1,096

Current Assets, Loans and Advances

Sundry debtors

27

30

49

49

Cash and bank balances

406

270

331

229

Other Current Assets

9

8

11

10

Loans and advances

45

111

90

96

Total Current Assets

487

419

481

384

Liabilities and Provisions:

Current liabilities and provisions

663

521

639

583

Total Curretn Liabilities

663

521

639

583

Total Net Current Assets

(176)

(102)

(158)

(199)

Deferred tax liability (net) (E)

9

11

13

16

Total Assets

494

697

849

1,074

Share capital

41

41

51

51

Stock Option Outstanding Account

-

-

-

-

Reserves and Surplus

-

-

-

-

Securities Premium

226

227

217

217

Amount recoverable from MCX ESOP Trust

(22)

(17)

(11)

(4)

Settlement Guarantee Fund

2

2

2

2

General Reserves

39

61

78

78

Balance in Profit and Loss Account

208

383

512

730

Minority interest

-

-

-

-

Total Liabilities

494

697

849

1,074

February 22, 2012

10

MCX | IPO Note

Cash Flow Statement

FY2009 FY2010 FY2011 9MFY2012

Cash flow from operating activities

Net profit before tax, as restated

2,109

3,231

2,458

3,122

Depreciation/Amortization

200

247

247

204

Interest expense

2

-

-

-

Dividend from investments

(260)

(144)

(323)

(309)

Diminution in value of investments

72

6

-

3

Profit on sale of investments

(914)

(1,473)

(56)

(82)

Loss on sale of assets or assets scrapped

3

1

13

1

Advertisement expense

-

6

-

-

Interest income

(171)

(220)

(174)

(140)

Operating profit before working capital chg.

1,040

1,654

2,165

2,801

(Inc.)/decrease in trade and other receivables

(176)

(566)

(56)

119

(Decrease)/inc.in trade payables and prov.

2,245

(1,453)

1,136

(462)

Cash generated from / (used in) operations

3,109

(365)

3,245

2,458

Tax paid

(256)

(553)

(546)

(821)

Net cash generated from / operating activities

2,853

(919)

2,700

1,637

Cash flow from investing activities

Additions to fixed assets

(757)

(96)

(312)

(187)

Deletion / Adjustment to Fixed Assets

34

9

27

5

Purchase of investments

(110,907)(99,346) (109,269) 105,446.65)

Redemption/sale of investments

110,145

99,421

106,784

103,699

Dividend from investments

260

144

323

309

Interest received

97

234

139

157

Cash generated from /

(1,129)

366

(2,309)

1,464.55)

(used in) investing activities

Tax Paid

(242)

(489)

(18)

(9)

Net Cash generated from /

(1,371)

(123)

(2,326)

1,473.29)

investing activities

Cash flow from financing activities

Proceeds from:

Equity share capital

16

-

-

-

Securities premium

213

-

-

-

Minority Shareholders of Subsidiary Co.

-

-

-

-

Share issue expenses adjusted in

(63)

-

-

-

Securities Premium Account

Dividend paid (including tax thereon)

(47)

(239)

(238)

(296)

Interest paid

(2)

(0)

(0)

(0)

Net cash generated from /financing activities

116

(239)

(238)

(296)

Net cash (outflow) / inflow during the year

1,598

(1,280)

135

(132)

Net incr./ (decr.) in cash and cash equivalents

1,598

(1,280)

135

(132)

February 22, 2012

11

MCX | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

February 22, 2012

12

MCX | IPO Note

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai - 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Shailesh Kanani

Infrastructure

Bhavesh Chauhan

Metals & Mining

Sharan Lillaney

Mid-cap

V Srinivasan

Research Associate (Cement, Power)

Yaresh Kothari

Research Associate (Automobile)

Hemang Thaker

Research Associate (Capital Goods)

Nitin Arora

Research Associate (Infra, Real Estate)

Ankita Somani

Research Associate (IT, Telecom)

Varun Varma

Research Associate (Banking)

Saurabh Taparia

Research Associate (Cement, Power)

Technicals:

Shardul Kulkarni

Sr. Technical Analyst

Sameet Chavan

Technical Analyst

Sacchitanand Uttekar

Technical Analyst

Derivatives:

Siddarth Bhamre

Head - Derivatives

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Hiten Sampat

Sr. A.V.P- Institution sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Akshay Shah

Sr. Executive

Production Team:

Simran Kaur

Research Editor

Dilip Patel

Production

CSO & Registered Office: G-1, Ackruti Trade Centre, Rd. No. 7, MIDC, Andheri (E), Mumbai - 400 093.Tel.: (022) 3083 7700. Angel Broking Ltd: BSE Sebi Regn No: INB010996539 / PMS Regd Code: PM/INP000001546 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / NSE Sebi Regn Nos: Cash: INB231279838 /

NSE F&O: INF231279838/Currency: INE231279838 / MCX Currency Sebi Regn No: INE261279838 / Member ID: 10500 / Angel Commodities Broking Pvt. Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

February 22, 2012

13