Advisory Desk

March 26, 2012

Jyothy Laboratories

BUY

CMP

`169

Exploring new opportunities with Henkel’s acquisition

Target Price

`248

Jyothy Laboratories Ltd. (JLL), a company having three brands, is set to transform

Investment Period

12 Months

into a multi-brand company with the acquisition of an 83.7% stake in Henkel

India (Henkel), which owns seven brands. As a result of this synergy, we expect

JLL’s consolidated revenue to post a CAGR of 35% to `1,627cr and profit to post

Stock Info

Sector

FMCG

a CAGR of 36% to `166cr over FY2011-14E. We initiate coverage on JLL with a

Market Cap (` cr)

1,360

Buy recommendation and a target price of `248, based on SOTP valuation.

Beta

0.4

Investment rationale

52 Week High / Low

322 / 125

Avg. Daily Volume

27,818

Turnaround of Henkel - A bright future for JLL

Face Value (`)

1

JLL acquired an 83.7% stake in Henkel in August 2011. Management is now

BSE Sensex

17,362

Nifty

5,278

planning various turnaround strategies for Henkel, such as a new management,

Reuters Code

JYOI.BO

revamping of all its brands and shifting its manufacturing to JLL’s units. We expect

Bloomberg Code

SRTY IN

Henkel’s turnaround to result in profit of `19cr in FY2014E.

Jyothy Fabricare Services Ltd. (JFSL) - A long-term growth driver

Shareholding Pattern (%)

We expect JFSL, JLL’s subsidiary engaged in the laundry business, to post a

Promoters

65.2

102.4% CAGR in its revenue to `193cr over FY2012E-14E with an operating

MF / Banks / Indian Fls

17.5

margin of 26.1% in FY2014E. Further, JFSL is expected to reach its breakeven

FII / NRIs / OCBs

12.8

and start yielding profit from FY2013E, registering a profit of `30cr in FY2014E.

Indian Public / Others

4.6

Outlook and valuation

We expect JLL’s consolidated revenue to post a CAGR of 35% to `1,627cr and

Abs.(%)

3m 1yr

3yr

profit to post a CAGR of 36% to `166cr over FY2011-14E. We initiate coverage

Sensex

8.7

(4.4)

82.5

on JLL with a Buy rating view and an SOTP target price of `248.

JLL

7.5

(16.4)

185.2

SOTP valuation

Expected Mcap

Method

Remarks

`/share

(` cr)

JLL

P/E

15.0x FY2014E earnings

1,643

204

Henkel P/E

13.4x FY2014E earning, (for 83.7% stake)

210

26

JFSL

Stake sell

Discounted at 50%, for 75% stake

150

19

Total

248

Source: Company, Angel Research

Key financials (Consolidated)

Y/E March (` cr)

FY2010 FY2011 FY2012E#

FY2013E

FY2014E

Net Sales

640

667

955

1,359

1,627

% chg

66.1

4.3

43.2

42.3

19.7

Adj. Net Profit

74

66

85

112

166

% chg

93.9

(11.6)

28.9

32.3

48.1

OPM (%)

14.4

10.9

8.3

10.3

12.9

EPS (`)

10.3

8.2

10.5

13.9

20.6

P/E (x)

18.3

20.7

16.0

12.1

8.2

P/BV (x)

3.5

2.2

4.8

4.0

2.9

RoE (%)

20.3

12.9

18.5

35.8

41.3

RoCE (%)

0.2

0.1

0.1

0.1

0.2

Tejashwini Kumari

EV/Sales (x)

2.0

1.6

2.1

1.4

1.1

022-39357800 Ext: 6856

EV/EBITDA (x)

13.7

15.1

24.9

13.9

8.7

Source: Company, Angel Research, #FY2012E includes Henkel numbers post August 22, 2011

Please refer to important disclosures at the end of this report

1

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Table of contents

Investment arguments

3

Henkel’s acquisition to expand JLL’s portfolio

3

Combined distribution network to increase penetration level

3

Turnaround of Henkel - A bright future for JLL

3

JFSL - A long-term growth driver

5

Henkel’s acquisition - A perfect synergy

6

Quarterly performance

7

JLL’s performance

7

Henkel’s performance

8

Financials

9

JLL (Standalone)

9

Henkel

11

JFSL

12

Outlook and valuation

13

Peer comparison on various parameters

14

Risk factors

15

Company background

16

JLL

16

Henkel

17

JLL and Henkel - Combined product portfolio

17

Fabric care

17

Dishwashing

18

Mosquito repellent

19

Personal care

19

FMCG industry in India

21

March 26, 2012

2

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Investment arguments

Henkel’s acquisition to expand JLL’s portfolio

The acquisition of Henkel is a major corporate transformation for JLL, which is set

to be positioned as a multi-brand company, owning 10 brands in total - three

brands of its own and seven brands of Henkel. This would provide JLL with

immense opportunities to explore in terms of achieving revenue and cost synergy,

which will result in substantial revenue growth, leading to higher operating margin.

Exhibit 1: Combined product portfolio

Mosquito

Dishwashing

Fabric care

Personal care

repellent

products

JLL

Ujala

Maxo

Exo

Henkel

Henko

Pril

Fa

Mr. White

Neem

Chek

Margo

Source: Company, Angel Research

The expanded product portfolio would provide JLL with a balanced presence in the

rural and urban areas, as JLL’s ratio of rural and urban presence is 75:25 and

that of Henkel is 30:70. The combined portfolio would complement both the

companies, expanding their geographic reach. Moreover, the company will be

able to cater to different income segment customers, as now the products would

span out in all economic segments. Moreover, with brands such as Fa, Neem and

Margo, the company will make a strong entry in the personal care segment.

Combined distribution network to increase penetration level

JLL’s products are available in ~2.9mn outlets in India (as of March 31, 2011).

The company has sales staff of over 1,800, servicing to ~3,500 distributors who

have a reach to ~1mn outlets. JLL has a strong presence in rural areas (according

to AC Nielsen, more than 80% of FMCG categories are growing faster in rural

India as compared to urban India). JLL’s reach, however, is limited when it comes

to the modern retail channel. Henkel, on the other hand, has a strong presence in

the urban market (70% of sales), reaching out to ~0.8mn outlets. This combined

distribution network will complement both the companies, facilitating them to enjoy

a pan-India presence at a low cost. Further, the combined sales force would lead

to increased sales volume, as the companies would be able to sell the existing

products to new customers. We expect JLL to post a consolidated revenue of

`1,627cr in FY2014E, posting a CAGR of 35% over FY2011-14E.

Turnaround of Henkel - A bright future for JLL

The acquisition of Henkel is a strategic step by JLL, which will start yielding

substantial results in the coming years. To achieve this, JLL is following a

turnaround strategy for Henkel. JLL has already shifted its outsourcing

arrangement and the purchase-supply chain of Henkel to JLL’s manufacturing

facilities in Mumbai w.e.f. August 2011. Also, the production of Henkel’s products

(except Henko Detergent Powder) has been started at JLL’s strategically placed

manufacturing plants, which would result in lower manufacturing and logistics

cost. Further, for the distribution, JLL has assigned a special task force to identify

March 26, 2012

3

Advisory Desk

Jyothy Laboratories | Initiating Coverage

the weaker areas of Henkel’s distribution channel, i.e. in the northern and western

regions, and plans to support them w.e.f. April 1, 2012, which would help

Henkel’s products to enjoy a pan-India presence.

Post production, the next big task to be done is to revamp Henkel’s brands. JLL

plans to reposition Henkel’s brands through new packaging and ad campaigns.

For instance, new ad campaigns for Margo (from the coming summer season,

April-May) and Pril (from March end) are on the cards. Also, JLL has removed most

of the freebies with Henkel’s products and plans to reinvest the saved money in

advertisements.

Further, JLL plans for a 15% price hike across all product categories of Henkel, as

management feels that Henkel’s products are currently underpriced compared to

competitors. JLL plans to take this price hike in a phased manner (50% in

4QFY2012 and remaining in 4QFY2013).

JLL also plans to sell Henkel’s Karaikal plant and other unused assets and use the

proceeds to pay off the company’s debt. However, the plan is on hold for now as,

according to the terms of the acquisition, JLL is supposed to keep 75% of Henkel’s

assets intact.

Considering all these factors, we expect Henkel’s turnaround to take place by

2014E, leading to net profit of `19cr in FY2014E.

Exhibit 2: Coming together - JLL and Henkel

Exhibit 3: Expected brand size by FY2014E

Revenue: `1,633cr

Henkel

JLL

Profit: `159cr

India

10 brands, Pan India presence

Ujala-`414cr

Henko - `250cr

Revenue: `933cr

Revenue: `676cr

Exo - `219cr

Pril - `142cr

Profit: `103cr

Profit: `19cr

Maxo - `173cr

Margo - `122cr

7 brands

3 brands

Mr.White - `76cr

(Henko, Mr. White, Chek,

(Ujala, Maxo, Exo)

Pril, Fa, Margo, Neem)

Fa - `42cr

Rural : Urban presence

Rural : Urban presence

Chek - `27cr

75:25

30:70

Neem - `17cr

JLL (Standalone)

Henkel

Source: Company, Angel Research, Note: Financials are for FY2014E

Source: Company, Angel Research

March 26, 2012

4

Advisory Desk

Jyothy Laboratories | Initiating Coverage

JFSL - A long-term growth driver

JLL entered a new business of organized laundry in 2009 under the name Jyothy

Fabricare Services Ltd. (JFSL) - JLL’s 75% subsidiary. JFSL has raised `100cr

through private equity funding from IL&FS (IL&FS has already invested `50cr and

rest is to be invested post the setting up of Chennai and Hyderabad plants). As per

the deal value, the valuation of JFSL is estimated to be `400cr.

Currently, JFSL has 113 outlets across India. The company processes 21,000

pieces in the institutional category and 2,500 pieces in the retail category per day

(as of March 31, 2010). JFSL has a key client base of 116, which includes hotels,

airlines, service apartments and health clubs. The company started working with

southwestern railways in December 2009; and in FY2011, the company serviced

15 railways and earned revenue of `0.9cr. Recently, the company bagged a

BOOT (build, own, operate and transfer) contract for 10 years from Western

Railways, Ahmedabad (minimum guaranteed business worth `65cr) and a BOOT

contract for 15 years from Delhi Airport Metro Express (DAME).

Expanding geographically

As a part of the growth strategy, JFSL acquired 100% stake in Delhi-based

Diamond Fabricare (now called Wardrobe) for `16.5cr and 100% stake in

Mumbai-based Akash Cleaners for `19.4cr w.e.f. April 1, 2011.

Exhibit 4: JFSL’s laundry chain

Service Brand

Location

No. of retail outlets

Bangalore

10

Fabricspa

Mumbai

3

Chennai

2

Snoways

Bangalore

28

Wardrobe

Delhi

61

Expert dry cleaners

Bangalore

3

Akash dry cleaners

Mumbai

4

Dhulaai

Pune

2

Total

113

Source: Company, Angel Research

JFSL further plans to expand to Tier I and Tier II cities through the franchisee

channel, where company’s share will be 35% and rest will be of the franchisee.

Presently, the company’s 11% volume comes from retail customers and rest 89%

comes from institutional tie-ups; however, retail contributes to 55% of revenue and

institution contributes the remaining 45%. The company is expecting the volume

mix to change and the contribution from retail to increase considerably, which

would substantially increase its revenue. According to management’s forecast,

JFSL’s revenue is expected to reach `193cr, with operating margin of 26.1% and

profit of `30cr by FY2014E.

March 26, 2012

5

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Henkel’s acquisition - A perfect synergy

JLL acquired a controlling stake of 83.7% in Henkel in August 2011. Henkel has a

strong urban presence, which complements JLL’s strong rural presence and

provides both the companies a tremendous scope for widening their market

coverage.

Exhibit 5: Acquisition details

Seller

% of shares

Value (` cr)

Tamilnadu Petroproducts (TPL )

16.7

68

Henkel AG

51.0

143

Open market

4.0

19

Open offer

12.1

58

Other transaction cost

28

Preference capital

43

Loan repayment

425

Total

83.7

783

Source: Company, Angel Research

Major highlights of the deal

Acquired the global rights for Margo, Chek and Neem

Acquired the trademark for India, Bangladesh and Sri Lanka for Henko and

Mr. White

Acquired the licence for Pril and Fa @2% royalty on net sales for technology

support

Acquired the Karaikal plant (62-acre land) and land at Ambattur and Kolkata

Carried forward loss of `400cr

For the acquisition, JLL has taken NCDs, which were renewed into term loan from

Axis Bank, effective from January 27, 2012. The interest rate will be 11.25%

floating based on RBI’s rate. The company has the advantage of pre-closing the

loan with a 30-day notice to the bank. It is a combination of the term loan with 18

months of moratorium period and repayment over a period of three-and-a-half

years thereafter.

March 26, 2012

6

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Quarterly performance

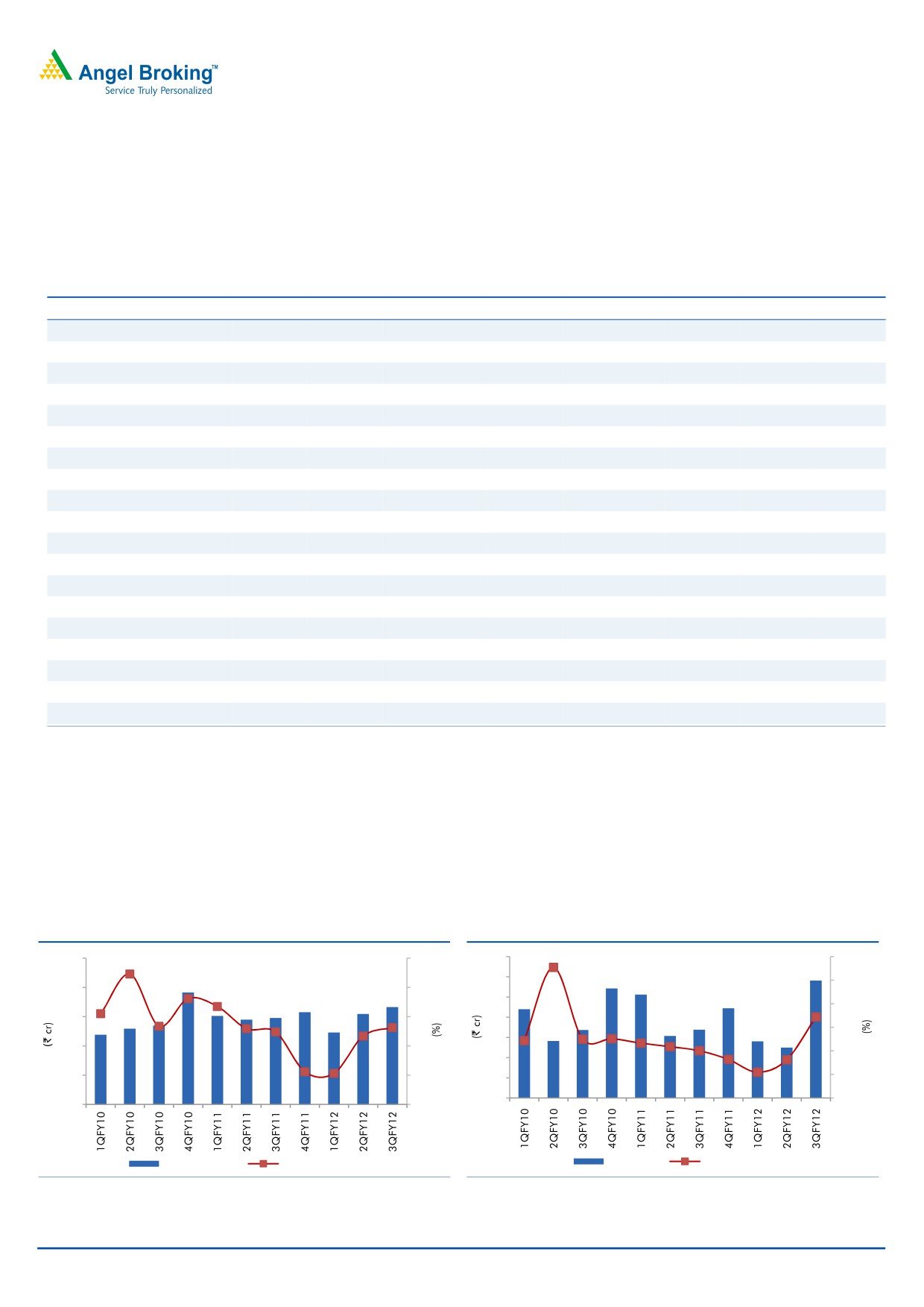

JLL’s performance

JLL reported 12.0% yoy growth in its revenue and 72.1% yoy growth in its profit to

`167cr and `29cr, respectively, in 3QFY2012.

Exhibit 6: JLL’s quarterly performance of JLL (Standalone)

Y/E March (` cr)

3QFY12 2QFY12

% chg. (qoq)

3QFY11

% chg. (yoy)

9MFY12 9MFY11

% chg

Total operating income

167

155

7.5

148.72

12.0

445

451

(1.3)

Net raw material

87

90

(3.4)

78.40

10.7

240.15

226

6.4

(% of Sales)

52.1

58.0

52.7

54.0

50.1

Employee cost

22

21

6.8

18.64

18.8

62.56

56

10.9

(% of Sales)

13.3

13.4

12.5

14.1

12.5

Other Expenses

29.38

37

(20.0)

33.90

(13.3)

95.14

98

(2.8)

(% of Sales)

17.6

23.7

22.8

21.4

21.7

Total expenditure

138

147

(6.1)

131

5.6

398

380

4.7

Operating profit

28

8

266.9

18

58.9

47

71

(34)

OPM (%)

17.0

5.0

1,199bp

12.0

500

10.5

15.7

(513)bp

Interest

2

2

15.1

0.06

3,716.7

6.04

0

6,611.1

Depreciation

6

4

73.3

3.04

104.6

13.61

9

50.4

Other income

14

15

(3.6)

6.82

109.5

41.21

10

296.6

PBT

34

17

100.9

22

58.3

68

72

(4.8)

(% of Sales)

20.4

10.9

14.5

15.4

15.9

Tax

5

4.45

11.2

4.60

7.6

12.80

14

(8.2)

(% of PBT)

14.5

26.3

21.4

18.7

19.4

Reported PAT

29

12

132.8

17

72.1

56

58

(3.9)

PATM (%)

17.5

8.1

11.4

12.5

12.8

Source: Company, Angel Research

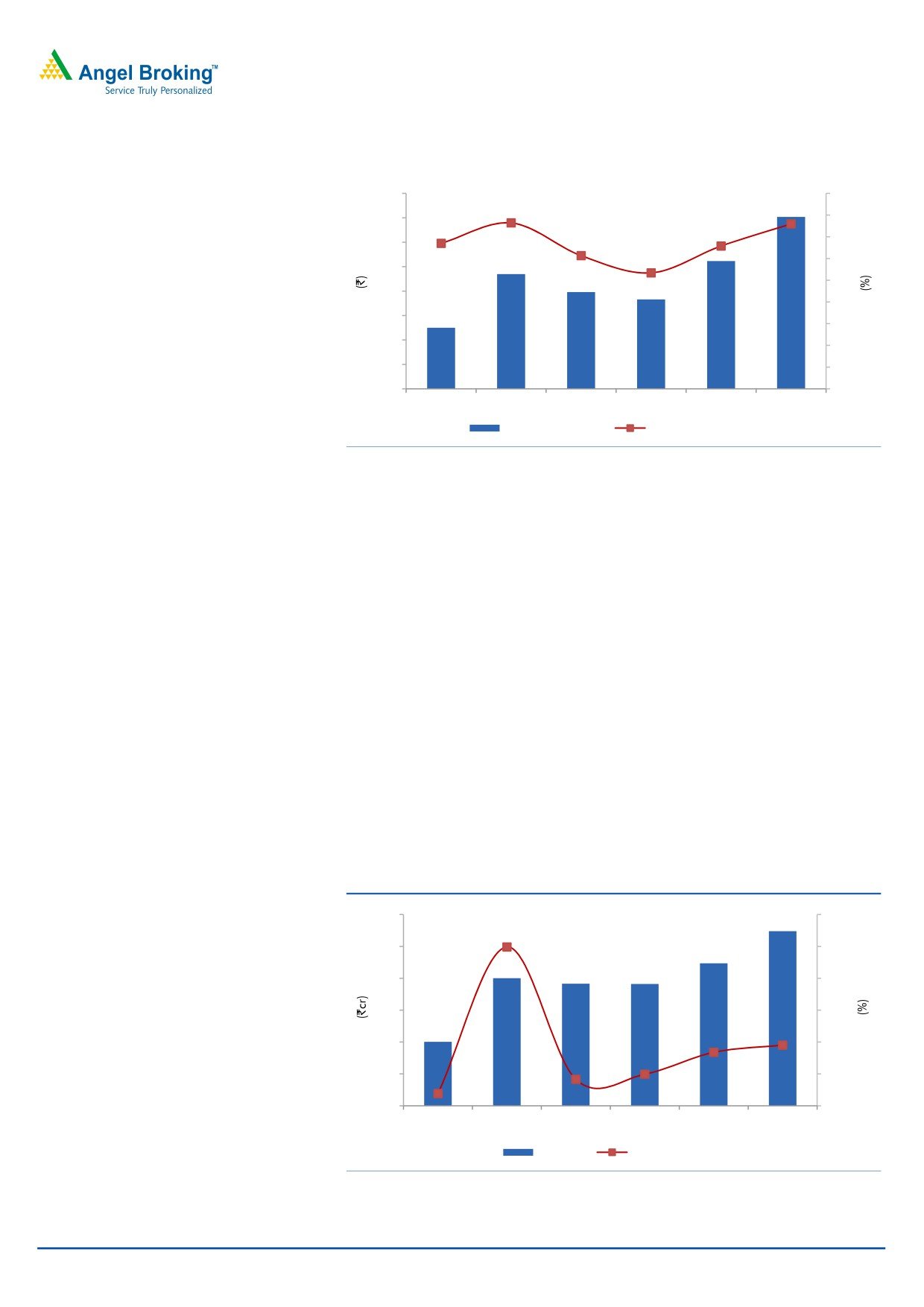

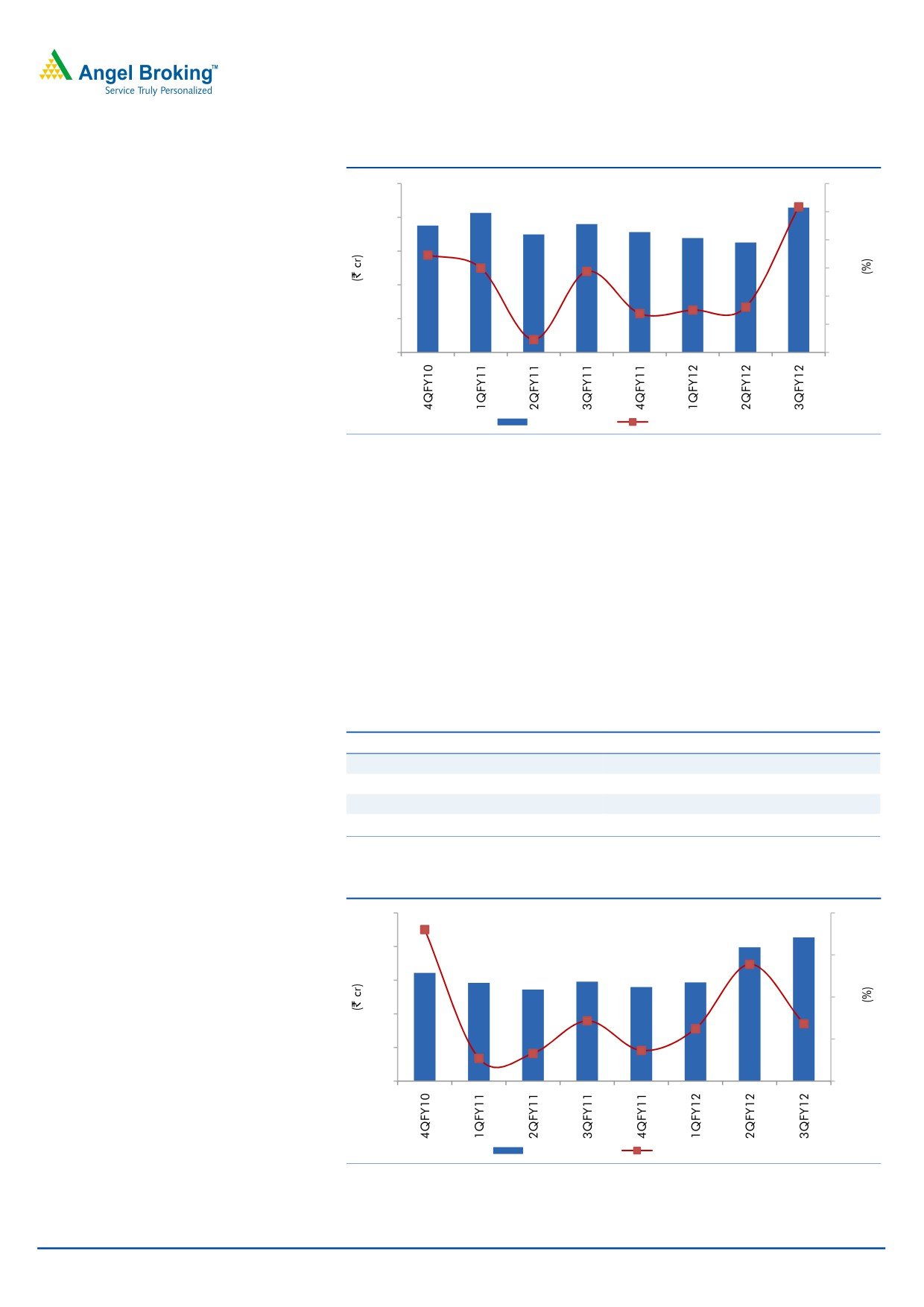

The company’s revenue growth can mainly be attributed to volume growth (10%

for Ujala and 38% for Exo). During the quarter, JLL’s other expenses declined

considerably because of lower advertisement spend. The company has taken a

price hike of 7% across all product portfolios to meet the increase in the

raw-material cost. However, the impact of the price hike was not seen in

3QFY2012 and is expected to be fully visible in the next quarter.

Exhibit 7: Revenue growth coming back on track

Exhibit 8: Earnings following the same trend

250

60

35

200

30

150

200

40

25

100

150

20

20

50

15

100

0

0

10

50

(20)

5

(50)

0

(100)

0

(40)

Revenue (LHS)

yoy growth (RHS)

PAT (LHS)

yoy growth (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

March 26, 2012

7

Advisory Desk

Jyothy Laboratories | Initiating Coverage

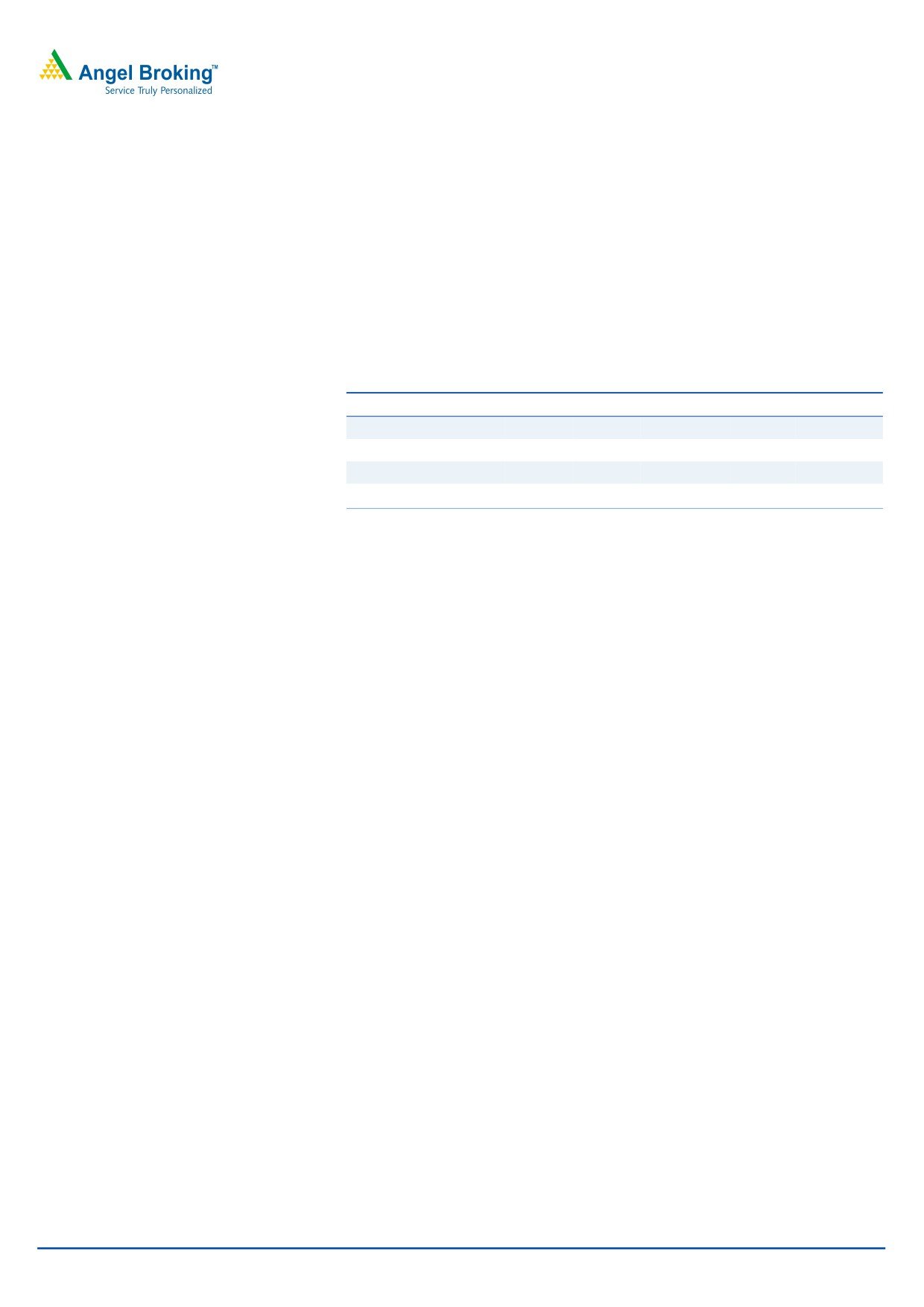

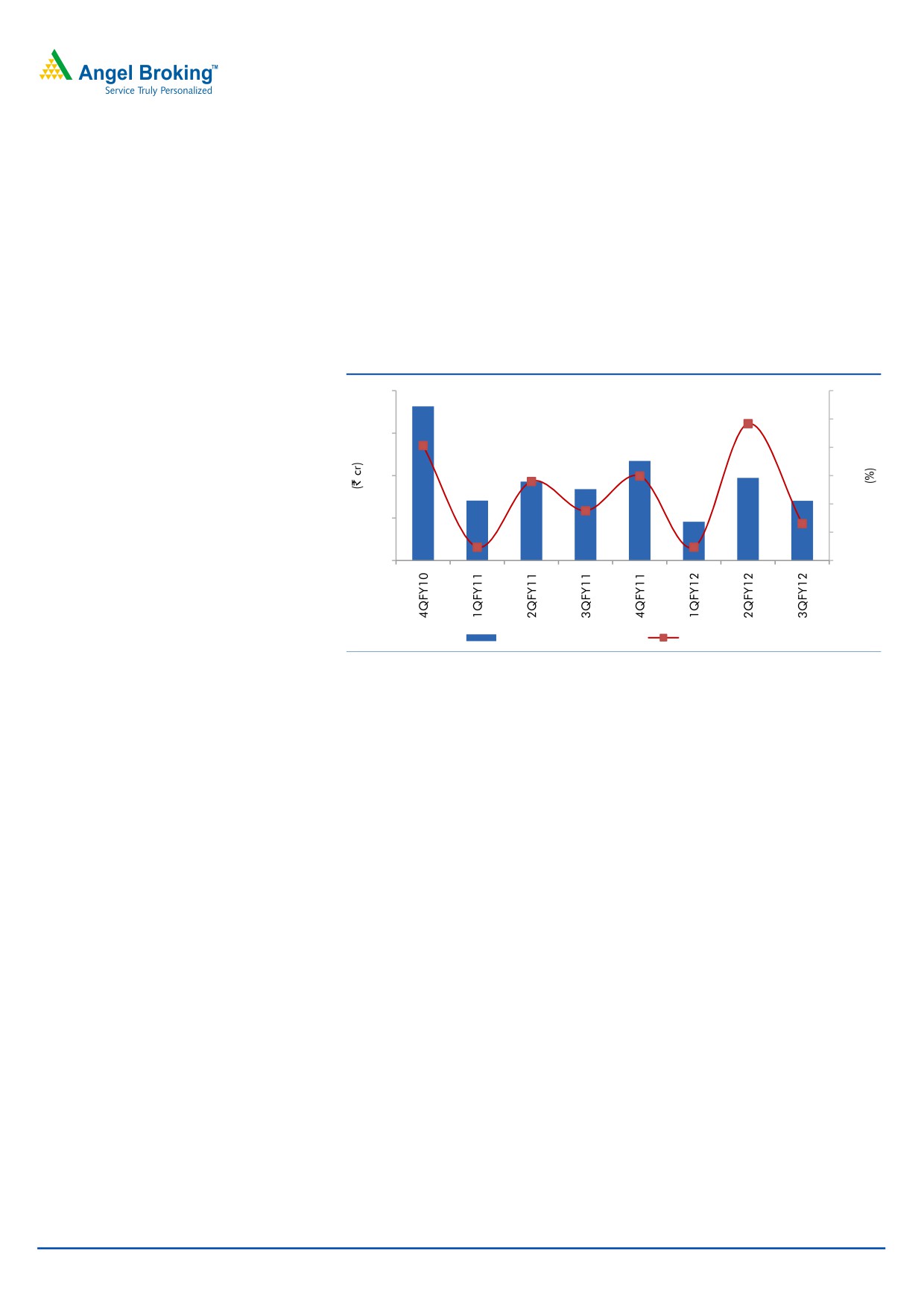

Henkel’s performance

Henkel’s performance dipped sharply in 4QCY2011, majorly because of labor

unrest at its Karaikal plant. The company reported a 28.4% qoq and 32.7% yoy

decline in its revenue. This was the sharpest decline in its top line after its

acquisition by JLL. Henkel lost `27cr and `7cr in its top line and EBITDA,

respectively, due to a 62-day shutdown at Karaikal plant (September 26 to

December 26), which manufactures Henko Stain Champion. Consequently, the

company’s EBITDA margin witnessed a dip of 834bp qoq and came in at 3.1%.

The company reported loss of `11cr for the quarter.

Exhibit 9: Henkel’s quarterly performance highlights

Y/E March (` cr)

4QCY11 3QCY11

% chg. (qoq) 4QFY10

% chg. (yoy)

Total operating income

77

107

(28.4)

114

(32.7)

Operating profit

2

12

(80.5)

(6)

(138.3)

OPM (%)

3.1

11.5

(834)

(5.4)

855

Adj. PAT

(11)

(1)

671.0

(11)

(1.1)

Source: Company, Angel Research

March 26, 2012

8

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Financials

JLL (Standalone) - Coming back on growth track

Top line to be driven by increased realization and volume growth

We expect JLL to report a revenue CAGR of 13% over FY2011-14E, from `646cr in

FY2011 to `926cr in FY2014E. Major drivers for the same will be the current 7%

increase in realization YTD and expected volume growth.

Assuming that rural GDP grows at 14.5% and 14.7% yoy (similar to the last

10-year CAGR) in 2013E and 2014E, respectively, we expect the company’s total

sales to post a CAGR of 12.9% over FY2011-14E, as most of the company’s sales

come from rural areas. We expect the home care segment to post a CAGR of 9.0%

to `276cr and the soaps and detergent segment to witness a CAGR of 15.0% to

`587cr over FY2011-14E. We expect volumes of manufactured products to post a

CAGR of 8.4% and 10.4% in the home care and soaps and detergent segments,

respectively, over FY2011-14E.

Exhibit 10: Sales growth

FY2009 (9M) FY2010 FY2011 FY2012E FY2013E FY2014E CAGR*

Rural GDP (at factor cost) growth (%)

16.0

16.0

17.9

14.7

14.5

14.7

14.6

Sales growth for JLL (Standalone) (%)

(5.4)

63.5

4.4

5.9

16.7

16.4

12.9

Home care (%)

5.4

54.2

(9.0)

2.6

11.7

12.9

9.0

Soaps and Detergents (%)

(12.2)

70.7

13.7

7.8

19.3

18.2

15.0

Source: Company, Angel Research, *CAGR over FY2011-14E

Exhibit 11: Volume growth and increase in realization to drive sales

1000

80

800

60

600

40

400

20

200

0

0

(20)

FY2009*

FY2010

FY2011

FY2012E FY2013E FY2014E

Revenue (LHS)

Revenue growth (RHS)

Source: Company, Angel Research, *FY2009 is for 9 months

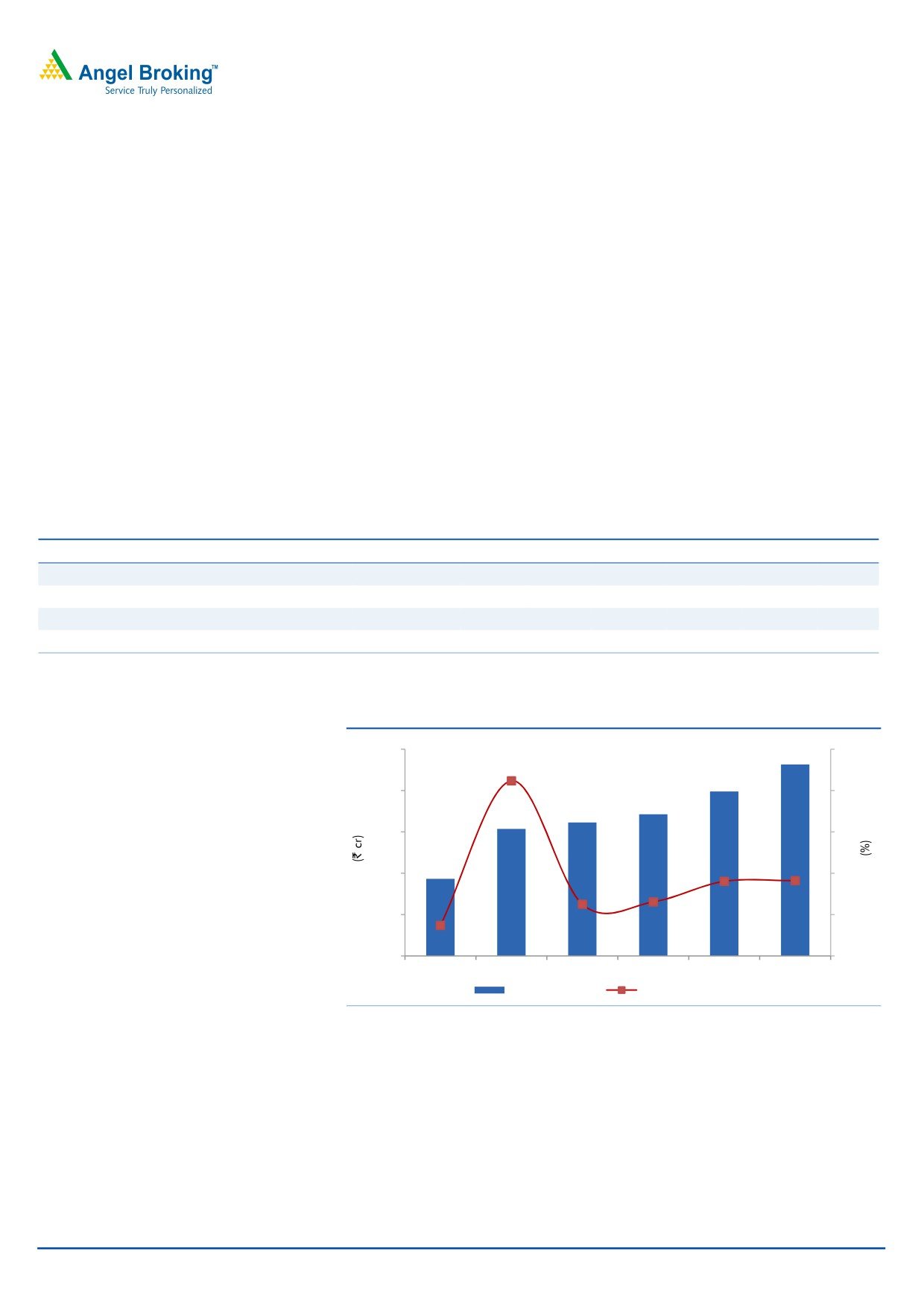

Stabilizing costs will lead to margin expansion

JLL witnessed margin pressure in FY2011 due to lower top-line growth and

increased expenditure. We further expect the company’s margin to contract by

159bp to 10.7% in FY2012E, as its employee cost and advertisement cost have

increased. However, we expect the company’s margin to improve thereafter by

124bp to 15.2% over FY2011-13E, as net raw-material cost as a percentage of

net sales is expected to decline to 44.3% and other costs are likely to stabilize.

March 26, 2012

9

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Exhibit 12: Decline in raw-material cost to improve operating margin…

160

18

140

16

14

120

12

100

10

80

8

60

6

40

4

20

2

0

0

FY2009*

FY2010

FY2011

FY2012E FY2013E FY2014E

EBITDA (LHS)

EBITDA Margin (RHS)

Source: Company, Angel Research, *FY2009 is for 9 months

Interest cost to be offset by other income

We expect JLL’s interest cost to rise to `50cr in FY2013E and `39cr in FY2014E, as

loans on books has increased. JLL has taken a term loan of `550cr from Axis Bank

at a rate of 11.25% w.e.f. January 27, 2012. However, JLL has given a loan of

`431cr from this amount to Henkel, for which it would receive interest income at a

rate of 11.5%. With this, there will be a rise in JLL’s other income as well, from

`28cr in FY2011 to `77cr in FY2014E. Further, we expect that JLL will be paying

off `135cr and `100cr debt in FY2013E and FY2014E respectively with the cash

generated through operations, leading to a decrease in its interest cost. Further,

the company would report higher tax from FY2014E at `49cr, as few of JLL’s fully

tax-exempted units will be losing their 100% tax benefit post FY2013E. However,

JLL plans to do the merger (JLL-Henkel) in FY2014E; if that happens, JLL will

further enjoy the tax shield due to the carried forward losses of Henkel.

On account of increasing revenue and expanding operating margin, we expect

JLL’s profit to post a CAGR of 13% over FY2011-14E, from `76cr in FY2011 to

`110cr in FY2014E.

Exhibit 13: … leading to growth on the earnings front

120

125

100

100

80

75

60

50

40

25

20

0

0

(25)

FY2009*

FY2010

FY2011

FY2012E FY2013E FY2014E

PAT (LHS)

PAT growth (RHS)

Source: Company, Angel Research, *FY2009 is for 9 months

March 26, 2012

10

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Henkel - Turnaround on cards

Henkel’s financials are set for a turnaround post the acquisition. We have assumed

that this year Henkel will be reporting financials for 15 months for FY2012E. A

hike of 15% in realization is expected across all segments of Henkel. Post the

acquisition, Henkel’s business is bound to be revamped, given the repositioning of

brands, price hike, change in distribution channel and reduction in total

expenditure as a percentage of net sales.

We expect the company’s revenue to post a CAGR of 8% by FY2014E (over

CY2010-FY2014E), majorly on the back of the expected 15% price hike supported

by volume growth, as JLL is set to rebrand and reposition Henkel’s brands.

Accordingly, we expect the company’s operating margin to expand by 1,544bp to

11.3% in FY2014E. Henkel’s interest cost is as high as `61cr on the loan of `531cr

at a rate of 11.5%. However, being a loss-making company, Henkel enjoys tax

shield. We expect the company to turnaround and register a profit of `19cr in

FY2014E.

Exhibit 14: Key financials of Henkel

Y/E March (` cr)

CY2009 CY2010 FY2012E* FY2013E FY2014E

Net sales

592

534

552

541

676

% chg

9.7

(9.9)

3.4

(2.0)

25.0

Adj. net profit

(32)

(55)

(39)

(22)

19

% chg

(50.1)

69.1

(28.7)

43.3

184.7

OPM (%)

(6.0)

(4.2)

3.1

7.7

11.3

EPS (`)

(2.8)

(4.7)

(3.3)

(1.9)

1.6

P/E (x)

(9.1)

(5.4)

(7.5)

(13.3)

15.7

P/BV (x)

(2.7)

(1.8)

(1.7)

(1.5)

(1.6)

RoE (%)

40.5

40.3

23.1

11.8

9.9

RoCE (%)

(0.2)

(0.1)

0.0

0.1

0.2

EV/Sales (x)

1.1

1.4

1.3

1.4

1.1

EV/EBITDA (x)

(19.0)

(33.5)

42.9

18.0

9.5

Source: Company, Angel Research, *FY2012 is for 15 months

March 26, 2012

11

Advisory Desk

Jyothy Laboratories | Initiating Coverage

JFSL - Breakeven in FY2013E

As per management, JFSL is expected to post a revenue CAGR of 102.4% to

`193cr over FY2012E-14E. In addition, the company’s operating margin is

expected to improve substantially by 2,048bp to 26.1% in FY2014E. Further, JFSL

is expected to reach its breakeven and start yielding profit from FY2013E,

registering profit of `30cr in FY2014E.

Exhibit 15: JFSL's growth projection

FY2012E

FY2013E

FY2014E

Service income

47

100

193

Washing expense

20

38

70

% of service income

41.6

38.1

36.3

Manpower cost

11

20

29

% of service income

23.4

19.8

15.2

Rent

5

12

16

% of service income

11.6

11.8

8.1

Other overheads

8

16

28

% of service income

17.9

16.3

14.4

Total Expenditure

44

86

142

% of service income

94.4

86.1

73.9

EBITDA

2.6

13.9

50.2

EBITDA margin

5.6

13.9

26.1

Interest and Depreciation

5

8

10

% of service income

10.3

7.6

5.2

PBT

(2)

6

40

Tax

-

-

11

% of PBT

-

-

26.7

PAT

(2)

6

30

Source: Company's corporate presentation, Angel Research

March 26, 2012

12

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Outlook and valuation

The synergy of JLL and Henkel is expected to result in substantial growth in revenue

and operating margin. On a consolidated basis, we expect JLL’s revenue to post a

35% CAGR over FY2011-14E to `1,627cr. With stabilizing costs after business

consolidation, JLL’s operating margin is likely to improve by 119bp to 12.9% and

its consolidated profit is expected to post a 36% CAGR to `166cr.

We have valued JLL (consolidated) on SOTP basis. JLL (standalone) is valued at a

target PE of 15x for FY2014E at a price of `204/share; the newly acquired

subsidiary, Henkel, has been valued at PE of 13.4x for FY2014E at a price of

`26/share for 83.7% stake; and JSFL has been valued by stake sell method,

discounted at 50% for 75% stake at a price of `19/share. Currently, at `169, JLL

(standalone) is trading at PE of 12.4x for FY2014E, at a discount of 31.1% to its

three-year median.

We initiate coverage on JLL with a Buy recommendation and a target price of

`248, based on SOTP valuation.

Exhibit 16: SOTP valuation of JLL

JLL (Standalone)

Mcap (in ` cr)

1,360

Net worth (2014E) (` cr)

788

PAT (2014E) (` cr)

110

Current PE (x)

12.4

Target PE (x)

15.0

Expected value (` cr)

1,643

Outstanding shares (in cr)

8.1

Expected price/ share (`) (A)

204

Henkel (Consolidated)

Mcap (in ` cr)

293

Net worth (2014E) (` cr)

(180)

PAT (2014E) (` cr)

19

Current PE (x)

15.7

Target PE (x)

13.4

Expected value (in ` cr) (for 83.7% stake)

210

Outstanding shares (cr)

8.1

Expected price/ share (`) (B)

26

JSFL

Total EV (in ` cr) (including debt of `60cr)

400

EV (Discounting at 50%) (in `cr)

200

Value for JLL's 75% stake in JFSL (in `cr)

150

Outstanding shares (in cr)

8.1

Expected price/ share (`) (C)

19

Target price (`) (A+B+C)

248

Source: Company, Angel Research

March 26, 2012

13

Advisory Desk

Jyothy Laboratories | Initiating Coverage

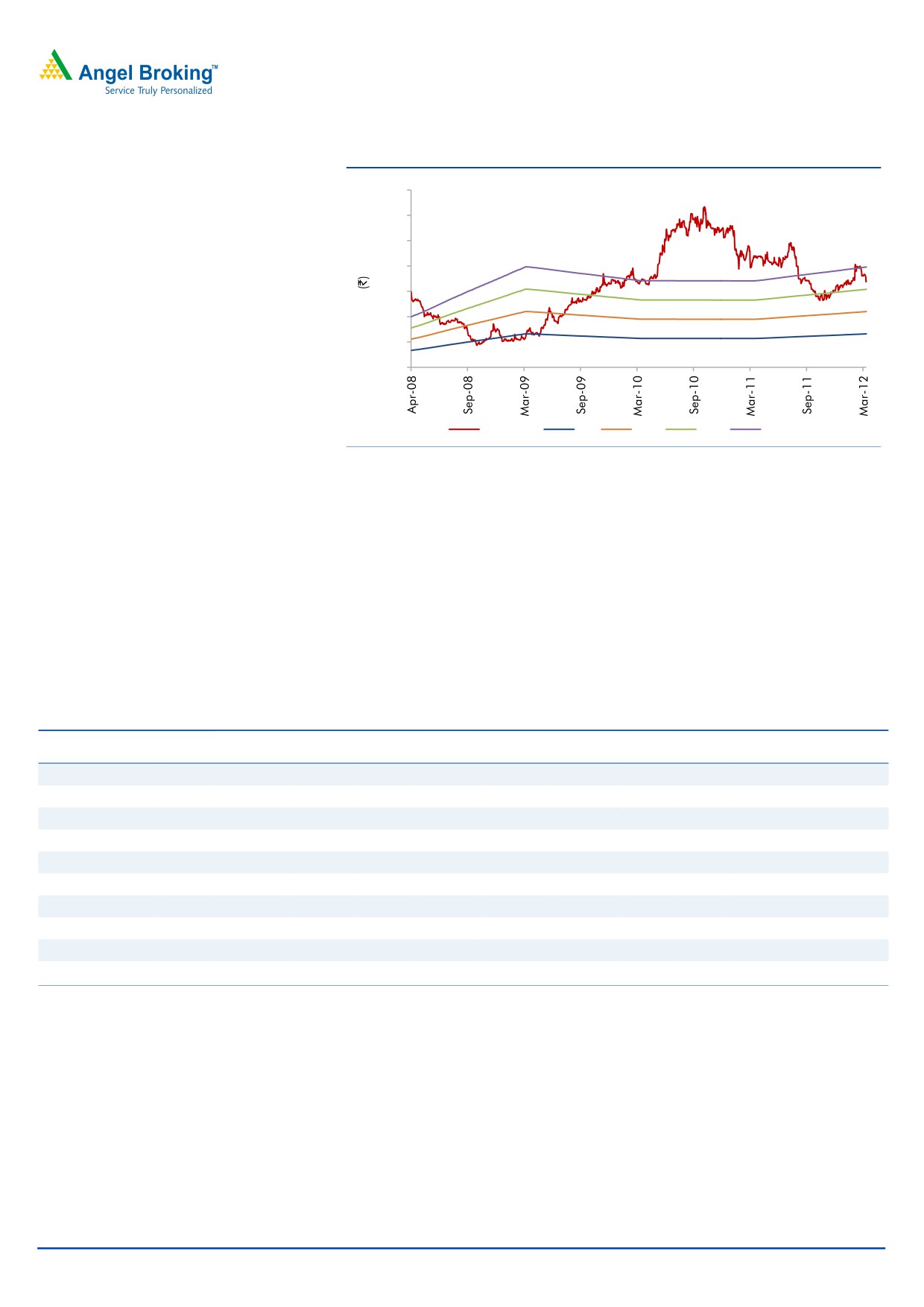

Exhibit 17: JLL's one-year forward PE band

350

300

250

200

150

100

50

0

Price (`)

6x

10x

14x

18x

Source: Company, Angel Research

Peer comparison on various parameters

On FY2013E basis, JLL (consolidated) is trading at PE of 12.1x, which looks

attractive vis-à-vis its peers. The company’s EPS stands at `13.9 for FY2013E,

which is higher than its peers - Marico and Dabur. Further, JLL’s ROE stands at

35.8%, which is higher than Marico and Emami; and we expect JLL’s ROE to

increase to 41.3% in FY2014E. The company is currently going through a

transition phase and is set for a turnaround in the coming years on a consolidated

basis.

Exhibit 18: Attractively valued as compared to peers

Mcap

Sales

OPM

PAT

EPS

RoE

P/E

P/BV

EV/Sales

EV/

Company

Year end

(` cr)

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

EBITDA (x)

JLL - Standalone

FY2012E

1360

685

10.7

76

9.5

11.5

17.8

2.0

2.1

19.4

FY2013E

1360

796

13.2

89

11.1

12.7

15.2

1.9

1.7

13.1

JLL - Consolidated FY2012E

1360

955

8.3

85

10.5

18.5

16.0

4.8

2.1

24.9

FY2013E

1360

1359

10.3

112

13.9

35.8

12.1

4.0

1.4

13.9

Emami*

FY2012E

5992

1500

19.5

264

17.5

34.6

22.7

7.1

4.0

20.6

FY2013E

5992

1778

19.9

315

20.8

34.4

19.0

5.8

3.4

17.1

Marico

FY2013E

10131

3779

12.7

305

5.0

25.6

33.2

8.5

2.7

21.4

FY2012E

10131

4341

13.3

390

6.3

25.9

26.0

6.7

2.3

17.2

Dabur

FY2013E

18484

5179

17.8

666

3.8

39.2

27.8

10.9

3.6

20.3

FY2012E

18484

5919

18.4

795

4.6

42.4

23.2

9.9

3.1

16.6

Source: Company, Angel Research, * Bloomberg estimates

March 26, 2012

14

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Risk factors

Business integration

Going forward, the major concern for JLL is the risk associated with the integration

of Henkel. JLL and Henkel are in the process of a consolidation - the companies

are combining their manufacturing and distribution processes and JLL is set to

revive most of Henkel’s brands with proper positioning. If things go haywire, JLL’s

growth could face a serious risk.

Raw-material cost

The company’s key raw materials include HDPE, acid slurry, synthetic organic dye,

Koylene, LABSA (sulphuric acid), Sumi 1 and Transfluthrin (insecticide) and brown

sawdust.

HDPE, which constitutes the largest raw-material expenditure, is a derivative of

crude oil and is exposed to great price fluctuation. Currently, the company has

only two suppliers for HDPE. For Transfluthrin, there is only one supplier in India;

however, one Chinese player is expected to enter the market soon, providing the

raw material at a much lower price. Until then, the company is completely

dependent on the limited supplier in the market, which restricts the company’s

bargaining power. Further, JLL does not have any long-term supply contracts with

its suppliers. Hence, any further hike in raw-material cost or any disruption in

raw-material inflow may pose a risk to the company’s business.

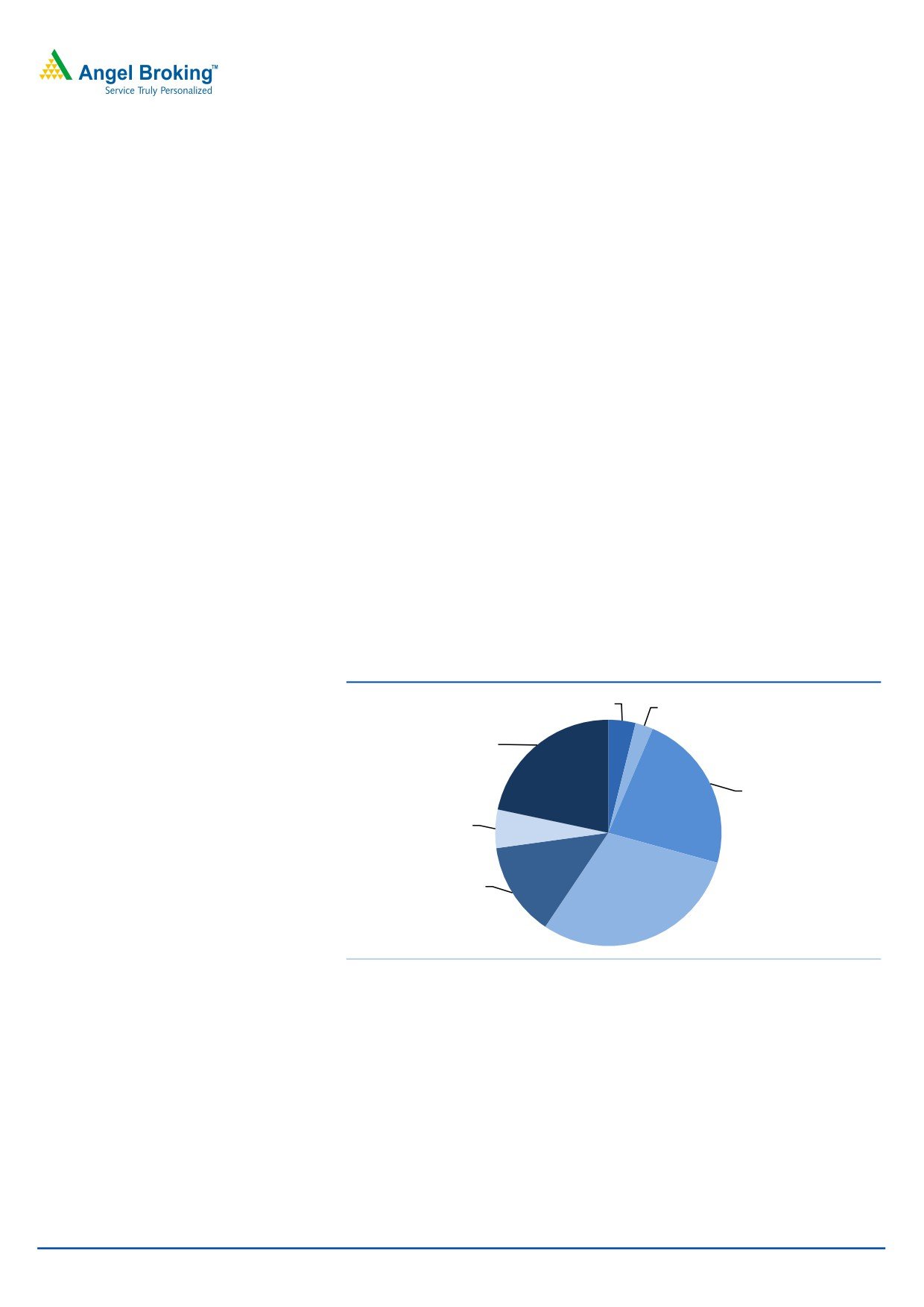

Exhibit 19: Raw material break-up

Synthetic Dye

Soap Noodles

4%

3%

Packaging

material

22%

Dyes &

Chemicals

23%

Others

5%

Plastic

Fatty Oils,

13%

Powder and

Perfumes

30%

Source: Company, Angel Research

March 26, 2012

15

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Company background

JLL

JLL is an FMGC company present in the fabric care (Ujala), household insecticide

(Maxo), surface cleaning (Exo), personal care (Jeeva) and air care segments

(Maya). The company was started in 1983 as a single-brand company, with Ujala

Fabric Whitener as its flagship product. However, over time, JLL has grown by

diversifying itself, both in terms of its product portfolio and market size across

India.

JLL’s manufacturing units are strategically present across India to maintain a lower

logistics cost. The company has 28 manufacturing facilities in 16 locations across

India, of which some are tax-efficient units. JLL’s products are available in ~2.9mn

outlets in India (as of March 31, 2011). The company has sales staff of over

1,800, servicing ~3,500 distributors.

JLL also operates in the laundry business under the name of JFSL, which has

become India’s largest laundry chain with 113 retail outlets in Bangalore, Delhi,

Mumbai, Pune and Chennai. Further, JFSL’s Hyderabad outlet is expected to be

operational by March 31, 2012.

Exhibit 20: Product portfolio

Market Share

Brand

Positioning

Brand Extension

Outlook

for Dec'11 (%)

Value Volume

Ujala

Liquid fabric whitener that does

73.6

60.1 • Washing powder launched in 2003 in

Focused in Southern India only

(Launched in

not leave clothes blue or patchy

Kerala and in other southern regions in

1983)

2009

•

Ujala Stiff and Shine launched in 2005

in Kerala and nationwide in 2008

Maxo

Mosquito repellant offering

19.8

22 • Liquids/Aerosols

Advanced version of the liquid

(Launched in

’corner-to-corner‘ protection

•

DEPA products for outdoor application

to be launched in 4QFY2012

2000)

Exo

Anti-bacterial dish wash

26.3

23.8 • Dishwashing liquid - Exo Liquid /Exo Gel National rollout

(Launched in

•

Dishwashing scrubber - Exo Safai

2000)

Source: Company, Angel Research

March 26, 2012

16

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Henkel

Headquartered at Chennai, Henkel was established in 1987 as a subsidiary of

Henkel AG & Co. KGaA, Germany. The company is engaged in the business of

laundry, home care, cosmetics, toiletries and hair care. The company comprises

brands such as Pril, Henko, Fa, Mr. White, Chek, Margo and Neem. In August

2011, JLL acquired an 83.7% stake in Henkel.

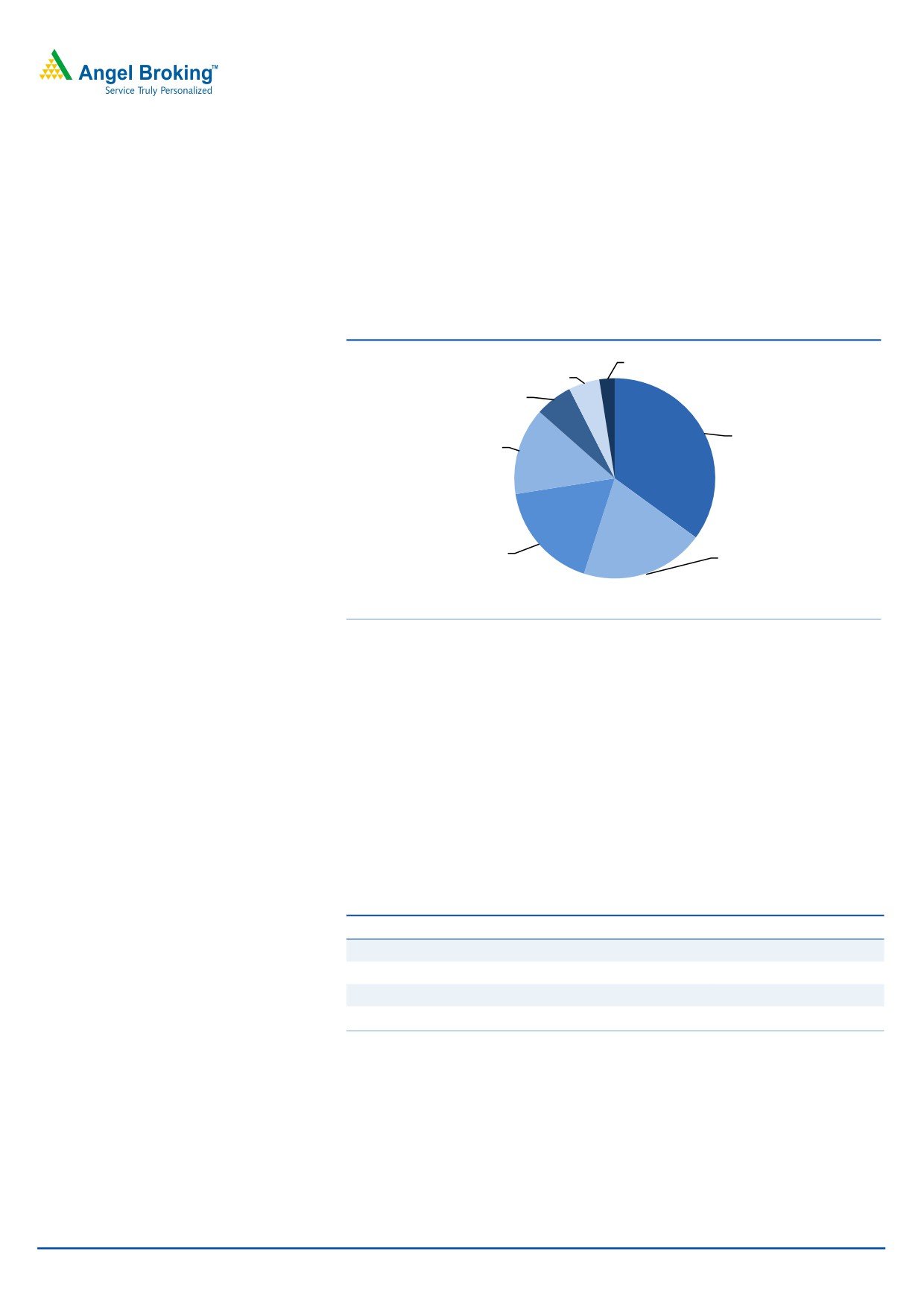

Exhibit 21: Revenue contribution - Product wise

Chek

Neem

5%

3%

Fa

6%

Henko Champion

Mr. White

35%

14%

Pril

Margo

17%

20%

Source: Company

JLL and Henkel - Combined product portfolio

Fabric care

Under the fabric care segment, JLL has Ujala Supreme, Ujala washing powder, Stiff

and Shine and Ujala Techno Bright. This segment is the core segment for JLL and

contributed 54% to its FY2011 revenue. JLL’s product range in the segment mainly

caters to the mass segment, majorly in South India. JLL plans to keep the sales of

Ujala detergent limited to southern India only and rollout and reposition Henkel

detergent in other parts of India to avoid any cannibalization. With this, the

company will be able to cater to other economic segments as well.

Exhibit 22: Combined portfolio of the fabric care segment

Segment

JLL

Henkel

Value

-

Check

Mid-premium

Ujala, Ujala Whitener

Mr. White. Mr. White bleach

Premium

Technobright

Henko Champion

Niche

Technobright Matic, Ujala Stiff & Shine

Henko Matic

Source: Company, Angel Research

March 26, 2012

17

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Exhibit 23: JLL’s core segment witnessing robust growth

100

40

30

80

20

60

10

40

0

20

(10)

0

(20)

Fabric care

qoq Growth (%)

Source: Company, Angel Research

Dishwashing

Under this segment, JLL has Exo dish wash bar and liquid targeting rural and

urban customers, respectively. The brand is positioned as an ‘anti-bacterial dish

wash’, as it contains Cyclozan, which works against bacterial contamination of

utensils. The products are doing well in southern India; however, it has been

recently launched in Maharashtra, Delhi, Punjab and West Bengal. National

rollout is the next step.

With the addition of Henkel’s portfolio, the segment will now be focussing on

urban Tier I and Tier II cities.

Exhibit 24: Combined portfolio for the dishwashing segment

Segment

JLL

Henkel

Value

-

-

Mid-premium

Exo bar

Pril Bar

Premium

Exo Liquid

Pril Liquid

Niche

Exo scrubber

-

Source: Company, Angel Research

Exhibit 25: JLL’s dishwashing segment witnessing decent growth

50

60

40

40

30

20

20

0

10

0

(20)

Dishwashing

qoq Growth (%)

Source: Company, Angel Research

March 26, 2012

18

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Mosquito repellent

This mosquito repellent segment consists of brands such as Maxo coil, Maxo

vaporiser liquid and Maxo aerosol. Maxo is facing strong pricing pressure, as it is

present in the increasingly competitive market segment. However, the company

had chosen to maintain its profit margin even at the cost of losing its top line. The

company withdrew the trade schemes and promotions i.e., trade discount by ~7%,

which affected the demand negatively, leading to decline in its revenue as well as

market share.

Exhibit 26: Maxo's revenue witnessing a decline

80

160

120

60

80

40

40

0

20

(40)

0

(80)

Mosquito repellent

qoq Growth (%)

Source: Company, Angel Research

JLL launched Maxo Military and Maxo safe & soft in February 2011, which uses

DEPA (Di-ethyl Phenyl Acetamide) and expects these products to boost its revenue

and the profit. The launch was in-line with the agreement with Department of

Research and Development Organisation (DRDO), which gives JLL the exclusive

right to develop DEPA multi-insect repellent.

Further, the segment has lost 2% of its market share in the past one year (on TTM

basis). Now, in order to revive the segment and maintain its market share, the

company has planned for new ad campaigns, which are expected to start soon.

Personal care

The personal care segment was an unexplored segment for JLL as it has only one

brand (Jeeva) under it, which contributes the least to the company’s sales.

However, with Henkel’s products, Fa, Neem and Margo, JLL has an opportunity to

explore this segment as well.

March 26, 2012

19

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Exhibit 27: Combined portfolio for the personal care segment

Segment

JLL

Henkel

Value

-

-

Mid-premium

Jeeva

Fa deo, Fa soap

Premium

Margo Neem

Niche

-

-

Source: Company, Angel Research

JLL has planned a new campaign for Margo to revive and rebrand the product,

which will help in repositioning the brand in the consumer’s mind. The campaign

is expected to be launched in the summer season (April-May 2012).

March 26, 2012

20

Advisory Desk

Jyothy Laboratories | Initiating Coverage

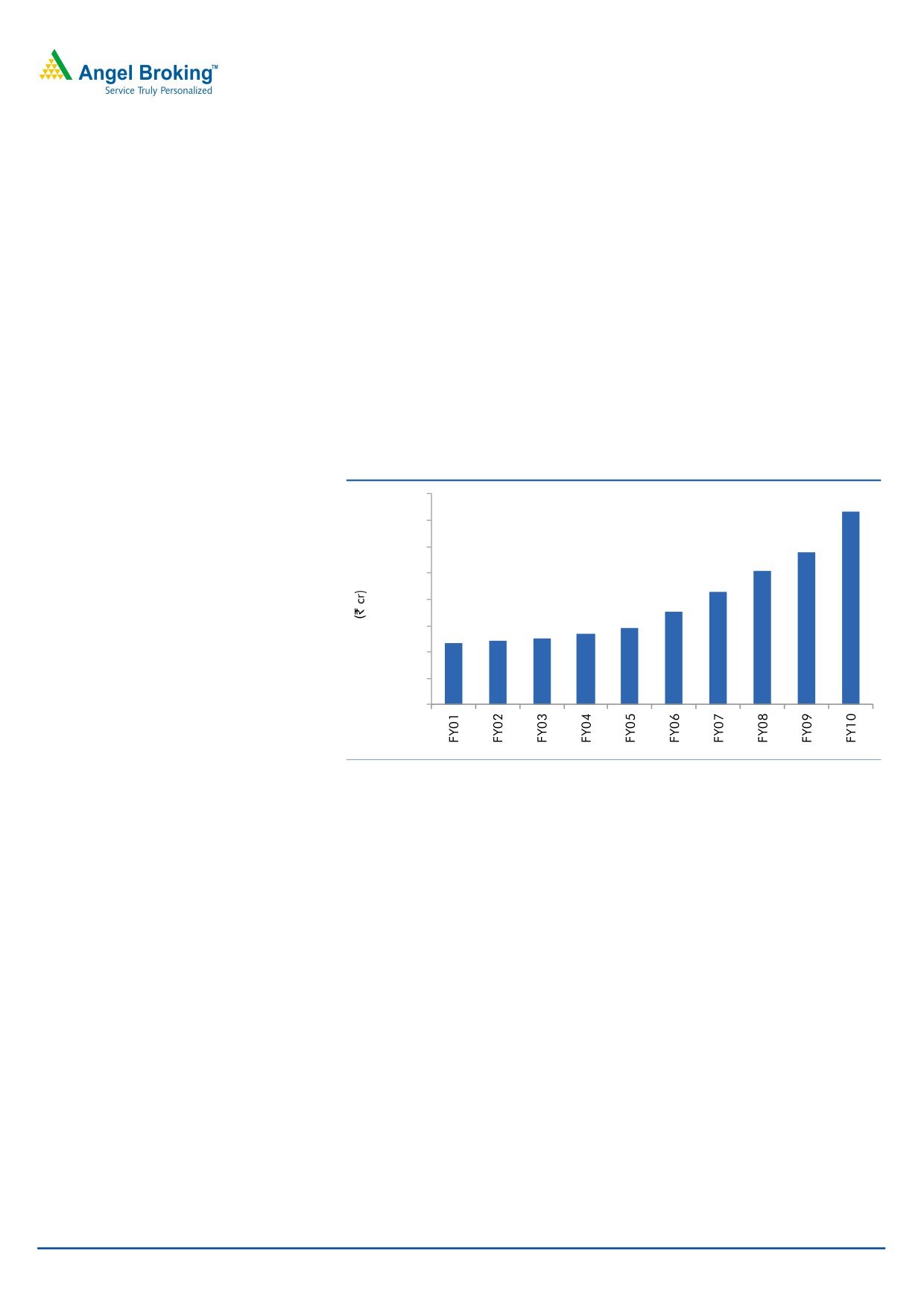

FMCG industry in India

The Indian FMCG industry has been on a fast growth track, majorly driven by

rising incomes driving domestic consumption, changing consumer behavior,

improved distribution channel and increasing marketing spends by players.

In the past five years, the annual growth rate of the sector has accelerated to 17%

compared to 11% in the last decade. As per AC Nielsen report on the FMCG

industry, March 2011, the FMCG market’s size stood at `1,46,300cr. According to

a report by Booz & Company, the industry is expected to report a 12-17% CAGR

and become a `4,00,000cr-6,20,000cr industry by 2020. Further, the industry is

set for a paradigm shift with increasing income levels (both urban and rural India)

and changing consumer behavior. However, the industry is also facing lot of

pressure on account of high inflation and rising cost of production.

Exhibit 28: FMCG market size - Growth over the past 10 years

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0

Source: Industry, Angel Research

March 26, 2012

21

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Profit and Loss (Standalone)

Y/E March (` cr)

FY2009*

FY2010

FY2011

FY2012E

FY2013E

FY2014E

Gross sales

384

626

665

703

820

955

Less: Excise duty

11

12

20

18

25

29

Net Sales

373

615

646

685

796

926

Other operating income

-

-

-

-

-

-

Total operating income

373

615

646

685

796

926

% chg

(5.2)

64.7

5.0

6.2

16.1

16.4

Net Raw Materials

197

311

311

335

369

411

% chg

6.6

58.1

0.1

7.5

10.1

11.3

Other Mfg costs

11

17

20

21

25

29

% chg

(7.9)

51.1

21.3

4.9

16.1

16.4

Personnel

40

61

67

89

103

120

% chg

(8.1)

51.2

11.2

32.0

16.1

16.4

Other

75

132

167

167

194

226

% chg

(16.9)

75.7

26.4

(0.2)

16.3

16.4

Total Expenditure

323

521

566

612

691

786

EBITDA

50

94

79

73

105

141

% chg

(20.5)

87.8

(15.7)

(7.6)

43.0

34.5

(% of Net Sales)

13.4

15.3

12.3

10.7

13.2

15.2

Depreciation& Amortisation

7

10

11

18

15

16

EBIT

43

83

68

56

90

125

% chg

(22.1)

93.2

(18.1)

(18.6)

61.2

39.4

(% of Net Sales)

11.6

13.6

10.6

8.1

11.3

13.5

Interest & other Charges

-

1

-

22

50

39

Other Income

8

18

28

61

73

77

(% of Net Sales)

2.1

3.0

4.3

8.9

9.2

8.4

Recurring PBT

43

83

68

34

40

86

% chg

(21.9)

93.4

(18.0)

(50.6)

18.7

116.9

PBT (reported)

51

101

96

94

113

164

Tax

10

21

15

18

24

54

(% of PBT)

20.7

20.8

16.0

19.1

21.1

33.1

PAT (reported)

40

80

80

76

89

110

Extraordinary Expense/(Inc.)

-

-

4

-

-

-

ADJ. PAT

40

80

77

76

89

110

% chg

(15.4)

99.6

(4.3)

(0.2)

16.9

22.6

(% of Net Sales)

10.7

13.0

11.9

11.2

11.2

11.8

Basic EPS (`)

5.5

11.0

9.5

9.5

11.1

13.6

Fully Diluted EPS (`)

5.5

11.0

9.5

9.5

11.1

13.6

% chg

(83.1)

99.6

(13.9)

(0.2)

16.9

22.6

Note: *FY2009 was only for 9 months

March 26, 2012

22

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Balance Sheet (Standalone)

Y/E March (` cr)

FY2009*

FY2010

FY2011

FY2012E

FY2013E

FY2014E

SOURCES OF FUNDS

Equity Share Capital

7

7

8

8

8

8

Reserves& Surplus

345

392

645

674

717

779

Shareholder’s Funds

352

399

653

682

725

788

Total Loans

0

0

64

614

479

379

Deferred Tax (Net)

11

13

16

16

16

16

Total Liabilities

363

412

732

1,312

1,219

1,182

APPLICATION OF FUNDS

Gross Block

225

249

270

284

298

313

Less: Acc. Depreciation

39

49

62

80

95

111

Less: Impairment

4

5

3

3

3

3

Net Block

182

195

204

200

200

199

Capital Work-in-Progress

6

3

19

29

29

29

Lease adjustment

-

-

-

-

-

-

Goodwill

3

3

3

3

3

3

Investments

17

18

78

376

376

376

Current Assets

219

309

534

824

748

730

Cash

100

121

278

182

88

50

Loans & Advances

33

52

86

536

536

536

Inventory

43

66

66

69

80

93

Debtors

42

70

104

38

44

51

Current liabilities

64

116

107

120

136

154

Net Current Assets

155

193

427

703

612

575

Misc. Exp. not written off

-

-

-

-

-

-

Total Assets

363

412

732

1,312

1,219

1,182

Note: *FY2009 was only for 9 months

March 26, 2012

23

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Cash Flow (Standalone)

Y/E March (` cr)

FY2009* FY2010 FY2011 FY2012E FY2013E FY2014E

Profit before tax

51

101

96

94

113

164

Depreciation

7

10

11

18

15

16

Change in Working Capital

(5)

(17)

(77)

(373)

(2)

(2)

Direct taxes paid

(10)

(21)

(15)

(18)

(24)

(54)

Others

(5)

(22)

(13)

(61)

(73)

(77)

Cash Flow from Operations

38

51

1

(340)

29

46

(Inc.)/Dec. in Fixed Assets

(7)

(21)

(37)

(24)

(14)

(15)

(Inc.)/Dec. in Investments

(15)

(1)

(61)

(297)

-

-

Others

7

9

9

61

73

77

Cash Flow from Investing

(16)

(12)

(89)

(260)

59

62

Issue of Equity

-

-

0.8

-

-

-

Inc./(Dec.) in loans

-

-

64

550

(135)

(100)

Dividend Paid (Incl. Tax)

(17)

(34)

(47)

(47)

(47)

(47)

Others

(0)

16

228

-

-

-

Cash Flow from Financing

(17)

(18)

245

503

(182)

(147)

Inc./(Dec.) in Cash

5

21

157

(97)

(93)

(38)

Opening Cash balances

95

100

121

278

182

88

Closing Cash balances

100

121

278

182

88

50

Note: *FY2009 was only for 9 months

March 26, 2012

24

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Key Ratios (Standalone)

Y/E March

FY2009*

FY2010

FY2011

FY2012E

FY2013E

FY2014E

Valuation Ratio (x)

P/E (on FDEPS)

33.9

17.0

17.7

17.8

15.2

12.4

P/CEPS

29.0

15.0

15.6

14.5

13.0

10.9

P/BV

3.9

3.4

2.1

2.0

1.9

1.7

EV/Net sales

3.3

2.0

1.7

2.1

1.7

1.4

EV/EBITDA

24.8

13.0

13.5

19.4

13.1

9.3

EV / Total Assets

3.5

3.1

1.5

1.1

1.1

1.1

Per Share Data (`)

EPS (Basic)

5.5

11.0

9.5

9.5

11.1

13.6

EPS (fully diluted)

5.5

11.0

9.5

9.5

11.1

13.6

Cash EPS

6.5

12.5

10.8

11.7

12.9

15.5

DPS

2.0

4.0

5.0

5.0

5.0

5.0

Book Value

48.6

55.0

80.9

84.6

89.9

97.7

DuPont Analysis

EBIT margin

11.6

13.6

10.6

8.1

11.3

13.5

Tax retention ratio

0.8

0.8

0.8

0.8

0.8

0.7

Asset turnover (x)

1.7

2.4

1.9

1.0

1.1

1.3

ROIC (Post-tax)

15.2

26.1

17.0

6.4

10.0

11.8

Cost of Debt (Post Tax)

167.7

268.4

1.1

5.3

7.2

6.0

Leverage (x)

(0.3)

(0.3)

(0.4)

0.1

0.0

(0.1)

Operating ROE

65.9

110.5

9.9

6.5

10.1

11.5

Returns (%)

ROCE (Pre-tax)

0.1

0.2

0.1

0.0

0.1

0.1

Angel ROIC (Pre-tax)

19.1

32.9

20.2

7.9

12.7

-

ROE

11.8

21.3

14.6

11.5

12.7

14.5

Turnover ratios (x)

Asset TO (Gross Block)

1.7

2.6

2.5

2.5

2.7

3.0

Inventory / Net sales (days)

42

32

38

36

34

34

Receivables (days)

33

33

49

20

20

20

Payables (days)

68

63

72

72

72

72

WC cycle (ex-cash) (days)

53

43

84

278

240

207

Solvency ratios (x)

Net debt to equity

(0.3)

(0.3)

(0.4)

0.1

0.0

(0.1)

Net debt to EBITDA

(2.3)

(1.5)

(3.7)

0.8

0.1

(0.3)

Int. Coverage (EBIT/ Int.)

116.8

136.8

166.8

2.5

1.8

3.2

Note: *FY2009 was only for 9 months

March 26, 2012

25

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Profit and Loss (Consolidated)

Y/E March (` cr)

FY2009*

FY2010

FY2011

FY2012E#

FY2013E

FY2014E

Gross sales

397

650

685

981

1,402

1,678

Less: Excise duty

11

10

18

26

42

51

Net Sales

385

640

667

955

1,359

1,627

Other operating income

-

-

-

-

-

-

Total operating income

385

640

667

955

1,359

1,627

% chg

66.1

4.3

43.2

42.3

19.7

Net Raw Materials

199

317

320

484

658

756

% chg

59.7

0.9

51.2

35.9

14.9

Other Mfg costs

14

24

25

32

40

47

% chg

70.7

4.7

29.3

25.8

17.7

Personnel

44

71

77

110

144

165

% chg

60.6

9.0

42.0

30.6

15.2

Other

80

136

172

250

378

448

% chg

70.9

26.7

44.8

51.4

18.5

Total Expenditure

336

548

595

876

1220

1417

EBITDA

49

92

73

80

139

210

% chg

88.3

(21.0)

9.6

75.3

50.5

(% of Net Sales)

12.7

14.4

10.9

8.3

10.3

12.9

Depreciation & Amortisation

7

12

13

23

25

26

EBIT

41

79

60

56

114

184

% chg

92.5

(25.1)

(5.7)

104.0

60.8

(% of Net Sales)

10.7

12.4

8.9

5.9

8.4

11.3

Interest & other Charges

1

2

2

22

61

50

Other Income

8

18

24

61

79

89

(% of Net Sales)

2.0

2.8

3.6

6.4

5.8

5.5

Recurring PBT

41

78

57

34

53

134

% chg

91.6

(26.2)

(40.7)

56.1

152.3

PBT (reported)

48

96

81

95

132

223

Tax

11

21

15

18

24

54

(% of PBT)

22.4

22.5

19.0

19.1

18.2

24.4

PAT (reported)

37

74

66

77

108

169

Minority interest

(1)

(0)

(3)

(6)

(4)

3

PAT after MI

38

74

69

84

112

165

Extraordinary Expense/(Inc.)

-

-

3

(1)

(1)

(1)

ADJ. PAT

38

74

66

85

112

166

% chg

93.9

(11.6)

28.9

32.3

48.1

(% of Net Sales)

10.0

11.6

9.9

8.9

8.3

10.2

Basic EPS (`)

5.3

10.3

8.2

10.5

13.9

20.6

Fully Diluted EPS (`)

5.3

10.3

8.2

10.5

13.9

20.6

% chg

93.9

(20.5)

28.9

32.3

48.1

Note: *FY2009 was only for 9 months, #FY2012E includes Henkel numbers post August 22, 2011

March 26, 2012

26

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2009* FY2010 FY2011 FY2012E# FY2013E FY2014E

SOURCES OF FUNDS

Equity Share Capital

7

7

8

8

8

8

Reserves& Surplus

340

381

623

276

335

453

Shareholders’ Funds

347

388

631

284

343

462

Minority Interest

0

1

0

(29)

(32)

(29)

Total Loans

1

18

74

624

589

489

Deferred Tax (Net)

10

13

16

16

16

16

Total Liabilities

358

419

722

896

916

938

APPLICATION OF FUNDS

Gross Block

242

287

306

438

452

467

Less: Acc. Depreciation

43

55

68

138

163

189

Less: Impairment

4

5

3

3

3

3

Net Block

195

228

235

297

286

276

Capital Work-in-Progress

11

4

20

30

30

30

Lease adjustment

-

-

-

-

-

-

Goodwill

5

6

6

538

538

538

Investments

0

0

61

-

-

-

Current Assets

214

302

510

259

310

384

Cash

102

122

281

3

7

22

Loans & Advances

22

35

55

72

102

122

Inventory

47

73

69

114

129

154

Debtors

43

71

105

70

72

86

Current liabilities

68

120

110

228

249

290

Net Current Assets

146

181

401

31

61

94

Misc. Exp. not written off

-

-

-

-

-

-

Total Assets

358

419

722

896

916

938

Note: *FY2009 was only for 9 months, #FY2012E includes Henkel numbers post August 22, 2011

March 26, 2012

27

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Cash Flow (Consolidated)

Y/E March (` cr)

FY2009* FY2010 FY2011 FY2012E# FY2013E FY2014E

Profit before tax

48

96

81

95

132

223

Depreciation

7

12

13

23

25

26

Change in Working Capital

(11)

(14)

(61)

93

(27)

(18)

Direct taxes paid

(11)

(21)

(15)

(18)

(24)

(54)

Others

(4)

(21)

(23)

(63)

(85)

(88)

Cash Flow from Operations

30

51

(6)

130

21

88

(Inc.)/Dec. in Fixed Assets

14

(39)

(34)

(675)

(14)

(15)

(Inc.)/Dec. in Investments

0

0

(61)

61

0

0

Others

(17)

1

(148)

(297)

79

89

Cash Flow from Investing

(2)

(37)

(243)

(911)

65

74

Issue of Equity

0

0

0.8

-

-

-

Inc./(Dec.) in loans

0

17

57

550

(35)

(100)

Dividend Paid (Incl. Tax)

(17)

(34)

(47)

(47)

(47)

(47)

Others

80

23

396

-

-

-

Cash Flow from Financing

63

7

407

503

(82)

(147)

Inc./(Dec.) in Cash

91

20

158

(277)

3

15

Opening Cash balances

11

102

122

281

3

7

Closing Cash balances

102

122

281

3

7

22

Note: *FY2009 was only for 9 months, #FY2012E includes Henkel numbers post August 22, 2011

March 26, 2012

28

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Key Ratios (Consolidated)

Y/E March

FY2009*

FY2010

FY2011

FY2012E#

FY2013E

FY2014E

Valuation Ratio (x)

P/E (on FDEPS)

35.4

18.3

20.7

16.0

12.1

8.2

P/CEPS

29.7

15.7

17.3

12.6

9.9

7.1

P/BV

3.9

3.5

2.2

4.8

4.0

2.9

EV/Net sales

3.3

2.0

1.6

2.1

1.4

1.1

EV/EBITDA

25.8

13.7

15.1

24.9

13.9

8.7

EV / Total Assets

3.6

3.1

1.5

2.3

2.2

2.0

Per Share Data (`)

EPS (Basic)

5.3

10.3

8.2

10.5

13.9

20.6

EPS (fully diluted)

5.3

10.3

8.2

10.5

13.9

20.6

Cash EPS

6.3

12.0

9.8

13.4

17.0

23.8

DPS

2.0

4.0

5.0

5.0

5.0

5.0

Book Value

47.8

53.4

78.3

35.3

42.5

57.2

DuPont Analysis

EBIT margin

10.7

12.4

8.9

5.9

8.4

11.3

Tax retention ratio

0.8

0.8

0.8

0.8

0.8

0.8

Asset turnover (x)

1.7

2.3

2.0

3.1

4.2

4.9

ROIC (Post-tax)

14.0

22.5

14.3

14.7

28.9

42.0

Cost of Debt (Post Tax)

105.9

14.6

3.8

5.1

8.3

7.0

Leverage (x)

(0.3)

(0.3)

(0.4)

2.2

1.7

1.0

Operating ROE

40.9

20.4

9.8

35.8

63.9

77.4

Returns (%)

ROCE (Pre-tax)

0.1

0.2

0.1

0.1

0.1

0.2

Angel ROIC (Pre-tax)

18.0

29.1

17.6

18.2

35.3

55.6

ROE

11.1

20.3

12.9

18.5

35.8

41.3

Turnover ratios (x)

Asset TO (Gross Block)

1.6

2.4

2.3

2.6

3.1

3.5

Inventory / Net sales (days)

45

34

39

35

33

32

Receivables (days)

41

32

48

33

19

18

Payables (days)

73

63

71

70

71

69

WC cycle (ex-cash) (days)

42

34

66

10

15

16

Solvency ratios (x)

Net debt to equity

(0.3)

(0.3)

(0.4)

2.2

1.7

1.0

Net debt to EBITDA

(2.1)

(1.1)

(3.7)

7.8

4.2

2.2

Int. Coverage (EBIT/ Int.)

58.1

46.7

27.7

2.5

1.9

3.7

Note: *FY2009 was only for 9 months, #FY2012E includes Henkel numbers post August 22, 2011

March 26, 2012

29

Advisory Desk

Jyothy Laboratories | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Jyothy Laboratories

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to 15%)

Sell (< -15%)

March 26, 2012

30