Advisory Desk

October 5, 2011

INEOS ABS (India)

BUY

CMP

`559

Ineos ABS India (INEOS), an 83% subsidiary of Ineos Global Group, is India's

leading manufacturer of an engineering plastic named acrylonitrile butadiene

Target Price

`702

styrene (ABS). On the back of capacity expansion and product development, the

Investment Period

12 Months

top line of the company is expected to grow at a CAGR of 19% during

CY2010-12E. The business of the company is to be transferred to ‘Styrolution’, a

50/50 JV between BASF and INEOS and as specified in the company release on

BSE, ‘an indirect change in control of INEOS ABS India Limited is expected’, which

may trigger an ‘Open Offer’ in the next one year, in our view. The stock is

attractive at 12.7x PE and 0.9x EV/Sales for CY2012E. We recommend Buy on

INEOS ABS India with a target price of `702, based on a target P/E of 16x and

implied EV/Sales of 1.1x for CY2012E.

Investment rationale

Transfer of business to ‘Styrolution’ to act as a key trigger

Ineos Group and BASF have agreed to form a 50/50 joint venture, which is to

include INEOS ABS, INEOS NOVA (sister concern) and Styrene, ABS, polystyrene

businesses of BASF to form a new company as ‘Styrolution’. The deal is expected

to be completed by 4QCY2011. As announced in the company release on BSE

that “an indirect change in control of INEOS ABS India Limited is expected”, which

we believe may trigger an ‘Open Offer’ in the next one year. Since Ineos group

holds 83% stake in INEOS ABS Ltd, a successful open offer may lead to delisting

of the company.

Capacity expansion to help tap the unfulfilled demand

As there is a gap between supply and demand of ABS, CRISIL Research estimates

supply would grow at a 17% CAGR to meet the demand of a 10% CAGR during

CY2010-15E. Assuming the market share of INEOS to remain constant at 60%,

volumes for INEOS ABS resin is likely to grow by 17% over the same period.

Considering the slowdown in the economy we have assumed that the volumes will

grow at 9% yoy and 10% yoy in CY2011E and CY2012E, for which the company

has already expanded its capacity by ~ 33% to 80,000 TPA in 2011.

Outlook and valuation

Net sales of the company is expected to grow at 19% CAGR during CY2010-12E.

The company’s EBITDA margin is expected to fall to 11.2% due to high raw-

material prices in CY2011E and CY2012E. We expect Net Profit to dip in

CY2011E by 3% yoy but rise by 14% yoy in CY2012E to `77cr. At the CMP of

`559, the stock is trading at PE of 12.7x and EV/Sales of 0.9x of CY2012E. We

recommend Buy on INEOS ABS India with a target price of `702, offering an

upside of 25% from current levels.

Key financials

Net

OPM PAT EPS ROE P/E P/BV

EV/

EV/

INEOS

sales (` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

EBITDA (x) Sales (x)

CY2010

742

15.2

70

40

21

14.0

2.9

7.3

1.1

CY2011E

896

11.3

68

39

17

14.5

2.5

8.5

1.0

Twinkle Gosar

Tel: 022- 3935 7800 Ext: 6848

CY2012E

1,049

11.2

77

44

17

12.7

2.1

7.7

0.9

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Advisory Desk

INEOS ABS India

Table of contents

Investment rationale

1

Transfer of business to ‘Styrolution’ to act as a key trigger

1

Capacity expansion to help tap the unfulfilled demand

1

Outlook and valuation

1

Investment arguments

3

Transfer of business to ‘Styrolution’ to act as a key trigger

3

Capacity expansion to help tap the unfulfilled demand

3

Financials

4

Risks

6

Competition

9

Petrochemicals - Polymers industry

10

End-user industry and uses of ABS

10

INEOS Group

12

Company background

12

Windmill Farm

12

Debt-free and cash-rich position

12

Customised/tailor-made products as per market/consumer demand

12

Products

13

ABSOLAC

13

ABSOLAN

14

October 5, 2011

2

Advisory Desk

INEOS ABS India

Investment arguments

Transfer of business to ‘Styrolution’ to act as a key trigger

Ineos Group and BASF have agreed to form a 50/50 joint venture, which is to

include INEOS ABS, INEOS NOVA (sister concern) and Styrene, ABS, polystyrene

businesses of BASF to form a new company as ‘Styrolution’. Since, as announced

in the news release on BSE that “an indirect change in control of INEOS ABS India

Limited is expected”, we believe that this may trigger an ‘Open Offer’ in the next

one year. As Ineos group holds 83% stake in INEOS ABS Ltd, a successful open

offer may lead to delisting of the company. The new entity ‘Styrolution’ is

forecasted to have annual sales of more than €5bn. The JV will be launched on a

global scale and will be a globally competitive producer of Styrene, ABS and

polystyrene, with a leading position in North America, Asia and Europe.

There have been quite a few merger and acquisition activities carried on in the

company in the past, as listed in the following exhibit:

Exhibit 2: History of M&A activities

1973 Incorporated as ABS Plastics Ltd.

1992 Name changed to ABS Industries Ltd.

1997 Bayer acquired 51% stake, name changed to Bayer ABS Ltd.

2004 Styrenic-based polymer business became part of Lanxess, name changed to

Lanxess ABS

2008

83.3% acquired by INEOS ABS Ltd., open offer at `201, name changed to

INEOS ABS India Ltd.

2011 Talks to transfer INEOS ABS to Styrolution, 50/50 JV of INEOS Group and BASF.

Source: Company

Capacity expansion to help tap the unfulfilled demand

Considering the industry demand for ABS vis-a-vis the supply, the gap has

persisted for long and continues to exist. The unfulfilled demand is being met by

the imports of ABS. Moreover, even domestic players have started expansion of the

capacity in order to tap the unfulfilled demand.

Exhibit 3: ABS Volumes in India

Particulars (TPA)

2007

2008

2009

2010

2011E

2012E

ABS production

72,403

77,350

69,581

82,162

91,090

107,607

ABS import

12,383

13,365

21,073

30,368

34,928

39,000

ABS export

1,687

1,307

1,539

60

4,753

11,000

ABS demand

85,000

95,000

88,859

106,329

116,983

128,705

INEOS capacity

50,000

60,000

60,000

60,000

80,000

110,000

INEOS production

49,427

48,053

50,515

54,904

65,053

76,849

INEOS volume

49,194

47,336

51,495

55,068

65,053

76,849

Source: CRISIL Research, Company, Department of Commerce

CRISIL Research estimates that the supply of ABS would grow at 17% CAGR to

meet the demand of a 10% CAGR during CY2010-15E. Assuming the market

share of INEOS to remain constant at 60%, volumes for ABS are likely to grow by

17% over this period. Company has already made capacity expansion from

60,000 TPA to 80,000 TPA in 2011 and also has plans to further augment the

October 5, 2011

3

Advisory Desk

INEOS ABS India

capacity to 110,000 TPA by the end of CY2012. Since SAN is an intermediate

product in the production of ABS, to assist and support increased ABS resins

production, the company has also started capacity expansion for SAN from the

existing 60,000 TPA to 100,000 TPA.

Financials

Key assumptions

CRISIL Research has estimated the supply of ABS to grow at a 17% CAGR during

CY2010-15E. However, considering the slowdown in the economy, we have

assumed volume to grow at 9% yoy and 10% yoy in CY2011E and CY2012E,

respectively. On the back of increased feedstock prices, raw-material prices are

assumed to grow at weighted average of 20% yoy and 9% yoy in CY2011E and

CY2012E, respectively. Increased raw-material prices will raise the price of ABS by

13% yoy in CY2011E and 2% yoy in CY2012E, resulting in realization growth of

24% yoy in CY2011E and 14% yoy in CY2012E.

Exhibit 4: Key assumptions

CY2011E

CY2012E

Total volume growth (ABS+SAN) (%)

9

10

Total realization growth (%)

24

14

Change in weighted raw material prices (%)

20

9

Source: Angel Research

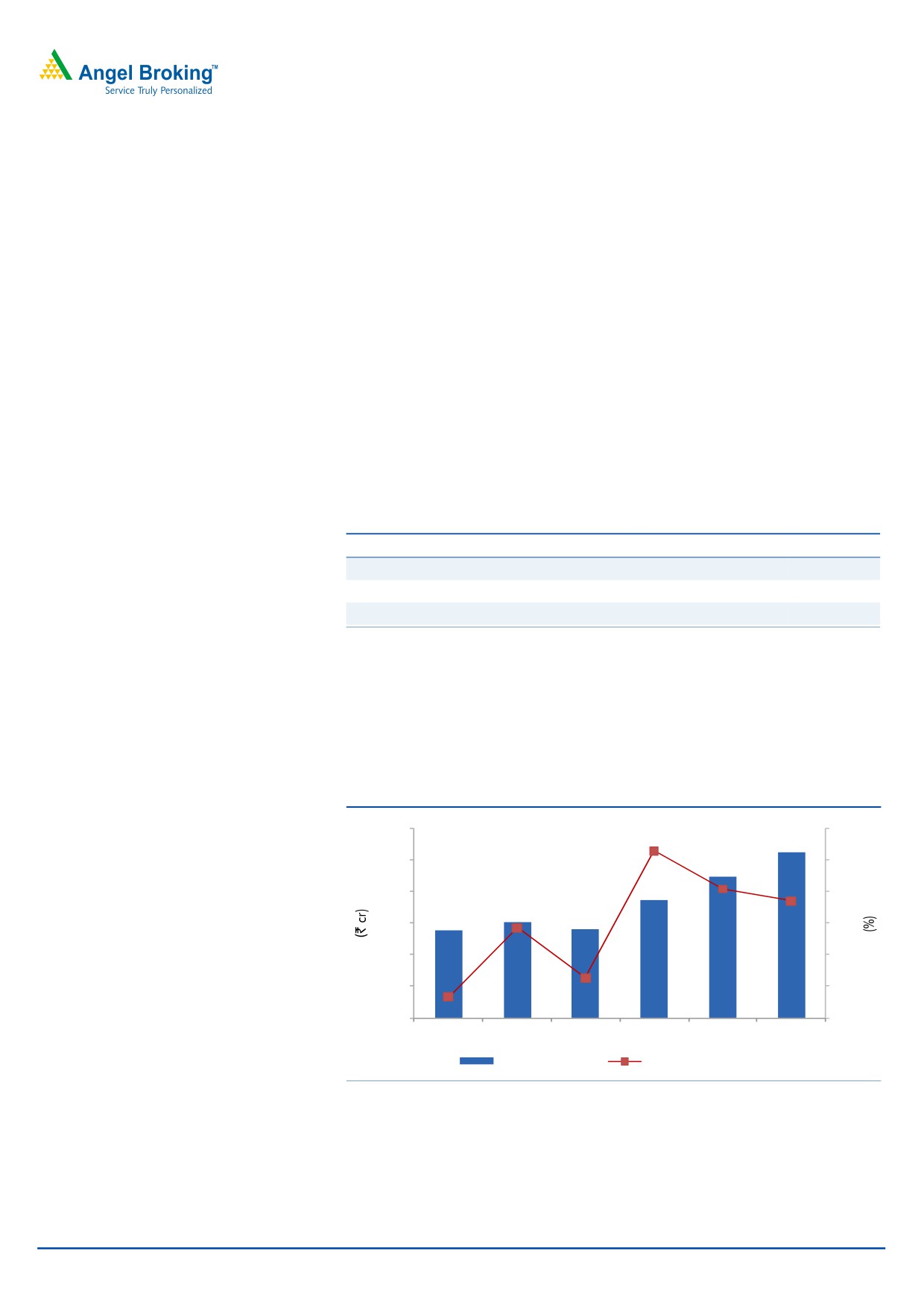

Net sales to grow at a 19% CAGR for CY2010-12E

Considering the capacity expansion and revived demand for ABS from the

automobile and home appliances sector, the company’s net sales are expected to

grow at a CAGR of 19% over CY2010-12E to `1,049cr.

Exhibit 5: Net sales & net sales growth

1200

40

1000

30

800

20

600

10

400

0

200

(10)

0

(20)

CY2007

CY2008

CY2009

CY2010

CY2011E CY2012E

Net Sales (LHS)

Net Sales growth (RHS)

Source: Company, Angel Research

October 5, 2011

4

Advisory Desk

INEOS ABS India

EBITDA margin to fall to 11.2% during CY2010-12E

Despite increased sales, improved operational efficiency through process

development and power generation through wind mills, on the back of high

growth in raw-material prices, the company’s EBITDA margin is expected to fall

from 15.2% in CY2010 to 11.2% in CY2011E and CY2012E. The company’s

EBITDA is expected to be around `117cr in CY2012E.

Exhibit 6: EBITDA & EBITDA margin

140

18

120

15

100

12

80

9

60

6

40

3

20

0

0

CY2007

CY2008

CY2009

CY2010

CY2011E CY2012E

EBITDA (LHS)

EBITDA margin (RHS)

Source: Company, Angel Research

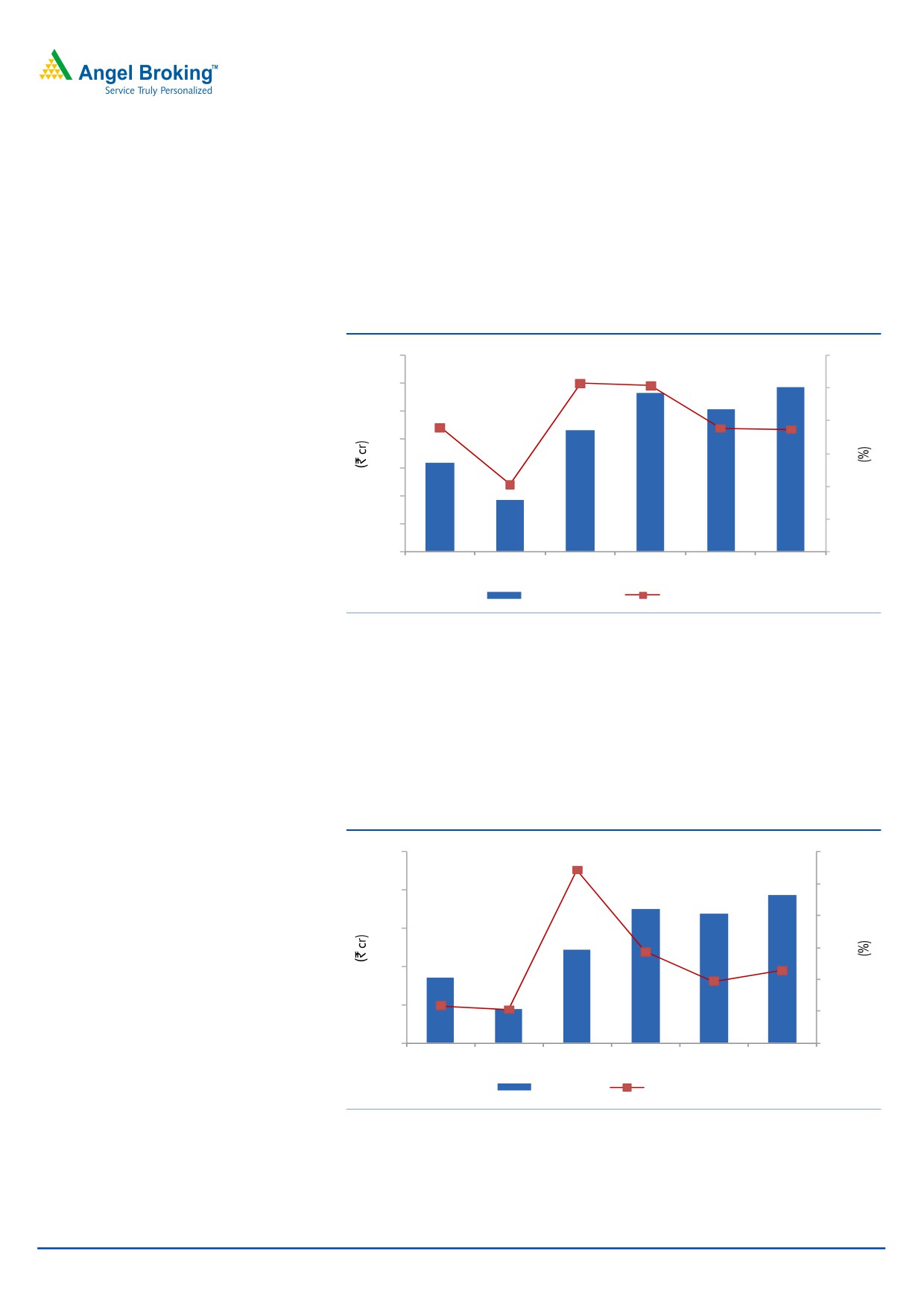

With capacity expansion, the gross block is expected to grow by 15% yoy and 25%

yoy in CY2011E and CY2012E, respectively, with a subsequent increase in the

depreciation from `14cr in CY2010 to `23cr in CY2012E. With zero debt and

cash surplus, the company’s other income is expected to rise from `5cr in CY2010

to `16cr in CY2012E. We expect Net Profit to dip in CY2011E by 3% yoy but rise

by 14% yoy in CY2012E to `77cr.

Exhibit 7: PAT & PAT growth

100

200

150

80

100

60

50

40

0

20

(50)

0

(100)

CY2007

CY2008

CY2009

CY2010

CY2011E CY2012E

PAT (LHS)

PAT growth (RHS)

Source: Company, Angel Research

October 5, 2011

5

Advisory Desk

INEOS ABS India

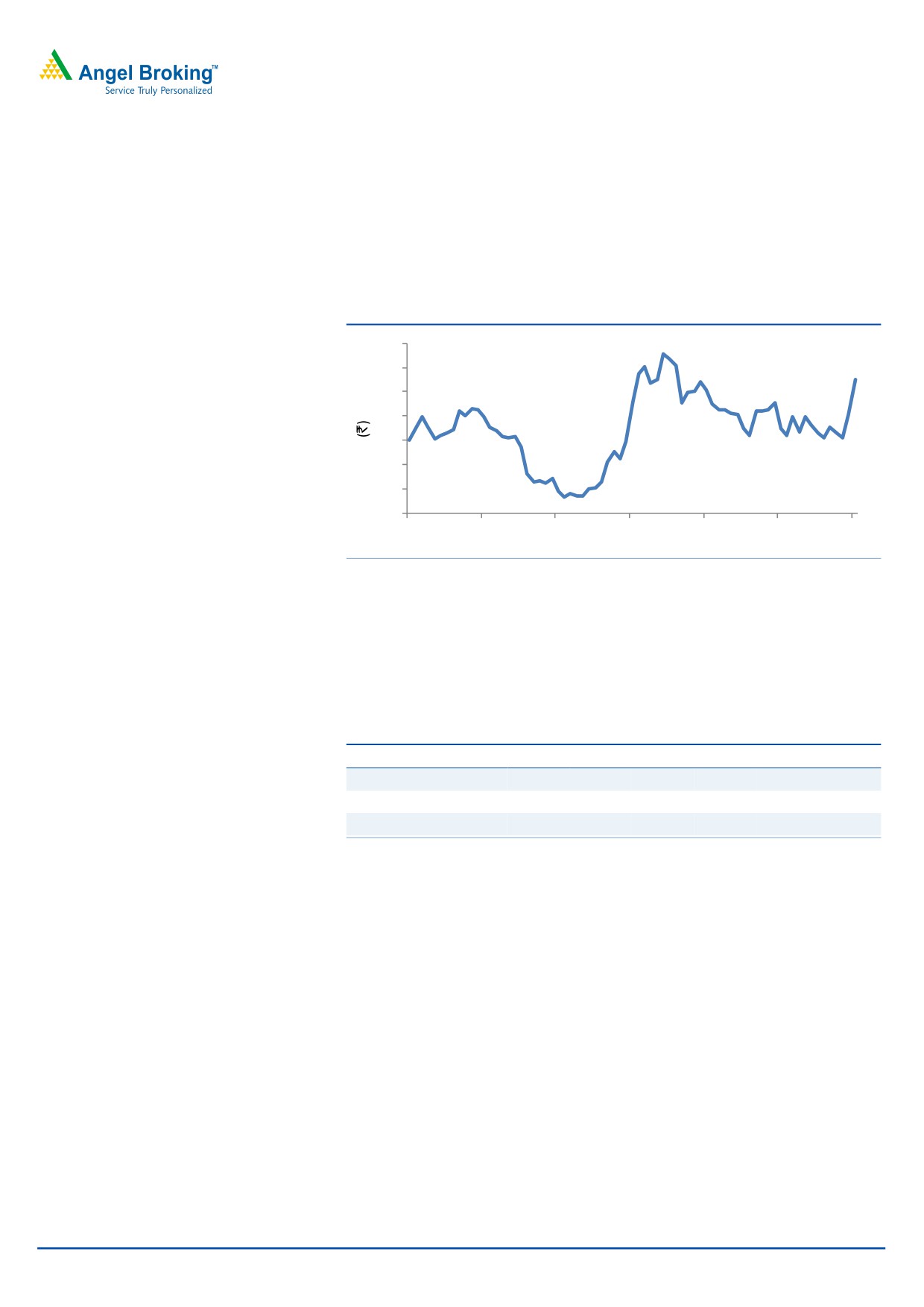

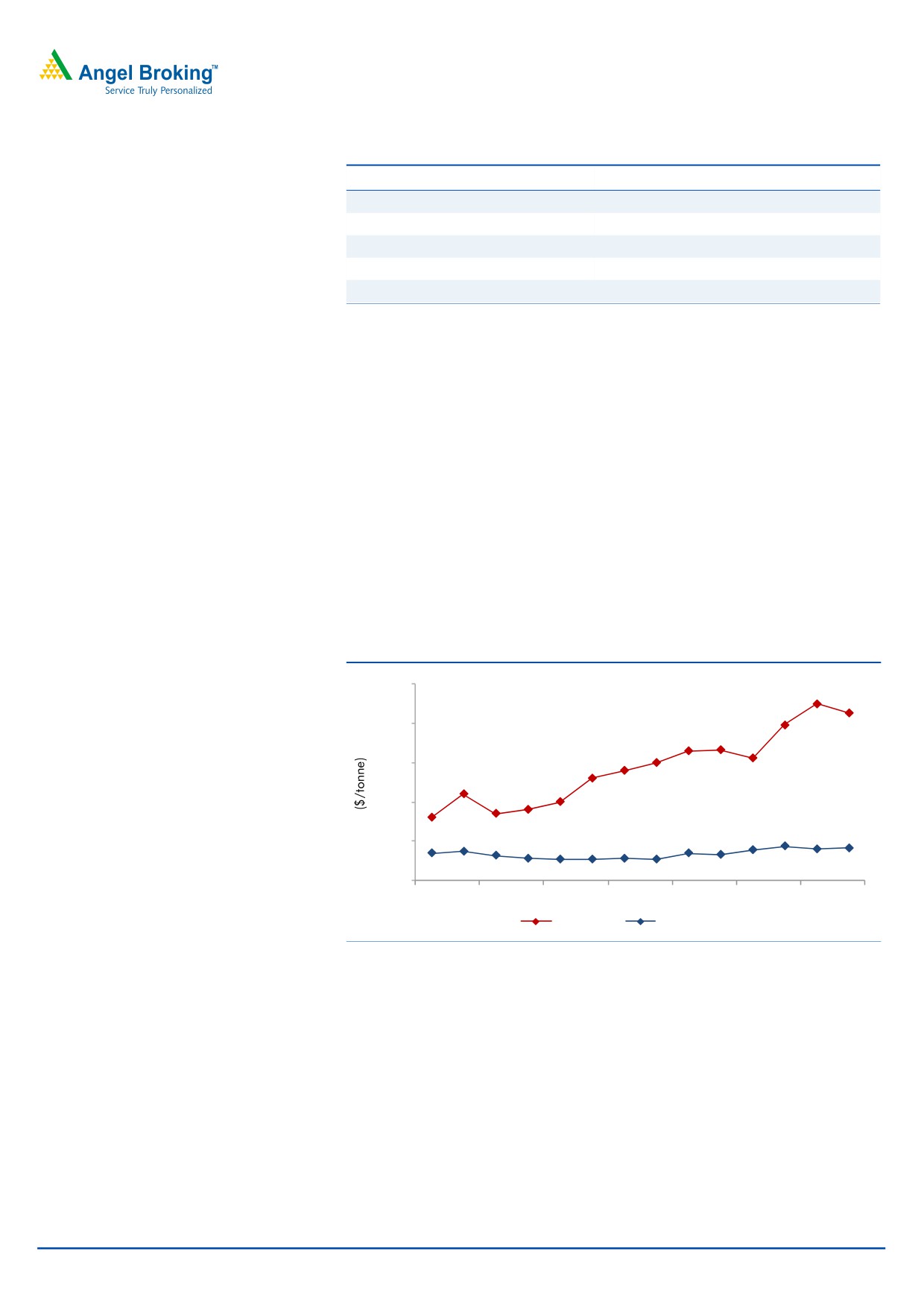

Risks

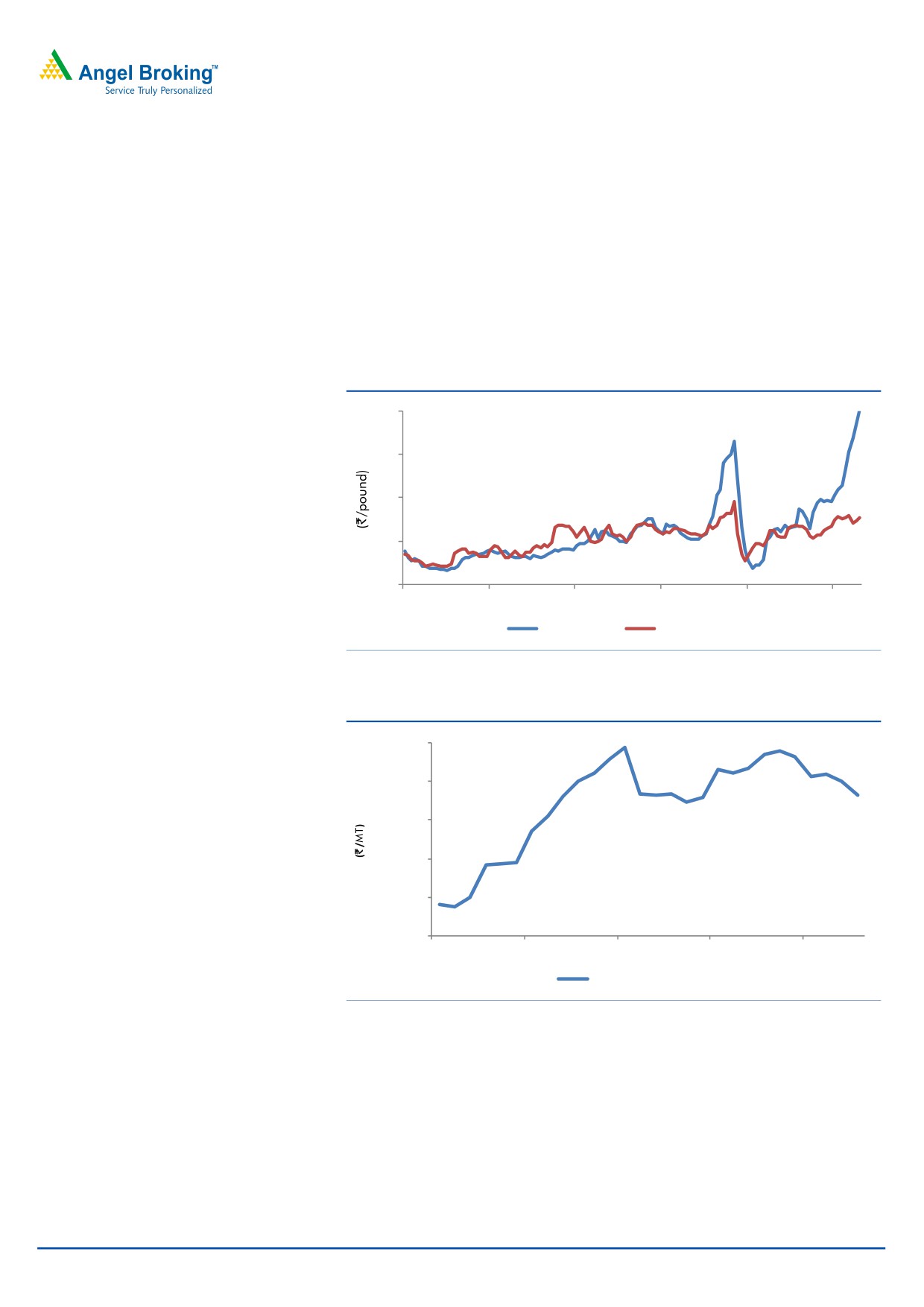

Raw-material supply and price volatility

Acrylonitrile, butadiene and styrene are the key raw materials for production of

ABS and SAN. About 81% of the total raw material used for the production is

imported. Supply of these raw materials is quite tight and inflexible. Moreover,

their prices have been fluctuating in a wide range, which in turn is likely to

negatively affect the company’s margins. On the back of high feedstock prices,

prices for ABS are also expected to rise.

Exhibit 8: Butadiene and Styrene price trend

80

60

40

20

0

Jan-01

Jan-03

Jan-05

Jan-07

Jan-09

Jan-11

Butadiene

Styrene

Source: Bloomberg

Exhibit 9: Acrylonitrile price trend

150,000

130,000

110,000

90,000

70,000

50,000

May-09

Nov-09

May-10

Nov-10

May-11

Acrylonitrile

Source: Bloomberg

October 5, 2011

6

Advisory Desk

INEOS ABS India

Exchange rate fluctuations

Raw materials form nearly 80% of the total operating cost, of which 81% is

imported. The exchange rate fluctuation can have an adverse effect on cost and,

thereby, the margins, so is a risk factor.

Exhibit 10: INR/USD Exchange Rate

52

50

48

46

44

42

40

38

Sep-05

Sep-06

Sep-07

Sep-08

Sep-09

Sep-10

Sep-11

Source: Bloomberg

Imports cheap as compared to domestic ABS

Imported ABS is available at a cheaper rate as compared to domestically available

ABS. Though the percentage price difference between international and domestic

ABS has narrowed, there is still a gap of around 18%.

Exhibit 11: International and domestic price variation of ABS

Particulars

2006

2007

2008

2009

2010

2011

International ABS price (`)

80,745

83,596

83,820

92,905

84,773

107,686

INEOS ABS price (`)

96,838

104,262

108,822

122,879

101,097

127,226

Price difference (%)

20

25

30

32

19

18

Source: Company, Department of Commerce

Sensitivity analysis of EPS

a) Realisation & Butadiene prices

The sensitivity analysis reflects the changes in EPS with respect to the

percentage change in realisation and butadiene prices. We have assumed

realisation to grow at 14.4% yoy in CY2012E and butadiene prices to grow at

10% yoy in CY2012E which will lead to EPS of `44.

October 5, 2011

7

Advisory Desk

INEOS ABS India

Exhibit 12: Impact on EPS w.r.t. % chg. in realisation & butadiene prices

(% chg. in Butadiene prices)

(10)%

0%

10%

20%

30%

50%

(10)%

(23.2)

(28.7)

(34.1)

(39.6)

(45.0)

(56.0)

0%

8.8

3.3

(2.1)

(7.6)

(13.0)

(24.0)

10%

40.8

35.4

29.9

24.4

19.0

8.0

14.4%

54.9

49.4

44.0

38.5

33.1

22.1

20%

72.8

67.4

61.9

56.4

51.0

40.1

25%

88.8

83.4

77.9

72.4

67.0

56.1

Source: Angel Research

b) Volume & Butadiene prices

A 10% yoy growth in CY2012E in volume and 10% yoy growth in butadiene

prices in CY2012E would deliver EPS of `44.

Exhibit 13: Impact on EPS w.r.t. % chg. in volume & butadiene prices

(% chg. in Butadiene prices)

(10)%

0%

10%

20%

30%

(10)%

105.5

101.1

96.6

92.1

87.7

0%

80.2

75.2

70.2

65.3

60.3

5%

67.5

62.3

57.0

51.8

46.6

10%

54.8

49.3

43.9

38.4

32.9

15%

42.1

36.4

30.7

25.0

19.3

20%

29.4

23.5

17.5

11.5

5.6

Source: Angel Research

c) Volume & Realisation

A growth of 10% yoy in CY2012E in volume and 14.4% yoy in CY2012E in

realisation would raise the EPS to `44.

Exhibit 14: Impact on EPS w.r.t. % chg. in volume & realisation

(% chg. in Realisation)

(10)%

0%

10%

14.4%

20%

25%

(10)%

18.6

50.6

82.6

96.7

114.6

130.6

0%

(7.8)

24.3

56.3

70.3

88.3

104.3

5%

(20.9)

11.1

43.1

57.2

75.1

91.1

10%

(34.1)

(2.1)

29.9

44.0

61.9

77.9

15%

(47.3)

(15.3)

16.7

30.8

48.7

64.7

20%

(60.5)

(28.5)

3.5

17.6

35.5

51.5

Source: Angel Research

October 5, 2011

8

Advisory Desk

INEOS ABS India

Competition

In the domestic market, INEOS ABS Ltd. holds 60% market share in ABS resins

segment and 68% in SAN resins segment while the remaining 40% in ABS resins

and 32% in SAN resins is held by Bhansali Engg. Ltd. As per CRISIL Research, total

demand for ABS is expected to grow by 10% CAGR during CY2010-15E to

~177,400 TPA. Assuming the market share of existing players to remain constant,

sales volume of INEOS is expected to almost double from 55,068 TPA in CY2010

to 106,440 TPA in CY2015E.

Exhibit 15: ABS volume growth

ABS trend

2008-09

2009-10

2014-15E

CAGR %

Volume

Market Volume Market Volume Market

2010-

(TPA) share (%) (TPA) share (%) (TPA) share (%)

2015E

INEOS ABS Ltd.

51,495

63

55,068

60

106,440

60

17

Bhansali Engg. Ltd.

30,667

37

36,022

40

70,960

40

17

Source: CRISIL Research, Angel Research

On the valuation front, the company is trading at attractive PE of 13.6x and P/BV

of 2.7x on TTM basis. Even on the ROE front, INEOS has delivered better returns of

around 20% compared to peer average of 16%.

Exhibit 16: Relative valuation

Net

EV/

Y/E June 2011

OPM

PAT EPS ROE P/E P/BV

EV/

Sales

Sales

(TTM)

(%)

(` cr)

(`)

(%)

(x)

(x) EBITDA (x)

(` cr)

(x)

INEOS ABS

804

14.1

72

40

20

13.6

2.7

7.4

1.0

Bhansali Engg.

450

12.3

38

2

17

10.9

1.9

8.2

1.0

BASF India

3,056

7.1

134

31

14

19.3

2.7

12.4

0.9

Clariant Chemicals

1,003

14.9

114

43

18

16.6

3.1

12.9

1.9

Source: Capital Line

October 5, 2011

9

Advisory Desk

INEOS ABS India

Petrochemicals - Polymers industry

According to CRISIL Research, global demand for polymers is expected to grow

by 4-4.5% CAGR during CY2010-15E, while domestic demand is expected to

increase at a CAGR of 10% during the same period.

ABS is an engineering or performance plastic product with applications in home

appliances, electronics and automobiles. According to CRISIL Research, the

domestic ABS industry is expected to grow by 17% yoy to 127,000 TPA in CY2011

due to healthy demand from the automobiles and home appliances segments.

The domestic ABS market is duopolistic in nature. INEOS ABS and Bhansali

Engineering are the major players in the ABS segment.

Exhibit 17: Capacity structure of ABS (TPA)

Company

Location

2009-10

2010-11

2011-12E

INEOS ABS India

Baroda, Gujarat

60,000

80,000

110,000

Bhansali Engg.

Aburoad, MP

50,000

51,000

75,000

Source: Industry, CRISIL Research

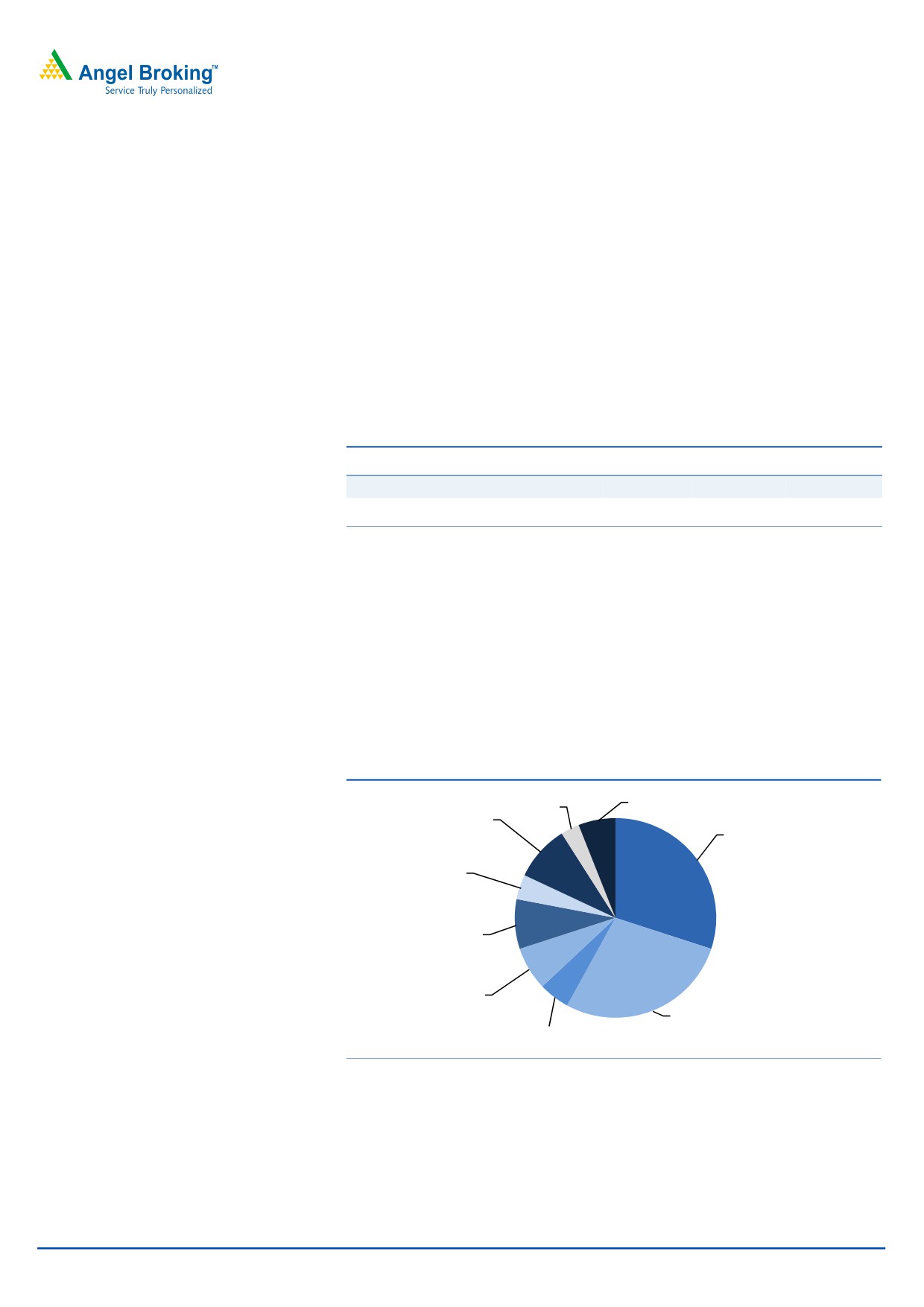

End-user industry and uses of ABS

ABS resins are composed of 50% styrene and varying amounts of butadiene and

acrylonitrile. Styrene provides rigidity and ease of processing, acrylonitrile offers

chemical resistance and heat stability and butadiene gives toughness and impact

strength. ABS applications are based on its properties such as lightweight, ability to

comprise various colors, good product finish and strength in withstanding

vibrations.

Exhibit 18: Use of ABS in various sectors in India

Others

Textiles

6%

Stationary/

3%

helmet

Home Appliances

9%

30%

Luggage & bus

body

4%

Business machine

office automation

8%

Electrical &

electronics

Automobiles

7%

Telecom

28%

5%

Source: Industry, CRISIL Research

Growth will continue to come from home appliances (including refrigerators,

washing machines and air conditioners), automobiles and business machines and

office automation segments. These three segments alone account for around 70%

of total demand in CY2010-11.

October 5, 2011

10

Advisory Desk

INEOS ABS India

Exhibit 19: ABS - End-use market trend

2010-11E

2010-11E

2015-16 E

2015-16 E

End-use market

(TPA)

(% share)

(TPA)

(% share)

Automobiles

41,224

32.5

70,723

30.8

Home appliances

37,424

29.5

77,254

33.7

Telecom

5,226

4.1

8,417

3.7

Electrical and electronics

8,330

6.6

16,304

7.1

Business machine office automation

11,254

8.9

18,792

8.2

Luggage and bus body

3,625

2.9

5,838

2.5

Stationary/helmet

9,652

7.6

16,264

7.1

Textiles

3,333

2.6

4,661

2

Others

6,893

5.4

11,101

4.8

Source: Industry, CRISIL Research

October 5, 2011

11

Advisory Desk

INEOS ABS India

INEOS Group

INEOS Group, the holding company of INEOS ABS India Ltd., is a leading and

global manufacturer of petrochemicals, specialty chemicals and oil products. The

company has a turnover of around US$28.4bn and comprises 15 businesses (all

these businesses have a major chemical heritage). Leading market positions allow

INEOS Group to be the supplier of choice for many of the largest customers in our

markets. The company’s production network spans 61 manufacturing facilities in

13 countries throughout the world; the group produces more than 40mn TPA of

petrochemicals and 20mn TPA of crude oil refined products (fuels) each year.

Company background

Incorporated in 1973 as ABS Plastics Ltd., the company is now known as INEOS

ABS India Ltd. Ineos Group holds an 83% share in the company. INEOS is a

leading manufacturer of an engineering plastic named ABS.

The company has three manufacturing plants in Gujarat at Nandesari, Katol and

Moxi. The Nandesari plant manufactures ABSOLAC (ABS polymer), while the Katol

plant produces ABSOLAN (SAN polymer). The Moxi plant blends the resins

manufactured at the above two plants in the required proportion to get the desired

grade of output. At Moxi, the company has a research and application

development cell to meet R&D requirements of global LANXESS activities in areas

of a) process and product development b) polymer characterisation c) tailor-made

grades and special color development.

Windmill Farm

The company has installed wind turbine generators (WTG) at Lamba, Dhank and

Pransala in Gujarat. Wind farms have been an important source of energy

generation, which in turn has reduced the power consumption worth 8 mio units.

Power generated by the windmills has enabled the company to rationalise its

power cost, which constitutes around 4% of the total operating cost.

Debt-free and cash-rich position

The company has zero debt with a cash surplus (including investments) of around

`147cr in June 2011, which will enable the company to finance the extended

capacity through internal accruals.

Tailor-made products as per market & consumer demand

ABS can be easily used in specific applications by co-polymerising i.e., changing

polymer composition and blending. Thus, taking advantage of its flexibility of

composition and structure, allowing its use in diverse applications, the company

has launched various tailor-made products.

October 5, 2011

12

Advisory Desk

INEOS ABS India

Exhibit 20: Product development

Product development

End-use products

Blend of ABS/PMMA

LCD TV market

Low gloss ABS

Bus roof and automotive body interior

Nylon/ABS blend

Indian automotive markets

ESCR grade extrusion grade ABS

Refrigerator application

Glass filled ABS

AC blower application

Source: Company

Products

The company manufactures two products ABSOLAC (ABS) and ABSOLYN (SAN).

ABS constitutes nearly 86% of the company’s total revenue, while SAN constitutes

14% of revenue.

ABSOLAC

ABS (acrylonitrile butadiene styrene) polymer is a versatile engineering plastic

accepted as a substitute for conventional materials. The mechanical and thermal

properties of ABS are comparable to metals. It is a high performance plastic, used

predominantly in automobiles and consumer durables. ABS also has its application

in refrigerator liners, telecommunications, consumer electronics, computer cabinets

and cameras.

Exhibit 21:International prices & margins of ABS

2500

2000

1500

1000

500

0

1999

2001

2003

2005

2007

2009

2011E

ABS Prices

Margins

Source: CRISIL Research

Considering the industry volume growth of ABS to reach ~177,400 TPA in

CY2014-15E and assuming the market share to remain constant, ABS sales

volume for INEOS is expected to grow at a CAGR of 17% during CY2010-15E.

October 5, 2011

13

Advisory Desk

INEOS ABS India

Exhibit 22: ABS volume & value growth

12

70

10

60

8

50

6

40

4

30

2

0

20

(2)

10

(4)

0

(6)

CY2007

CY2008

CY2009

CY2010 CY2011E CY2012E

ABS Resins (LHS)

ABS volume growth (RHS)

Source: Company, Angel Research

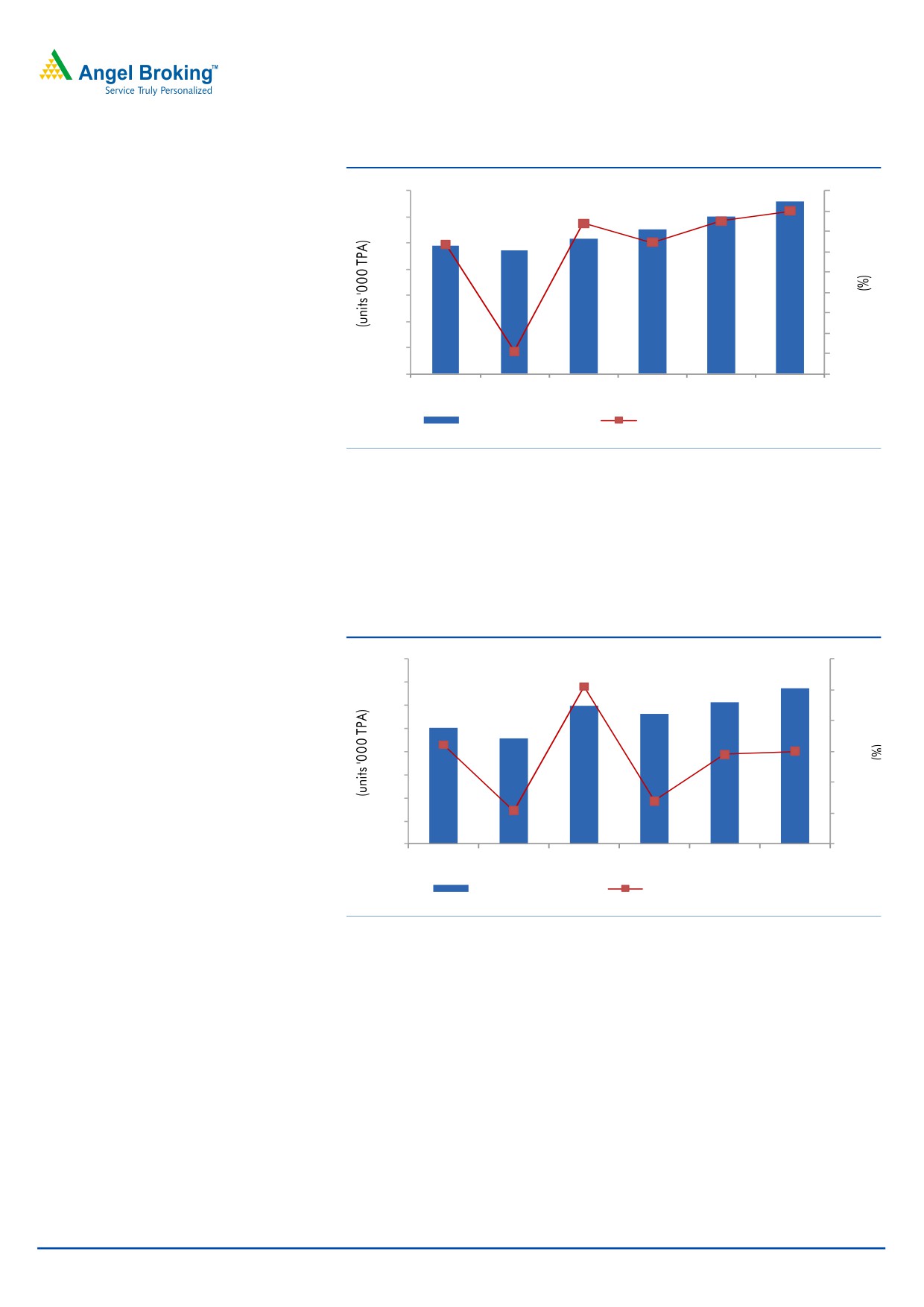

ABSOLAN

SAN (styrene acrylonitrile) is a polymerised plastic resin giving 95% transparent

finish. It has its applications in lightings, stationeries and novelties, refrigerators

and cosmetic packing.

Exhibit 23: SAN volume & value growth

16

40

14

30

12

20

10

8

10

6

0

4

(10)

2

0

(20)

CY2007

CY2008

CY2009

CY2010

CY2011E CY2012E

SAN Resins (LHS)

SAN volume growth (RHS)

Source: Company, Angel Research

ABS segment has capacity of 60,000 TPA and the utilisation rate is 91.5%, while

the SAN segment is equipped with 60,000 TPA capacity utilised at

82.4%.

Additional capacity of 20,000 TPA for ABS is operational since early 2011, while

the company has plans to further augment the capacity to 110,000 TPA. To

support the additions in ABS production, SAN capacity is also planned to be

extended to 100,000 TPA.

October 5, 2011

14

Advisory Desk

INEOS ABS India

Standalone profit & loss account

Y/E December (` cr)

CY2007

CY2008

CY2009

CY2010

CY2011E

CY2012E

Gross sales

644

689

606

816

1008

1153

Less: Excise duty

87

85

47

74

112

104

Net Sales

557

604

559

742

896

1049

Other operating income

-

-

-

-

-

-

Total operating income

557

604

559

742

896

1049

% chg

-

8

(7)

33

21

17

Net Raw Materials

410

467

360

522

663

787

% chg

-

14

(23)

45

27

19

Other Mfg costs

29

33

34

36

44

49

% chg

-

12

6

6

21

12

Personnel

14

17

18

20

26

26

% chg

-

15

6

16

28

1

Other

41

51

61

51

62

69

% chg

-

25

19

(16)

21

12

Total Expenditure

494

495

496

497

498

499

EBITDA

63

37

86

113

101

117

% chg

-

(42)

133

31

(10)

16

(% of Net Sales)

11

6

15

15

11

11

Depreciation& Amortisation

14

15

14

14

16

23

EBIT

50

22

72

99

85

94

% chg

-

(55)

222

38

(14)

11

(% of Net Sales)

9

4

13

13

10

9

Interest & other charges

1

2

1

2

0

0

Other Income

6

7

4

5

12

16

(% of Net Sales)

1

1

1

1

1

2

Extraordinary Expense/(Inc.)

1

-

-

-

-

-

PBT (reported)

54

27

75

103

97

110

Tax

19

9

26

33

29

33

(% of PBT)

35

34

35

32

30

30

PAT (reported)

34

18

49

70

68

77

PAT after MI (reported)

34

18

49

70

68

77

ADJ. PAT

34

18

49

70

68

77

% chg

0

(48)

171

43

(3)

14

(% of Net Sales)

6

3

9

9

8

7

Basic EPS (`)

20

10

28

40

39

44

Fully Diluted EPS (`)

20

10

28

40

39

44

% chg

0

(48)

171

43

(3)

14

Dividend

5

4

6

7

8

10

Retained Earning

29

14

43

63

59

67

October 5, 2011

15

Advisory Desk

INEOS ABS India

Standalone balance sheet

Y/E December (` cr)

CY2007

CY2008

CY2009

CY2010

CY2011E

CY2012E

SOURCES OF FUNDS

Equity Share Capital

18

18

18

18

18

18

Preference Capital

-

-

-

-

-

-

Reserves& Surplus

200

213

255

317

376

443

Shareholders’ Funds

218

231

272

334

394

461

Minority Interest

-

-

-

-

-

-

Total Loans

-

-

-

-

-

-

Deferred Tax Liability

30

29

27

25

25

25

Total Liabilities

247

259

300

360

419

486

APPLICATION OF FUNDS

Gross Block

280

307

310

318

365

457

Less: Acc. Depreciation

140

154

168

181

198

220

Net Block

140

153

142

136

168

236

Capital Work-in-Progress

24

8

11

12

13

14

Lease adjustment

-

-

-

-

-

-

Goodwill

-

-

-

-

-

-

Investments

24

45

71

93

93

93

Current Assets

213

179

199

281

358

391

Cash

40

32

37

60

27

(15)

Loans & Advances

15

18

19

41

108

147

Inventory

69

56

57

71

89

102

Debtors

89

74

85

109

134

157

Current liabilities

155

127

128

166

212

249

Net Current Assets

58

52

71

115

145

143

Misc. Exp. not written off

-

-

-

-

-

-

Total Assets

247

259

300

360

419

486

October 5, 2011

16

Advisory Desk

INEOS ABS India

Key ratios

Y/E December

CY2007

CY2008

CY2009

CY2010

CY2011E

CY2012E

Valuation Ratio (x)

P/E (on FDEPS)

28.5

54.4

20.1

14.0

14.5

12.7

P/CEPS

20.5

30.0

15.5

11.7

11.7

9.8

P/BV

4.5

4.3

3.6

2.9

2.5

2.1

Dividend yield (%)

0.5

0.4

0.6

0.7

0.9

1.0

EV/Net sales

1.6

1.5

1.6

1.1

1.0

0.9

EV/EBITDA

14.5

24.5

10.1

7.3

8.5

7.7

EV / Total Assets

3.7

3.5

2.9

2.3

2.1

1.9

Per Share Data (`)

EPS (Basic)

19.6

10.3

27.9

39.8

38.5

43.9

EPS (fully diluted)

19.6

10.3

27.9

39.8

38.5

43.9

Cash EPS

27.3

18.6

36.1

47.8

47.7

56.8

DPS

3.0

2.5

3.5

4.0

4.8

5.8

Book Value

123.9

131.2

154.9

190.1

223.8

261.9

DuPont Analysis

EBIT margin

8.9

3.7

12.8

13.3

9.5

9.0

Tax retention ratio

0.6

0.7

0.7

0.7

0.7

0.7

Asset turnover (x)

3.5

3.5

3.1

3.8

3.1

2.7

ROIC (Post-tax)

20.2

8.5

26.1

34.6

20.8

16.8

Cost of Debt (Post Tax)

-

-

-

-

-

-

Leverage (x)

(0.3)

(0.3)

(0.4)

(0.5)

(0.3)

(0.2)

Operating ROE

14.3

5.7

15.7

18.8

14.5

14.0

Returns (%)

ROCE (Pre-tax)

20.1

8.6

24.0

27.5

20.3

19.4

Angel ROIC (Pre-tax)

31.3

12.8

39.9

50.7

29.7

24.0

ROE

15.8

7.8

18.0

21.0

17.2

16.7

Turnover ratios (x)

Asset TO (Gross Block)

2.0

2.0

1.8

2.3

2.5

2.3

Inventory / Net sales (days)

45

34

38

35

36

36

Receivables (days)

58

44

56

54

55

55

Payables (days)

114

81

99

96

97

97

WC cycle (ex-cash) (days)

12

12

22

27

48

55

Solvency ratios (x)

Net debt to Equity

(0.3)

(0.3)

(0.4)

(0.5)

(0.3)

(0.2)

Net debt to EBITDA

(1.0)

(2.1)

(1.3)

(1.3)

(1.2)

(0.7)

Int. Coverage (EBIT/ Int.)

42.6

11.6

55.6

55.0

-

-

October 5, 2011

17

Advisory Desk

INEOS ABS India

Advisory Team Tel: (91) (022) 39500777

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

INEOS ABS (India) Ltd

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to 15%)

Sell (< -15%)

October 5, 2011

18