IPO Note | Cable

June 20, 2017

GTPL Hathway Limited

NEUTRAL

sue Open: June 21, 2017

Is

Issue Close: June 23, 2017

GTPL Hathway Ltd. (GTPL) was initially incorporated by Aniruddhasinhji Jadeja

and Kanaksinh Rana, through the consolidation of cable service businesses in

Present Eq. Paid up Capital: `98.4cr

Ahmedabad and Vadodara. In October 2007, Hathway acquired a 50% share of

business. GTPL is a leading regional Multi System Operator (MSO) in India,

Offer for Sale: **1.44cr Shares

offering cable television and broadband services with a market share of 67% of

cable television subscribers in Gujarat and number 2 MSO in Kolkata and

Fresh issue: `240 cr

Howrah in West Bengal with a market share of

24% of cable television

subscribers. As of January 31, 2017, the company’s digital cable television

Post Eq. Paid up Capital: `112.5cr

services reached 189 towns across India, including towns in Gujarat, West

Bengal, Maharashtra, Bihar, Assam, Jharkhand, Madhya Pradesh, Telangana,

Issue size (amount): *`480cr -**485 cr

Rajasthan and Andhra Pradesh.

Positives: (a) One of the leading regional MSOs with significant market share in

Price Band: `167-170

Gujarat and Kolkata; (b) High quality infrastructure network; (c) Balanced local

and regional content to attract and retain subscribers; (d) Strong traction on

Lot Size: 88 shares and in multiple

digitization; (e) Successful track record of identifying, acquiring and integrating

thereafter

MSOs, ISOs and LCOs; (f) Experienced promoters and management team

Post-issue implied mkt. cap: *`1878cr -

backed by promoter company Hathway Cable & Datacom.

**`1912cr

Investment concerns: (a) None of the players in the cable industry within peer

Promoters holding Pre-Issue: 98.9%

group (Den Networks, Hathway Cable & Datacom, Ortel Communication & Siti

Promoters holding Post-Issue: 73.7%

Cable Networks) have reported profits in last 3-5 years; (b) Cable business is

highly Local Cable Operator (LCO) dependent revenue model, which posses

*Calculated on lower price band

inherent risk (Cable biz contributes ~80% revenues); (c) Presence of the Hathway

in the same geography may cannibalize the potential subscribers; (d) Intensifying

** Calculated on upper price band

competition - new entrants at pan India level in broadband and DTH business

Book Building

may further create pricing pressure; (e) GTPL has low asset turnover ratio and in

order to remain competitive it will need to continuously upgrade technology; (f)

QIBs

60% of issue

Experienced Promotor (Hathway Cable & Datacom) is making loses from last four

fiscal years.

Non-Institutional

15% of issue

Outlook and Valuation: In terms of valuation, GTPL’s P/BV multiple annualised

Retail

35% of issue

9MFY2017 at 3.1x, as compared to peers i.e. Den Networks 1.8x, Hathway

Cable & Datacom 0.7x, Ortel Comm. 1.4x, Siti Networks 4.8x. The cable industry

is already undergoing a period of weak performance and with disruptive pricing

Post Issue Shareholding Patter

of new entrants, there is a high probability that the performance may weaken

further. Hence, we recommend NEUTRAL rating on the issue.

Promoters

74%

Others

26%

Key Financials

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

9MFY17

Net Sales

453.2

577.2

622.8

844.6

689.3

% chg

26.6

27.4

7.9

35.6

-

Net Profit

38.3

24.0

16.7

69.0

43.2

% chg

26.6

(37.2)

(30.4)

313.3

OPM (%)

23.6

27.0

24.0

31.3

29.5

EPS (`)

226.0

120.1

83.5

7.0

4.4

P/E (x)

1.5

2.8

4.0

47.4

-

P/BV (x)

0.3

0.2

9.8

7.1

-

RoE (%)

16.3

7.7

6.1

12.8

-

EV/Sales (x)

0.5

0.5

5.5

4.2

-

Abhishek Lodhiya

EV/EBITDA (x)

2.3

1.9

23.0

13.3

-

+022 39357600, Extn: 6811

Source: RHP, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

Please refer to important disclosures at the end of this report

1

GTPL Hathway | IPO Note

Company background

GTPL Hathway Ltd. (GTPL) was initially incorporated by Aniruddhasinhji Jadeja and

Kanaksinh Rana, through the consolidation of cable service businesses in

Ahmedabad and Vadodara. In October 2007, Hathway acquired a 50% share of

business. GTPL is a leading regional MSO in India, offering cable television and

broadband services. GTPL is number 1 MSO in Gujarat with a market share of

67% of cable television subscribers in 2015, accounting for ~3.7 million of 5.6

million cable television households in Gujarat. Also, it is number 2 MSO in Kolkata

and Howrah in West Bengal with a market share of 24% of cable television

subscribers in this market in 2015, accounting for approximately ~0.7 million of

3.0 million cable television households in Kolkata and Howrah. Gujarat is an

important market for broadcasters and advertisers, as it contributed to more than

a 5% viewership share on an all-India basis and more than 8% of the Hindi

speaking market in India in 2015. GTPL accounted for a 14% share of the total

cable carriage and placement fee market in India in FY2016.

As of January 31, 2017, GTPL’s digital cable television services reached 189 towns

across India, including towns in Gujarat, West Bengal, Maharashtra, Bihar, Assam,

Jharkhand, Madhya Pradesh, Telangana, Rajasthan and Andhra Pradesh. As of

January 31, 2017, company seeded ~6.55 million STBs and had ~5.69 million

active digital cable subscribers. As of August 31, 2016, it received requisitions

from LCOs for ~2.02 million STBs (Set-Top box). Between September 1, 2016 and

January 31, 2017, it has seeded 0.46 million STBs. As of January 31, 2017,

Company had

228,217 broadband subscribers (based on the number of

broadband subscribers of Subsidiary, GTPL Broadband Private Limited; the

broadband business of Company was transferred to GTPL Broadband Private

Limited with effect from April 1, 2016). As of January 31, 2017, GTPL provided

broadband services primarily in the state of Gujarat and had established a home

pass of ~1.05 million households.

GTPL’s primary source of revenue from cable services is subscription income

received from subscribers and placement / carriage income received from carriage

fees payable by broadcasters for carrying their channels and placement fees

payable by broadcasters for placing their channels on a preferred channel number

or position. As of January 31, 2017, company offered up to 285 pan-India

standard definition channels,

158 regionally-transmitted standard definition

channels, 32 pan-India high definition channels and 39 regionally-transmitted

high definition channels on digital cable platform. GTPL also owns and operates

27 channels offering localized content developed for the states in which company

broadcasts, including a range of religious and cultural content, film, music and

educational channels. GTPL also has the right to place the “Gujarat News”

channel on its network, which is produced by Group Company, Gujarat Television

Private Limited. Company produces its own content and also offers third-party

content on its local channels to ensure that it has a suitable mix of content that

appeals to a range of demographics. Company believes its local content offering

is a key strength, and provides a competitive advantage to attract, retain and grow

its subscriber base.

June 20, 2017

2

GTPL Hathway | IPO Note

Exhibit 1: GTPL’s Journey

Source: IPO Presentation, Angel Research

Issue details

The company is raising `240cr through a fresh issue of equity shares in the price

band of `167-170. The fresh issue will constitute ~12.6% of the post-issue paid-

up equity share capital of the company, assuming the issue is subscribed at the

upper end of the price band. The company is offering 1.44cr shares that are being

sold by the promoter group.

Exhibit 2: Pre and Post-IPO shareholding pattern

No. of shares (Pre-issue)

(%)

No. of shares (Post-issue)

(%)

Promoters

9,73,10,088

98.9

8,29,10,088

73.7

Others

10,35,300

1.1

2,95,52,947

26.3

9,83,45,388

100.0

11,24,63,035

100.0

Source: RHP, Angel Research; Note: Calculated on upper price band

Objects of the offer

Repayment/pre-payment, in full or part, of certain borrowings availed by

Company (`228.9Cr will be utilized).

Remaining will be utilized for general corporate purpose.

June 20, 2017

3

GTPL Hathway | IPO Note

Investment Rationale

One of the leading regional MSOs with significant market share in Gujarat and

Kolkata

GTPL is one of the leading regional MSOs in India offering cable television and

broadband services. As of January 31, 2017, company’s digital cable television

services reached 189 towns across India, including towns in Gujarat, West Bengal,

Maharashtra, Bihar, Assam, Jharkhand, Madhya Pradesh, Telangana, Rajasthan

and Andhra Pradesh. GTPL is number 1 MSO in Gujarat with a market share of

67% of cable television subscribers in 2015, accounting for ~3.7 million of 5.6

million cable television households in Gujarat. Also, number 2 MSO in Kolkata

and Howrah in West Bengal with a market share of ~24% of cable television

subscribers in this market in 2015, accounting for ~0.7 million of 3.0 million

cable television households in Kolkata and Howrah. Company believes that the

significant market shares in Gujarat, Kolkata and Howrah are a result of early

entry into these regions, strong relationships with LCOs that have developed &

consolidated since entering these markets, continuous investment in advanced

technology development and GTPL’s niche and exclusive local content offerings

that appealed to subscribers in these regions. Gujarat is an important market for

broadcasters and advertisers, as it contributed to more than a 5% viewership share

on an all-India basis and more than 8% of the Hindi speaking market in India in

2015. GTPL accounted for a 14% share of the total cable carriage and placement

fee market in India in Fiscal 2016.

High quality infrastructure network

GTPL’s services are supported by its owned and leased fiber optic cable network

(using HFC), digital head-ends, analog head-ends, advanced CAS, SMS and

advanced internet nodes facilitating seamless delivery of services. GTPL believes

that its ability to improve and maintain its network infrastructure to keep pace with

the constantly evolving subscriber preferences and technology landscape provides

a competitive advantage. GTPL’s digital services platform is supported by its

owned intercity and intra-city optical fiber cable network, which, as of January 31,

2017, spanned ~5,406 kilometers (on a consolidated basis), and the fiber

network leased to the Company, which spanned ~3,615 kilometers (on a

standalone basis). Its digital cable services across coverage area are supported by

two main digital head-ends located in Ahmedabad and Kolkata. Currently, GTPL is

in the process of upgrading its main head-end in Ahmedabad with advanced

technology from Harmonic International AG. GTPL also has four support digital

head-ends located in Dibrugarh, Adilabad, Visakhapatnam and Patna, which are

connected via leased-line network from various telecom operators, who in turn

deliver these leased line circuits through GTPL’s own optical fiber cable network

spanning over 25,000 kilometers (on a standalone basis). These head-ends are

used to insert certain encrypted local channels along with the feed received from

the main head-ends. The support head-ends also provide backup in the event of

any disruption or outage in the leased line. As of January 31, 2017, the

Company’s digital cable TV transmission used a spectrum ranging from 306 MHz

to 682 MHz.

June 20, 2017

4

GTPL Hathway | IPO Note

GTPL sources the equipment for digital service offerings from some of the leading

international vendors of digital components. Company procures STBs primarily

from NDS Limited, Changhong (Hong Kong) Trading Limited, Shenzhen Skyworth

Digital Technology Co. Limited and Tele System Communication Pte. Ltd.

Moreover, other equipments such as head-ends and servers are procured from

some of the leading suppliers, including Harmonic International AG and NDS

Limited. CAS is sourced from Nagravision S.A. and NDS Limited and fiber is

procured from vendors such as Sterlite Technologies Limited. GTPL’s services are

supported by Magnaquest Technologies Limited, which is an advanced software

platform.

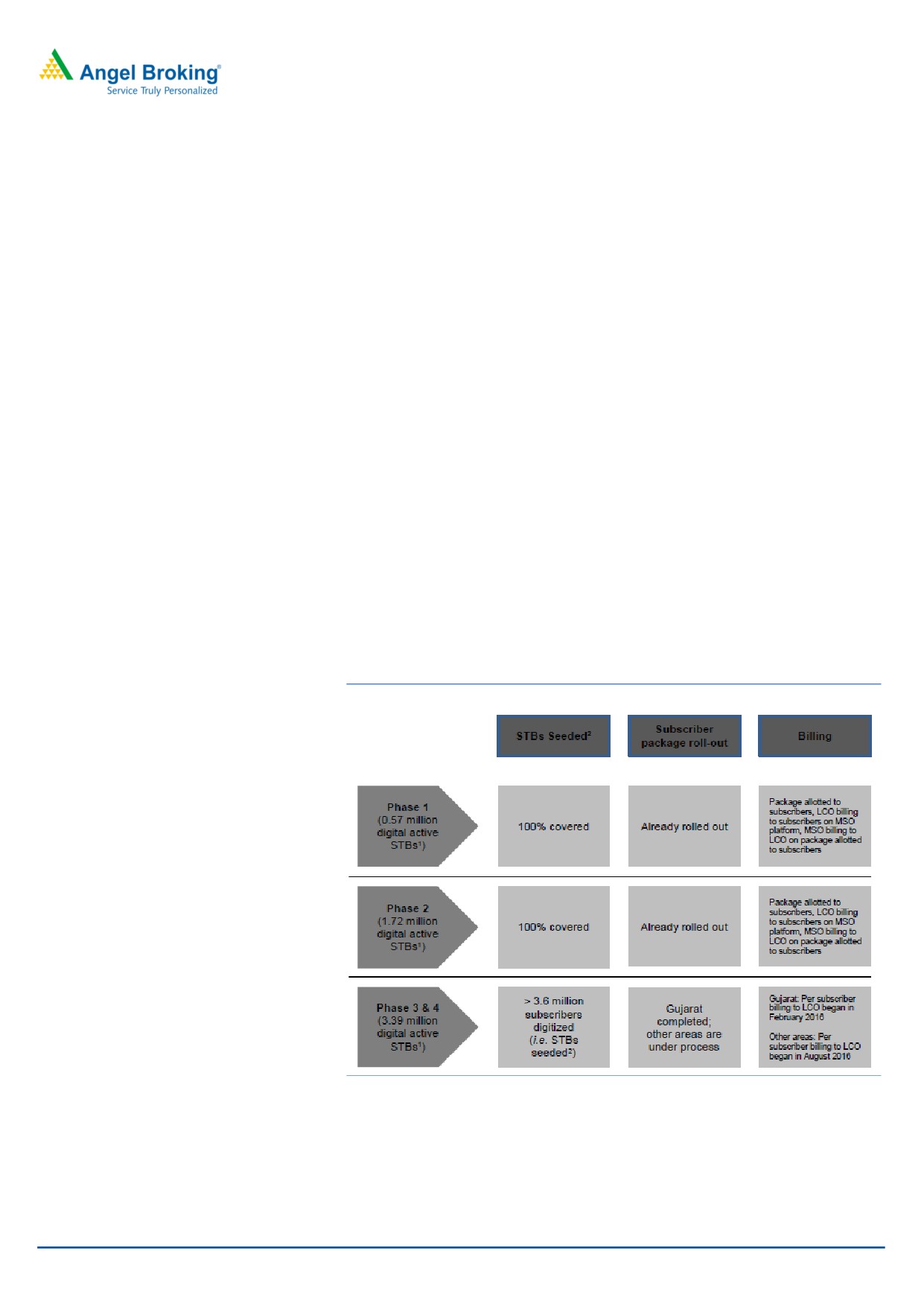

Strong traction on digitization

GTPL’s market position and industry expertise has provided it with the ability to

take advantage of the four-phased policy on digitization announced by the MIB

(Management Information Base), pursuant to which the cable television industry

must transition the distribution of channel signals in India to DAS (Direct Attached

Storage) by March 31, 2017, thereby requiring cable operators to transmit digital

signals through addressable STBs. In accordance with the digitization schedule set

out by the MIB, company has completed roll-out of STBs in Phase I, Phase II and

Phase III areas and is working towards completing the roll-out of STBs in Phase IV

areas.

Exhibit 3: Digitalization Schedule

Source: RHP, Angel Research

Successful track record of identifying, acquiring and integrating MSOs, ISOs and

LCOs

As on January 31, 2017, GTPL had active relationships with 14,606 LCOs.

Company had added 4,004 and 1,286 LCOs on a net basis in Fiscal 2016 and

June 20, 2017

5

GTPL Hathway | IPO Note

Fiscal 2015, respectively, and another 3,338 LCOs on a net basis in Fiscal 2017

through January 31, 2017. Company believes that its understanding of the cable

television distribution industry and its acquisition experience has enabled it to

identify and successfully acquire MSOs/ISOs/LCOs. Typically, company retains the

existing management of an MSO/ISO/LCO at the time company acquires its

majority interest, which allows it to leverage its existing relationships with

subscribers. In addition, company generally allows the senior management and

promoters of an acquired MSO/ISO/LCO to retain a significant minority interest,

which it believes aligns their long-term interest with GTPL. As employees of LCOs

often have established relationships with subscribers, company generally structures

its relationship such that the LCO continues to act as the principal contact with

subscribers in the relevant local area. In certain instances, company acquires the

cable television subscribers of LCOs, thereby enrolling them as primary subscribers

and allowing it direct subscriber access, which results in improved monetization

prospects. Company has implemented a range of training initiatives for employees

of LCOs, including training intended to improve their familiarity with services and

procedures, to help ensure that the LCOs provide subscribers with quality service.

Outlook and Valuation

In terms of valuation, GTPL’s P/BV multiple annualised 9MFY2017 at 3.1x,

compared to peers i.e. Den Networks 1.8x, Hathway Cable & Datacom 0.7x, Ortel

Comm. 1.4x, Siti Networks 4.8x. The cable industry is already undergoing a period

of weak performance and with disruptive pricing of new entrants, there is a high

probability that the performance may weaken further. Hence, we recommend

NEUTRAL rating on the issue.

Key risks

There are various proceedings involving Company, Directors, Subsidiaries,

Promoters and Group Companies, which if determined against them, may

adversely affect business.

The new tariff regime introduced by the Tariff Order may have a significant

impact on future ARPUs, pay TV economics, pricing model, operational

flexibility and results of operations.

The success of the company’s broadband services may be slowed or halted by

competition from wireless internet or fixed broadband offerings in India.

June 20, 2017

6

GTPL Hathway | IPO Note

Consolidated Income Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

9MFY17

Total operating income

453

577

623

845

689

% chg

26.6

27.4

7.9

35.6

-

Total Expenditure

346

421

474

580

486

License fees

260

318

352

414

329

Personnel

36

49

60

80

78

Others Expenses

51

54

61

86

79

EBITDA

107

156

149

264

203

% chg

51.1

46.0

(4.4)

77.3

(% of Net Sales)

23.6

27.0

24.0

31.3

29.5

Depreciation& Amortisation

29

72

84

104

102

EBIT

78

84

65

160.1

102

% chg

44.6

8.4

(22.6)

144.8

(% of Net Sales)

17.2

14.6

10.5

19.0

14.7

Interest & other Charges

20

40

42

46

43

Other Income

2

2

9

8

11

(% of PBT)

3.4

4.6

28.5

7.0

16.3

Recurring PBT

60

46

33

108

70

% chg

(23.4)

(28.6)

226.2

Tax

19

22

13

49

25

PAT (reported)

42

25

20

59

45

% chg

(41.1)

(17.4)

192.2

(% of Net Sales)

9.2

4.3

3.3

7.0

6.6

Basic & Fully Diluted EPS (Rs)

226.0

120.1

83.5

7.0

4.4

% chg

(46.9)

(30.4)

(91.6)

Source: RHP, Angel Research

June 20, 2017

7

GTPL Hathway | IPO Note

Consolidated Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

9MFY17

SOURCES OF FUNDS

Equity Share Capital

2

2

2

98

98

Reserves& Surplus

254

316

331

366

409

Shareholders Funds

255

318

333

464

508

Minority Interest

37

43

48

57

59

Total Loans

230

282

240

348

436

Deferred Tax Liability

12

22

28

43

43

Total Liabilities

534

666

649

912

1,046

APPLICATION OF FUNDS

Gross Block

1,261

1,446

1,445

1,645

1,845

Less: Acc. Depreciation

344

442

453

569

701

Net Block

480

674

696

917

1,004

Capital Work-in-Progress

23

22

11

61

62

Investments

4

9

15

9

6

Current Assets

286

354

393

467

577

Inventories

-

-

-

-

-

Sundry Debtors

121

199

228

245

326

Cash

46

40

61

83

97

Loans & Advances

77

97

72

108

108

Other Assets

42

18

32

30

46

Current liabilities

259

393

466

542

606

Net Current Assets

27

(39)

(73)

(75)

(29)

Deferred Tax Asset

0

0

0

0

3

Mis. Exp. not written off

-

-

-

-

-

Total Assets

534

666

649

912

1,046

Source: RHP, Angel Research

June 20, 2017

8

GTPL Hathway | IPO Note

Consolidated Cash Flow Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

9MFY17

Profit before tax

60

46

33

121

70

Depreciation

29

72

84

104

102

Change in Working Capital

(3)

72

77

50

(38)

Interest / Dividend (Net)

16

33

32

32

36

Direct taxes paid

(15)

(11)

(7)

(34)

(25)

Others

11

7

(10)

(4)

5

Cash Flow from Operations

99

218

209

271

150

(Inc.)/ Dec. in Fixed Assets

(225)

(265)

(97)

(375)

(166)

(Inc.)/ Dec. in Investments

2

3

1

9

10

Cash Flow from Investing

(223)

(263)

(96)

(366)

(155)

Issue of Equity

0

0

0

0

0

Inc./(Dec.) in loans

220

141

60

276

137

Others

(79)

(102)

(151)

(159)

(119)

Cash Flow from Financing

141

40

(92)

117

18

Inc./(Dec.) in Cash

16

(5)

21

22

13

Opening Cash balances

30

46

40

61

83

Closing Cash balances

46

40

61

13

97

Source: RHP, Angel Research

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

Valuation Ratio (x)

P/E (on FDEPS)

1.5

2.8

4.0

47.4

P/CEPS

0.8

0.7

0.6

18.5

P/BV

0.3

0.2

9.8

7.1

EV/Sales

0.5

0.5

5.5

4.2

EV/EBITDA

2.3

1.9

23.0

13.3

EV / Total Assets

0.5

0.5

5.3

3.9

Per Share Data (Rs)

EPS (Basic)

226.0

120.1

83.5

7.0

EPS (fully diluted)

226.0

120.1

83.5

7.0

Cash EPS

417.7

481.0

520.5

18.0

Book Value

1,277.4

1,589.3

33.9

47.2

Returns (%)

ROCE

16.1

14.1

11.4

19.7

Angel ROIC (Pre-tax)

17.9

15.3

13.2

22.2

ROE

16.3

7.7

6.1

12.8

Turnover ratios (x)

Inventory / Sales (days)

-

-

-

-

Receivables (days)

98

126

134

106

Payables (days)

27

29

38

27

Working capital cycle (ex-cash) (days)

70

96

96

79

Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

June 20, 2017

9

GTPL Hathway | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

June 20, 2017

10