FPO Note | Infrastructure

February 5, 2014

Engineers India

SUBSCRIBE

Issue Open: February 06, 2014

Attractively priced

Issue Close: February 10, 2014

Engineers India Ltd (EIL) is one of the leading design and engineering organizations

Issue Details

in South Asia. The company provides engineering consultancy and EPC services,

Face Value: `5

and is principally focused on the oil & gas and petrochemical industries.

Present Eq. Paid-up Capital: `169cr

Leadership position in project implementation in hydrocarbon business: EIL

Offer Size: 3.37cr Shares

has developed indigenous technology and expertise for offshore platforms,

oil & gas processing, oil refining, petrochemicals and pipeline projects over the

Post Eq. Paid-up Capital: `169cr

last 48 years enabling it to provide a gamut of management services from project

Issue size (amount): `489-506cr

conception to commissioning in hydrocarbon business. EIL’s leadership in project

implementation and long-term relationships with its clients gives it a competitive

Price Band: `145-150

advantage over its peers.

Discount to retail inv./employees: `6

Diversified operations across sectors and geographies: Over the years, the

Promoters holding Pre-Issue: 80.4%

company has diversified across various segments such as LNG, fertilizer, power,

Promoters holding Post-Issue: 70.4%

mining and metallurgy and infrastructure to encash the untapped infra

opportunity not only in Indian but globally (presence in Middle East, Africa, Asia

and South-east Asia) as well and has an excellent track record of achieving the

same. This will help the company to benefit from any recovery in the capex cycle

Post Issue Shareholding Pattern

both domestically and internationally.

Promoters Group

70.4

Healthy order inflows over past couple of quarters: The company has secured

MF/Banks/Indian

FIs/FIIs/Public &

orders worth `1,800cr (up 39.5 % yoy) in 9MFY2014, taking the order backlog to

Others

29.6

`3,820cr, implying an order backlog to sales ratio of 2.1x on a trailing basis. This

includes a major order worth US$139mn bagged from Dangote Group in

Nigeria for project management consultancy and EPC management.

Outlook and valuation: Although the company has reported weak revenues in

9MFY2014, the improvement in order inflows indicates recovery in revenue going

forward. At the lower and upper limit of the price-band of `145 and `150, the

stock is currently trading at valuations of 8.4x and 8.7x FY2015E Bloomberg EPS

respectively which is lower than its 3-year average PE of 14.8x. Considering EIL’s

dominance in the hydrocarbon business and attractive valuations, we recommend

Subscribe on the stock.

Key financials (Standalone)

Y/E March (` cr)

FY2010

FY2011

FY2012

FY2013

Net sales

1,994

2,823

3,699

2,506

% chg

30.1

41.6

31.0

(32.2)

Net profit (Adj.)

425

522

610

598

% chg

23.4

22.8

16.8

(1.9)

EBITDA margin (%)

24.7

22.8

19.1

23.4

EPS (`)

12.6

15.5

18.1

17.8

Viral Shah

P/E (x)

11.9

9.7

8.3

8.4

022-39357800 Ext: 6842

P/BV (x)

4.5

3.5

2.7

2.3

RoE (%)

34.2

40.8

37.1

29.3

RoCE (%)

38.6

48.7

41.2

27.9

Amit Patil

EV/Sales (x)

1.6

1.2

0.9

1.3

022-39357800 Ext: 6839

EV/EBITDA (x)

6.6

5.2

4.8

5.5

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Engineers India | FPO Note

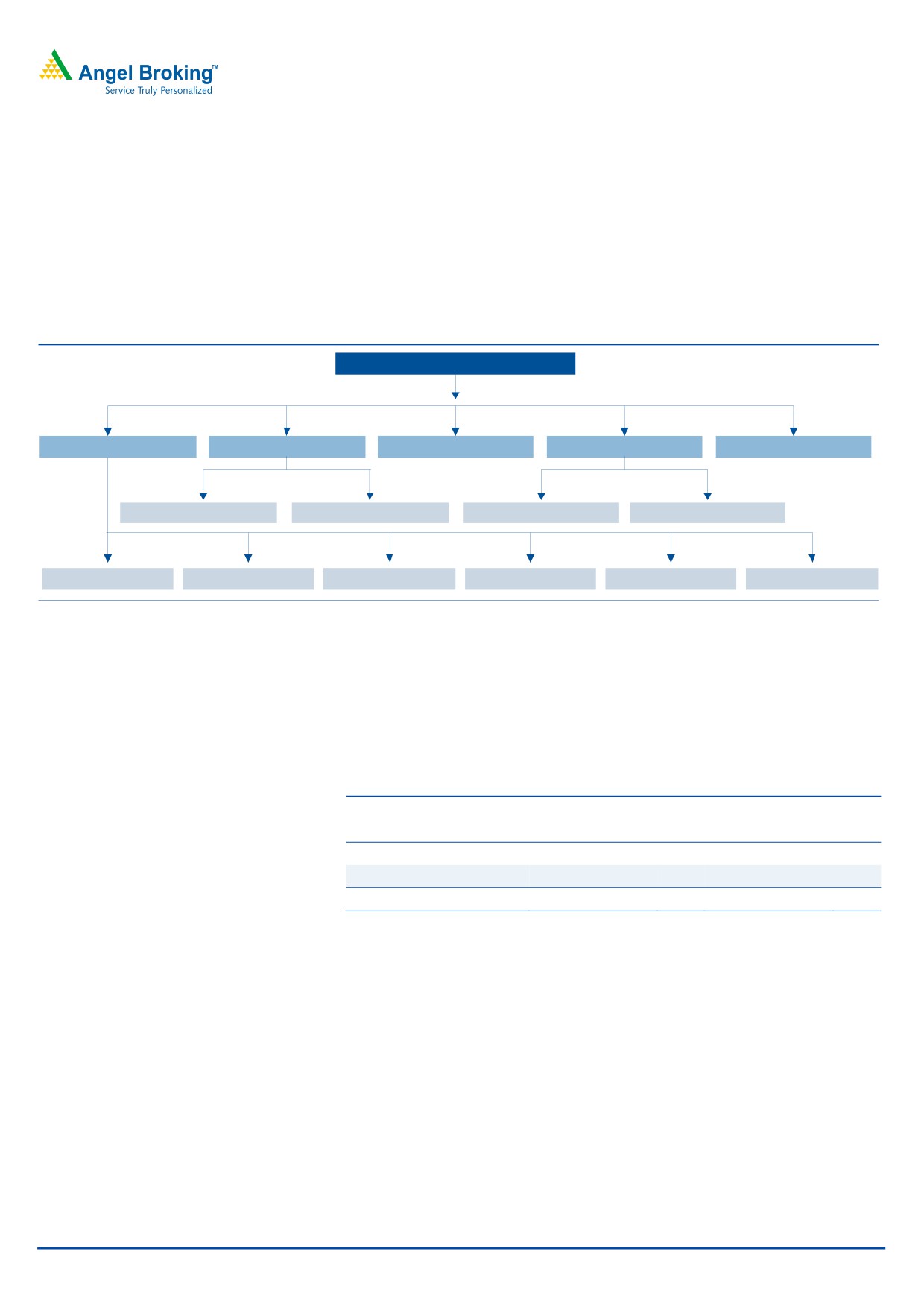

Company background

EIL is an engineering consultancy company which provides a gamut of

management services from project conception to commissioning which includes

design, engineering, procurement, construction and integrated project

management services. It also provides specialist services such as heat and mass

transfer equipment design, environmental engineering, specialist materials and

maintenance and plant operations and safety services.

Exhibit 1: Company various business sagments

ENGINEERS INDIA LTD

Hydrocarbon

Chemicals & Fertilizers

Mining & Metallurgy

Infrastructure

Power

Petrochemicals

Fertilizers

Infrastructure

Water & Waste Management

Petroleum Refining Onshore Oil & Gas Offshore Oil & Gas

Pipelines

Ports & Terminals

Strategic Storages

Source: Company, Angel Research

Issue details

The issue comprises an offer for sale of 3.37cr equity shares of face value of

`5 each. There is no fresh issue of equity. EIL has fixed the price band of the issue

at `145 to `150 and assigned a discount of `6/share on the issue price to the

retail investors and employees of the company.

Exhibit 2: Shareholding Pattern

Pre-Issue

Post-Issue

Particulars

No. of shares

(%)

No. of shares

(%)

Promoter and promoter group

270,900,540

80.4

237,206,880

70.4

Total public holding

66,036,060

19.6

99,729,720

29.6

Total

336,936,600

100.0

336,936,600

100.0

Source: Source: DRHP, Angel Research

February 5, 2014

2

Engineers India | FPO Note

Investment arguments

Leadership position in project implementation in hydrocarbon

business

EIL has developed indigenous technology and expertise for offshore platforms, oil

& gas processing, oil refining, petrochemicals and pipeline projects over the last

48 years, enabling it to provide a gamut of management services from project

conception to commissioning in hydrocarbon business. EIL’s leadership in project

implementation and long-term relationships with its clients gives it a competitive

advantage over its peers.

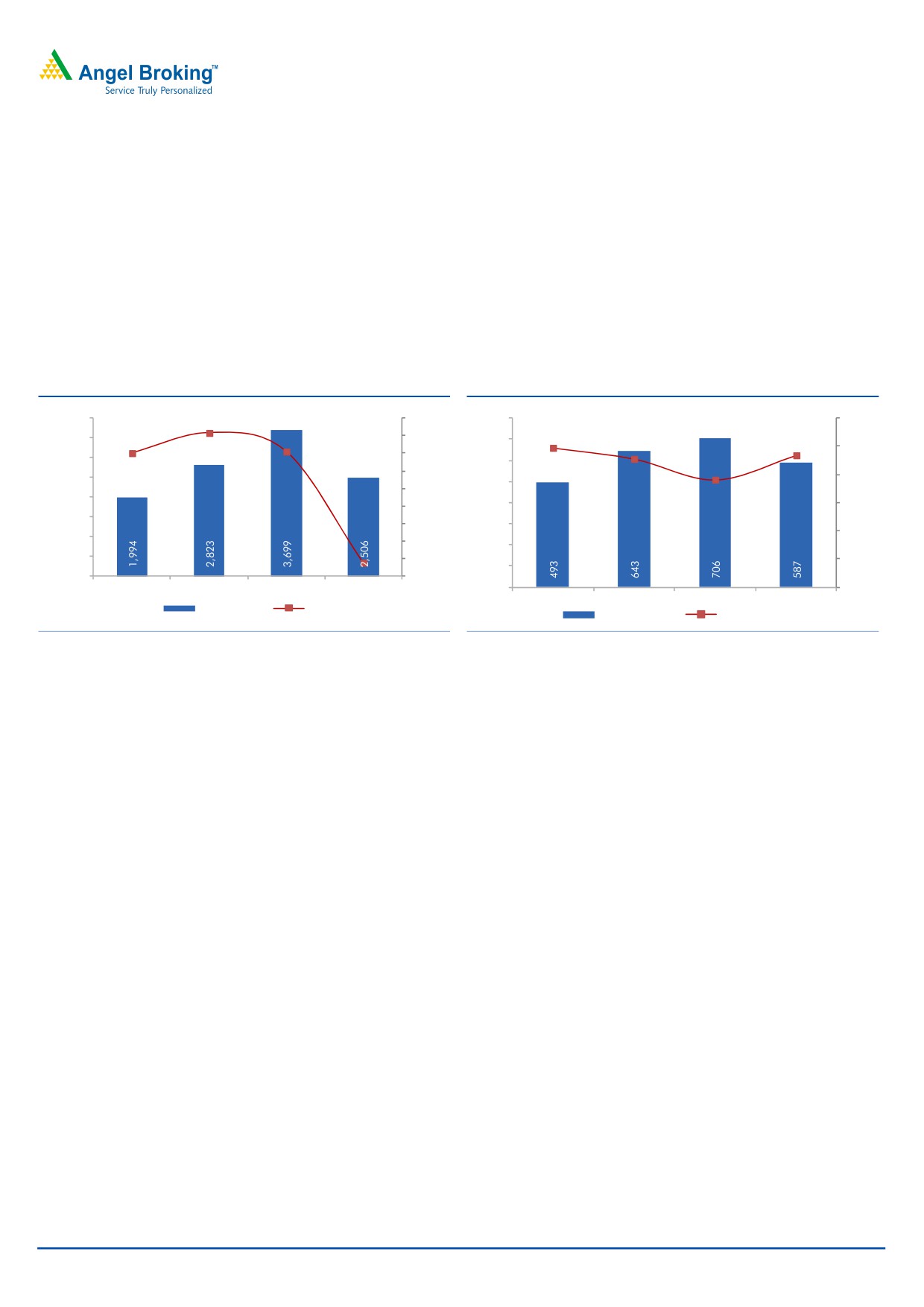

Exhibit 3: Revenue trend

Exhibit 4: EBITDA and EBITDAM

4,000

41.6

50.0

800

30.0

30.1

24.7

3,500

40.0

700

23.4

22.8

25.0

31.0

30.0

3,000

600

19.1

20.0

2,500

20.0

500

10.0

2,000

0.0

400

15.0

1,500

(10.0)

300

10.0

1,000

(20.0)

200

500

(32

.2)(30.0)

5.0

100

0

(40.0)

FY2010

FY2011

FY2012

FY2013

0

0.0

FY2010

FY2011

FY2012

FY2013

Sales (` cr)

% yoy chg

EBITDA (` cr)

EBITDAM (%)

Source: Company, Angel Research

Source: Company, Angel Research

Diversified operations across sectors and geographies

Over the years, the company has diversified across various segments such as LNG,

fertilizer, power, mining and metallurgy and infrastructure to encash the untapped

infra opportunity not only in Indian but globally (presence in Middle East, Africa,

Asia and South-east Asia) as well and has an excellent track record of achieving

the same. This will help the company to benefit from any recovery in the capex

cycle both domestically and internationally.

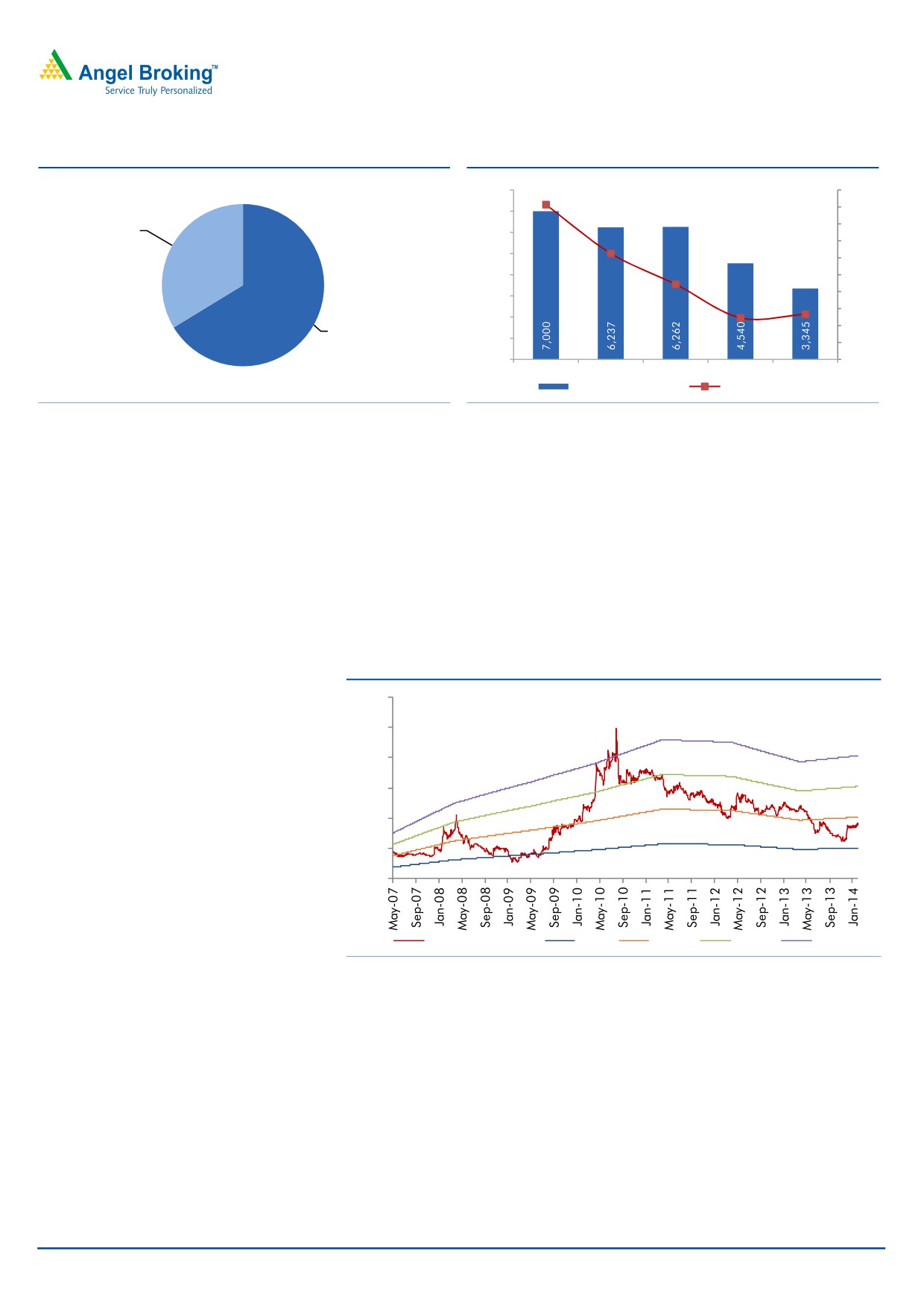

Healthy order inflows over past few quarters

The company has secured orders worth `1,800cr (up 39.5 % yoy) in 9MFY2014,

taking the order backlog to `3,820cr implying an order backlog to sales ratio of

2.1x on trailing basis. This includes a major order worth US$139mn bagged from

Dangote Group in Nigeria for project management consultancy and EPC

management.

February 5, 2014

3

Engineers India | FPO Note

Exhibit 5: Health order inflow of `1800cr in 9MFY14

Exhibit 6: Order backlog trend

8,000

4.6

5.0

3.1

4.5

7,000

2.2

LSTK, 29

4.0

6,000

3.5

5,000

1.2

3.0

4,000

1.3

2.5

3,000

2.0

1.5

2,000

Consultancy,

1.0

57

1,000

0.5

0

0.0

FY2009

FY2010

FY2011

FY2012

FY2013

Order book (` cr)

Order book/sales

Source: Company, Angel Research

Source: Company, Angel Research

Outlook and valuation

Although the company has reported weak revenues in 9MFY2014, the

improvement in order inflows indicates recovery in revenue going forward. At the

lower and upper limit of the price-band of `145 and `150, the stock is currently

trading at valuations of 8.4x and 8.7x FY2015E Bloomberg EPS respectively which

is lower than its 3-year average PE of 14.8x. Considering EIL’s dominance in the

hydrocarbon business and attractive valuations, we recommend Subscribe on the

stock.

Exhibit 7: 1-year forward P/E trend

600

500

400

300

200

100

0

Share Price (`)

6x

12x

18x

24x

Source: Angel Research, Bloomberg

Key concern

High dependence on government contracts

EIL bags a major portion of its order book from government entities funded by

government itself or multi-lateral development finance institutions. Hence, it is

remains susceptible to risks such as high regulatory scrutiny and delay in receipt of

collectibles.

February 5, 2014

4

Engineers India | FPO Note

Profit & Loss Statement (Standalone)

Y/E March (` cr)

FY2010

FY2011

FY2012

FY2013

Operating income

1,994

2,823

3,699

2,506

% chg

30.1

41.6

31.0

(32.2)

Total Expenditure

1,501

2,180

2,993

1,919

EBITDA

493

643

706

587

(% of Net Sales)

24.7

22.8

19.1

23.4

Depreciation& Amortization

13

15

19

11

EBIT

480

628

686

576

Interest & other Charges

3

4

4

1

Other Income

184

160

232

316

PBT

660

784

915

891

Tax

250

296

317

284

Deferred tax

(25)

(34)

(39)

(22)

PAT

435

523

636

629

Extraordinary items

10.3

0.4

26.5

30.2

Adjusted PAT

425

522

610

598

% chg

23.4

22.8

16.8

(1.9)

Basic EPS (`)

12.6

15.5

18.1

17.8

Balance Sheet (Standalone)

Y/E March (` cr)

FY2010

FY2011

FY2012

FY2013

SOURCES OF FUNDS

Equity Share Capital

56

168

168

168

Preference Capital

-

-

-

-

Reserves & Surplus

1,059

1,274

1,676

2,069

Shareholders’ Funds

1,115

1,442

1,844

2,238

Total Loans

-

-

-

-

Other liabilities

-

21

25

25

Total Liabilities

1,115

1,463

1,869

2,262

APPLICATION OF FUNDS

Net Block

60

60

53

50

Capital Work-in-Progress

12

13

52

136

Investments

101

512

635

653

Deferred Tax Asset

142

176

214

236

Current Assets

2,519

2,597

2,734

2,722

Cash

1,764

1,728

1,643

1,848

Loans & Advances

395

560

782

541

Inventories

43

1

1

1

Debtors

317

308

307

332

Current liabilities & Provisions

1,719

2,006

1,875

1,582

Net Current Assets

801

591

859

1,140

Other Assets

-

111

57

47

Total Assets

1,115

1,463

1,869

2,262

February 5, 2014

5

Engineers India | FPO Note

Cash Flow Statement (Standalone)

Y/E March (` cr)

FY2010

FY2011

FY2012

FY2013

Profit before tax

660

784

915

895

Depreciation

13

15

19

11

(Inc)/Dec in Working Capital

89

86

(299)

(45)

Others

(174)

(126)

(212)

(180)

Direct taxes paid

(233)

(266)

(317)

(240)

Cash Flow from Operations

355

493

107

441

(Inc.)/Dec.in Fixed Assets

(22)

(25)

(40)

(17)

(Inc.)/Dec. in Investments

228

(317)

108

(21)

Other income

-

-

-

-

Cash Flow from Investing

207

(342)

69

(38)

Issue of Equity

-

-

-

-

Inc./(Dec.) in loans

-

-

-

-

Dividend Paid (Incl. Tax)

(692)

(134)

(234)

(220)

Others

-

-

-

-

Cash Flow from Financing

(692)

(134)

(234)

(220)

Inc./(Dec.) in Cash

(131)

17

(59)

183

Opening Cash balances

1,894

1,764

1,728

1,643

Adjustments

(53)

(27)

22

Closing Cash balances

1,764

1,728

1,643

1,848

Key Ratios

Y/E March

FY2010

FY2011

FY2012

FY2013

Valuation Ratio (x)

P/E (on FDEPS)

11.9

9.7

8.3

8.4

P/CEPS

11.3

9.4

7.7

7.9

P/BV

4.5

3.5

2.7

2.3

EV/Sales

1.6

1.2

0.9

1.3

EV/EBITDA

6.6

5.2

4.8

5.5

Per Share Data (Rs)

EPS (Basic)

12.6

15.5

18.1

17.8

Cash EPS

13.3

15.9

19.5

19.0

Book Value

33.1

42.8

54.7

66.4

Returns (%)

RoCE (Pre-tax)

38.6

48.7

41.2

27.9

RoE

34.2

40.8

37.1

29.3

Solvency ratios (x)

Net debt to Equity

(1.6)

(1.2)

(0.9)

(0.8)

Net debt to EBITDA

(3.7)

(2.7)

(2.3)

(3.2)

February 5, 2014

6

Engineers India | FPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

February 5, 2014

7

Engineers India | FPO Note

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Bhavesh Chauhan

Sr. Analyst (Metals & Mining)

Viral Shah

Sr. Analyst (Infrastructure)

V Srinivasan

Analyst (Cement, FMCG)

Yaresh Kothari

Analyst (Automobile)

Ankita Somani

Analyst (IT, Telecom)

Sourabh Taparia

Analyst (Banking)

Bhupali Gursale

Economist

Vinay Rachh

Research Associate

Amit Patil

Research Associate

Twinkle Gosar

Research Associate

Tejashwini Kumari

Research Associate

Akshay Narang

Research Associate

Harshal Patkar

Research Associate

Nishant Sharma

Research Associate

Technicals:

Sameet Chavan

Technical Analyst

Derivatives:

Siddarth Bhamre

Head - Derivatives

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Production Team:

Tejas Vahalia

Research Editor

Dilip Patel

Production

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE: INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

February 5, 2014

8