OFS Note | Mining

January 30, 2015

Coal India Ltd.

SUBSCRIBE

Issue Open: January 30, 2015

Attractively Priced

Issue Close: January 30, 2015

Incorporated in 1973, Coal India Ltd (CIL) is the largest coal producer in the

Issue Details

world with reserves of

65bn tonnes. The company produced

462MT and

dispatched 472MT of raw coal in FY2014. CIL accounts for 81.1% of India's

Face Value: `10

overall coal production and commands ~74% of the Indian coal market. The

Present Eq. Paid-up Capital: `6,316cr

company has 429 mines of which 237 are underground, 166 opencast and 26

Offer Size: 63.16cr Shares

are mixed mines.

Post Eq. Paid-up Capital: `6,316cr

Volume growth to drive revenues: The coal ministry is making all efforts to

resolve issues related to various mining projects. For the first time, the government

Issue size (amount): `22,386cr

will be drawing mine-wise plans to help CIL achieve production targets. The

OFS Floor Price: `358

government is also showing strong signs of acting swiftly on important reforms,

Retail Discount: 5%

such as land acquisition. Although, we do not expect CIL to achieve its production

OFS Floor Price (Retail): `340

growth target of 12.2% (CAGR) over FY2014-20, with such support from the

government, we expect production to grow at a CAGR of ~8% over FY2014-20,

Post-issue implied market cap: `238,948cr

much higher than its historical CAGR of just 2.8% over FY2009-14.

Promoters holding Pre-Issue: 89.7%

Operating efficiencies and low realisations to help improve margins:

Promoters holding Post-Issue: 79.7%

CIL’s net realisation is significantly lower than the landed price of imported coal,

providing enough cushion against any decline in international coal prices. The

Post Issue Shareholding Pattern

gap also provides ample scope for CIL to pass on any cost escalations. The

increasing share of washed coal will also help improve realisations. Further,

Promoters Group

79.7

technological and infrastructural enhancements, coupled with operating

MF/Banks/Indian

FIs/FIIs/Public &

efficiencies from rising production will help to keep production costs low.

Others

20.3

Outlook and valuation: At the offer-for-sale (OFS) price of `358, the stock is

available at ~11.4x the consensus FY2017E EPS of `31.4. Retail shareholders will

get an additional discount of 5%, implying an OFS price of `340. At the OFS

price for retail bidders, the stock is available at a P/E ratio of 10.8x consensus

FY2017E EPS, which is attractive. We also believe, post issue, the overhang of the

share sale on the price will be gone. Hence, we recommend investors to apply for

CIL shares in the OFS.

Key financials (Consolidated)

Y/E March (` cr)

FY11

FY12

FY13

FY14

Net sales

50,229

62,415

68,303

68,810

% chg

12.6

24.3

9.4

0.7

Net profit

10,867

14,788

17,356

15,112

% chg

12.9

36.1

17.4

(12.9)

FDEPS (`)

17.2

23.5

27.6

23.9

OPM (%)

26.8

25.1

26.5

23.2

P/E (x)

22.0

16.1

13.7

15.8

P/BV (x)

7.2

5.9

4.9

5.6

RoE (%)

36.8

40.1

39.0

33.3

RoCE (%)

37.5

35.8

35.6

30.3

Rahul Dholam

EV/Sales (x)

4.0

3.1

2.7

2.6

Tel: 022- 39357600 Ext: 6847

EV/EBITDA (x)

15.0

12.4

10.1

11.1

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Coal India | OFS Note

Company Background

Incorporated in 1973, Coal India Ltd is the largest coal producer in the world with

reserves of 65bn tonnes. The company produced 462MT and dispatched 472MT

of raw coal in FY2014. CIL accounts for 81.1% of India's overall coal production

and commands nearly 74% of the Indian coal market. Coal operations are

primarily carried out across 82 mining areas through its seven wholly owned

subsidiaries, spread across 8 provincial states of India. The company has 429

mines of which 237 are underground, 166 opencast and 26 are mixed mines. CIL

also operates 17 coal washeries (13 coking coal and 4 non-coking coal) with a

total capacity of 39.4MTY.

With more than 60% of the country’s installed power capacity being coal based,

the power sector accounts for ~75% of the coal off take. CIL accounts for ~76% of

total thermal power generating capacity of the Utility sector.

The company was granted the 'Maharatna' status on 11 April, 2011 by the

Government of India making it the 5th PSU in the country, of a total of 215 public

sector companies, to have been conferred with this status.

Issue Details

The Promoter (Government of India), proposes to sell 31,58,18,220 equity shares

of face value of `10 each representing 5% of the total paid up equity share capital

of the company, with an option to sell an additional 5% stake. CIL has fixed the

OFS floor price at `358 per share (at a 5.4% discount to its closing price as on

January 29, 2015). Retail shareholders will get an additional discount of 5%,

implying a floor price of `340. For the first time, 20% of the issue is reserved for

retail investors, as against the minimum requirement of 10%.

Exhibit 1: Shareholding Pattern

Pre-Issue

Post-Issue

Particulars

No. of shares

(%)

No. of shares*

(%)

Promoter and promoter group

5,66,26,90,126

89.7

5,03,10,53,686

79.7

Total public holding

65,36,74,274

10.3

1,28,53,10,714

20.3

Total

6,31,63,64,400

100

4,13,05,25,289

100

*Assuming issue of the optional shares

Source: Company, Angel Research

January 30, 2015

2

Coal India | OFS Note

Investment rationale

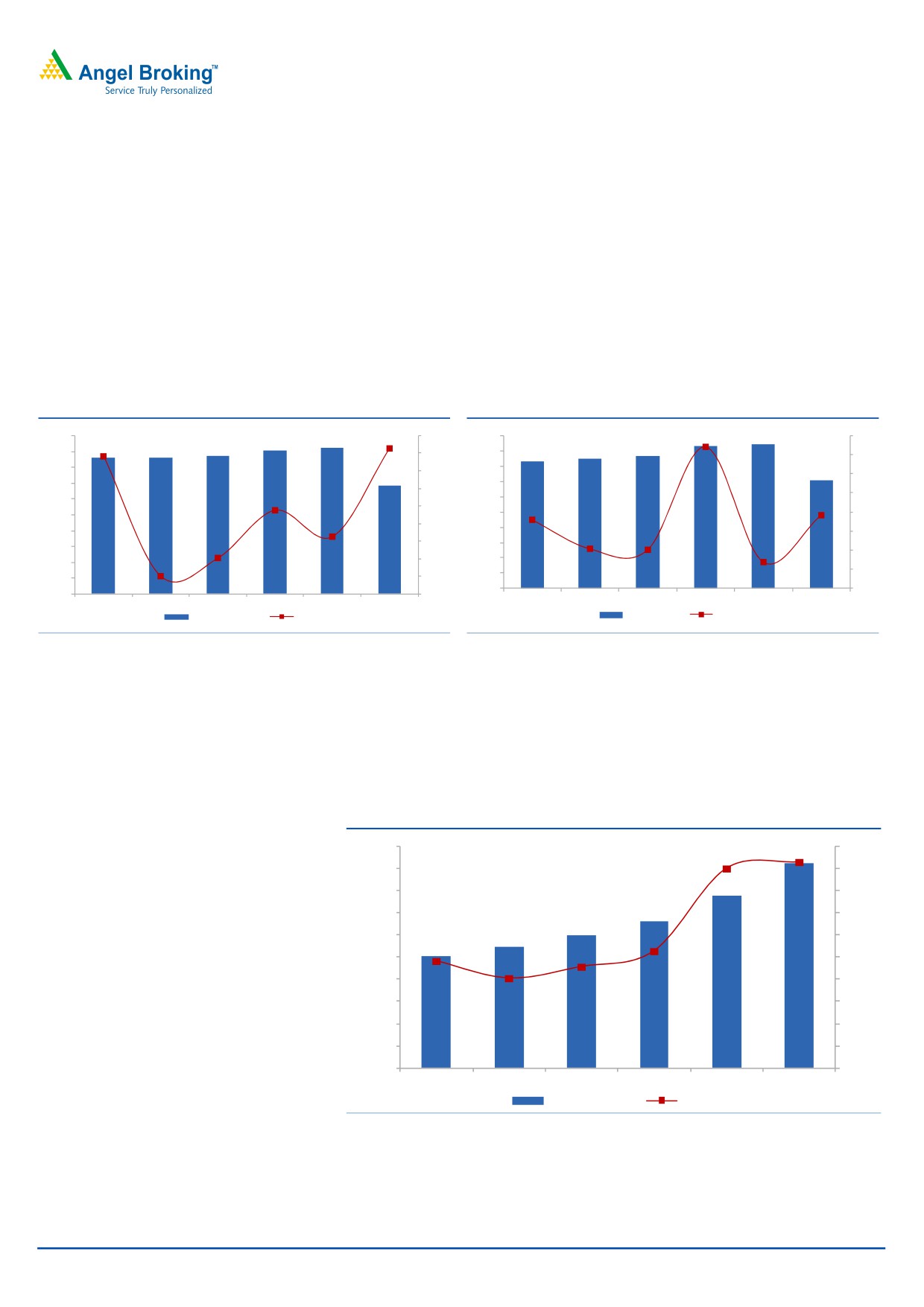

Strong production growth to drive revenues

Coal India’s production increased 7.3% yoy in 9MFY2015 to 355MT, as against a

muted growth of 2.3% in FY2014. Two of its subsidiaries, Mahanadi Coalfields

and Western Coalfields, which account for 1/3rd of its production, expect double

digit growth in output this fiscal, as they use more sophisticated machinery and

expand mines. Off take growth also picked up to 3.8% yoy in 9MFY2015 as

against 1.4% in FY2014. Production and offtake growth jumped significantly in

3Q2015 at 10.7% and 6.3% yoy, respectively after a muted 1H2015.

Exhibit 2: Production (MT)

Exhibit 3: Offtake (MT)

500

462

8.0

500

465

472

8.0

452

431

431

436

433

450

7.3

450

416

425

7.4

6.8

7.0

7.0

400

400

355

342

6.0

6.0

350

350

5.0

5.0

300

300

3.8

4.0

250

4.0

250

3.6

3.8

3.0

200

200

3.0

2.3

2.0

150

150

2.1

2.0

2.0

1.0

1.0

100

100

0.0

1.4

1.0

50

0.0

50

0

0.0

0

-1.0

FY10

FY11

FY12

FY13

FY14

9M15

FY10

FY11

FY12

FY13

FY14

9M15

Production (MT)

Growth (%)

Offtake (MT)

Growth (%)

Source: Company

Source: Company

According to the coal ministry, with rising demand for power, demand for coal is

estimated to increase to 1.6 billion tonnes by the year FY2020. CIL has already

finalised plans to achieve targeted production of 925MT by FY2020 and is

planning to increase production to 1bn tonne. The target production implies a

12.2% CAGR growth in production over FY2014-20.

Exhibit 4: Coal India Production Target

1000

18.0

925

20.0

900

18.0

18.6

780

800

16.0

661

700

14.0

598

600

548

12.0

507

10.5

500

10.0

400

9.6

9.1

8.0

8.1

300

6.0

200

4.0

100

2.0

0

0.0

FY15E

FY16E

FY17E

FY18E

FY19E

FY20E

Production (MT)

Growth (%)

Source: Company

We believe the production growth target is a bit too optimistic. However, we

believe production growth will definitely inch up going forward, as compared to

the muted growth over recent years. The company has consistently missed its

January 30, 2015

3

Coal India | OFS Note

production targets with a CAGR of just 2.8% over the FY2009-14 period, largely

due to its inability to start new projects or increase capacity at existing mines on

account of land acquisition issues. CIL’s new blocks, which are expected to

contribute ~115MT of the additional production, are stuck in land acquisition

hurdles with delays ranging from 2-7 years.

Exhibit 5: Production Vs Target

490

99%

482

480

98%

98%

98%

470

97%

98%

464

462

460

452

97%

447

450

440

97%

440

436

431

96%

96%

430

96%

420

410

95%

400

95%

FY11

FY12

FY13

FY14

Target (MT)

Production (MT)

Achieved (%)

Source: Company

The government is showing strong signs of acting swiftly on important reforms,

such as land acquisition. The coal ministry is also making all efforts to resolve

issues related to various mining projects. For the first time, the government will be

drawing mine-wise plans, to help CIL achieve its production targets. With such

strong support from the government, we expect CIL’s production to grow at a

CAGR of ~8% during FY2014-20 as against the target of 12.2%.

Operating efficiencies and low realisations to help improve margins

CIL’s net realisation was $24 per tonne in FY2014, significantly lower than the

landed price of imported coal. This gap provides enough cushion against any

decline in international coal prices. The gap also provides ample scope for CIL to

pass on any cost escalations and maintain margins.

The company also plans to add 16 coal washeries, which will increase its coal

washing capacity from 39.4MTY to 140MTY. Construction job of three washeries

are in progress and two washeries have been awarded. The increasing share of

washed coal will help drive realisations for the company.

CIL is one of the lowest cost producers of coal (~$19 per tonne), with 90% of

production through open cast mining. The company plans to improve productivity

in its mines through upgradation of technology, with installation of high capacity

equipments. In addition, the company plans to install continuous miner technology

on a large scale, long-wall technology at selected mines, man riding system in

major mines and tele-monitoring techniques in their underground mines. The

company also plans to pursue implementation of e-procurement to secure

equipment and spare part supplies; as well as use of e-tender systems to manage

works, services and other operations.

January 30, 2015

4

Coal India | OFS Note

The coal ministry is pushing to ensure timely completion of the three railways lines

(Jharkhand, Odisha & Chattisgarh), which have a potential to add another 200-

300MT of traffic capacity. CIL has already provided `300cr to Railways for these

projects, which have a total outlay of `7,500cr. These projects, aimed at increasing

the output from CIL mines in these states, are getting delayed mainly on account of

forest clearance and land acquisition issues.

The technological and infrastructural improvements, coupled with operating

efficiencies from rising production will help to keep production costs low.

Outlook and valuation

We expect CIL earnings to grow at a fast clip led by 1) Strong domestic demand

from power, steel and cement 2) Aggressive targets to drive production growth

with support from the new Government 3) Huge pricing gap between realisations

and landed cost of imported coal

4) Infrastructure and technological

enhancements, increase in coal washing capacities helping improve margins.

At the OFS price of `358, the stock is available at ~11.4x the consensus FY2017E

EPS of `31.4, which is attractive. Retail shareholders will get an additional discount

of 5%, implying an OFS price of `340. At the OFS price for retail bidders, the stock

is available at a P/E ratio of 10.8x consensus FY2017E EPS. We also believe, post

issue, the overhang of the share sale on the price will be gone. Hence, we

recommend investors to apply for CIL shares in the OFS.

January 30, 2015

5

Coal India | OFS Note

Profit & loss statement (Consolidated)

Y/E March (` cr)

FY11

FY12

FY13

FY14

Gross sales

60,241

78,410

88,281

89,375

Less: excise duty

10,012

15,995

19,979

20,564

Net sales

50,229

62,415

68,303

68,810

Other operating income

-

-

-

-

Total operating income

50,229

62,415

68,303

68,810

% chg

12.6

24.3

9.4

0.7

Total expenditure

36,752

46,748

50,219

52,847

Net raw materials

5,273

5,504

6,062

7,022

Power & Fuel

1,749

2,013

2,333

2,282

Personnel

18,932

26,387

27,321

27,769

Other

10,798

12,844

14,503

15,773

EBITDA

13,478

15,668

18,084

15,963

% chg

27.9

16.3

15.4

(11.7)

(% of net sales)

26.8

25.1

26.5

23.2

Depreciation

1,765

1,969

1,813

1,996

EBIT

11,712

13,699

16,271

13,967

% chg

27.2

17.0

18.8

(14.2)

(% of net sales)

23.3

21.9

23.8

20.3

Interest expenses

74

54

45

58

Other income

4,872

7,537

8,747

8,969

(% of PBT)

41.9

55.2

53.9

64.5

Recurring PBT

16,511

21,182

24,972

22,878

% chg

17.8

28.3

17.9

(8.4)

Extraordinary inc/(expense)

(47)

91

7

1

PBT (reported)

16,463

21,273

24,979

22,880

Tax

5,596

6,484

7,623

7,768

(% of PBT)

34.0

30.5

30.5

34.0

PAT (reported)

10,867

14,788

17,356

15,112

Add: Share of earnings of asso.

-

-

-

-

Less: Minority interest

-

-

-

0.04

Discontinued operations

(0.01)

(0.01)

(0.01)

(0.01)

PAT after MI (reported)

10,867

14,788

17,356

15,112

Adj. PAT after MI

10,915

14,697

17,350

15,110

% chg

12.8

34.7

18.0

(12.9)

(% of net sales)

19.3

17.5

21.5

25.2

Basic EPS (`)

17.19

23.47

27.63

23.92

FDEPS (`)

17.19

23.47

27.63

23.92

% chg

12.9

36.5

17.7

(13.4)

January 30, 2015

6

Coal India | OFS Note

Balance sheet (Consolidated)

Y/E March (` cr)

FY11

FY12

FY13

FY14

SOURCES OF FUNDS

Equity Share Capital

6,316

6,316

6,316

6,316

Reserves & Surplus

26,998

34,137

42,156

36,088

Shareholders Funds

33,314

40,453

48,472

42,404

Minority Interest

33

54

64

64

Total Loans

1,334

1,305

1,078

171

Other Long term liabilities

2,057

2,647

3,137

3,529

Long Term Provisions

22,461

28,271

31,144

33,639

Total Liabilities

59,199

72,730

83,895

79,807

APPLICATION OF FUNDS

Gross Block

36,714

38,096

39,011

40,897

Less: Acc. Depreciation

23,871

24,656

25,545

26,302

Net Block

12,843

13,440

13,466

14,595

Capital Work-in-Progress

2,057

2,903

3,496

4,505

Goodwill

-

-

-

-

Investments

851

947

1400

1188

Deferred Tax Assets

873

1194

2255

1972

Long Term loans and adv.

845

1,017

1,181

1,164

Other non- current assets

76

69

74

593

Current Assets

68,318

87,415

88,423

80,227

Cash

45,806

58,203

62,236

52,390

Loans & Advances

11,180

13,478

4,920

6,596

Other

11,332

15,734

21,267

21,241

Current liabilities

26,666

34,256

26,401

24,435

Net Current Assets

41,652

53,159

62,022

55,792

Mis. Exp. not written off

-

-

-

-

Total Assets

59,199

72,730

83,895

79,807

January 30, 2015

7

Coal India | OFS Note

Cash flow statement (Consolidated)

Y/E March (` cr)

FY11

FY12

FY13

FY14

Profit before tax

16,463

21,273

24,979

22,880

Depreciation

1,765

1,969

1,839

1,996

Change in Working Capital

(4,328)

3,565

(6,839)

244

Less: Other income

427

(214)

(2,218)

(1,769)

Direct taxes paid

(5,623)

(6,704)

(8,652)

(8,826)

Cash Flow from Operations

8,704

19,888

9,109

14,525

(Inc.)/ Dec. in Fixed Assets

(2,568)

(3,409)

(2,454)

(4,116)

(Inc.)/ Dec. in Investments

218

(11,219)

(5,022)

6,221

(Inc.)/ Dec. in loans and adv.

0

0

0

0

Other income

3,390

4,218

5,643

6,475

Cash Flow from Investing

1,040

(10,410)

(1,833)

8,580

Issue of Equity

0

0

0

0

Inc./(Dec.) in loans

(577)

(301)

(274)

(1,321)

Dividend Paid (Incl. Tax)

(2,583)

(7,429)

(7,907)

(24,243)

Others

144

348

329

214

Cash Flow from Financing

(3,017)

(7,382)

(7,852)

(25,350)

Inc./(Dec.) in Cash

6,728

2,095

(575)

(2,246)

Opening Cash balances

39,078

10,165

12,260

11,685

Closing Cash balances

45,806

12,260

11,685

9,439

January 30, 2015

8

Coal India | OFS Note

Key Ratios (Consolidated)

Y/E March

FY11

FY12

FY13

FY14

Valuation Ratio (x)

P/E (on FDEPS)

22.0

16.1

13.7

15.8

P/CEPS

18.8

14.3

12.5

14.0

P/BV

7.2

5.9

4.9

5.6

Dividend yield (%)

1.0

2.6

3.7

7.7

EV/Sales

4.0

3.1

2.7

2.6

EV/EBITDA

15.0

12.4

10.1

11.1

EV / Total Assets

3.4

2.7

2.2

2.2

Per Share Data (`)

EPS (Basic)

17.2

23.5

27.6

23.9

EPS (fully diluted)

17.2

23.5

27.6

23.9

Cash EPS

20.1

26.4

30.3

27.1

DPS

3.9

10

14

29

Book Value

52.7

64.0

76.7

67.1

Dupont Analysis

EBIT margin

23.3

21.9

23.8

20.3

Tax retention ratio (%)

66.0

69.5

69.5

66.0

Asset turnover (x)

0.8

0.9

0.8

0.9

ROIC (Post-tax)

13.1

13.1

13.5

11.6

Cost of Debt (Post Tax)

2.9

2.8

2.6

6.1

Leverage (x)

1.8

1.8

1.7

1.9

Operating RoE

31.1

31.6

32.2

21.8

Returns (%)

RoCE (Pre-tax)

37.5

35.8

35.6

30.3

RoE

36.8

40.1

39.0

33.3

Turnover ratios (x)

Asset Turnover (Gross Block)

1.4

1.7

1.8

1.7

Inventory / Sales (days)

49.6

45.5

42.5

38.6

Receivables (days)

20.3

26.6

43.1

49.7

Payables (days)

6.4

5.8

6.1

5.7

Solvency ratios (x)

Net debt to equity

(1.4)

(1.3)

(1.4)

(1.3)

Net debt to EBITDA

(2.8)

(2.8)

(3.1)

(3.8)

January 30, 2015

9

Coal India | OFS Note

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Angel Broking Pvt. Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Pvt. Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking

or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or

in the past.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Coal India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to -15%)

Sell (< -15%)

January 30, 2015

10

Coal India | OFS Note

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research (Banking)

Amarjeet Maurya

Analyst (FMCG, Media, Mid-Cap)

Bharat Gianani

Analyst (Automobile)

Rahul Dholam

Analyst (Metal, Oil & Gas)

Santosh Yellapu

Analyst (Infrastructure)

Shrenik Gujrathi

Analyst (Cap Goods, Cement)

Umesh Matkar

Analyst (Banking)

Twinkle Gosar

Analyst (Mid-Cap)

Tejas Vahalia

Research Editor

Technicals and Derivatives:

Siddarth Bhamre

Head - Technical & Derivatives

Sameet Chavan

Technical Analyst

Sneha Seth

Associate (Derivatives)

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Assistant Manager

Production Team:

Dilip Patel

Production Incharge

CSO & Registered Office: G-1, Ackruti Trade Centre, Road No. 7, MIDC, Andheri (E), Mumbai - 93. Tel: (022) 3083 7700. Angel Broking Pvt. Ltd: BSE Cash: INB010996539 / BSE F&O: INF010996539, CDSL Regn. No.: IN - DP - CDSL - 234 - 2004, PMS Regn. Code: PM/INP000001546, NSE Cash: INB231279838 /

NSE F&O: INF231279838 / NSE Currency: INE231279838, MCX Stock Exchange Ltd: INE261279838 / Member ID: 10500. Angel Commodities Broking (P) Ltd.: MCX Member ID: 12685 / FMC Regn. No.: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn. No.: NCDEX / TCM / CORP / 0302.

January 30, 2015

11