IPO Note | Other Telecom Services

June 13, 2017

Tejas Networks Limited

SUBSCRIBE

sue Open: June 14, 2017

Is

Issue Close: June 16, 2017

Tejas Networks Ltd (TNL) is an optical and data networking products company. It

designs, develops and sells products to telecommunications & internet service

providers, utility companies, defense companies and government entities in India and

Issue Details

over 60 countries. TNL derives 63% of its revenues from domestic markets, while rest

comes from international markets. As of May 15, 2017, the company had 313

Face Value: `10

employees in its R&D team and had filled 333 patents applications across the globe,

out of which 56 patents have been granted.

Present Eq. Paid up Capital: `74cr

Rise in optical network capex expected: Less than 20% of cell towers in India are

Offer for Sale: **1.27cr Shares

connected with fibre, as compared to 70-80% in developed countries. In our view, the

optical network capex in India is likely to grow at 14% CAGR over FY2014-20.

Fresh issue: `450 cr

Further, evaluation of high speed internet technologies would require existing telcos to

upgrade network capacities for higher data traffic domestically as well as globally.

Post Eq. Paid up Capital: `91.52cr

Government’s push for ‘Digital India’ to further strengthen business: We believe that

government’s push for ‘Digital India’ through projects such as the National Optical

Fibre Network (BharatNet, where 250,000 gram panchayats would be connected

Issue size (amount): *`755cr -**776 cr

through optical fibres), and Smart Cities will provide better growth opportunities for

business. In addition, policies such as ‘Make in India’ and ‘Preferential Market Access

Price Band: `250-257

Policy’ would further benefit TNL’s business prospects.

Favorably placed to capture the industry growth: We believe that TNL would benefit

Lot Size: 55 shares and in multiple

from the industry growth owing to - (1) Leadership position in the fast growing Indian

thereafter

optical equipment market (2nd, 15% market share); (2) Strong professional team with

Post-issue implied mkt. cap: *`2239cr -

significant industry experience; (3) High product reliability, as it delivered <15 min

**`2301cr

down time a year since 2008; (4) Expanding exports into markets with similar

economic pattern as India i.e. South East Asia, Latin America, Africa, etc. (5) Less

Instituional Investor Pre-Issue: 100%

competition owing to high entry barriers related to huge initial investment in R&D; and

(6) An end-to-end portfolio of optical networking products for access, metro and long-

haul networks.

*Calculated on lower price band

Strong operating leverage with asset light business: Going forward, we expect TNL to

benefit from operating leverage, as the company has achieved necessary scale

** Calculated on upper price band

required in R&D. Further, company is adopting an asset light strategy by outsourcing

most of its manufacturing to reputed electronics manufacturing services companies.

Book Building

Therefore, Its ROE has improved from 8% in FY2016 to 12.9% for FY2017, and we

believe it will strengthen going ahead.

QIBs

75% of issue

Outlook and Valuation: TNL has reported strong revenue CAGR of 24.2% CAGR over

Non-Institutional

15% of issue

FY2013-17 and PAT of `64cr in FY2017 (loss of `79cr in FY2013). The RoE improved

from 8% in FY2016 to 12.9% in FY2017, primarily owing to ongoing capex on Optical

Retail

10% of issue

Network by Telcos, strong operating leverage with asset light business and strong

professional team with significant industry experience. At the upper end of the price

band, the pre-issue P/E works out to be 29.3x its 2017 earnings, 3.7x of FY2017 Book

Value. Moreover, the company’s debt free balance sheet post IPO coupled with the

Post Issue Shareholding Patter

government’s push for digital India would support the growth momentum. Thus, we

Instituitional Investor

66%

recommend a SUBSCRIBE on the issue.

Others

34%

Key Financials

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

Net Sales

423

387

627

878

% chg

14.6

(8.6)

62.2

40.0

Net Profit

3

(18)

29

64

% chg

-

-

-

122.4

EBITDA (%)

22.4

17.7

18.0

19.8

EPS (Rs)

0.4

(2.5)

4.0

8.8

P/E (x)

667

(104)

64

29

P/BV (x)

5.7

5.6

5.1

3.7

RoE (%)

0.9

(5.4)

8.0

12.9

Jaikishan J Parmar

RoCE (%)

6.7

3.6

12.2

16.2

+022 39357600, Extn: 6810

EV/Sales (x)

4.9

5.2

3.2

2.3

EV/EBITDA (x)

22.0

29.5

18.0

11.5

Source: Company, Angel Research; Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

Please refer to important disclosures at the end of this report

1

Tejas Networks Ltd| IPO Note

Company background

Tejas Network Ltd is an India based optical and data networking products

company with customers in over 60 countries. TNL designs, develops and sells

high performance and cost competitive products to telecommunication service

providers, internet service providers, utility companies, defence companies and

government entities (collectively, “Communication Service Providers”). The products

are used to build high-speed communication networks that carry voice, data and

video traffic from fixed line, mobile and broadband networks over optical fibre.

The products use programmable software-defined hardware architecture with a

common software code-base that delivers an app-like ease of development and

upgradation of new features and technology standards. Currently, India is the

largest geographic segment (in terms of revenue) and we believe TNL is well

positioned to take advantage of the growth opportunities arising out of ‘Digital

India’ and ‘Make-in-India’ programs of the Indian Government.

For the year ended March 31, 2016, TNL was the second largest optical

networking products company in terms of market share in India, with a market

share of 15% in the overall optical networking market. (Source: Ovum Market

Share Spreadsheet: 1Q16 ON Subregional EMEA and AP, published in June

2016).

Exhibit 1: Tejas Network products get used at

Source: Company, Angel Research,RHP

June 13, 2017

2

Tejas Networks Ltd| IPO Note

The current product portfolio targets access networks (i.e. the outer perimeter of a

telecommunications network, which connects to the end consumers), metro

networks (i.e. networks that aggregate and distribute traffic collected from access

networks within a large city or region) and long-haul networks (i.e. networks that

interconnect metro networks using high bandwidth transmission).

As of April 30, 2017, TNL had filed 333 patent applications, with 203 filings in

India, 89 filings in the United States and 6 filings in Europe, out of which 56

patents have been granted and the company has also filed 35 patent applications

under the Patent Co-operation Treaty.

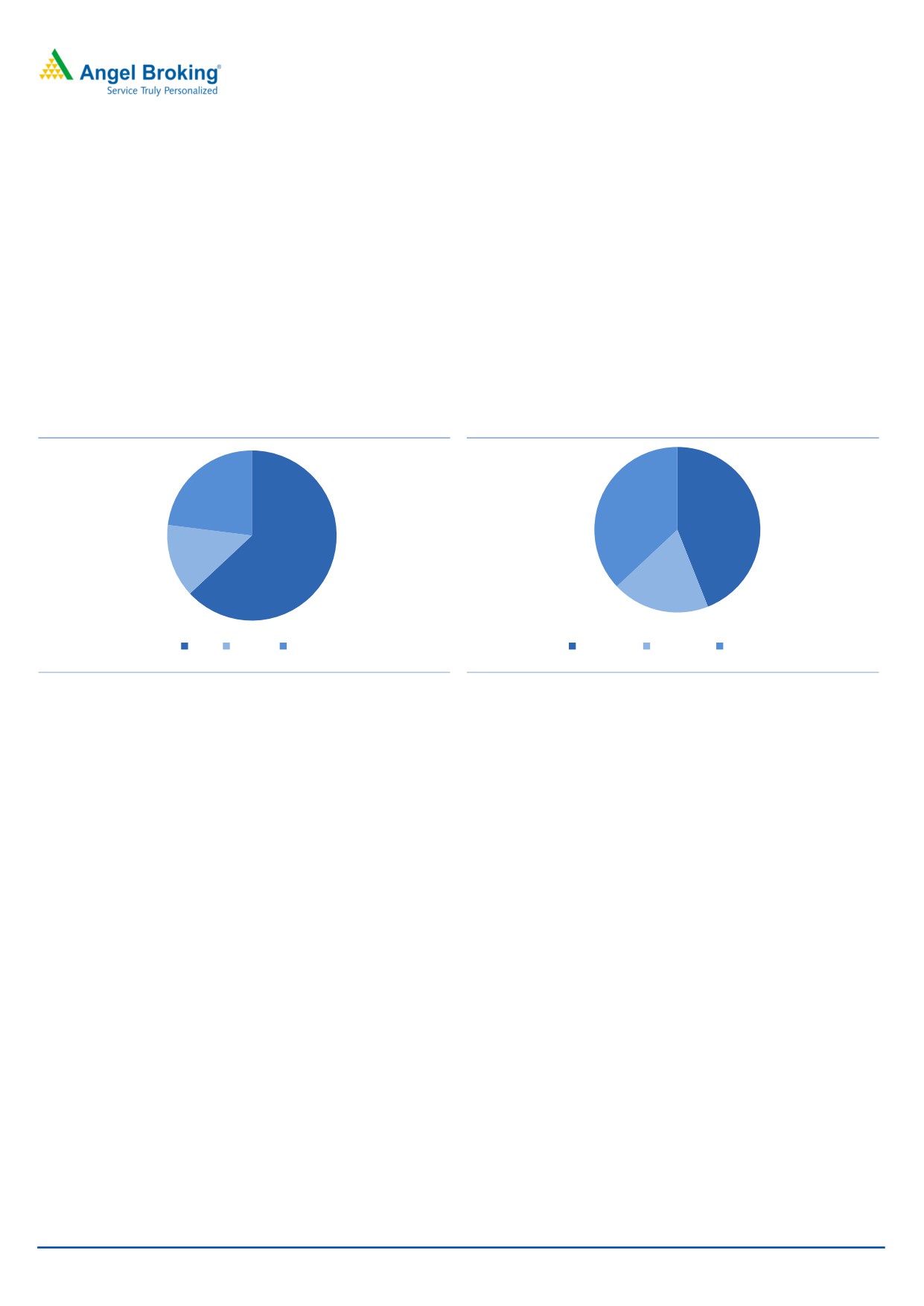

Exhibit 2: Geographical Segmentation of revenue (%)

Exhibit 3: Customer Segment of revenue (%) FY17

23

37

44

14

63

19

India

America Other

India - PSU

India - PVT

International

Source: Company, Angel Research

Source: Company, Angel Research

June 13, 2017

3

Tejas Networks Ltd| IPO Note

Issue details

The company is raising `450cr through a fresh issue of equity shares in the price

band of `250-257. The fresh issue will constitute ~19.55% of the post-issue paid-

up equity share capital of the company, assuming the issue is subscribed at the

upper end of the price band. The company is offering 1.27cr shares that are being

sold by certain exiting investors and management.

Investors selling shares in the IPO include Cascade Capital Management

Mauritius, India Industrial Growth Fund (Frontline Strategy), Intel Capital and

Sandstone Capital.

Exhibit 4: Pre and Post-IPO shareholding pattern

No. of shares (Pre-issue)

(%)No. of shares (Post-issue)

(%)

Institutional Investors

7,20,38,130

100%

5,93,26,525 66.2%

Public/DII/FII

0

0%

3,02,21,333 33.8%

7,20,38,130

100%

8,95,47,858

100%

Source: RHP, Angel Research; Note: Calculated on upper price band

Objects of the offer

More than 65% of the proceeds will go towards working capital (`303cr), a part of

it will be spent on capital expenditure and towards payment of salaries and wages

of Research & Development team (`45cr). The remaining will be set aside for

general purposes (`102cr).

Key Management Personnel

Sanjay Nayak: Managing Director and Chief Executive Officer - Mr. Nayak has

been with TNL since the company’s inception. He has spent his career in the area

of Information Communication Technology and Electronics Manufacturing. He is

the co-chairman of the Telecom Equipment and Services Export Promotion

Council. Prior to joining TNL, he was the managing director of Synopsys (India)

Private Limited.

Balakrishnan V.: He is the Non-Executive, Independent Director and Chairman of

the Company. He has been a Director of TNL since November 9, 2009. Mr.

Balakrishna has served as the group’s Chief Financial Officer and member of the

board of directors of Infosys Limited.

Kumar N. Sivarajan: Chief Technology officer - Mr. Sivarajan has been associated

with TNL since year 2000. He holds a PHD from California Institute of Technology.

June 13, 2017

4

Tejas Networks Ltd| IPO Note

Investment Rationale

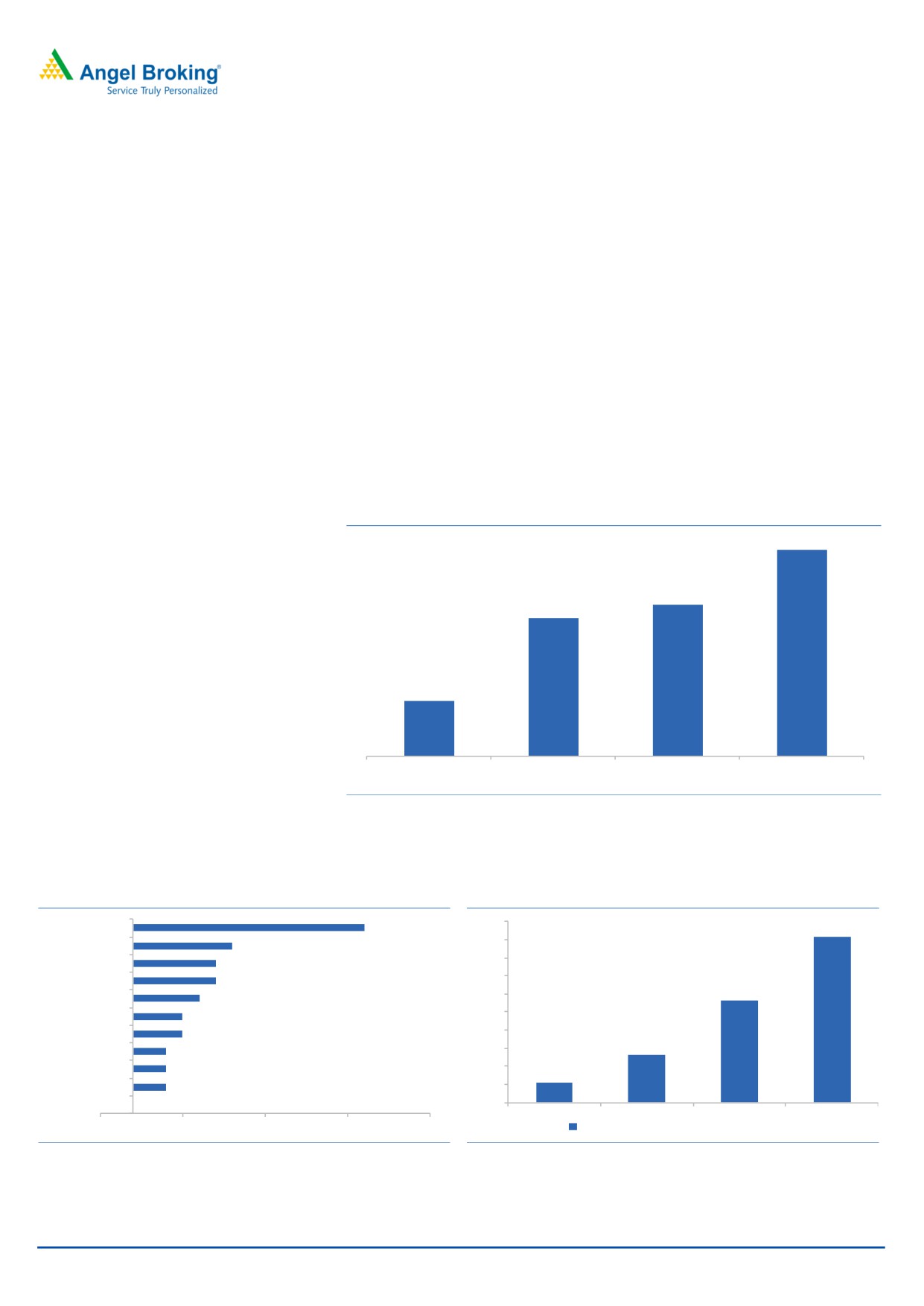

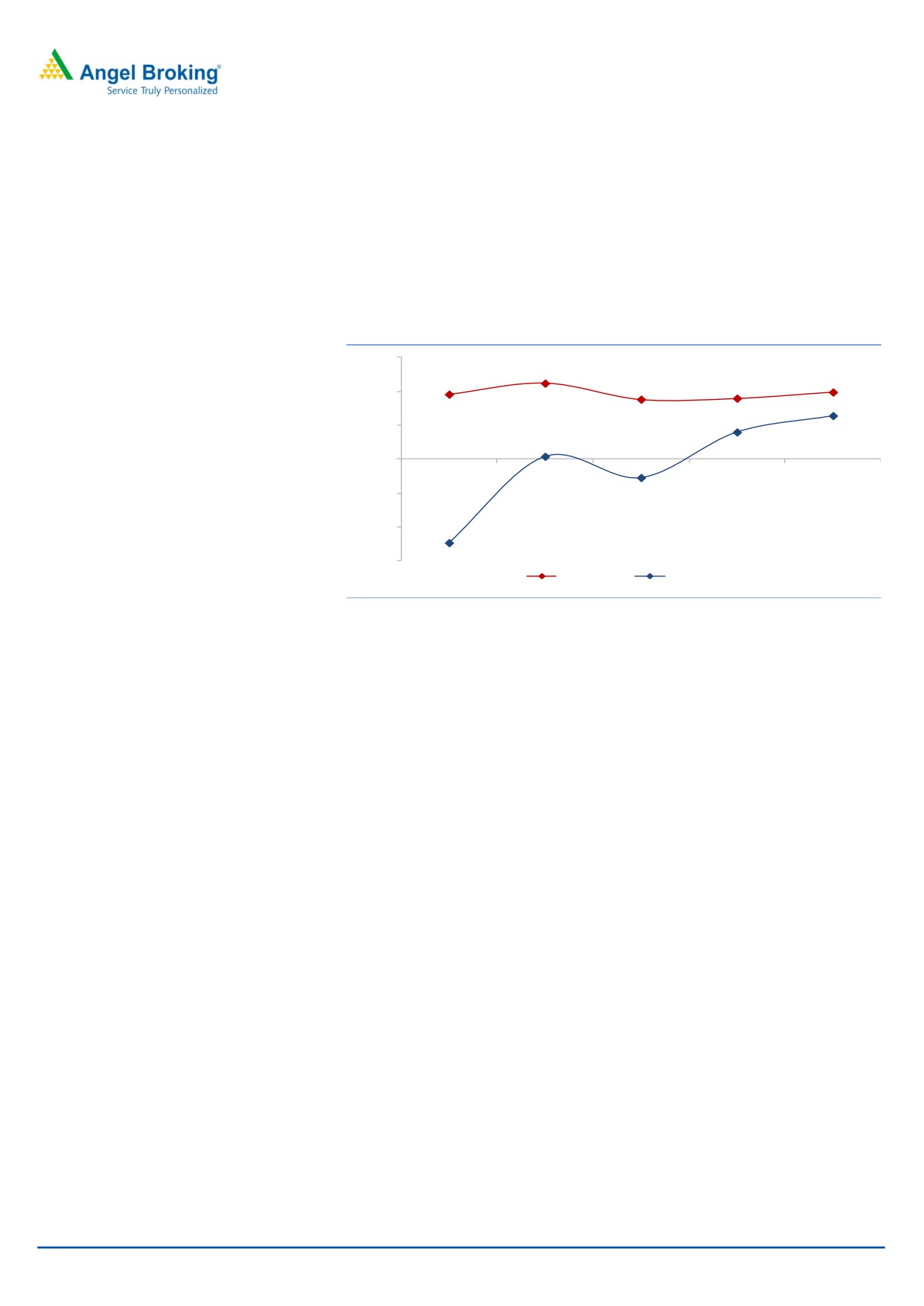

Rise in Optical Network capex expected

The Indian network operators have under invested in optical fiber transmission as

compared to their peers in China and the United States. This under investment is

due to the initial focus on voice offering services and challenges in getting laying

optical fiber in the crowded cities. Less than 20% of cell towers in India are

connected with fibre as compared to 70-80% in developed countries (according to

Delloite). In our view, Indian optical capex is likely to grow at 14% CAGR over

FY201420. Further, considering factors such as evaluation of high speed internet

technologies, proliferation of powerful networking devices & Smartphone’s, growth

in enterprise cloud services & data, and games & HD videos would require existing

telcos to upgrade network capacities for higher data traffic domestically as well as

globally.

Exhibit 5: Proportion of network sites around the world in 2015

70-80%

50-60%

45-55%

<20%

India

South Africa

SEA Benchmark

Developed Country

Source: Company, Angel Research, Delloite

Exhibit 6: Growth in optical capex from FY2014-20

Exhibit 7: Increased use of Smartphones drives data

1000

918

India

14%

900

China

6%

800

LATM& Caribben

5%

700

Asia-Oceania

5%

566

600

Global

4%

500

North america

3%

400

MEA

3%

261

EMEA

2%

300

Big 5 EU

2%

200

107

RoAo

2%

100

Japan

0%

0

2014

2016

2018

2020

-2%

3%

8%

13%

18%

Mobile broadband subscription in india (mn Users)

Source: Company, Angel Research

Source: Company, Angel Research,Ovum

June 13, 2017

5

Tejas Networks Ltd| IPO Note

Government’s push for ‘Digital India’ to further strengthen business

We believe that government’s push for ‘Digital India’ through projects such as the

National Optical Fibre Network (BharatNet, where 250,000 gram panchayats

would be connected through optical fibres), and Smart Cities will provide better

growth opportunities for business. In addition, policies such as ‘Make in India’ and

‘Preferential Market Access Policy’ would further benefit TNL’s business prospects.

Exhibit 8: Government schemes supporting ‘Make in India’ & ‘Digital

India’

Make In India

Preferential Market Access (PMA): In government procurement for domestic products

Fiscal Incentives : Supports domestic manufacturing in the form of Capital Subsidy,

Tejas is approved under M-SIPS(2)

Anti-Dumping Duties: On imports of SDH transmission equipment from China & Israel

Merchandise exports from India scheme: For enhancing India’s export competitiveness

Karnataka (State) ESDM Policy: Providing research and development grant

Digital India

National Optical Fiber Network (BharatNet): Connecting 250,000 gram panchayats (villages)

using GPON (FTTX) technology

Smart Cities: Robust IT connectivity and digitalization for 100

Right-of-Way: New rules to ease right of way for faster optical fibre and mobile tower

infrastructure rollouts

Source: Company, Angel Research

Favorably placed to capture the industry growth: We believe that TNL would

benefit from the industry growth owing to - (1) Leadership position in the fast

growing Indian optical equipment market (2nd, 15% market share); (2) Strong

professional team with significant industry experience; (3) High product reliability,

as it delivered <15 min down time a year since 2008; (4) Expanding exports into

markets with similar economic pattern as India i.e. South East Asia, Latin America,

Africa, etc. (5) Less competition owing to high entry barriers related to huge initial

investment in R&D; and (6) An end-to-end portfolio of optical networking products

for access, metro and long-haul networks.

June 13, 2017

6

Tejas Networks Ltd| IPO Note

Strong operating leverage with asset light business: Going forward, we expect TNL

to benefit from operating leverage, as the company has achieved necessary scale

required in R&D. Further, company is adopting an asset light strategy by

outsourcing most of its manufacturing to reputed electronics manufacturing

services companies. Therefore, Its ROE has improved from 8% in FY2016 to 12.9%

for FY2017, and we believe it will strengthen going ahead.

Exhibit 9: Improving EBITDA margin & ROE

30.0

22.4

17.7

20.0

18.0

19.8

19.2

10.0

12.9

0.9

8.0

-

FY13

FY14

FY15

FY16

FY17

-10.0

-5.4

-20.0

-24.6

-30.0

EBITDA (%)

ROE (%)

Source: Company, Angel Research

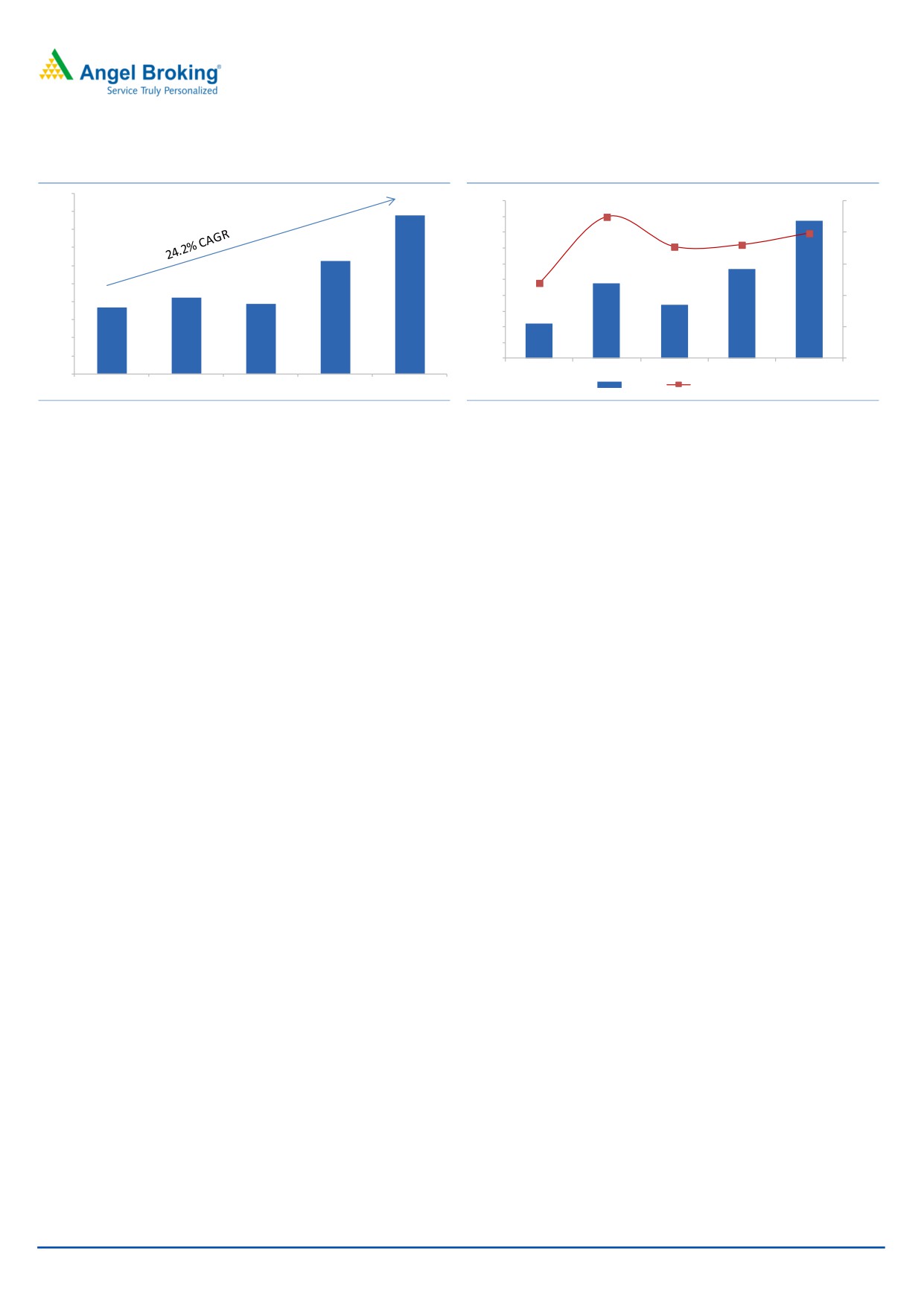

Financial performance track record

TNL is consistently reporting improved numbers on the fronts of revenue, EBITDA

and return ratios. The revenues have grown from `369cr in FY2013 to `878cr in

FY2016, showing a 4 year CAGR of 24.2%. For FY2017, the company reported

PAT of `63cr (after considering onetime expenses of `30cr) from loss of `79cr in

FY2013.

EBITDA margins have improved from 12% in FY2013 to 19.8% in FY2017, largely

owing to better operating leverage. The company has made basic investments in

R&D and professional man power in order to achieve the necessary scale. Hence,

except cost of material, which is linked to revenue, majority of the operating costs

are almost fixed. Therefore, we believe that the company would continue to report

higher EBITDA margins and return ratios going ahead. From a loss making

company in FY2013 it has been able to report RoE of 12.9% in FY2017, which is

commendable.

June 13, 2017

7

Tejas Networks Ltd| IPO Note

Exhibit 10: Historical revenue Trend

Exhibit 11: Historical EBITDA trend

1000

878

200

25.0%

900

180

19.8%

800

160

22.4%

20.0%

18.0%

700

627

140

17.7%

600

120

15.0%

12.0%

500

100

423

369

387

80

10.0%

400

60

300

40

5.0%

200

20

44

95

69

113

174

100

-

0.0%

0

FY13

FY14

FY15

FY16

FY17

FY13

FY14

FY15

FY16

FY17

EBITDA

EBITDA Margin

Source: Company, Angel Research

Source: Company, Angel Research

Outlook and Valuation: TNL has reported strong revenue CAGR of 24.2% CAGR

over FY2013-17 and PAT of 64cr in FY2017 (loss of `79cr in FY2013). The RoE

improved from 8% in FY2016 to 12.9% in FY2017, primarily owing to ongoing

capex on Optical Network by Telcos, strong operating leverage with asset light

business and strong professional team with significant industry experience. At the

upper end of the price band, the pre-issue P/E works out to be 29.3x its 2017

earnings, 3.7x of FY2017 Book Value. Moreover, the company’s debt free balance

sheet post IPO coupled with the government’s push for digital India would support

the growth momentum. Thus, we recommend a SUBSCRIBE on the issue.

Key risks

Client concentration

In FY2017, the company has generated 58% of the revenue from 5 customers

however, any customer back out could severely impact revenue growth.

Outstanding legal & Tax proceedings

Total number of Tax proceedings against TNL is 40 and the amount involved is

`159cr. The amount involved in civil cases is `19cr. Unfavorable verdict could

disturb the financial condition of the company.

Fluctuations in currency exchange rates

As of Fiscal Years 2015, 2016 and 2017, US Dollar-denominated revenues

represented 57.66%, 30.23% and 33.65% of total revenues respectively. Hence,

any adverse or volatile movement in Currency could impact the financials of the

company.

June 13, 2017

8

Tejas Networks Ltd| IPO Note

Consolidated Income Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017

Total operating income

369

423

387

627

878

% chg

-

14.6

(8.6)

62.2

40.0

Total Expenditure

325

328

318

514

704

License fees

226

209

198

351

514

Personnel

45

45

50

67

76

Others Expenses

54

75

71

97

114

EBITDA

44

95

69

113

174

% chg

(145.9)

115.0

(27.8)

65.0

54.1

(% of Net Sales)

12.0

22.4

17.7

18.0

19.8

Depreciation& Amortisation

48

56

49

38

56

EBIT

(4)

39

20

74.8

118

% chg

-

-

(49.0)

274.8

57.5

(% of Net Sales)

(1.0)

9.2

5.2

11.9

13.4

Interest & other Charges

36

46

47

49

32

Other Income

9

10

9

4

9

(% of PBT)

(31.7)

347.1

(51.1)

12.1

13.5

Extraordinary Items

49

-

-

-

30

Share in profit of Associates

Recurring PBT

(30)

3

(18)

29

64

% chg

-

-

-

122.4

Tax

0

-

-

-

1.3

PAT (reported)

(30)

3

(18)

29

64

% chg

-

-

-

(% of Net Sales)

(8.2)

0.7

(4.6)

4.6

7.3

Basic & Fully Diluted EPS (Rs)

(11.0)

0.4

(2.5)

4.0

8.8

% chg

-

-

-

118.0

June 13, 2017

9

Tejas Networks Ltd| IPO Note

Consolidated Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017

SOURCES OF FUNDS

Equity Share Capital

101

101

126

67

74

Reserves& Surplus

220

223

206

294

427

Shareholders Funds

321

324

331

361

501

Total Loans

220

262

220

253

228

Total Liabilities

541

586

551

614

729

APPLICATION OF FUNDS

Net Block

77

65

51

94

92

Capital Work-in-Progress

71

84

88

52

19

Investments

-

-

0

0

0

Current Assets

459

509

532

605

659

Inventories

214

209

221

232

182

Sundry Debtors

138

223

208

254

358

Cash

58

23

50

69

71

Loans & Advances

43

38

32

34

42

Other Assets

5

16

22

15

7

Current liabilities

115

159

177

225

188

Net Current Assets

344

350

355

380

472

Other Non Current Asset

50

88

58

88

146

Total Assets

541

586

551

614

729

Note - Net block includes Intangible Asset

June 13, 2017

10

Tejas Networks Ltd| IPO Note

Consolidated Cash Flow Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017

Profit before tax

(79)

3

(18)

29

64

Depreciation

48

56

49

38

56

Change in Working Capital

2

(84)

(14)

1

(95)

Interest / Dividend (Net)

(4)

11

18

2

56

Direct taxes paid

0.2

(3)

(2)

(2)

(6)

Others

58

44

43

59

7

Cash Flow from Operations

25

27

76

127

83

(Inc.)/ Dec. in Fixed Assets

(23)

(56)

(39)

(46)

(51)

(Inc.)/ Dec. in Investments

23

(18)

10

(5)

(90)

Cash Flow from Investing

(0)

(74)

(29)

(50)

(141)

Issue of Equity

39

0

0

0

0

Inc./(Dec.) in loans

5

61

(16)

9

(5)

Others

(36)

(46)

(23)

(49)

46

Cash Flow from Financing

8

15

(40)

(41)

40

Inc./(Dec.) in Cash

34

(32)

8

36

(18)

Opening Cash balances

3

37

5

13

49

Closing Cash balances

37

5

13

13

31

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

FY2017

Valuation Ratio (x)

P/E (on FDEPS)

(23.4)

666.7

(103.6)

63.8

29.3

P/CEPS

(74.2)

39.3

75.0

34.2

19.2

P/BV

5.8

5.7

5.6

5.1

3.7

EV/Sales

5.5

4.9

5.2

3.2

2.3

EV/EBITDA

45.6

22.0

29.5

18.0

11.5

EV / Total Assets

3.7

3.6

3.7

3.3

2.8

Per Share Data (Rs)

EPS (Basic)

(11.0)

0.4

(2.5)

4.0

8.8

(11.0)

0.4

(2.5)

4.0

8.8

EPS (fully diluted)

Cash EPS

(3.5)

6.5

3.4

7.5

13.4

Book Value

44.6

45.0

46.0

50.0

69.5

Returns (%)

ROCE

(0.7)

6.7

3.6

12.2

16.2

(0.8)

6.9

4.0

13.7

17.9

Angel ROIC (Pre-tax)

ROE

(24.6)

0.9

(5.4)

8.0

12.9

Turnover ratios (x)

Inventory / Sales (days)

212

180

208

135

76

Receivables (days)

136

193

196

148

149

102

118

130

116

58

Payables (days)

** Working capital cycle

246

254

274

167

166

Source: Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price

band **(ex-cash) (days)

June 13, 2017

11

Tejas Networks Ltd| IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Company Name

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

June 13, 2017

12