IPO Note | FMCG

October 3, 2017

Godrej Agrovet Limited

SUBSCRIBE

sue Open: October 04, 2017

Is

IPO Note

Issue Close: October 06, 2017

Godrej Agrovet Limited (GAVL) is a leading Agri-business company operating

across five different business verticals i.e. Animal Feed, Crop Protection, Oil Palm,

Issue Details

Dairy and Poultry & Processed Foods. GAVL is the largest crude palm producer in

India. Company is the 4th largest animal feed producer in Bangladesh through its

Face Value: `10

50:50 JV ACI Godrej.

Present Eq. Paid up Capital: `185.3cr

Diversified business with multiple growth drivers: GAVL is a diversified, R&D

focused agri-business Company. It used to derive 80% of its revenue from animal

Offer for Sale: *1.9cr shares (`853.5cr)-

**1.9cr shares (`865.8cr)

feed business; however the same has come down to 53% in FY17 due to

successful diversification of its business. Currently, palm oil business contributes

Fresh issue: `291.5cr ( *64.8 lakh -**63.4

10% while crop protection (16%) and dairy (21%) have also sizable presence. All

lakh shares)

Post Eq. Paid up Capital:*`192.2cr

-

of its businesses have multiple growth drivers such as high growth potential,

**`192.1cr

increasing organized segment, new product launches, etc. GAVL is likely to

Issue size (amount): *`1,145cr -**1,157 cr

continue the growth momentum which will further diversify its revenue streams.

Price Band: `450-460

Track record of consistent profitability: GAVL clocked revenue/PAT CAGR of

15.5% and 27% respectively over last 5 years as favorable revenue mix led to

Lot Size: 32 shares and in multiple thereafter

improvement in EBITDA margins from 7% in FY13 to 8.9% in FY17. This is also

Post-issue implied mkt. cap:

*`8,649cr

-

helped by the acquisition of Astec LifeScience (Animal protection business) which

**`8,835cr

has superior margin profile. We believe that with the rising contribution of crop

Promoters holding Pre-Issue: 74.8%

protection (FY17: 22% EBIT margins) and palm oil business (FY17: 20% EBIT

Employee reservation: Up to `20cr

(*4.44

margins), overall margins and profitability is likely to improve further.

lakh -**4.35lakh)

Promoters holding Post-Issue:

*68.6%-

Strong return profile: GAVL consistently reported >30% ROE between FY14-FY16.

**68.8%

In FY17, company reported 27% ROE and with the favorable revenue mix, we

*Calculated on lower price band

believe that GAVL is expected to remain a high ROE company going ahead.

** Calculated on upper price band

Valuations and outlook: At the upper end of the price band (`450-`460),

Book Building

company is asking for a market cap of `8,835cr, at the PE multiple of 33.5x of its

FY17 adj. PAT. While there is no exact peer to compare with GAVL’s diversified

QIBs

50% of issue

business, we note that businesses which are present in at least one of the

Non-Institutional

15% of issue

segments of GAVL, trade in a PE multiple range of 22x-57x and ROE profile

range of 15%-30%. At 33.5x, GAVL does not appear expensive as PE multiple is

Retail

35% of issue

in the mid of this range and ROE is at the higher end of the range. We assign a

subscribe rating to this IPO considering its diversified business profile, decent

margins, strong return ratios, healthy balance sheet and strong history of its

parent.

**Post Issue Shareholding Pattern

Promoters Group

68.8

Key Financials

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

DIIs/FIIs/Public & Others

31.2

Net Sales

3,102

3,312

3,750

4,911

% chg

12.4

6.7

13.2

31.0

Net Profit

157

210

261

274

% chg

61.8

34.2

24.3

5.1

OPM (%)

7.8

9.2

7.9

8.9

EPS (Rs)

8.4

9.4

9.0

13.7

P/E (x)

54.5

49.1

51.2

33.5

P/BV (x)

16.4

13.3

10.9

8.4

Shrikant Akolkar

RoE (%)

30.2

32.8

33.3

27.2

RoCE (%)

18.8

20.3

11.8

21.8

+91 22 39357800 Ext: 6846

EV/Sales (x)

3.0

2.9

2.7

1.9

EV/EBITDA (x)

38.7

31.1

34.0

21.5

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Godrej Agrovet| IPO Note

Company background

Godrej Agrovet was incorporated in 1991 with a focus on agricultural business

and has become a diversified business along the way. Company operates 5

separate businesses i.e. animal feeds, crop protection, oil palm, dairy, and poultry

and processed foods. Animal feed is its largest business which contributes more

than half of its total revenue.

In 1994, company entered the poultry business while in 2004, company entered in

the animal feed business in Bangladesh by forming a JV (ACI Godrej) with

Advanced Chemical Industries Limited. In 2008, company entered into a JV with

Tyson India Holding Limited to grow its poultry and processed foods business.

In 2005, GAVL acquired a 26% stake in Creamline Dairy Products Ltd and raised

this stake to 51.9% in 2015. Creamline dairy is involved in the business of milk

and milk-based products under the Jersey brand. GAVL also acquired a majority

stake in Astec LifeSciences to boost its manufacturing capabilities in agro-

chemicals and to backward integrate its crop protection business.

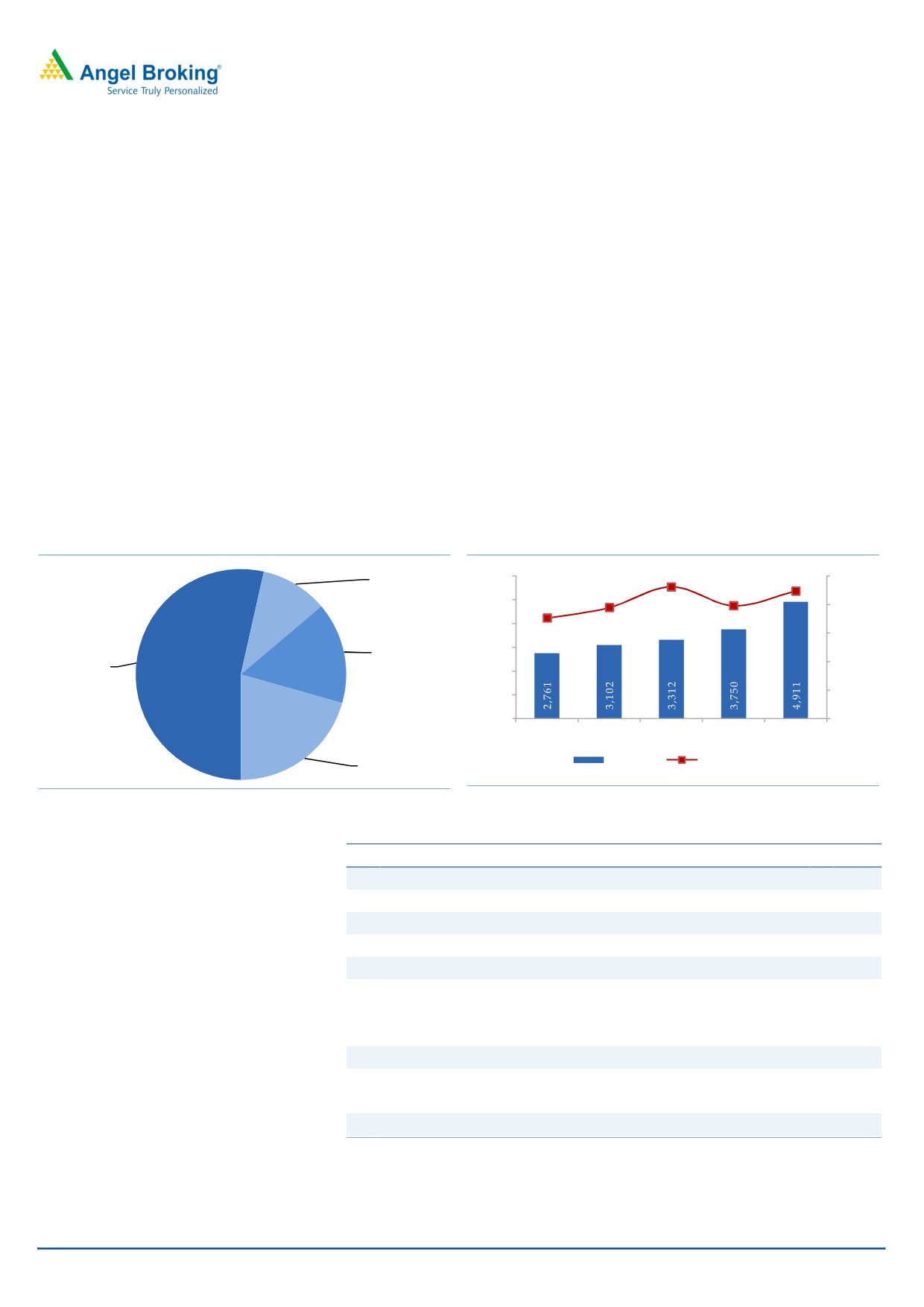

Exhibit 1: Business mix (FY17)

Exhibit 2: Revenue growth and margin profile

9.2%

Vegetable oil,

6,000

8.9%

10.0%

10%

7.8%

7.9%

5,000

7.0%

8.0%

4,000

Crop

6.0%

protection,

3,000

Animal feed,

16%

4.0%

2,000

53%

2.0%

1,000

0

0.0%

FY13

FY14

FY15

FY16

FY17

Dairy, 21%

Net sales

EBITDA marigns

Source: Company, Angel Research, #JVs are not consolidated

Source: Company, Angel Research, #includes Astec LifeScinece revenues

Exhibit 3: Evolution of GAVL’s business

Year

Milestone

1991

Incorporation of GAVL

1992

Acquisition of the agrovet division from Godrej Soaps Limited

1997

Acquisition of the oil palm business from Godrej Soaps Limited

1999

Acquisition of the poultry business from IPF Breeders Private Limited

2004

JV in Bangladesh (ACI Godrej)

Acquisition of 26% stake in Polchem Hygiene Laboratories

2005

Acquisition of 26% stake in Creamline Dairy

Acquisition of shrimp feed business from Higashimaru Feeds (India) Limited

2012

V-Sciences buys 19.99% equity stake in GAVL

Acquisition of majority stake in Astec Lifescience

2015

Increases its stake from 26% to 52% in Creamline Dairy

2016

Sold its stake in Polchem Hygiene Laboratories

Source: Company, Angel Research

October 3, 2017

2

Godrej Agrovet| IPO Note

Business segments

Animal feed business: GAVL produces cattle feed, poultry feed (broiler and layer),

aqua feed (fish and shrimp) and specialty feed at its 35 facilities with production

capacity of 2.36 million MT/ annum. It has a pan-India distribution network of

~4,000 distributors. GAVL also has a 50:50 joint venture in Bangladesh named

ACI Godrej which produces cattle, poultry and fish feed in Bangladesh and has 2

manufacturing facilities with production capacity of 0.57 million MT/annum.

Crop protection business: GAVL manufactures a wide range of products such as

plant growth regulators, organic manures, generic agrochemicals and specialized

herbicides and sells it to retail customers. In October 2015, GAVL acquired

56.82% stake in Astec LifeSciences which is in the manufacturing of agrochemical

active ingredients (technical), bulk and formulations and intermediates. Astec sells

products in India as well as exports them to 24 countries. GAVL has distribution

network of ~6,000 distributors in India.

Palm oil business: GAVL produces crude palm oil, crude palm kernel oil and palm

kernel cake. Company purchases fresh fruit bunches (FFB) from palm oil farmers.

GAVL has access to ~61,700 hectares land under oil palm plantation and has set

up 5 palm oil mills in India with an aggregate FFB processing capacity of 125 MT

/hour and a palm kernel processing capacity of 7 MT /hour.

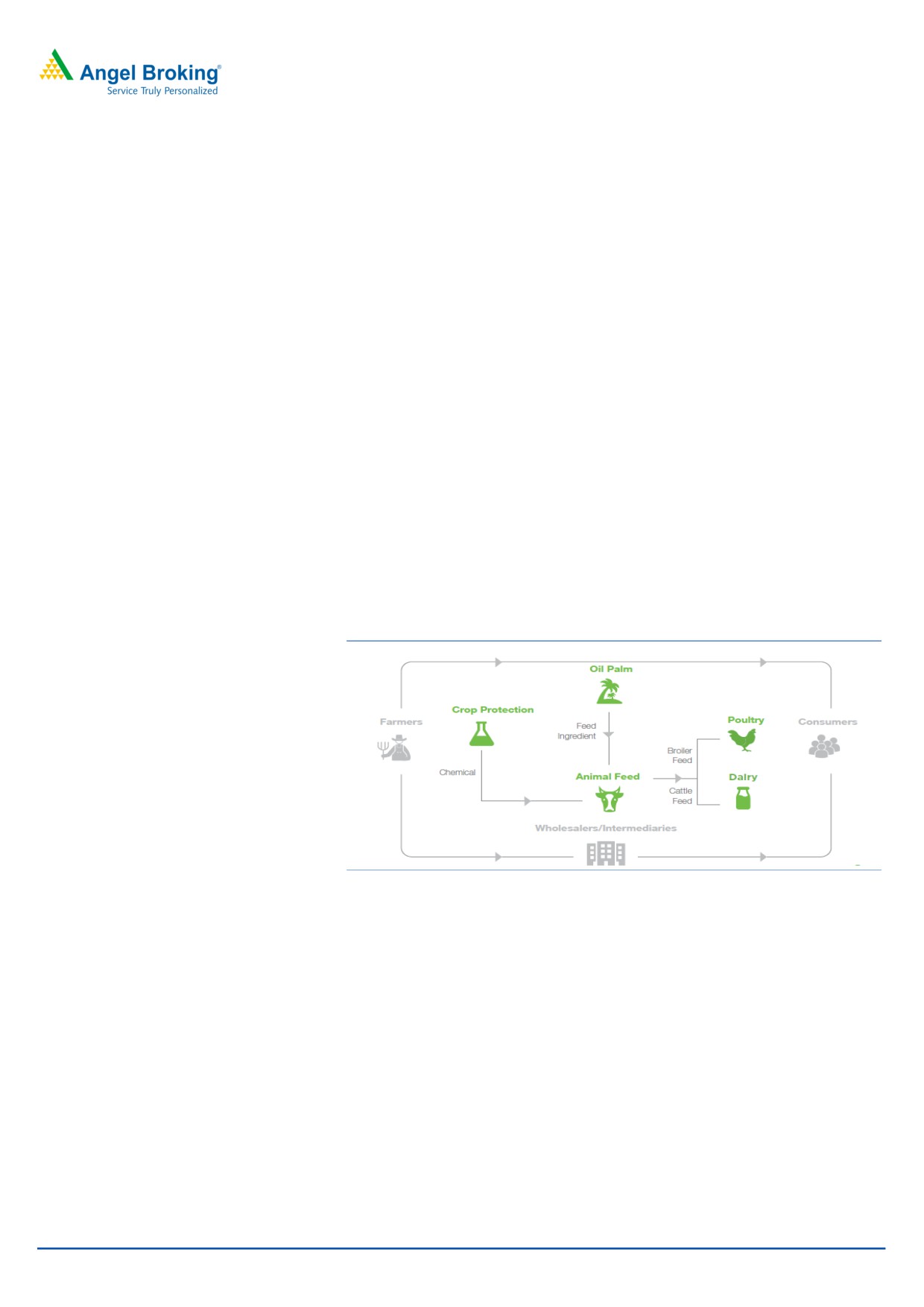

Exhibit 4: Inter-linkages Between Business Verticals

Source: Company, Angel Research

Dairy business: Company sells milk and milk based products under the brand

‘Jersey’ through its subsidiary, Creamline Dairy, across the states of Telangana,

Andhra Pradesh, Tamil Nadu, Karnataka and Maharashtra. Company owns and

operates 9 milk processing units and has a supply network of 120 chilling centers

and 4,000 milk distributors, ~3,000 milk product distributors and 50 retail

parlors, as of June-2017.

Poultry business: It manufactures and markets processed poultry and vegetarian

products through its brands Real Good Chicken and Yummiez. Company ventured

into the poultry business in 1994 by launching the Real Good Chicken bran. In

2008, to grow its poultry and processed foods business, company entered into a

joint venture with Tyson India Holding Limited. It has set up 2 processing plants

with integrated breeding and hatchery operations and has a diverse customer base

comprising of retail customers as well as institutional clients such as restaurants,

food service companies and hotels.

October 3, 2017

3

Godrej Agrovet| IPO Note

Issue details

The IPO consists of OFS (`854cr on lower band and `866cr on upper band) and a

fresh issue of `292cr. Through this IPO, V-Sciences Investments Pte Ltd, an indirect

wholly owned subsidiary of Temasek Holdings (Private) Limited will take a partial

exit while promoters will also sell some part of their shares from the company.

Before the IPO, V-Sciences Investments held 20% stake in the company which was

bought in 2012. After the IPO, the stake of V-Sciences Investments would come

down to 12.9% while promoters’ stake would come down to 68.8% from existing

74.8%. `20cr of the issue is reserved to the employees.

Separately a total 4,05,500 shares will be issued by the company to its already

identified employees as per GAVL’s Employee Share Purchase Scheme which will

fetch it `18.2cr on the lower band and `18.7cr on the upper band.

In the pre-IPO placement, GAVL has already issued `8.5cr by issuing 192,901

shares at `440/share.

Exhibit 5: Selling shareholders and pre and post IPO shareholding pattern

Pre-Issue

Post-Issue

Shareholder

No of shares

% of shareholding

No of shares

% of shareholding

Promoter

138,614,840

74.8

132,093,101

68.8

V-Sciences Investments Pte Ltd

37,007,698

20.0

24,707,698

12.9

Other public

9,701,239

5.2

35,265,696

18.4

185,323,777

100.0

192,066,494

100.0

Source: Company, Angel Research

Objects of the fresh issue

Repayment of working capital facilities (`100cr)

Repayment of commercial papers (`150cr)

General corporate purposes

October 3, 2017

4

Godrej Agrovet| IPO Note

Investment Rationale

A diversified business with improving business mix: GAVL operates a diversified

business model, the business segments of which are also interlinked together.

While the animal feed is its largest business, the company has been seeing a rapid

change in its revenue mix. Animal feed used to contribute 81% of revenue in FY13

the same however has come down to 53% in FY17. During this period, palm oil

business contribution has remained constant at 10% and crop protection business

has seen rapid increase in its contribution which has increased from 8% in FY13 to

~16% in FY17. Contribution of dairy business has also seen rapid growth from 1%

of total revenue in FY13 to 20% in FY17.

During this period, GAVL adopted an inorganic route to expand its business with

acquisition of Astec LifeSciences in crop protection business and increasing its

stake in the company Creamline Dairy in milk business.

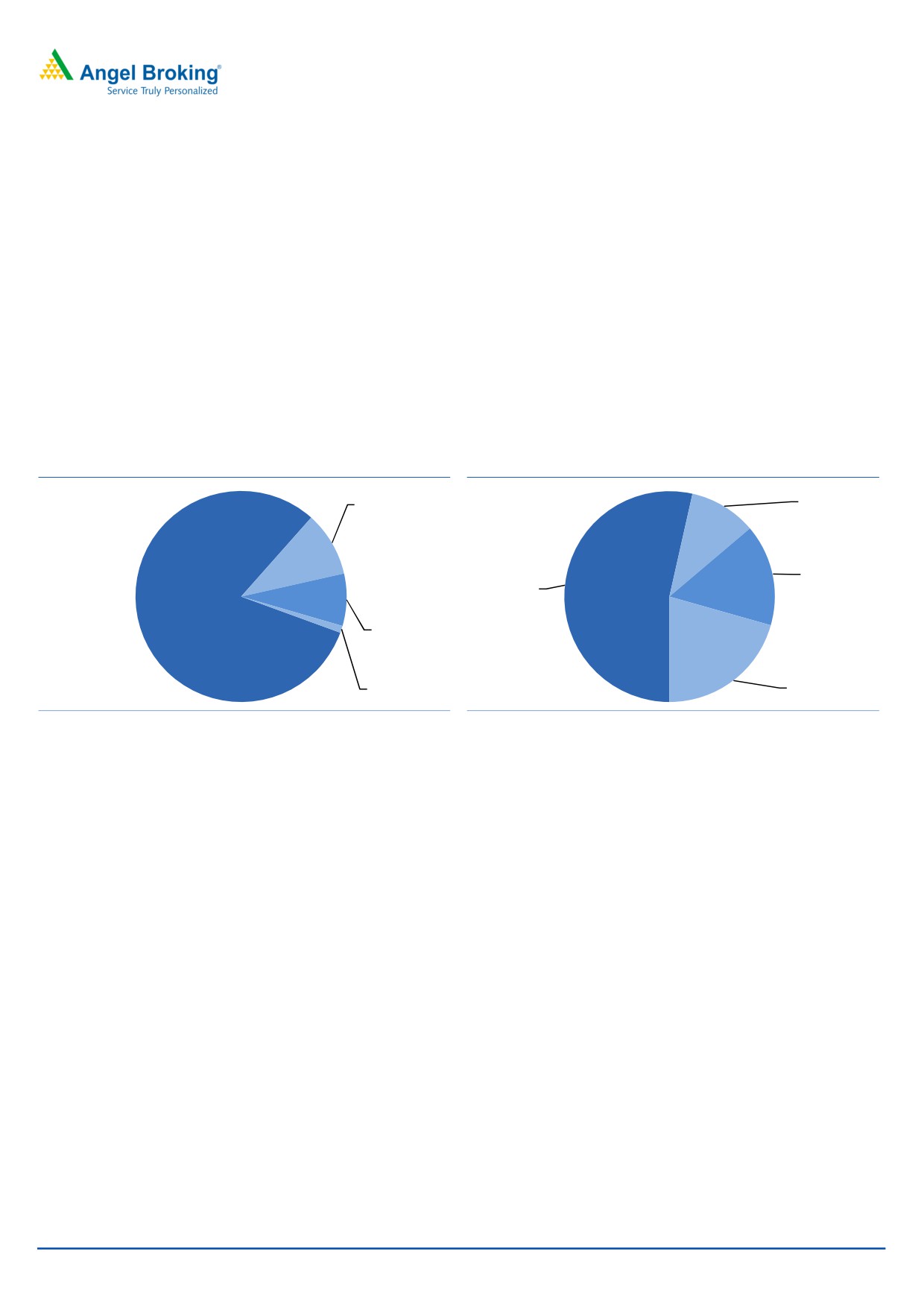

Exhibit 6: Evolution of its business mix

Exhibit 7: 27% CAGR in revenue between FY13-FY17

Vegetable oil,

Vegetable oil,

10%

10%

Crop

protection,

Animal feed,

16%

53%

Crop

Animal feed,

protection, 8%

81%

Dairy, 1%

Dairy, 21%

Source: DRHP, Angel Research, #JVs are not consolidated

Source: DRHP, Angel Research, #JVs are not consolidated

Additionally company also has a joint venture in its poultry business with Tyson

India Holdings Limited (subsidiary of Tyson Foods inc) named as Godrej Tyson

Foods. Godrej holds 49% stake in this business and this is a sizable business with

`446cr in revenues in FY17. While this business is not consolidated in total

revenues, at 49% of `446cr, poultry business can make ~4% of its total revenue.

We like GAVL’s diversified business model and that each business has a multiple

growth drivers which will benefit the company.

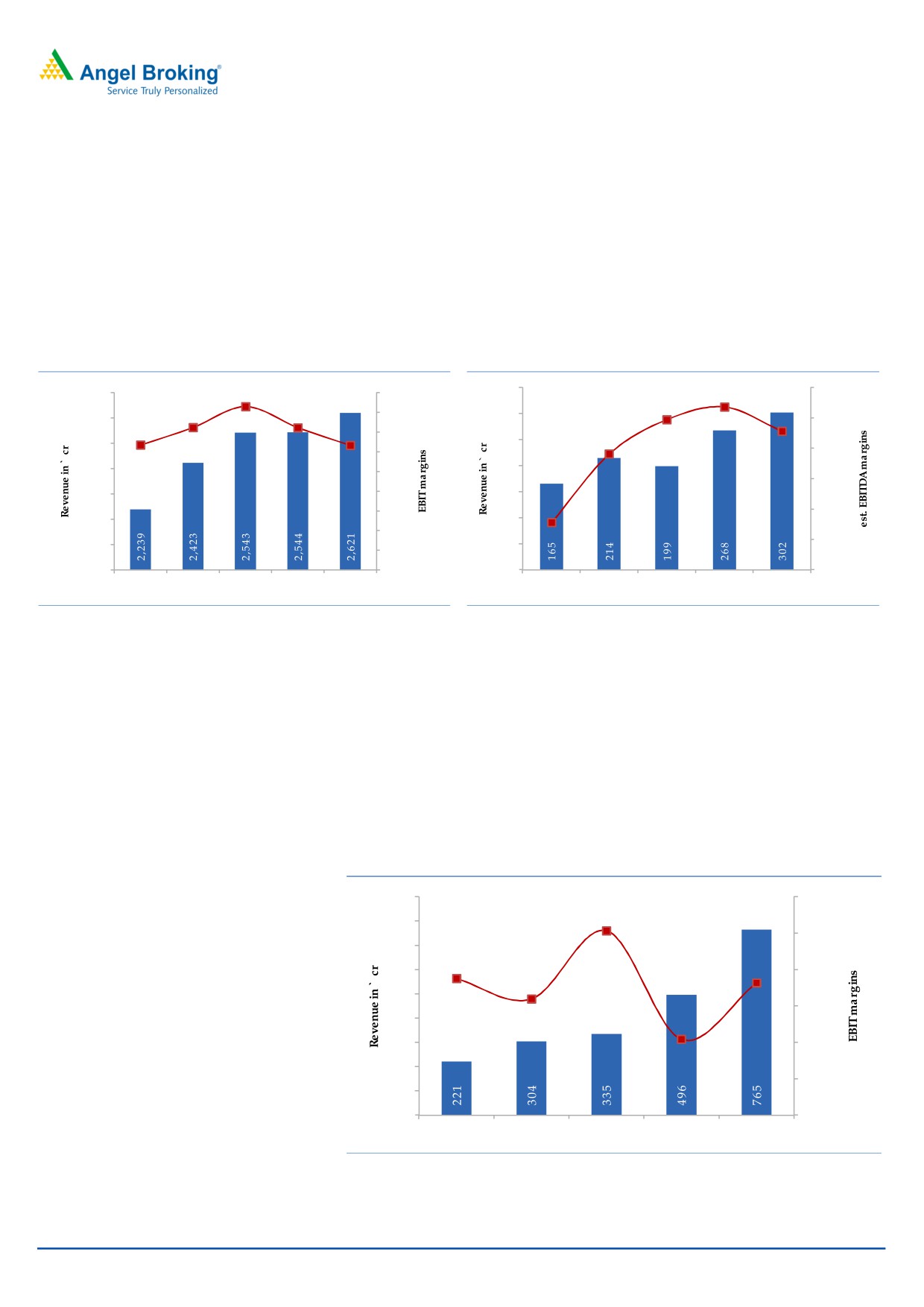

GAVL’s business segments have multiple growth drivers: GAVL’s diversified

business has multiple growth drivers in place.

1) ANIMAL FEED

Domestic animal feed industry drivers: Currently animal feed industry is about

`715bn-`725bn expected to grow at 13-14% over next 3 years. Within this

industry, poultry feed contributes 67% while cattle feed contributes ~21% and

rest 12% is contributed by aqua feed. The animal food industry is expected to

grow at ~14% CAGR to reach `1,060bn in 2020, within this poultry feed and

aqua feed segments will grow at 15% CAGR each while cattle feed will grow

by ~10% CAGR. The feed industry has a huge contribution of unorganized

segment (cattle feed ~88%, fish food 50% and shrimp food 80%) which

means that organized players like GAVL can gain market share in the industry

leading to a sizable growth opportunity.

October 3, 2017

5

Godrej Agrovet| IPO Note

Bangladesh animal feed industry drivers: The Company has a joint venture

named ACI Godrej in Bangladesh which operates in the animal feed business.

This industry in Bangladesh has a demand gap meaning demand is outpacing

the supply which is favorable for companies operating in this segment.

GAVL is present in all three animal feed segments in India (Poultry, cattle and

fish) and has seen revenue growth at CAGR 4% between FY13-FY17. ACI

Godrej is a 4th largest company in Bangladesh animal feed market growing at

a strong revenue CAGR of 16% (FY13-FY17)

Exhibit 8: Evolution of its business mix

Exhibit 9: 16% CAGR in revenue between FY13-FY17

350

9.9%

10.7%

12.0%

2,700

8.3%

9.0%

6.3%

7.2%

7.2%

8.0%

300

2,600

9.1%

10.0%

6.3%

7.0%

3.1%

250

7.6%

2,500

8.0%

6.0%

2,400

200

5.0%

6.0%

2,300

4.0%

150

3.0%

4.0%

2,200

100

2.0%

2.0%

2,100

50

1.0%

2,000

0.0%

0

0.0%

FY13

FY14

FY15

FY16

FY17

FY13

FY14

FY15

FY16

FY17

Source: DRHP, Angel Research

Source: DRHP, Angel Research

2) CROP PROTECTION

Industry drivers: The Indian crop protection market is ~`205bn in 2017 and it

is growing at a CAGR of 9.7% since 2013. Of this ~52% is domestic

consumption and 48% is exports. The crop protection industry has strong

drivers like increasing farm income, need to increase crop yields, rising use of

herbicides and pesticides, etc. Currently insecticides form 54% of the total

industry which will come down to 52% while herbicides’ contribution will

increase from 20% in 2017 to 21% in 2020 and fungicides’ contribution will

increase from 21% in 2017 to 22% in 2020.

Exhibit 10: 36% CAGR in Crop protection revenues

900

27.0%

25.1%

800

22.3%

25.0%

700

22.5%

600

23.0%

21.4%

19.2%

500

21.0%

400

300

19.0%

200

17.0%

100

0

15.0%

FY13

FY14

FY15

FY16

FY17

Source: DRHP, Angel Research, #Includes Astec LifeSciences revenues

GAVL is present in herbicides and plant growth regulators and through the

acquisition of Astec LifeSciences it also has a acquired a portfolio of

October 3, 2017

6

Godrej Agrovet| IPO Note

agricultural active ingredients and intermediates. Company has

2

manufacturing facilities and it exports to 24 countries.

3) PALM OIL

Industry drivers: India is seeing rapid increase in the palm oil consumption

and 50% of the total supply is imported which makes India as largest imported

of edible oil in the world. India’s edible oil consumption is expected to

increase from average 14.8kg per capita (2012-14) to 19 kg per capita in

2024 which still will be below the global average of 21kg per capita. To

reduce the reliance on edible oil imports, government has sponsored palm oil

cultivation in the country.

GAVL is the market leader in domestic palm oil business with 35% market

share. It has 5 oil mills with fresh fruit bunches processing capacity of 125MT

per hour. It has 61,700 hectares land under oil palm cultivation (1/5th of the

total land under oil palm cultivation in India.

Exhibit 11: 16.5% CAGR in oil palm revenues

600

25.0%

20.3%

19.7%

500

17.7%

20.0%

16.2%

15.2%

400

15.0%

300

10.0%

200

5.0%

100

0

0.0%

FY13

FY14

FY15

FY16

FY17

Source: DRHP, Angel Research

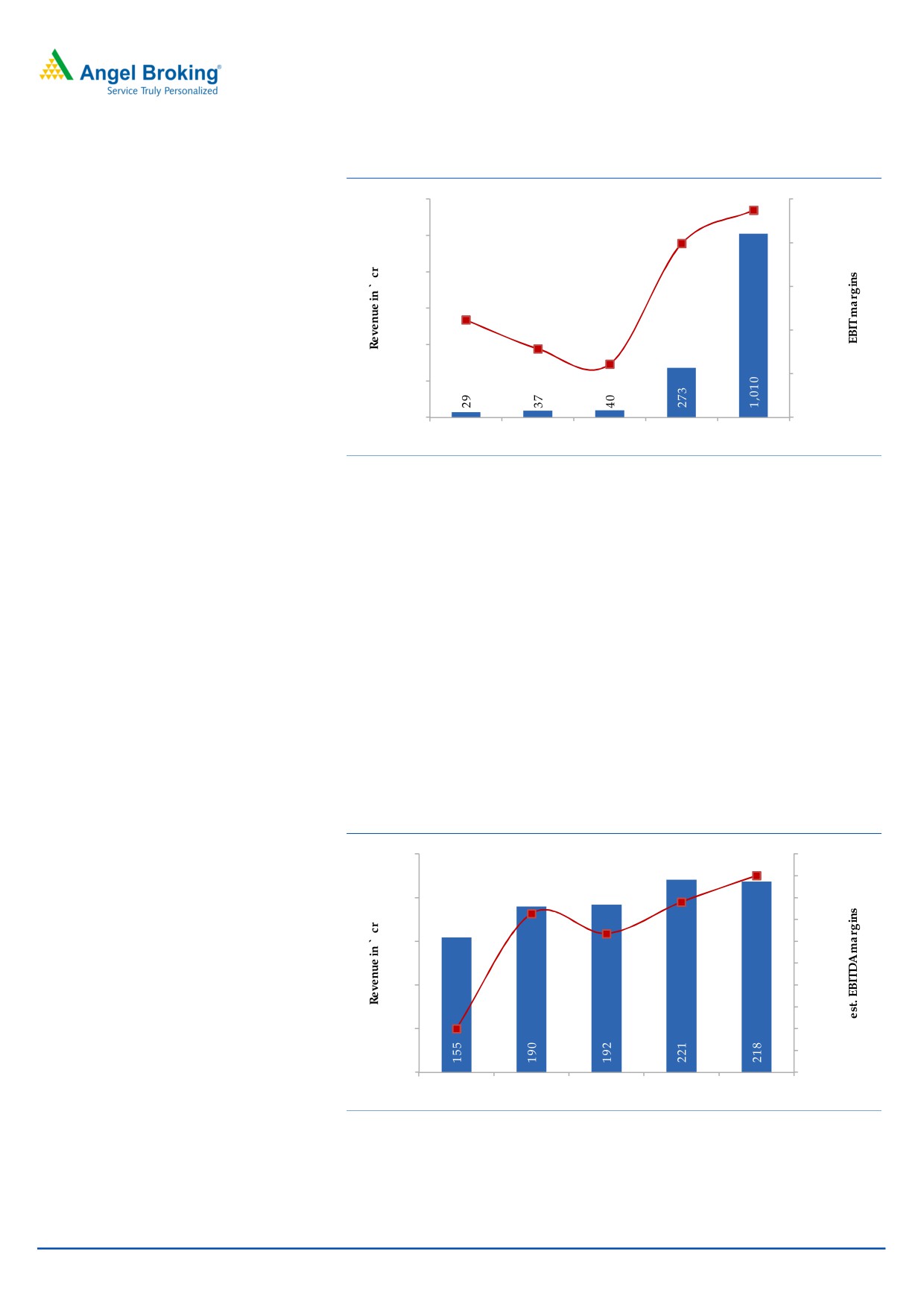

4) DAIRY BUSINESS

Industry drivers: While India is one of the largest milk produce, we are lagging

behind in the milk consumption. Rising population and rising income levels

are the structural growth drivers for the industry. The high share of the

unorganized players (73% in 2017) also makes a case of growth for the

organized players like GAVL.

GAVL sells milk products under its brand, Jersey. Its main focus area is

Maharashtra, Karnataka, Andhra Pradesh, Telangana and Tamil Nadu.

Company has 4,000 milk distributors and 3,000 milk product distributors.

Company plans to increase value added product in its portfolio which will help

it achieve revenue growth and improve the margin profile.

October 3, 2017

7

Godrej Agrovet| IPO Note

Exhibit 12: GAVL’s dairy business is sizable

3.7%

1,200

5.0%

-0.1%

1,000

0.0%

800

-5.0%

-8.9%

600

-12.2%

-10.0%

400

-13.9%

-15.0%

200

0

-20.0%

FY13

FY14

FY15

FY16

FY17

Source: DRHP, Angel Research, Includes revenue of Creamline Dairy

5) POULTRY AND PROCESSED FOODS

Industry drivers: Meat consumption in India (3.7kg per year) is well below the

global average (17Kg per year). However this has been growing at a CAGR of

15-20% over the last decade due to the favorable demographics. India’s

poultry market is ~`5.65bn (3.5 million MT) of which 98% is live poultry and

the rest 2% is processed chicken market. The emergence of malls and hyper

markets is set to change this scenario. The 70% of the industry is organized

while 30% is unorganized.

GAVL through its JV with Godrej Tyson sells fresh and processed chicken

through its brands Real Good chicken and Yummiez. Company has

2

vertically integrated facilities. Company plans to introduce new value added

products and increase its reach in this market.

Exhibit 13: Poultry business growing at 9% CAGR

250

10.0%

9.0%

7.8%

9.0%

6.4%

200

7.3%

8.0%

2.0%

7.0%

150

6.0%

5.0%

100

4.0%

3.0%

50

2.0%

1.0%

0

0.0%

FY13

FY14

FY15

FY16

FY17

Source: DRHP, Angel Research

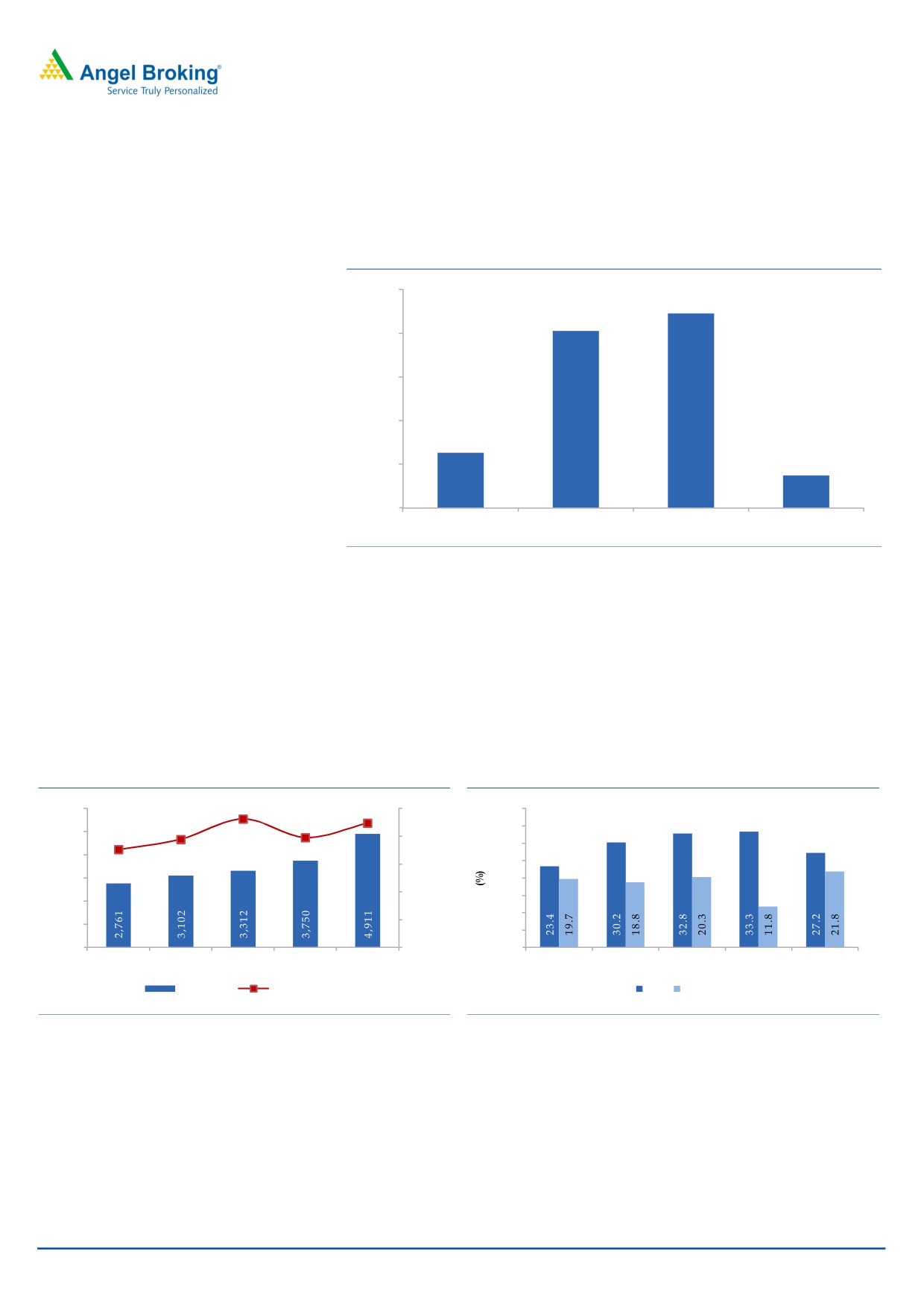

Margin improvement likely with favorable business mix: GAVL is seeing rapid

change in the business mix with rising contribution of segments with higher

operating margins. The vegetable oil and crop protection business clocked

operating margins of 20% and 22% respectively in FY17 and these two businesses

October 3, 2017

8

Godrej Agrovet| IPO Note

contribute 25% of the total revenues in FY17 vs. 18% in FY13. With the growth

expected to be strong going ahead, we believe that GAVL is likely to see

improvement in operating margins which will pave way for higher profitability and

improvement in the return ratios.

Exhibit 14: Margin profile of GAVL’s major segments

25.0%

22.3%

20.3%

20.0%

15.0%

10.0%

6.3%

5.0%

3.7%

0.0%

Animal feed

Vegetable oil

Crop protection

Dairy

Source: DRHP, Angel Research

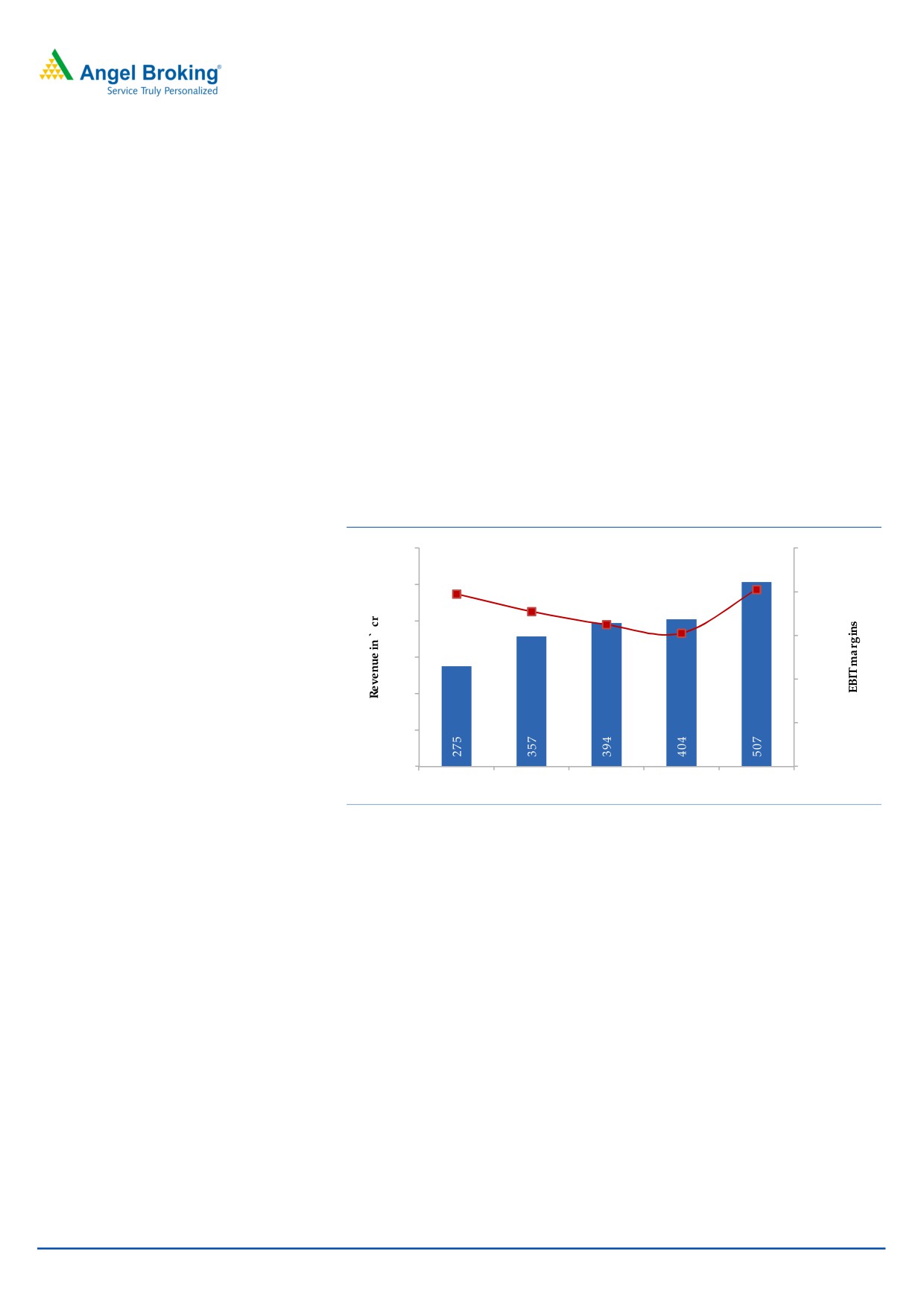

Proven track record of profitability and returns: GAVL has shown a strong track

record of growth and profitability. Company has clocked a top line CAGR of

15.6% between FY13-FY17. Thanks to its favorable business mix, margins have

improved from 7% in FY13 to 8.9% in FY17. Its poultry JV during this period has

shown a CAGR of 9% and has shown turned around from loss of `11cr in FY13 to

profit of `15cr in FY17. Similarly its Bangladesh JV in animal feed business has

seen revenue CAGR of 16% (FY13-17). The Bangladesh JV has also seen a

turnaround with profit of `23cr in FY17 from loss of `4cr in FY13.

Exhibit 15: Sales CAGR of 15.5%, Margins improving

Exhibit 16: Trends in ROE and ROCE

9.2%

6,000

8.9%

10.0%

40.0

7.8%

7.9%

35.0

5,000

7.0%

8.0%

30.0

4,000

6.0%

25.0

3,000

20.0

4.0%

15.0

2,000

10.0

2.0%

1,000

5.0

0

0.0%

-

FY13

FY14

FY15

FY16

FY17

FY13

FY14

FY15

FY16

FY17

Net sales

EBITDA marigns

ROE ROCE

Source: Company, Angel Research

Source: Company, Angel Research

Owing to the strong growth in the business, PAT has grown at 2.6x over the last

five years (CAGR of 27%). The return on equity has also moved up from 23% in

FY13 to 27% in FY17 with >30% ROE between FY14-FY16. Company has a

strong balance sheet with debt of `660cr and debt to equity ratio of 0.6x in FY17.

Working capital days had increased in FY15 and FY16; however the same has

seen improvement in FY17.

October 3, 2017

9

Godrej Agrovet| IPO Note

Outlook and Valuation:

At the upper end of the price band (`450-`460), company is asking for a market

cap of `8,835cr, at the PE multiple of 33.5x of its FY17 adj. PAT. While there is no

exact peer to compare with GAVL’s diversified business, we note that businesses

which are present in at least one of the segments of GAVL, trade in a PE multiple

range of 22x-57x and ROE profile range of 15%-30%. At 33.5x, GAVL does not

appear expensive as PE multiple is in the mid of this range and ROE is at the

higher end of the range. We assign a subscribe rating to this IPO considering its

diversified business profile, decent margins, strong return ratios, healthy balance

sheet and strong history of its parent.

Downside risks

Higher competition in the existing business

Lower profitability of crop protection and palm oil business

Underperformance of the JVs (ACI Godrej and Godrej Tyson)

October 3, 2017

10

Godrej Agrovet| IPO Note

Income statement

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

Net Sales

2,761

3,102

3,312

3,750

4,911

% chg

12.4

6.7

13.2

31.0

Total Expenditure

2,566

2,861

3,006

3,454

4,472

Raw Material Consumed

2,243

2,504

2,616

2,945

3,796

Personnel Expenses

104

130

133

156

232

Others Expenses

218

227

257

353

444

EBITDA

195

242

306

297

439

% chg

24.1

26.7

(3.1)

48.1

(% of Net Sales)

7.0

7.8

9.2

7.9

8.9

Depreciation& Amortisation

19

28

37

52

75

EBIT

175

214

269

244

365

% chg

22.1

25.8

(9.2)

49.2

(% of Net Sales)

6.3

6.9

8.1

6.5

7.4

Share of equity-accounted

(1)

19

17

33

19

investees, net of tax

Other income

11

15

14

63

57

Interest & other Charges

49

40

65

98

86

Recurring PBT

137

207

234

242

354

% chg

51.3

13.1

3.3

46.3

Exceptional Items

-

-

36

95

20

PBT (reported)

137

207

271

337

374

Tax

40

51

61

75

100

(% of PBT)

29.4

24.4

22.4

22.4

26.6

PAT before MI

97

157

210

261

274

Minority Interest (after tax)

-

-

-

-

-

Profit/Loss of Associate Company

-

-

-

-

-

PAT after MI(reported)

97

157

210

261

274

Exceptional Items

-

-

-

-

-

Reported PAT

97

157

210

261

274

% chg

61.8

34.2

24.3

5.1

(% of Net Sales)

3.5

5.0

6.3

7.0

5.6

Basic EPS (`)

5.2

8.4

9.4

9.0

13.7

Fully Diluted EPS (`)

5.2

8.4

9.4

9.0

13.7

% chg

61.8

10.9

(4.1)

52.8

Source: DRHP, Angel Research

October 3, 2017

11

Godrej Agrovet| IPO Note

Balance Sheet

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

SOURCES OF FUNDS

Equity Share Capital

13

13

93

93

185

Reserves& Surplus

400

505

548

691

825

Shareholders’ Funds

414

519

640

783

1,010

Minority Interest

-

-

-

232

254

Total Loans

476

620

685

1,281

660

Other long term liabilities

1

8

12

54

51

Long-term provisions

9

12

14

20

27

Deferred Tax Liability

26

43

57

146

167

Total Liabilities

925

1,203

1,407

2,517

2,169

APPLICATION OF FUNDS

Gross Block

308

486

602

1,147

1,340

Less: Acc. Depreciation

21

46

80

49

118

Net Block

287

440

522

1,099

1,222

Intangible assets

33

26

22

256

251

Biological assets

18

18

12

9

5

Capital Work in Progress

125

149

138

62

50

Other non current assets

172

164

238

289

265

Current Assets

580

779

820

1,409

1,422

Inventories

278

319

389

667

738

Sundry Debtors

182

226

269

455

522

Cash

21

114

13

31

54

Loans & Advances

78

86

100

149

34

Other Assets

20

34

49

107

75

Current liabilities

289

374

346

607

1,046

Net Current Assets

291

405

474

802

376

Total Assets

925

1,203

1,407

2,517

2,169

Source: DRHP, Angel Research

October 3, 2017

12

Godrej Agrovet| IPO Note

Cash Flow Statement

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

Profit before tax

137

207

271

337

374

Depreciation

19

28

37

52

75

Change in Working Capital

(127)

(23)

(209)

(273)

442

Interest / Dividend (Net)

49

40

65

98

86

Direct taxes paid

(33)

(42)

(56)

(46)

(80)

Cash Flow from Operations

45

210

109

168

897

(Inc.)/ Dec. in Fixed Assets

(159)

(188)

(112)

(133)

(205)

(Inc.)/ Dec. in Investments

(8)

(3)

(19)

(295)

118

Cash Flow from Investing

(167)

(191)

(131)

(428)

(87)

Issue of Equity

103.1

(0.5)

-

0.2

0.8

Inc./(Dec.) in loans

71.8

145.0

68.6

474.8

(702.7)

Dividend Paid (Incl. Tax)

-

(29.4)

(82.6)

(54.1)

-

Interest / Dividend (Net)

(50.3)

(42.1)

(65.0)

(142.4)

(86.1)

Cash Flow from Financing

125

73

(79)

278

(788)

Inc./(Dec.) in Cash

2

92

(101)

19

22

Opening Cash balances

19

22

114

13

31

Closing Cash balances

21

114

13

31

54

Source: DRHP, Angel Research

October 3, 2017

13

Godrej Agrovet| IPO Note

Key Ratios

Y/E March

FY13

FY14

FY15

FY16

FY17

Valuation Ratio (x)

P/E (on FDEPS)

88.1

54.5

49.1

51.2

33.5

P/CEPS

73.4

46.3

34.5

27.2

24.4

P/BV

20.6

16.4

13.3

10.9

8.4

Dividend yield (%)

0.0

0.3

0.8

0.5

0.0

EV/Sales

3.4

3.0

2.9

2.7

1.9

EV/EBITDA

47.7

38.7

31.1

34.0

21.5

EV / Total Assets

7.6

5.9

5.4

3.2

2.9

Per Share Data (`)

EPS (Basic)

5.2

8.4

9.4

9.0

13.7

EPS (fully diluted)

5.2

8.4

9.4

9.0

13.7

Cash EPS

6.3

9.9

13.3

16.9

18.8

DPS

0.0

1.4

3.8

2.4

0.0

Book Value

22.3

28.0

34.6

42.3

54.5

Returns (%)

ROCE

19.7

18.8

20.3

11.8

21.8

Angel ROIC (Pre-tax)

24.1

24.6

23.1

14.2

27.6

ROE

23.4

30.2

32.8

33.3

27.2

Turnover ratios (x)

Asset Turnover (Gross Block)

9.0

6.4

5.5

3.3

3.7

Inventory / Sales (days)

37

38

43

65

55

Receivables (days)

24

27

30

44

39

Payables (days)

24

27

24

33

62

Working capital cycle (ex-cash) (days)

37

37

49

76

31

Solvency ratios (x)

Net debt to equity

1.1

1.0

1.0

1.6

0.6

Net debt to EBITDA

2.3

2.1

2.2

4.2

1.4

Interest Coverage (EBIT / Interest)

3.6

5.3

4.1

2.5

4.2

Source: DRHP, Angel Research

October 3, 2017

14

Godrej Agrovet| IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager and investment advisor with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

October 3, 2017

15