1QFY2018 Result Update | IT

July 24, 2017

Wipro

NEUTRAL

CMP

`286

Performance Highlights

Target Price

-

(` cr)

1QFY18

4QFY17

% chg (qoq)

1QFY17

% chg (yoy)

Investment Period

12 Months

Net revenue

13,626

13,988

(2.6)

13,599

0.2

EBITDA

2,992

2,818

6.2

2,616

14.4

Stock Info

EBITDA margin (%)

22.0

20.1

181bps

19.2

272bps

Sector

IT

PAT

2,083

2,267

(8.1)

2,059

1.1

Market Cap (` cr)

1,39,374

Source: Company, Angel Research

Net Debt (` cr)

(32,513)

For 1QFY2018 Wipro announced a good set of numbers. The IT services sales came

Beta

0.5

in at US$1,971.7mn v/s. US$1,950mn expected, a qoq growth of 0.9%, while in

52 Week High / Low

291/205

Constant Currency (CC) terms qoq growth of 0.3%.On operating front, the EBIT

Avg. Daily Volume

1,81,148

margins came in at 16.2% v/s. 14.3% in 4QFY2017.This was against the expectations

Face Value (`)

2

of 13.0%. The net profit during the quarter was ` 2,083cr v/s. `1,659cr expected, a

BSE Sensex

32,029

qoq dip of 8.1%. For 2QFY2018, the company expects revenues from its IT Services

Nifty

9,915

business to US$1,962-2,001mn, growth in the range of (0.5)-1.5% qoq. The Board of

Reuters Code

WIPR.BO

Directors approved a buyback proposal for purchase by the company of up to

Bloomberg Code

WPRO@IN

343.75mn equity shares of ₹2 each (representing 7.1% of total equity capital). The

buyback price will be ₹320/share payable in cash for an aggregate amount not

exceeding ₹11,000cr.We maintain our neutral rating.

Shareholding Pattern (%)

Promoters

73.2

Quarterly highlights: The IT services sales came in at US$1,971.7mn v/s.

MF / Banks / Indian Fls

7.1

US$1,950mn expected, a qoq growth of 0.9% qoq, while in Constant Currency (CC)

FII / NRIs / OCBs

13.4

terms qoq growth of 0.3% was registered. In Rupee terms, revenues came in

Indian Public / Others

6.4

at`13,626cr v/s. `12,610cr expected, a qoq dip of 2.6%. On operating front, the EBIT

margins came in at 16.2% v/s. 14.3% in 4QFY2017, mainly driven by the better than

expected growth and internal efficiencies. This was against the expectations of 13.0%.

Abs.(%)

3m 1yr

3yr

The net profit during the quarter was ` 2,082cr v/s. `1,659cr expected, a qoq dip of

Sensex

9.1

15.6

24.6

8.1%. For 2QFY2018, the company expects revenues from its IT Services business to

Wipro

16.1

5.7

5.1

be in the range of $1,962mn to $2,001mn.

Outlook and valuation: The management has set a target of US$15bn of revenue and

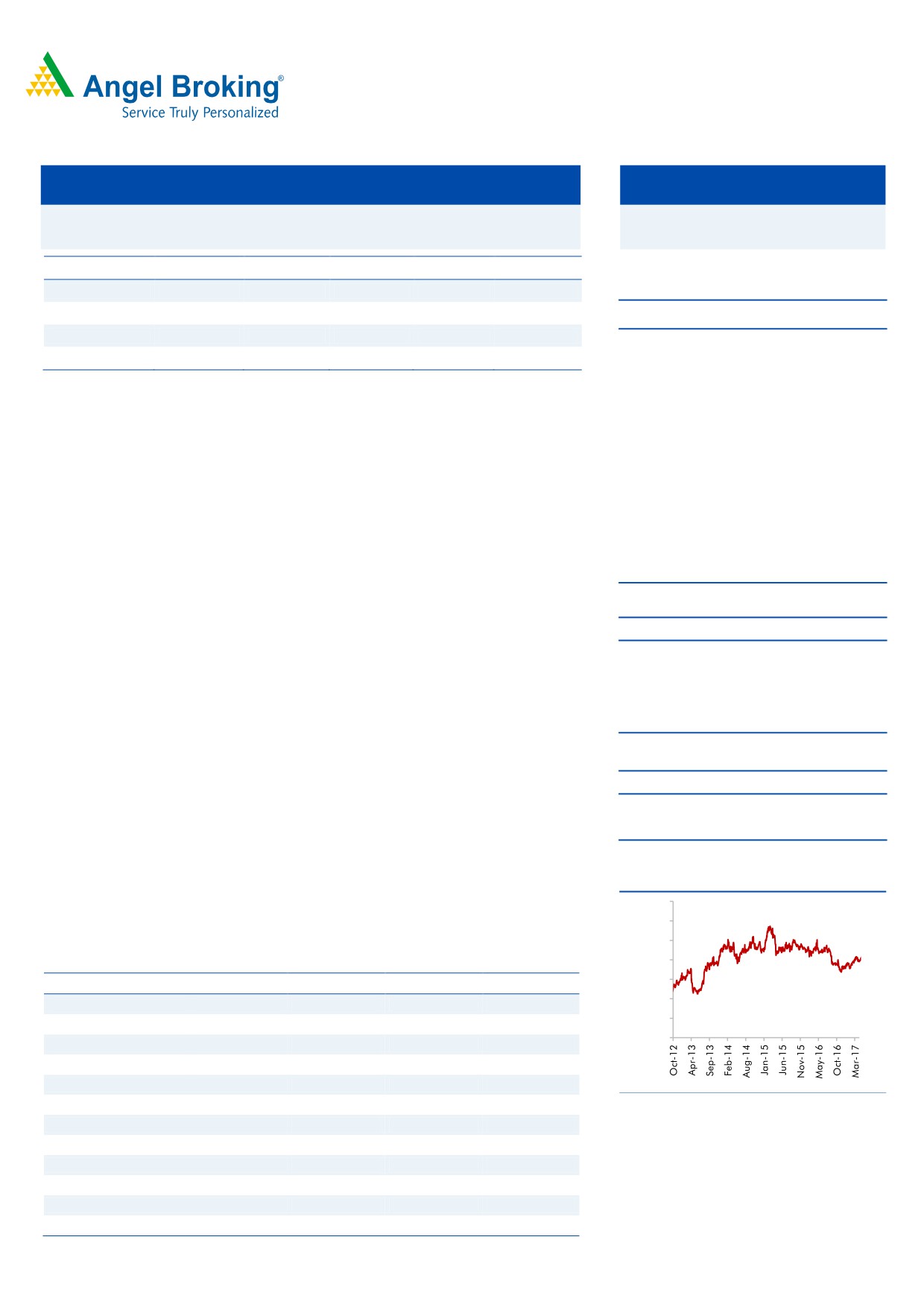

3-year price chart

an EBIT margin of 23% by 2020. However, the near term guidance target appears to be

400

disappointing. Nevertheless, we project a moderate top-line and net profit growth for

350

FY2017-19E. However, given the valuations, we maintain our neutral rating.

300

250

Key financials (Consolidated, IFRS)

200

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

150

Net sales

51,631

55,421

58,536

61,858

100

% chg

10.0

7.3

5.6

5.7

50

Net profit

8,975

8,517

8,863

9,276

% chg

3.7

(5.1)

4.1

4.7

EBITDA margin (%)

21.7

20.4

20.3

20.3

Source: Company, Angel Research

EPS (`)

18.4

17.5

18.2

19.1

P/E (x)

15.5

16.4

15.7

15.0

P/BV (x)

3.0

2.9

2.4

2.1

RoE (%)

19.2

19.2

14.6

13.4

Sarabjit kour Nangra

RoCE (%)

13.4

13.4

10.6

10.2

+91 22-39357800 Ext: 6806

EV/Sales (x)

2.3

2.1

1.7

1.5

EV/EBITDA (x)

10.5

10.4

8.3

7.2

Source: Company, Angel Research; Note: CMP as of July 21, 2017

Please refer to important disclosures at the end of this report

1

Wipro | 1QFY2018 Result Update

Exhibit 1: 1QFY2018 performance (Consolidated, IFRS)

Y/E March (` cr)

1QFY18

4QFY17

% chg (qoq)

1QFY17

% chg (yoy)

FY2017

FY2016

% chg (yoy)

Net revenue

13,626

13,988

(2.6)

13,599

0.2

55,040

51,244

7.4

Cost of revenue

8,893

9,259

(4.0)

9,209

(3.4)

36,844

34,175

7.8

Gross profit

4,733

4,728

0.1

4,390

7.8

18,196

17,069

6.6

SGA expense

1,741

1,910

(8.9)

1,774

(1.9)

7,284

6,272

16.1

EBITDA

2,992

2,818

6.2

2,616

14.4

10,913

10,796

1.1

Dep. and amortisation

818

818

-

430

90.2

2,311

1,497

54.3

EBIT

2,174

2,000

8.7

2,186

(0.6)

8,602

9,299

(7.5)

Other income

508

941

(46.0)

485

4.8

2,434

2,194

10.9

PBT

2,682

2,941

(8.8)

2,671

0.4

11,036

11,493

(4.0)

Income tax

599

674

(11.1)

612

(2.1)

2,521

2,537

(0.6)

PAT

2,083

2,267

(8.1)

2,059

1.1

8,490

8,908

(4.7)

Minority interest

-

-

-

25

49

Adj. PAT

2,083

2,267

(8.1)

2,059

1.1

8,514

8,957

(4.9)

Diluted EPS

4.3

4.7

(8.1)

4.2

1.1

17.5

18.4

(4.9)

Gross margin (%)

34.7

33.8

93bps

32.3

245bps

33.1

33.3

(25)bps

EBITDA margin (%)

22.0

20.1

181bps

19.2

272bps

19.8

21.1

(124)bps

EBIT margin (%)

16.0

14.3

166bps

16.1

(12)bps

15.6

18.1

(252)bps

PAT margin(%)

15.3

16.2

(92)bps

15.1

14bps

15.5

17.5

(201)bps

Source: Company, Angel Research

Exhibit 2: 1QFY2018 - Actual vs Angel estimates

(` cr)

Actual

Estimate

Variation (%)

Net revenue

13,626

12,610

8.1

EBIT margin (%)

16.0

13.0

298bps

PAT

2,083

1,659

25.5

Source: Company, Angel Research

Revenues higher than expected in $ terms

For 1QFY2018 Wipro announced a good set of numbers. The IT services sales

came in at US$1,971.7mn v/s. US$1,950mn expected, a qoq growth of 0.9%

qoq, while in Constant Currency (CC) terms qoq growth of 0.3% was registered. In

Rupee terms, revenues came in at `13,626cr v/s. `12,610cr expected, a qoq dip

of 2.6%.

In terms of geography, the CC growth was - USA (0.2% qoq), Europe (-2.6% qoq),

India & Middle East (5.1% qoq), while APAC & Other Emerging markets de-grew

(2.6% qoq). In terms of verticals, the CC growth was Manufacturing and

Technology (-0.9% qoq), Finance Solutions (3.2% qoq), Consumer Business Unit

(0.1% qoq), Energy, Natural Resources & Utilities (2.2% qoq). The verticals which

dipped were - Communications (-2.6% qoq) and Healthcare, Life Sciences &

Services (-3.1% qoq).

Going into FY2018, the company is very cautious and expects a decline in the

verticals like Healthcare and Retail. Also, the ongoing restructuring in its India and

Middle East business is expected to pose pressure in FY2018.

July 24, 2017

2

Wipro | 1QFY2018 Result Update

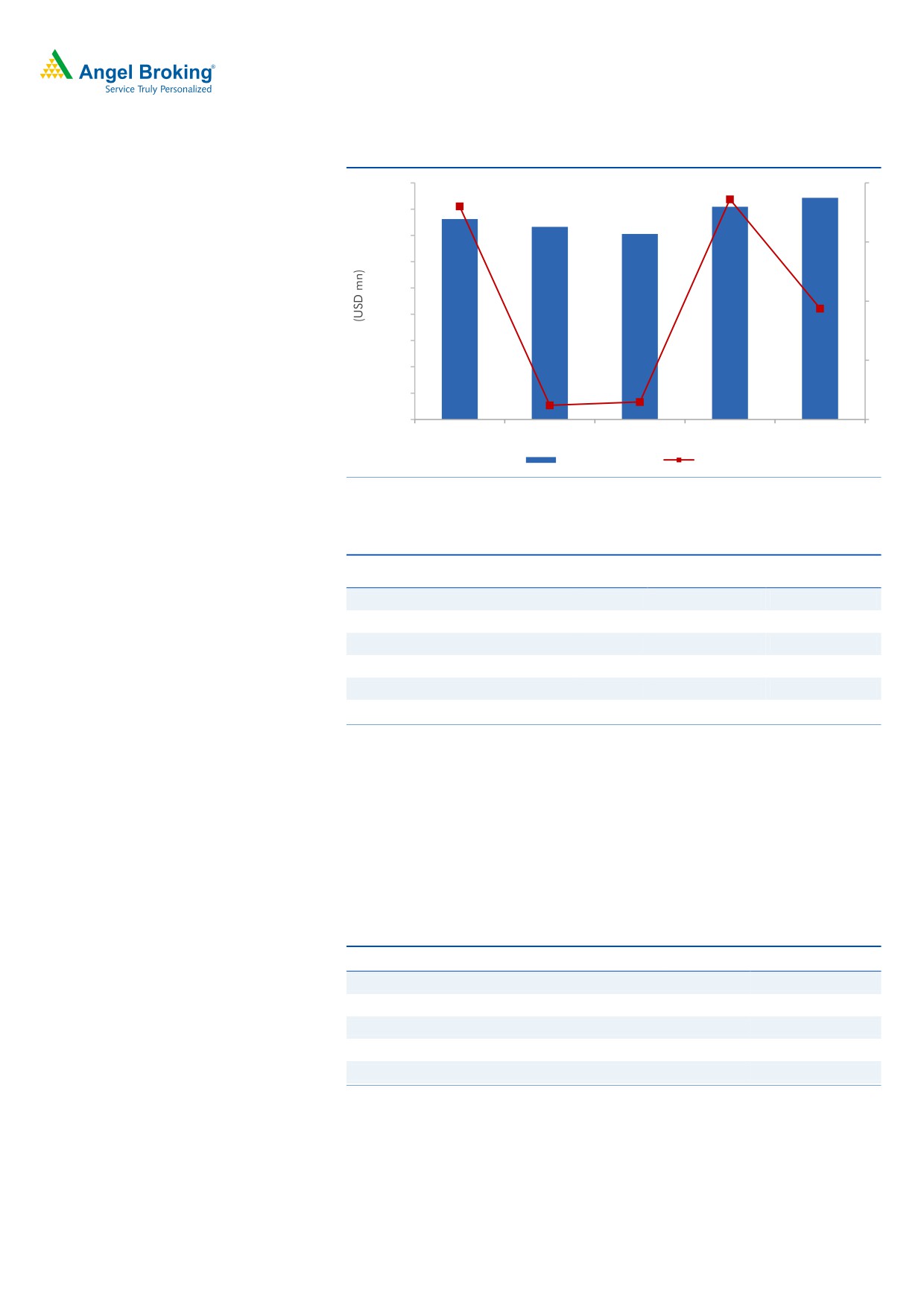

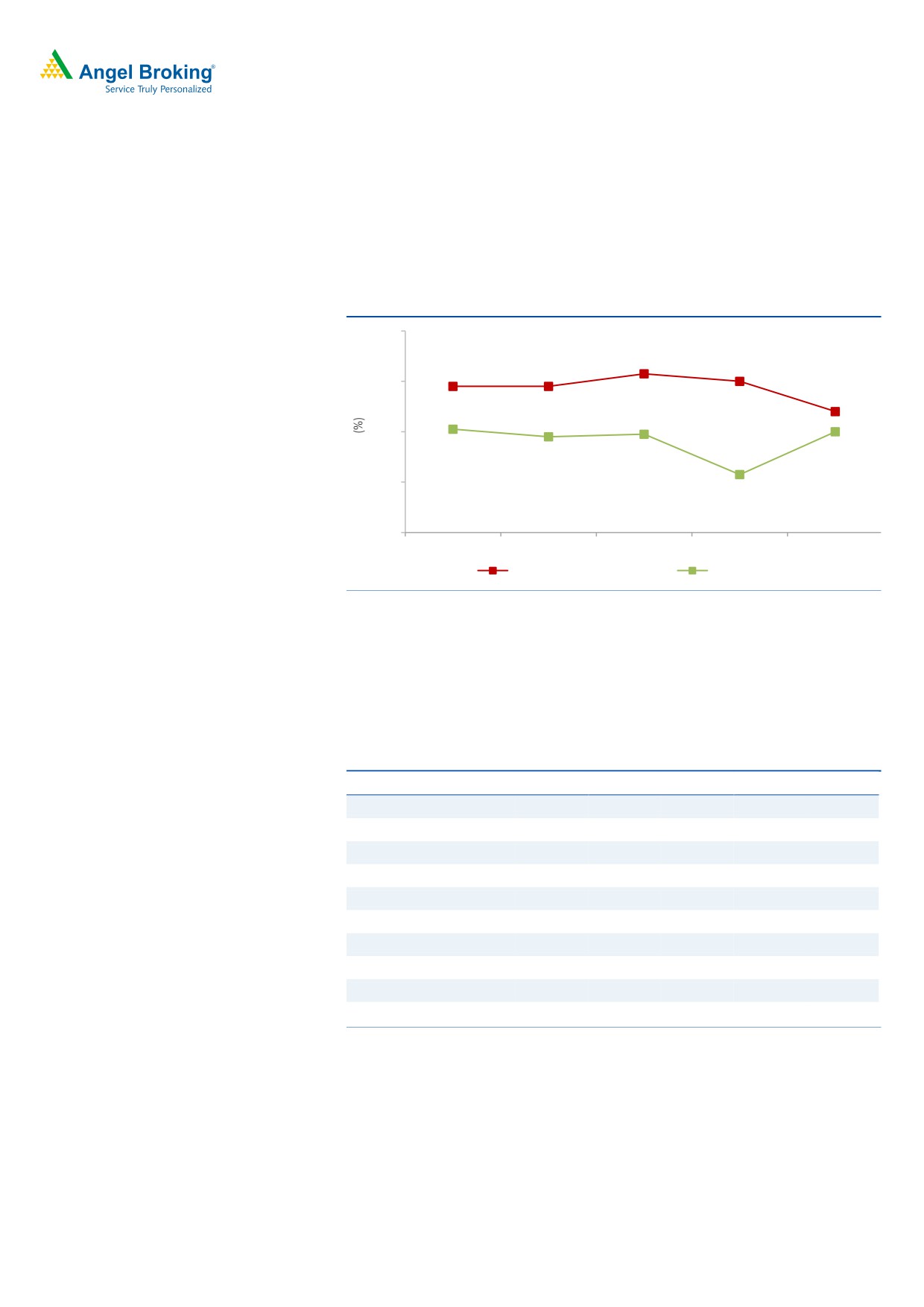

Exhibit 3: Trend in IT Services revenue

2,000

1,931

1955

1971.7

3

1,916

2.6

1,950

1903

2.7

1,900

2

1,850

1,800

1

0.9

1,750

1,700

0

1,650

1,600

(0.7)

1,550

(0.8)

-

1QFY17

2QFY17

3QFY17

4QFY17

1QFY18

IT services

qoq growth (%)

Source: Company, Angel Research

Exhibit 4: Revenue growth (Industry wise - CC basis)

% to

% growth

% growth

revenue

(QoQ)

(yoy)

Global media and telecom

6.8

(2.6)

(7.8)

Financial solutions

26.7

3.2

7.0

Manufacturing and hi-tech

22.5

(0.9)

2.6

Healthcare, life sciences and services

14.8

(3.1)

(0.6)

Consumer

15.8

0.1

2.9

Energy and utilities

13.4

2.2

7.0

Source: Company, Angel Research

Services wise, Wipro’s anchor service lines ADM (contributed 45.8% to revenue)

and Technology Infrastructure Services (contributed 28.1% to revenue) registering a

growth of 0.6% qoq and a growth of 0.6% qoq respectively. Analytics and

Information Management, which contributed 7.0% of sales, grew by 3.6% qoq,

while, Product Engineering and Mobility contributed 7.0% of sales and de-grew by

1.8% qoq.

Exhibit 5: Revenue growth (Service wise)

Service verticals

% to revenue

% growth (qoq)

Technology infrastructure services

28.1

0.2

Analytics and information management

7.0

3.6

BPO

12.0

(1.6)

Product engineering and mobility

7.0

(1.8)

ADM

45.8

0.6

Source: Company, Angel Research

Geography wise, the developed economies such as America and Europe grew by

0.2% qoq and -2.6% qoq in CC terms respectively. India posted a 5.1% qoq CC

growth during the period. However, APAC and other emerging markets posted a

2.6% qoq de-growth for the quarter.

July 24, 2017

3

Wipro | 1QFY2018 Result Update

Exhibit 6: Revenue growth (Geography wise, CC basis)

% to revenue

% growth (QoQ)

% growth (yoy)

America

54.5

0.2

4.2

Europe

24.2

(2.6)

3.1

India and Middle East

10.9

5.1

(0.1)

APAC and other emerging markets

10.4

2.6

3.2

Source: Company, Angel Research

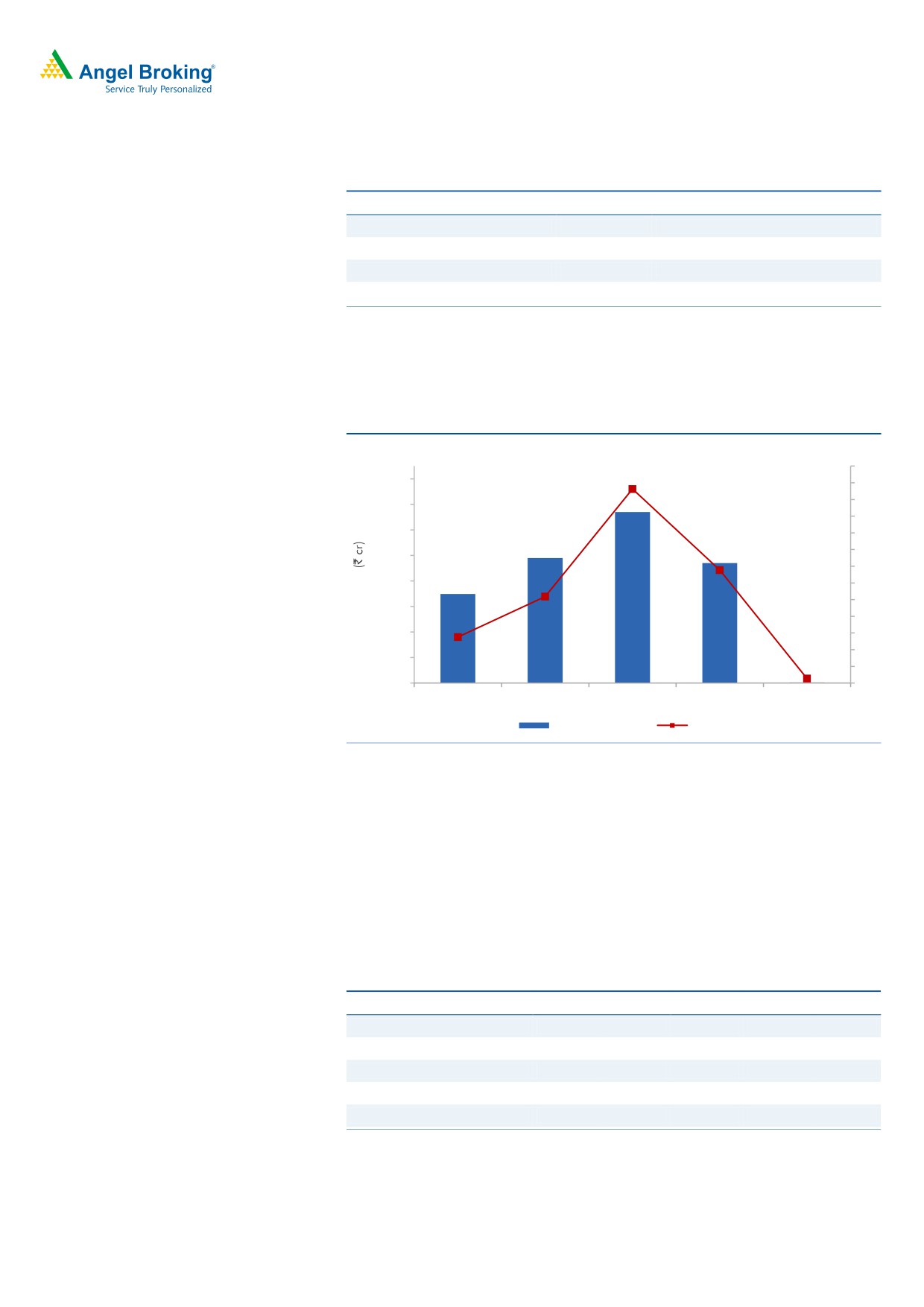

The IT Products segment reported a 77.3% yoy de-growth in revenue to `102cr

during the quarter.

Exhibit 7: IT Products - Revenue growth (yoy)

50

900

36.3

40

30

800

20

700

770

10

(12.3)

0

600

590

-10

500

570

-20

(28.2)

-30

400

(77.3)

-40

300

449

-50

(52.5)

-60

200

-70

100

-80

4QFY16

1QFY2017

2QFY17

3QFY17

4QFY17

IT products

yoy growth (%)

Source: Company, Angel Research

Hiring and utilization

Wipro reported a net addition of 1,309 employees in its IT Services employee

base, which now stands at 1,66,790 employees. Though voluntary attritions

(annualized) in the global IT business have increased considerably, it remained

stagnant on a net basis at 15.9%. The utilization rate of the global IT business

moved down by 100bps sequentially to 72.0%. Going ahead, an improvement in

utilization level will be an important margin lever.

Exhibit 8: Employee pyramid

Employee pyramid

1QFY17

2QFY17

3QFY17

4QFY17

1QFY18

Utilization - Global IT (%)

69.9

71.2

71.6

73.1

72.0

Attrition (%)

Global IT

16.5

16.6

16.3

16.3

15.9

BPO

11.7

12.2

10.7

11.2

12.8

Net additions

951

375

4,891

2,353

1,309

Source: Company, Angel Research

July 24, 2017

4

Wipro | 1QFY2018 Result Update

Margins higher than expected

On EBIT front, the company posted EBIT of 16.0% (13.0% expected) v/s 14.3% in

4QFY2017, expansion of 166bps qoq, mainly aided by improved profitability in

the product business. The company expects to contain margins in a narrow band

of 17.5-18%, which it achieved in FY2017.

Exhibit 9: Segment-wise EBIT margin trend

20

18.3

18.0

17.8

17.8

16.8

18

16

16.1

16.0

15.8

15.9

14

14.3

12

1QFY2017

2QFY17

3QFY17

4QFY17

1QFY18

IT services

Consolidated

Source: Company, Angel Research

Client pyramid

Wipro added 45 new clients during the quarter with its active client base now

standing at 1,244. Amongst these, 2 have been in the US$75mn+ bracket and 9

in the US$5mn+ bracket.

Exhibit 10: Client metrics

Particulars

1QFY17

2QFY17

3QFY17

4QFY17

1QFY18

US$100mn plus

9

8

9

9

9

US$75mn-$100mn

10

11

8

9

9

US$50mn-$75mn

14

14

16

16

18

US$20mn-$50mn

58

58

57

57

54

US$10mn-$20mn

79

80

80

72

73

US$5mn-$10mn

82

87

94

100

99

US$3mn-$5mn

84

83

85

86

95

US$1mn-$3mn

229

230

227

248

267

New client addition

50

47

108

51

45

Active customers

1,208

1,180

1,259

1,323

1,244

Source: Company, Angel Research

July 24, 2017

5

Wipro | 1QFY2018 Result Update

Investment highlights

Grim outlook on growth: For 2QFY2018, the company has given a revenue

guidance of US$1,962-2,001mn implying a US$ qoq growth in the range of -0.5-

1.5% in CC terms. The outlook factors in the decline in performance of the

verticals like Healthcare and Retail. With this, the ongoing restructuring in

company’s India and Middle East business would be an additional deterrent to the

growth in FY2018. We expect US$ and INR revenue CAGR to be at 5.6% over

FY2017-19E.

Target sales CAGR of 20% and EBIT Margin of 23%: Company, as part of its vision

for 2020 is targeting to reach US$15bn revenues with 23% EBIT margin, implying

revenue CAGR of ~20% over the next four years. If the margins expand by

300bps, then it would imply an even higher CAGR for earnings. Going by the

guidance, the company’s organic growth outlook is not even closer to its peers.

However, on the acquisition front, the company has been very aggressive in

comparison to its peers. Also, given the Brexit in FY2016, and performance in

FY2017, the company remains well short of the run-rate implied in achieving the

aspiration, thereby making the goal difficult for the remainder period.

During 4QFY2017, company announced the acquisition of Appirio, a leading

cloud services company in areas like Sales force and Workday implementation.

Appirio’s CY2015 revenue was US$196mn and purchase consideration for the

acquisition is US$500mn. Its customers include Virgin America, Four Seasons

Hotels & Resorts, Coca Cola, eBay, Home Depot, Honeywell, NYSE Euronext,

Toyota and Facebook, among others.

Earlier, the company had acquired HealthPlan Services from Water Street

Healthcare Partners. Since partnering with Water Street in 2008, HealthPlan

Services has grown to become the leading independent technology and Business

Process as a Service (BPaaS) provider in the US health insurance market. As part of

the agreement, Wipro will acquire 100% of HealthPlan Services' shares for a

purchase consideration of US$460mn. Headquartered in Tampa, Florida,

HealthPlan Services employs over 2,000 associates. It offers market-leading

technology platforms and a fully integrated BPaaS solution to health insurance

companies in the individual, group and ancillary markets. HealthPlan Services’

BPaaS solutions are ideal for players who want to operate in the private and public

exchanges and the off-exchange individual market in the US.

Outlook and valuation

The new CEO of the company has put in place an aggressive target of 20%

revenue CAGR over the next four years, with much improved profitability (where

the company has significant levers in the form of automation and improving

utilization levels), which looks steep in the given circumstances. The Board of

Directors approved a buyback proposal for purchase by the company of up to

343.75mn equity shares of ₹2 each (representing 7.1% of total equity capital).The

buyback price will be ₹320 per equity share payable in cash for an aggregate amount

not exceeding ₹11,000cr.

July 24, 2017

6

Wipro | 1QFY2018 Result Update

On the valuation front, the stock is currently trading at 15.7x its FY2018E and

15.0x its FY2019E EPS. We recommend our neutral rating on the stock.

Exhibit 11: Key assumptions

FY2018E

FY2019E

Revenue growth - IT services (USD)

6.5

6.5

USD-INR rate (realized)

67.0

67.0

Revenue growth - Consolidated (`)

5.6

5.7

EBITDA margin (%)

20.3

20.3

Tax rate (%)

22.8

22.8

EPS growth (%)

4.1

4.7

Source: Company, Angel Research

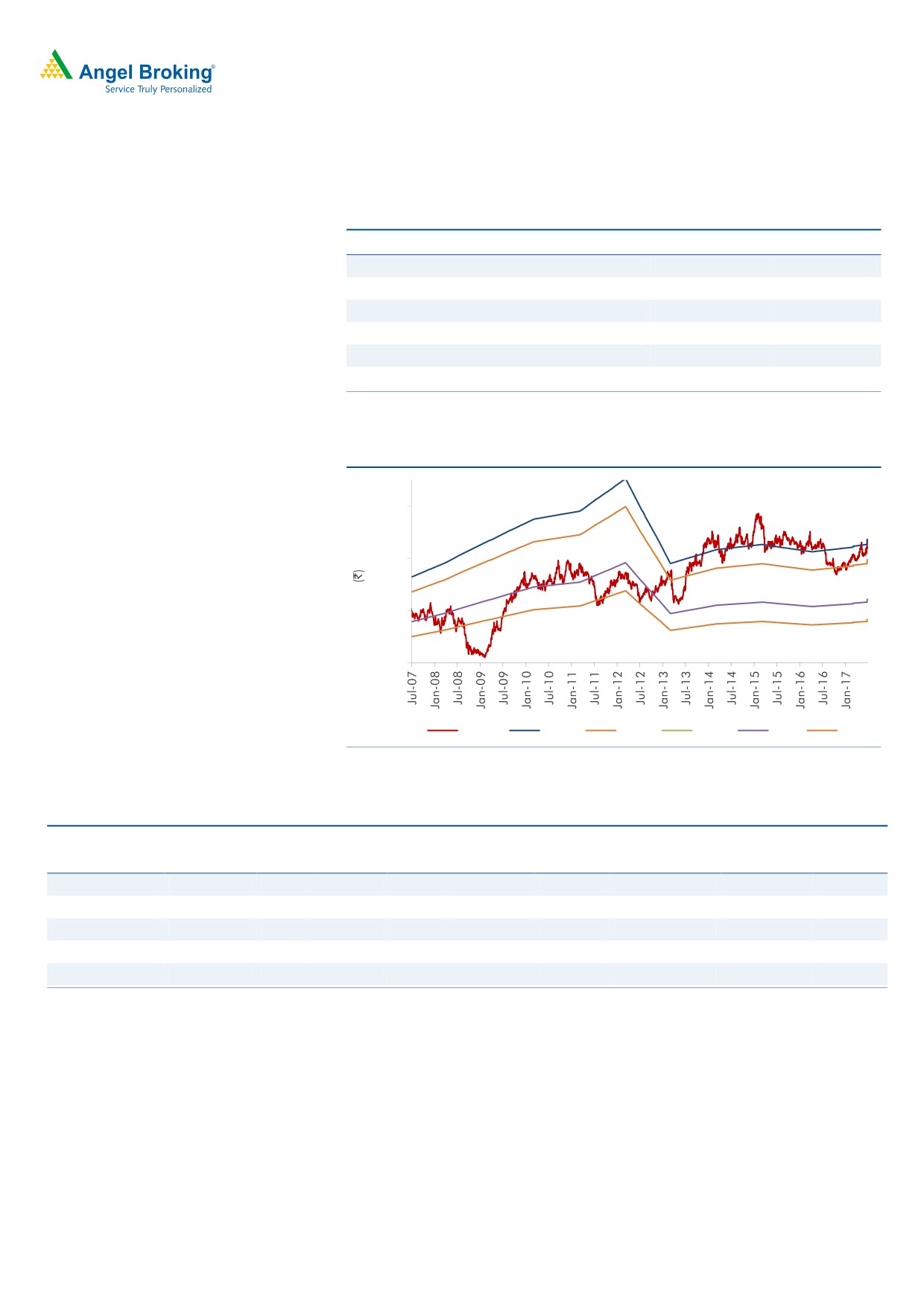

Exhibit 12: One-year forward PE chart

350

250

150

50

Price

15x

13x

11x

9x

7x

Source: Company, Angel Research

Exhibit 13: Recommendation summary

Company

Reco

CMP

Tgt. price

Upside

FY2019E

FY2019E

FY2017-19E

FY2019E

FY2019E

(`)

(`)

(%)

EBITDA (%)

P/E (x)

EPS CAGR (%)

EV/Sales (x)

RoE (%)

HCL Tech

Accumulate

905

1,014

12.1

20.9

13.4

6.2

1.8

20.6

Infosys

Buy

980

1,179

20.3

26.0

14.1

5.3

2.2

19.6

TCS

Accumulate

2,491

2,651

6.4

27.6

15.4

7.8

3.1

29.8

Tech Mahindra

Buy

395

533

34.9

15.0

10.4

8.6

1.1

16.3

Wipro

Neutral

286

-

-

20.3

15.0

4.4

1.5

13.4

Source: Company, Angel Research

Company background

Wipro is among the leading Indian companies, majorly offering IT services. The

company is also engaged in the IT hardware (10% of sales) business. Wipro's IT

arm is India's fourth largest IT firm, employing more than 181,482 professionals,

offering a wide portfolio of services such as ADM, consulting and package

implementation, and servicing more than 1,000 clients.

July 24, 2017

7

Wipro | 1QFY2018 Result Update

Profit & Loss account (Consolidated, IFRS)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

Net revenue

46,955

51,631

55,421

58,536

61,858

Cost of revenues

30,846

34,325

36,844

38,927

41,135

Gross profit

16,108

17,306

18,577

19,610

20,722

% of net sales

34.3

33.5

33.5

33.5

33.5

Selling and mktg exp.

3,063

3,319

4,082

4,332

4,577

% of net sales

6.5

6.4

7.4

7.4

7.4

General and admin exp.

2,585

2,788

3,202

3,395

3,588

% of net sales

5.5

5.4

5.8

5.8

5.8

Depreciation and amortization

1,282

1,496

2,310

2,459

2,598

% of net sales

2.7

2.9

4.2

4.2

4.2

EBIT

9,179

9,703

8,983

9,424

9,959

% of net sales

19.5

18.8

16.2

16.1

16.1

Other income, net

1,990

1,770

2,056

2,056

2,056

Share in profits of eq. acc. ass.

0

0

0

0

0

Profit before tax

11,168

11,473

11,039

11,480

12,015

Provision for tax

2,462

2,498

2,521

2,618

2,739

% of PBT

22.0

21.8

21.8

22.8

22.8

PAT

8,706

8,975

8,517

8,863

9,276

Share in earnings of associate

-

-

-

-

-

Minority interest

53

-

-

-

-

Adj. PAT

8,653

8,975

8,517

8,863

9,276

Diluted EPS (`)

17.8

18.4

17.5

18.2

19.1

July 24, 2017

8

Wipro | 1QFY2018 Result Update

Balance sheet (Consolidated, IFRS)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

Assets

Goodwill

6,808

10,199

12,580

12,580

12,580

Intangible assets

793

1,584

1,592

1,584

1,584

Property, plant & equipment

5,421

6,495

6,979

7,279

7,579

Investment in equ. acc. investees

387

491

710

710

710

Derivative assets

74

26

11

26

11

Non-current tax assets

1,141

1,175

1,201

1,201

1,201

Deferred tax assets

295

380

310

310

310

Other non-current assets

1,437

1,583

2,079

2,079

2,079

Total non-current assets

16,354

21,933

25,462

25,769

26,054

Inventories

485

539

392

392

392

Trade receivables

9,153

10,238

9,485

9,951

10,516

Other current assets

7,336

10,407

3,075

3,075

3,075

Unbilled revenues

4,234

4,827

4,510

4,510

4,510

Available for sale investments

5,391

13,294

29,203

37,191

45,410

Current tax assets

649

781

980

980

980

Derivative assets

508

568

975

975

975

Cash and cash equivalents

15,894

9902

5271

5688

5889

Total current assets

43,649

50,556

53,890

62,762

71,745

Total assets

60,003

72,489

79,352

88,531

97,799

Equity

Share capital

493

494

973

973

973

Share premium

1,403

1,462

47

47

47

Retained earnings

37,225

42,574

48,606

56,983

65,772

Share based payment reserve

131

223

356

356

356

Other components of equity

1,545

1,853

2,049

2,049

2,049

Shares held by controlled trust

-

-

-

-

-

Eq. attrib. to shareholders of Co.

40,789

46,606

52,031

60,407

69,197

Minority interest

165

222

239

239

239

Total equity

40,954

46,828

52,270

60,646

69,436

Liabilities

Long term loans and borrowings

1,271

1,736

1,961

1,961

1,961

Deferred tax liability

324

511

661

661

661

Derivative liabilities

16

12

0

-

0

Non-current tax liability

670

823

955

955

955

Other non-current liabilities

366

723

550

550

550

Provisions

1

-

-

-

-

Total non-current liabilities

2647

3804

4127

4127

4127

Loans and bank overdraft

6,621

10,786

12,280

12,280

12,280

Trade payables

5,875

6,819

6,549

6,890

7,281

Unearned revenues

1,655

1,808

1,615

1,878

1,879

Current tax liabilities

804

702

810

1,047

1,096

Derivative liabilities

75

234

271

234

271

Other current liabilities

1,222

1,382

1,303

1,303

1,303

Provisions

152

126

127

126

127

Total current liabilities

16,403

21,856

22,954

23,758

24,236

Total liabilities

19,050

25,661

27,082

27,885

28,363

Total equity and liabilities

60,003

72,489

79,352

88,531

97,799

July 24, 2017

9

Wipro | 1QFY2018 Result Update

Cash flow statement (Consolidated, IFRS)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

Pre tax profit from operations

11,168

11,473

11,473

11,480

12,015

Depreciation

1,282

1,496

1,496

2,459

2,598

Expenses (deferred)/written off

(13)

(13)

(13)

(13)

(13)

Pre tax cash from operations

12,438

12,956

12,956

13,926

14,600

Other income/prior period ad

1,990

1,770

2,056

2,056

2,056

Net cash from operations

14,428

14,726

15,012

15,982

16,656

Tax

(2,462)

(2,498)

(2,521)

(2,618)

(2,739)

Cash profits

11,965

12,228

12,491

13,365

13,917

(Inc)/dec in current assets

(8,181)

(6,906)

(3,334)

(8,872)

(8,983)

Inc/(dec) in current liab.

2,757

5,453

1,098

803

478

Net trade working capital

(5,423)

(1,453)

(2,236)

(8,069)

(8,505)

Cashflow from oper. actv.

6,542

10,775

10,255

5,296

5,412

(Inc)/dec in fixed assets

(276)

(1,075)

(484)

(300)

(300)

(Inc)/dec in intangibles

(600)

(791)

(8)

8

-

(Inc)/dec in investments

(119)

(104)

(220)

-

-

(Inc)/dec in net def. tax assets

-

-

-

-

-

(Inc)/dec in derivative assets

-

-

-

-

-

(Inc)/dec in non-current tax asset

7

146

496

-

-

(Inc)/dec in minority interest

9

(53)

-

-

-

Inc/(dec) in other non-current liab

273

510

(41)

-

-

(Inc)/dec in other non-current ast.

(122)

(34)

(26)

-

-

Cashflow from investing activities

(826)

(1,401)

(1,401)

(282)

(292)

Inc/(dec) in debt

180

465

-

225

-

Inc/(dec) in equity/premium

314

(14,052)

(12,999)

(4,335)

(4,434)

Dividends

(1,736)

(3,504)

(486)

(486)

(486)

Cashflow from financing activities

(1,242)

(17,090)

(13,485)

(4,596)

(4,920)

Cash generated/(utilized)

4,474

(7,716)

(4,631)

418

200

Cash at start of the year

11,420

15,894

9,902

5,271

5,688

Cash at end of the year

15,894

9,902

5,271

5,688

5,889

July 24, 2017

10

Wipro | 1QFY2018 Result Update

Key Ratios

Y/E March

FY2015

FY2016

FY2017

FY2018E

FY2019E

Valuation ratio (x)

P/E (on FDEPS)

16.1

15.5

16.4

15.7

15.0

P/CEPS

7.1

13.3

13.3

12.3

11.7

P/BVPS

1.7

3.0

2.9

2.4

2.1

Dividend yield (%)

4.2

2.1

0.3

0.3

0.3

EV/Sales

2.5

2.3

2.1

1.7

1.5

EV/EBITDA

11.4

10.5

10.4

8.3

7.2

EV/Total assets

2.0

1.6

1.5

1.1

0.9

Per share data (`)

EPS (Fully diluted)

17.8

18.4

18.4

18.2

19.1

Cash EPS

40.2

21.5

21.5

23.3

24.4

Dividend

12.0

6.0

1.0

1.0

1.0

Book value

165.7

96.2

99.9

117.1

135.2

Return ratios (%)

RoCE (pre-tax)

15.3

13.4

13.4

10.6

10.2

Angel RoIC

28.8

24.8

24.8

28.5

29.4

RoE

21.1

19.2

19.2

14.6

13.4

Turnover ratios(x)

Asset turnover (fixed assets)

8.9

8.7

7.9

8.5

8.5

Receivables days

69

69

70

71

72

Payable days

67

67

67

67

67

July 24, 2017

11

Wipro | 1QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Wipro

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

July 24, 2017

12