1QFY2018 Result Update | Pharmaceutical

August 14, 2017

Indoco Remedies

SELL

CMP

`191

Performance Highlights

Target Price

`153

Y/E March (` cr)

1QFY18

4QFY17

% chg (qoq) 1QFY17

% chg (yoy)

Investment Period

-

Net sales

204

266

(23.1)

253

(19.1)

Other operating income

6

13

(56.7)

5

13.9

Stock Info

Gross profit

133

168

(20.9)

164

(18.7)

Operating profit

(3)

21

-

37

-

Sector

Pharmaceutical

Net profit

(22)

18

-

20

-

Market Cap (` cr)

1,760

Source: Company, Angel Research

Net Debt (` cr)

188

For 1QFY2018 Indoco Remedies posted poor set of numbers. Sales came in at `204cr

Beta

0.2

(`214cr expected) v/s. `253cr in 1QFY2017, a yoy de-growth of 19.1%. The company

52 Week High / Low

360/179

witnessed a disruptive 1QFY2018, with domestic as well International sales getting

Avg. Daily Volume

13,718

affected adversely due to GST implementation in India and voluntary stoppage of

Face Value (`)

2

ophthalmic product supplies to US respectively. On operating front, the EBITDA

BSE Sensex

31,214

margins came in at (1.7%) ((0.9%) expected) v/s. 14.7% in 1QFY2017, mainly on the

Nifty

9,711

back of lower than expected sales during the quarter. Thus, the PAT came in at `

Reuters Code

INRM.BO

(21.7)cr (`(13.8)cr expected) v/s. `19.7cr in 1QFY2017. We maintain our sell rating

Bloomberg Code

INDR@IN

on the stock, with a price target of `153.

Results lower than expected: Sales came in at `204cr (`214cr expected) v/s. `253cr in

1QFY2017, a yoy de-growth of

19.1%. The company witnessed a disruptive

Shareholding Pattern (%)

1QFY2018, with domestic as well International sales getting affected adversely due to

Promoters

59.1

GST implementation in India and voluntary stoppage of ophthalmic product supplies

MF / Banks / Indian Fls

12.1

to US respectively. The formulation sales (`185.7cr; 90.9% of sales in 1QFY2018)

FII / NRIs / OCBs

11.9

posted a dip of 20.7% yoy. The domestic formulation sales (`99.7cr) registered a dip

Indian Public / Others

17.0

of 29.7% yoy. The International formulation sales (`86.0cr) posted a yoy dip of 6.9%.

The API sales (`14.9cr) posted a yoy dip of 15.1%. On operating front, the EBITDA

margins came in at (1.7%) ((0.9%) expected) v/s. 14.7% in 1QFY2017, mainly on the

Abs. (%)

3m 1yr 3yr

back of lower than expected sales during the quarter. Gross margins came in at 65.2%

Sensex

4.8

12.0

22.3

v/s. 64.8% in 1QFY2017; while R&D expenses were 6.6% of sales in 1QFY2018 v/s.

Indoco

(18.7)

(39.9)

(15.8)

4.7% of sales in 1QFY2017. Thus, the PAT came in at ` (21.7)cr (`(13.8)cr expected)

v/s. `19.7cr in 1QFY2017.

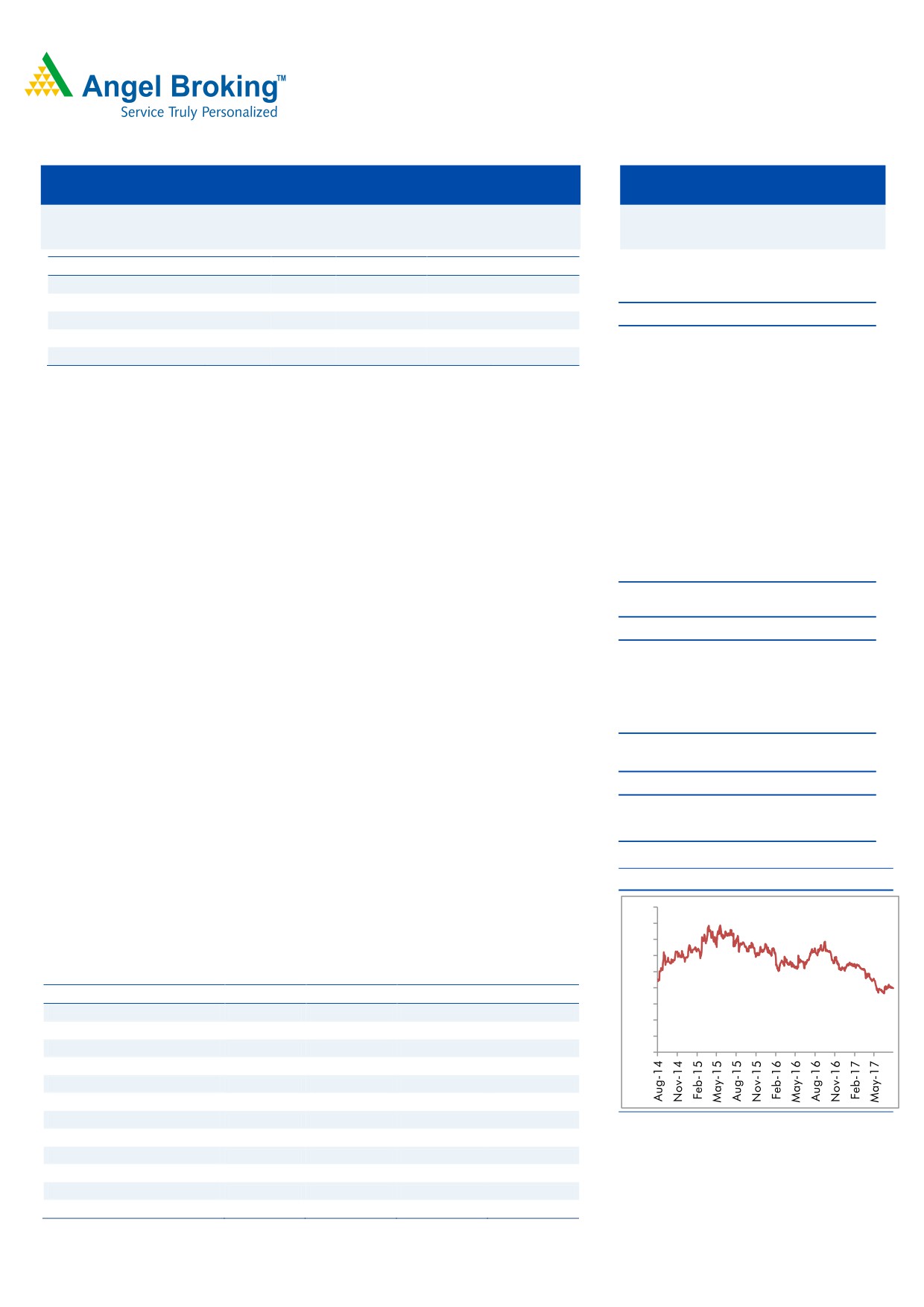

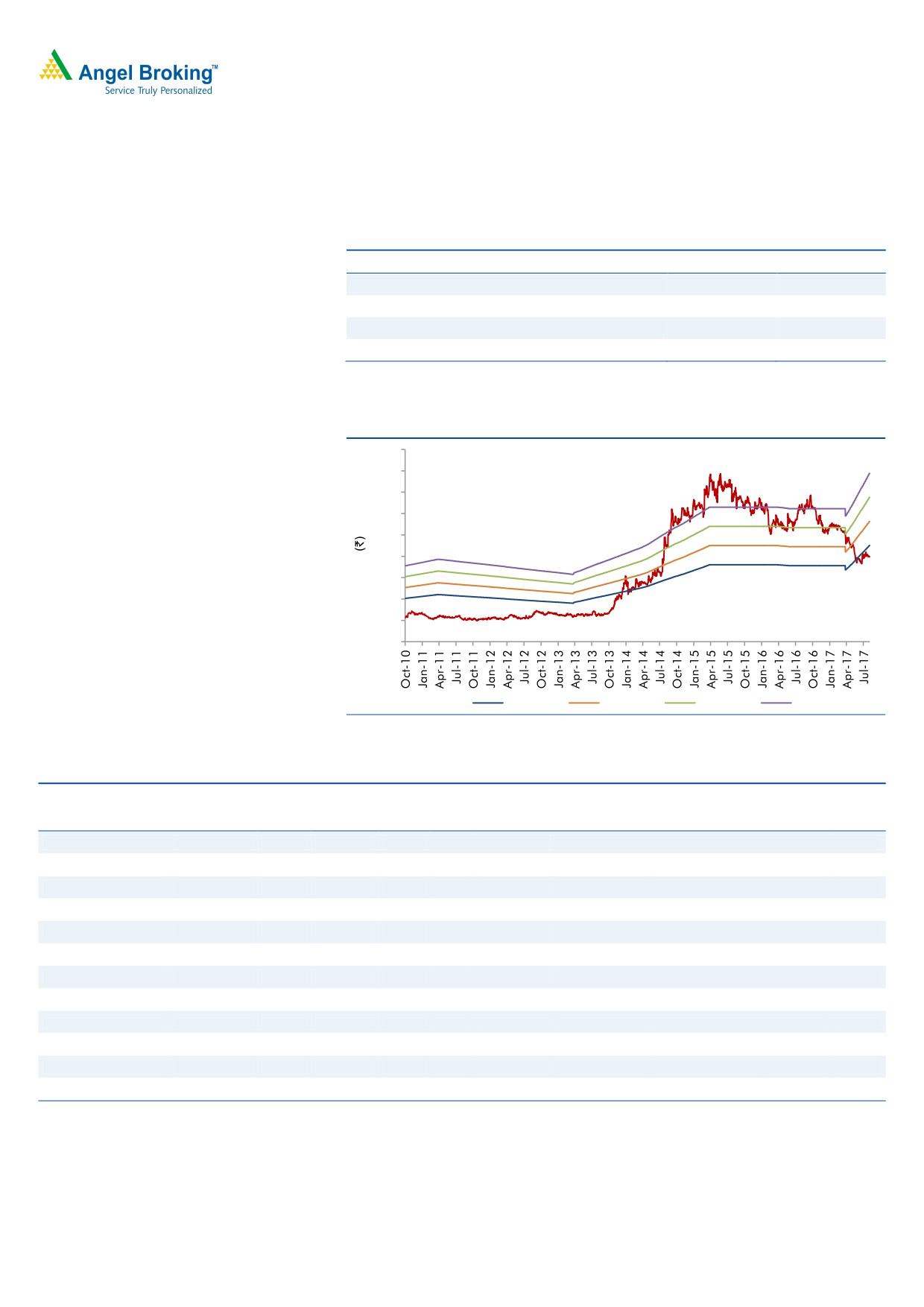

3-Year Daily Price Chart

Outlook and valuation: We expect net sales to post a CAGR of 10.8% to `1,310cr and

450

EPS to post a CAGR of 23.0% to `12.7 over FY2017-19E. We maintain our SELL rating

400

350

on back of the valuations and the corresponding lower profitability.

300

250

Key financials (Consolidated)

200

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

150

Net sales

977

1067

1124

1310

100

% chg

14.6

9.2

5.4

16.5

50

Net profit

83.0

77.5

71.4

117.3

0

% chg

0.2

(6.7)

(7.8)

64.3

EPS (`)

9.0

8.4

7.7

12.7

EBITDA margin (%)

14.9

12.1

11.9

14.9

P/E (x)

21.2

22.7

24.7

15.0

Source: Company, Angel Research

RoE (%)

15.1

12.6

10.6

15.6

RoCE (%)

11.9

7.9

6.2

11.3

P/BV (x)

3.0

2.7

2.5

2.2

Sarabjit Kour Nangra

EV/Sales (x)

1.9

1.8

1.8

1.5

+91 22 39357600 - Ext: 6806

EV/EBITDA (x)

12.9

15.1

15.0

10.0

Source: Company, Angel Research; Note: CMP as of August 11, 2017

Please refer to important disclosures at the end of this report

1

Indoco Remedies | 1QFY2018 Result Update

Exhibit 1: 1QFY2018 (Consolidated) performance

Y/E March (` cr)

1QFY2018

4QFY2017

% chg (qoq)

1QFY2017

% chg (yoy)

FY2017

FY2016

% chg (yoy)

Net sales

204

266

(23.1)

253

(19.1)

1067

981

8.8

Other income

5.7

13.1

(56.7)

5

13.9

32

28

12.7

Total income

210

279

(24.7)

257

(18.5)

1098

1009

8.9

Gross profit

133

168

(20.9)

164

(18.7)

685

635

7.9

Gross margins (%)

65.2

63.4

64.8

64.2

64.7

Operating profit

(3.5)

21.2

-

37.2

-

129.2

145.2

(11.0)

OPM (%)

(1.7)

8.0

14.7

12.1

14.8

Interest

6

(2)

(492.9)

2

149.6

5

13

(61.5)

Dep & amortisation

17

15

9.5

17

0.4

63

60

5.0

PBT

(21)

20

-

23

-

93

100

(7.4)

Provision for taxation

0.9

2.4

(62.3)

3

(70.1)

14

18

(22.2)

Reported Net profit

(22)

18

-

20

-

77

82

(5.9)

Less : Exceptional items

0

0

-

(0)

0

0

PAT after exceptional items

(22)

18

-

20

-

77

82

(5.9)

EPS (`)

-

1.9

2.2

8.4

8.9

Source: Company, Angel Research

Exhibit 2: 1QFY2018 - Actual vs. Angel estimates

(` cr)

Actual

Estimate

Variation (%)

Net sales

204

214

(4.8)

Other operating income

6

5

13.9

Operating profit

(3)

(2)

-

Tax

1

0

Net profit

(22)

(14)

-

Source: Company, Angel Research

Revenues below expectations: Sales came in at `204cr (`214cr expected) v/s.

`253cr in 1QFY2017, a yoy de-growth of 19.1%. The company witnessed a

disruptive 1QFY2018, with domestic as well International sales getting affected

adversely due to GST implementation in India and voluntary stoppage of

ophthalmic product supplies to US respectively. The formulation sales (`185.7cr;

90.9% of sales in 1QFY2018) posted a dip of

20.7% yoy. The domestic

formulation sales (`99.7cr) registered a dip of 29.7% yoy. The International

formulation sales (`86.0cr) posted a yoy dip of 6.9%. The API sales (`14.9cr)

posted a yoy dip of 15.1%.

In US, during the quarter, the revenues de-grew by 6.8% at `86.0cr as against

`92.3cr for the same period last year. In terms of filings, the company (through

partners or by itself), filed 32 ANDAs, which are pending approvals with 10

ANDAs approved till date, with 2 tentative approvals.

With reference to warning letter from USFDA for the company’s Goa Plant II &

III, the remediation process is going on in co-ordination with a US based

consultant and the packaging component manufacturer from Europe. After

sending the comprehensive response in May 2017, the company has sent the

first update to USFDA in July 2017 & the second and final update will be sent

soon.

August 14, 2017

2

Indoco Remedies | 1QFY2018 Result Update

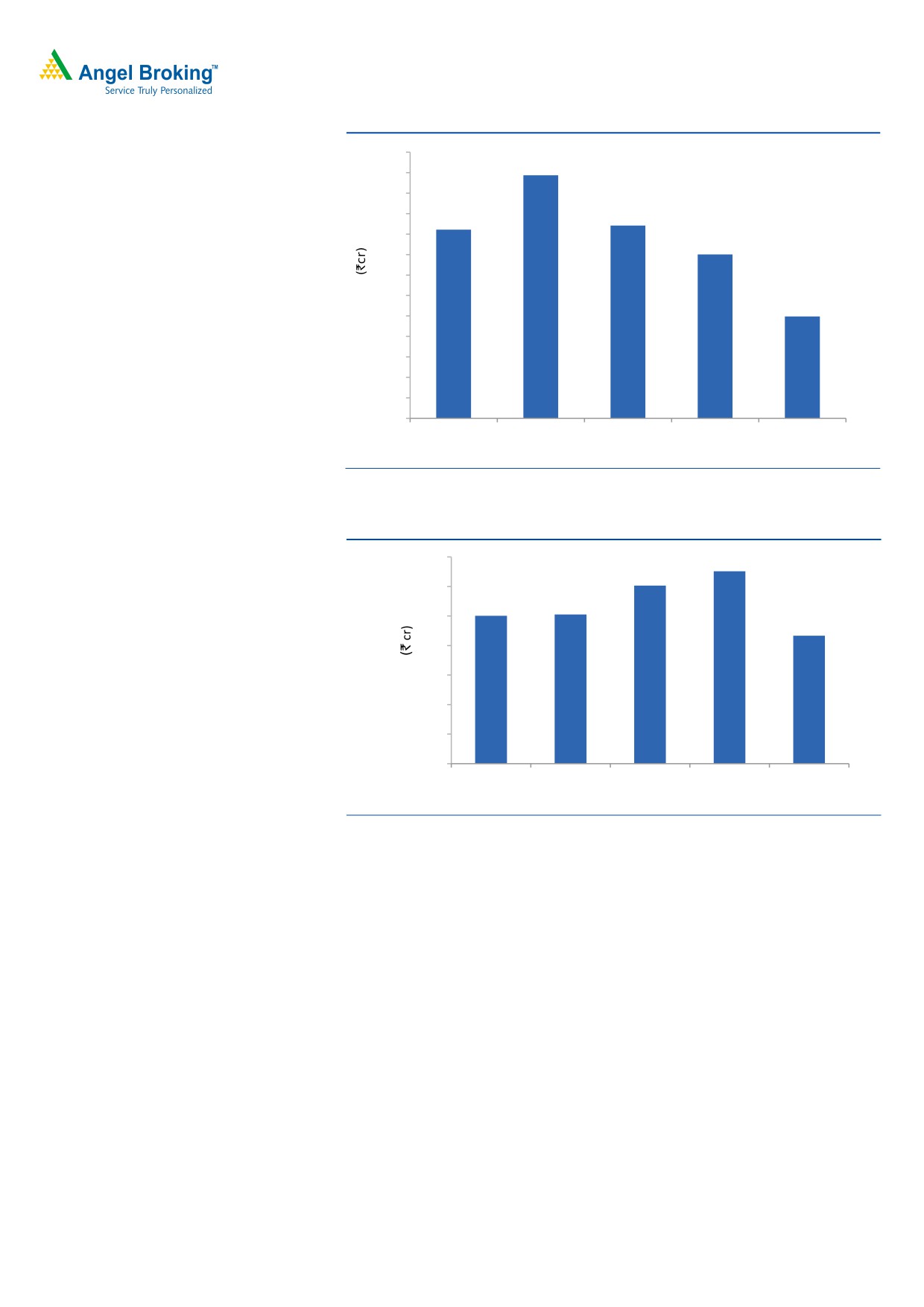

Exhibit 3: Domestic Formulation sales trend

180

169

170

160

150

142

144

140

130

130

120

110

100

100

90

80

70

60

50

1QFY2017 2QFY2017 3QFY2017

4QFY2017

1QFY2018

Source: Company, Angel research

Exhibit 4: Export sales trend

140

130

121

120

100

101

100

87

80

60

40

20

0

1QFY2017 2QFY2017 3QFY2017 4QFY2017

1QFY2018

Source: Company, Angel research

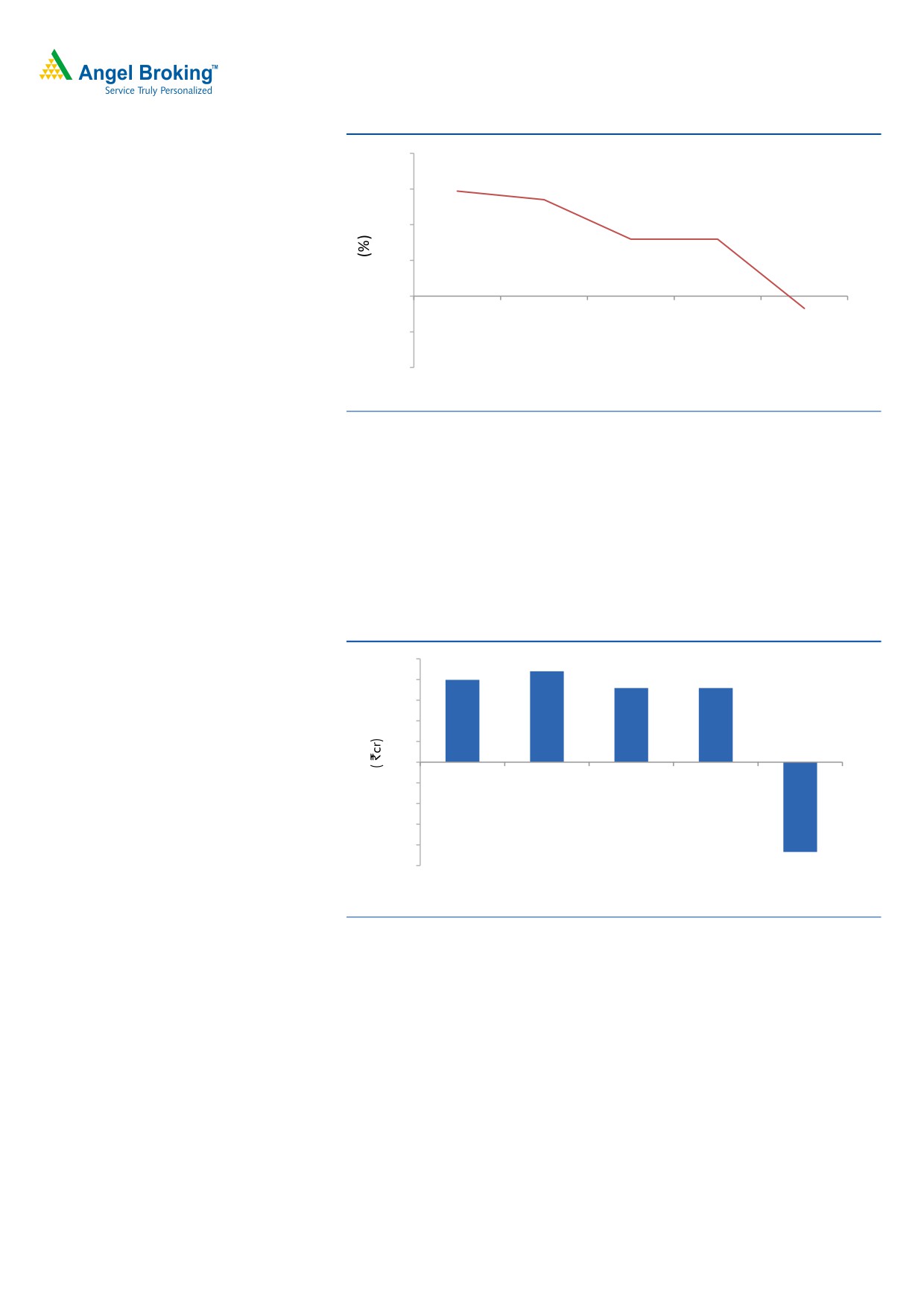

OPM negative: On operating front, the EBITDA margins came in at (1.7%) ((0.9%)

expected) v/s. 14.7% in 1QFY2017, mainly on the back of lower than expected

sales during the quarter. Gross margins came in at 65.2% v/s. 64.8% in

1QFY2017; while R&D expenses were 6.6% of sales in 1QFY2018 v/s. 4.7% of

sales in 1QFY2017.

August 14, 2017

3

Indoco Remedies | 1QFY2018 Result Update

Exhibit 5: OPM trend

20.0

14.7

13.5

15.0

8.0

8.0

10.0

5.0

0.0

1QFY2017 2QFY2017 3QFY2017 4QFY2017 1QFY2018

(5.0)

-1.7

(10.0)

Source: Company, Angel Research

Net profit lower than expectation: Consequently, PAT came in at ` (21.7)cr

(`(13.8)cr expected) v/s. `19.7cr in 1QFY2017. The lower than expected net profit

was on the back of lower than expected sales and OPM. Also, the interest expenses

during the quarter were higher, which accentuated the dip in the net profit.

However, the other income came in at `6cr v/s. `5cr during the corresponding

period last year.

Exhibit 6: Net profit trend

25.0

22

20

18

18

20.0

15.0

10.0

5.0

0.0

1QFY2017 2QFY2017 3QFY2017 4QFY2017 1QFY2018

(5.0)

(10.0)

(15.0)

(20.0)

(25.0)

-22

Source: Company, Angel Research

August 14, 2017

4

Indoco Remedies | 1QFY2018 Result Update

Concall takeaways

Management expects that stoppage of export its ophthalmic solution to US, &

sluggish growth in the unregulated markets are one-offs. All these markets are

expected to deliver robust growth going ahead.

The company has incurred one time one-off expense of `2.5cr in the quarter,

which is an expense incurred on the US consultant.

Domestic Formulations likely to bounce back in 2QFY2018.

Investment arguments

Focus on domestic formulations- Aiming for a higher-than-industry growth: Indoco

has a strong brand portfolio of 135 products and a base of ~2,800 MRs. It

operates in various therapeutic

segments, including anti-infective,

anti-diabetic, CVS, ophthalmic, dental care, pain management and respiratory.

Prominent Indoco brands include Cyclopam, Vepan, Febrex Plus, ATM,

Sensodent-K and Sensoform. The company has seen strong growth across the

respiratory, anti-infective, ophthalmic and alimentary therapeutic segments.

Further, the company is investing to enhance the share of the chronic segment,

which constitutes 10% of overall sales. With a market share of ~0.7% and overall

rank of 31, the company is still a marginal player with some top brands in smaller

categories such as stomatologicals. We expect the domestic formulation segment

to grow at a CAGR of 13.0% over FY2017-19E.

Scaling-up on the exports front: Indoco has also started focusing on regulated

markets by entering into long-term supply contracts. The company is currently

executing several contract-manufacturing projects, and covering a number of

products for its clients in the UK, Germany and Slovenia. Indoco has received a

nod from the USFDA for two of its facilities in Goa. The company derived ~49% of

its revenues from exports in 2016-17. The US cumulative ANDA filings stood at 42

with 29 pending approvals (including 3 tentative approvals). Of these, 18 were

filed under the Actavis deal. The Goa plant warning letter is likely to weigh on

company’s US business, as most of the pending ANDAs are from this unit. Watson

deal, which is at the core of US business prospects, is also likely to witness a

slowdown, as the development may lead to a delay in approval for products that

are part of the deal. The deal covers 18 pending ANDAs. We expect the exports

segment to grow at 15.0% CAGR over FY2017-19E.

Partnering with pharmaceutical majors: The company has a large customer base

of small and medium sized generic companies across the globe and has major tie-

ups with generic companies for certain territories and products. The company has

a deal with Watson Pharmaceuticals to develop and manufacture a number of

sterile (ophthalmic) products for marketing in the USA. The agreement with South

Africa's largest pharmaceutical company, Aspen Pharmacare, encompasses a

number of solid dosages and ophthalmic products, extending to 30 emerging

market countries, while the contract signed with DSM, Austria is for marketing 8 of

Indoco's APIs in various geographies. These deals have further strengthened

Indoco's image in the international arena.

August 14, 2017

5

Indoco Remedies | 1QFY2018 Result Update

Valuation: We expect net sales to post a CAGR of 10.8% to `1,310cr and EPS to

post a CAGR of 23.0% to `12.7 over FY2017-19E. At the current market price, the

stock is trading at

24.7x and

15.0x its FY2018E and FY2019E earnings

respectively. We recommend a SELL rating on the stock considering the valuations.

Exhibit 7: Key assumptions

FY2018E

FY2019E

Domestic sales growth (%)

13.0

13.0

Exports growth

15.0

15.0

Operating margins (%)

11.9

14.9

Capex (` cr)

90.0

60.0

Source: Company, Angel Research

Exhibit 8: One-year forward PE band

450

400

350

300

250

200

150

100

50

0

20x

25x

30x

35x

Source: Company, Angel Research

Exhibit 9: Recommendation summary

Company

Reco

CMP

Tgt. price

Upside

FY2019E

FY17-19E

FY2019E

(`)

(`)

(%) PE (x) EV/Sales (x) EV/EBITDA (x) CAGR in EPS (%) RoCE (%) RoE (%)

Alembic Pharma

Buy

512

600

17.3

18.8

2.1

11.0

12.8

24.3

20.6

Aurobindo Pharma

Buy

705

823

16.8

13.7

2.1

9.6

14.2

25.3

22.7

Cadila Healthcare

Reduce

483

420

(13.0)

22.7

3.7

18.0

21.0

17.3

22.9

Cipla

Sell

543

461

(15.1)

22.4

2.4

14.5

39.2

11.0

13.2

Dr Reddy's

Accumulate

2,011

2,219

10.4

19.0

2.3

12.3

23.6

11.2

13.0

Dishman Pharma

Under Review

301

-

-

18.9

1.3

10.1

(7.2)

2.9

2.5

GSK Pharma

Neutral

2,368

-

-

40.4

5.4

30.3

30.6

28.9

26.5

Indoco Remedies

Sell

191

153

(20.0)

15.0

1.5

10.0

23.0

11.3

15.6

Ipca labs

Buy

412

620

50.5

16.3

1.3

8.4

27.9

12.8

11.2

Lupin

Buy

942

1,467

55.7

14.1

1.9

8.2

8.2

20.5

17.5

Sanofi India*

Reduce

4,104

3,845

(6.3)

26.7

2.8

16.4

9.2

23.9

25.8

Sun Pharma

Buy

451

712

57.8

13.9

2.5

10.0

1.2

15.1

18.8

Source: Company, Angel Research; Note: *December year ending,

August 14, 2017

6

Indoco Remedies | 1QFY2018 Result Update

Company Background

Indoco has a strong brand portfolio of 135 products and a base of 2,300 MRs.

The company operates in various therapeutic segments including anti-infective,

anti-diabetic, CVS, ophthalmic, dental care, pain management and respiratory

areas. Prominent Indoco brands include Cyclopam, Vepan, Febrex Plus, ATM,

Sensodent-K and Sensoform. The company’s top-10 brands contribute over 50%

of its domestic sales. Indoco now proposes to scale up its exports through higher

exposure to the regulated markets.

Profit & loss statement (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

FY2018E

FY2019E

Gross sales

735

863

987

1,078

1,137

1,325

Less: Excise duty

13

11

10

12

13

15

Net sales

722

852

977

1,067

1,124

1,310

Other operating income

10

5

27

27

27

27

Total operating income

733

857

1,004

1,094

1,152

1,338

% chg

16.2

17.0

17.1

9.0

5.3

16.1

Total expenditure

612

691

831

937

991

1,115

Net raw materials

272

300

341

382

416

485

Other mfg costs

42

50

57

62

66

77

Personnel

130

140

183

216

228

265

Other

168

201

250

277

281

288

EBITDA

110

161

145

129

134

195

% chg

23.5

46.1

(9.7)

(11.0)

3.6

45.9

(% of Net Sales)

15.2

18.9

14.9

12.1

11.9

14.9

Depreciation& amortisation

31

47

60

63

75

83

EBIT

79

114

85

66

59

113

% chg

21.0

43.7

(25.4)

(22.2)

(11.2)

92.2

(% of Net Sales)

11.0

13.3

8.7

6.2

5.2

8.6

Interest & other charges

19

11

13

6

6

6

Other income

2

2

1

4

4

4

(% of PBT)

2.4

1.6

1.1

4.5

4.9

3.0

Share in profit of Associates

-

-

1.0

2.0

3.0

4.0

Recurring PBT

72

110

101

91

84

138

PBT (reported)

72

110

101

91

84

138

Tax

14

27

18

14

13

21

(% of PBT)

19.6

24.3

17.5

15.2

15.0

15.0

PAT (reported)

58

83

83

77

71

117

Add: Share of earnings of asso.

-

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

-

Prior period items

-

-

-

-

-

-

PAT after MI (reported)

58

83

83

77

71

117

ADJ. PAT

58

83

83

77

71

117

% chg

36.5

42.3

0.2

(6.7)

(7.8)

64.3

(% of Net Sales)

8.1

9.7

8.5

7.3

6.3

9.0

Basic EPS (`)

6.3

9.0

9.0

8.4

7.7

12.7

Fully Diluted EPS (`)

6.3

9.0

9.0

8.4

7.7

12.7

% chg

36.5

42.3

0.2

(6.7)

(7.8)

64.3

August 14, 2017

7

Indoco Remedies | 1QFY2018 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

FY2018E

FY2019E

SOURCES OF FUNDS

Equity share capital

18

18

18

18

18

18

Reserves & surplus

439

500

566

633

684

781

Shareholders funds

457

519

583

651

702

798

Minority Interest

-

-

-

-

-

-

Total loans

72

88

127

251

300

250

Other Long Term Liab.

9

9

10

10

10

10

Long Term Provisions

16

16

17

19

19

19

Deferred tax liability

31

27

24

(28)

(28)

(28)

Total liabilities

585

659

762

903

974

1,021

APPLICATION OF FUNDS

Gross block

481

561

560

715

805

865

Less: acc. depreciation

156

203

264

327

402

485

Net block

325

358

296

388

403

380

Capital work-in-progress

44

44

44

44

44

44

Goodwill

-

0

88

98

98

98

Investments

0

0

15

0

0

0

Long Term Loans And Adv.

55

58

71

66

110

128

Current assets

305

385

448

572

597

693

Cash

13

15

15

63

49

55

Loans & advances

42

85

78

107

112

131

Other

249

285

355

403

435

507

Current liabilities

144

187

201

265

277

323

Net current assets

160

199

247

307

319

370

Mis. Exp. not written off

-

-

-

-

-

-

Total assets

585

659

762

903

974

1,021

August 14, 2017

8

Indoco Remedies | 1QFY2018 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

FY2018E FY2019E

Profit before tax

72

110

101

91

84

138

Depreciation

31

47

60

63

75

83

(Inc)/Dec in working capital

(18)

(39)

(62)

(8)

(70)

(63)

Less: Other income

2

2

1

4

4

4

Direct taxes paid

14

27

18

14

13

21

Cash Flow from Operations

69

90

81

128

73

133

(Inc.)/Dec.in fixed assets

(41)

(80)

1

(155)

(90)

(60)

(Inc.)/Dec. in investments

-

-

-

-

-

-

Other income

2

2

1

4

4

4

Cash Flow from Investing

(39)

(78)

3

(151)

(86)

(56)

Issue of equity

-

-

(1)

-

-

-

Inc./(Dec.) in loans

(9)

16

41

126

49

(50)

Dividend Paid (Incl. Tax)

(12)

(22)

(21)

(21)

(21)

(21)

Others

(7)

(4)

(103)

(35)

(29)

-

Cash Flow from Financing

(28)

(10)

(83)

70

(0)

(71)

Inc./(Dec.) in Cash

2

2

(0)

48

(14)

6

Opening Cash balances

12

13

15

15

63

49

Closing Cash balances

13

15

15

63

49

55

August 14, 2017

9

Indoco Remedies | 1QFY2018 Result Update

Key Ratios

Y/E March

FY2014

FY2015

FY2016

FY2017

FY2018E

FY2019E

Valuation Ratio (x)

P/E (on FDEPS)

30.2

21.2

21.2

22.7

24.7

15.0

P/CEPS

19.7

13.5

12.3

12.5

12.0

8.8

P/BV

3.9

3.4

3.0

2.7

2.5

2.2

Dividend yield (%)

0.5

1.0

1.0

1.0

1.0

1.0

EV/Sales

2.5

2.2

1.9

1.8

1.8

1.5

EV/EBITDA

16.5

11.4

12.9

15.1

15.0

10.0

EV / Total Assets

3.1

2.8

2.5

2.2

2.1

1.9

Per Share Data (`)

EPS (Basic)

6.3

9.0

9.0

8.4

7.7

12.7

EPS (fully diluted)

6.3

9.0

9.0

8.4

7.7

12.7

Cash EPS

9.7

14.1

15.6

15.3

15.9

21.7

DPS

1.0

2.0

2.0

2.0

2.0

2.0

Book Value

49.6

56.3

63.3

70.6

76.1

86.6

Dupont Analysis

EBIT margin

11.0

13.3

8.7

6.2

5.2

8.6

Tax retention ratio

80.4

75.7

82.5

84.8

85.0

85.0

Asset turnover (x)

1.3

1.4

1.4

1.4

1.3

1.4

ROIC (Post-tax)

11.6

14.2

10.3

7.2

5.8

10.3

Cost of Debt (Post Tax)

18.7

10.0

9.6

2.8

1.9

1.9

Leverage (x)

0.2

0.1

0.2

0.2

0.3

0.3

Operating ROE

10.4

14.8

10.5

8.3

7.0

12.9

Returns (%)

ROCE (Pre-tax)

13.9

18.3

11.9

7.9

6.2

11.3

Angel ROIC (Pre-tax)

15.3

20.2

14.0

10.0

7.9

14.0

ROE

13.4

17.0

15.1

12.6

10.6

15.6

Turnover ratios (x)

Asset Turnover (Gross Block)

1.6

1.6

1.8

1.7

1.5

1.6

Inventory / Sales (days)

50

55

54

63

62

62

Receivables (days)

64

62

68

80

79

79

Payables (days)

40

46

42

49

48

50

WC cycle (ex-cash) (days)

68

70

75

79

82

80

Solvency ratios (x)

Net debt to equity

0.1

0.1

0.2

0.3

0.4

0.2

Net debt to EBITDA

0.5

0.5

0.8

1.5

1.9

1.0

Interest Coverage (EBIT / Int.)

4.2

10.7

6.8

10.7

9.5

18.3

August 14, 2017

10

Indoco Remedies | 1QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Indoco Remedies

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

August 14, 2017

11