Initiating Coverage | Recreation/Amusement Parks

August 31, 2015

Wonderla Holidays

BUY

CMP

`275

A joy ride candidate

Target Price

`322

Investment Period

12 Months

Investment Arguments

New amusement park at Hyderabad to boost footfalls: We expect Wonderla

Holidays to report a healthy growth in footfalls (~18% CAGR over FY2015-17E)

Stock Info

with it setting up a new amusement park in Hyderabad, which would be

Sector

Amusement Parks

operational in FY2017. The company also has plans to venture across other parts

Market Cap (` cr)

1,557

of India to cater to a wider audience. In its first year of operation in Hyderabad,

Net Debt (` cr)

(187)

we expect the company to achieve ~7 lakh footfalls with lower utilisation of

~19%. Going forward, we expect the company to be able to report strong

Beta

1.0

footfalls growth on back of increase in utilisation. Further, we expect the existing

52 Week High / Low

349 / 242

parks in Kochi and Bengaluru to post a ~4% CAGR over FY2015-17E. Moreover,

Avg. Daily Volume

6,735

the company has a proven track record and is expected to consistently increase its

Face Value (`)

10

average realisation (realisation CAGR of ~10% over FY2009-15). The company is

expected to incur strong cash flows and achieve higher assets turnover due to lower

BSE Sensex

26,392

capex requirement, as most of the rides are manufactured at the in-house plant.

Nifty

8,002

Huge potential for F&B segment to grow: Apart from ticket sales, the company

Reuters Code

NA

also generates income from food and beverage (F&B) sales, and product sales at

Bloomberg Code

WONH@IN

its amusement parks, which contribute by almost 25% to the company’s total

revenue. As per a report by CARE Ratings, global amusement parks draw 60-65%

of their revenues from other segments (non-ticket sales). Since FY2009, the

Shareholding Pattern (%)

company’s revenue from other segments has increased from 15% to 25% and we

expect such contribution to rise further.

Promoters

71.0

Company to benefit from higher occupancy rate at Wonderla Resort and

MF / Banks / Indian Fls

2.0

turnaround at the operating level: Over the last three years, Wonderla Resort’s

FII / NRIs / OCBs

9.1

occupancy rate has increased significantly from ~30% to ~45%. Also, Wonderla

Indian Public / Others

17.9

Resort has turned around at the operating level in FY2015. Increase in footfalls at

the Bengaluru park is likely to further boost growth for Wonderla Resort.

Moreover, we expect occupancy rate as well as profitability to rise, going forward.

Abs. (%)

3m 1yr

3yr

Outlook and Valuation: India’s young demographic profile and increasing

Sensex

(4.1)

(14.3)

49.6

discretionary spends are expected to benefit the entertainment industry in the

Wonderla

5.3

14.2

NA

country. Also, the addition of a new park in the company’s portfolio and expected

increase in contribution from other segments like F&B, resort, etc will drive growth

for the company, going forward. Further, the company has negative working

Historical share price chart

capital and negligible debt on its balance sheet. With the company’s stock price

360

having corrected by 20-22% from its all time high, the company now poses as a

340

good buying opportunity in our view. At the current market price, the stock trades

320

at a P/E of 21.3x its FY2017E EPS. We initiate coverage on the stock with a Buy

300

recommendation and target price of `322 (25x FY2017E EPS), indicating an

280

upside of ~17% in the stock price from the present levels.

260

Key Financials

240

Y/E March (` cr)

FY2014

FY2015E

FY2016E

FY2017E

220

Net sales

154

182

206

308

% chg

11.4

18.4

13.4

49.5

Net profit

40

51

51

73

% chg

18.8

27.0

0.6

43.0

Source: Company, Angel Research

EBITDA margin (%)

46.0

44.3

44.0

43.6

EPS (`)

7.1

9.0

9.0

12.9

P/E (x)

39.0

30.7

30.5

21.3

P/BV (x)

10.4

4.4

4.2

3.8

RoE (%)

26.6

14.2

13.7

17.8

RoCE (%)

33.1

17.3

18.9

24.5

Amarjeet S Maurya

EV/Sales (x)

10.1

7.5

7.4

4.9

022-39357800 Ext: 6831

EV/EBITDA (x)

22.0

17.0

16.9

11.3

Source: Company, Angel Research, Note: CMP as of August 28, 2015

Please refer to important disclosures at the end of this report

1

Wonderla Holidays | Initiating Coverage

Investment Arguments

Healthy growth in existing parks coupled with new addition of

Hyderabad Park to drive growth

The company is continuously making efforts to increase footfalls through capacity

expansion and introducing innovative rides at the existing amusement parks. For

Total capex for Hyderabad amusement

instance, over FY2009-15, the company has reported a CAGR of 7.3% in footfalls.

park is `250cr which has been funded

Moreover, the company is setting up a new amusement park in Hyderabad at a

partly through IPO money (`180cr) and

total capex is `250cr which has been partly funded through IPO money (`180cr)

balance from internal accrual

and the balance from internal accruals. The company also plans to expand by

venturing into other parts of India and thereby cater to a wider audience. Going

forward, we believe that the company would witness an increase in footfalls

through new and existing amusement parks.

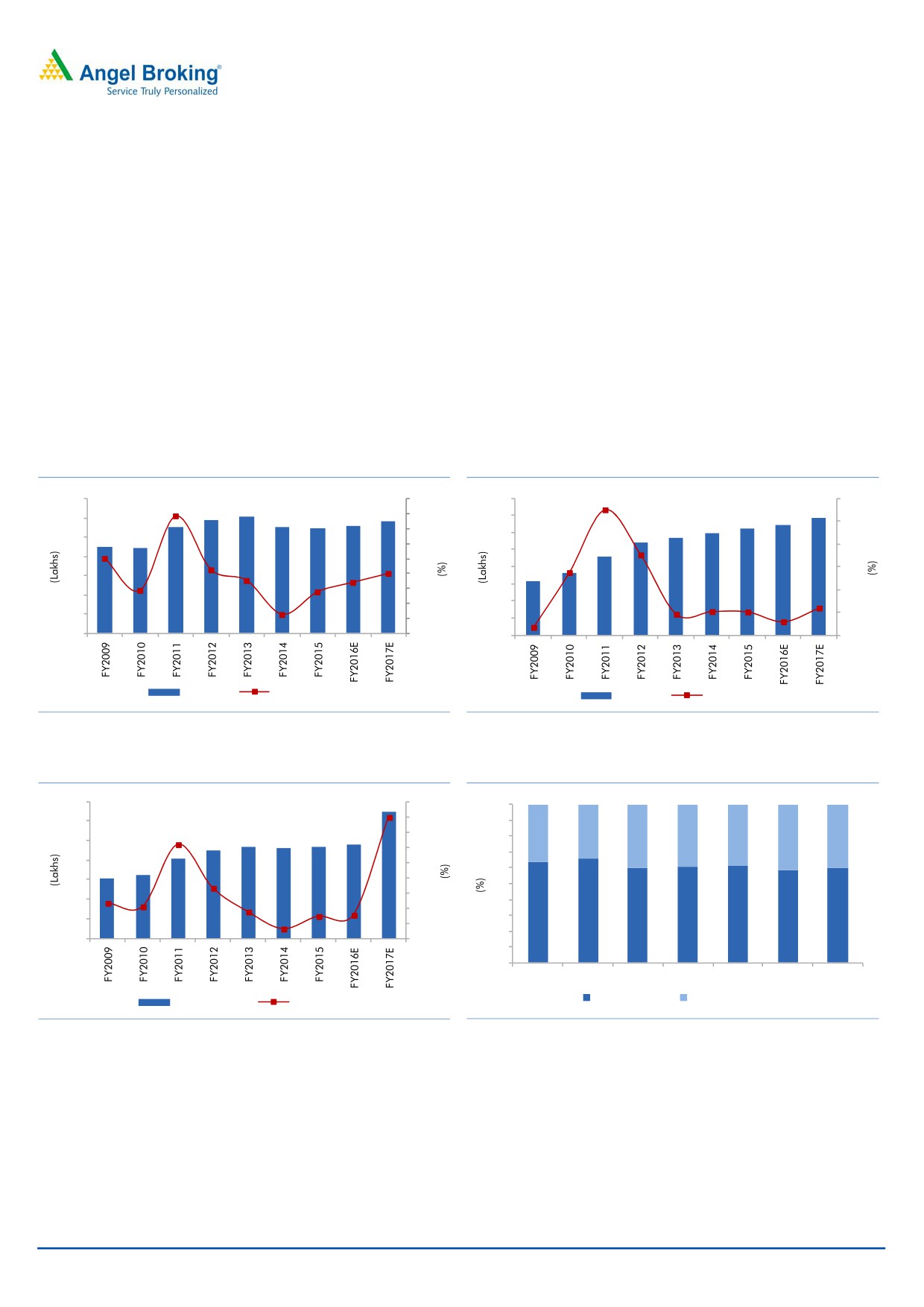

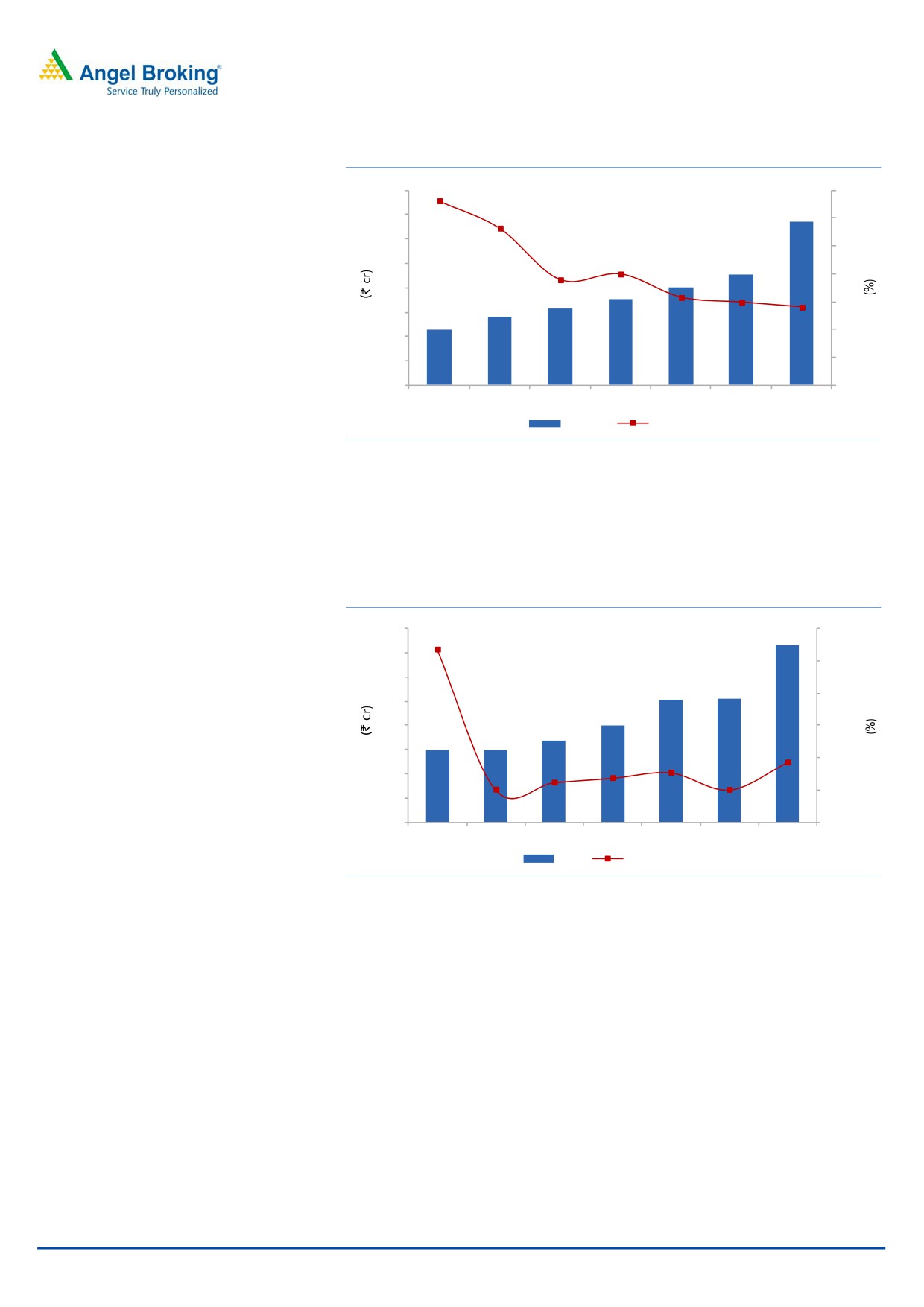

Exhibit 1: Kochi Park footfalls growth trend

Exhibit 2: Bengaluru Park footfalls growth trend

14

11.1

30

16

27.5

30

11.8

12.1

11.7

13.6

11.0

10.9

11.1

25

14

12.5

12.9

12

11.9

25

20

10.8

11.3

9.0

8.9

24.3

12

10

15

9.2

20

10

8

6.2

5.0

10

7.2

2.6

2.0

8

15

10.0

6.3

17.7

6

(0.7)

(1.2)

5

6

13.8

-

10

4

5.2

5.1

6.0

(8.8)

4

4.6

(5)

3.0

2

1.8

5

(10)

2

0

(15)

0

0

Footfalls

yoy growth (%)

Footfalls

yoy growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 3: New + Existing Parks’ footfall growth trend

Exhibit 4: Customer mix

35

32.3

40

100

35

30

90

25.7

24.0

34.7

30

34

22.6

23.4

22.9

23.4

80

36

40

39

39

41

40

25

25

20.3

70

20

16.1

20

15.3

60

11.4

15

15

50

6.5

5.3

10

10

3.6

2.1

2.5

40

5

66

(2.0)

30

64

60

61

61

60

5

59

-

20

0

(5)

10

0

FY2009

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015

Walk-in Visitors

Institutional Visitors

Total Footfalls

yoy growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

We expect the company to report a CAGR of 17.5% in footfalls over FY2015-17E

on the back of healthy growth in existing parks, ie Kochi (3.5% CAGR expected

over FY2015-17E) and Bengaluru (4.5% CAGR expected over FY2015-17E), and

also owing to expected growth of the new park at Hyderabad where we have

factored in 7 lakh footfalls and average realisation of `800.

August 31, 2015

2

Wonderla Holidays | Initiating Coverage

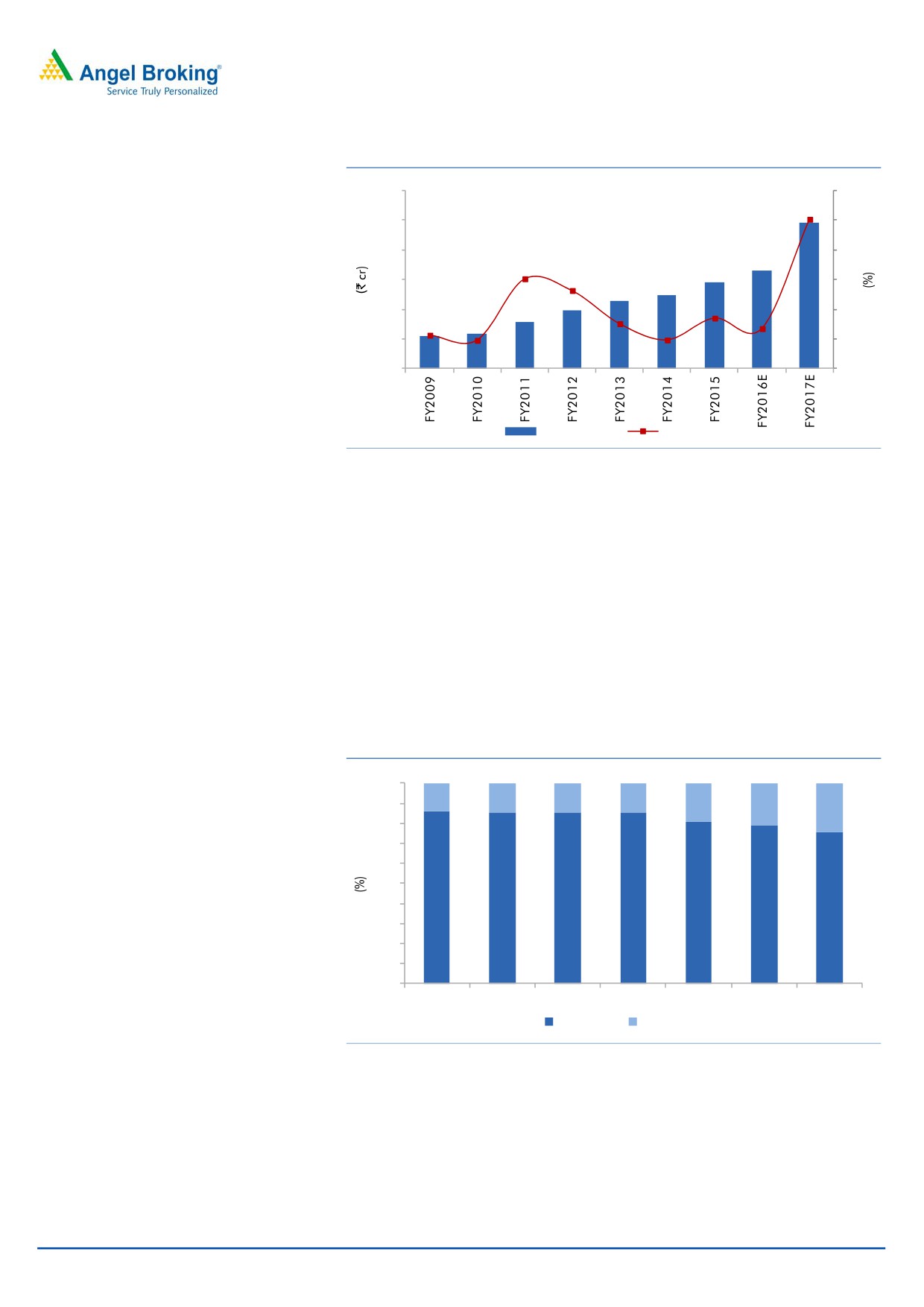

Exhibit 5: Net Revenue from Amusement park segment

300

60

247

250

50

50.3

200

40

164

30.2

145

26.3

150

124

30

113

98

17.0

100

78

13.4

20

54

60

9.6

50

15.1

10

11.2

9.5

0

0

Net Revenue

yoy growth (%)

Source: Company, Angel Research

We expect the company to report a

Thus, considering the above factors, we expect the company to report strong top-

30.6% CAGR over FY2015-17E to

line growth in its core business (amusement parks). We expect the company to

~`247cr.

report a CAGR of 30.6% in its top-line to ~`247cr, over FY2015-17E.

Surge in F&B revenue to contribute to overall growth

Apart from ticket sales, the company also generates income from other segments

like F&B operations as well as direct merchandising operations at amusement

Since FY2009, the company’s revenue

parks on a revenue sharing basis. Since FY2009, the company’s revenue contribution

contribution from ticket sales has

from ticket sales has reduced from 86% to 75% due to increase in revenue from other

reduced from 86% to 75%.

segments and also due to introduction of the new Wonderla Resort.

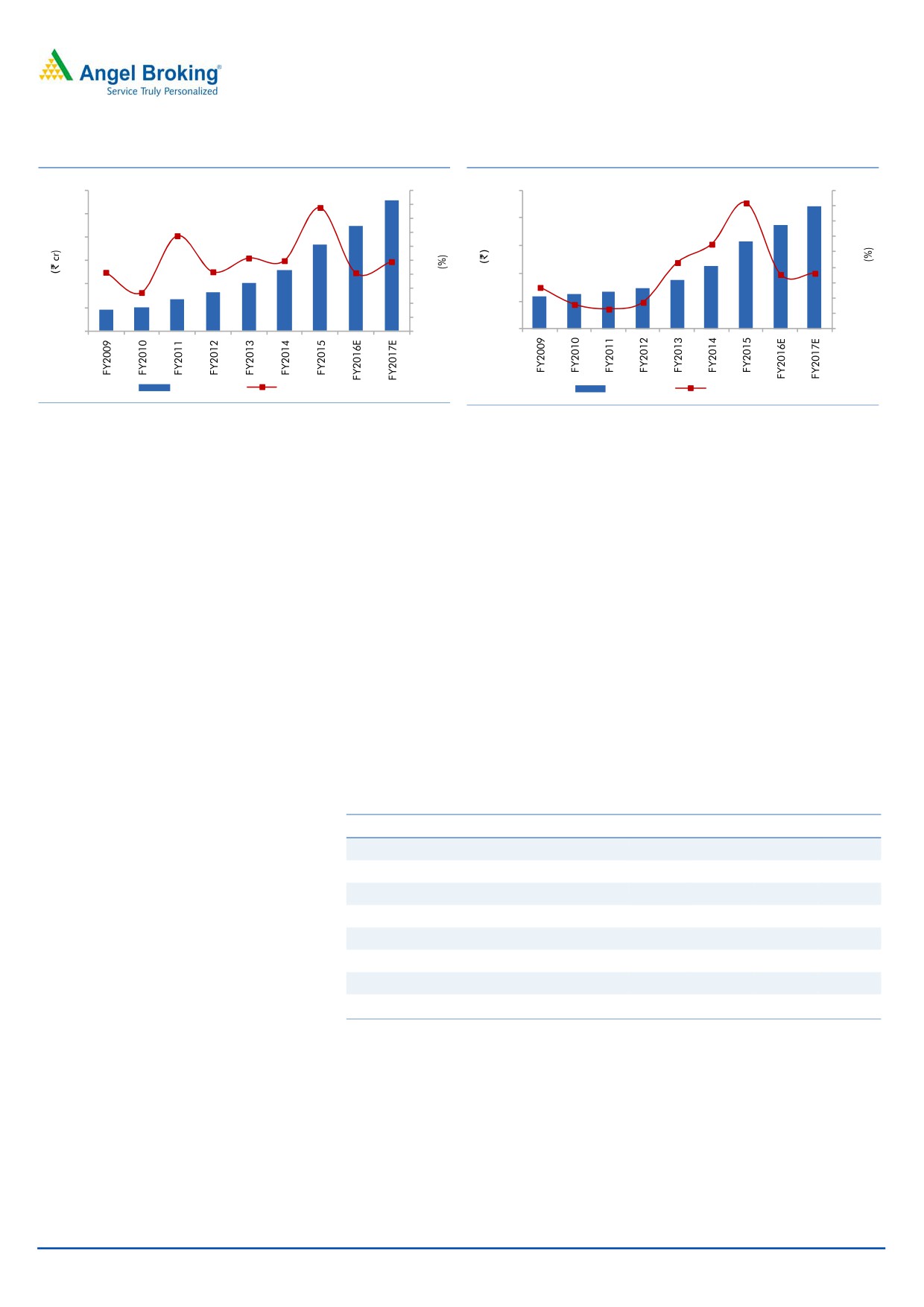

Exhibit 6: Revenue contribution from other segments on the rise

100

14

15

15

14

90

19

21

25

80

70

60

50

86

85

85

86

40

81

79

75

30

20

10

0

FY2009

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015

Ticket Sales

Others

Source: Company, Angel Research

The company is generating lower revenue from other segments (non-ticket sales)

compared to other global amusement parks. As per a report by CARE Ratings,

entry fees constitute only 31% to 35% of total revenues of global amusement

parks. Resorts and other rentals contribute

35% to

37%, and F&B and

merchandising typically contribute 32% to 35% to the total revenue of global

amusement parks.

August 31, 2015

3

Wonderla Holidays | Initiating Coverage

Exhibit 7: Net Revenue growth from F&B and

Exhibit 8:

other segments and average price trend

60

43.9

50

250

40.9

45

45

40

50

33.8

40

200

35

27.5

40

35

30

25.9

25.0

30

150

21.6

25

20.8

21.0

20.7

18.1

30

25

17.7

24.6

20

20

100

13.5

13.6

8.6

20

6.4

15

15

7.9

10

50

10

10

9

10

14

16

21

26

37

45

56

5

58

63

67

73

88

112

158

186

220

5

0

0

0

0

Net revenue

yoy growth (%)

Realisation

yoy growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

Thus, we see strong opportunity for the company to capture additional revenue

from other segments, in line with global amusement parks. The company is

making efforts to increase such income by expanding F&B as well as

merchandising operations at amusement parks. Going forward, we expect the

company to report strong revenue CAGR of 22.6% over FY2015-17E to `56cr.

Turnaround in Wonderla Resort will aid overall margins

The company, in March 2012, launched a 3-Star leisure resort attached to the

amusement park in Bengaluru. The objective of Wonderla Resort is to enable

The resort has 84 luxury rooms and 4

visitors to stay longer at the park, which would lead to increased spends on their

banquet halls

/ conference rooms,

part. Moreover, it would also enhance visitor experience. The resort has 84 luxury

totalling 8,900 sq ft with a capacity to

rooms, 4 banquet halls / conference rooms, totaling 8,900 sq ft with a capacity to

hold 800 guests; plus, the resort has a

hold 800 guests and has a well equipped board room. The resort is also suitable

well equipped board room

for hosting wedding receptions, parties and other corporate events and meetings.

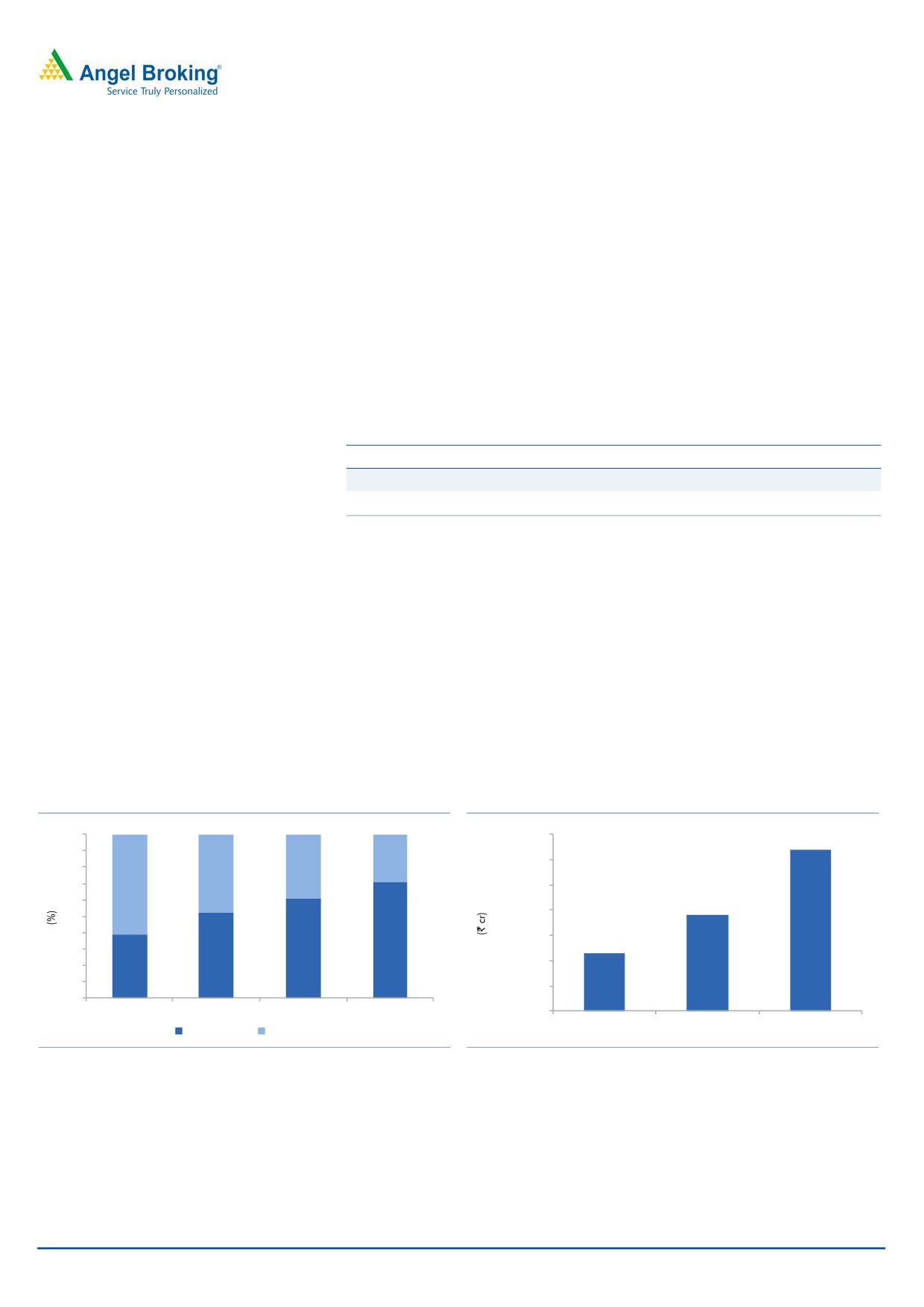

Exhibit 9: Financial overview Wonderla Resort

FY2012

FY2013

FY2014

FY2015

Total No. of Room Nights Available

30,660

30,660

30,660

No. of Rooms Available for Guests Paid Guests

28,596

29,889

29,121

No. of Rooms Occupied

9,730

8,849

13,186

Occupancy Ratio %

34

30

45

Revenue (` cr)

0.0

6.0

6.6

10.4

EBITDA (` cr)

(0.9)

(2.2)

0.1

2.1

Margin (%)

-

-

1.2

20.3

PAT (` cr)

(1.5)

(5.2)

(2.7)

(0.6)

Source: Company, Angel Research

The company reported a revenue CAGR of 32.3% to `10cr over FY2013-15 and

increased occupancy rate from 34% in FY2013 to 45% in FY2015. Since the last

four years, the company’s resort is making losses at both the EBITDA and PAT

levels due to lower occupancy rate and high fixed cost. In FY2015, the company

has reported a profit of `2cr at the EBITDA level due to increase in occupancy rate.

Going forward, we believe that Wonderla Resort would be able to increase its

occupancy rate which will result in profitability for the Bengaluru amusement park

August 31, 2015

4

Wonderla Holidays | Initiating Coverage

as well, on the back of healthy footfall growth. Thus, this would provide margin

benefit to the company and also help to increase profitability.

In-house ride manufacturing facility leads to cost efficiency

To reduce maintenance cost and capex requirement, the company has developed

in-house manufacturing facility in Kochi to manufacture amusement rides and

attractions and also modify the rides (as per visitors’ feedback). The company has

constructed 42 rides for its amusement parks till date. Going forward, we believe

The company has constructed 42 rides

that the company will benefit from its in-house manufacturing capacity which

for its amusement parks till date

would reduce its capex (the cost of a ride manufactured in-house is one-third of

the cost of buying it externally) and maintenance costs.

Exhibit 10: Number of rides imported for park

Number of rides

Imported

Kochi

55

10

Bangalore

55

18

Source: Company, Angel Research

Strong demand drivers for amusement park industry

Despite the recent economic slowdown, there has been a continuous and sustained

Rising disposable incomes, increasing

shift in consumer demand pattern from basic necessities to lifestyle products and

discretionary spending, urbanization,

services. According to McKinsey Global Institute (MGI), discretionary spending will

and demographic advantage are likely

account for 71% of the total consumer spending by the year 2025. Further,

to drive growth for the amusement park

average disposable income is expected to surge from `1.9 lakh in CY2015E to

industry

`3.2 lakh in CY2030E, which would direct higher spending on entertainment

activities such as vacations, visits to multiplexes, restaurants, amusement parks etc.

Exhibit 11: Shifting consumer preferences

Exhibit 12: Rising disposable incomes

100

3,50,000

3,19,518

90

29

3,00,000

80

39

48

70

61

2,50,000

60

1,90,639

2,00,000

50

40

1,50,000

71

1,13,744

30

61

52

1,00,000

20

39

10

50,000

0

CY1995

CY2005

CY2015E

CY2025E

-

CY2005

CY2015E

CY2025E

Discretionary

Necessities

Source: McKinsey Global Institute (MGI)

Source: McKinsey Global Institute (MGI)

August 31, 2015

5

Wonderla Holidays | Initiating Coverage

Exhibit 13: India has demographic advantages

Exhibit 14: Demand driven by increasing urbanization

700

50

45.4

45

590

600

40

37.1

35.9

500

35

30

26.5

400

340

25

290

300

20

15

200

10

100

5

0

0

2001

2008

2030

India

USA

Japan

China

Source: CIA World Factbook

Source: McKinsey Global Institute (MGI)

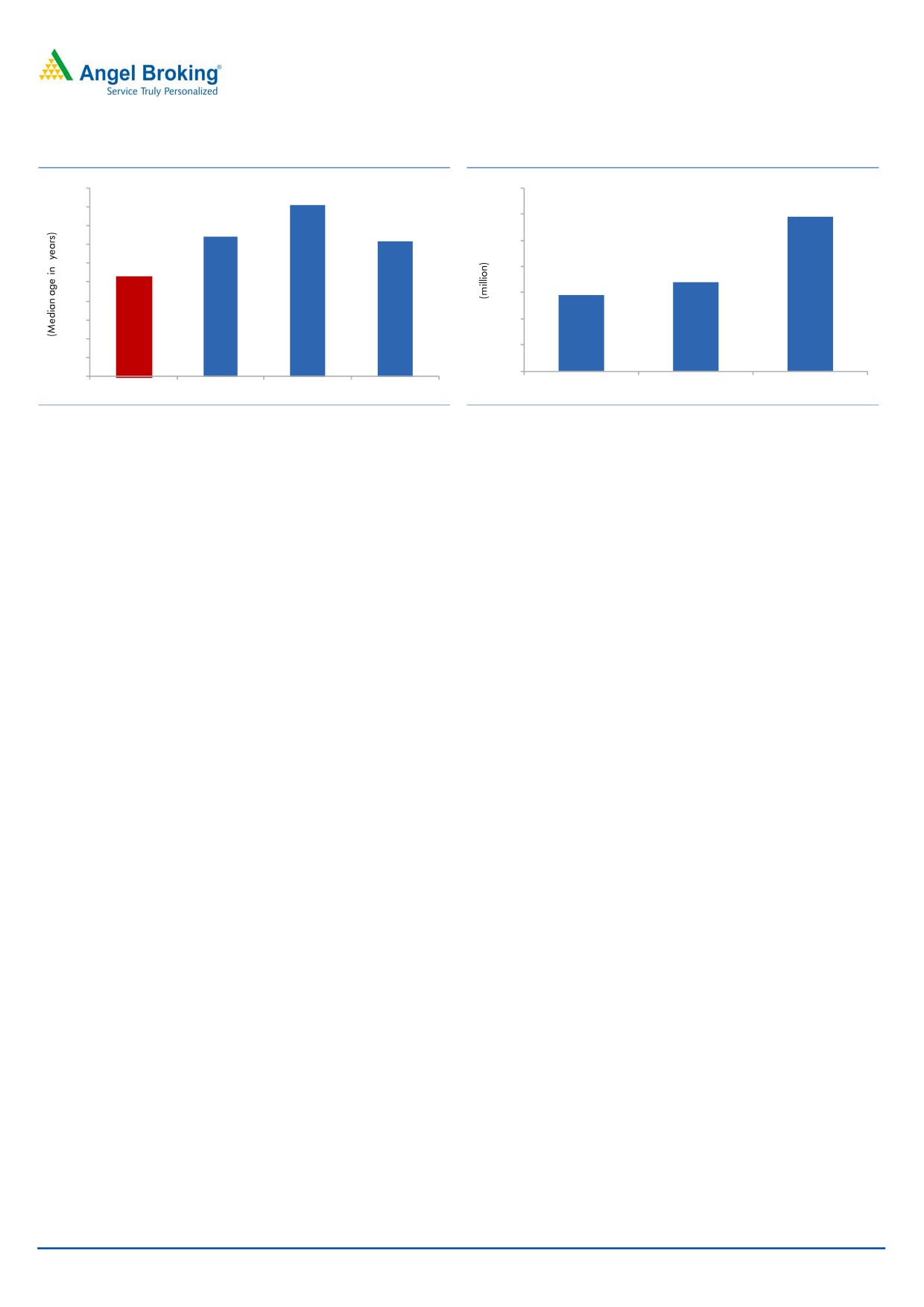

Hence, given India’s young demographic profile and urban population expected to

grow from 340mn in 2008 to 590mn in 2030E (as per MGI), amusement parks

are likely to draw higher footfalls, supported by increase in discretionary spending.

In our opinion, Wonderla Holidays is well-placed to take advantage of this

unfolding opportunity.

Outlook and Valuation

Going ahead, we expect Wonderla Holidays to report a top-line CAGR of ~30%

over FY2015-17E to ~`308cr owing to healthy growth in footfalls, which are likely

to grow at a CAGR of ~18% over the same period owing to addition of new

amusement park in Hyderabad. Going forward, we believe that the company will

be able to increase its net revenue owing to increase in innovative rides at the

existing amusement parks and on plans to expand in other cities. Further,

Wonderla Resort will also contribute revenue for the company.

On the bottom-line front, we expect the company to report an ~20% CAGR over

FY2015-17E on account of strong revenue growth and also on account of benefits

accruing from Wonderla Resort which has turned profit making at the operating

level in FY2015. Wonderla Resort is expected to report profit at the bottom-line

level due to increase in occupancy. Moreover, the company has negative working

capital (payment received upfront), negligible debt, and is able to post a healthy

return ratio, which make the balance sheet all the more attractive.

At the current market price, the stock trades at a P/E of 21.3x its FY2017E EPS. We

initiate coverage on the stock with a Buy recommendation and target price of `322

(25x FY2017E EPS), indicating an upside of ~17% in the stock price from the

present levels.

August 31, 2015

6

Wonderla Holidays | Initiating Coverage

The downside risks to our estimates include

1) The company’s revenue comes from the discretionary category, which is

completely dependent upon an individual’s disposable income and healthy

growth of the economy. Slowdown in the Indian economy could adversely

affect the business.

2) Entry of new players in this segment will create competition for the company.

Other than this, the existing entertainment parks in Hyderabad, namely

Ramoji Film City and Ocean Park, may also pose a challenge even though

they are different in terms of their attractions.

3) The company’s current revenue comes from operations of its two amusement

parks, but any accident at any one of them may result in temporary closure of

the park, thereby generating adverse publicity and in turn affecting revenues

of the company.

4) The company is currently involved in two cases of litigation pertaining to 14.7

acres of land acquired in Hyderabad to set up the park. The Management

has indicated that initially the park will be set up across 27 acres, which

excludes the land under litigation. Hence, no delay is expected in setting up

the park. However, any adverse result of litigation may result in limited

expansion of the park in future, thus resulting in lower-than-expected

revenue.

August 31, 2015

7

Wonderla Holidays | Initiating Coverage

Company Background

Wonderla Holidays Ltd (Wonderla), founded in 2002, is one of the largest

amusement park operators in India. The company currently owns and operates

two amusement parks under the brand name ‘Wonderla’. The company also owns

and operates a resort besides an amusement park in Bengaluru under the brand

name ‘Wonderla Resort’, which has been operational since March

2012.

Wonderla is promoted by Mr Kochouseph Chittilappilly (promoter of V-Guard

Industries) and Mr Arun Kochouseph Chittilappilly.

The promoters of the company launched the first amusement park in Kochi in

2000 with the name ‘Veegaland’ and the second amusement park in Bengaluru in

2005 with the name Wonderla. Veega Holidays and Parks Pvt Ltd, which owned

and operated Veegaland, was merged with Wonderla Holidays Ltd with effect from

April 1, 2008. Consequently, both amusement parks are being operated under the

name Wonderla. Wonderla has a proven track record of managing amusement

parks with established brand equity. The company has been able to maintain high

standards of safety and hygiene, which has been able to attract organized visits

from schools, colleges and corporate segment.

Exhibit 15: Details about Wonderla Holidays Parks

Wonderla Bengaluru Wonderla Kochi

Total Area (in acres)

81.75

93.17

Total Area utilised(in acres)

39.2

28.75

Rides (Land + Water)

59

62

Capacity (footfalls per day)

12,000

12,000

Average price ticket price (`)

673

555

Footfalls (in Lakhs) in FY2015

12.49

10.91

Revenues (` cr) for FY2015

106.4

75.3

EBITDA (` cr) for FY2015

57.4

31.3

EBITDA margins (%)

53.9

41.6

Proportion of non ticketing revenues (%)

21.0

19.5

Source: Company, Angel Research

Exhibit 16: Wonderla Bengaluru amusement park

Exhibit 17: Wonderla Kochi amusement park

Source: Company, Angel Research

Source: Company, Angel Research

August 31, 2015

8

Wonderla Holidays | Initiating Coverage

Exhibit 18: Details about Wonderla Hyderbad Parks

Wonderla Hyderbad

Total Area (in acres)

49.5

Total Area utilized (in acres)

27

Rides (Land + Water)

43

Capacity (footfalls per day)

10,000

Capex (`)

250

Source: Company, Angel Research

Exhibit 19: Construction of roller coaster

Exhibit 20: Construction of wonder splash

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 21: Construction of termite coaster track

Exhibit 22: Construction of waves restaurant

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 23: Details about Wonderla Resort at Bengaluru

Wonderla Resort

Number of rooms

84

Banquet halls / conference rooms (8,900 sq. ft)

4

Banquet halls / conference rooms (Capacity for guests)

800

Occupancy rate in FY2015

45%

Revenues (` cr) for FY2015

10.4

EBITDA (` cr) for FY2015

2.1

EBITDA margins (%)

20.3

Source: Company, Angel Research

August 31, 2015

9

Wonderla Holidays | Initiating Coverage

Exhibit 24: Wonderla Resort

Source: Company, Angel Research

August 31, 2015

10

Wonderla Holidays | Initiating Coverage

Financial outlook

Top-line likely to clock a CAGR of ~30% over FY2015-17E

Wonderla Holidays has reported net revenue CAGR of ~17% over FY2012-15 on

Going forward, we expect Wonderla

the back of growth in footfall and significant hike in average ticket price. Going

Holidays to register healthy top-line

forward, we expect Wonderla Holidays to register healthy net revenue CAGR of

CAGR of ~30% over FY2015-17E

~30% over FY2015-17E supported by healthy growth in footfalls and price hike at

existing amusement parks. Further, the company’s new amusement park in

Hyderabad is likely to generate additional footfalls (we have factored 7 lakh

footfalls from this park in our model) in FY2017E. Apart from this core segment,

we expect the company to also witness growth in other segments like F&B, product

sales and Wonderla Resort. Hence, we expect Wonderla Holidays’ net revenue to

grow by ~13.4% yoy and ~49.5% yoy in FY2016 and FY2017, respectively.

Exhibit 25: Projected Net Revenue growth trend

350

60

49.5

300

50

250

40

200

30.2

26.2

30

150

21.9

18.4

20

13.4

100

11.4

10

50

90

113

138

154

182

206

308

0

0

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

Top-line growth

yoy growth (%)

Source: Company, Angel Research

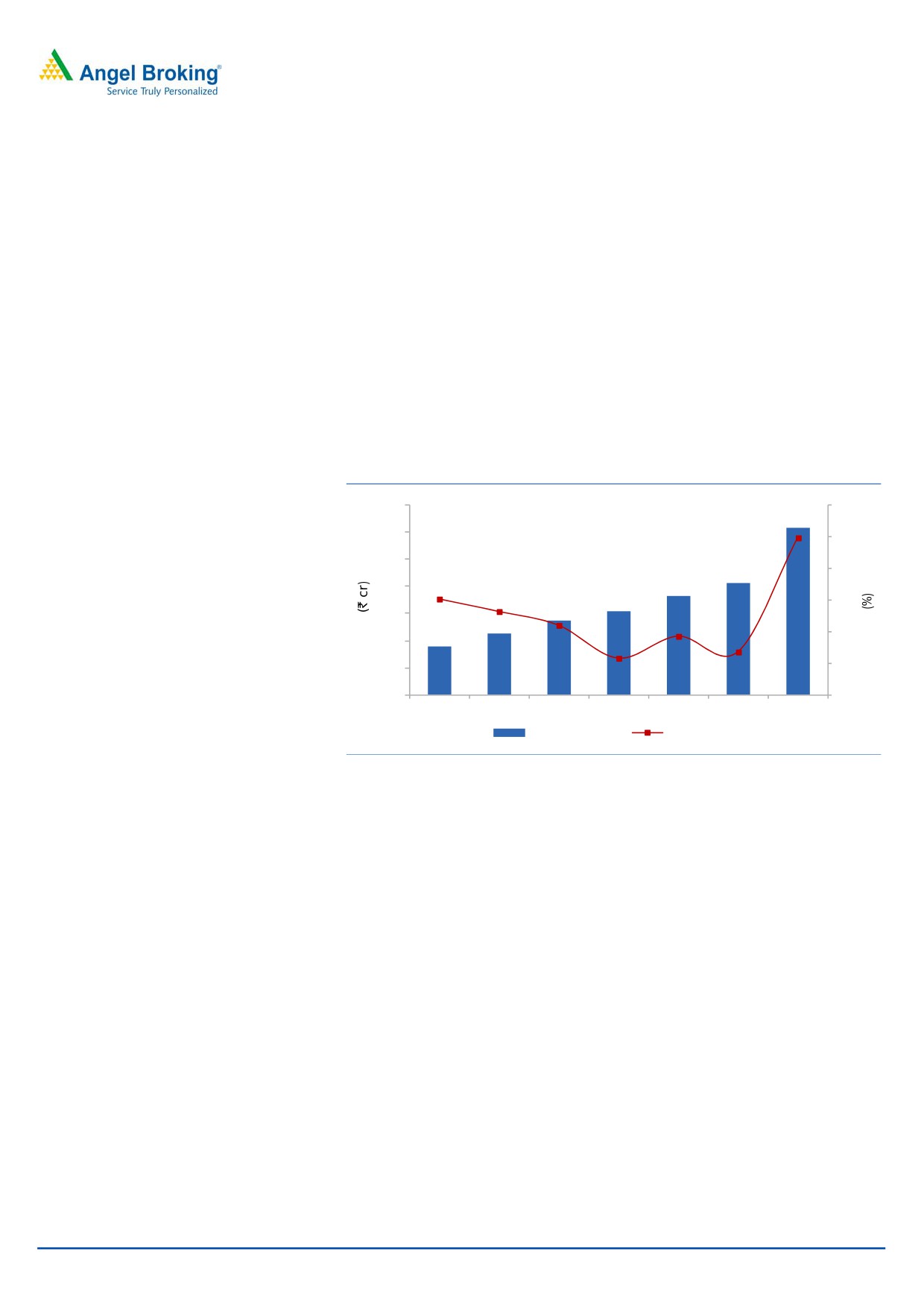

EBITDA to witness a CAGR of ~29% over FY2015-17E

Going forward, we expect the

Going forward, we expect the company’s operating margin to be under pressure

company’s EBITDA margin to be in the

due to increase in operating costs as the new amusement park in Hyderabad. Thus

range of 43-44%

operating margin is likely to be lower owing to lower utilization with it being the

first year of operation. We expect operating margin to be at 44% in FY2016E and

43.6% in FY2017E.

August 31, 2015

11

Wonderla Holidays | Initiating Coverage

Exhibit 26: Projected EBIDTA and margin trend

51.2

160

52

140

49.3

50

120

48

46.0

100

45.6

46

44.3

80

44.0

43.6

44

60

42

40

40

20

46

56

63

71

81

91

134

0

38

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

EBITDA

Margin (%)

Source: Company, Angel Research

Company to report healthy growth

We expect ~20% CAGR in Net Profit

We expect the company to post ~20% CAGR in net profit over FY2015-17E,

over FY2014-17E

mainly led by strong revenue growth.

Exhibit 27: Projected Net Profit growth trend

80

250

217.4

73

70

200

60

51

51

150

50

40

40

34

100

30

30

30

43.0

27.0

50

18.8

11.8

20

0.9

0.6

-

10

0

(50)

FY2011

FY2012

FY2013

FY2014

FY2015 FY2016E FY2017E

PAT

yoy growth (%)

Source: Company, Angel Research

Return ratios expected to bounce back

We expect the company to report improvement in its ROE and ROCE on the back

of healthy profitability with strong revenue growth (on back of strong footfalls

growth and increase in average price). In our view, the company is likely to report

a ROE of 13.7% to 17.8% and ROCE of 18.9% to 24.5% in FY2016 and FY2017,

respectively.

August 31, 2015

12

Wonderla Holidays | Initiating Coverage

Exhibit 28: Improving ROE & ROCE

45

40

35

30

25

20

15

10

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

ROE

ROCE

Source: Company, Angel Research

August 31, 2015

13

Wonderla Holidays | Initiating Coverage

Profit & Loss Statement

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

Total operating income

113

138

154

182

206

308

% chg

26.2

21.9

11.4

18.4

13.4

49.5

Total Expenditure

57

75

83

101

116

174

Personnel Expenses

21

22

24

27

31

47

Others Expenses

37

53

59

74

84

126

EBITDA

56

63

71

81

91

134

% chg

21.4

12.7

12.5

14.0

12.5

48.3

(% of Net Sales)

49.3

45.6

46.0

44.3

44.0

43.6

Depreciation& Amortisation

12

12

13

16

17

30

EBIT

44

51

57

64

73

104

% chg

29.6

15.4

12.7

12.1

13.9

42.0

(% of Net Sales)

39.1

37.0

37.4

35.4

35.5

33.8

Interest & other Charges

1

2

2

2

2

2

Other Income

1

2

2

10

2

3

(% of PBT)

3.1

3.0

4.1

14.0

2.7

2.8

Share in profit of Associates

-

-

-

-

-

-

Recurring PBT

44

50

58

73

74

106

% chg

4.4

12.6

15.7

26.0

1.2

43.0

Prior Period & Extra. Exp./(Inc.)

PBT (reported)

44

50

58

73

74

106

Tax

14

16

18

22

23

33

(% of PBT)

32.4

32.9

31.1

30.6

31.0

31.0

PAT (reported)

30

34

40

51

51

73

Add: Share of earnings of asso.

Less: Minority interest (MI)

-

-

-

-

-

-

PAT after MI (reported)

30.0

33.6

39.9

50.7

50.9

72.9

ADJ. PAT

30.0

33.6

39.9

50.7

50.9

72.9

% chg

0.9

11.8

18.8

27.0

0.6

43.0

(% of Net Sales)

26.6

24.4

26.0

27.8

24.7

23.6

Basic EPS (`)

5.3

5.9

7.1

9.0

9.0

12.9

Fully Diluted EPS (`)

5.3

5.9

7.1

9.0

9.0

12.9

% chg

0.9

11.8

18.8

27.0

0.6

43.0

August 31, 2015

14

Wonderla Holidays | Initiating Coverage

Balance Sheet

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

42

42

42

57

57

57

Reserves& Surplus

52

78

108

300

316

354

Shareholders Funds

94

120

150

356

372

410

Total Loans

22

21

24

15

15

15

Deferred Tax Liability

3

5

4

-

-

-

Total Liabilities

120

145

178

372

387

426

APPLICATION OF FUNDS

Gross Block

208

242

255

270

290

490

Less: Acc. Depreciation

87

98

110

130

147

178

Net Block

121

144

145

139

142

312

Capital Work-in-Progress

4

6

20

40

180

-

Investments

-

-

-

194

14

14

Current Assets

14

16

35

23

64

119

Inventories

2

3

3

4

7

11

Sundry Debtors

0

0

0

1

1

1

Cash

2

2

19

8

22

33

Loans & Advances

1

3

4

10

17

37

Other Assets

8

8

7

0

19

37

Current liabilities

20

21

23

26

14

20

Net Current Assets

(6)

(5)

12

(3)

50

99

Deferred Tax Asset

-

1

1

1

1

1

Total Assets

120

145

178

372

387

426

August 31, 2015

15

Wonderla Holidays | Initiating Coverage

Cashflow Statement

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015 FY2016E FY2017E

Profit before tax

44

50

58

73

74

106

Depreciation

12

12

13

16

17

30

Change in Working Capital

2

(0)

(2)

(2)

(39)

(37)

Interest / Dividend (Net)

1

2

1

(6)

2

2

Direct taxes paid

(14)

(15)

(20)

(25)

(23)

(33)

Others

-

0

0

1

-

-

Cash Flow from Operations

45

49

50

56

31

67

(Inc.)/ Dec. in Fixed Assets

(39)

(37)

(26)

(29)

(185)

(40)

(Inc.)/ Dec. in Investments

-

-

-

(194)

180

-

Cash Flow from Investing

(39)

(37)

(26)

(223)

(5)

(40)

Issue of Equity

-

-

-

170

-

-

Inc./(Dec.) in loans

5

(2)

3

(3)

-

-

Dividend Paid (Incl. Tax)

(7)

(7)

(7)

(10)

(10)

(15)

Interest / Dividend (Net)

(1)

(2)

(3)

(2)

(2)

(2)

Cash Flow from Financing

(4)

(11)

(7)

156

(12)

(16)

Inc./(Dec.) in Cash

2

0

17

(12)

14

11

Opening Cash balances

(0)

2

2

19

8

22

Closing Cash balances

2

2

19

8

22

33

August 31, 2015

16

Wonderla Holidays | Initiating Coverage

Key Ratios

Y/E March

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

51.7

46.3

39.0

30.7

30.5

21.3

P/CEPS

37.3

34.2

29.3

23.2

22.8

15.1

P/BV

16.6

13.0

10.4

4.4

4.2

3.8

Dividend yield (%)

2.3

2.3

3.1

3.1

3.7

5.3

EV/Sales

13.9

11.4

10.1

7.5

7.4

4.9

EV/EBITDA

28.2

25.0

22.0

17.0

16.9

11.3

EV / Total Assets

11.3

9.4

7.7

3.4

3.8

3.4

Per Share Data (`)

EPS (Basic)

5.3

5.9

7.1

9.0

9.0

12.9

EPS (fully diluted)

5.3

5.9

7.1

9.0

9.0

12.9

Cash EPS

7.4

8.0

9.4

11.8

12.1

18.3

DPS

6.3

6.3

8.5

8.5

10.2

14.6

Book Value

16.6

21.2

26.5

63.1

65.9

72.7

Returns (%)

ROCE

38.0

36.2

33.1

17.3

18.9

24.5

Angel ROIC (Pre-tax)

38.8

36.9

37.4

38.1

20.9

27.5

ROE

32.0

28.0

26.6

14.2

13.7

17.8

Turnover ratios (x)

Asset Turnover (Gross Block)

0.5

0.6

0.6

0.7

0.7

0.6

Inventory / Sales (days)

6

7

8

8

12

13

Receivables (days)

1

1

1

1

1

1

Payables (days)

12

13

10

7

8

7

WC cycle (ex-cash) (days)

(5)

(4)

(1)

2

5

7

August 31, 2015

17

Wonderla Holidays | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Wonderla Holidays

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

August 31, 2015

18