4QFY2016 Result Update | Cement Products

May 21, 2016

Visaka Industries

BUY

CMP

`135

Performance Highlights

Target Price

`162

Investment Period

12 Months

Y/E March (` cr)

4QFY16 4QFY15

% chg (yoy) 3QFY16

% chg (qoq)

Net sales

276

285

(3.3)

215

28.0

Stock Info

EBITDA

29

27

6.6

16

73.8

Sector

Cement Products

EBITDA Margin (%)

10.4

9.4

96bp

7.7

274bp

Market Cap (` cr)

215

Adjusted PAT

10

6

58.6

1

767.2

Source: Company, Angel Research

Net Debt

262

Beta

1.5

Visaka Industries posted a good set of numbers for 4QFY2016. Although the top-line

52 Week High / Low

189 / 89

declined, the performance on the operating and bottom-line fronts was favorable.

The top-line declined by 3.3% yoy to `276cr. On the operating front the EBITDA grew

Avg. Daily Volume

18,326

by 6.6% yoy to `29cr and the EBITDA margin improved by 96bp yoy to 10.4%. There

Face Value (`)

10

was an exceptional expense related to diminution in value of investment during the

BSE Sensex

25,302

quarter amounting to `1cr, adjusting for which, other expenses declined by 192bp

Nifty

7,750

yoy to 24.6% of sales. Raw material and employee expenses remained flat as a

Reuters Code

VSKI.BO

proportion of sales, thus resulting in EBITDA margin expansion. Aided by lower

Bloomberg Code

VSKI.IN

interest and depreciation, the adjusted net profit grew by 58.6% yoy to `10cr.

Overall long term prospects intact: The company’s performance in FY2016 was

Shareholding Pattern (%)

impacted on account of drop in volumes and realizations for its main business, ie

Promoters

37.5

Asbestos Cement Sheets (ACS). However, the company is aiming at growing its

MF / Banks / Indian Fls

0.5

Boards and Synthethic yarn business in order to lower its dependence on the ACS

FII / NRIs / OCBs

3.3

business. While the long term prospects of ACS are intact the outlook for the Boards

and Synthetic yarn business also looks favorable which should drive growth for the

Indian Public / Others

58.7

company going forward. The Yarn business has better margins while the Boards

business has shown significant improvement in profitability which should only improve

Abs.(%)

3m 1yr

3yr

once the business scales up.

Sensex

7.1

(8.1)

25.6

Outlook and Valuations: We have introduced our FY2018E estimates for the

Visaka

42.0

14.6

28.3

company and have lowered our expectation for FY2017E on account of near term

dampness in the ACS division. At the current market price of `135, the stock is trading

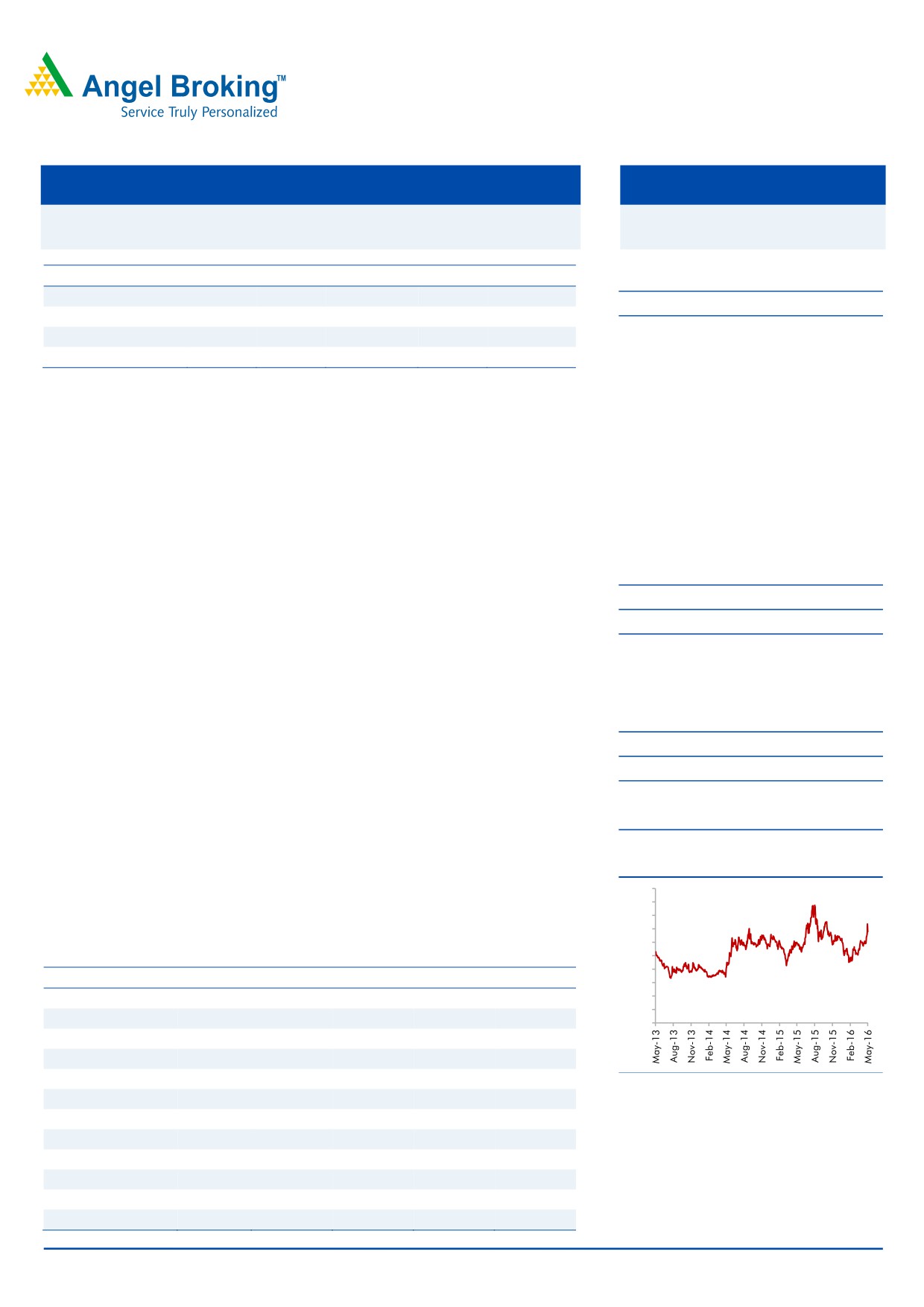

3 Year Price Chart

200

at a valuation of 5.9x its FY2018E EPS, which is attractive. We continue to maintain

180

our Buy rating on the stock with a revised price target of `162, valuing the stock at

160

7.0x its FY2018E earnings.

140

120

100

Key financials

80

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E

FY2018E

60

40

Net sales

892

1,021

1,005

1,051

1,138

20

% chg

(2.6)

14.5

(1.6)

4.6

8.3

-

Adj. net profit

12

21

28

33

37

% chg

(76.3)

76.6

29.8

21.0

10.2

EBITDA Margin (%)

6.4

9.4

9.9

10.3

10.4

Source: Company, Angel Research

EPS (`)

7.5

13.4

17.4

21.0

23.1

P/E (x)

17.9

10.1

7.8

6.4

5.9

P/BV (x)

0.6

0.6

0.6

0.6

0.5

RoE (%)

3.6

6.4

7.9

9.0

9.2

RoCE (%)

5.3

7.7

8.8

8.7

8.6

Milan Desai

EV/Sales (x)

0.5

0.5

0.4

0.5

0.4

+91 22 4000 3600 Ext: 6846

EV/EBITDA (x)

7.7

5.0

4.5

4.5

4.2

Source: Company, Angel Research; Note: CMP as of May 20, 2016

Please refer to important disclosures at the end of this report

1

Visaka Industries | 4QFY2016 Result Update

Exhibit 1: 2QFY2016 performance

Y/E March (` cr)

4QFY16

4QFY15

% chg (yoy)

3QFY16

% chg (qoq)

FY2016

FY2015

% chg (yoy)

Total operating income

276

285

(3.3)

215

28.0

1,005

1,021

(1.6)

Net raw material

162

167

(3.2)

124

30.5

572

578

(1.0)

(% of Sales)

58.8

58.7

4bp

57.7

110bp

56.9

56.6

33bp

Employee cost

17

15

13.4

17

3.7

68

59

14.5

(% of Sales)

6.3

5.4

93bp

7.8

(147)bp

6.8

5.8

95bp

Other Expenses

68

75

(10.3)

58

16.8

266

288

(7.9)

(% of Sales)

24.6

26.5

(192)bp

26.9

(237)bp

26.4

28.2

(181)bp

Total expenditure

247

258

(4.3)

199

24.2

905

925

(2.2)

EBITDA

29

27

6.6

16

73.8

100

96

4.0

EBITDA Margin (%)

10.4

9.4

96bp

7.7

274bp

9.9

9.4

53bp

Interest

5

7

(26.6)

6

(8.2)

21

22

(3.3)

Depreciation

8

10

(12.6)

9

(7.4)

36

43

(15.7)

Other income

0

0

108.0

0

(5.1)

3

2

12.7

Extraordinary Exp./(Inc.)

1

-

-

5

-

PBT

15

10

(7.8)

2

(23.4)

40

33

9.6

(% of Sales)

5.3

3.7

1.0

4.6

4.3

Tax

5.6

4.3

28.5

1.1

398.2

16

12

33.1

(% of PBT)

38.4

41.7

50.2

39.5

36.0

Reported PAT

9

6

47.1

1

704.1

24

21

15.0

Exceptional items

1

-

-

3.15

-

Adjusted PAT

10

6

58.6

1

767.2

28

21

29.8

PATM (%)

3.5

2.1

0.5

2.7

2.1

Source: Company, Angel Research

Exhibit 2: Actual vs. Estimate

Actual v/s Angel's Estimates

Actual (` cr)

Estimate (` cr)

% variation

Total Income (` cr)

276

291

(5.3)

EBITDA (` cr)

29

21

36.0

EBITDA Margin (%)

10.4

7.2

316bp

Adjusted PAT (` cr)

10

7

46.0

Source: Company, Angel Research

Top-line disappoints, margin and bottom-line impress

The top-line during the quarter witnessed a de-growth of 3.3% yoy to `276cr which

is below our estimate of `291cr. This was on account of decline in volumes and

realizations for the ACS division and lower realizations for the Synthetic Yarn

segment. On the operational front, raw material and employee expense both as a

percentage of sales remained flat while other expenses, adjusting for provision for

diminution in value of `1cr (`4.5cr for FY2016), declined by 192bp yoy to 24.6%

of sales. Aided by lower other expense, the EBITDA grew by 6.6% yoy to `29cr and

the EBITDA margin expanded by 96bp yoy to 10.4%. The deviation in the EBITDA

margin from our estimates is on account of we having estimated for higher other

expenses. Interest expense declined by 26.6% yoy to `5cr while depreciation

declined by 12.6% yoy to `8cr. Consequently, the adjusted net profit grew by

58.6% yoy to `10cr.

May 21, 2016

2

Visaka Industries | 4QFY2016 Result Update

Segmental performance

Building products: The sgements’ top-line for the quarter witnessed a 3.3% yoy

decline to `229.3cr on account of decline in volumes as well as realizations for the

ACS division. However, the V-boards division’s revenue improved by ~23% yoy,

thus arresting any sharp decline in overall revenues. Aided by improvement in

profitability, the Boards division’s building products EBIT grew by 14.0% yoy to

`18.6cr. As per the management, the boards division’s EBIDTA margin improved

to 7.9% (in 4QFY2016) after having posted -2.5% margin in 4QFY2015.

Synthetic Yarn: The segment’s top-line remained flat at `44.6cr while the margins

reported a 32bp yoy improvement to 13.5%.

Exhibit 3: Segment-wise performance

Y/E Mar (` cr)

4QFY16

4QFY15

% chg (yoy) 3QFY16

% chg (qoq)

Total Revenue

A) Building Products

229.3

237.2

(3.3)

167.4

37.0

B) Synthetic Yarn

44.6

44.6

(0.0)

40.9

8.9

Total

273.9

46.0

496.0

208.3

31.5

EBIT

A) Building Products

18.6

16.3

14.0

6.6

181.3

B) Synthetic Yarn

6.0

5.9

2.4

5.5

9.9

Total

24.6

191.2

(87.1)

12.1

103.7

EBIT Margin (%)

A) Building Products

8.1

6.9

123bp

3.9

415bp

B) Synthetic Yarn

13.5

13.2

32bp

13.3

12bp

Source: Company, Angel Research

Concall highlights

The ACS division witnessed a volume decline of ~3.0% for FY2016 while the

realizations were down by ~2.5%. The division has been impacted by poor

rural economy and cannibalization by Chinese steel roofing (color coated)

sheets. The Management is optimistic that the division will see improvement on

the back of increased rural allocation by the government and expectation of a

better monsoon this year which should slowly bring back demand for ACS.

The company sold 7.0 lakh tons in FY2016 against 7.2 lakh tons in FY2015

and produced 6.9 lakh tons in FY2016 against 7.7 lakh tons in FY2015, thus

resulting in a decline in inventory levels.

The Boards division has been witnessing good traction and the company has

been aggressive in promotion of products. The company has spent ~`3.5-4cr

on advertisement which will likely be ~`8cr for FY2017. The division’s

production stood at ~91,000 tons for FY2016 which can reach peak capacity

of 1,20,000 tons. The company expects the division to be a significant

contributor to revenues in the future.

The Synthetic yarn segment was impacted on account of lower realizations in

FY2016. The company expects margins to improve in FY2017 on account of

inventory gains and pickup in demand on account of reversal of in the

realization cycle. The company has lined up a capex of ~`70cr which will get

operational by September 2016. Of this, `60cr will be funded via debt which

May 21, 2016

3

Visaka Industries | 4QFY2016 Result Update

will entail interest rebate from the Government of Maharashtra. This will likely

benefit the company as the debt servicing cost will come down to ~6%. The

capacity of the division post expansion will increase by 26%.

Overall, the company is expected to benefit from lower chrysotile asbestos

fiber prices in FY2016 and we expect the currency to remain stable which will

likely keep a check on raw material prices. The company has been prudent

with managing expenses and the Management has stated at the same

continuing and the trend being sustainable.

Investment arguments

Boards business to drive growth for Building Products segment

The company’s ACS business which used to account for ~80% of the revenue in

the past has seen its contribution decline to ~65% in FY2016. This has been on

account of poor rural sentiment which has impacted volumes as well as

realizations in FY2016. Also, this could also be attributable to improvement in the

contribution of the Boards business as the company has been aggressive in

promoting its V-next (boards) products and expects good growth in the division

which will also witness improvement in margins with scale.

Synthetic yarn business to witness improvement with increase in

realizations

The company’s Synthetic yarn business, which although is a commoditized

business, uses superior technology (Japanese twin jet machines) to produce high

quality yarn. The yarn is supplied to key clients like Raymond, Siyaram Silk Mills,

Pantaloons, etc which require superior quality yarn for their fabrics and hence the

product entails better margin for the company in comparison to other yarn

manufacturers. The business’ contribution to overall revenue in FY2016 has

declined owing to falling realizations which however should turnaround once poly

staple fibre and oil prices stabilize and rebound. Overall, the outlook for the

business looks stable in the near term owing to improvement in domestic demand

for the Indian textile sector although exports have been hindered due to a poor

global demand scenario. This should support volumes for the company till we

witness a revival in global demand.

May 21, 2016

4

Visaka Industries | 4QFY2016 Result Update

Financials

On account of bleak near term outlook for the ACS division, we have estimated a

revenue CAGR of ~4.0% for the division over FY2016E-FY2018E. We have built in

a revenue CAGR of 12.8% for the Boards division in our estimates led by

volume/realization CAGR of ~8%/5% over FY2016E-18E. We expect the Synthetic

yarn business’ volumes/realization to post a CAGR of ~8%/4% over FY2016E-

18E, resulting in revenue CAGR of 12.5%. As a result, the overall revenue is

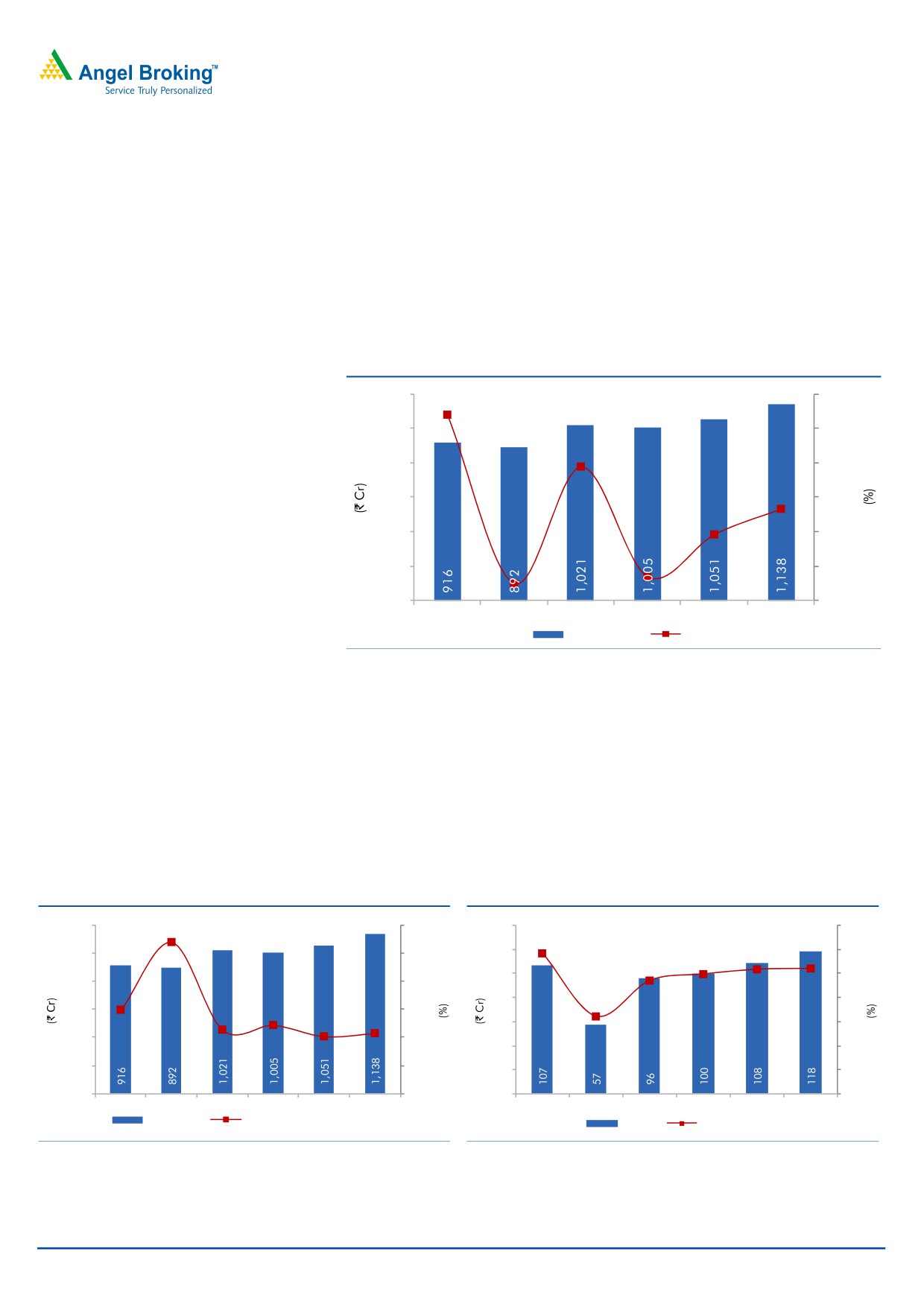

expected to post a CAGR of 6.4% over FY2016-18E to `1,138cr.

Exhibit 4: Sales to post a CAGR of 6.4% over FY2016-18E

1,200

25.0

22.0

1,000

20.0

800

15.0

14.5

600

10.0

8.3

400

5.0

4.6

200

-

-1.6

(2.6)

-

(5.0)

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Net Sales

Sales yoy growth

Source: Company, Angel Research

EBIDTA margin to trend upwards

With chrysotile fibre prices are expected to remain soft and with the currency

expected to remain stable, we expect the raw material cost to come down in

FY2017E and increase from thereon. The company has undertaken steps to curb

its expense which has resulted in savings in the past year and we expect the cost to

sustain at the same levels in term of percentage of sales. As a result, the EBIDTA

margin will improve from 9.9% in FY2016 to 10.4% in FY2017E.

Exhibit 5: Raw material costs remain stable

Exhibit 6: EBITDA margin to improve to 10.2%

1,200

64.0

140

14.0

11.6

62.8

10.4

1,000

62.0

120

10.3

12.0

9.9

9.4

100

10.0

800

60.0

80

6.4

8.0

600

58.0

58.0

56.6

56.9

60

6.0

56.1

56

.3

400

56.0

40

4.0

200

54.0

20

2.0

-

52.0

-

-

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Net Sales

Raw material as % of net sales

EBIDTA

EBIDTA margins

Source: Company, Angel Research

Source: Company, Angel Research

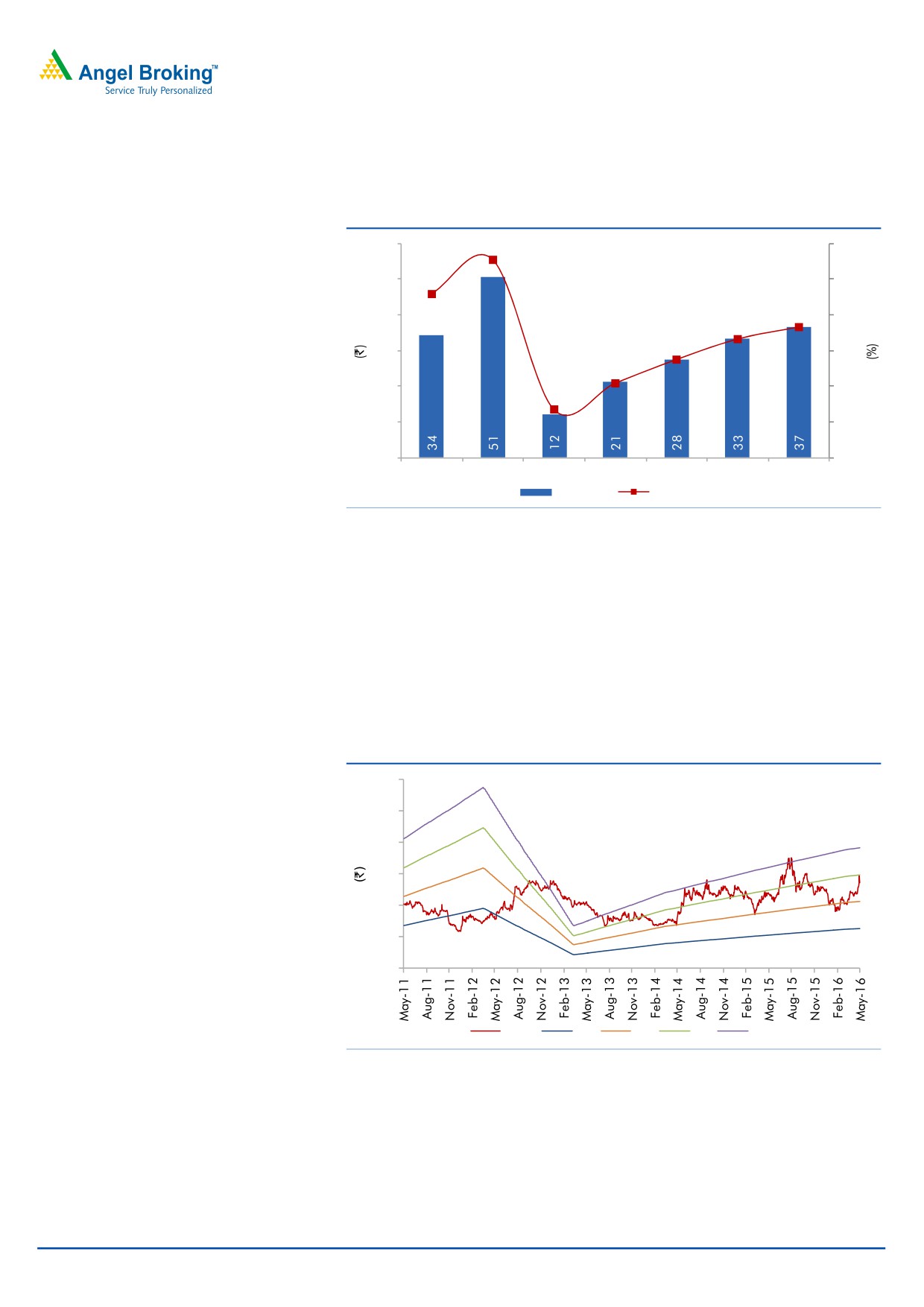

On account of extended capacities being operationalized in FY2017E (Synthetic

Yarn) and FY2018E (Boards), the depreciation expense is estimated to increase

May 21, 2016

5

Visaka Industries | 4QFY2016 Result Update

from current levels. On factoring the same, the bottom-line is expected to improve

from `28cr in FY2016 to `37cr in FY2018E.

Exhibit 7: PAT and PAT margins to improve

60

5.5

6.0

50

4.6

5.0

3.7

40

3.3

4.0

2.7

30

3.0

1.3

2.1

20

2.0

10

1.0

-

-

FY2012

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

ADJ. PAT

PAT margins

Source: Company, Angel Research

Outlook and valuation

We have introduced our FY2018E estimates for the company and have lowered

our expectation for FY2017E on account of near term dampness in the ACS

division. At the current market price of `135, the stock is trading at a valuation of

5.9x FY2018E EPS, which is attractive. We continue to maintain our Buy rating on

the stock, with a revised target price of `162, valuing the stock at 7.0x its FY2018E

earnings.

Exhibit 8: One-year forward PE band

300

250

200

150

100

50

-

Price

3x

5x

7x

9x

Source: Company, Angel Research

May 21, 2016

6

Visaka Industries | 4QFY2016 Result Update

Exhibit 9: Comparative analysis

Company

Year end

Mcap

Sales

OPM PAT

EPS

RoE P/E P/BV

EV/EBITDA

EV/Sales

Visaka Industries

FY2018E

215

1,138

10.4

37

23.1

9.2

5.9

0.5

4.2

0.4

Everest Industries*

FY2018E

438

1,687

7.8

61

39.9

15.4

7.2

1.1

4.7

0.4

Hyderabad

FY2018E

387

1,325

9.9

61

81.7

11.9

6.4

0.7

4.0

0.4

Industries*

Source: Company, Angel Research, *Bloomberg

Key concerns

Forex risk: Asbestos fibre is a key raw material and accounts for 60% of overall

costs and is 100% imported. Since exports are limited and imports are significant,

the company is exposed to forex risk.

Dependence on rural growth: Rural demand for housing is a key growth driver

which depends upon increase in spending power and on government schemes.

High inflation and lower spend could have an adverse impact on roofing in rural

India.

Ban-Asbestos lobby: Asbestos fibre, included with other forms of asbestos, is being

considered to be a human carcinogen by the International Agency for Research on

Cancer (IARC) and by the U.S. Department of Health and Human Services. Any

government initiative to completely ban or restrict use of asbestos fibre will be a

negative.

Lack of entry barriers: Lack of entry barriers is attracting new entrants into this line

of business.

Company Background

Visaka Industries (established in 1985) is engaged in two businesses - building

products (cement asbestos products and fibre cement flat products like V-Boards

and V-Panels) and textiles. Its manufacturing facilities are spread across

11 locations supported by 9 marketing offices. The company is the second largest

cement asbestos products manufacturer in India with a 17% market share. The

spinning plant, with 33 MURATA Twinjet spinning machines is the world's largest

installation of its kind, producing about ~10,800 tons of yarn per annum.

May 21, 2016

7

Visaka Industries | 4QFY2016 Result Update

Profit and Loss

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E

FY2018E

Total operating income

892

1,021

1,005

1,051

1,138

% chg

(2.6)

14.5

(1.6)

4.6

8.3

Net Raw Materials

560

578

572

589

641

% chg

5.5

3.1

(1.0)

3.1

8.7

Personnel

52

59

68

74

78

% chg

10.6

14.1

14.5

8.3

6.0

Other Expenses

223

288

266

280

301

% chg

(3.6)

29.5

(7.9)

5.3

7.7

Total Expenditure

835

925

905

943

1,020

EBITDA

57

96

100

108

118

% chg

(46.3)

67.4

4.0

8.7

9.1

EBITDA Margin

6.4

9.4

9.9

10.3

10.4

Depreciation & Amortisation

22

43

36

39

43

EBIT

35

53

63

70

75

% chg

(60.0)

51.6

20.1

9.7

7.6

(% of Net Sales)

3.9

5.2

6.3

6.9

7.5

Interest & other Charges

21

22

21

23

24

Other Income

5

2

3

3

4

(% of Net Sales)

0.6

0.2

0.3

0.3

0.4

Recurring PBT

13

31

42

47

51

% chg

(81.3)

129.1

36.8

10.7

8.6

Extraordinary Expense/(Inc.)

-

-

5

-

-

PBT (reported)

19

33

40

50

55

Tax

7

12

16

16

18

(% of PBT)

36.3

36.0

39.5

33.0

33.0

PAT (reported)

12

21

24

33

37

Exceptional Item

0.1

-

3.2

-

-

ADJ. PAT

12

21

28

33

37

% chg

(76.3)

76.6

29.8

21.0

10.2

(% of Net Sales)

1.3

2.1

2.7

3.3

3.7

Basic EPS (`)

7.5

13.4

17.4

21.0

23.1

Fully Diluted EPS (`)

7.5

13.4

17.4

21.0

23.1

% chg

(76.4)

77.5

29.8

21.0

10.2

May 21, 2016

8

Visaka Industries | 4QFY2016 Result Update

Balance Sheet

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

FY2018E

SOURCES OF FUNDS

Equity Share Capital

16

16

16

16

16

Preference Capital

-

-

-

-

-

Reserves& Surplus

317

316

331

355

382

Shareholders’ Funds

333

332

347

371

398

Minority Interest

-

-

-

-

-

Total Loans

265

304

318

378

417

Other long term liabilities

24

27

32

32

32

Net Deferred tax liability

30

26

22

22

22

Total Liabilities

652

689

719

803

870

APPLICATION OF FUNDS

Gross Block

527

567

589

648

743

Less: Acc. Depreciation

192

255

291

330

373

Net Block

334

312

298

318

370

Capital Work-in-Progress

21

0

0

40

10

Lease adjustment

-

-

-

-

-

Goodwill

-

-

-

-

-

Investments

15

15

10

10

10

Other non-current assets

0

0

0

0

0

Current Assets

341

444

483

500

548

Cash

26

28

75

99

120

Loans & Advances

30

37

29

30

33

Other current assets

0

0

0

0

0

Current liabilities

77

101

99

93

98

Net Current Assets

264

343

384

407

450

Mis. Exp. not written off

-

-

-

-

-

Total Assets

652

689

719

803

870

May 21, 2016

9

Visaka Industries | 4QFY2016 Result Update

Cash flow statement

Y/E March (` cr)

FY2014 FY2015 FY2016 FY2017E FY2018E

Profit Before Tax

19

33

40

50

55

Depreciation

22

43

36

39

43

Other Income

(5)

(2)

(3)

(3)

(4)

Change in Working Capital

59

(77)

5

1

(22)

Direct taxes paid

(7)

(12)

(16)

(16)

(18)

Cash Flow from Operations

88

(15)

63

70

54

(Incr)/ Decr in Fixed Assets

(111)

(19)

(22)

(98)

(65)

(Incr)/Decr In Investments

22

(2)

(2)

(1)

(2)

Other Income

5

2

3

3

4

Cash Flow from Investing

(83)

(18)

(22)

(96)

(63)

Issue of Equity/Preference

-

-

-

-

-

Incr/(Decr) in Debt

(7)

39

15

60

39

Dividend Paid (Incl. Tax)

(5)

(10)

(10)

(10)

(10)

Others

(1)

6

-

-

-

Cash Flow from Financing

(12)

35

6

51

30

Incr/(Decr) In Cash

(7)

2

46

24

21

Opening cash balance

34

26

28

75

99

Closing cash balance

26

28

75

99

120

May 21, 2016

10

Visaka Industries | 4QFY2016 Result Update

Key Ratios

Y/E March

FY2014

FY2015

FY2016

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

17.9

10.1

7.8

6.4

5.9

P/CEPS

6.2

3.3

3.4

3.0

2.7

P/BV

0.6

0.6

0.6

0.6

0.5

Dividend yield (%)

2.2

4.5

4.5

4.5

4.5

EV/Net sales

0.5

0.5

0.4

0.5

0.4

EV/EBITDA

7.7

5.0

4.5

4.5

4.2

EV / Total Assets

0.7

0.7

0.6

0.6

0.6

Per Share Data (`)

EPS (Basic)

7.5

13.4

17.4

21.0

23.1

EPS (fully diluted)

7.5

13.4

17.4

21.0

23.1

Cash EPS

21.7

40.5

40.2

45.5

50.5

DPS

2.5

5.0

5.0

5.0

5.0

Book Value

209.9

209.2

218.6

233.5

250.6

DuPont Analysis

EBIT margin

3.9

5.2

6.3

6.6

6.6

Tax retention ratio

0.6

0.6

0.6

0.7

0.7

Asset turnover (x)

1.5

1.6

1.6

1.6

1.6

ROIC (Post-tax)

3.8

5.2

6.1

7.1

6.9

Cost of Debt (Post Tax)

5.1

4.6

4.1

4.1

3.9

Leverage (x)

0.7

0.8

0.7

0.7

0.7

Operating ROE

2.8

5.7

7.4

9.4

9.0

Returns (%)

ROCE (Pre-tax)

5.3

7.7

8.8

8.7

8.6

Angel ROIC (Pre-tax)

5.9

8.2

10.0

10.6

10.3

ROE

3.6

6.4

7.9

9.0

9.2

Turnover ratios (x)

Asset TO (Gross Block)

1.7

1.8

1.7

1.6

1.5

Inventory / Net sales (days)

94

78

88

82

80

Receivables (days)

38

40

50

45

45

Payables (days)

31

36

36

36

35

WC cycle (ex-cash) (days)

109

99

113

107

102

Solvency ratios (x)

Net debt to equity

0.7

0.8

0.7

0.7

0.7

Net debt to EBITDA

3.9

2.7

2.3

2.5

2.4

Int. Coverage (EBIT/ Int.)

1.6

2.4

3.0

3.0

3.1

May 21, 2016

11

Visaka Industries | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Visaka Industries

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

May 21, 2016

12