2QFY2016 Result Update | Cement Products

November 18, 2015

Visaka Industries

BUY

CMP

`119

Performance Highlights

Target Price

`144

Y/E March (` cr)

2QFY16 2QFY15

% chg (yoy) 1QFY16

% chg (qoq)

Investment Period

12 Months

Net sales

192

210

(8.2)

321

(40.2)

Stock Info

EBITDA

15

19

(21.6)

36

(57.6)

EBITDA Margin (%)

7.9

9.3

(135)bp

11.2

(326)bp

Sector

Cement Products

Adjusted PAT

0.8

3.7

(78.9)

13.6

(94.3)

Market Cap (` cr)

189

Source: Company, Angel Research

Net Debt

262

For 2QFY2016, Visaka Industries reported a mixed set of numbers. The top-line,

Beta

1.4

at `192cr (8.2% yoy decline), was marginally below our estimate of `205cr. The

52 Week High / Low

189 / 85

EBITDA declined by 21.6% yoy to `15cr and the EBITDA margin contracted by

Avg. Daily Volume

17,961

135bp yoy to 7.9%, owing to a 109bp yoy increase in raw material cost as a

percentage of sales to 50.2% and 157bp yoy increase in employee expense to

Face Value (`)

10

8.0% of sales. Other expenses declined by 131bp yoy to 33.9% of sales. We had

BSE Sensex

25,864

built in an EBITDA margin estimate of 6.4%. Interest expense at `5cr was higher

Nifty

7,838

by 19.7% on a yoy basis. Consequently, the net profit declined by 78.9% yoy to

Reuters Code

VSKI.BO

`0.8cr, against our estimate of `1.5cr.

Bloomberg Code

VSKI.IN

Near term pressure for Asbestos Cement Products (ACP); Overall long term

prospects intact: The ACP division of the Building Products segment is likely to

Shareholding Pattern (%)

face pressure in the near term on account of subdued rural sentiment. However,

Promoters

37.5

the company is a major player with ~17% market share. With the rural economy

expected to improve in the longer run, we expect the division to perform well

MF / Banks / Indian Fls

0.7

going forward. The Building products segment is also supported by strong

FII / NRIs / OCBs

3.9

performance of its V-boards division which is expected to post a robust

Indian Public / Others

57.8

performance on account of growing acceptance and cost advantages against

substitute products and increasing contribution of exports. Additionally, we expect the

Abs.(%)

3m 1yr

3yr

Synthetic yarn segment to remain a steady contributor, thus aiding top-line growth.

Sensex

(7.6)

(8.6)

40.7

Outlook and Valuations: We have marginally revised our estimates downwards

Visaka

(25.8)

(6.3)

(4.8)

for FY2017E to factor in the lower than estimated numbers. At the current market

price of `119, the stock is trading at a valuation of 4.1x FY2016E EPS, which

continues to be attractive. We continue to maintain our Buy rating on the stock,

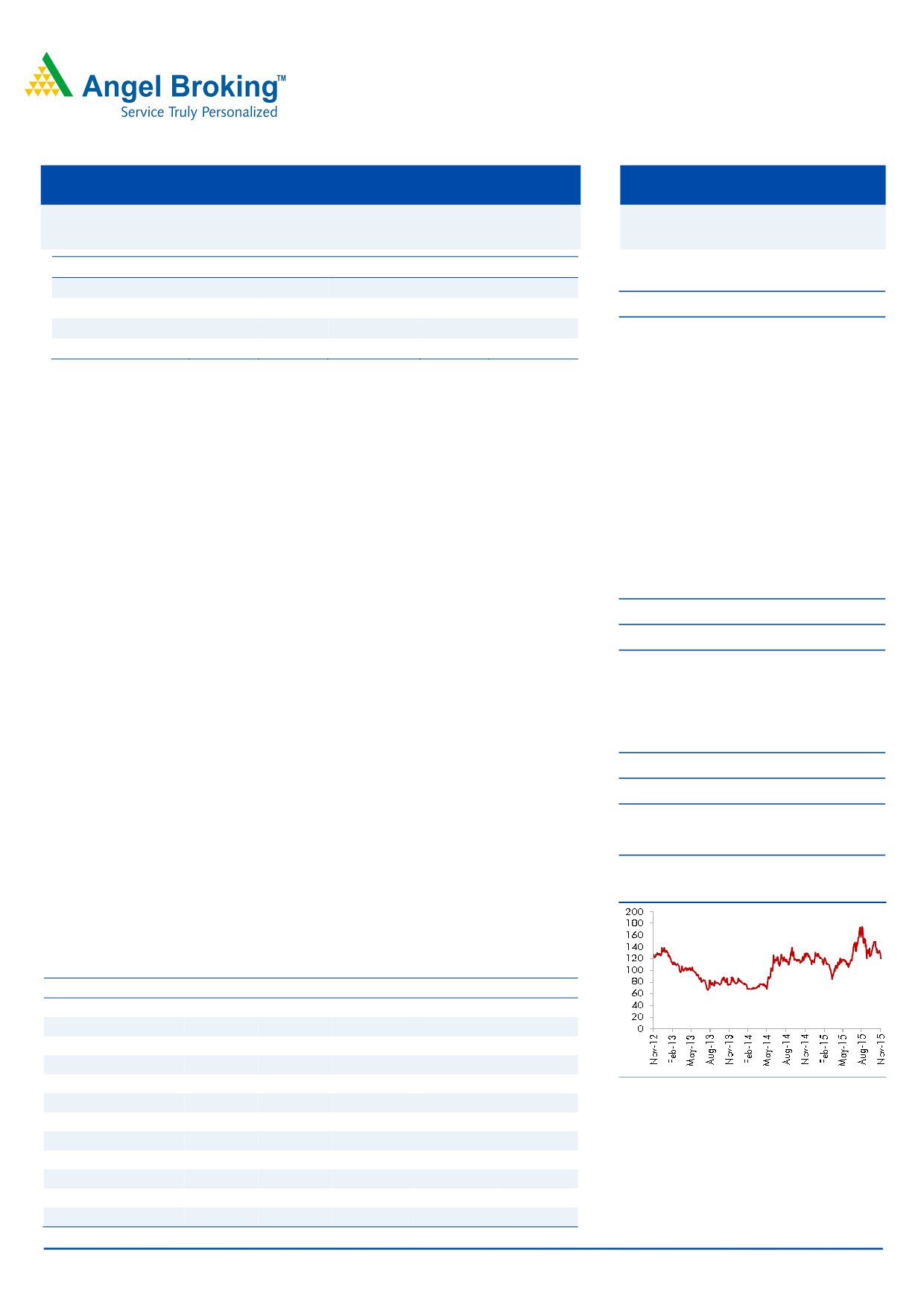

3 Year Price Chart

with a revised target price of `144, valuing the stock at 5.0x on FY2017E

earnings.

Key financials

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Net sales

916

892

1,021

1,086

1,197

% chg

22.0

(2.6)

14.5

6.4

10.2

Adj. net profit

51

12

21

34

46

% chg

47.5

(76.3)

76.5

61.0

33.5

EBITDA Margin (%)

11.6

6.4

9.4

9.9

10.2

Source: Company, Angel Research

EPS (`)

31.9

7.5

13.4

21.5

28.7

P/E (x)

3.7

15.7

8.9

5.5

4.1

P/BV (x)

0.6

0.6

0.6

0.5

0.5

RoE (%)

15.6

3.6

6.4

9.6

11.6

RoCE (%)

13.4

5.3

7.7

10.1

11.7

Milan Desai

EV/Sales (x)

0.5

0.5

0.4

0.4

0.4

+91 22 4000 3600 Ext: 6846

EV/EBITDA (x)

9.5

3.9

5.2

6.5

7.0

Source: Company, Angel Research; Note: CMP as of November 17, 2015

Please refer to important disclosures at the end of this report

1

Visaka Industries | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance

Y/E March (` cr)

2QFY16

2QFY15

% chg (yoy)

1QFY16

% chg (qoq)

1HFY16

1HFY15

% chg

Total operating income

192

210

(8.2)

321

(40.2)

514

522

(1.6)

Net raw material

97

103

(6.2)

189

(48.8)

285

296

(3.7)

(% of Sales)

50.2

49.1

109bp

58.7

(849)bp

55.5

56.8

(124)bp

Employee cost

15

13

14.2

19

(17.1)

34

31

10.9

(% of Sales)

8.0

6.4

157bp

5.8

223bp

6.6

5.9

74bp

Other Expenses

65

74

(11.7)

78

(16.8)

143

141

1.4

(% of Sales)

33.9

35.2

(131)bp

24.3

952bp

27.9

27.1

81bp

Total expenditure

177

190

(6.9)

286

(38.0)

463

468

(1.2)

EBITDA

15

19

(21.6)

36

(57.6)

51

54

(4.6)

EBITDA Margin (%)

7.9

9.3

(135)bp

11.2

(326)bp

10.0

10.3

(32)bp

Interest

5

4

19.7

5

(11.8)

10

9

15.1

Depreciation

10

10

(6.1)

9

0.3

19

24

(20.0)

Other income

1

1

(16.6)

1

(56.0)

2

2

21.9

PBT

1

6

21.1

22

17.0

24

22

5.6

(% of Sales)

0.7

2.8

6.9

4.6

4.3

Tax

0.6

2.2

(70.8)

8.6

(92.5)

9

7

23.4

(% of PBT)

45.3

37.4

38.7

39.1

33.5

Reported PAT

0.8

4

78.9

14

(94.3)

14

15

(3.4)

Exceptional items

0

0

0

0

0

Adjusted PAT

1

4

78.9

14

(94.3)

14

15

(3.4)

PATM (%)

0.4

1.8

4.2

2.8

2.9

Source: Company, Angel Research

Result mostly below our expectations

For 2QFY2016, Visaka Industries reported a mixed set of numbers. The top-line at

`192cr (8.2% yoy decline) was below our estimates of `205cr. The EBITDA

declined by 21.6% yoy to `15cr and the EBITDA margin contracted by 135bp yoy

to 7.9% owing to a 109bp yoy increase in raw material cost as a percentage of

sales to 50.2% and 157bp yoy increase in employee expense to 8.0% of sales. We

had accounted for a higher raw material expense (52.3% of sales on account of

USD appreciation against INR). Other expenses declined by 131bp yoy to 33.9%

of sales. We had built in an EBITDA margin estimate of 6.4%. The interest expense

at `5cr was higher by 19.7% on a yoy basis. As a result, the net profit declined by

78.9% yoy to `0.8cr. We had estimated a net profit of `1.5cr for the quarter.

Exhibit 2: Actual vs. Estimate

Actual v/s Angel's Estimates

Actual (`cr)

Estimate (`cr)

% variation

Total Income (` cr)

192

205

(6.1)

EBITDA (`cr)

15

13

16.8

EBITDA Margin (%)

7.9

6.4

155bp

Adjusted PAT (` cr)

0.8

1.5

(48.4)

Source: Company, Angel Research

November 18, 2015

2

Visaka Industries | 2QFY2016 Result Update

Segmental performance

Sales of the Building products segment declined by 7.7% yoy to `147.7cr, while

that of Synthetic yarn segment declined by 13.2% yoy to `41.9cr. The Building

products segment reported an EBIT of `3.4cr and EBIT margin of 2.3% as against

EBIT and EBIT margin of `6.7cr and 4.2%, respectively in the corresponding

quarter a year ago. The Synthetic yarn division reported EBIT and EBIT margin of

`7.1cr and 16.9% respectively, as against `6.0cr and 12.4%, in the corresponding

quarter a year ago.

Exhibit 3: Segment-wise performance

Y/E Mar (` cr)

2QFY16

2QFY15

% chg (yoy) 1QFY16

% chg (qoq)

Total Revenue

A) Building Products

147.7

160.0

(7.7)

273.5

(46.0)

B) Synthetic Yarn

41.9

48.3

(13.2)

44.3

(5.4)

Total

189.6

(51.4)

(468.7)

317.8

(40.3)

EBIT

A) Building Products

3.4

6.7

(49.0)

24.5

(86.1)

B) Synthetic Yarn

7.1

6.0

18.3

7.7

(8.1)

Total

10.5

(94.2)

(111.1)

32.2

(67.5)

EBIT Margin (%)

A) Building Products

2.3

4.2

(187)bp

9.0

(667)bp

B) Synthetic Yarn

16.9

12.4

451bp

17.4

(49)bp

Source: Company, Angel Research

November 18, 2015

3

Visaka Industries | 2QFY2016 Result Update

Investment arguments

Long term prospects intact, near term pressure for ACP division

The company’s Building products segment’s sales are dominated by Asbestos

Cement Products (accounting for 72% of FY2015 revenue). The company has

expanded its capacity from 6,52,000MT in FY2011 to 7,52,000MT in FY2012 to

cater to the rising rural demand. In the near term, we expect the Asbestos Cement

Products performance to be under pressure on account of poor monsoons

impacting rural sentiment. The company has been the second largest cement

asbestos products manufacturer in India with a 17% market share supported by its

outdoor advertising campaign and strong dealer network. In the longer run, we

expect the division to perform well once the rural sentiment turns positive.

The growth in the Building product segment is also supported by strong

performance of its V-boards division (capacity of 1,20,000MT). We expect the

V-boards division to post a robust performance going ahead as well, on account

of growing acceptance in India due to cost advantages against substitute products

and increasing contribution of exports.

The company’s Synthetic yarn segment has an installed capacity of 55,000 ring

spindles (31 MT M/CS). Strong growth in exports coupled with improvement in

realizations due to rupee depreciation would enable the company to post decent

revenue growth going ahead. As per the Federation of Indian Chamber of

Commerce and Industry (FICCI), India’s textile exports are expected to rise from

US$21bn in 2012 to US$145.6bn by 2023. This augurs well for the company as it

is expected to increase its focus on the export business which has higher margins.

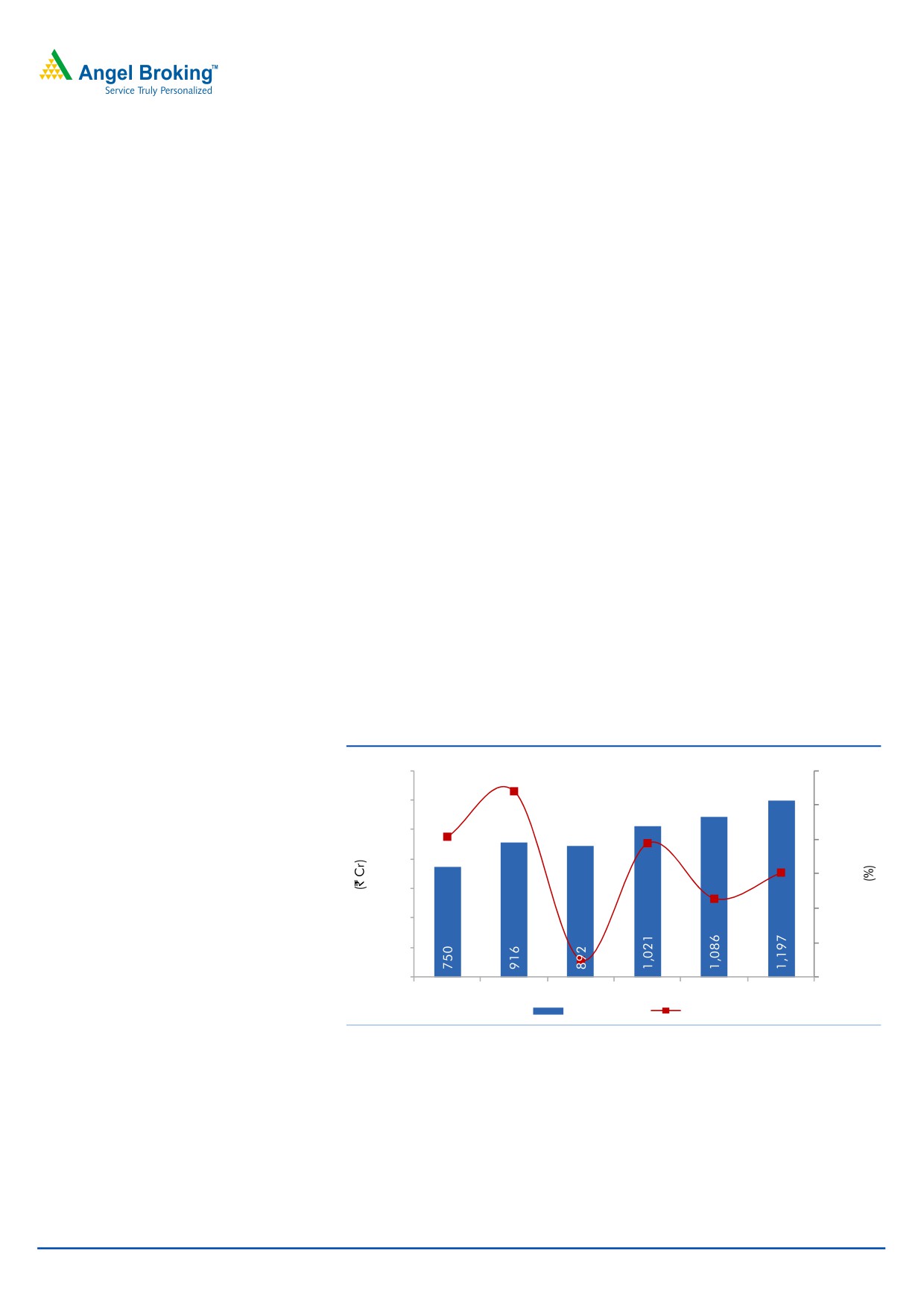

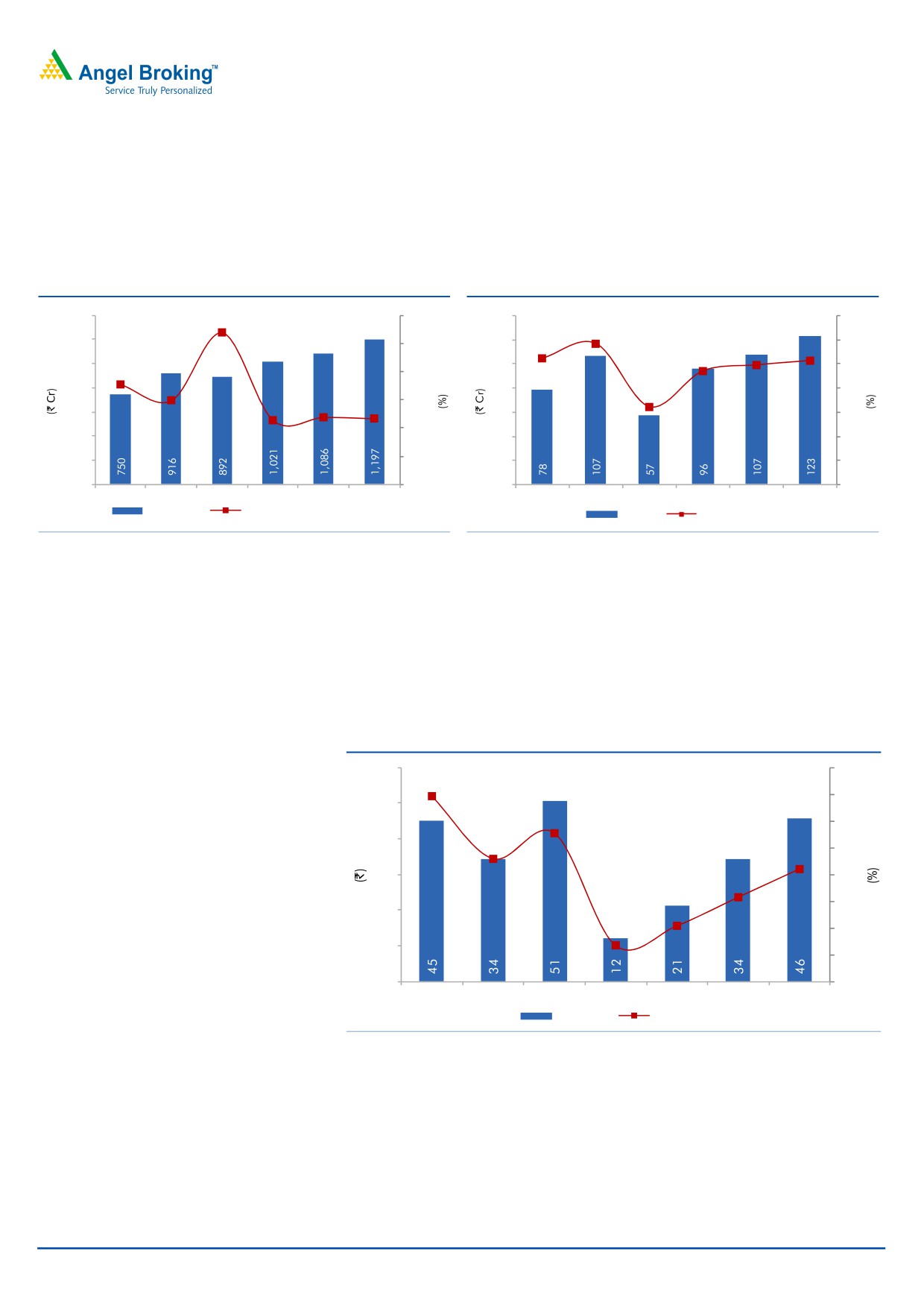

Exhibit 4: Sales to post a CAGR of 8.3% over FY2015-17E

1,400

25.0

22.0

1,200

20.0

1,000

15.4

15.0

14.5

800

10.

2

10.0

600

6.4

5.0

400

-

200

(2.6)

-

(5.0)

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

Net Sales

Sales yoy growth

Source: Company, Angel Research

EBIDTA margin to witness an uptrend

The company’s raw material cost is expected to more or less be at levels of

FY2015. The company’s net raw-material cost as a percentage of sales is expected

to be at ~56.7% of sales in FY2017E. Asbestos fibre, the key raw material for

asbestos cement products is 100% imported and accounts for 60% of raw material

cost of building products segment. The recent depreciation of INR against the USD

November 18, 2015

4

Visaka Industries | 2QFY2016 Result Update

will impact the raw material cost to some extent. Moreover, asbestos fibre, cement

and fly ash prices are expected to remain flat. Freight costs too are expected to

remain stable as diesel prices have cooled down. The company is expected to

increase exports in its Synthetic yarn business, which has higher margins. As a result,

the EBIDTA margin will improve from 9.4% in FY2015 to 10.2% in FY2017E.

Exhibit 5: Raw material costs remain stable

Exhibit 6: EBITDA margin to improve to 10.2%

1,400

64.0

140

14.0

62.8

1,200

120

12.0

62.0

11.6

10.4

9.9

10

.2

1,000

100

10.0

60.0

9.4

800

59.1

80

8.0

58.0

58.0

56.8

6.4

600

56

.7

60

6.0

56.6

56.0

400

40

4.0

54.0

200

20

2.0

-

52.0

-

-

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

Net Sales

Raw material as % of net sales

EBIDTA

EBIDTA margins

Source: Company, Angel Research

Source: Company, Angel Research

PAT to grow at a CAGR of 46.6% over FY2015-17E

With improvement in EBIDTA margins coupled with lower depreciation cost,

especially in FY2017E, the PAT is expected to grow at a CAGR of 46.6% over

FY2015-17E to `46cr. As a result, the PAT margins are expected to improve from

2.1% in FY2015 to 4.2% in FY2017E.

Exhibit 7: PAT and PAT margins to improve

60

8.0

6.9

5.5

7.0

4.2

50

6.0

40

4.6

3.1

5.0

30

4.0

2.1

3.0

20

1.3

2.0

10

1.0

-

-

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

ADJ. PAT

PAT margins

Source: Company, Angel Research

Outlook and valuation

We have marginally revised our estimates downwards for FY2017E to factor in

lower than estimated numbers for the quarter. At the current market price of `119,

the stock is trading at a valuation of 4.1x FY2017E EPS, which continues to be

attractive. We continue to maintain our Buy rating on the stock, with a revised

target price of `144, valuing the stock at 5.0x on FY2017E earnings.

November 18, 2015

5

Visaka Industries | 2QFY2016 Result Update

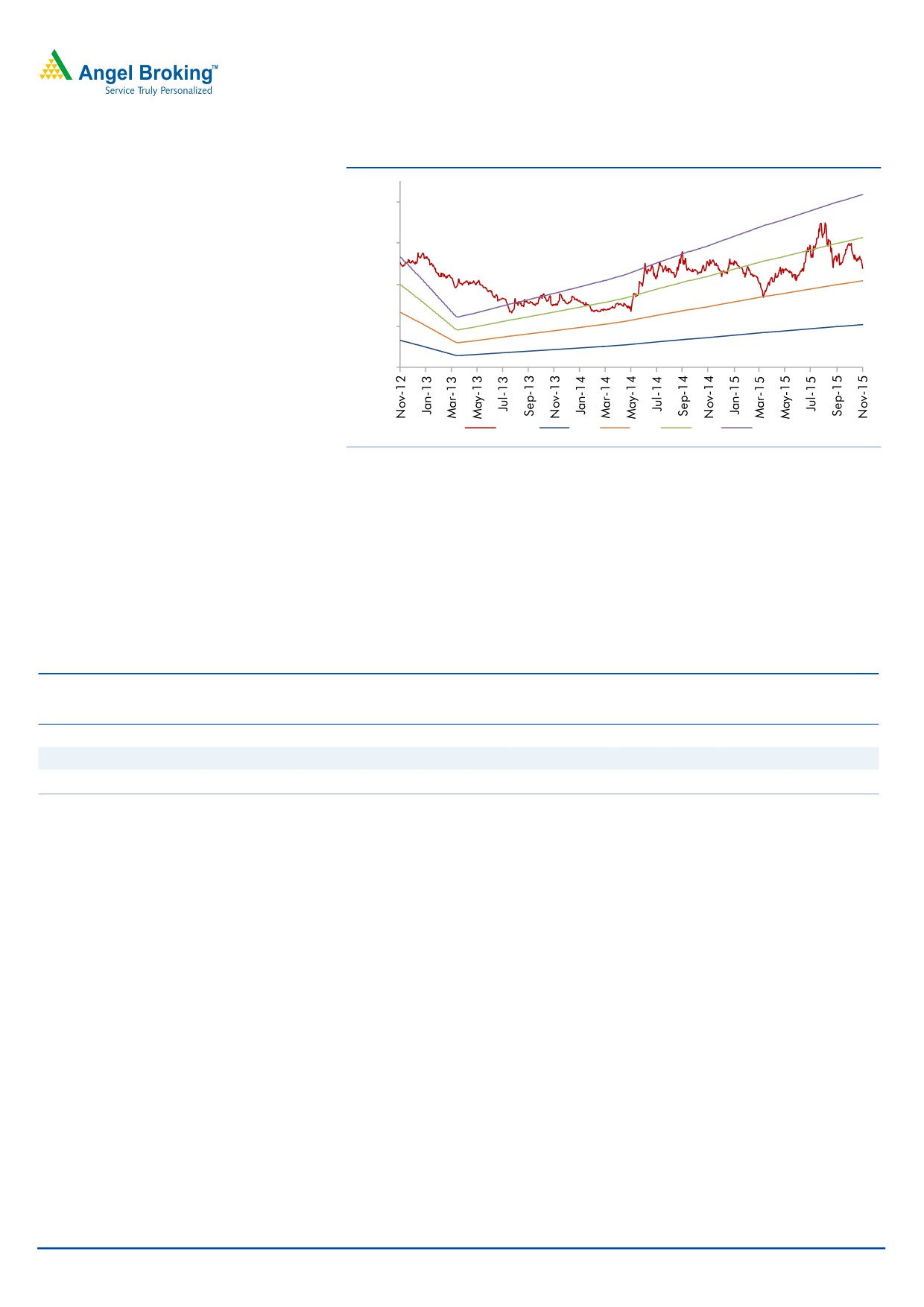

Exhibit 8: One-year forward PE band

200

150

100

50

-

Price

2 x

4 x

6 x

8 x

Source: Company, Angel Research

Relative valuation

The leading players in the industry are Hyderabad Industries, Visaka Industries,

Everest Industries and Ramco Industries. These companies account for 70-75% of

industry capacity. Visaka Industries is trading at a cheap valuation of 4.1x P/E and

0.5x P/BV on FY2017E as compared to its peers which are trading at relatively

high valuations.

Exhibit 9: Comparative analysis

Company

Year end

Mcap

Sales

OPM PAT

EPS

RoE

P/E

P/BV

EV/Sales

EV/EBIDTA

Visaka Industries

FY2017E

189

1,197

10.2

46

28.7

11.6

4.1

0.5

3.5

0.4

Everest Industries*

FY2017E

437

1,596

7.6

55

36.0

15.1

7.9

1.2

5.5

0.4

Hyderabad Industries*

FY2017E

437

1,370

11.1

81

108.6

16.8

5.4

0.9

3.7

0.4

Source: Company, Angel Research, *Bloomberg

Key concerns

Increase in input costs due to rupee depreciation: The continuous increase in cost

of inputs is a matter of concern. Asbestos fibre, cement and fly ash and polyester

fibre are the key materials. Asbestos fibre is a key raw material and accounts for

60% of overall cost and is 100% imported. Since exports are limited and imports

are significant, the company is exposed to forex risk.

Dependence on rural growth: Rural demand for housing is the key growth driver

which depends upon increase in spending power and on government schemes.

High inflation and lower spend could have an adverse impact on roofing in rural

India.

Ban Asbestos Lobby: Asbestos fibre, included with other forms of asbestos, is being

considered to be a human carcinogen by the International Agency for Research on

Cancer (IARC) and by the U.S. Department of Health and Human Services. Any

government initiative to completely ban or restrict use of asbestos fibre will be a

negative.

November 18, 2015

6

Visaka Industries | 2QFY2016 Result Update

Lack of entry barriers: Lack of entry barriers is attracting new entrants into this line

of business. Closure of Canadian and Zimbabwean asbestos mines are a matter

of concern.

Company Background

Visaka Industries (established in 1985) is engaged in two businesses - building

products (cement asbestos products and fibre cement flat products like V-Boards

and V-Panels) and textiles. Its manufacturing facilities are spread across

11 locations supported by nine marketing offices. The company is the second

largest cement asbestos products manufacturer in India with a 17% market share.

The spinning plant, with

31 MURATA Twinjet spinning machines and

112

Two-For-One twisting machines, is the world's largest installation of its kind,

producing about 9,000 tons of yarns per annum.

November 18, 2015

7

Visaka Industries | 2QFY2016 Result Update

Profit and Loss

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Net Sales

916

892

1,021

1,086

1,197

Other operating income

-

-

-

-

-

Total operating income

916

892

1,021

1,086

1,197

% chg

22.0

(2.6)

14.5

6.4

10.2

Net Raw Materials

531

560

578

617

678

% chg

19.7

5.5

3.1

6.8

10.0

Power and Fuel costs

51

48

51

53

59

% chg

31.4

(6.4)

6.3

4.9

10.2

Personnel

47

52

59

67

75

% chg

12.2

10.6

14.1

13.5

12.0

Selling & Admin Expenses

79

86

119

127

139

% chg

11.9

8.7

38.1

6.1

9.8

Other

101

89

118

115

123

% chg

31.0

(12.0)

33.6

(2.7)

6.7

Total Expenditure

809

835

925

979

1,074

EBITDA

107

57

96

107

123

% chg

36.1

(46.3)

67.4

12.0

14.2

EBITDA Margin

11.6

6.4

9.4

9.9

10.2

Depreciation & Amortisation

20

22

43

37

39

EBIT

87

35

53

70

84

% chg

43.3

(60.0)

51.6

33.4

19.1

(% of Net Sales)

9.5

3.9

5.2

6.5

7.7

Interest & other Charges

15

21

22

21

18

Other Income

3

5

2

3

3

(% of Net Sales)

0.3

0.6

0.2

0.3

0.3

Recurring PBT

72

13

31

49

66

% chg

54.7

(81.3)

129.0

59.2

35.5

PBT (reported)

75

19

33

52

69

Tax

24

7

12

18

24

(% of PBT)

32.1

36.3

36.1

34.0

34.0

PAT (reported)

51

12

21

34

46

Extraordinary Expense/(Inc.)

(0.1)

(0.1)

-

-

-

ADJ. PAT

51

12

21

34

46

% chg

47.5

(76.3)

76.5

61.0

33.5

(% of Net Sales)

5.5

1.3

2.1

3.1

4.2

Basic EPS (`)

31.9

7.5

13.4

21.5

28.7

Fully Diluted EPS (`)

31.9

7.5

13.4

21.5

28.7

% chg

47.5

(76.4)

77.3

61.0

33.5

November 18, 2015

8

Visaka Industries | 2QFY2016 Result Update

Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

SOURCES OF FUNDS

Equity Share Capital

16

16

16

16

16

Preference Capital

-

-

-

-

-

Reserves& Surplus

310

317

316

341

377

Shareholders’ Funds

326

333

332

357

393

Minority Interest

-

-

-

-

-

Total Loans

277

265

304

288

273

Other long term liabilities

21

24

27

27

27

Net Deferred tax liability

26

30

26

26

26

Total Liabilities

651

652

689

698

719

APPLICATION OF FUNDS

Gross Block

421

527

567

606

624

Less: Acc. Depreciation

171

192

255

291

330

Net Block

250

334

312

315

294

Capital Work-in-Progress

16

21

0

0

0

Lease adjustment

-

-

-

-

-

Goodwill

0

0

0

0

0

Investments

15

15

15

15

15

Other non-current assets

0

0

0

0

0

Current Assets

419

341

444

445

497

Cash

34

26

28

30

63

Loans & Advances

26

30

37

39

43

Other current assets

0

0

0

0

0

Current liabilities

89

77

101

97

107

Net Current Assets

330

264

343

348

390

Mis. Exp. not written off

-

-

-

-

-

Total Assets

651

652

689

698

719

November 18, 2015

9

Visaka Industries | 2QFY2016 Result Update

Cash flow statement

Y/E March (` cr)

FY2013 FY2014 FY2015 FY2016E FY2017E

Profit Before Tax

75

19

33

52

69

Depreciation

20

22

43

37

39

Other Income

(3)

(5)

(2)

(3)

(3)

Change in Working Capital

(136)

59

(77)

(4)

(8)

Direct taxes paid

(24)

(7)

(12)

(18)

(24)

Cash Flow from Operations

(68)

88

(15)

64

73

(Incr)/ Decr in Fixed Assets

(37)

(111)

(19)

(40)

(18)

(Incr)/Decr In Investments

(29)

22

(2)

-

-

Other Income

3

5

2

3

3

Cash Flow from Investing

(63)

(83)

(18)

(37)

(15)

Issue of Equity/Preference

-

-

-

-

-

Incr/(Decr) in Debt

123

(7)

39

(16)

(15)

Dividend Paid (Incl. Tax)

(11)

(5)

(10)

(10)

(10)

Others

(0)

(1)

6

-

-

Cash Flow from Financing

111

(12)

35

(26)

(25)

Incr/(Decr) In Cash

(20)

(7)

2

2

33

Opening cash balance

54

34

26

28

30

Closing cash balance

34

26

28

30

63

November 18, 2015

10

Visaka Industries | 2QFY2016 Result Update

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

3.7

15.7

8.9

5.5

4.1

P/CEPS

2.7

5.5

2.9

2.7

2.2

P/BV

0.6

0.6

0.6

0.5

0.5

Dividend yield (%)

5.9

2.5

5.1

5.1

5.1

EV/Net sales

0.5

0.5

0.4

0.4

0.4

EV/EBITDA

3.9

7.2

4.7

4.0

3.5

EV / Total Assets

0.6

0.6

0.7

0.6

0.6

Per Share Data (`)

EPS (Basic)

31.9

7.5

13.4

21.5

28.7

EPS (fully diluted)

31.9

7.5

13.4

21.5

28.7

Cash EPS

44.3

21.7

40.5

44.8

53.2

DPS

6.0

2.5

5.0

5.0

5.0

Book Value

205.3

209.9

209.2

224.6

247.3

DuPont Analysis

EBIT margin

9.5

3.9

5.2

6.5

7.0

Tax retention ratio

0.7

0.6

0.6

0.7

0.7

Asset turnover (x)

1.6

1.5

1.6

1.7

1.9

ROIC (Post-tax)

10.1

3.8

5.2

7.1

8.6

Cost of Debt (Post Tax)

3.7

5.1

4.6

4.9

4.2

Leverage (x)

0.7

0.7

0.8

0.7

0.5

Operating ROE

14.6

2.8

5.7

8.6

10.8

Returns (%)

ROCE (Pre-tax)

13.4

5.3

7.7

10.1

11.7

Angel ROIC (Pre-tax)

14.9

5.9

8.2

10.8

13.1

ROE

15.6

3.6

6.4

9.6

11.6

Turnover ratios (x)

Asset TO (Gross Block)

2.2

1.7

1.8

1.8

1.9

Inventory / Net sales (days)

85

94

78

85

78

Receivables (days)

32

38

40

40

40

Payables (days)

35

31

36

36

36

WC cycle (ex-cash) (days)

91

109

99

106

98

Solvency ratios (x)

Net debt to equity

0.7

0.7

0.8

0.7

0.5

Net debt to EBITDA

2.1

3.9

2.7

2.3

1.6

Int. Coverage (EBIT/ Int.)

5.8

1.6

2.4

3.3

4.8

November 18, 2015

11

Visaka Industries | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Visaka Industries

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 18, 2015

12