4QFY2016 Result Update | Capital Goods

June 1, 2016

VA Tech Wabag

BUY

CMP

`575

Performance Highlights

Target Price

`681

Quarterly highlights - Standalone

Investment Period

12 Months

Y/E March (` cr)

4QFY16 4QFY15 3QFY16

% chg (yoy)

% chg (qoq)

Stock Info

Net sales

553

568

371

(2.6)

49.0

Sector

Capital Goods

EBITDA

93

78

37

19.2

153.2

Market Cap (` cr)

3,134

Reported PAT

56

52

21

8.2

171.8

Net debt (` cr)

19

Source: Company, Angel Research;

Beta

0.8

For 4QFY2016, VA Tech Wabag (Wabag) reported a 2.6% yoy decline in sales to

52 Week High / Low

833/409

`553cr, reflecting weak execution across the EPC-Municipal business. The EBITDA

Avg. Daily Volume

212,407

grew 19.2% yoy to `93cr while the EBITDA margin expanded by 306bp yoy to

Face Value (`)

2

16.8%. In-line with the EBITDA margin, the PAT margin expanded to 10.2%

BSE Sensex

26,836

during the quarter vs 9.1% in 4QFY2015.

Nifty

8,160

Reuters Code

VATE.BO

International revenues declined 10.4% yoy to `303cr, on account of Euro

Bloomberg Code

VATW@IN

depreciation and with some of the projects being at early stages of execution and

therefore not contributing to revenues. A poor operating performance coupled with

a higher tax rate led to losses in the international business during the quarter.

Shareholding Pattern (%)

The order book as of 4QFY2016-end stood at `8,315cr, reflecting order book /

Promoters

29.0

last twelve month (LTM) sales ratio of 3.3x.

MF / Banks / Indian Fls

25.4

FII / NRIs / OCBs

27.1

Valuation: Wabag trades at FY2017E/2018E P/E multiple of

22.1x/16.0x.

Indian Public / Others

18.5

Recently the company reported large ticket order wins from the Middle East and

Asian sub-continent (worth `2,862cr), which tend to enjoy higher margins than

orders from Europe. These order wins have now taken the order book to highs of

Abs. (%)

3m 1yr 3yr

`8,315cr, reflecting OB/LTM ratio at 3.3x. With better revenue visibility, we now

Sensex

12.1

(4.2)

36.0

expect Wabag to report 23.0% top-line and 45.6% bottom-line CAGR during

Wabag

36.7

(22.8)

146.2

FY2016-18E, respectively. Accordingly, we expect RoEs to expand from 9.7% in

FY2016 to 15.9% in FY2018E. Given such earnings growth and RoE expansion

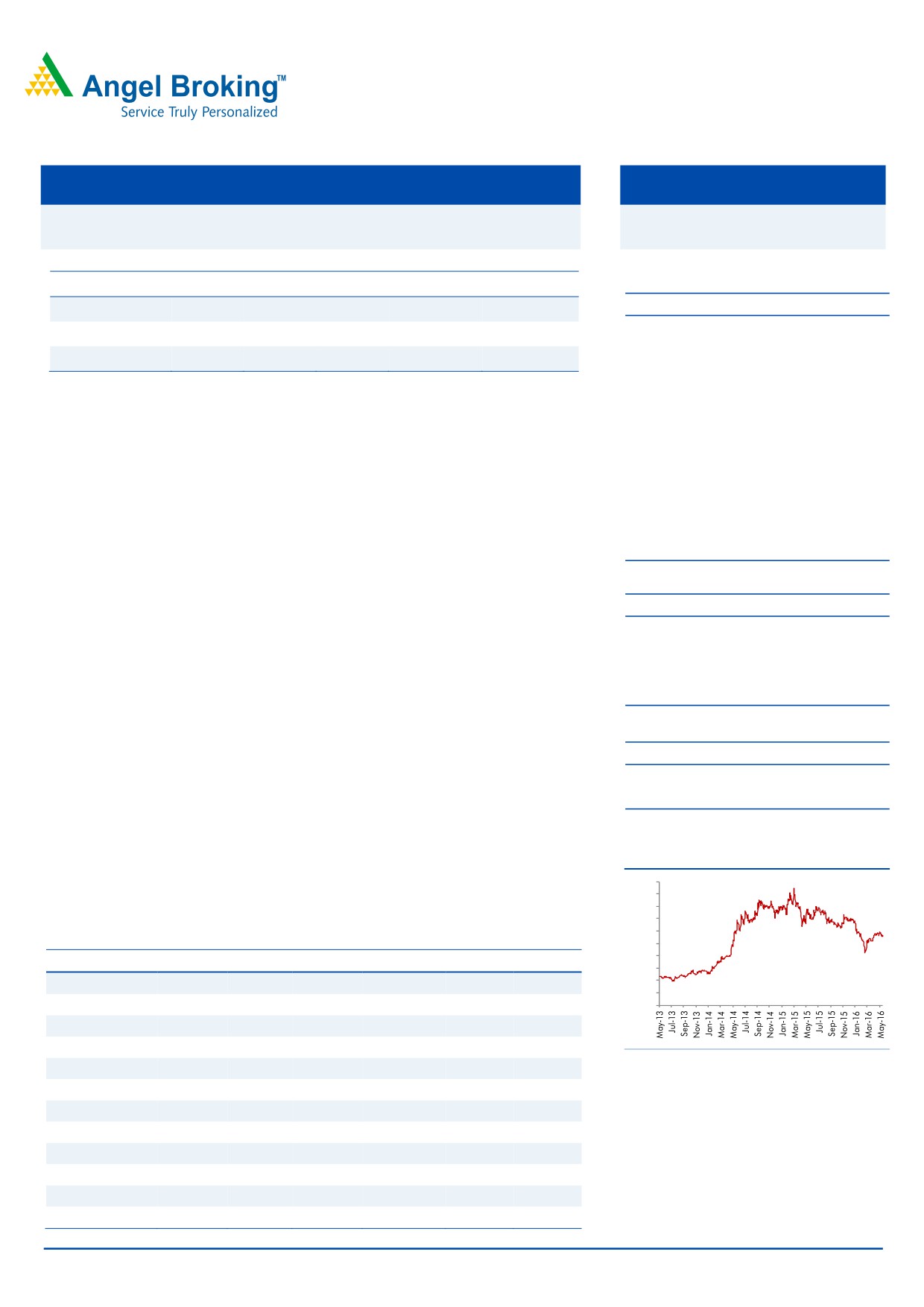

3-Year Daily Price Chart

potential, we assign 19.0x P/E multiple to our FY2018E EPS of `35.9 to arrive at

1000

a price target of

`681. Given the 18.5% upside potential, we upgrade our

900

800

recommendation on the stock to BUY.

700

600

Key financials (Consolidated)

500

400

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

300

200

Net Sales

1,619

2,239

2,435

2,542

3,136

3,845

100

% chg

12.1

38.3

8.8

4.4

23.3

22.6

0

Net Profit

90

114

112

94

144

197

% chg

22.5

25.5

(2.9)

(16.3)

53.9

37.7

Source: Company, Angel Research

EBITDA (%)

9.6

8.4

8.6

8.6

8.9

9.1

EPS (`)

34

42

20

17

26

36

P/E (x)

17.0

13.6

28.5

34.0

22.1

16.0

P/BV (x)

2.1

1.8

3.5

3.2

2.8

2.4

RoE (%)

12.6

14.6

12.6

9.7

13.4

15.9

RoCE (%)

20.1

20.6

22.0

19.9

22.4

24.5

Yellapu Santosh

EV/Sales (x)

0.8

0.6

1.2

1.2

0.9

0.7

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

8.5

7.0

14.3

14.5

10.3

7.8

Source: Company, Angel Research; CMP as of May 31, 2016

Please refer to important disclosures at the end of this report

1

VA Tech Wabag | 4QFY2016 Result Update

Exhibit 1: Quarterly Performance (Standalone)

Particulars (` cr)

4QFY16

3QFY16

% chg (qoq)

4QFY15

% chg (yoy)

FY16

FY15

% chg

Net Sales

553

371

49.0

568

(2.6)

1,503

1,220

23.2

Total Expenditure

460

335

37.5

490

(6.0)

1,307

1,084

20.6

Cost of materials consumed

425

311

36.7

422

0.7

1,190

958

24.3

Change in Inventories

3

(22)

(112.9)

30

(90.8)

(36)

(15)

131.2

Employee benefits Expense

24

23

1.0

19

22.5

94

81

16.7

Other Expenses

9

22

(59.3)

18

(50.1)

59

61

(4.5)

EBITDA

93

37

153.2

78

19.2

195

136

43.7

EBIDTA %

16.8

9.9

13.7

13.0

11.1

Depreciation

3

3

1.0

3

(10.0)

12

7

62.0

EBIT

90

34

166.4

75

20.5

183

129

42.6

Interest and Financial Charges

6

5

35.1

0

nmf

15

6

166.7

Other Income & forex (gain)/loss

2

2

41.1

4

nmf

11

13

(19.8)

PBT before Exceptional Items

86

31

179.4

78

10.0

179

136

31.3

Exceptional Items

0

0

0

0

0

PBT after Exceptional Items

86

31

179.4

78

10.0

179

136

31.3

Tax

30

10

195.0

26

13.4

61

46

34.0

% of PBT

34.6

32.7

33.5

34.2

33.5

Net Profit/ (Loss) after taxes

56

21

171.8

52

8.2

117

90

29.9

PAT %

10.2

5.6

9.1

7.8

7.4

Dil. EPS (after extra-ord. Items)

10.26

3.79

170.7

9.53

7.7

21.43

16.59

29.2

Source: Company, Angel Research; Note: nmf- Not meaningful

Standalone business performance

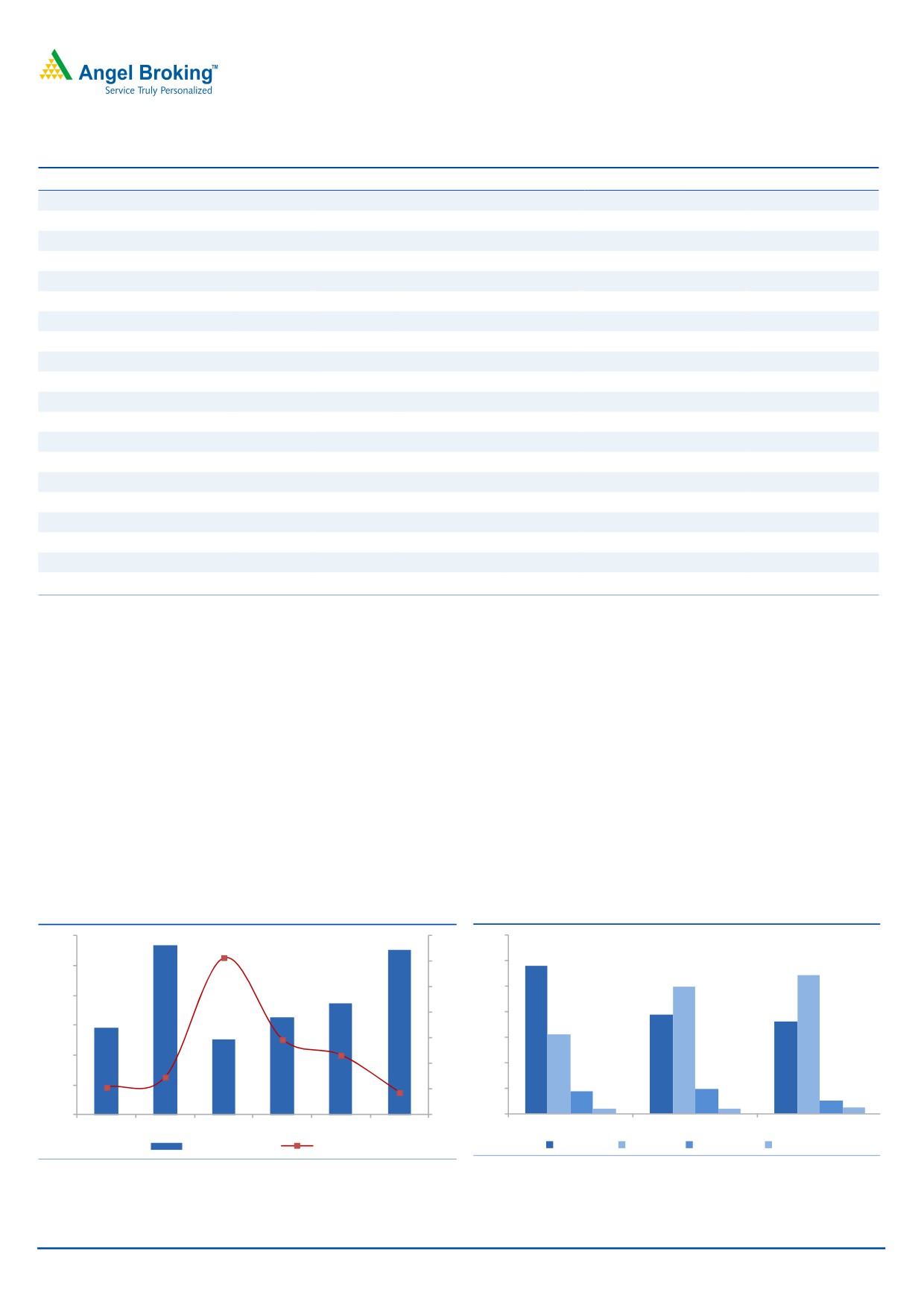

Revenues grow 26.6% yoy

Wabag reported 2.6% yoy decline in its revenues for the quarter to `553cr, which

is below our expectations. Decline in the yoy revenues is mainly attributable to (1)

39.3% yoy decline in EPC- Municipal segment business (36.2% of 4QFY2016

revenues) and (2) 46.1% yoy decline in O&M- Municipal segment business (5.0%

of 4QFY2016 revenues). The following 3 projects contributed 29.8% to the

4QFY2016 standalone revenues, (1) APGENCO project (`117.5cr), (2) 147 MLD

WTP project at Habra, West Bengal (`29.2cr), and (3) 100 MLD Desal. plant-

O&M works at Nemmeli, Chennai (`18.1cr).

Exhibit 2: Revenues decline 2.6% yoy

Exhibit 3: EPC-Industrial contributes highest share

600

120

70

568

553

58.1

100

60

54.4

500

102.8

49.8

80

50

371

400

325

38.9

60

40

36.2

293

300

254

31.0

40

30

200

38.8

20

20

26.6

8.9

9.6

100

0

10

5.0

9.5

1.9

1.7

2.5

1.5

(2.6)

0

(20)

0

3QFY2015 4QFY2015 1QFY2016 2QFY2016 3QFY2016 4QFY2016

4QFY2015

3QFY2016

4QFY2016

Revenues (` cr)

yoy growth (%)

EPC- Mun.

EPC- Ind.

O&M- Mun.

O&M- Ind.

Source: Company, Angel Research

Source: Company, Angel Research

June 1, 2016

2

VA Tech Wabag | 4QFY2016 Result Update

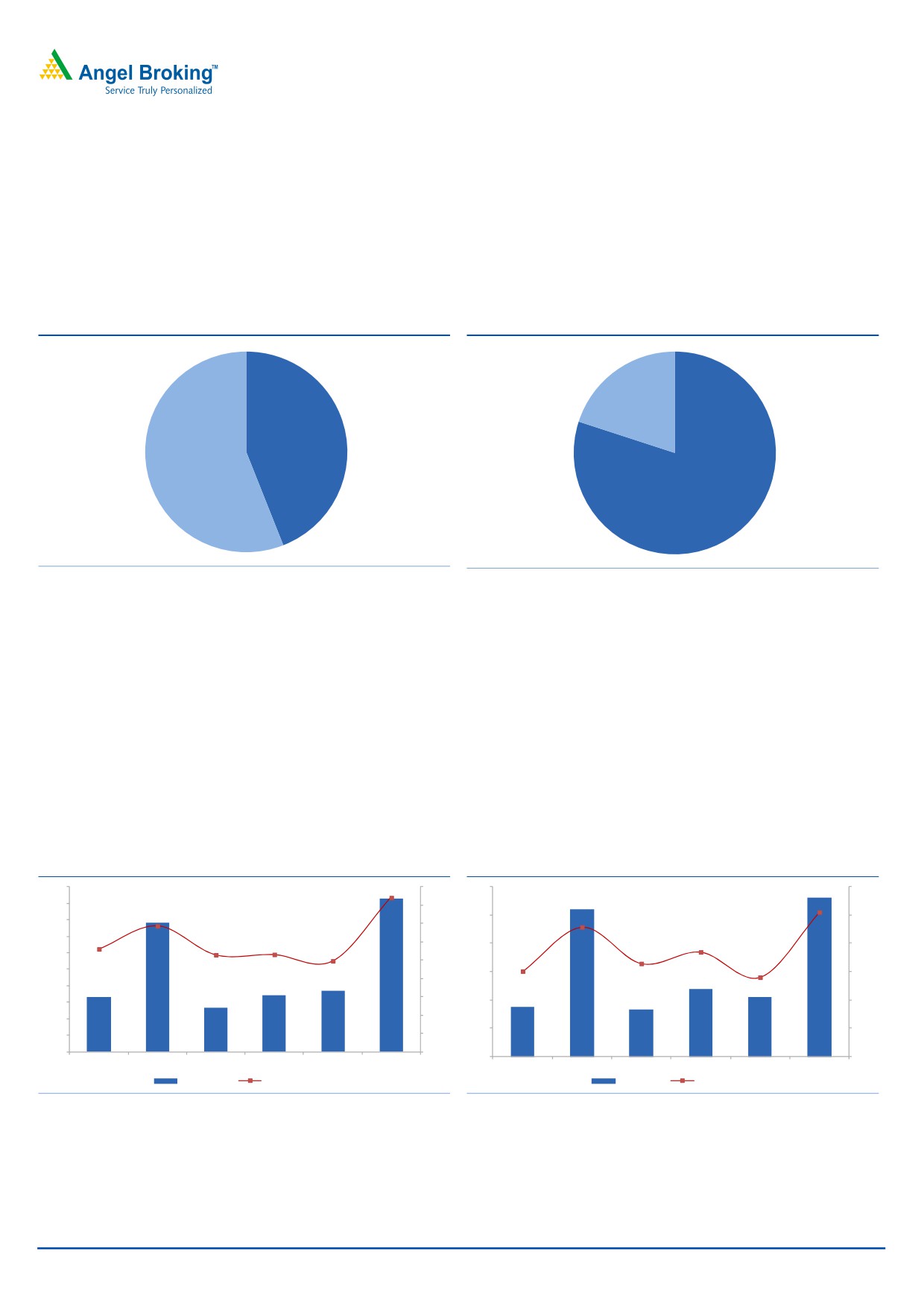

For the full year, Wabag reported 23.2% yoy increase in revenues led by strong

revenue booking seen across the (1) APGENCO project (`398.3cr), (2) 147 MLD

WTP project at Habra, West Bengal (`86.4cr), and (3) 100 MLD Desal. plant-

O&M works at Nemmeli, Chennai (`63.8cr). If we look at the business segments,

then the Industrial EPC segment (31.2% of FY2016 revenues) reported a 135.0%

yoy increase in revenues.

Exhibit 4: Business-wise FY2016 Revenue split

Exhibit 5: Vertical-wise FY2016 Revenue split

O&M, 20.0

Municipal,

44.0

Industrial,

56.0

EPC, 80.0

Source: Company, Angel Research

Source: Company, Angel Research

EBITDA margin expands yoy to 16.8%

Wabag reported 19.2% yoy increase in EBITDA to `93cr, while EBITDA margin

expanded 306bp yoy to 16.8% in 4QFY2016. EBITDA margin expansion was

restricted on account of 22.5% increase in employee expenses. Such increase in

employee expenses is attributable to incentive payments made to employees for

FY2015 and FY2016. On normalizing the impact of such incentive payments,

employee expenses would have remained flat on a yoy basis.

For FY2016, EBITDA margins expanded 186bp yoy to 13.0%, benefitting from

4.5% decline in other expenses to `59cr.

Exhibit 6: EBITDA margins expand yoy to 16.8%

Exhibit 7: PAT margins also expand to 10.2%

100

18.0

60

12.0

90

16.0

16.8

50

10.0

80

14.0

10.2

70

13.7

9.1

12.0

40

8.0

60

11.2

10.0

7.4

50

10.6

10.6

9.9

30

6.0

8.0

6.6

40

6.0

5.6

30

6.0

20

4.0

20

4.0

10

2.0

10

2.0

33

78

27

34

37

93

18

52

17

24

21

56

0

0.0

0

0.0

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

EBITDA (` cr)

EBITDA margin (%)

PAT (` cr)

PAT Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

PAT margin expand yoy to 10.2%

In-line with the EBITDA margin, PAT margins expanded from 9.1% in 4QFY2015

to 10.2% in 4QFY2016. EBITDA margin expansion coupled with 10.0% yoy decline

in depreciation expenses (to `3cr) led to PAT margin expansion.

June 1, 2016

3

VA Tech Wabag | 4QFY2016 Result Update

For FY2016, Wabag reported 40bp yoy PAT margin expansion to 7.8%. Entire

benefits of yoy EBITDA margin expansion have not flown down to the PAT level, as

(1) interest expenses increased sharply to `15cr, and (2) tax rate increased from to

34.2% in FY2016 from 33.5% in FY2015.

Update on Subsidiaries’ performance

The company’s international subsidiaries’ revenues declined 10.4% on a yoy basis

to `303cr, which is attributable to

(1)

7% Euro depreciation, (2) some of the

projects being at early stages of execution and not contributing to revenues, and

(3) delays in the Egyptian and Saudi Arabian projects (mainly owing to engineering

issues; expected to start contributing to revenues in the next 2 quarters). If we look

at 4QFY2016 revenue composition from international subsidiaries, then

(1)

Petronas, Malaysia contributed

`82.3cr,

(2) DAWASA, Tanzania contributed

`39.4cr, and (3) O&M, Istanbul project contributed `37.0cr. Notably, EPC-

Municipal segment reported 4.1% yoy decline in revenues to `182.1cr (60.1% of

4QFY2016 revenues).

For FY2016, subsidiaries reported 14.0% yoy revenue decline to `1,039cr, as

there were delays in international projects on account of engineering issues.

The EBITDA margins of the international business declined yoy owing to 13.6% increase

in employee expenses. Other expenses during the quarter declined as no more

provisions related to the Gubrah project were made (as had been made in the earlier

quarters). A poor operating performance coupled with higher tax rate led to losses at the

international business.

For FY2016, the EBITDA declined owing to higher other expenses. A poor

operating performance, higher interest expenses coupled with higher tax expenses

led to higher losses in FY2016.

June 1, 2016

4

VA Tech Wabag | 4QFY2016 Result Update

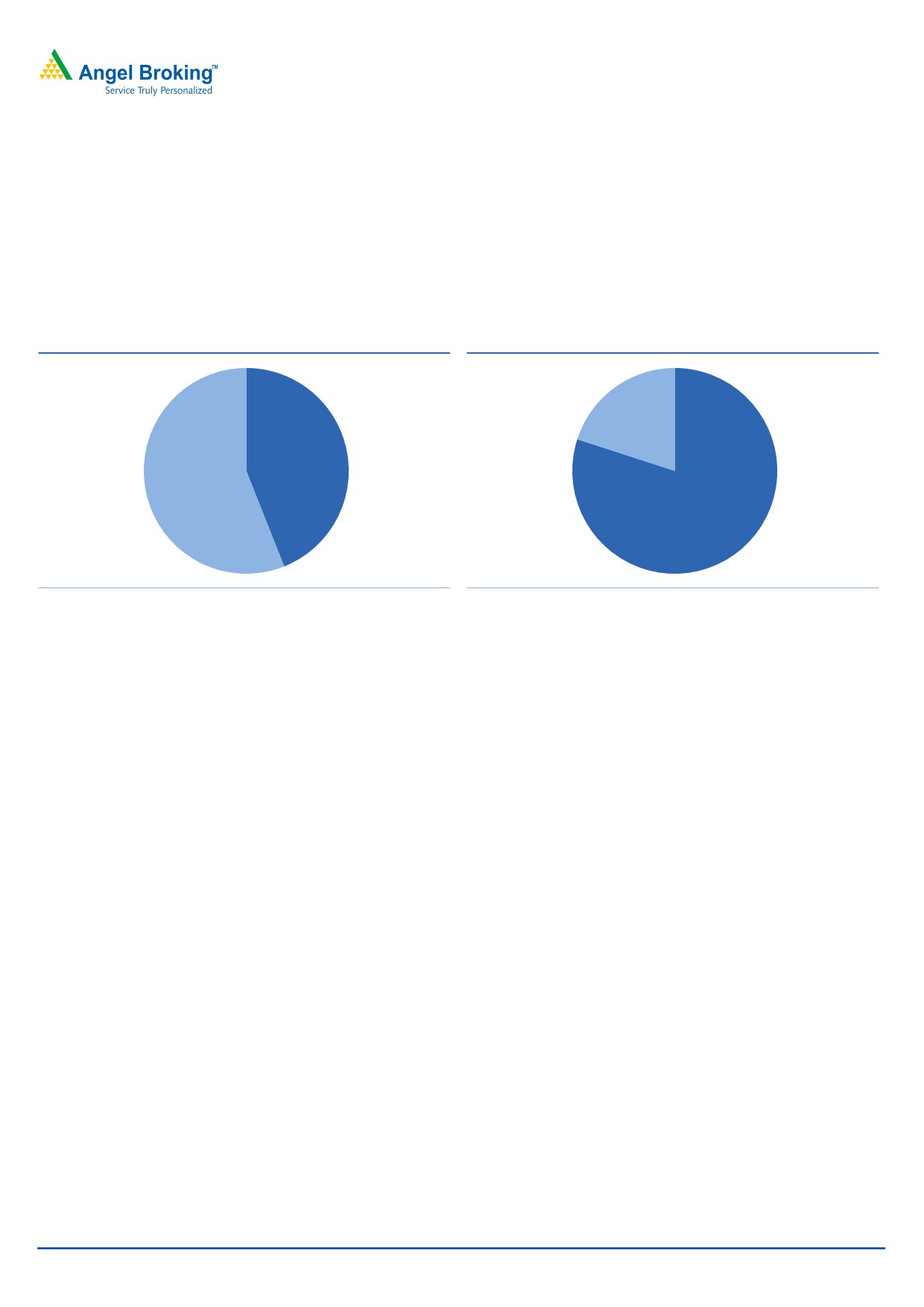

`1,784cr of Order Inflows in 4QFY2016

Wabag reported `1,784cr of order wins in 4QFY2016, which is up 17.2% yoy. The

company reported key order wins from Polgahawela WTP (`734cr) and Chennai

TTP (`594cr). The company has already won `500cr of projects year-to-date

FY2017 (waste water treatment project at Nepal, Reliance waste water treatment

plant at Jamnagar, and Czech waste water treatment plant). For FY2016 Wabag

reported highest ever yearly order inflows of `5,140cr.

Exhibit 8: Business-wise FY2016 Order Inflows split

Exhibit 9: Vertical-wise FY2016 Order Inflows split

O&M, 20.0

Municipal,

44.0

Industrial,

56.0

EPC, 80.0

Source: Company, Angel Research

Source: Company, Angel Research

Order book as of 4QFY2016-end stood at `8,315cr, reflecting Order book / last

twelve month (LTM) sales ratio of 3.3x.

Management Guidance & Concall Updates

For FY2017, the company’s Management maintained its order inflow guidance of

`4,000-4,200cr (down 18-22% to reported order inflows of FY2016).

Wabag’s Management has given a revenue guidance of `3,000-3,200cr for

FY2017E (up 18-26% from FY2016 reported revenues).

The Management highlighted that it expects to see reasonable improvement in the

FY2017 EBITDA margins from the 8.6% levels reported in FY2016.

Update on some of the projects: (1) Basic engineering works have been approved

at Bahrain Suez project. Civil works have already started. Ordering of the key

equipments is at advanced stages. (2) The Dangote project is at final stages of

engineering and major dispatches are expected to be done in FY2017E. (3) Oman

desalinization plant has been handed over to the client. For past 30 continuous

days, trial/reliability runs are ongoing. Arbitration discussions are ongoing, which

are expected to complete in the next 1 quarter. (4) For AP Genco project, boiler

testing is done, turbine generator is erected, conveyor handling systems have been

started, and the company is on track to finish the project in FY2017. Currently no

profits are being taken up from the project; post hand-over, once no risks are

attached, then profits would be taken up.

June 1, 2016

5

VA Tech Wabag | 4QFY2016 Result Update

Investment arguments

Strong market positioning: Wabag in our view has a strong portfolio of offerings in

the water treatment/ waste water/ desalination space. Unlike most of the domestic

EPC players, Wabag has a differentiated business model, given its in-house

technology. Strong technological know-how coupled with large talent positions it to

successfully execute complex water projects.

Asset-light business model drives RoEs: Wabag pursues an asset-light business

model. Its strategy of keeping core areas of work in-house and outsourcing the

non-critical, low-value work helps it maintain high RoEs. Also, it takes on large

volume projects, thereby enabling it to generate high RoEs.

India & Emerging markets hold huge opportunity: India has low per capita water

supply vis-a-vis developed nations, indicating huge growth potential for the

company’s business. Also, with rising stringency in norms for waste water

treatment, scope for Wabag is huge, given that ~30% of industrial waste water is

not treated. Wabag has made strong in-roads in emerging markets like

Philippines, China, Saudi Arabia, Egypt, Spain and Turkey.

Risks & Concerns

Delays in revival of international business could impact our margin

assumptions.

Any significant loss of market share could be a risk to our assumptions.

Execution delays in the domestic markets could be a risk to our assumptions.

Valuation

At CMP of `675, VA Tech Wabag stock trades at FY2017E/2018E P/E multiple of

22.1x/16.0x. Recently Wabag reported large ticket order wins from the Middle

East and Asian sub-continent (worth `2,862cr), which tend to have a better margin

profile than orders executed in Europe. These order wins have now taken the order

book to the highs of `8,315cr, reflecting OB/LTM ratio at 3.3x. With better revenue

visibility, declining contribution of low margin projects, we now expect VA Tech

Wabag to report 23.0% top-line and 45.6% bottom-line CAGR during FY2016-

18E, respectively. On the back of such strong earnings growth, we expect the RoEs

of the company to expand from 9.7% in FY2016 to 15.9% in FY2018E. Given the

strong earnings growth and RoE expansion potential, we assign 19.0x P/E multiple

to our FY2018E EPS of `35.9 to arrive at a price target of `681. Given the 18.5%

upside, we upgrade our recommendation on the stock to BUY.

June 1, 2016

6

VA Tech Wabag | 4QFY2016 Result Update

Company background

VA Tech Wabag is a multinational player in the water treatment industry with

presence across India, Middle East, North Africa, Central and Eastern Europe,

China and South East Asia. Wabag offers an entire range of solutions including

conceptualisation, design, engineering, procurement, supply, installation,

construction and O&M (operational and maintenance) services. The company also

provides range of EPC and O&M solutions for sewage treatment, processed &

drinking water treatment, effluents treatment, sludge treatment, desalination and

reuse for institutional clients like municipal corporations and companies in the

infrastructure sector.

June 1, 2016

7

VA Tech Wabag | 4QFY2016 Result Update

Profit & Loss (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

Net Sales

1,619

2,239

2,435

2,542

3,136

3,845

% Chg

12.1

38.3

8.8

4.4

23.3

22.6

Total Expenditure

1,464

2,050

2,226

2,324

2,858

3,493

Cost of sales & services

1,165

1,689

1,848

2,038

2,355

2,919

Changes in inventory

10

9

(15)

(49)

8

(9)

Employee benefits Expense

209

222

278

218

346

418

Other Expenses

80

130

115

117

149

165

EBITDA

155

189

209

218

278

352

% Chg

19.1

21.7

11.1

4.1

27.3

26.7

EBIDTA %

9.6

8.4

8.6

8.6

8.9

9.1

Depreciation

11

15

11

21

23

26

EBIT

144

173

199

198

254

326

% Chg

18.5

20.5

14.4

(0.5)

28.7

28.1

Interest and Financial Charges

22

25

39

42

49

42

Other Income

13

13

8

7

7

9

EBT & exceptional items

135

161

167

162

213

293

Exceptional Items

0

5

0

0

0

0

EBT

135

166

167

162

213

293

Tax Expenses

46

53

57

69

71

98

% of PBT

33.7

32.6

33.9

42.6

33.3

33.3

EAT before share of Profit in asso.

90

114

110

93

142

196

Share of profit in Associate

1

1

2

1

2

2

PAT before Minority Interest

90

114

112

94

144

197

Minority Interest

0

1

2

2

2

2

PAT

90

113

110

92

142

195

% Chg

22.5

25.5

(2.9)

(16.3)

53.9

37.7

PAT %

5.6

5.1

4.5

3.6

4.5

5.1

Diluted EPS

33.8

42.1

20.2

16.9

26.0

35.9

% Chg

21.2

24.8

(52.1)

(16.3)

53.9

37.7

June 1, 2016

8

VA Tech Wabag | 4QFY2016 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16E FY17E FY18E

Sources of Funds

Equity Capital

5

5

11

11

11

11

Reserves & Surplus

710

836

892

981

1,123

1,318

Networth

715

841

903

992

1,134

1,329

Total Debt

82

158

181

377

342

315

Minority Interest & Share

2

3

5

8

10

12

appl. pending allot.

Other Long-term Liabilities & Prov.

112

182

242

172

275

295

Total Liabilities

912

1,185

1,331

1,550

1,761

1,951

Application of Funds

Gross Block

107

175

252

259

284

315

Accumulated Depreciation

56

56

61

81

105

131

Net Block

51

119

191

178

180

185

Cap. WIP & Intan.

48

69

1

0

0

0

Assets underDevelop.

Investments

3

23

38

28

28

28

Current Assets

Inventories

41

35

47

98

69

74

Sundry Debtors

1,109

1,387

1,481

1,768

1,976

2,412

Cash and Bank Balance

287

370

311

358

628

690

Loans & Advances

116

100

116

125

129

127

Other Current Asset

225

320

361

444

375

395

Current Liabilities

979

1,251

1,237

1,457

1,658

2,002

Net Current Assets

798

962

1,078

1,336

1,519

1,697

Other Assets

11

11

23

8

35

42

Total Assets

912

1,185

1,331

1,550

1,761

1,951

June 1, 2016

9

VA Tech Wabag | 4QFY2016 Result Update

Cash Flow Statement

Y/E March (` cr)

FY13

FY14

FY15

FY16E FY17E FY18E

Profit before tax

135

161

167

162

213

293

Depreciation & Other Non-cash Chrg.

89

85

135

132

136

87

Change in Working Capital

(115)

(84)

(257)

(321)

87

(116)

Interest & Financial Charges

7

7

15

15

17

15

Direct taxes paid

(34)

(57)

(55)

(69)

(71)

(98)

Cash Flow from Operations

82

112

6

(82)

382

181

(Inc)/ Dec in Fixed Assets

(41)

(103)

(28)

(7)

(25)

(31)

(Inc)/ Dec in Investments & Oth. Adj.

1

5

(39)

0

0

0

Cash Flow from Investing

(40)

(97)

(68)

(7)

(25)

(31)

Issue/ (Buy Back) of Equity

3

1

20

0

0

0

Inc./ (Dec.) in Borrowings

(43)

76

22

197

(35)

(27)

Dividend Paid (Incl. Tax)

(19)

(22)

(25)

(22)

(33)

(46)

Interest Expenses & Oth. Adj.

(7)

(8)

(15)

(15)

(17)

(15)

Cash Flow from Financing

(65)

48

2

160

(85)

(88)

Inc./(Dec.) in Cash & forex translation

(21)

86

(91)

72

272

62

Opening Cash balances

265

244

330

240

312

583

Closing Cash balances

244

330

240

312

583

645

June 1, 2016

10

VA Tech Wabag | 4QFY2016 Result Update

Ratio Analysis (x)

Y/E March

FY13

FY14

FY15

FY16E FY17E FY18E

Valuation Ratio (x)

Adj. P/E (on FDEPS)

17.0

13.6

28.5

34.0

22.1

16.0

Adj. P/CEPS

15.1

11.9

25.8

27.8

19.0

14.2

Dividend yield (%)

1.0

1.2

0.7

0.7

0.9

1.1

EV/Sales

0.8

0.6

1.2

1.2

0.9

0.7

EV/EBITDA

8.5

7.0

14.3

14.5

10.3

7.8

EV / Total Assets

1.5

1.1

2.2

2.0

1.6

1.4

Per Share Data (`)

Adj. EPS (fully diluted)

33.8

42.1

20.2

16.9

26.0

35.9

Cash EPS

38.1

48.3

22.3

20.7

30.3

40.6

DPS

6.0

7.0

4.0

3.9

4.9

6.2

Book Value

269

316

166

182

208

244

Returns (%)

RoCE (Pre-tax)

20.1

20.6

22.0

19.9

22.4

24.5

Angel RoIC (Pre-tax)

14.1

13.3

12.0

10.0

11.7

14.5

RoE

12.6

14.6

12.6

9.7

13.4

15.9

Turnover ratios (x)

Asset Turnover (Gross Block) (x)

1.8

1.9

1.8

1.6

1.8

2.0

Inventory / Sales (days)

9

6

7

8

8

7

Receivables (days)

250

226

222

228

230

229

Payables (days)

221

204

185

195

193

190

WC (days)

39

28

44

41

45

46

Leverage Ratios (x)

D/E ratio (x)

0.1

0.2

0.2

0.4

0.3

0.2

Note: nmf- Not Meaningful

June 1, 2016

11

VA Tech Wabag | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

VA Tech Wabag

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

June 1, 2016

12