3QFY2016 Result Update | Capital Goods

March 18, 2016

VA Tech Wabag

NEUTRAL

CMP

`509

Performance Highlights

Target Price

-

Quarterly highlights - Standalone

Investment Period

-

Y/E March (` cr)

3QFY16 3QFY15 2QFY16

% chg (yoy)

% chg (qoq)

Stock Info

Net sales

371

293

325

26.6

14.4

Sector

Capital Goods

EBITDA

37

33

34

11.7

6.4

Market Cap (` cr)

2,771

Reported PAT

21

18

24

17.0

(13.4)

Net debt (` cr)

(131)

Source: Company, Angel Research;

Beta

1.1

VaTech Wabag (Wabag) reported a 26.6% yoy increase in sales to `371cr in

52 Week High / Low

957/409

3QFY2016, reflecting strong execution across its AP Genco project. The EBITDA

Avg. Daily Volume

141,944

for the quarter grew 11.7% yoy to `37cr. The EBITDA margin declined 132bp yoy

Face Value (`)

2

to 9.9%, owing to a sharp increase in other expenses to `22cr (vs `5cr in

BSE Sensex

24,953

3QFY2015). In-line with the EBITDA margin, the PAT margin declined from 6.0%

Nifty

7,604

in the corresponding quarter of the previous year to 5.6% in 3QFY2016.

Reuters Code

VATE.BO

International revenues declined 20.8% yoy to `258cr, on account of (1) Euro

Bloomberg Code

VATW@IN

depreciation, (2) some of the projects being at early stages of execution and not

contributing to revenues (inclusive of Nepal based projects), and (3) lower

Shareholding Pattern (%)

revenue from Al Gubrah project (nearing completion). A poor operating

Promoters

29.0

performance coupled with higher interest expenses (at `5.5cr) led to international

MF / Banks / Indian Fls

25.0

business losses.

FII / NRIs / OCBs

27.4

The order book as of 3QFY2016-end stood at `7,952cr, reflecting Order book /

Indian Public / Others

18.7

last twelve month (LTM) sales ratio of 3.1x.

Valuation: The stock trades at FY2017E/2018E P/E multiple of 26.1x/20.7x,

Abs. (%)

3m 1yr 3yr

which continues to be at the higher end of the historical band. On considering

Sensex

(3.0)

(44.2)

145.0

the 25% correction in the stock price in the last 3 months period, valuations in

Wabag

(25.8)

(12.4)

34.3

our view still do not factor in the muted order inflow environment, modest

earnings growth, and stretched working capital cycle. We assign a 20.0x P/E

multiple to our FY2017E EPS of `25 to arrive at a price target of `492. Given the

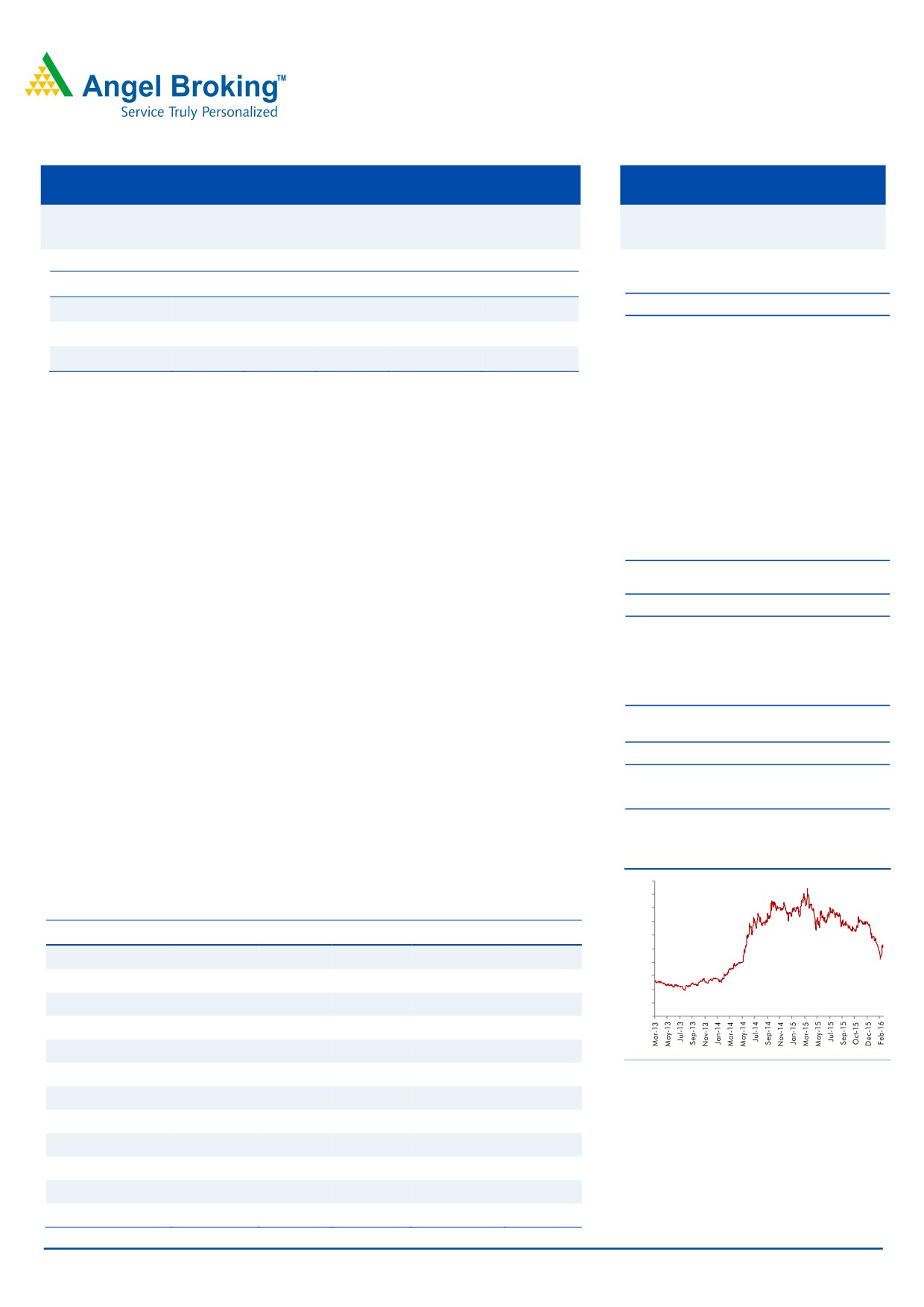

3-Year Daily Price Chart

limited upside potential, we recommend a Neutral rating on the stock.

1000

900

800

Key financials (Standalone)

700

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

600

500

Net Sales

1,619

2,239

2,435

2,722

3,336

400

300

% chg

12.1

38.3

8.8

11.8

22.5

200

100

Net Profit

90

114

112

107

135

0

% chg

22.5

25.5

(2.9)

(3.8)

26.2

EBITDA (%)

9.6

8.4

8.6

7.9

8.1

EPS (`)

34

42

20

20

25

Source: Company, Angel Research

P/E (x)

15.1

12.1

25.2

26.1

20.7

P/BV (x)

1.9

1.6

3.1

2.7

2.4

RoE (%)

12.6

14.6

12.6

11.1

12.4

RoCE (%)

20.1

20.6

22.0

19.5

21.3

Yellapu Santosh

EV/Sales (x)

0.7

0.5

1.1

0.9

0.8

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

7.4

6.1

12.6

11.8

9.3

Source: Company, Angel Research; CMP as of March 18, 2016

Please refer to important disclosures at the end of this report

1

VA Tech Wabag | 3QFY2016 Result Update

Exhibit 1: Quarterly Performance (Standalone)

Particulars (` cr)

3QFY16

2QFY16

% chg (qoq) 3QFY15

% chg (yoy)

9mFY16

9mFY15

% chg

Net Sales

371

325

14.4

293

26.6

950

652

45.6

Total Expenditure

335

290

15.4

261

28.4

852

591

44.1

Cost of materials consumed

311

251

23.7

234

32.7

766

536

42.9

Change in Inventories

(22)

11

(298.7)

4

(722.3)

(38)

(46)

(16.2)

Employee benefits Expense

23

21

9.9

18

29.1

70

61

14.9

Other Expenses

22

7

231.3

5

368.3

54

40

35.9

EBITDA

37

34

6.4

33

11.7

98

61

59.7

EBIDTA %

9.9

10.6

11.2

10.3

9.4

Depreciation

3

3

(3.3)

3

(9.5)

9

4

119.3

EBIT

34

31

7.4

30

14.0

89

57

55.4

Interest and Financial Charges

5

3

38.1

2

nmf

9

5

71.6

Other Income & forex (gain)/loss

2

8

(80.0)

(1)

(327.0)

13

6

113.3

PBT before Exceptional Items

31

36

(15.6)

27

15.6

93

58

60.0

Exceptional Items

0

0

nmf

0

nmf

0

0

nmf

PBT after Exceptional Items

31

36

(15.6)

27

15.6

93

58

60.0

Tax

10

13

(20.0)

9

12.9

31

19

61.7

% of PBT

32.7

34.5

(5.1)

33.5

(2.4)

33.9

33.5

1.1

Net Profit/ (Loss) after taxes

21

24

(13.4)

18

17.0

61

38

59.1

PAT %

5.6

7.4

(24.3)

6.0

(7.5)

6.4

5.9

9.3

Dil. EPS (after extra-ord. Items)

3.79

4.38

(13.5)

3.26

16.3

11.23

7.10

58.2

Source: Company, Angel Research; Note: nmf- Not meaningful

Revenues grow 26.6% yoy

VaTech Wabag reported a 26.6% yoy increase in sales to `371cr in 3QFY2016.

Revenue growth was mainly on account of strong execution seen across the AP

Genco project (has contributed `280cr to the top-line for 9MFY2016).

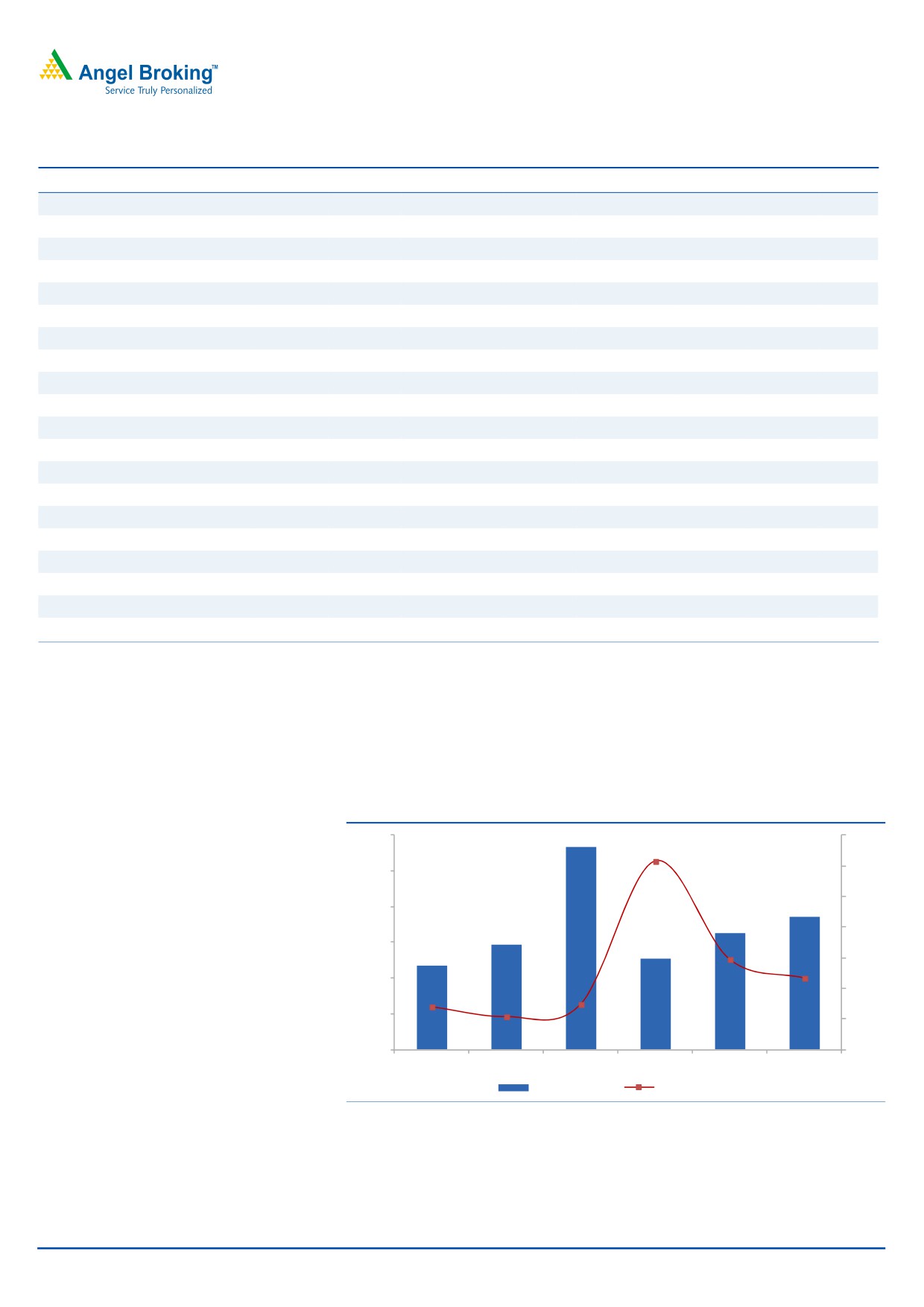

Exhibit 2: Quarterly revenue trend

600

568

120

100

500

102.8

80

400

371

325

60

293

300

254

234

40

200

38.8

20

26.6

100

9.5

0

7.9

1.5

0

-20

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

Revenues (` cr)

yoy growth (%)

Source: Company, Angel Research

February 18, 2015

2

VA Tech Wabag | 3QFY2016 Result Update

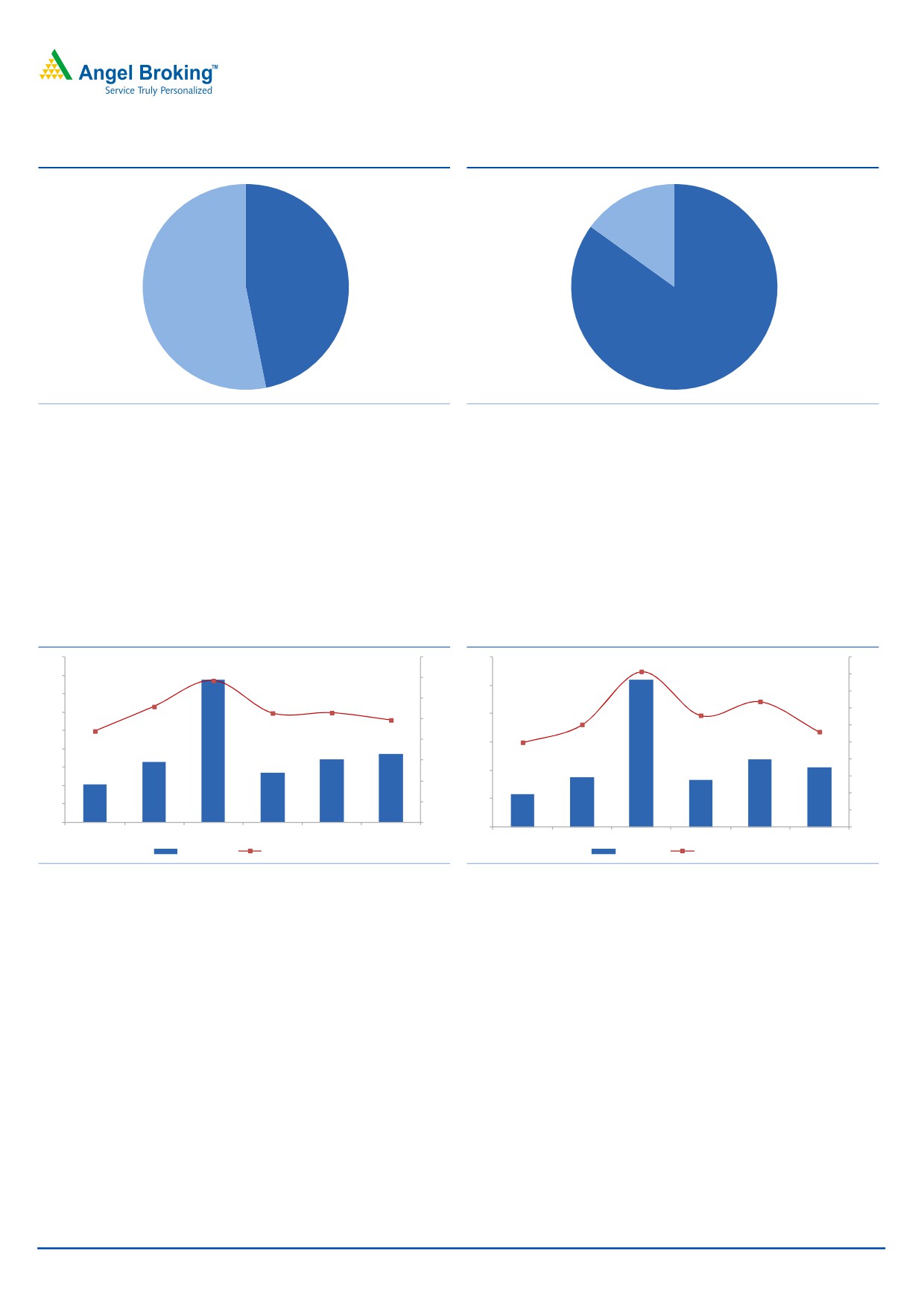

Exhibit 3: Business-wise 9MFY2016 Revenue split

Exhibit 4: Vertical-wise 9MFY2016 Revenue split

O&M, 15.1

Municipal,

46.8

Industrial,

53.2

EPC, 84.9

Source: Company, Angel Research

Source: Company, Angel Research

EBITDA margin declines yoy

Wabag reported an 11.7% yoy increase in EBITDA to `37cr while the EBITDA

margin declined 132bp yoy to 9.9%, in 3QFY2016. The compression in the

EBITDA margin is owing to a sharp increase in other expenses to `22cr (vs `5cr in

3QFY2015). Such increase in other expenses is attributable to higher doubtful

debts provisioning of `12cr, which is in-line with the company’s internal policy of

ageing debtors.

Exhibit 5: EBITDA margins compress yoy

Exhibit 6: PAT margins also decline...

90

16.0

60

10.0

80

14.0

9.0

50

9.1

70

13.7

8.0

12.0

60

7.0

40

7.4

11.2

10.0

10.6

10.6

6.6

6.0

50

9.9

8.0

6.0

8.8

30

5.6

5.0

40

5.0

6.0

4.0

30

20

3.0

4.0

20

2.0

2.0

10

10

21

33

78

27

34

37

1.0

12

18

52

17

24

21

0

0.0

0

0.0

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

EBITDA (` cr)

EBITDA margin (%)

PAT (` cr)

PAT Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

PAT margin down yoy

In-line with the EBITDA margin, the PAT margin declined from 6.0% in 3QFY2015

to 5.6% in 3QFY2016. This is in spite of a 9.5% decline in yoy depreciation

expenses (to `3cr) and a lower tax rate (at 32.7%).

February 18, 2015

3

VA Tech Wabag | 3QFY2016 Result Update

Update on subsidiaries’ performance

The company’s International subsidiaries’ revenues declined 20.8% on a yoy basis

to `258cr which is attributable to (1) Euro depreciation (over 10%), and (2) some

of the projects being at early stages of execution and not contributing to revenues

(inclusive of Nepal based projects), and (3) lower revenue booking from Al Gubrah

project (is nearing completion).

A poor operating performance coupled with higher interest expenses (at `5.5cr) led to

international business losses. Surge in yoy interest expenses is on account of Ujams

BOOT project, Namibia.

`276cr of Order Inflows in 3QFY2016

Wabag reported `276cr of order wins in 3QFY2016, which is down 59% yoy.

Wabag reported a key order win from Sanliurfa WWTP, Turkey. The Management

attributed client side delays on project finalization in domestic markets as the

key reason for decline in yoy order inflows. For 9MFY2016 Wabag reported

~130% yoy increase in order inflows to `3,356cr.

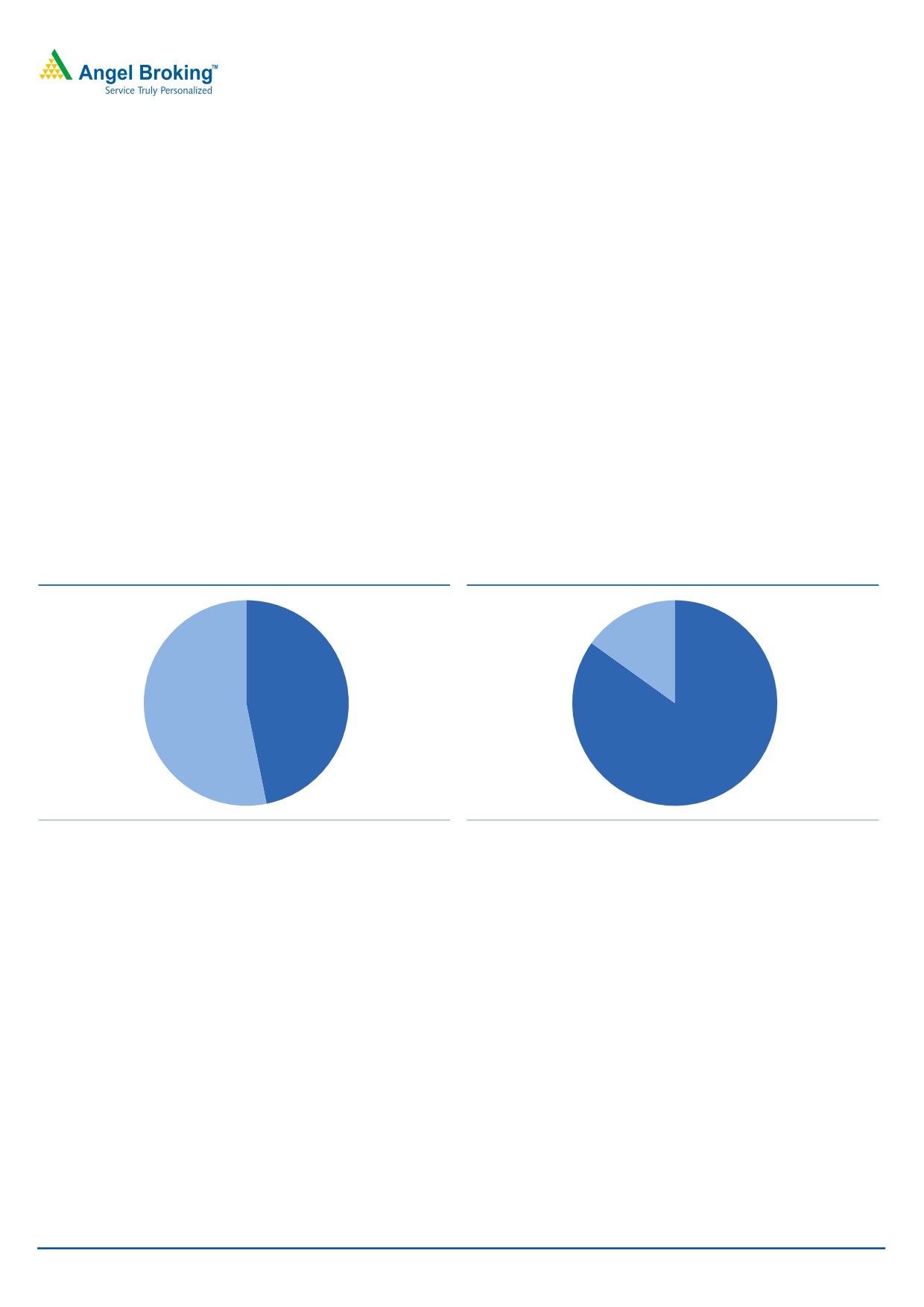

Exhibit 7: Business-wise 9MFY2016 Order Inflows split

Exhibit 8: Vertical-wise 9MFY2016 Order Inflows split

O&M, 15.1

Municipal,

46.8

Industrial,

53.2

EPC, 84.9

Source: Company, Angel Research

Source: Company, Angel Research

Order book as of 3QFY2016-end stood at `7,952cr, reflecting Order book / last

twelve month (LTM) sales ratio of 3.1x.

Management Guidance & Concall Updates

For FY2016, the company’s Management maintained its order inflow guidance of

`3,500-3,700cr (up 18-24% yoy). Considering Wabag having won `680cr of

Polghawella Water Supply scheme in Sri Lanka in 4QFY2016, and with `3,356cr

of order inflows for 9MFY2016, we believe that the company has a fair chance to

attain its order inflow guidance for FY2016.

Wabag’s Management has given a revenue guidance of `2,800-3,000cr (up 15-

24%) for FY2016.

The Management highlighted that it expects to maintain FY2016 EBITDA margins

on the lines of ~8.7%, as reported in FY2015. This in our view is a challenging

task, given that Wabag will have to report 12.6% margin in 4QFY2016 vs 5.9%

reported in 9MFY2016.

February 18, 2015

4

VA Tech Wabag | 3QFY2016 Result Update

Investment arguments

Strong market positioning: Wabag in our view has a strong portfolio of offerings in

the water treatment/ waste water/ desalination space. Unlike most of the domestic

EPC players, Wabag has a differentiated business model, given its in-house

technology. Strong technological know-how, coupled with large talent positions it

to successfully execute complex water projects.

Asset-light business model drives RoEs: Wabag pursues an asset-light business

model. Its strategy of keeping core areas of work in-house and outsourcing the

non-critical, low-value work helps it maintain high RoEs. Also, it takes on large

volume projects, thereby enabling it to generate high RoEs.

India & Emerging markets hold huge opportunity: India has low per capita water

supply vis-a-vis developed nations, indicating huge growth potential for the

company’s business. Also, with rising stringency in norms for waste water

treatment, scope for Wabag is huge, given that ~30% of industrial waste water is

not treated. Wabag has made strong in-roads in emerging markets like

Philippines, China, Saudi Arabia, Egypt, Spain and Turkey.

Risks & Concerns

Delays in revival of international business could impact our margin

assumptions.

Any significant loss of market share could be a risk to our assumptions.

Execution delays in the domestic markets could be a risk to our assumptions.

Valuation

The stock trades at FY2017E/2018E P/E multiple of 26.1x/20.7x, which continues

to be at the higher end of the historical band. On considering the 25% correction

in the stock price in the last 3 months period, valuations in our view still do not

factor in the muted order inflow environment, modest earnings growth, and

stretched working capital cycle. We assign a 20.0x P/E multiple to our FY2017E

EPS of `25 to arrive at a price target of `492. Given the limited upside potential,

we recommend Neutral rating on the stock.

February 18, 2015

5

VA Tech Wabag | 3QFY2016 Result Update

Company background

VA Tech Wabag is a multinational player in the water treatment industry with

presence across India, Middle East, North Africa, Central and Eastern Europe,

China and South East Asia. Wabag offers an entire range of solutions including

conceptualisation, design, engineering, procurement, supply, installation,

construction and O&M (operational and maintenance) services. The company also

provides range of EPC and O&M solutions for sewage treatment, processed &

drinking water treatment, effluents treatment, sludge treatment, desalination and

reuse for institutional clients like municipal corporations and companies in the

infrastructure sector.

February 18, 2015

6

VA Tech Wabag | 3QFY2016 Result Update

Profit and Loss Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Net Sales

1,619

2,239

2,435

2,722

3,336

% Chg

12.1

38.3

8.8

11.8

22.5

Total Expenditure

1,464

2,050

2,226

2,506

3,066

Cost of sales & services

1,165

1,689

1,848

2,067

2,550

Changes in inventory

10

9

(15)

11

8

Employee benefits Expense

209

222

278

304

366

Other Expenses

80

130

115

123

142

EBITDA

155

189

209

216

270

% Chg

19.1

21.7

11.1

3.3

24.6

EBIDTA %

9.6

8.4

8.6

7.9

8.1

Depreciation

11

15

11

20

26

EBIT

144

173

199

197

243

% Chg

18.5

20.5

14.4

(1.0)

23.8

Interest and Financial Charges

22

25

39

45

50

Other Income

13

13

8

7

7

EBT & exceptional items

135

161

167

159

200

Exceptional Items

0

5

0

0

0

EBT

135

166

167

159

200

Tax Expenses

46

53

57

53

67

% of PBT

33.7

32.6

33.9

33.3

33.3

EAT before share of Profit in asso.

90

114

110

106

134

Share of profit in Associate

1

1

2

2

2

PAT before Minority Interest

90

114

112

107

135

Minority Interest

0

1

2

2

2

PAT

90

113

110

106

134

% Chg

22.5

25.5

(2.9)

(3.8)

26.2

PAT %

5.6

5.1

4.5

3.9

4.0

Diluted EPS

33.8

42.1

20.2

19.5

24.6

% Chg

21.2

24.8

(52.1)

(3.5)

26.2

February 18, 2015

7

VA Tech Wabag | 3QFY2016 Result Update

Balance Sheet (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Sources of Funds

Equity Capital

5

5

11

11

11

Reserves & Surplus

710

836

892

998

1,131

Networth

715

841

903

1,009

1,142

Total Debt

82

158

181

207

227

Minority Interest &

2

3

5

6

8

Share appl. pending allot.

Other Long-term Liabilities & Prov.

112

182

242

255

275

Total Liabilities

912

1,185

1,331

1,477

1,652

Application of Funds

Gross Block

107

175

252

277

302

Accumulated Depreciation

56

56

61

81

107

Net Block

51

119

191

197

195

Capital WIP & Intan.

48

69

1

0

0

Assets under Develop.

Investments

3

23

38

38

38

Current Assets

Inventories

41

35

47

60

73

Sundry Debtors

1,109

1,387

1,481

1,700

2,102

Cash and Bank Balance

287

370

311

414

469

Loans & Advances

116

100

116

125

129

Other Current Asset

225

320

361

370

375

Current Liabilities

979

1,251

1,237

1,454

1,764

Net Current Assets

798

962

1,078

1,215

1,384

Other Assets

11

11

23

28

35

Total Assets

912

1,185

1,331

1,477

1,652

February 18, 2015

8

VA Tech Wabag | 3QFY2016 Result Update

Cash Flow Statement

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Profit before tax

135

161

167

159

200

Depreciation & Other Non-cash Charges

89

85

135

80

72

Change in Working Capital

(115)

(84)

(257)

(34)

(114)

Interest & Financial Charges

7

7

15

16

17

Direct taxes paid

(34)

(57)

(55)

(53)

(67)

Cash Flow from Operations

82

112

6

168

109

(Inc)/ Dec in Fixed Assets

(41)

(103)

(28)

(24)

(25)

(Inc)/ Dec in Investments & Oth. Adj.

1

5

(39)

0

0

Cash Flow from Investing

(40)

(97)

(68)

(24)

(25)

Issue/ (Buy Back) of Equity

3

1

20

0

0

Inc./ (Dec.) in Borrowings

(43)

76

22

27

20

Dividend Paid (Incl. Tax)

(19)

(22)

(25)

(25)

(31)

Interest Expenses & Oth. Adj.

(7)

(8)

(15)

(16)

(17)

Cash Flow from Financing

(65)

48

2

(14)

(29)

Inc./(Dec.) in Cash & forex translation

(21)

86

(91)

130

55

Opening Cash balances

265

244

330

240

369

Closing Cash balances

244

330

240

369

424

February 18, 2015

9

VA Tech Wabag | 3QFY2016 Result Update

Ratio Analysis (x)

Y/E March

FY13

FY14

FY15

FY16E

FY17E

Valuation Ratio (x)

Adj. P/E (on FDEPS)

15.1

12.1

25.2

26.1

20.7

Adj. P/CEPS

13.3

10.5

22.8

22.0

17.2

Dividend yield (%)

1.2

1.4

0.8

0.8

1.0

EV/Sales

0.7

0.5

1.1

0.9

0.8

EV/EBITDA

7.4

6.1

12.6

11.8

9.3

EV / Total Assets

1.3

1.0

2.0

1.7

1.5

Per Share Data (`)

Adj. EPS (fully diluted)

33.8

42.1

20.2

19.5

24.6

Cash EPS

38.1

48.3

22.3

23.1

29.5

DPS

6.0

7.0

4.0

3.9

4.9

Book Value

269

316

166

186

210

Returns (%)

RoCE (Pre-tax)

20.1

20.6

22.0

19.5

21.3

Angel RoIC (Pre-tax)

14.1

13.3

12.0

10.3

11.7

RoE

12.6

14.6

12.6

11.1

12.4

Turnover ratios (x)

Asset Turnover (Gross Block) (x)

0.6

0.5

0.5

0.5

0.5

Inventory / Sales (days)

9

6

7

8

8

Receivables (days)

250

226

222

228

230

Payables (days)

221

204

185

195

193

WC (days)

39

28

44

41

45

Leverage Ratios (x)

D/E ratio (x)

0.1

0.2

0.2

0.2

0.2

February 18, 2015

10

VA Tech Wabag | 3QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

VA Tech Wabag

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

February 18, 2015

11