3QFY2016 Result Update | Agrichemical

February 3, 2016

United Phosphorus

BUY

CMP

`416

Performance Highlights

Target Price

`480

Y/E March (` cr)

3QFY2016 2QFY2016

% chg (qoq) 3QFY2015

% chg (yoy)

Investment Period

12 Months

Net sales

3,050

2729

11.8

3010

1.3

Other income

131

51

155.2

51

157.1

Stock Info

Gross profit

1652

1362

21.4

1469

12.5

Sector

Agrichemical

Operating profit

579

450

28.5

538

7.5

Market Cap (` cr)

17,811

Adj. net profit

306

190

60.7

264

15.9

Source: Company, Angel Research

Net Debt (` cr)

1,113

Beta

1.1

For 3QFY2016, United Phosphorus (UPL) posted sales of `3,050cr, a yoy growth of

52 Week High / Low

576/359

1.3%. Overall, growth was driven by price and volume growth of 3% and 11%

Avg. Daily Volume

158531

respectively, while exchange had a weigh down effect by 13%, which impacted the

Face Value (`)

2

sales. On the operating front, the OPM came in at 19.0% V/s 17.9% in 3QFY2015.

BSE Sensex

24,539

This is in spite of lower sales as the GPM improved to 54.2% V/s 48.8% in

Nifty

7,456

3QFY2015 on back of healthy volume growth and price rise. This aided the Adj.

Reuters Code

UNPO.BO

net profit to come in at `306cr V/s `264cr in 3QFY2015, a yoy growth of 15.9%.

The Management has maintained its guidance of 12-13% volume growth with

Bloomberg Code

UNTP@IN

100bps margin expansion in FY2016. We maintain our Buy recommendation on

the stock with a price target of `480.

Shareholding Pattern (%)

Quarterly highlights: For the quarter, UPL posted sales of `3,050cr, a yoy growth of

Promoters

29.8

1.3%. USA and Latin America posted a 12% and 14% yoy growth, respectively,

MF / Banks / Indian Fls

22.0

during the quarter. Other key markets like India, Europe and ROW posted a dip of

FII / NRIs / OCBs

38.4

17%, 9% and 8% yoy, respectively. Overall, growth was driven by price and volume

Indian Public / Others

9.8

growth of 3% and 11% respectively, while exchange had a weigh down effect by

13%. On the operating front, the OPM came in at 19.0% V/s 17.9% in 3QFY2015.

This is in spite of lower sales as the GPM improved to 54.2% V/s 48.8% in

Abs. (%)

3m 1yr

3yr

3QFY2015 on back of healthy volume growth and price rise. This aided the Adj.

Sensex

(7.6)

(15.7)

24.1

net profit to come in at `306cr V/s `264cr in 3QFY2015, a yoy growth of 15.8%.

UPL

(9.3)

5.7

215.8

Outlook and valuation: We expect UPL to post a CAGR of 9.9% and 15.8% in sales

and PAT respectively, over FY2015-17E. The Management has maintained its guidance

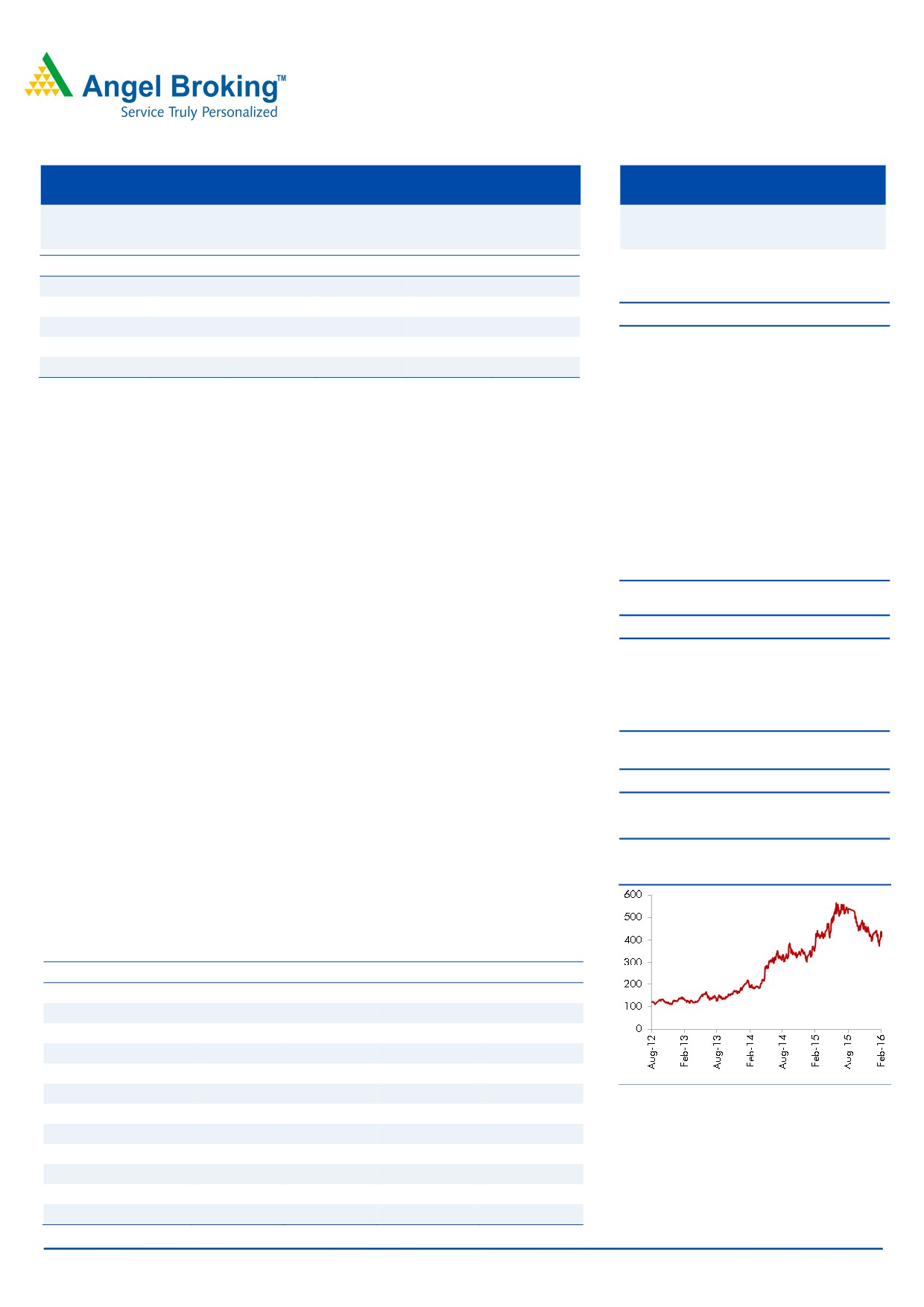

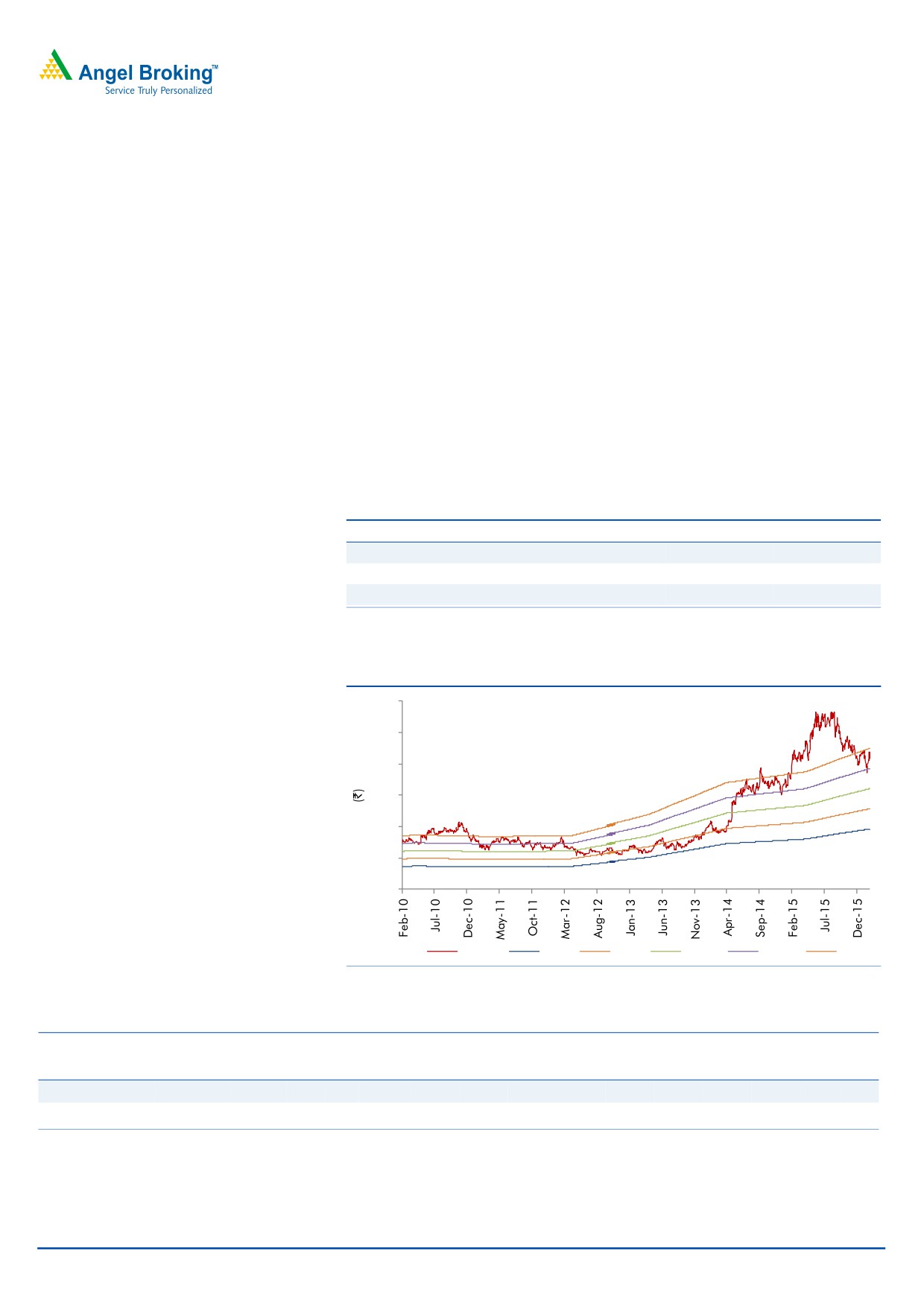

3-year price chart

of 12-13% volume growth with 100bp margin expansion in FY2016. We recommend a

Buy a price target of `480.

Key financials (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

Total revenue

10,580

11,911

12,500

14,375

% chg

17.4

12.6

4.9

15.0

Adj. profit

1,040

1,147

1,277

1,537

% chg

38.0

10.2

11.4

20.4

EBITDA (%)

17.3

18.3

18.3

18.3

EPS (`)

24.3

26.7

29.8

35.9

Source: Company, Angel Research

P/E (x)

17.1

15.5

13.9

11.6

P/BV (x)

3.4

3.0

2.6

2.2

RoE (%)

21.0

20.6

20.0

20.3

RoCE (%)

17.7

19.9

18.7

19.5

Sarabjit Kour Nangra

EV/Sales (x)

2.4

2.1

2.0

1.7

+91-22-3935 7800 ext. 6806

EV/EBITDA (x)

13.9

11.6

10.8

9.0

Source: Company, Angel Research; Note: CMP as of February 2, 2016

Please refer to important disclosures at the end of this report

1

United Phosphorus | 3QFY2016 Result Update

Exhibit 1: 3QFY2016 Performance (Consolidated)

Y/E March (` cr)

3QFY2016

2QFY2016

% chg (qoq) 3QFY2015

% chg (yoy) 9MFY2016 9MFY2015

% chg

Net sales

3,050

2,729

11.8

3,010

1.3

8,790

8,348

5.3

Other income

131

51

155.2

51

157.1

210

155

35.6

Total income

3,181

2,780

14.4

3,061

3.9

9,001

8,503

5.9

Gross profit

1652

1362

21.4

1469

12.5

4524

4192

7.9

Gross margin (%)

54.2

49.9

48.8

51.5

50.2

Operating profit

579

450

28.5

538

7.5

1554

1460

6.4

Operating margin (%)

19.0

16.5

17.9

17.7

17.5

Financial cost

182

135

34.1

138

31.6

419

394

Depreciation

123

111

10.6

109

13.0

343

321

6.7

PBT

405

255

58.9

342

18.4

1003

900

11.4

Provision for taxation

73

77

(5.8)

60

21.0

219

194

12.7

PAT Before Exc. And MI

332

178

86.9

282

17.9

784

706

11.0

Minority Income/ ( Exp.)

(8)

(2)

(23)

(5)

(40)

Income from Associate/ (Exp)

(14)

13

9

4

29

Extra ordinary Income/( Exp.)

(24)

(8)

(18)

(36)

10

Reported PAT

287

185

54.8

249

15.0

747

704

6.1

Adjusted PAT

306

190

60.7

264

15.9

775

696

11.3

EPS (`)

7.1

4.4

6.0

18.1

16.2

Source: Company, Angel Research

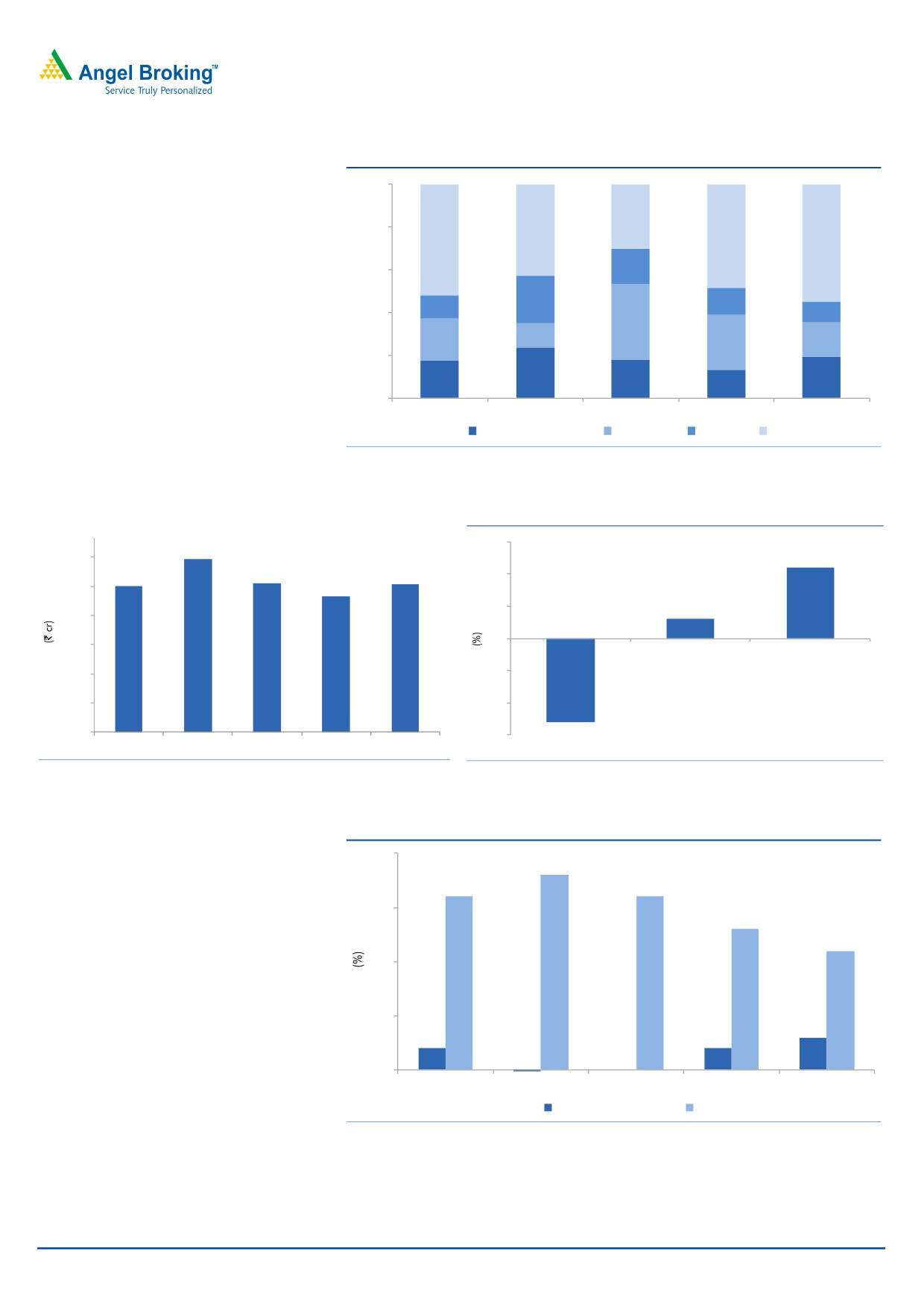

Top-line growth supported mainly by USA and Latin America

During the quarter, United Phosphorus posted sales of `3,050cr, a yoy growth of

1.3%. Sales were impacted as all the key markets were under pressure, while USA

and Latin America posted a 12% and 14% yoy growth, respectively, during the

quarter. Other key markets like India, Europe and ROW posted a dip of 17%, 9%

and 8% yoy, respectively. Overall, growth was driven by price and volume growth

of 3% and 11% respectively, while exchange had a weigh down effect by 13%.

India (`498cr) posted a 17% yoy dip in revenue owing to serious drought

conditions affecting agrochemical usage, both in Kharif & Rabi crops. However,

UPL’s new products and power brands continued to register healthy growth.

Europe (`300cr) posted a 9% yoy dip due to devaluation of the Euro, which

impacted growth in INR terms. Going forward, European markets are likely to be

flat or posting de-growth.

Latin America (`1,279cr) posted a 14% yoy growth on back of high demand of

fungicide. UPL expects to maintain the growth momentum on the back of new

product launches. Ease of export tax on agricultural commodities in Argentina is to

further aid demand for agrochemicals.

UPL’s North America (`594cr) business registered a 12% yoy revenue growth led

by healthy demand for its newly launched products. However, low pest infestation

in field crops, dry weather conditions in Western USA and higher competitive

intensity continued to weigh on the company’s overall performance in the region.

Extreme winter snowfall in many parts of North America could delay sowing and

impact 4QFY2016 performance; the business could shift to the next season.

February 3, 2016

2

United Phosphorus | 3QFY2016 Result Update

Exhibit 2: Sales Break-up (Marketwise)

100%

923

80%

1,557

1,587

1,354

1,705

60%

505

805

358

330

40%

300

1,083

401

601

715

498

20%

861

529

553

594

374

0%

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

North America

India

EU

Others

Source: Company

Exhibit 3: Sales performance (including export incentives)

Exhibit 4: Growth break-up

15

3,563

3,600

11

3,064

3,050

3,010

10

2,801

3,000

5

3

2,400

0

1,800

1,200

(5)

600

(10)

0

(15)

(13)

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

Exchange impact

Realisation

Volume

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 5: Volume and realisation break-up (yoy)

20

18

16

16

15

13

11

10

5

3

2

2

0

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

(2)

0

Realisation

Volume

Source: Company, Angel Research

February 3, 2016

3

United Phosphorus | 3QFY2016 Result Update

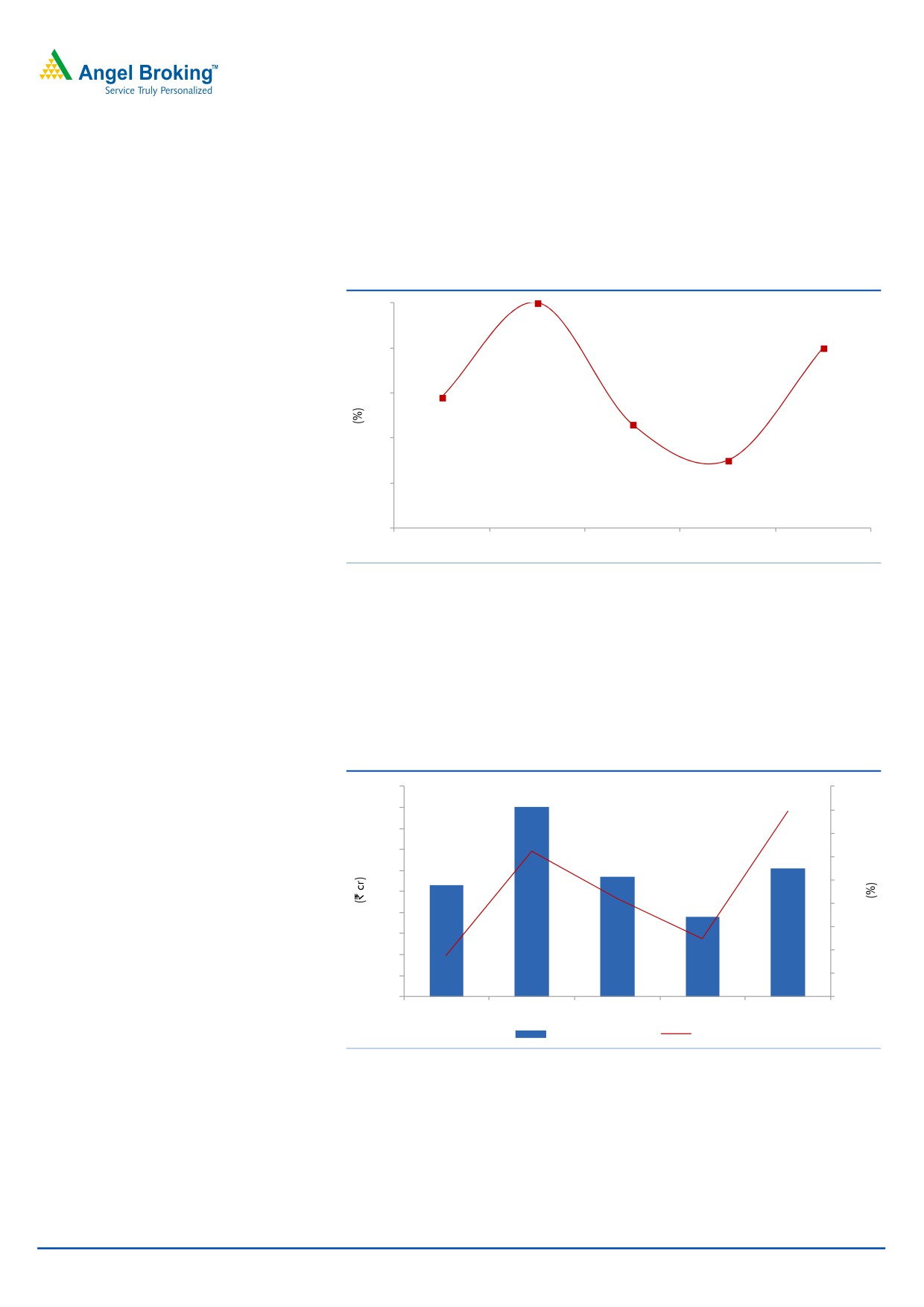

EBITDA margin improves

On the operating front, the OPM came in at 19.0% V/s 17.9% in 3QFY2015, in

spite of lower sales, as the GPM improved to 54.2% V/s 48.8% in 3QFY2015 on

back of healthy volume growth and price rise.

Exhibit 6: EBITDA margin trend

20.0

20.0

19.0

19.0

18.0

17.9

17.0

17.3

16.0

16.5

15.0

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

Source: Company, Angel Research

Adj net profit grew 15.8% yoy

This aided the Adj. net profit to come in at `306cr V/s `264cr in 3QFY2015, a

15.8% yoy growth. While the sales growth was meager, higher other income lead

the PAT growth to be robust. Other income during the quarter came in at `131cr

V/s `51cr in 3QFY2015, a yoy growth of 157.1%.

Exhibit 7: Adjusted PAT trend

500

18

451

450

16

400

14

350

306

12

285

300

264

10

250

190

8

200

6

150

4

100

50

2

0

0

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

Adj PAT

% YoY

Source: Company, Angel Research

February 3, 2016

4

United Phosphorus | 3QFY2016 Result Update

Concall Highlights

The company expects to maintain the growth momentum in Latin America on

the back of new product launches. Ease of export tax on agricultural

commodities in Argentina is to further aid demand for agrochemicals.

Low pest infestation in field crops, dry weather conditions in Western USA and

higher competitive intensity continue to weigh on the company’s overall

performance in the region.

The Management expects to report a flat performance or possibly a de-growth

in Europe for FY2016. Challenges persist in South Europe which faces a dry

season with low disease pressure.

Invvestment arguments

Innovators dominant in the off-patent space; Generic firms in

a sweet spot

The global agrichem industry, valued at US$53bn (CY2014), is dominated by the

top six innovators, viz Bayer, Syngenta, Monsanto, BASF, DuPont and Dow, which

enjoy a large market share of the patented (28%) and off-patent (32%) market.

The top six innovators enjoy a large share of the off-patent market due to high

entry barriers for pure generic players. Thus, one-third of the total pie worth

US$18bn, which is controlled by the top six innovators through proprietary

off-patent products, provides a high-growth opportunity for larger integrated

generic players like UPL.

Generic segment’s market share to increase

Generic players have been garnering a high market share; their share has

increased from 32% levels in 1998 to 40% by 2006-end. The industry registered a

CAGR of 3% over 1998-2006, while generic players outpaced the industry with a

CAGR of 6%. Going ahead, given the opportunities and a drop in the rate of new

molecule introduction by innovators, we expect generic players to continue to

outpace the industry’s growth rate and augment their market share in the overall

pie. Historically, global agrichem players have been logging in-line growth with

global GDP. Going ahead, over CY2015-16, the global economy is expected to

grow by 3-4%. Assuming this trend plays out in terms of growth for the agrichem

industry, and the same rate of genericisation occurs, then the agrichemical generic

industry could log in 6-8% yoy growth during the period and garner a market

share of 44-45%.

A global generic play

UPL figures among the top five global generic agrichemical players with presence

across major markets including the US, EU, Latin America, and India. Given the

high entry barriers by way of high investments, entry of new players is restricted.

Thus, amidst this scenario and on account of having a low-cost base,

we believe UPL enjoys an edge over competition and is placed in a sweet spot to

leverage the upcoming opportunities in the global generic space.

February 3, 2016

5

United Phosphorus | 3QFY2016 Result Update

Outlook and valuation

Over the last few years, the global agriculture sector has been reviving on the back

of rising food prices. Food security is also a top priority for most governments;

reducing food loss is one of the easiest ways to boost food inventory. Hence, we

believe agrichemical companies would continue to do well in the wake of

heightened food security risks, and strong demand is likely to be witnessed across

the world. Overall, we expect the global agrichemical industry to perform well

from here on. Generics are expected to register a healthy growth due to a)

increasing penetration and wresting market share from innovators and b) patent

expiries worth US$3bn-4bn during the next five years.

We estimate UPL to post a 9.9% and 15.8% CAGR in sales and PAT, respectively,

over FY2015-17E. The stock is trading at 11.6x FY2017E EPS, which we believe,

provides some room for appreciation. Hence we recommend a BUY rating on the

stock.

Exhibit 8: Key assumption

FY2016E

FY2017E

Sales growth

4.9

15.0

EBITDA margin

18.3

18.3

Tax rate

20.0

20.0

Source: Company, Angel Research

Exhibit 9: P/E band

600

500

400

300

200

100

0

Price

6x

8x

10x

12x

14x

Source: Company, Angel Research

Exhibit 10: Peer valuation

Company

Reco

Mcap CMP TP Upside

P/E (x)

EV/Sales (x)

EV/EBITDA (x)

RoE (%)

CAGR (%)

(` cr)

(`)

(`)

(%) FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E Sales PAT

Rallis

Neutral

3,075

158

-

-

22.0

18.3

2.5

2.1

17.6

14.8

16.5

18.0

3.7

3.4

United Phosphorus Buy

17,811

416

480

15.4

13.9

11.6

2.0

1.7

10.8

9.0

20.0

20.3

9.9

15.8

Source: Company, Angel Research, Bloomberg

February 3, 2016

6

United Phosphorus | 3QFY2016 Result Update

Company background

United Phosphorus (UPL) is a global generic crop protection, chemicals and seeds

company. The company is fully backward and forward integrated by taking

advantage of the consolidation opportunities within the agrochemical industry. UPL

is the largest Indian agrochemical company and had revenue of about `11,911cr

for the year ended March 2015.

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Net Sales

7,534

9,010

10,580

11,911

12,500

14,375

Other operating income

137

184

191

45

45

45

Total operating income

7,671

9,195

10,771

11,956

12,545

14,420

% chg

33.2

19.9

17.1

11.0

4.9

14.9

Total Expenditure

6,328

7,568

8,751

9,736

10,207

11,738

Net Raw Materials

4,058

4,687

5,441

6,016

6,413

7,374

Other Mfg costs

590

741

1,034

1,164

1,113

1,279

Personnel

686

853

946

1,043

1,094

1,259

Other

994

1,287

1,330

1,513

1,588

1,826

EBITDA

1,206

1,442

1,829

2,175

2,293

2,637

% chg

28.1

19.6

26.8

19.0

5.4

15.0

(% of Net Sales)

16.0

16.0

17.3

18.3

18.3

18.3

Depreciation& Amortisation

292

354

407

425

486

507

EBIT

1,051

1,273

1,613

1,796

1,852

2,175

% chg

25.3

21.1

26.7

11.4

3.1

17.4

(% of Net Sales)

13.7

13.8

15.0

15.0

14.8

15.1

Interest & other Charges

415

429

487

517

362

362

Other Income

97

73

131

131

131

131

(% of PBT)

13

8

10

9

8

7

Recurring PBT

734

917

1,257

1,410

1,622

1,945

% chg

11.4

25.0

37.1

12.2

15.0

19.9

Extraordinary Expense/(Inc.)

(5)

27

85

(2)

-

-

PBT (reported)

729

944

1,172

1,413

1,622

1,945

Tax

128

203

222

244

324

389

(% of PBT)

17.6

21.5

18.9

17.3

20.0

20.0

PAT (reported)

601

741

950

1,169

1,298

1,556

Add: Share of earnings of asso.

(40)

32

30

21

23

26

Less: Minority interest (MI)

5

(2)

7

43

43

43

Prior period items

-

-

24

-

1

2

PAT after MI (reported)

556

775

950

1,144

1,277

1,537

ADJ. PAT

561

754

1,040

1,147

1,277

1,537

% chg

1.6

34.3

38.0

10.2

11.4

20.4

(% of Net Sales)

7.5

8.4

9.8

9.6

10.2

10.7

Basic EPS (`)

12.2

17.0

24.3

26.7

29.8

35.9

Fully Diluted EPS (`)

12.2

17.0

24.3

26.7

29.8

35.9

% chg

1.6

40.1

42.5

10.2

11.4

20.4

February 3, 2016

7

United Phosphorus | 3QFY2016 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

SOURCES OF FUNDS

Equity Share Capital

92

89

86

86

86

86

Preference Capital

-

-

-

-

-

-

Reserves& Surplus

4,081

4,557

5,162

5,775

6,837

8,160

Shareholders’ Funds

4,173

4,645

5,247

5,860

6,923

8,246

Minority Interest

250

234

172

44

88

131

Total Loans

3,389

4,203

2,873

2,781

2,781

2,781

Other Long term liabilities

301

395

311

594

594

594

Long Term Provisions

51

51

53

53

53

53

Deferred Tax Liability

(6)

(13)

57

45

45

45

Total Liabilities

8,158

9,516

8,714

9,378

10,484

11,850

APPLICATION OF FUNDS

Gross Block

4,687

5,386

6,039

6,792

7,092

7,392

Less: Acc. Depreciation

2,605

3,173

3,580

4,005

4,491

4,998

Net Block

2,082

2,213

2,459

2,787

2,601

2,394

Capital Work-in-Progress

306

378

378

378

378

378

Goodwill / Intangilbles

1,141

1,277

1,212

1,449

1,449

1,449

Investments

795

1,025

737

764

764

764

Long Term Loan & Adv.

321

277

389

418

439

504

Current Assets

5,625

7,154

7,572

8,372

9,880

12,141

Cash

1,566

1,548

1,023

1,010

1,587

2,604

Loans & Advances

602

852

771

586

1,182

1,359

Other

3,458

4,754

5,779

6,776

7,111

8,178

Current liabilities

2,111

2,807

4,033

4,789

5,026

5,780

Net Current Assets

3,514

4,346

3,539

3,582

4,854

6,361

Others

-

-

-

-

-

-

Total Assets

8,158

9,516

8,714

9,378

10,484

11,850

February 3, 2016

8

United Phosphorus | 3QFY2016 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015 FY2016E FY2017E

Profit before tax

729

944

1,172

1,413

1,622

1,945

Depreciation

292

354

407

425

486

507

Change in Working Capital

318

(806)

171

(86)

(715)

(556)

Less: Other income

-

-

-

-

-

-

Direct taxes paid

(128)

(203)

(222)

(244)

(324)

(389)

Cash Flow from Operations

1,211

288

1,528

1,508

1,069

1,507

(Inc.)/ Dec. in Fixed Assets

(989)

(771)

(653)

(753)

(300)

(300)

(Inc.)/ Dec. in Investments

29

(231)

-

-

-

-

Inc./ (Dec.) in loans and adv.

-

-

-

-

-

-

Other income

-

-

-

-

-

-

Cash Flow from Investing

(961)

(1,002)

(653)

(753)

(300)

(300)

Issue of Equity

-

-

(3)

-

-

-

Inc./(Dec.) in loans

(989)

(908)

1,413

(192)

(0)

(0)

Dividend Paid (Incl. Tax)

(134)

(129)

(201)

(214)

(214)

(214)

Others

1,738

1,733

(2,612)

(362)

23

24

Cash Flow from Financing

615

696

(1,403)

(768)

(192)

(190)

Inc./(Dec.) in Cash

866

(18)

(525)

(13)

577

1,017

Opening Cash balances

700

1,566

1,548

1,023

1,010

1,587

Closing Cash balances

1,566

1,548

1,023

1,010

1,587

2,604

February 3, 2016

9

United Phosphorus | 3QFY2016 Result Update

Key Ratios

Y/E March

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

34.2

24.4

17.1

15.5

13.9

11.6

P/CEPS

22.5

16.6

12.3

11.3

10.1

8.7

P/BV

4.6

4.0

3.4

3.0

2.6

2.2

Dividend yield (%)

0.6

0.6

0.6

0.6

0.6

0.6

EV/Sales

3.4

2.9

2.4

2.1

2.0

1.7

EV/EBITDA

21.0

18.0

13.9

11.6

10.8

9.0

EV / Total Assets

3.1

2.7

2.9

2.7

2.4

2.0

Per Share Data (`)

EPS (Basic)

12.2

17.0

24.3

26.7

29.8

35.9

EPS (fully diluted)

12.2

17.0

24.3

26.7

29.8

35.9

Cash EPS

18.5

25.0

33.8

36.7

41.1

47.7

DPS

2.5

2.5

2.5

2.5

2.5

2.5

Book Value

90.4

105.0

122.4

136.7

161.5

192.4

DuPont Analysis

EBIT margin

13.7

13.8

15.0

15.0

14.8

15.1

Tax retention ratio

82.4

78.5

81.1

82.7

80.0

80.0

Asset turnover (x)

1.4

1.4

1.5

1.6

1.6

1.7

ROIC (Post-tax)

15.8

15.4

18.5

20.3

18.8

20.9

Cost of Debt (Post Tax)

11.3

8.9

11.2

15.1

10.4

10.4

Leverage (x)

0.5

0.5

0.5

0.3

0.2

0.1

Operating ROE

18.0

18.6

21.9

22.0

20.8

21.9

Returns (%)

ROCE (Pre-tax)

14.4

14.4

17.7

19.9

18.7

19.5

Angel ROIC (Pre-tax)

19.5

20.0

23.2

24.7

23.5

26.2

ROE

14.2

17.1

21.0

20.6

20.0

20.3

Turnover ratios (x)

Asset Turnover (Gross Block)

1.8

1.8

1.9

1.9

1.8

2.0

Inventory / Sales (days)

78

78

83

86

89

85

Receivables (days)

93

102

83

86

89

85

Payables (days)

102

108

69

72

74

71

WCcycle (ex-cash) (days)

105

96

92

78

85

89

Solvency ratios (x)

Net debt to equity

0.5

0.4

0.6

0.4

0.3

0.2

Net debt to EBITDA

2.1

1.5

1.8

1.0

0.8

0.5

Interest Coverage (EBIT / Int.)

2.5

3.0

3.3

3.5

5.1

6.0

February 3, 2016

10

United Phosphorus | 3QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

UPL

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 3, 2016

11