2QFY2016 Result Update | Steel

November 6, 2015

Tata Steel

NEUTRAL

CMP

`226

Performance Highlights

Target Price

-

Investment Period

-

Standalone (` cr)

2QFY16

2QFY15

yoy % 1QFY16

qoq %

Net revenue

9,531

10,785

(11.6)

9,094

4.8

EBITDA

1,862

3,094

(39.8)

1,689

10.2

Stock Info

Margin (%)

19.5

28.7

(916bp)

18.6

96bp

Sector

Steel

Adj. PAT

3,844

1,330

189.2

1,143

236.4

Market Cap (` cr)

21,911

Source: Company, Angel Research

Net Debt (` cr)

73,477

Raw Material purchases impact EBITDA: Tata Steel’s standalone revenues for

Beta

1.5

2QFY2016 declined

12% yoy to

`9,531cr

(7% ahead of our estimate of

52 Week High / Low

493/200

`8,879cr), led by better than expected volumes and pricing. However, increased

Avg. Daily Volume

87,13,227

raw material expenses on account of external purchases of iron ore resulted in the

Face Value (`)

10

EBITDA declining sharply by 40% yoy to `1,862cr, 3% below our expectation of

BSE Sensex

26,304

`1,918cr. The adjusted net profit nearly doubled to `3,844cr led by a sharp jump

Nifty

7,955

in other income on account of gains from sale of quoted investments of `3,505cr,

Reuters Code

TISC.BO

while interest expenses were lower on account of debt repayments in 1QFY2015.

Bloomberg Code

TATA IN

Consolidated (` cr)

2QFY16

2QFY15

yoy %

1QFY16

qoq %

Net revenue

29,305

35,777

(18.1)

30,300

(3.3)

Shareholding Pattern (%)

EBITDA

1,830

3,643

(49.8)

2,774

(34.0)

Margin (%)

6.2

10.2

(394bp)

9.2

(291bp)

Promoters

31.4

Adj. PAT

2,092

109

1,814.1

605

246.1

MF / Banks / Indian Fls

25.9

Source: Company, Angel Research

FII / NRIs / OCBs

11.8

Indian Public / Others

30.9

Overseas operations remain under pressure: The EBITDA of the European

operations turned negative, led by a steep decline in realisations and on account

of lower volumes. Tata Steel Europe (TSE)’s sales volumes declined 3% yoy to

Abs. (%)

3m 1yr

3yr

3.27MT, 7% below our expectation of 3.53MT. Realisation declined 20% yoy to

Sensex

(6.8)

(5.8)

40.2

$798/tonne, but 10% ahead of our estimate of $723/tonne. SEA volumes

Tata Steel

(14.0)

(52.8)

(43.3)

continued to remain under pressure, with deliveries declining 27% yoy to 0.69MT.

Outlook and valuation: Given the weak outlook on steel prices and with the

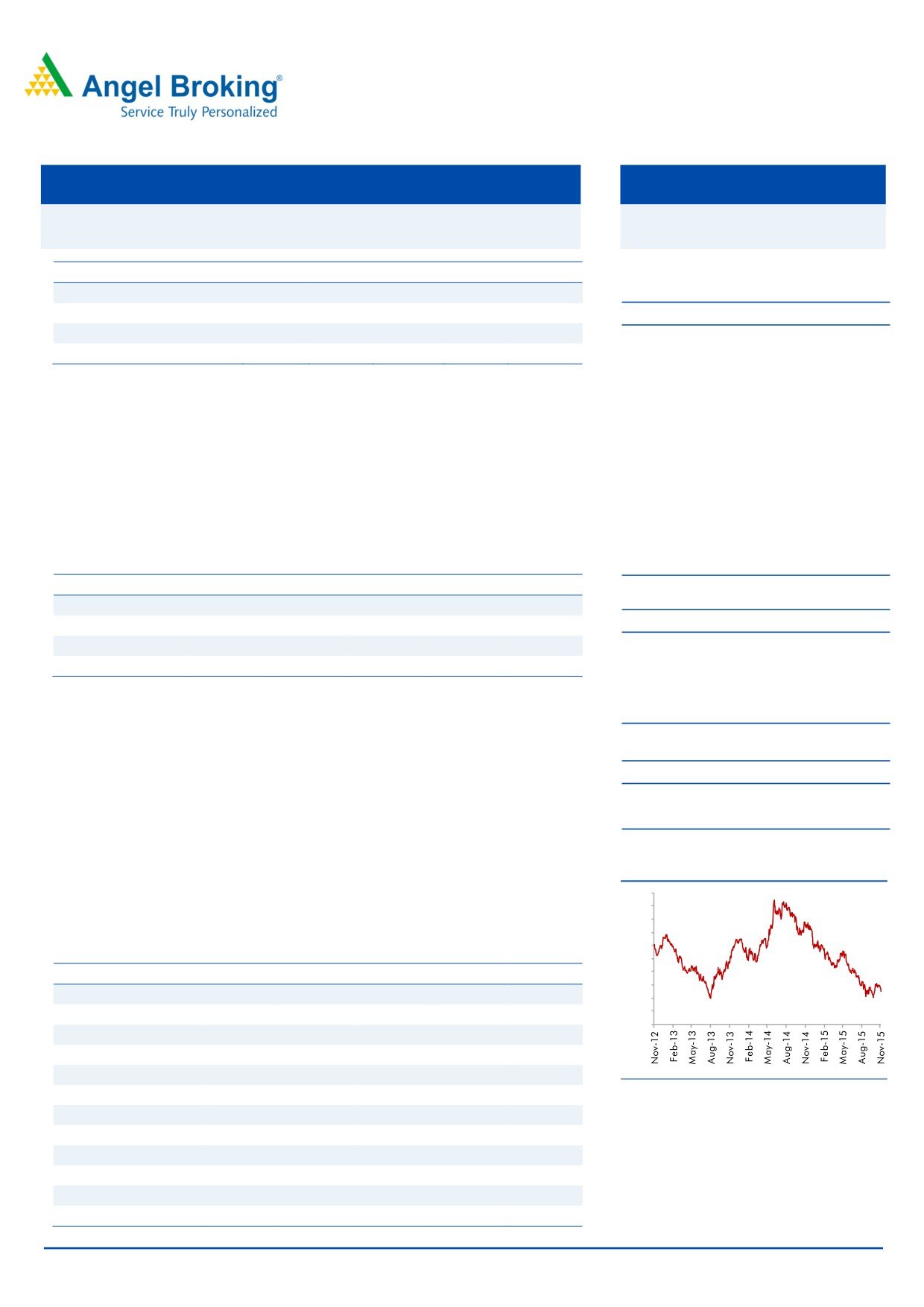

3-year price chart

European business already in the red at the operating level, we expect tough

600

times to continue for the stock. The stock is currently trading at an EV/EBITDA of

550

500

6.8x FY2017E EBITDA. We retain our Neutral rating on the stock.

450

400

Key financials (Consolidated)

350

Y/E March (` cr)

FY2013

FY2014

FY2015E FY2016E FY2017E

300

250

Net sales

1,34,712

1,48,614

1,39,504

1,23,985

1,30,520

200

150

% chg

1.4

10.3

(6.1)

(11.1)

5.3

100

Reported PAT

(7,058)

3,595

(3,926)

(2,473)

1,714

% chg

-

-

-

-

(169.3)

Adj. EPS (`)

3.4

37.3

0.0

(25.5)

17.6

Source: Company, Angel Research

EBITDA margin (%)

9.1

11.0

9.0

5.4

11.3

P/E (x)

66.0

6.0

-

(8.9)

12.8

P/BV (x)

0.6

0.5

0.7

0.8

0.8

RoE (%)

0.9

9.7

0.0

(8.4)

6.1

RoCE (%)

6.3

8.8

5.6

0.9

5.9

Rahul Dholam

EV/Sales (x)

0.6

0.6

0.6

0.8

0.8

Tel: 022- 3935 7800 Ext: 6847

EV/EBITDA (x)

6.3

5.5

7.2

14.7

6.8

Source: Company, Angel Research: Note CMP as of Nov 05, 2016

Please refer to important disclosures at the end of this report

1

Tata Steel | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance (Standalone)

Y/E March (` Cr)

2QFY16

2QFY15

yoy %

1QFY16

qoq %

FY2015

FY2014

yoy %

Net Sales

9,531

10,785

(11.6)

9,094

4.8

41,785

41,711

0.2

- Consumption of Raw Material

2,936

2,594

13.2

2,368

24.0

11,651

9,875

18.0

(% of Net Sales)

30.8

24.0

26.0

27.9

23.7

- Power& Fuel

668

677

(1.3)

694

(3.7)

2,570

2,565

0.2

(% of Net Sales)

7.0

6.3

7.6

6.2

6.1

- Staff Costs

1,085

1,143

(5.1)

1,082

0.3

4,606

3,673

25.4

(% of Net Sales)

11.4

10.6

11.9

11.0

8.8

Freight & Handling

707

694

1.9

695

1.7

2,883

2,755

4.7

(% of Net Sales)

7.4

6.4

7.6

6.9

6.6

- Other expenses

2,272

2,582

(12.0)

2,565

(11.4)

10,065

10,026

0.4

(% of Net Sales)

23.8

23.9

28.2

24.1

24.0

Total Expenditure

7,670

7,691

(0.3)

7,405

3.6

31,776

28,894

10.0

EBITDA

1,862

3,094

(39.8)

1,689

10.2

10,009

12,817

(21.9)

EBITDA Margin (%)

19.5

28.7

18.6

24.0

30.7

Interest

331

489

(32.2)

396

(16.3)

1,976

1,821

8.5

Depreciation

481

475

1.4

468

2.7

1,998

1,929

3.6

Other Income

2,933

262

1,017.7

749

291.6

583

788

(26.0)

Exceptional Items

(1,322)

1,147

106

1,891

(142)

Profit before Tax

2,660

3,540

(24.8)

1,679

58.4

8,509

9,714

(12.4)

(% of Net Sales)

27.9

32.8

18.5

20.4

23.3

Tax

138

1,064

(87.1)

431

(68.1)

2,070

3,301

(37.3)

(% of PBT)

5.2

30.0

25.6

24.3

34.0

Net income

2,523

2,476

1.9

1,249

102.1

6,439

6,412

0.4

Adjusted net income

3,844

1,330

189.2

1,143

236.4

4,548

6,554

(30.6)

Source: Company, Angel Research

Exhibit 2: 2QFY2016 Standalone - Actual vs Angel estimates

(` cr)

Actual

Estimates

Variation (%)

Net sales

9,531

8,879

7.3

EBITDA

1,862

1,918

(2.9

EBITDA margin (%)

19.5

21.6

(207bp)

Source: Company, Angel Research

Result highlights - Standalone

External raw material purchases impact EBITDA

Standalone revenues declined by 12% yoy and 5% on a sequential basis to

`9,531cr (7% ahead of our estimate of `8,879cr). Standalone sales volume

increased 11% yoy to 2.33MT, well ahead of our expectation of 2.15MT, while

blended realisation declined by 20% to `40,853/tonne, but 7% higher than our

estimate of `38,058/tonne. Steel realisation declined 20% to `39,286, lower than

the decline in domestic average landed HRC prices, which declined 38% on a yoy

basis.

November 6, 2015

2

Tata Steel | 2QFY2016 Result Update

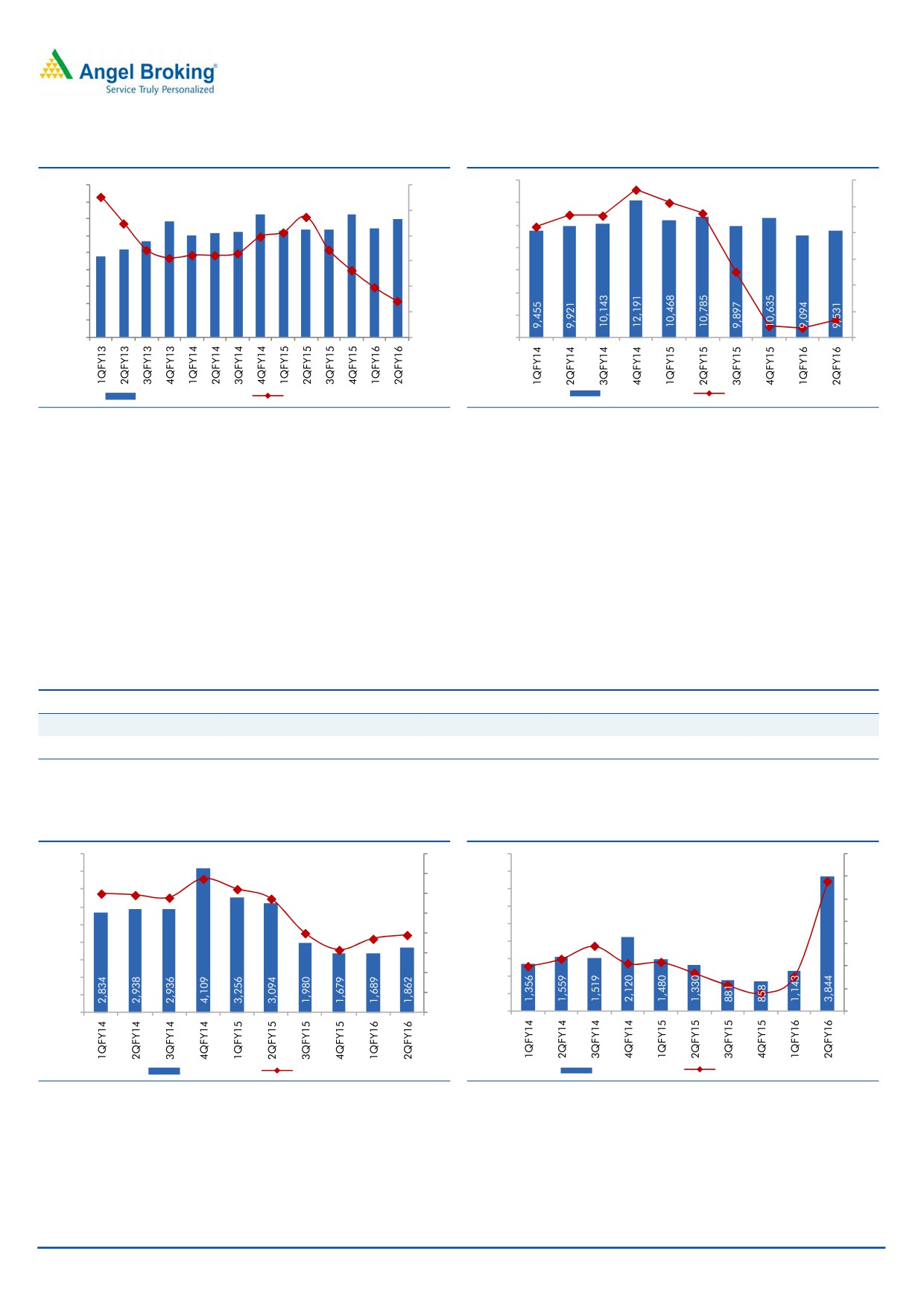

Exhibit 3: Blended realisation continues to fall

Exhibit 4: Top-line declines ~12% yoy

14,000

15

53,000

3.0

51,000

2.4

2.4

12,000

2.3

2.3

10

2.5

2.1

2.1

2.1

2.1

49,000

2.0

2.0

2.1

1.9

10,000

47,000

1.7

2.0

5

1.6

8,000

45,000

1.5

0

43,000

6,000

41,000

1.0

-5

4,000

39,000

0.5

2,000

-10

37,000

35,000

0.0

0

-15

Sales Volume (MT)

Realisation (`/tonne)

Revenue (` cr)

yoy change (%)

Source: Company, Angel Research

Source: Company, Angel Research

Raw material expenses, at `2,937cr (~31% of revenues), were ahead of our

estimates on account of external purchases of iron as operations at the Naomundi

mine were suspension for a major part of the quarter. Staff, power and freight

expenses too came in ahead of our expectations, resulting in the EBITDA seeing a

sharp decline of 40% yoy to `1,862cr, 3% below our expectation of `1,918cr,

despite revenue being ahead of our expectations. The adjusted net profit nearly

doubled to `3,844cr, led by a sharp jump in other income on account of gains

from sale of quoted investments of `3,505cr, while interest expenses were lower on

account of debt repayments in 1QFY2015.

Exhibit 5: Quarterly Performance Trend (Standalone)

1QFY14

2QFY14

3QFY14

4QFY14

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Realisation (US$/tonne)

799

720

725

759

775

813

731

689

644

605

EBITDA (US$/tonne)

258

232

229

276

259

242

150

112

124

123

Source: Company, Angel Research

Exhibit 6: EBITDA margin inches up qoq to ~20%

Exhibit 7: Other income boosts net profit

4,500

40

4,500

250

33.7

189.2

4,000

31.1

35

4,000

30.0

29.6

200

28.9

28.7

3,500

3,500

30

150

3,000

3,000

20.0

25

18.6

19.5

100

2,500

2,500

15.8

20

45.1

2,000

2,000

16.2

6.4

9.1

50

15

(0.0)

1,500

1,500

(14.7)

(22.8)

(42.0)

0

1,000

10

1,000

(59.5)

(50)

500

5

500

0

0

0

(100)

EBITDA (` cr)

Margin (%)

Net Profit (` cr)

yoy change (%)

Source: Company, Angel Research

Source: Company, Angel Research

November 6, 2015

3

Tata Steel | 2QFY2016 Result Update

Exhibit 8: 2QFY2016 performance (Consolidated)

Y/E March (` Cr)

2QFY16

2QFY15

% chg (yoy)

1QFY16

% chg (qoq)

FY2015

FY2014

yoy %

Net Sales

29,305

35,777

(18.1)

30,300

(3.3)

1,39,504

1,48,614

(6.1)

- Consumption of Raw Material

11,290

14,096

(19.9)

11,045

2.2

55,667

62,737

(11.3)

(% of Net Sales)

38.5

39.4

36.5

39.9

42.2

- Power& Fuel

1,379

1,528

(9.7)

1,448

(4.8)

5,913

6,036

(2.0)

(% of Net Sales)

4.7

4.3

4.8

4.2

4.1

- Staff Costs

4,990

5,399

(7.6)

4,896

1.9

21,408

20,303

5.4

(% of Net Sales)

17.0

15.1

16.2

15.3

13.7

Freight & Handling

2,045

2,190

(6.6)

2,031

0.7

8,811

9,008

(2.2)

(% of Net Sales)

7.0

6.1

6.7

6.3

6.1

- Other expenses

7,770

8,920

(12.9)

8,106

(4.1)

35,168

34,119

3.1

(% of Net Sales)

26.5

24.9

26.8

25.2

23.0

Total Expenditure

27,474

32,134

(14.5)

27,526

(0.2)

1,26,968

1,32,203

(4.0)

EBITDA

1,830

3,643

(49.8)

2,774

(34.0)

12,536

16,411

(23.6)

EBITDA Margin (%)

6.2

10.2

9.2

9.0

11.0

Interest

1,049

1,233

(14.9)

1,098

(4.5)

4,848

4,337

11.8

Depreciation

1,371

1,430

(4.1)

1,347

1.8

5,944

5,841

1.8

Other Income

2,938

322

813.8

762

285.5

796

517

54.1

Exceptional Items

(564)

1,145

158

(3,929)

(28)

Profit before Tax

1,785

2,447

(27.0)

1,250

42.8

(1,388)

6,722

(120.6)

(% of Net Sales)

6.1

6.8

4.1

(1.0)

4.5

Tax

240

1,175

(79.6)

515

(53.4)

2,567

3,058

(16.0)

(% of PBT)

13.5

48.0

41.2

(185.0)

45.5

Profit after Tax

1,545

1,272

21.5

735

110.3

(3,955)

3,664

(208.0)

Share of profit

(16)

(15)

21

13

(70)

Minority interest

(1)

(3)

7

17

1

Profit after Tax

1,529

1,254

21.9

763

100.4

(3,926)

3,595

(209.2)

(% of Net Sales)

5.2

3.5

2.5

(2.8)

2.4

Adjusted net income

2,092

109

1,814.1

605

246.1

3

3,623

(99.9)

Source: Company, Angel Research

Exhibit 9: Consolidated - 2QFY2015 Actual vs Angel estimates

(` cr)

Actual

Estimates

Variation (%)

Net sales

29,305

28,504

2.8

EBITDA

1,830

2,632

(30.5)

EBITDA margin (%)

6.2

9.2

(299)bp

Source: Company, Angel Research

November 6, 2015

4

Tata Steel | 2QFY2016 Result Update

Result highlights - Consolidated

Overseas operations remain under pressure

On a consolidated basis, the company’s net sales declined by ~18% yoy to

`29,305cr (~3% ahead of our estimate of `28,504cr). The EBITDA however came

in much lower than expected at `1,830cr, 31% lower than our estimate of

`2,632cr, on account of the EBITDA loss at the European business.

Tata Steel Europe (TSE)’s sales volumes declined 3% yoy to 3.27MT, 7% below our

expectation of 3.53MT. Realisation declined 20% yoy to $798/tonne, but was 10%

ahead of our estimate of $723/tonne. TSE however reported an EBITDA level loss

of `139cr as against an EBITDA profit of `929cr in 2QFY2015 and vs our

expectation of a profit of `984cr. Europe EBITDA continued to get affected by

adverse currency movement of the GBP against the USD and EUR, and pressure

from imports. The Management indicated that steel demand in increasing at a

slower pace than expected and that most of the incremental demand would be

catered to by imports.

SEA volumes continued to remain under pressure, with deliveries declining 27%

yoy to

0.69MT. However, SEA operations posted an EBITDA of

`70cr for

2QFY2016, as against an EBITDA loss of `281cr in 2QFY2015. The other

subsidiaries saw a steep sequential decline in EBITDA at `91cr as against `476cr

in 1QFY2016.

Exhibit 10: Quarterly Performance Trend (Tata Steel Europe)

1QFY14

2QFY14

3QFY14

4QFY14

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Deliveries (MT)

3.1

3.5

3.2

4.1

3.2

3.4

3.3

3.8

3.4

3.3

Realisation (US$/tonne)

2

2

2

2

2

2

2

2

2

2

EBITDA (US$/tonne)

777.0

554.0

860.0

817.0

995.0

929.0

1008.0

1053.0

575.0

-139.0

Source: Company, Angel Research

Exhibit 11: Quarterly Performance Trend (SEA)

1QFY14

2QFY14

3QFY14

4QFY14

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Deliveries (MT)

0.86

0.96

1.09

1.07

1.08

0.95

0.80

0.76

0.69

0.69

Revenue (` Cr)

3,908

4,179

4,537

4,365

4,045

3,710

2,831

2,461

2,262

2,001

EBITDA (` Cr)

93

129

137

80

30

(281)

(18)

(232)

34

70

Source: Company, Angel Research

November 6, 2015

5

Tata Steel | 2QFY2016 Result Update

Investment arguments

Capacity expansion remains on track

Tata Steel is setting up a 6mn-tonne integrated steel plant (including cold rolling

mill) in two phases of 3mn tonne each. The Kalinganagar Steel Plant is a state-of-

the-art steel plant that will increase production capacity, widen the product

portfolio and help Tata Steel to diversify the customer base. Commercial

production at Phase-1 of the new Kalinganagar plant is expected to commence in

this quarter. The Management expects ramp up to remain slow as it is a greenfield

capacity. We factor in an additional production of just 0.5MT for FY2016, in-line

with the guidance. We expect an additional production of 1MT over each of the

next two fiscals, leading to a CAGR of ~10% in production volumes.

Outlook for steel prices continues to remain negative

Steel prices continue to remain under pressure led by Chinese exports and

depreciation of the Russian ruble. Demand continues to remain weak across the

world. The World Steel Association has forecasted steel demand to decline 1.7% in

CY2015 and increase marginally

(0.7%) in CY2016. Chinese demand is

forecasted to fall by 3.5% and 2% in CY2015 and CY2016 respectively. Global

supply of iron ore also continues to remain strong, with the iron ore majors

continuing to increase production. We therefore expect prices on the raw material

side to also remain under pressure resulting in downward pressure on product

prices.

November 6, 2015

6

Tata Steel | 2QFY2016 Result Update

Outlook and valuation

Given the weak outlook on steel prices and with the European business already in

the red at the operating level, we expect tough times to continue for the stock. The

stock is currently trading at an EV/EBITDA of 6.8x FY2017E EBITDA. We retain our

Neutral view on the stock.

Company background

Incorporated in 1907, Tata Steel is the world's tenth largest steel company and the

world's second most geographically diversified steel producer with major

operations in India and Europe. During April 2007, the company acquired Corus

(now Tata Steel Europe), the second largest steel producer in Europe, for a

consideration of US$12bn. Its India operations’ capacity stands at ~13mn tonne,

while its European operations’ capacity stands at ~17MT.

November 6, 2015

7

Tata Steel | 2QFY2016 Result Update

Profit & Loss Statement (Consolidated)

Y/E March (` Cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Total operating income

1,34,712

1,48,614

1,39,504

1,23,985

1,30,520

% chg

1.4

10.3

(6.1)

(11.1)

5.3

Total Expenditure

1,22,390

1,32,203

1,26,968

1,17,303

1,15,791

Net raw materials

60,536

62,737

55,667

44,050

43,946

Other mfg costs

12,988

15,044

14,725

11,159

11,747

Personnel

18,918

20,303

21,408

20,032

20,777

Other

29,948

34,119

35,168

42,062

39,320

EBITDA

12,321

16,411

12,536

6,682

14,729

% chg

(0.8)

33.2

(23.6)

(46.7)

120.4

(% of Net Sales)

9.1

11.0

9.0

5.4

11.3

Depreciation& Amortisation

5,575

5,841

5,944

6,897

8,024

EBIT

6,746

10,570

6,592

(215)

6,706

% chg

(14.6)

56.7

(37.6)

(103.3)

(3,224.7)

(% of Net Sales)

5.0

7.1

4.7

(0.2)

5.1

Interest & other Charges

3,968

4,337

4,848

4,854

4,973

Other Income

479

517

796

1,336

800

(% of PBT)

14.7

7.7

31.3

(35.8)

31.6

Share in profit of Associates

-

-

-

-

-

Recurring PBT

3,257

6,750

2,541

(3,733)

2,533

% chg

(37.6)

107.2

(62.4)

(246.9)

(167.9)

Extra. Inc/(Expense)

(7,390)

(28)

(3,929)

0

0

PBT (reported)

(4,133)

6,722

(1,388)

(3,733)

2,533

Tax

3,229

3,058

2,567

(1,232)

836

(% of PBT)

(78.1)

45.5

(185.0)

33.0

33.0

PAT (reported)

(7,362)

3,664

(3,955)

(2,501)

1,697

Add: Share of earnings of asso.

90

1

17

19

22

Less: Minority interest (MI)

214

(70)

13

8

(6)

PAT after MI (reported)

(7,058)

3,595

(3,926)

(2,473)

1,714

ADJ. PAT

332

3,623

3

(2,473)

1,714

% chg

(83.6)

990.3

(99.9)

(78,623.3)

(169.3)

(% of Net Sales)

0.2

2.4

0.0

(2.0)

1.3

November 6, 2015

8

Tata Steel | 2QFY2016 Result Update

Balance Sheet (Consolidated)

Y/E March (` Cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

SOURCES OF FUNDS

Equity Share Capital

971

984

984

984

984

Reserves & Surplus

33,201

39,561

30,378

26,768

27,343

Shareholders Funds

34,172

40,532

31,349

27,740

28,314

Share Warrants

21

20

20

20

20

Hybrid perpetual securities

2,275

2,275

2,275

2,275

2,275

Minority Interest

1,669

1,738

1,704

1,695

1,701

Total Loans

68,507

81,609

80,701

83,201

84,701

Deferred Tax Liability

3,155

2,596

2,885

2,885

2,885

Other LT liabilities

6,477

7,994

9,211

9,211

9,211

Total Liabilities

1,16,277

1,36,764

1,28,145

1,27,027

1,29,107

APPLICATION OF FUNDS

Gross Block

1,34,774

1,56,143

1,77,511

1,90,331

2,00,588

Less: Acc. Depreciation

79,838

96,984

1,02,928

1,09,825

1,17,849

Net Block

54,937

59,158

74,583

80,506

82,740

Capital Work-in-Progress

14,277

26,822

8,788

8,110

9,996

Goodwill

13,065

15,749

13,408

13,408

13,408

Investments

3,258

5,093

3,455

3,063

2,106

Current Assets

53,464

55,321

52,220

45,746

46,401

Cash

9,834

8,605

8,750

3,674

3,952

Loans & Advances

4,061

3,193

4,603

4,603

4,603

Other

38,085

42,886

38,460

37,062

37,439

Current liabilities

30,636

34,881

30,800

30,298

32,035

Net Current Assets

22,829

20,440

21,420

15,448

14,366

Mis. Exp. not written off

0

0

0

0

0

Total Assets

1,16,277

1,36,764

1,28,145

1,27,027

1,29,107

November 6, 2015

9

Tata Steel | 2QFY2016 Result Update

Cash flow statement (Consolidated)

Y/E March (` Cr)

FY2013

FY2014

FY2015E FY2016E FY2017E

Profit before tax

(4,133)

6,722

(1,388)

(3,733)

2,533

Depreciation

5,575

5,841

5,944

6,897

8,024

Change in Working Capital

3,841

(1,270)

(834)

895

1,361

Less: Other income

11,321

4,865

2,712

-

-

Direct taxes paid

(2,569)

(3,013)

(2,567)

1,232

(836)

Cash Flow from Operations

14,035

13,146

3,866

5,291

11,081

(Inc.)/ Dec. in Fixed Assets

(15,222)

(16,126)

(3,334)

(12,143)

(12,143)

(Inc.)/ Dec. in Investments

1,926

(326)

1,638

393

957

(Inc.)/ Dec. in loans and advances

-

-

-

-

-

Other income

Cash Flow from Investing

(13,297)

(16,451)

(1,696)

(11,750)

(11,186)

Issue of Equity

262

12

-

-

-

Inc./(Dec.) in loans

2,918

5,875

(908)

2,500

1,500

Dividend Paid (Incl. Tax)

(1,359)

(924)

(1,117)

(1,117)

(1,117)

Others

(3,602)

(3,948)

-

-

-

Cash Flow from Financing

(1,780)

1,015

(2,025)

1,383

383

Other Adjustments

198

1,073

-

-

-

Inc./(Dec.) in Cash

(844)

(1,218)

145

(5,076)

278

Opening Cash balances

10,513

9,669

8,605

8,750

3,674

Closing Cash balances

9,669

8,451

8,750

3,674

3,952

November 6, 2015

10

Tata Steel | 2QFY2016 Result Update

Key ratios

Y/E March

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

66.0

6.0

6,957.1

(8.9)

12.8

P/CEPS

-

2.3

10.9

5.0

2.3

P/BV

0.6

0.5

0.7

0.8

0.8

P/BV (ex Goodwill)

1.0

0.9

1.2

1.5

1.5

Dividend yield (%)

-

4.4

4.4

4.4

4.4

EV/Sales

0.6

0.6

0.6

0.8

0.8

EV/EBITDA

6.3

5.5

7.2

14.7

6.8

EV/Total Assets

0.7

0.7

0.7

0.8

0.8

Per Share Data (`)

EPS (Basic)

3.4

37.3

(40.4)

(25.5)

17.6

Adjusted EPS (fully diluted)

3.4

37.3

0.0

(25.5)

17.6

Cash EPS

(15.3)

97.1

20.8

45.5

100.2

DPS

8.0

10.0

10.0

10.0

10.0

Book Value

351.8

417.2

322.7

285.6

291.5

Book Value (adj. for Goodwill)

217.3

255.1

184.7

147.5

153.5

Dupont Analysis

EBIT margin

5.0

7.1

4.7

(0.2)

5.1

Tax retention ratio (%)

178.1

54.5

285.0

67.0

67.0

Asset turnover (x)

1.4

1.4

1.2

1.0

1.1

ROIC (Post-tax)

12.0

5.4

15.9

(0.1)

3.6

Cost of Debt (Post Tax)

13.1

3.6

19.1

4.3

4.2

Leverage (x)

1.7

1.8

2.3

2.9

2.9

Operating ROE

10.2

8.8

8.8

(12.8)

2.1

Returns (%)

ROCE (Pre-tax)

6.3

8.8

5.6

0.9

5.9

Angel ROIC (Pre-tax)

23.8

27.3

20.3

14.1

23.5

ROE

0.9

9.7

0.0

(8.4)

6.1

Turnover ratios (x)

Asset Turnover (Gross Block)

1.1

1.0

0.8

0.7

0.7

Inventory (days)

73

69

74

74

74

Receivables (days)

39

36

38

38

38

Payables (days)

53

51

54

54

54

WC cycle (ex-cash) (days)

34

30

32

36

31

Solvency ratios (x)

Net debt to equity

1.7

1.8

2.3

2.9

2.9

Net debt to EBITDA

4.8

4.4

5.7

11.9

5.5

Interest Coverage (EBIT / Int.)

1.7

2.4

1.4

(0.0)

1.3

November 6, 2015

11

Tata Steel | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Tata Steel

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 6, 2015

12