3QFY2016 Result Update | Automobile

February 1, 2016

TVS Motor Company

ACCUMULATE

CMP

`295

Performance Highlights

Target Price

`322

Y/E Mar. (` cr) - Standalone 3QFY16 3QFY15

% chg (yoy) 2QFY16

% chg (qoq)

Investment Period

12 Months

Net Sales

2,940

2,639

11.4

2,881

2.0

EBITDA

202

160

26.3

212

(4.6)

Stock Info

EBITDA margin (%)

6.9

6.1

80 bp

7.4

(50 bp)

Sector

Automobile

Net Profit

113

90

25.7

116

(2.6)

Market Cap (` cr)

14,032

Source: Company, Angel Research

Net Debt (` cr)

965

In line numbers adjusted for one offs: TVS Motor Company (TVSM)’s 3QFY2016

Beta

0.9

results adjusted for one-off items have come in in line with our estimates.

52 Week High / Low

315/201

Revenues grew 11% yoy to `2,940cr, driven majorly by an 8% yoy growth in

Avg. Daily Volume

236,430

volumes. Market share gains on back of success of new launches enabled TVSM

Face Value (`)

1.0

to post healthy volume growth during the quarter. Realisation/vehicle grew about

BSE Sensex

24,825

3% yoy to `41,868 driven by a better product mix. During the quarter TVSM

Nifty

7,556

reported one-off expenses of `12.4cr (`7.5cr towards damages caused by

Reuters Code

TVSM.BO

Chennai floods and `4.9cr towards increase in bonus expenses retrospectively

Bloomberg Code

TVSL@IN

from April 2015). Adjusted for one-off items, the operating margin came in at

7.3% which is in line with our estimate. The adjusted net profit at `120.7cr was

in line with our estimates.

Shareholding Pattern (%)

Promoters

57.4

Outlook and valuation: The two wheeler industry is expected to recover in

MF / Banks / Indian Fls

15.4

FY2017 on back of implementation of Seventh pay commission and recovery in

FII / NRIs / OCBs

13.4

the rural demand. Also, TVS Motor is likely to continue gaining market share on

Indian Public / Others

13.8

back of new product launches and expanding geographical presence. Further,

the realization/vehicle is likely to improve given the increased proportion of the

non-moped segment. TVSM margins are also likely to improve as volumes pick

Abs. (%)

3m 1yr 3yr

up, given the benefits of operating leverage, gradual reduction in marketing

Sensex

(6.9)

(14.9)

25.5

expenses and reduction in material prices due to better vendor negotiations. We

TVS Motor

11.3

(4.2)

593.3

expect TVS Motor to report revenue and Net profit growth of 16% and 53%

respectively in FY2017. We maintain our positive view on the stock and assign

“Accumulate” rating on the stock with a revised price target of `322 (based on

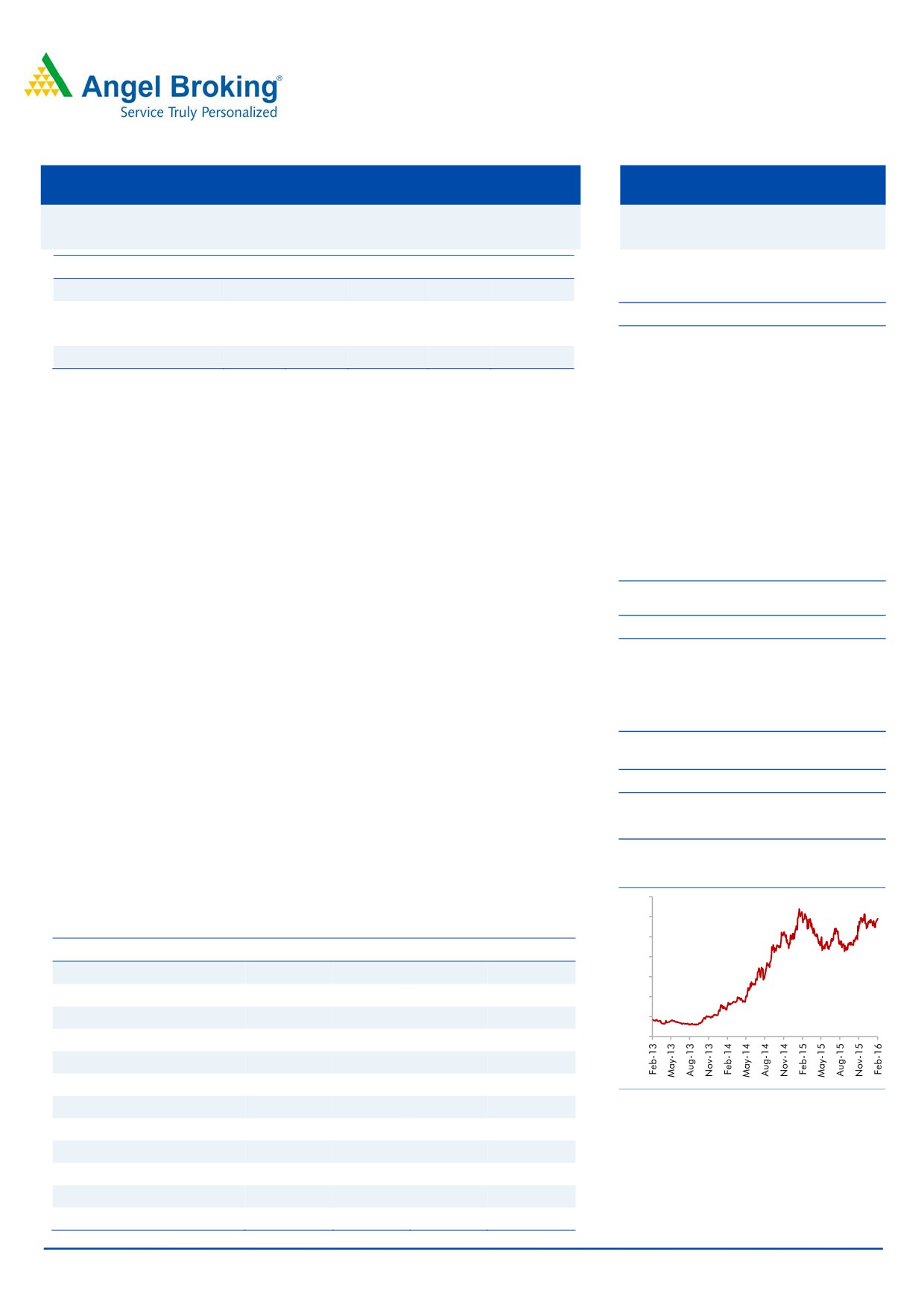

3-year price chart

350

22x FY2017 earnings).

300

Key financials (Standalone)

250

Y/E March (` cr)

FY2014

FY2015 FY2016E

FY2017E

200

Net Sales

7,962

10,069

11,263

13,106

150

% chg

11.1

26.4

11.9

16.4

100

Adj. net Profit

260

356

436

696

50

0

% chg

25.9

35.3

22.3

59.7

EBITDA (%)

6.1

6.1

6.9

8.3

EPS (`)

5.5

7.5

9.2

14.6

Source: Company, Angel Research

P/E (x)

53.2

39.3

32.2

20.1

P/BV (x)

9.9

8.5

7.3

4.8

RoE (%)

18.6

21.7

22.7

29.1

RoCE (%)

13.6

13.7

15.5

20.3

Bharat Gianani

EV/Sales (x)

1.8

1.5

1.3

1.1

022-3935 7800 Ext: 6817

EV/EBITDA (x)

29.9

24.6

19.1

13.5

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

TVS Motor Company | 3QFY2016 Result Update

Exhibit 1: Quarterly financial performance (Standalone)

Y/E March (` cr)

3QFY16

3QFY15

% chg (yoy)

2QFY16

% chg (qoq)

9MFY16 9MFY15

% chg (yoy)

Net Sales

2,940

2,639

11.4

2,881

2.0

8,429

7,612

10.7

Consumption of RM

2,106

1,938

8.7

2,054

2.5

6,048

5,576

8.5

(% of Sales)

71.6

73.4

71.3

71.8

73.3

Staff Costs

169

155

9.1

166

2.0

490

450

9.1

(% of Sales)

5.8

5.9

5.8

5.8

5.9

Other Expenses

463

386

19.8

449

3.1

1,312

1,129

16.2

(% of Sales)

15.7

14.6

15.6

15.6

14.8

Total Expenditure

2,737

2,479

10.4

2,669

2.6

7,851

7,155

9.7

Operating Profit

202

160

26.3

212

(4.6)

578

457

26.4

OPM (%)

6.9

6.1

7.4

6.9

6.0

Interest

10

5

89.0

10

(1.6)

33

15

125.9

Depreciation

49

37

32.9

47

5.8

138

107

28.7

Other Income

12

6

100.0

6

104.9

27

20

33.4

Profit Before Tax

155

124

25.1

161

(3.9)

434

356

22.0

(% of Sales)

5.3

4.7

5.6

5.1

4.7

Provision for Taxation

41

34

23.3

45

(7.1)

114

98

15.7

(% of PBT)

26.7

27.1

27.7

26.2

27.6

Reported PAT

108

90

19.4

116

(7.5)

314

257

22.2

Exceptional items

(6)

-

-

(6)

-

PAT after exceptionals

113

90

25.7

116

(2.6)

320

257

24.4

Adj. PATM

3.9

3.4

4.0

3.8

3.4

Equity capital (cr)

47.5

47.5

-

47.5

-

47.5

47.5

-

Reported EPS (`)

2.3

1.9

19.4

2.5

(7.5)

6.6

5.4

22.2

Adjusted EPS (`)

2.4

1.9

25.7

2.5

(2.6)

6.7

5.4

24.4

Source: Company, Angel Research

Exhibit 2: 3QFY2016 - Actual vs Angel estimates

Y/E March (` cr)

Actual

Estimates

Variation (%)

Net Sales

2,940

2,935

0.2

EBITDA

202

215

(5.9)

EBITDA margin (%)

6.9

7.3

(40 bp)

Net Profit

113

124

(8.5)

Source: Company, Angel Research

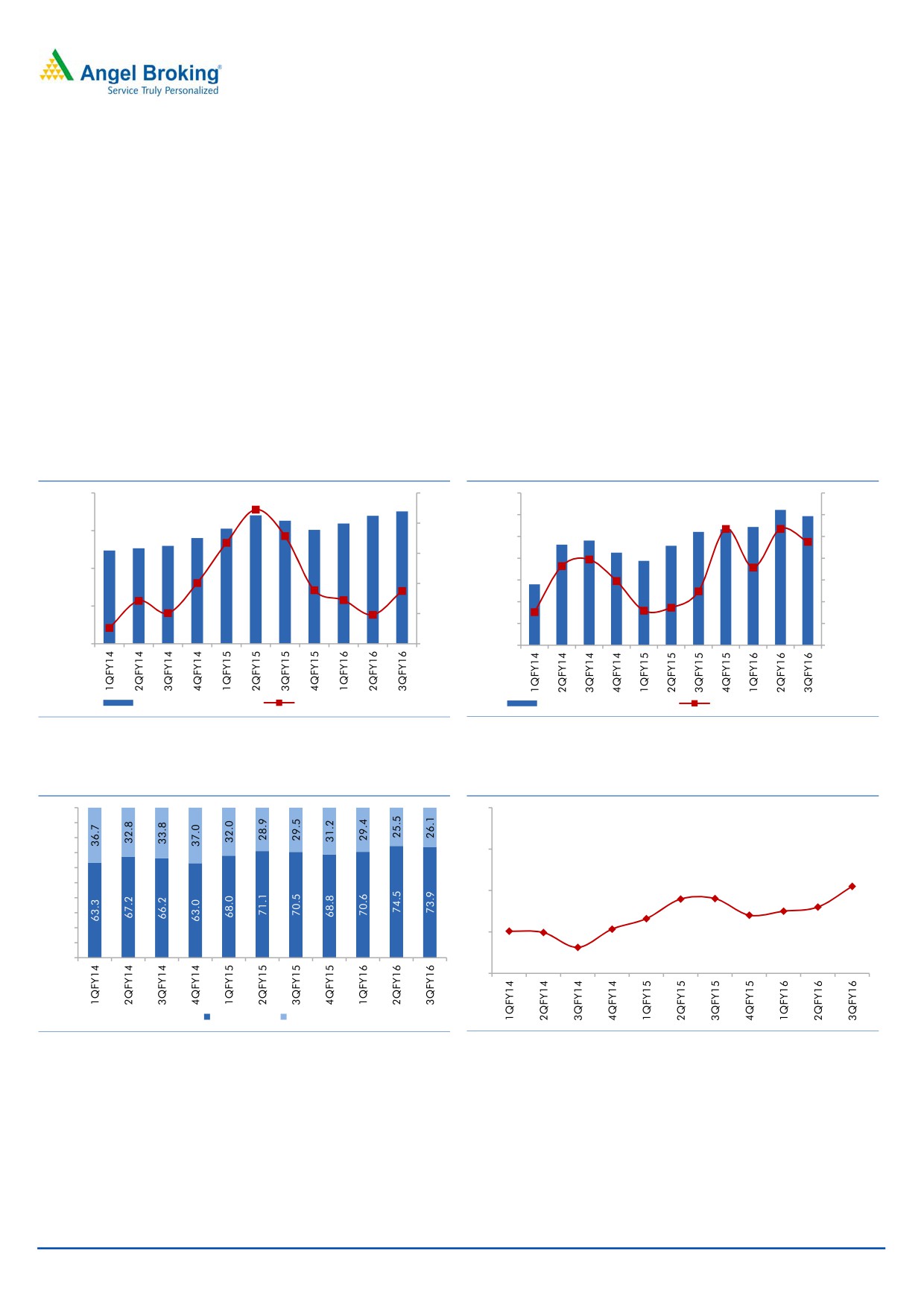

Exhibit 3: Quarterly volume performance

Volumes

3QFY16

3QFY15

yoy%

2QFY16

qoq%

9MFY16

9MFY15

yoy%

Domestic motorcycles

190,195

171,786

10.7

172,713

10.1

538,331

514,806

4.6

Domestic scooters

220,352

181,361

21.5

205,579

7.2

582,906

517,058

12.7

Domestic Mopeds

179,594

190,608

(5.8)

169,554

5.9

532,568

562,990

(5.4)

Domestic two wheelers

590,141

543,755

8.5

547,846

7.7

1,653,805

1,594,854

3.7

Exports two wheelers

85,743

83,778

2.3

97,231

(11.8)

275,042

240,505

14.4

Total two wheelers

675,884

627,533

7.7

645,077

4.8

1,928,847

1,835,359

5.1

Three wheelers

26,225

28,015

(6.4)

32,922

(20.3)

89,376

80,943

10.4

Total volumes

702,109

655,548

7.1

677,999

3.6

2,018,223

1,916,302

5.3

Source: Company, Angel Research

February 1, 2016

2

TVS Motor Company | 3QFY2016 Result Update

TVSM reported a healthy volume growth of 7% yoy in 3QFY2016. Growth was

once again led by the scooter and the motorcycle segments which grew by

22% and 11% yoy, respectively. The moped segment however posted a decline

of 6% yoy, being severely impacted by a hit in rural demand.

Realisation/vehicle grew 4% yoy to `41,868, led by a better product mix and

price hikes. The share of the high realisation non-moped segment in overall

volumes improved to

73% in 9MFY2016 as against

69.9% in the

corresponding period last year. Contribution/vehicle improved by 11% yoy

due to better product mix and soft commodity prices.

TVSM continued to outperform the domestic two-wheeler industry on back of

success of its new launches. In 9MFY2016, TVSM’s market share improved by

30bp yoy to 13.5%.

Exhibit 4: Volumes led by scooters and motorcycles

Exhibit 5: Realisation and contribution/vehicle trend

800,000

40

44,000

13,000

42,000

12,500

30

600,000

40,000

12,000

20

38,000

11,500

400,000

36,000

11,000

10

34,000

10,500

200,000

0

32,000

10,000

0

(10)

30,000

9,500

Overall volumes (LHS)

yoy growth (%) (RHS)

Realisation/vehicle (`)

Contribution/vehicle (`)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 6: Share of non-mopeds rise

Exhibit 7: Domestic market share improves yoy

100%

18

90%

80%

70%

16

60%

14.2

50%

13.6

13.6

14

13.2

40%

12.8

13.0

12.6

30%

12.1

12.0

12.0

20%

12

11.3

10%

0%

10

Non moped Moped

Source: Company, Angel Research

Source: Company, SIAM, Angel Research

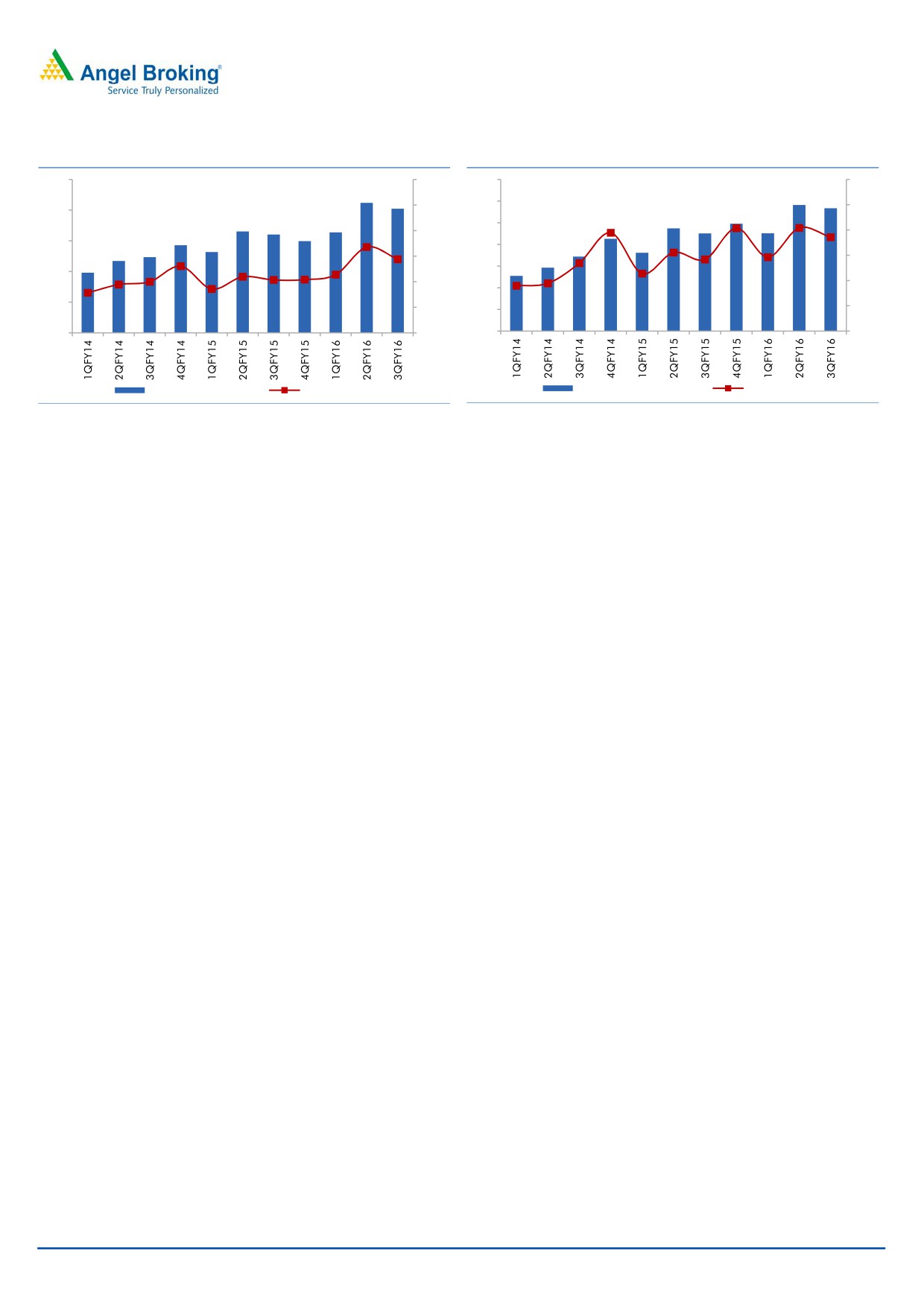

TVSM’s margins, adjusted for net one-off provisions of `12cr, stood at 7.3%.

The margins improved sharply by 120bp yoy, led by improving volumes and

realisation and soft commodity prices.

Adjusting for the one-off items, the net profit at `120.7cr was in line with our

estimates.

February 1, 2016

3

TVS Motor Company | 3QFY2016 Result Update

Exhibit 8: EBITDA margins improve yoy

Exhibit 9: Net profit meets estimates

250

10.0

140

5.0

120

9.0

4.5

200

100

8.0

4.0

150

80

7.0

3.5

60

100

6.0

3.0

40

50

5.0

20

2.5

0

4.0

0

2.0

EBIDTA (` cr) (LHS)

Margin (RHS)

Net Profit (` cr) (LHS)

Margin (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

Conference Call - Key highlights

TVSM expects the two-wheeler industry demand to remain lackluster in the

near term given the weak rural sentiments. Two consecutive years of deficient

rainfall coupled with moderate growth in MSPs have impacted the incomes in

rural areas which account for about 40% of the two-wheeler demand.

For 4QFY2016, TVSM expects the industry to grow in low single digits

(about 3-4%).

TVSM is aiming to continue outpacing the industry growth on back of new

product launches. TVSM recently reintroduced “Victor” motorcycle in the

executive segment where it has relatively weak presence. TVSM is aiming to

reach market share of 16% by the end of FY2016 as against its current market

share of 14%. Further TVSM is aiming to reach 18% market share by the end

of FY2017.

TVSM export volumes have been impacted with the company reporting low

single digit growth of 2% during 3QFY2016 as against healthy double digit

growth in 1HFY2016. Exports have been impacted in the near term given the

lower availability of USD in key markets of Africa which forms about half of

export volumes. Slide in crude prices have led to severe devaluation of the

local African currencies (such as Nigeria) thereby impacting the demand.

TVSM expects the export segment to remain under pressure in the near term

and expects a recovery in the next two to three quarters.

Given the focus on increasing volumes, TVSM has maintained the target of

reaching double-digit operating margins by FY2018. As per the Management,

creation of strong brands would lead to higher volumes and eventually lead to

operating leverage which would drive margins.

In view of demand potential domestically and expected recovery in the export

markets, TVSM is increasing its three-wheeler capacity from 1.5 lakh units to 2

lakh units in the next two quarters.

TVSM Indonesian operations profitability improved with the EBIDTA losses

reducing from 7 mn USD in 2014 to 5 mn USD in 2015. Improved product

mix coupled with cost control measures have led to operational improvement.

TVSM expects commodity prices to remain stable in the near term.

TVSM has guided for an overall capex of `350cr in FY2016.

February 1, 2016

4

TVS Motor Company | 3QFY2016 Result Update

Investment arguments

Success of new launches and increased penetration to help outpace industry

growth: TVS Motor outpaced the domestic two-wheeler industry, reporting a

growth of 20% in FY2015 as against an industry growth of 9%. Success of new

products such as Jupiter, Star City+ and Scooty Zest enabled the company to

gain market share. We believe TVS Motor is well poised to outpace the

industry over FY2015-2017 given the increasing penetration (expansion in

dealer network) and a strong product pipeline. We expect TVS Motor to report

a healthy 10% volume CAGR over the FY2015-2017 period.

Operating margins to improve going ahead: We expect the operating margin

to gradually inch upwards in FY2016 and FY2017, driven by improving

product-mix, operating leverage benefits and raw material cost reduction

efforts. With the company establishing strong brands, TVS Motor has scope to

raise product prices going ahead (TVS Motor’s products are currently priced at

a discount to larger peers such as Hero Motocorp and Honda) which would be

a strong margin driver going ahead. We expect the company’s margin to

improve by ~220bp over the next two years.

Tie-up with BMW positive in the long run: TVS Motor has entered into a long

term co-operation agreement with BMW's motorcycle division, BMW Motorrad,

to develop and produce a new series of motorcycles that will cater to the sub-

500cc segment. As a part of the deal, TVS Motor will invest EUR20mn in the

collaboration, which is expected to introduce a new product in 2016. We see

this as a positive development for TVS Motor and a step in the right direction

as the BMW association will provide technological access to the company. The

tie-up is also expected to help TVS Motor expand its presence in the premium

motorcycle space, where it currently offers the Apache (160cc and 180cc)

series. In the near term though, we believe that this agreement is unlikely to

alter the current positioning of the company in the domestic motorcycle

industry.

Outlook and valuation

The two wheeler industry is expected to recover in FY2017 on back of

implementation of Seventh pay commission and recovery in the rural demand.

Also, TVS Motor is likely to continue gaining market share on back of new product

launches and expanding geographical presence. Further, the realization/vehicle is

likely to improve given the increased proportion of the non-moped segment. TVSM

margins are also likely to improve as volumes pick up, given the benefits of

operating leverage, gradual reduction in marketing expenses and reduction in

material prices due to better vendor negotiations. We expect TVS Motor to report

revenue and Net profit growth of 16% and 53% respectively in FY2017. We

maintain our positive view on the stock and assign “Accumulate” rating on the

stock with a revised price target of `322 (based on 22x FY2017 earnings).

February 1, 2016

5

TVS Motor Company | 3QFY2016 Result Update

Exhibit 10: Key assumptions

Y/E March

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Total volume (units)

2,197,017

2,032,622

2,081,220

2,549,321

2,692,670

3,045,115

Motorcycles

843,114

749,806

793,480

960,602

1,027,844

1,161,464

Scooters

529,316

441,557

476,428

707,537

813,668

935,718

Mopeds

785,942

792,069

729,672

773,220

734,559

808,015

Three-Wheelers

38,645

49,190

81,640

107,962

116,599

139,919

Change yoy (%)

8.1

(7.5)

2.4

22.5

5.6

13.1

Motorcycles

0.8

(11.1)

5.8

21.1

7.0

13.0

Scooters

17.1

(16.6)

7.9

48.5

15.0

15.0

Mopeds

11.7

0.8

(7.9)

6.0

(5.0)

10.0

Three-Wheelers

(3)

27.3

66

32.2

8.0

20.0

Domestic (units)

1,910,551

1,786,994

1,769,037

2,133,477

2,226,924

2,495,536

Exports (units)

286,466

245,628

312,183

415,844

465,745

549,579

Source: Company, Angel Research

Company background

TVS Motor Company, the flagship company of the TVS Group, is the third largest

2W manufacturer in India. The company is present across the motorcycles,

scooters, and mopeds segments, having a market share of ~7%, ~15% and

100%, respectively. The company successfully ventured into the 3W segment in

FY2009 and garnered a market share of 11% as of March 31, 2015. The

company has three manufacturing facilities in India, located at Hosur (Tamil

Nadu), Mysore (Karnataka) and Solan (Himachal Pradesh) with 2W and 3W

capacity of 3mn and 150,000 units, respectively. The company is also the second

largest exporter of two-wheelers in the country.

February 1, 2016

6

TVS Motor Company | 3QFY2016 Result Update

Profit and loss statement (Standalone)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Total operating income

7,142

7,065

7,962

10,098

11,263

13,106

% chg

13.6

(1.1)

11.1

26.8

11.9

16.4

Total expenditure

6,672

6,656

7,484

9,494

10,486

12,012

Net raw material costs

5,261

5,097

5,673

7,297

8,058

9,207

Employee expenses

370

407

476

585

645

735

Others

1,041

1,153

1,335

1,611

1,782

2,070

EBITDA

469

409

478

616

777

1,094

% chg

19.7

(12.9)

16.9

27.8

25.6

40.7

(% of total op. income)

6.6

5.8

6.0

6.1

6.9

8.3

Depreciation & amortization

118

130

132

153

185

201

EBIT

352

279

377

496

635

978

% chg

23.5

(20.8)

24.5

30.2

28.1

54.1

(% of total op. income)

5.0

4.0

4.7

4.9

5.6

7.5

Interest and other charges

57

48

25

27

40

25

Other income

22

25

30

33

42

85

Recurring PBT

316

255

351

468

595

953

% chg

27.6

(19.4)

38.1

31.7

27.0

60.3

Tax

67

48

91

108

159

257

(% of PBT)

21.3

28.9

25.9

23.1

26.7

27.0

Extraordinary income/(exp.)

-

91

1

0

0

0

PAT (reported)

249

117

262

348

436

696

ADJ. PAT

249

208

260

356

436

696

% chg

25.3

(16.5)

25.9

35.3

22.3

59.7

(% of total op. income)

3.5

3.0

3.3

3.5

3.9

5.3

Basic EPS (`)

5.2

2.5

5.5

7.3

9.2

14.6

Adj. EPS (`)

5.2

4.4

5.5

7.5

9.2

14.6

% chg

25.3

(16.5)

25.9

35.3

22.3

59.7

February 1, 2016

7

TVS Motor Company | 3QFY2016 Result Update

Balance sheet statement (Standalone)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015 FY2016E FY2017E

SOURCES OF FUNDS

Equity share capital

48

48

48

48

48

48

Reserves & surplus

1,122

1,177

1,368

1,598

1,868

2,344

Shareholders’ Funds

1,169

1,225

1,415

1,645

1,916

2,391

Total loans

715

546

528

970

930

800

Deferred tax liability

98

93

125

153

153

153

Other long term liabilities

-

-

-

Long term provisions

49

53

53

44

79

92

Total Liabilities

2,031

1,917

2,121

2,812

3,077

3,436

APPLICATION OF FUNDS

Gross block

2,154

2,248

2,472

2,822

3,172

3,522

Less: Acc. depreciation

1,129

1,236

1,347

1,492

1,677

1,877

Net Block

1,026

1,011

1,126

1,330

1,495

1,645

Capital work-in-progress

53

36

48

89

89

89

Investments

931

869

896

1,012

1,112

1,212

Long term loans and adv.

57

73

86

144

113

131

Current assets

1,048

1,130

1,409

2,029

2,257

2,634

Cash

13

17

83

5

30

61

Loans & advances

243

302

364

633

676

786

Other

793

810

962

1,391

1,551

1,786

Current liabilities

1,083

1,202

1,444

1,792

1,989

2,275

Net current assets

(35)

(73)

(35)

237

268

358

Total Assets

2,031

1,917

2,121

2,812

3,077

3,436

February 1, 2016

8

TVS Motor Company | 3QFY2016 Result Update

Cash flow statement (Standalone)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015 FY2016E FY2017E

Profit before tax

316

254

351

468

595

953

Depreciation

118

108

110

146

185

201

Change in working capital

63

83

112

(350)

(6)

(60)

Others

33

(115)

30

(59)

66

(6)

Direct taxes paid

(67)

(48)

(91)

(108)

(159)

(257)

Cash Flow from Operations

441

282

513

97

681

831

(Inc.)/Dec. in fixed assets

(177)

(77)

(236)

(391)

(350)

(350)

(Inc.)/Dec. in investments

(270)

62

(27)

(117)

(100)

(100)

Cash Flow from Investing

(425)

(15)

(263)

(507)

(450)

(450)

Issue of equity

-

-

-

Inc./(Dec.) in loans

(72)

(197)

(107)

443

(40)

(130)

Dividend paid (Incl. Tax)

72

(66)

(77)

(110)

(165)

(220)

Others

(150)

-

-

Cash Flow from Financing

(150)

(263)

(184)

333

(206)

(350)

Inc./(Dec.) in cash

(135)

4

65

(78)

25

31

Opening Cash balances

6

13

17

83

6

30

Closing Cash balances

13

17

83

6

30

61

February 1, 2016

9

TVS Motor Company | 3QFY2016 Result Update

Key ratios

Y/E March

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

56.7

67.8

53.2

39.3

32.2

20.1

P/CEPS

38.3

41.6

35.5

27.5

22.6

15.6

P/BV

12.0

11.4

9.9

8.5

7.3

4.8

Dividend yield (%)

0.5

0.4

0.5

0.7

1.0

1.0

EV/Sales

2.1

2.0

1.8

1.5

1.3

1.1

EV/EBITDA

30.0

35.7

29.9

24.6

19.1

13.5

EV / Total Assets

6.9

7.3

6.8

5.3

4.8

4.3

Per Share Data (`)

EPS (Basic)

5.2

4.4

5.5

7.5

9.2

14.6

EPS (fully diluted)

5.2

4.4

5.5

7.5

9.2

14.6

Cash EPS

7.7

7.1

8.3

10.7

13.1

18.9

DPS

1.3

1.2

1.4

2.0

3.0

4.0

Book Value

24.6

25.8

29.8

34.6

40.3

50.3

Returns (%)

ROCE (Pre-tax)

18.5

12.7

13.6

13.7

15.5

20.3

Angel ROIC (Pre-tax)

17.4

15.2

18.7

17.7

20.8

29.0

ROE

22.9

16.9

18.6

21.7

22.7

29.1

Turnover ratios (x)

Asset Turnover (Gross Block)

3.5

3.2

3.2

3.6

3.6

3.7

Inventory / Sales (days)

29

26

25

30

29

28

Receivables (days)

12

16

15

18

18

18

Payables (days)

54

55

63

61

61

60

WC cycle (ex-cash) (days)

(1)

(13)

(23)

(13)

(14)

(14)

Solvency ratios (x)

Net debt to equity

(0.2)

0.5

0.3

0.6

0.5

0.3

Net debt to EBITDA

(0.5)

1.5

0.9

1.6

1.2

0.7

Interest Coverage (EBIT / Int.)

6.2

6.3

15.0

18.1

15.9

39.1

February 1, 2016

10

TVS Motor Company | 3QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel has received in-principal

approval from SEBI for registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014. Angel or its associates

has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its

associates including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company

covered by Analyst. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of

securities of the company covered by Analyst during the past twelve months. Angel/analyst has not served as an officer, director or

employee of company covered by Analyst and has not been engaged in market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

TVS Motor Company

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

February 1, 2016

11