1QFY2017 Result Update | IT

July 21, 2016

Tata Consultancy Services (TCS)

BUY

CMP

`2,493

Performance highlights

Target Price

`2,867

(` cr)

1QFY17 4QFY16

% chg (qoq) 1QFY16

% chg (yoy)

Investment Period

12 Months

Net revenue

29,305

28,449

3.0

25,668

14.2

Adj. EBITDA

7,065

7,883

(10.4)

6,982

1.2

Stock Info

Adj. EBITDA margin (%)

26.7

27.7

(50)bp

27.2

(50)bp

Sector

IT

Adj. PAT

6,317

6,341

(0.4)

5,709

10.6

Market Cap (` cr)

491,277

Source: Company, Angel Research

Net Debt (` cr)

(14,442)

Beta

0.6

TCS posted a 3.7% sequential growth in USD revenues to US$4,362mn for

52 Week High / Low

2,769/2,119

1QFY2017 (V/s US$4,375mn expected), which was mostly volume led (3.4%

Avg. Daily Volume

71,114

qoq growth). On constant currency (CC) basis, the revenue growth is of 3.1%

Face Value (`)

1

qoq. On the operating front, the EBITDA and EBIT margins came in at 26.7%

BSE Sensex

27,916

and 25.1%, a dip of ~97bp and ~98bp qoq respectively, which is mostly in line

Nifty

8,566

with our expectations. Consequently, the PAT came in at `6,317cr (V/s `6,151cr

expected), a de-growth of 0.4% qoq. We maintain our Buy on the stock.

Reuters Code

TCS.BO

Bloomberg Code

TCS@IN

Quarterly highlights: The company posted a 3.7% sequential growth in USD

revenues to US$4,362mn for 1QFY2017 (V/s US$4,375mn expected), which

was mostly volume led (3.4% qoq growth). On constant currency (CC) basis, the

Shareholding Pattern (%)

revenue growth is of 3.1% qoq. In terms of geography, USA posted a CC qoq

Promoters

73.3

growth of 2.5%, while Latin America posted CC qoq growth of 0.3%. In terms of

MF / Banks / Indian Fls

5.5

verticals, its key industries BFSI, Retail & CPG, and Manufacturing posted a CC

FII / NRIs / OCBs

17.0

qoq growth of 1.7%, 2.7%, and 3.1%, respectively. On the operating front, the

Indian Public / Others

4.2

EBITDA and EBIT margins came in at 26.7% and 25.1%, a dip of ~97bp and

~98bp qoq respectively, which is mostly in line with our expectations.

Consequently, the PAT came in at `6,317cr (V/s `6,151cr expected), a de-

Abs.(%)

3m 1yr

3yr

growth of 0.4% qoq.

Sensex

8.0

(1.8)

38.5

TCS

1.7

(3.3)

43.1

Outlook and valuation: With headwinds from Diligenta and Latin America

behind, still an uncertain BFSI may mar the company’s growth (although the

same is not currently being encountered). However, even on conservative

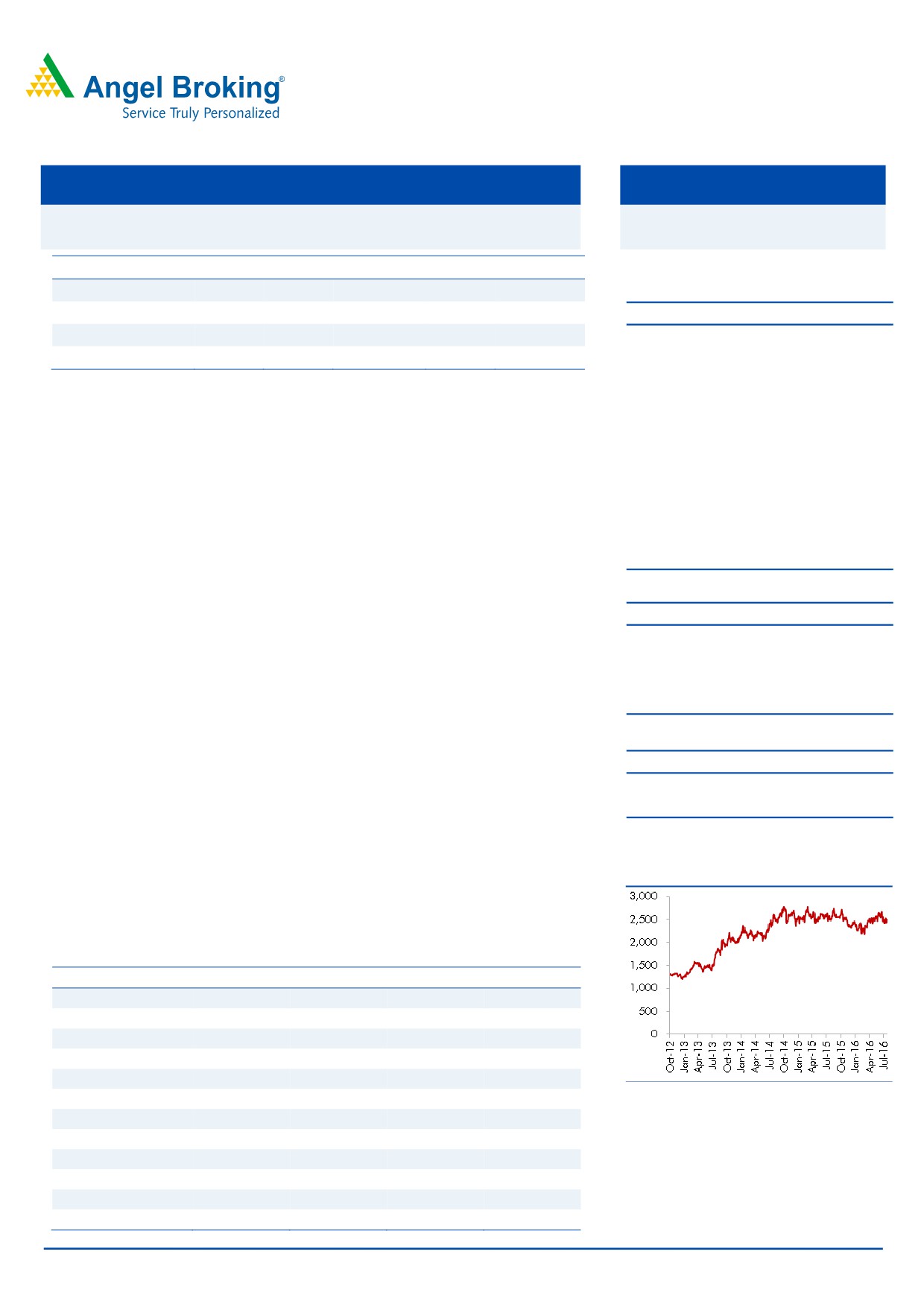

3-Year Daily Price Chart

estimates, we expect TCS to post a revenue CAGR of 12.0% in USD as well as

INR terms over FY2016-18E. The stock trades at 16.6x its FY2018E EPS, which is

attractive.

Key financials (Consolidated, IFRS)

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

Net sales

94,648

1,08,646

1,21,684

1,36,286

% chg

15.7

14.8

12.0

12.0

Net profit

21,696

24,215

26,432

29,369

% chg

13.5

11.6

9.2

11.1

EBITDA margin (%)

28.2

28.3

27.3

27.3

EPS (`)

110.9

123.7

135.0

150.1

Source: Company, Angel Research

P/E (x)

22.5

20.2

18.5

16.6

P/BV (x)

8.5

6.7

6.1

5.6

RoE (%)

34.2

33.1

33.2

33.9

RoCE (%)

33.9

31.6

26.9

27.5

Sarabjit kour Nangra

EV/Sales (x)

4.9

4.2

3.6

3.2

+91 22 3935 7800 Ext: 6806

EV/EBITDA (x)

17.3

14.9

13.2

11.5

sarabjit @angelbroking.com

Source: Company, Angel Research; Note: CMP as of July 20, 2016

Please refer to important disclosures at the end of this report

1

TCS | 1QFY2017 Result Update

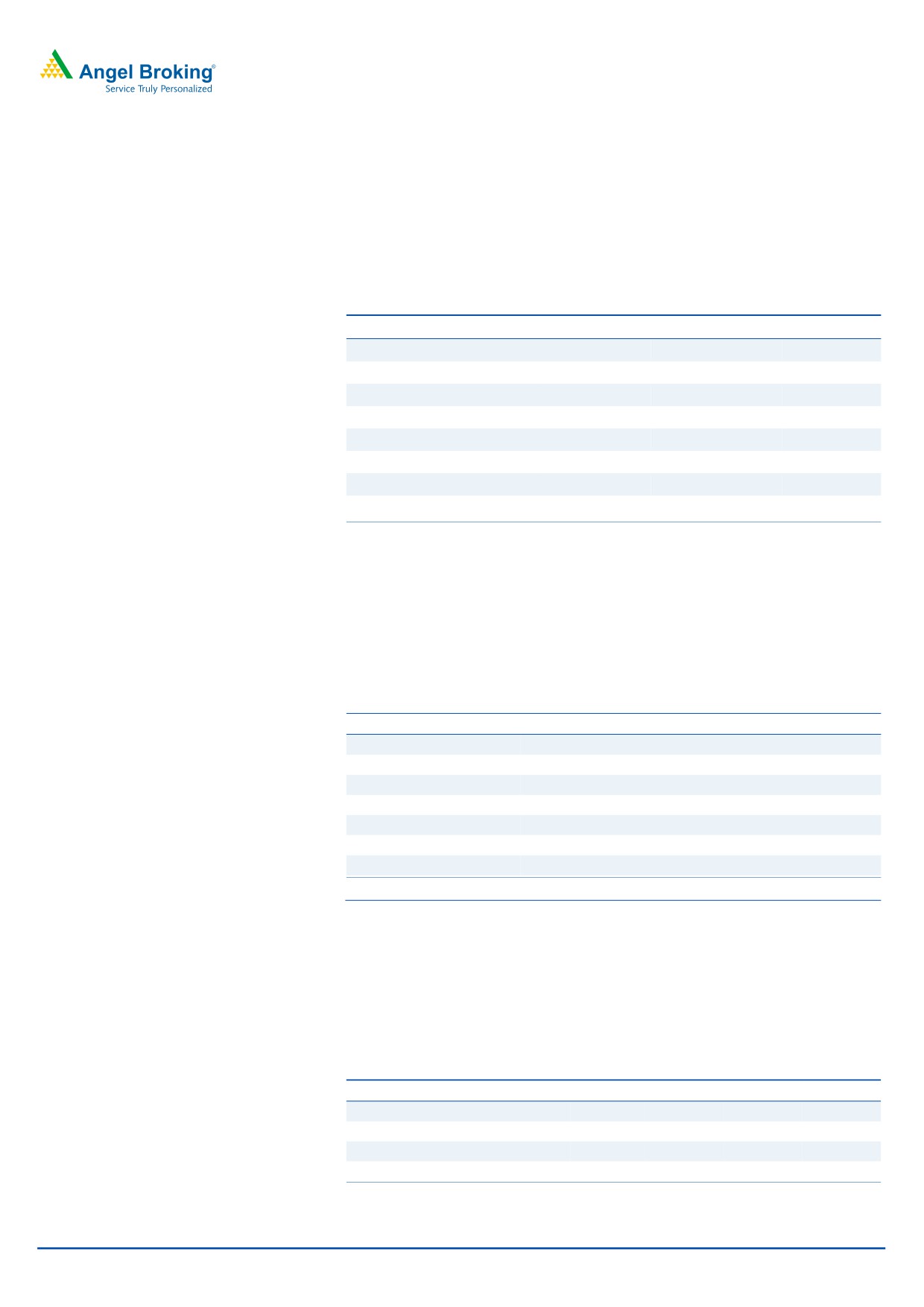

Exhibit 1: 1QFY2017 performance (Consolidated, IFRS)

(` cr)

1QFY17

4QFY16

% chg (qoq)

1QFY16

% chg (yoy)

FY2016

FY2015

% chg(yoy)

Net revenue

29,305

28,449

3.0

25,668

14.2

1,08,646

94,648

14.8

Cost of revenue

16,312

15,592

4.6

13,984

16.6

59,459

53,227

11.7

Gross profit

12,993

12,857

1.1

11,684

11.2

49,187

41,421

18.7

SG&A expense

5,156

4,975

3.6

4,452

15.8

18,956

17,353

9.2

EBITDA

7,837

7,883

(0.6)

7,232

8.4

30,231

24,068

25.6

Dep. and amortisation

490

471

4.1

484

1.2

1,441

1,272

13.3

EBIT

7,347

7,412

(0.9)

6,748

8.9

28,790

22,796

26.3

Other income

963

905

6.4

771

24.9

3,050

3,140

PBT

8,310

8,317

(0.1)

7,519

10.5

31,840

25,936

22.8

Income tax

1,992

1,970

1,747

14.0

7,503

6,083

23.3

PAT

6,318

6,347

(0.5)

5,772

9.5

24,338

19,853

22.6

Earnings in affiliates

-

-

-

-

-

-

-

-

Minority interest

1

6

(82.1)

64

(98.4)

123

205

(40.1)

Reported PAT

6,317

6,341

(0.4)

5,709

10.6

24,215

19,648

23.2

Adj. PAT

6,317

6,341

(0.4)

5,709

10.6

24,215

21,696

11.6

EPS

32.1

32.2

(0.4)

29.1

10.2

123.2

110.8

11.2

Gross margin (%)

44.3

45.2

(86)bp

45.5

(118)bp

45.3

43.8

151bp

EBITDA margin (%)

26.7

27.7

(97)bp

28.2

(143)bp

27.8

25.4

240bp

EBIT margin (%)

25.1

26.1

(98)bp

26.3

(122)bp

26.5

24.1

241bp

Source: Company, Angel Research

Exhibit 2: Actual vs Angel estimates

(` cr)

Actual

Estimate

Var. (%)

Net revenue

29,305

29,362

(0.2)

EBIT margin (%)

25.1

25.1

1.1bps

Adj. PAT

6,317

6,151

2.7

Source: Company, Angel Research

Numbers mostly in line of expectations

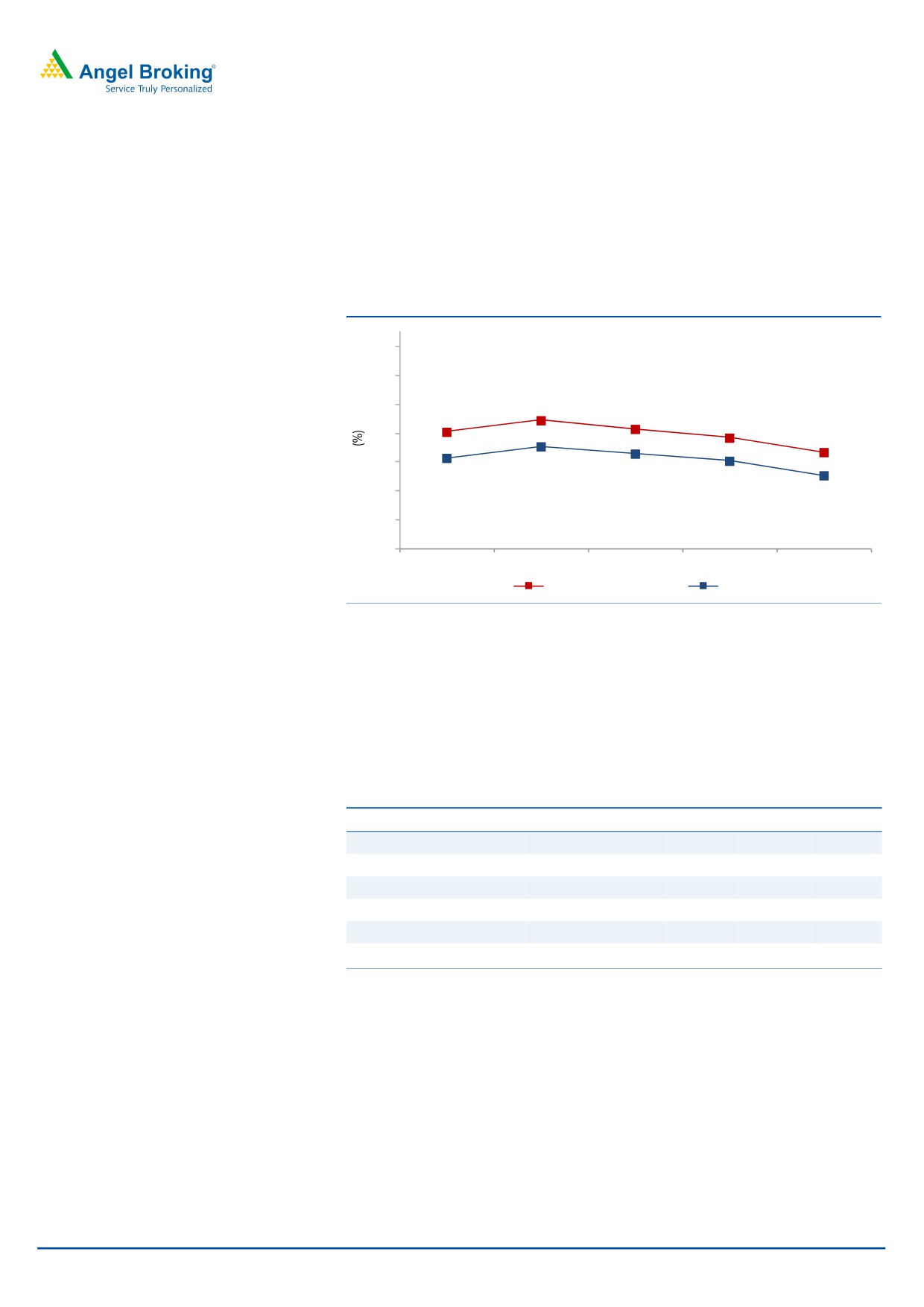

TCS posted sales in line of expectations for the quarter, while it outperformed on

the net profit front on back of higher than expected EBIT and other income. The

company posted a 3.7% sequential growth in USD revenues to US$4,362mn (V/s

US$4,375mn expected), which was mostly volume led (3.4% qoq growth). On CC

basis, the company posted a revenue growth of 3.1% qoq; while in INR terms

revenues grew 3.0% qoq to `29,305cr (V/s `29,362cr expected).

In terms of geography, USA and Latin America grew 2.5% qoq and 0.3% qoq

(CC), respectively. In Europe - UK grew 3.8% qoq (CC) while Continental Europe

grew 4.6% qoq (CC). India posted an 8.5% CC qoq growth.

In terms of verticals, BFSI posted a CC qoq growth of 1.7%, Retail & CPG posted a

CC qoq growth of 2.7%, Communication & Media posted a CC qoq growth of

7.0%, Manufacturing posted a CC qoq growth of 3.1%, Life Sciences & Healthcare

posted a CC qoq growth of 3.9%, Energy & Utilities posted a CC qoq growth of

7.4%, Travel & Hospitality posted a CC qoq growth of 8.6% and Hi-Tech posted a

CC qoq de-growth of 0.3%.

July 21, 2016

2

TCS | 1QFY2017 Result Update

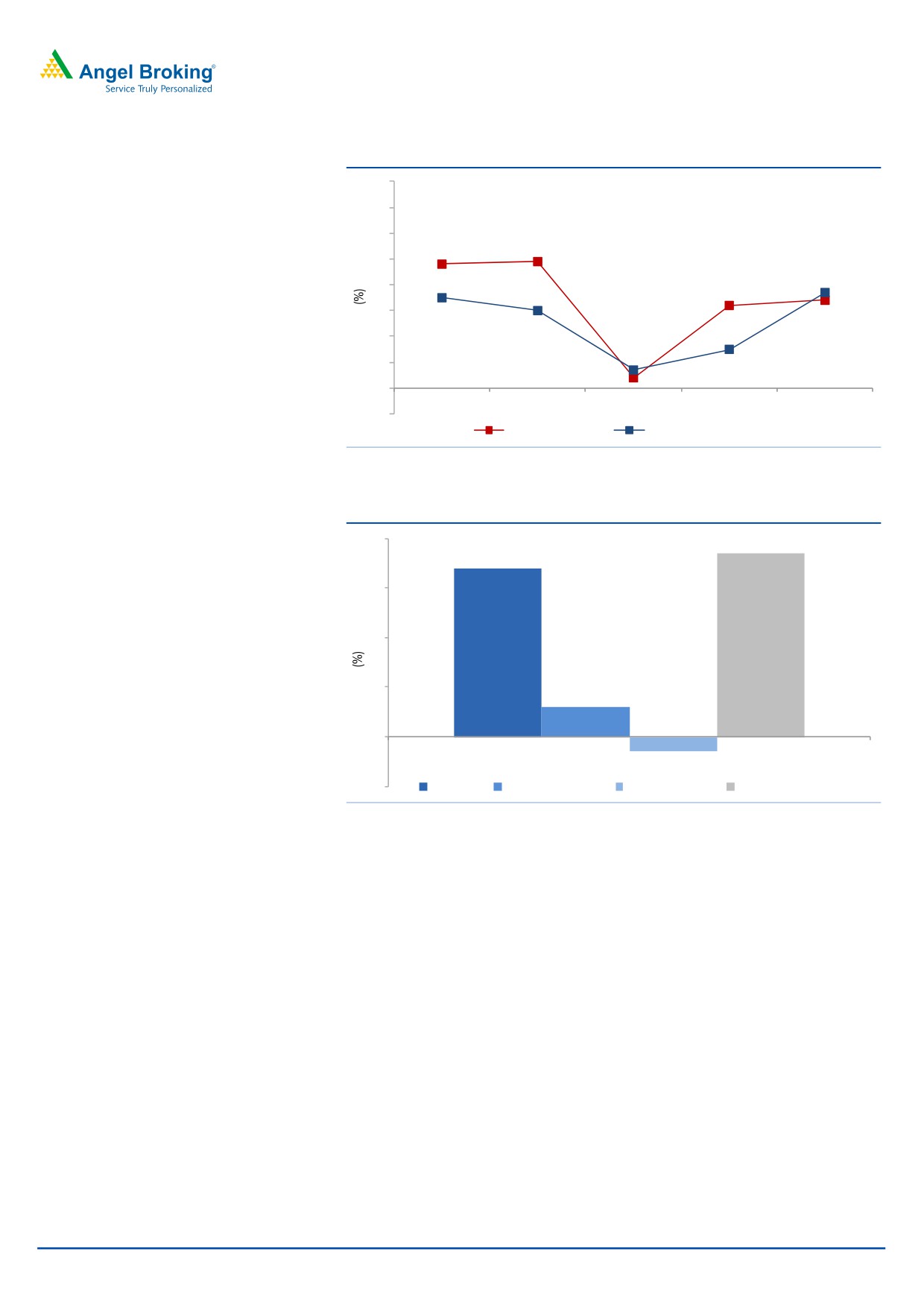

Exhibit 3: Trend in volume and revenue growth (qoq)

8

7

6

4.8

4.9

5

3.7

4

3.2

3

3.5

3.4

3.0

2

0.7

1

1.5

0.4

0

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

(1)

Volume growth

Revenue growth (USD terms)

Source: Company, Angel Research

Exhibit 4: Revenue drivers for 4QFY2016

4

3.7

3.4

3

2

1

0.6

0

(0.3)

(1)

Volume

Currency impact

CC realization

Total revenue growth

Source: Company, Angel Research

BFSI growth lagged remaining business, owing to an uncertain macro

environment; the company expressed that the potential ramifications of the Brexit

on BFSI are still not totally clear. Digital continued showing strength as it grew by

6.4% qoq to US$694mn and accounted for 15.9% of total revenue during the

quarter.

July 21, 2016

3

TCS | 1QFY2017 Result Update

Exhibit 5: Revenue growth (Industry wise on CC basis)

% to revenue

% chg (CC qoq)

% chg (yoy)

BFSI

40.4

1.7

10.1

Manufacturing

10.4

3.1

13.9

Telecom & Media

11.3

7.0

13.0

Life sciences and healthcare

7.3

3.9

15.6

Retail and distribution

14.0

2.7

11.1

Transportation & Hospitality

3.9

8.6

21.0

Energy and utilities

4.2

7.4

19.3

Hi-tech

5.4

(0.3)

(0.2)

Others

3.1

3.0

(20.7)

Source: Company, Angel Research

July 21, 2016

4

TCS | 1QFY2017 Result Update

Service line wise, Infrastructure Services reported a sequential growth of 5.4% on

CC basis. In the company’s anchor service line - IT Solutions and Services - ADM

grew 0.4% qoq on CC basis, and Enterprise Solutions and Assurance Services

grew by 6.7% qoq and 3.2% qoq on a CC basis. The BPO segment grew by 2.8%

qoq on a CC basis during the quarter. Asset Leveraged Solutions (3.2% of sales)

grew by 2.5% qoq on CC basis.

Exhibit 6: Revenue growth (Service wise on CC basis)

% to revenue

% chg (CC qoq)

% chg (yoy)

IT solutions and services

ADM

38.5

0.4

4.9

Enterprise solutions

17.7

6.7

8.1

Assurance services

8.8

3.2

14.8

Engg. and industrial services

4.8

7.0

18.4

Infrastructure services

15.5

5.4

15.4

Asset-leveraged solutions

3.2

2.5

42.4

BPO

11.5

2.8

11.2

Source: Company, Angel Research

Geography wise, growth in INR sales in key geographies was as follows: - USA

(2.5% qoq on CC basis), Latin America (0.3% qoq on CC basis), Continental

Europe (3.8% qoq on CC basis), India (8.5% qoq on CC basis) and MEA (3.3%

qoq on CC basis). The UK and Asia Pacific posted a growth of

3.8% qoq and 1.3% qoq on CC basis, respectively.

Exhibit 7: Revenue growth (Geography wise in INR terms)

% of revenue

% chg (CC qoq)

% chg (yoy)

U.S.

53.5

2.5

9.7

Latin America

2.0

0.3

24.3

U.K.

14.8

3.8

7.4

Continental Europe

11.5

4.6

12.9

India

6.2

8.5

11.6

Asia Pacific

9.6

1.3

7.7

MEA

2.4

3.3

20.0

Source: Company, Angel Research

Attrition rate declines

In 1QFY2017, TCS witnessed a gross addition of 17,792 employees and net

addition of 8,236 employees, taking its total employee base to 3,62,079. During

the quarter, the attrition rate (last twelve month [LTM] basis) for the company

decreased to 13.6% from 14.7% in 4QFY2016.

Exhibit 8: Hiring and attrition trend

Particulars

1QFY16 2QFY16

3QFY16

4QFY16

1QFY17

Gross addition

25,186

25,186

22,118

22,576

17,792

Net addition

5,279

10,685

9,071

9,152

8,236

Total employee base

3,24,935

3,35,620

3,44,691

3,53,843

3,62,079

Attrition (%) - LTM basis

15.9

16.2

15.9

14.7

13.6

Source: Company, Angel Research

July 21, 2016

5

TCS | 1QFY2017 Result Update

Margin dips

On the operating front, the EBITDA and EBIT margins came in at 26.7% and

25.1% a dip of ~97bp and ~98bp qoq respectively, which is more or less in line

with our expectations. Margins breakup for the quarter was as follows - wage hikes

(-200bp), currency movement (-20bp) and others (+120bp).

Exhibit 9: Adj. Margin profile

34

32

30

28.9

28.1

28.3

27.7

28

26.7

26

27.1

26.6

26.3

26.1

24

25.1

22

20

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

EBITDA margin

EBIT margin

Source: Company, Angel Research

Client metrics

The client pyramid during the quarter witnessed a qualitative improvement with

client additions seen in higher revenue brackets. The clients in $50mn+ revenue

band increased by 4, in $20mn+ revenue band by 2 and in $5mn+ revenue

band by 10.

Exhibit 10: Client pyramid

1QFY16 2QFY16 3QFY16 4QFY16 1QFY17

US$1mn-5mn

391

415

425

400

408

US$5mn-10mn

123

130

132

131

141

US$10mn-20mn

96

103

108

125

119

US$20mn-50mn

103

106

108

100

102

US$50mn-100mn

39

32

31

36

40

US$100mn plus

30

33

34

37

37

Source: Company, Angel Research

July 21, 2016

6

TCS | 1QFY2017 Result Update

Investment Argument

Guidance - Outlook unchanged: The Management refrained from giving any

additional color on FY2017E revenue growth outlook, but expects FY2017 to be

better than FY2016 as most of the headwinds (like Diligenta and Japan’s

underperformance) that were effecting the company’s growth in FY2016, seem to

be diminishing. However uncertainty on back of the Brexit and its impact could

impair growth in the near term, though the Management expects ramp up in deal

execution. We expect the company to post a US$ revenue CAGR of 12.0% over

FY2016-18E.

Deal pipeline outlook healthier: The company has given a positive outlook for

FY2017. It expects a strong demand environment across the board in most areas

that it focuses on. TCS, post 4QFY2016, is in a much better position relative to the

end of FY2015. The key reasons behind the same are - dramatic acceleration in

the adoption of digital technologies; good resilience and strong momentum in

BFSI, North America and Continental Europe; major headwinds of Diligenta,

Insurance vertical, Japan and Latin America are now behind; strong order book

and pipeline; and robust growth in platforms.

Outlook and valuation

Over FY2016-18E, we expect TCS’ revenue to post a CAGR of 12.0% in

USD and INR terms. The company highlighted that it stands comfortable of

sustaining the EBIT margin in the range of

26-28%. On the

EBIT and PAT fronts, we expect the company to post an 11.1% and 10.1% CAGR

over FY2016-18E, respectively. The stock is trading at 16.6x FY2018E EPS of

`150. We maintain our Buy rating on the stock with a target price of `2,867.

Exhibit 11: Key assumptions

FY2017E

FY2018E

Revenue growth (USD)

12.0

12.0

USD-INR rate (realized)

65.7

65.7

Revenue growth (`)

12.0

12.0

EBITDA margin (%)

27.3

27.3

Tax rate (%)

23.5

23.5

EPS growth (%)

9.2

11.1

Source: Company, Angel Research

July 21, 2016

7

TCS | 1QFY2017 Result Update

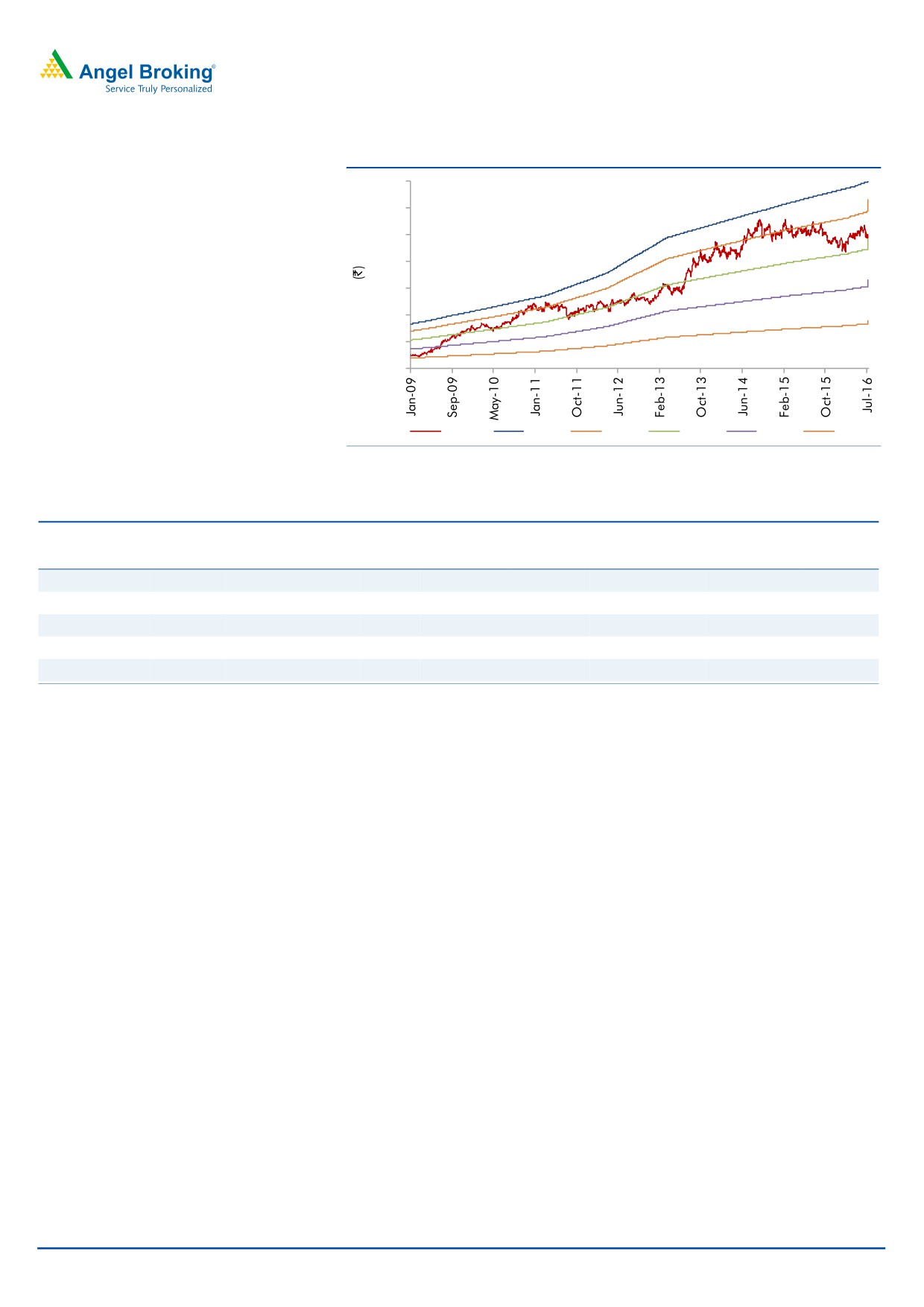

Exhibit 12: One-year forward PE chart

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Price

25x

21x

16x

11x

6x

Source: Company, Angel Research

Exhibit 13: Recommendation summary

Company

Reco

CMP Tgt. price Upside

FY2018E FY2018E

FY2016-18E

FY2018E FY2018E

(`)

(`)

(%)

EBITDA (%)

P/E (x)

EPS CAGR (%)

EV/Sales (x)

RoE (%)

HCL Tech

Buy

729

1,000

37.2

20.5

11.4

9.6

1.2

17.9

Infosys

Buy

1,083

1,370

26.5

27.5

15.0

10.4

2.6

22.3

TCS

Buy

2,493

2,867

15.0

27.3

16.6

10.1

3.2

33.9

Tech Mahindra

Buy

505

700

38.6

17.0

12.2

13.2

1.2

20.7

Wipro

Buy

539

680

26.1

23.8

11.8

9.9

1.5

19.6

Source: Company, Angel Research

July 21, 2016

8

TCS | 1QFY2017 Result Update

Company background

TCS is Asia's largest IT services provider and is amongst the top 10 technology

firms in the world. The company has a global footprint with an employee base of

over 3.0 lakh professionals, offering services to more than 1,000 clients across

various industry segments. The company has one of the widest portfolios of

services offerings, spanning across the entire IT service value chain - from

traditional application development and maintenance to consulting and package

implementation to products and platforms.

July 21, 2016

9

TCS | 1QFY2017 Result Update

Profit & Loss statement (Consolidated, IFRS)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E FY2018E

Net sales

81,809

94,648

1,08,646

1,21,684

1,36,286

Cost of revenue

42,207

50,599

58,952

65,709

73,594

Gross profit

39,603

44,049

49,695

55,975

62,691

% of net sales

48.4

46.5

45.7

46.0

46.0

SGA expenses

14,471

17,353

18,956

22,755

25,485

% of net sales

17.7

18.3

17.4

18.7

18.7

EBITDA

25,132

26,696

30,738

33,220

37,206

% of net sales

30.7

28.2

28.3

27.3

27.3

Dep. and amortization

1324

1272

1948

1535

1655

% of net sales

1.6

1.3

1.8

1.3

1.2

EBIT

23,808

25,424

28,790

31,685

35,551

% of net sales

29.1

26.9

26.5

26.0

26.1

Other income, net

1589

3140

3050

3050

3050

Profit before tax

25,397

28,564

31,840

34,735

38,601

Provision for tax

6,071

6,083

7,503

8,163

9,071

% of PBT

23.9

21.3

23.6

23.5

23.5

PAT

19,326

22,481

24,338

26,572

29,530

Minority interest

209

205

123

141

161

Extra-ordinary (Exp.)/ Inc.

-2627.9

Reported PAT

19,117

19,648

24,215

26,432

29,369

Adj. PAT

19,117

21,696

24,215

26,432

29,369

Diluted EPS (`)

97.6

110.9

123.7

135.0

150.1

July 21, 2016

10

TCS | 1QFY2017 Result Update

Balance sheet (Consolidated, IFRS)

Y/E March (` cr)

FY2014 FY2015

FY2016 FY2017E FY2018E

Assets

Cash and cash equivalents

1,469

1,862

1,862

1,267.2

939.0

Other current financial assets

18,107

16,383

4,833

27,366

35,229

Accounts receivable

18,230

20,440

24,073

26,272

29,424

Unbilled revenues

4,006

3,827

3,992

5,347

5,348

Other current assets

-

6,414

5,975

5,975

5,975

Property and equipment

10,364

11,572

11,790

12,790

13,790

Intangible assets and goodwill

4,157

3,931

3,946

3,946

3,946

Investments

3,449

9,619

22,822

22,822

22,822

Other non current assets

-

906

11,919

11,919

11,919

Total assets

68,913

74,954

91,212

1,17,704

1,29,393

Liabilities

Current liabilities

10,906

14,428

15,407

35,112

39,325

Short term borrowings

170

243

162

162

162

Redeemable preference shares

-

-

(0)

-

1

Long term debt

127

114

83

83

83

Other non current liabilities

1,684

1,778

2,017

2,333

2,613

Minority interest

691

914

354

495

656

Shareholders funds

55,335

57,477

73,190

79,520

86,554

Total liabilities

68,913

74,954

91,212

1,17,704

1,29,393

July 21, 2016

11

TCS | 1QFY2017 Result Update

Cash flow statement (Consolidated, IFRS)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E

FY2018E

Pre-tax profit from oper.

23,808

22,481

24,338

26,572

29,530

Depreciation

1,324

1,272

1,948

1,535

1,655

Exp. (deferred)/written off

209

160

174

-

-

Pre tax cash from oper

24,923

23,913

26,460

28,107

31,185

Other inc./prior period ad

1,589

1,272

1,948

1,535

1,655

Net cash from operations

26,512

25,185

28,408

29,642

32,840

Tax

6,071

6,083

7,503

8,163

9,071

Cash profits

20,441

19,102

20,905

21,479

23,768

(Inc)/dec in acc. recv.

(4,154)

(2,210)

(3,633)

(2,199)

(3,153)

(Inc)/dec in unbilled rev.

(846)

179

(165)

(1,355)

(1)

(Inc)/dec in oth. current asst.

(6,650)

(6,414)

439

-

-

Inc/(dec) in current liab.

2,223

(1,207)

(218)

(1,000)

(1,000)

Net trade working capital

(9,427)

(9,652)

(3,577)

(4,554)

(4,154)

Cash flow from opert. actv.

11,015

9,450

17,328

16,925

19,615

(Inc)/dec in fixed assets

(3,494)

(1,207)

(218)

(1,000)

(1,000)

(Inc)/dec in investments

(1,409)

(4,446)

(1,653)

(22,533)

(7,863)

(Inc)/dec in intangible asst.

(651)

(226)

16

-

-

(Inc)/dec in non-cur.asst.

(1,335)

(906)

(11,013)

-

-

Cash flow from invt. actv.

(6,889)

(6,786)

(12,869)

(23,533)

(8,863)

Inc/(dec) in debt

203

61

(113)

-

-

Inc/(dec) in equity

34

223

(559)

141

161

Inc/(dec) in minority int.

(14,666)

(19,923)

(18,415)

(20,101)

(22,335)

Dividends

9,929

17,369

14,629

26,622

11,989

Cash flow from finan. actv.

(4,500)

(2,271)

(4,459)

6,661

(10,185)

Cash generated/(utilized)

(374)

393

-

(595)

(328)

Cash at start of the year

1,843

1,469

1,862

1,862

1,267

Cash at end of the year

1,469

1,862

1,862

1,267

939

July 21, 2016

12

TCS | 1QFY2017 Result Update

Key ratios

Y/E March

FY2014

FY2015

FY2016

FY2017E

FY2018E

Valuation ratio(x)

P/E (on FDEPS)

25.5

22.5

20.2

18.5

16.6

P/CEPS

23.9

23.3

18.7

17.5

15.7

P/BVPS

8.8

8.5

6.7

6.1

5.6

Dividend yield (%)

1.3

1.7

1.6

1.8

2.0

EV/Sales

5.7

4.9

4.2

3.6

3.2

EV/EBITDA

18.5

17.3

14.9

13.2

11.5

EV/Total assets

6.8

6.1

5.0

3.7

3.3

Per share data (`)

EPS

97.6

110.9

123.7

135.0

150.1

Cash EPS

104.4

106.8

133.6

142.8

158.4

Dividend

32.0

43.5

40.2

43.9

48.7

Book value

283

294

374

406

442

Dupont analysis

Tax retention ratio (PAT/PBT)

0.8

0.8

0.8

0.8

0.8

Cost of debt (PBT/EBIT)

1.1

1.1

1.1

1.1

1.1

EBIT margin (EBIT/Sales)

0.3

0.3

0.3

0.3

0.3

Asset turnover ratio (Sales/Assets)

1.2

1.3

1.2

1.0

1.1

Leverage ratio (Assets/Equity)

1.2

1.3

1.2

1.5

1.5

Operating ROE

34.9

39.1

33.3

33.4

34.1

Return ratios (%)

RoCE (pre-tax)

34.5

33.9

31.6

26.9

27.5

Angel RoIC

51.9

54.0

46.7

47.8

50.5

RoE

34.5

34.2

33.1

33.2

33.9

Turnover ratios(x)

Asset turnover (fixed assets)

7.9

8.2

9.2

9.5

9.9

Receivables days

81

79

81

79

79

July 21, 2016

13

TCS | 1QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

TCS

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

July 21, 2016

14