Initiating coverage | Cons. Durable

April 29, 2015

Surya Roshni

BUY

CMP

`109

Initiating Coverage - A Brighter Future

Target Price

`149

Surya Roshni Ltd is a 38 year old conglomerate with its core business comprising

Investment Period

12 Months

of lighting and steel tube products. The Lighting business has superior profitability

than the latter and the company is among the largest players in the lighting

Stock Info

industry with a market share in excess of 25%. The company has a pan India

Sector

Cons. Durable

presence spanning a network of ~2 lakh retailers. Although the Steel business is

expected to grow at a muted pace, the division will perform well owing to

Market Cap (` cr)

480

increased spend on Infra projects and with government initiatives like building

Beta

1.5

smart cities across India.

52 Week High / Low

81/143

Structural shift in the Lighting industry presents new growth opportunity: The

Avg. Daily Volume

96,896

Lighting business is primed for a good performance owing to the structural shift in

Face Value (`)

10.00

the industry towards LED (Light Emitting Diodes) lights. Citing cost efficient nature

BSE Sensex

27,226

of LEDs, Electric Lamp and Components Manufacturers Association (ELCOMA)

projects the share of LEDs in the Lighting industry to increase substantially. Major

Nifty

8,230

initiatives like changing all street lights and lights in public spaces to LED lights, by

Reuters Code

SURR.BO

the government, are expected to fuel growth of LEDs. As a result, the lighting

Bloomberg Code

SYR@IN

industry is expected to grow at a CAGR of 22.8% over FY2014-17E to `25,000cr

and reach the `37,000cr mark by FY2021E. This bodes well for the Lighting

division of the company which is likely to contribute more significantly to the

Shareholding Pattern (%)

overall top-line, mainly due to its vast retail presence. We expect the Lighting

Promoters

64.0

business’ revenues to grow at a CAGR of 13.1% over FY2015E-17E to `1,400cr

MF / Banks / Indian Fls

0.1

and this will have a favourable impact on the overall margins due to better

profitability of the business.

FII / NRIs / OCBs

0.0

Indian Public / Others

35.9

Exploring newer avenues: Thanks to its strong network of retailers, the Fan

business (which was launched in January 2014) has received a good response in

a relatively shorter period of time; clocking revenues of ~`60cr in FY2015.

Encouraged by the good response, the company has entered the Home

Abs. (%)

3m 1yr

3yr

Appliances business and will also be venturing into the business of providing solar

Sensex

(7.3)

21.1

59.4

based lighting systems for rural and urban use. Leveraging upon its strong

Surya Roshni

(14.8)

22.1

87.9

network, we expect the company to successfully scale up its new ventures.

Outlook and Valuation: With higher contribution from the Lighting business and

entry into newer businesses, we expect the company to post a CAGR of 6.2% in

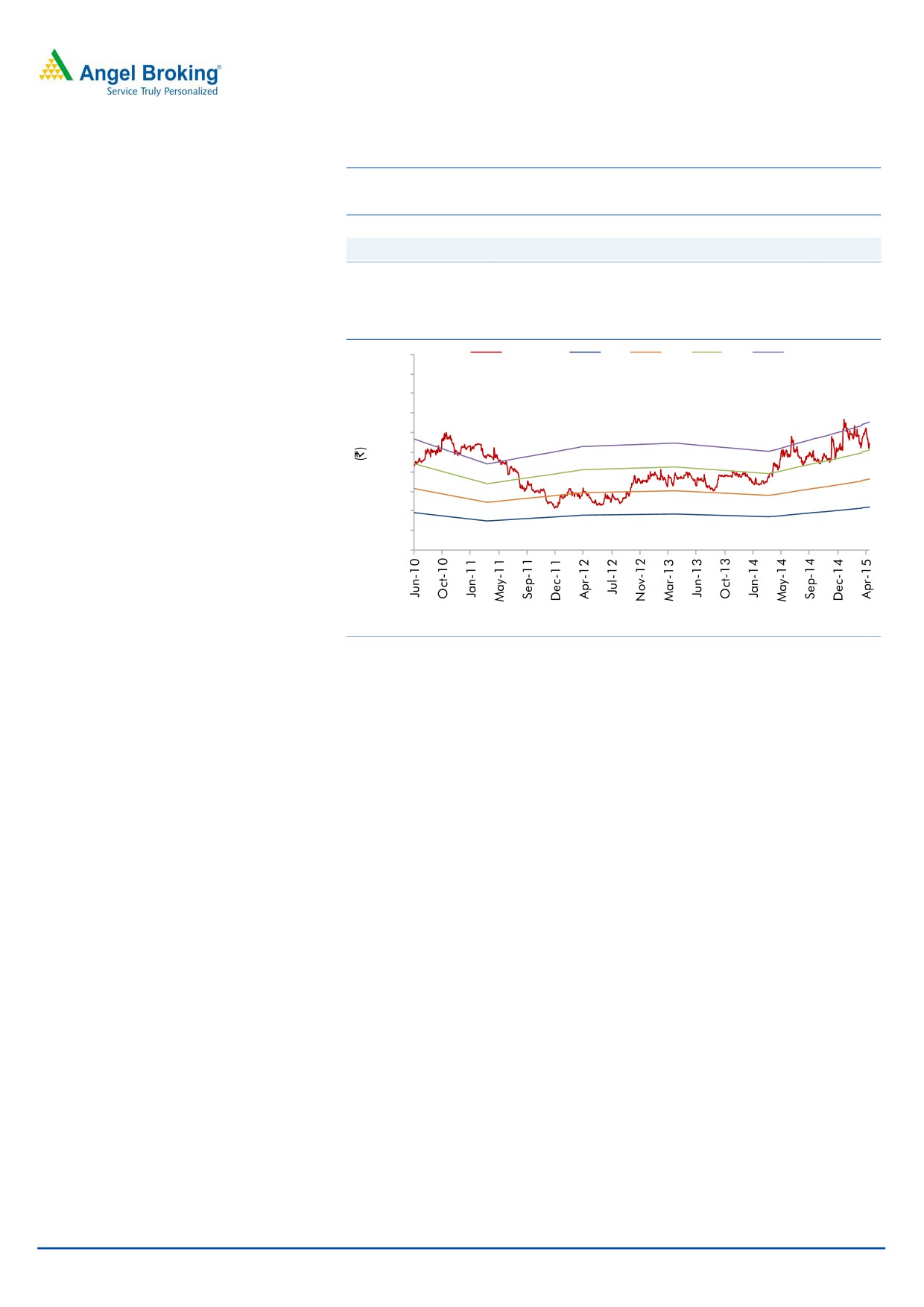

3-year daily price chart

the top-line over FY2015E-17E to `3,216cr. Owing to better margin profile of the

160

Lighting business, the EBITDA margins are estimated to improve from 8.1% in

140

FY2015E to 8.6% in FY2017E. Consequently, the net profit is expected to post a

120

CAGR of 27.7% over FY2015E-17E to `80cr. At the current market price, the

100

80

stock is trading at 6.0x its FY2017E earnings. We initiate coverage on the company

60

with a Buy rating and target price of `149 based on SOTP valuation.

40

20

SOTP Valuation

0

Particulars

Remarks

Exp. Mcap (` cr)

`/Share

Steel Business

3x its FY2017E EBIT (minus `913cr of debt)

(749)

(171)

Lighting Business

9x its FY2017E EBIT

1,405

320

Total

149

Source: Company, Angel Research

Source: Company, Angel Research

Financials

Y/E

Sales OPM PAT

EPS

RoE P/E P/BV EV/BITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2015E

2,853

8.1

49

11.2

8.0

9.8

0.8

5.9

0.5

Milan Desai

FY2016E

2,990

8.3

63

14.3

9.4

7.6

0.7

5.4

0.5

022 4000 3600

FY2017E

3,216

8.6

80

18.3

10.9

6.0

0.6

4.8

0.4

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Initiating coverage | Surya Roshni

Investment Arguments

Structural shift in the Industry presents growth opportunity.

In-line with the industry trend, the company has added a wide range of LED

products to its offering. LED bulbs are a newer innovation in the lighting industry

and they differ in technology from CFL and GLS bulbs. Although cost of initial

purchase is far higher than CFL and GLS bulbs, LEDs prove to be most cost

efficient over the life of the bulb in comparison to the latter two. Below table

highlights the approximate cost savings by switching to LEDs.

Exhibit 1: Comparison (GLS-CFL-LED)

Particulars

GLS

CFL

LED

Average Life Span (Hours)

1,200

8,000

35,000

Watts (equivalent 60 watts)

60

14

8

Cost Per Bulb

20

150

480

Electricity cost (`/kWh) - Residential

3.5

3.5

3.5

Daily Cost (Assuming 5 hours/day)

1.1

0.245

0.14

Bulbs needed for 50k hours

41.7

6.3

1.4

Cost for 50k hours of use

10,500

2,450

1,400

Cost of Bulbs

833

938

686

Total Spend

11,333

3,388

2,086

Source: Company, Angel Research

As per industry reports, there will be a structural shift in the lighting industry

towards LEDs owing to several measures taken by the government like, changing

all street lights and lights in public spaces to LED lights, making all LED

specifications mandatory, and providing free LED lamps instead of CFL bulbs to

below poverty line (BPL) families.

Of the potential drivers for the segment listed above, we believe that switchover to

LED lighting for street and public lighting provides significant opportunity to the

company in the segment. Energy Efficiency Services Ltd (EESL), in its toolkit for

street light energy efficiency, has projected that retrofitting conventional streetlight

with LED could result in potential savings of 4,300mn kWh of energy. As per the

revisited BEE (Bureau of Energy Efficiency) supported project report, there are

269 municipal corporations having 33.65 lakh streetlights, that could be replaced

at an investment of `2,500cr.

April 29, 2015

2

Initiating coverage | Surya Roshni

Exhibit 2: Street light segment opportunities

State and # of Municipalities

Investment (` cr)

No. of Lights

Andhra Pradesh (9)

360.0

3,56,162

Assam (6)

1.9

4,372

Bihar (6)

12.4

11,129

Chattisgarh (4)

32.4

54,811

Haryana (9)

45.9

54,151

Himachal Pradesh (4)

2.0

5,913

Kerala (9)

99.3

1,44,515

Maharashtra (10)

428.3

4,01,303

Madhya Pradesh (13)

120.6

4,01,303

Punjab (6)

8.3

1,16,291

Rajasthan (6)

105.9

1,82,117

Uttar Pradesh (11)

296.5

3,48,332

Uttarakhand (1)

21.2

23,367

West Bengal (17)

294.4

3,99,457

Gujarat (159)

637.9

8,62,000

Total

2,466.8

33,65,223

Source: EESL, BEE, Angel Research

Citing this structural shift, ELCOMA expects LED market size to touch ~`10,500cr

by FY2017E and reach ~`21,630cr by FY2021E. As per the projections, LEDs are

expected to account for ~58% of the total lighting industry.

Exhibit 3: LEDs’ contribution to increase significantly

40

GLS

Others

LED

CFL

FTL

35

30

25

22

20

19

19

15

15

10

8

10

5

2

5

-

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

Source: ELCOMA, Angel Research

Currently, LED revenues for the company for FY2015 are estimated to be at

~`100cr. The Management is upbeat about the prospects and expects LEDs to

contribute ~30% to the company’s Lighting business’ turnover in the next two to

three years, while targeting revenue of ~`500cr from the segment. We believe that

there is a great opportunity for Surya Roshni in the fast growing LED market owing

to shift in preference towards cost efficient lighting solutions.

April 29, 2015

3

Initiating coverage | Surya Roshni

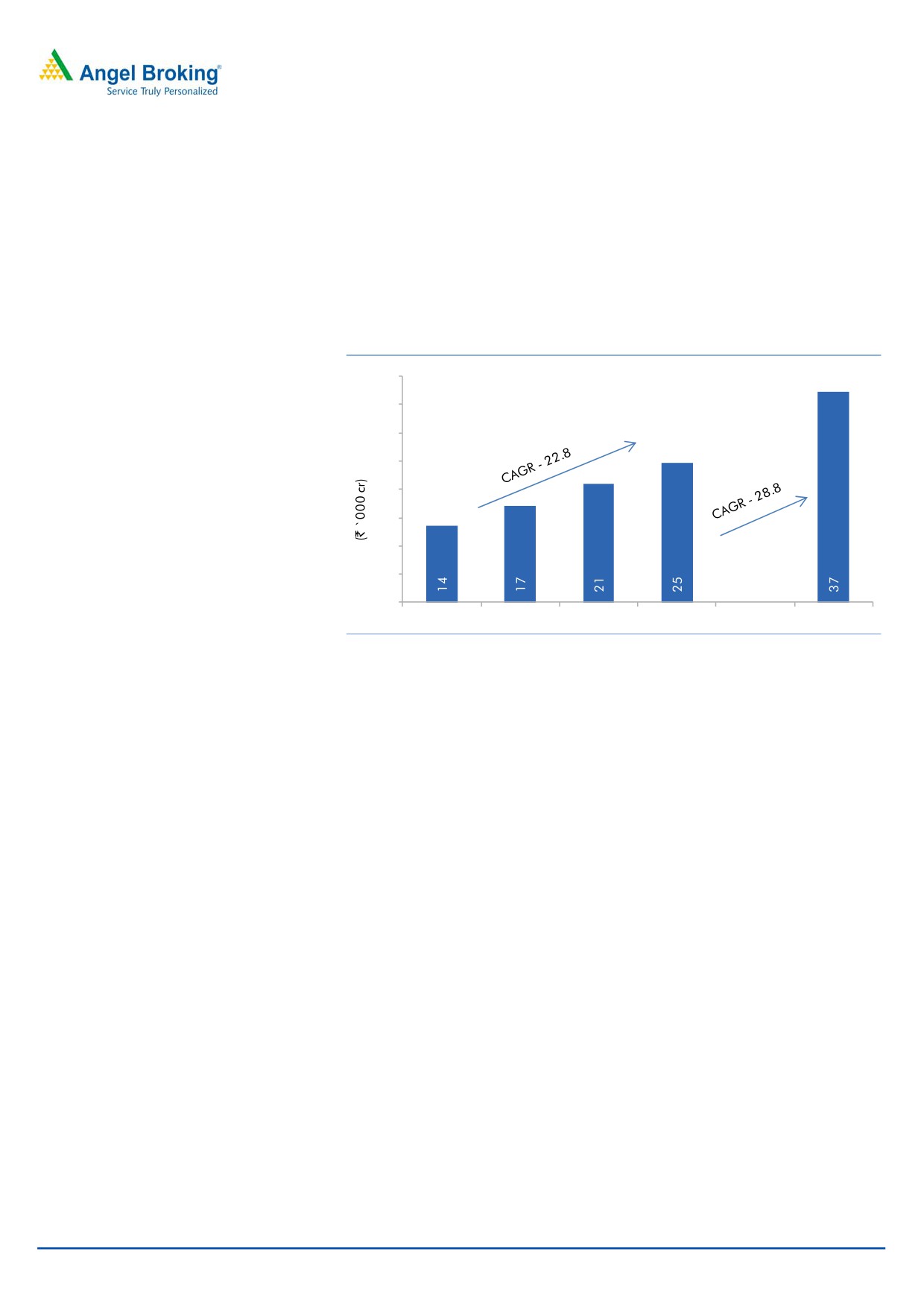

Strong position in the lighting industry

As per ELCOMA, the Indian lighting industry has displayed strong growth over the

years, posting a CAGR of 18.6% over FY2011-14 to reach `13,500cr. The growth

has been largely driven by shift from GLS lamps to CFLs. With the next round of

growth coming from the LED segment, the Indian lighting industry is expected to

grow at a CAGR of 22.8% over FY2014-17E to `25,000cr and reach the

`37,000cr mark by FY2021E.

Exhibit 4: Indian lighting Industry projection

40

35

30

25

20

15

10

5

-

FY2014

FY2015E FY2016E FY2017E

FY2021E

Source: ELCOMA, Angel Research

This positive outlook on the lighting industry augurs well for Surya Roshni as it is

the second largest lighting company in India with nearly three decades of

experience. In the domestic lighting segment, Surya is a prominent brand in the

consumer market and it has a market share in excess of 25%. It has a network of 2

lakh retailers across India and also has international presence in over more than

54 countries. The company has maintained its brand identity over the years and

offers a wide range of world class energy efficient lighting solutions (LED, CFL,

Tube Light, GLS, Luminaries and Accessories, High Mast Lighting Systems, Lighting

Poles etc.) for segments that include domestic, industrial, designer, commercial,

and street lights. It has a state of the art research and development centre in Noida

which assists the company in launching efficient products for the markets.

Additionally, the company has decided to venture into the business of solar power

based lighting systems for rural and urban use which will be an additional revenue

source for the company.

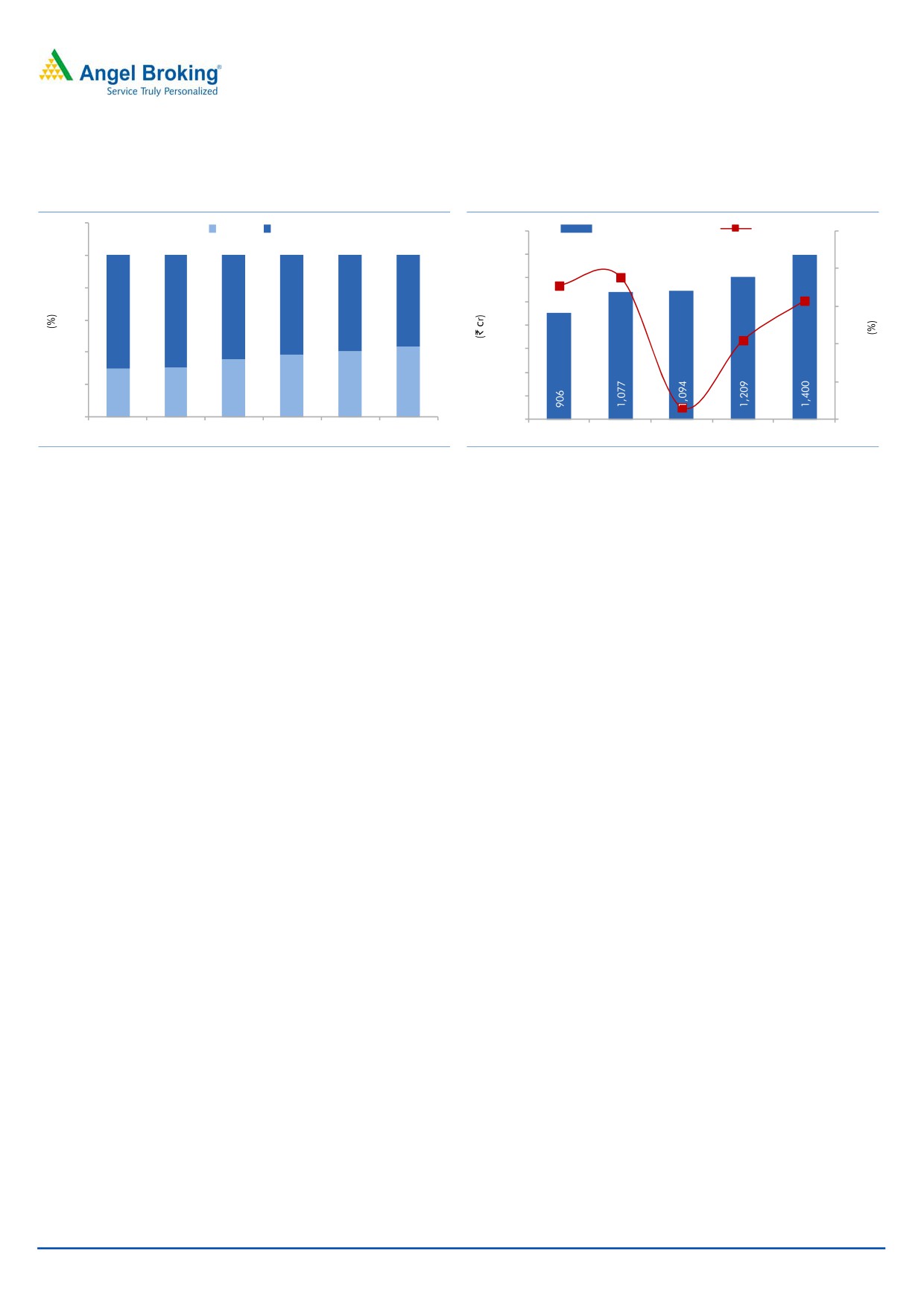

Higher contribution from the Lighting Division to boost profitability

Historically, the company’s Steel division has been a major contributor to the

overall revenues vis-à-vis its Lighting division. In the past the contribution has been

70%-30% in favor of the Steel division. As for profitability, the Lighting business

has a better margin profile than the Steel business. The Lighting division’s margins

are at ~11% as of 9MFY2015 as against the Steel division’s margin of ~3.2%. A

look at the recent performance suggests that the trend seems to be changing,

especially since FY2014, where the Lighting business accounted for 35.5% of

overall sales vs 30.6% in FY2013. This share has further climbed up to ~39% in

9MFY2015 and we expect it to reach levels of 44% by FY2017E.

April 29, 2015

4

Initiating coverage | Surya Roshni

Exhibit 5: Lighting business contribution to improve

Exhibit 6: Lighting business Revenue Trend

120

Lighting

Steel

1,600

Lighting Revenue (LHS)

Growth (RHS)

25.0

1,400

100

20.0

1,200

18.8

80

17.7

56

1,000

64

62

60

15.7

15.0

70

69

60

800

10.0

40

600

10.5

400

20

38

40

44

5.0

30

31

36

200

1.6

-

-

-

FY2012

FY2013

FY2014

FY2015E FY2016E FY2017E

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Source: Company, Angel Research

Source: Company, Angel Research

Surya Roshni is the only lighting company with 100% backward integration, which

benefits the company in terms of availability of best quality raw materials at

effectively lower costs. We expect increase in contribution from the Lighting

division, driven by shift towards LEDs, to boost the overall profitability of the

company.

Fans Business receiving good response

In January 2014, the company pronounced its presence in the `5,000cr Indian fan

industry by launching its ‘Surya’ brand of fans. Its nationwide reach through its

strong retail network and brand pull enjoyed by the company has enabled it to

post ~`60cr of revenue in FY2015E. The Management expects to achieve `200cr

of sales from the Fans business by FY2016E and further targets to reach the

`500cr mark in a span of three-four years. Given the wide range of products in its

portfolio along with existing network of 2 lakh retailers, we expect the contribution

from the business to increase in the long run.

Foray into Appliances business

Encouraged by the impressive performance of its Fans business in a relatively

shorter period of time, the company has recently forayed into the Home

Appliances business in the Indian market. The range of product offerings includes

water heaters/room heaters, dry irons, steam irons and mixer-grinders. The

company expects to garner revenue of `200cr from this segment by FY2017E. We

expect the Appliances business to enjoy similar success as the company’s Fans

business, and add to company’s revenues once the business gets ramped up.

Steel business to improve at a snail pace

Although the Steel business’ share in overall revenues of the company has been

declining in recent times, it is still a major part of the company’s operations. It is a

leader in the steel tube industry in India with products for infra, oil & gas, and

construction sectors. Apart from the stand alone business, the company has

investment in Surya Global Steel Tubes Ltd (SGSTL), holding 49.99% stake in it.

SGSTL is into manufacturing of ERW and Spiral Pipes at its plant in Bhuj (Gujarat),

mainly catering towards exports (75%). The last reported revenue from the

subsidiary was `610cr for September 2012.

April 29, 2015

5

Initiating coverage | Surya Roshni

In the near term, we expect the performance of the division to just be stable and

not be impressive owing to a slew of recent events that have been unfavorable for

the division. Most important of them are lower oil prices, which have dampened

demand from the oil exploration side, and lower global commodity prices. Hence

we have factored in negligible growth rate for the division. However, in the long

run, the division should post better results once the demand from oil and gas, infra

and other sectors begins to pick up. Further, the government’s vision to build 100

smart cities will have a favorable impact on the steel pipe business, in the longer

term time horizon.

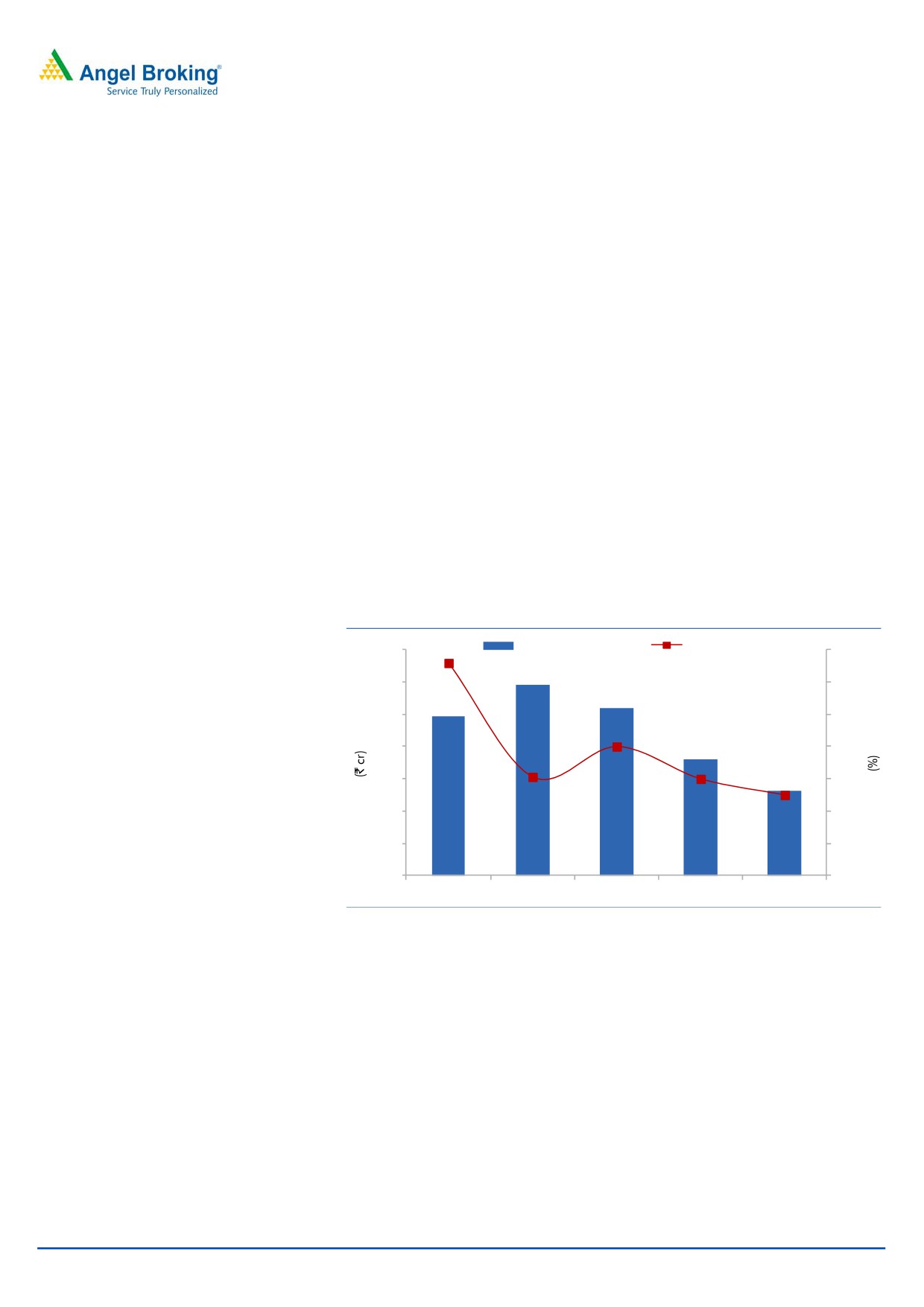

Lower interest cost to add to bottom-line

The recent trend of declining interest rates is likely to benefit leveraged companies

like Surya Roshni. The Reserve Bank of India (RBI), since the beginning of the

current calendar year, has reduced interest rates by 50bp and is expected to

further cut down rates by 50-75bp. We have accounted for a 75bp reduction in

interest expense for the company over FY2015E-17E. We have reduced the debt

quantum for FY2015E, in-line with the number reported by the company in its half-

yearly statement, and taken marginal reductions, going forward. We estimate the

interest expense to decline from `111cr in FY2015E to `98cr in FY2017E. This

lower interest outgo will add directly to the bottom-line.

Exhibit 7: Decline in interest cost

Interest Expense (LHS)

% of Debt (RHS)

120

13.0

12.8

115

12.5

110

12.0

11.5

105

11.5

11.0

100

11.0

11.0

10.8

95

10.5

90

10.0

110

114

111

103

98

85

9.5

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Source: Company, Angel Research

April 29, 2015

6

Initiating coverage | Surya Roshni

Financials

Exhibit 8: Segment Finance

(in ` cr)

FY2014

FY2015E

FY2016E

FY2017E

Revenue

Lighting

1,077

1,094

1,209

1,400

% chg

18.8

1.6

10.5

15.7

% of total

35.5

38.4

40.4

43.5

Steel

1,954

1,758

1,781

1,816

% chg

(4.8)

(10.0)

1.3

2.0

% of total

64.5

61.6

59.6

56.5

Total Segment Revenue

3,031

2,853

2,990

3,216

EBIT

Lighting

108

120

134

156

% yoy

9.2

11.4

11.0

16.7

% of total

60.7

70.0

71.8

74.1

Steel

70

52

53

54

% yoy

(13.8)

(26.1)

1.6

3.7

% of total

39.3

30.0

28.2

25.9

Total

178

172

186

211

Source: Company, Angel Research

Exhibit 9: Key assumptions - Lighting Division

(in ` cr)

FY2015E

FY2016E

FY2017E

Net Revenue

LED

105

168

269

% yoy

320.0

60.0

60.0

CFL

405

324

259

% yoy

(10.0)

(20.0)

(20.0)

Luminaries

205

226

259

% yoy

36.7

10.0

15.0

Fans

60

160

255

% yoy

-

166.0

60.0

Others

319

332

357

% yoy

(29.4)

4.0

7.4

Total

1,094

1,209

1,400

Source: Company, Angel Research

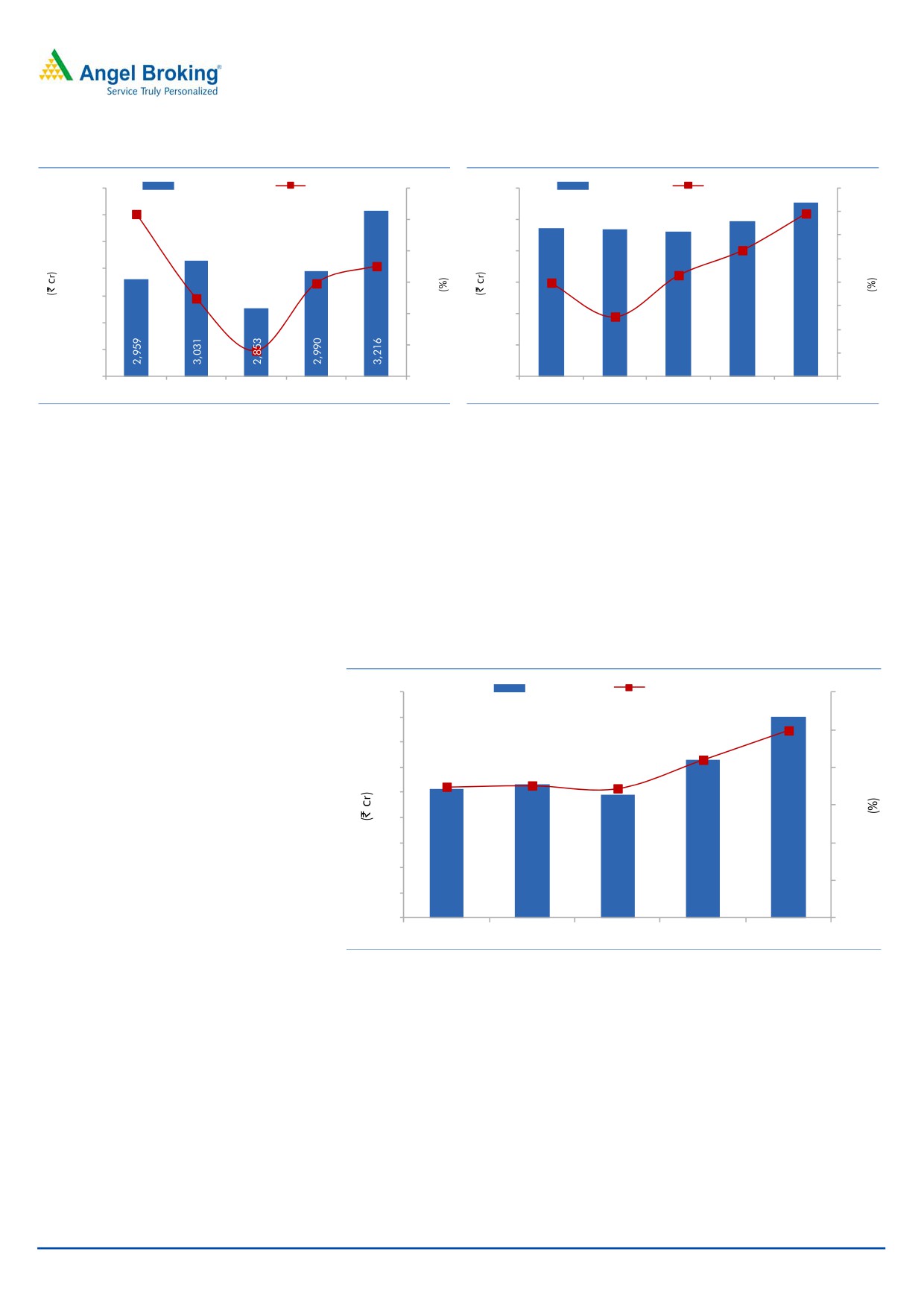

With steady performance from the Steel business and surging contribution of the

Lighting business (on the back of shift from CFL to LED), we expect the company’s

revenue to improve from `2,853cr in FY2015E to `3,216cr in FY2017E. We also

expect the Fans business’ contribution to improve and expect the Appliances

business to benefit from the brand pull and pan India retail network of the

company, much like the Fans business.

April 29, 2015

7

Initiating coverage | Surya Roshni

Exhibit 10: Revenue trend

Exhibit 11: EBITDA Margins to improve

3,300

Revenue (LHS)

Growth (RHS)

20.0

300

EBITDA (LHS)

EBITDA Margins (RHS)

8.8

3,200

15.8

8.6

15.0

250

8.6

8.4

3,100

10.0

200

8.3

8.2

3,000

7.6

8.1

5.0

150

8.0

8.0

2,900

4.8

2.4

7.8

-

100

7.7

2,800

7.6

(5.9)

(5.0)

50

2,700

7.4

237

234

230

247

276

2,600

(10.0)

0

7.2

FY2013

FY2014

FY2015E FY2016E FY2017E

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Source: Company, Angel Research

Source: Company, Angel Research

Higher contribution from Lighting to maintain EBITDA margins

Owing to higher contribution from the Lighting business, the EBITDA margins for

the company are expected to improve from 8.1% in FY2015E to 8.6% in FY2017E

despite of declining profitability of the Steel business. The declining interest rate

environment will have a positive impact on leveraged companies like Surya Roshni.

We expect interest expense to decline from `111cr in FY2015E to `98cr in

FY2017E. With the above estimates we believe that the company’s net profit

should improve from `49cr in FY2015E to `80cr in FY2017E.

Exhibit 12: PAT trajectory

PAT (LHS)

PAT Margins (RHS)

90

3.0

80

2.5

2.5

70

2.1

60

1.8

2.0

1.7

1.7

50

1.5

40

30

1.0

20

0.5

10

52

53

49

63

80

0

0.0

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Source: Company, Angel Research

Sensitivity Analysis

Currently, we are accounting for reduction in interest cost for the company with the

rate of interest declining to 10.8% in FY2017E. In the event of the rate increasing

by 150bp, we expect the net profit to be `70cr. Favorably, similar level of decline

will result in a net profit in the range of `90cr.

April 29, 2015

8

Initiating coverage | Surya Roshni

Exhibit 13: IR Sensitivity analysis

FY2017E Interest Rate (%)

FY2017E Net Profit

9.3

89

9.8

86

10.3

83

10.8

80

11.3

77

11.8

73

12.3

70

Source: Company, Angel Research

Outlook and Valuation

We believe that given the shift in trend towards LED lighting, which is expected to

bring a new wave of growth in the lighting industry, the company’s Lighting

business will become a significant contributor to the overall top-line of the

company. Additionally, exploration of newer avenues like foray into the Fans and

Appliances businesses is likely to be a long term revenue driver for the company.

We expect the top-line to post a CAGR of 6.2% over FY2015E-17E to `3,216cr.

Despite of declining profitability of the Steel business, the EBITDA margins are

estimated to improve to 8.6%, mainly due to higher contribution from the Lighting

business. Consequently, the net profit is expected to post a CAGR of 27.7% over

FY2015E-17E to `80cr.

At the current market price, the stock is trading at 6.0x its FY2017E earnings. We

have allocated the entire debt to the Steel business and valued the company on

SOTP basis. We initiate coverage on the company with a Buy rating and target

price of `149.

Exhibit 14: Sum of Parts Valuation

Sum of Parts

EBIT (`)

Target Multiple (x)

Value

Lighting Business

156

9

1,405

Steel Business (net of `913cr of debt)

54

3

(749)

Total Market Cap

655

No. of Shares

4.4

Target Price (`)

149

Source: Company, Angel Research

Exhibit 15: Steel Business Peer comparison (TTM basis)

Sales

EBIT

EBIT Margin

Capital Employed ROCE

(` cr)

(` cr)

(%)

(` cr)

(%)

APL Apollo Consolidated

3,306

169

5.1

1,036

16.4

Surya Roshni

1,992

57

2.9

1,117

5.1

Source: Company, Angel Research

April 29, 2015

9

Initiating coverage | Surya Roshni

Exhibit 16: Lighting Business Peer comparison (TTM basis)

Sales

EBIT

EBIT Margin

Capital Employed

ROCE

(` cr)

(` cr)

(%)

(` cr)

(%)

Orient Paper & Ind Ltd

1,183

43

3.7

328

13.2

Surya Roshni

1,068

122

11.4

643

18.9

Source: Company, Angel Research

Exhibit 17: One-year forward P/E band

200

Price (`)

3x

5x

7x

9x

180

160

140

120

100

80

60

40

20

0

Source: Company, Angel Research

Key Risks

Competition from Unorganized players - Competition from the unorganized sector

and cheaper imports from China could hurt company’s sales.

Sharp movement in commodity prices - Metal is a major raw material in steel tube

and pipes segment. Steep increase in raw material cost will have a negative impact

on the performance of the company.

Downturn in Economy - Failure in revival of the economy or deterioration in the

economic condition will have a negative impact on both the Steel and Lighting

businesses.

Corporate Guarantee for Loans to Subsidiary - The company has provided

corporate guarantee in favor of bank for loans to its subsidiary Surya Global Steel

Tubes Limited for the sum of `135cr (outstanding portion is `56cr as on 31st March

2014). Non repayment of the loan may result in an increase in debt, thus working

against our estimates. The consolidated debt of the company is estimated to be at

`1,400cr.

We have based our assumptions on the structural shift in the Lighting industry

towards LED lighting. Delay in switchover to LED or any other issues that may

impact the LED switchover will have a negative impact on the revenues of the

company.

April 29, 2015

10

Initiating coverage | Surya Roshni

Company Background

Surya Roshni Limited is a 38 year old conglomerate with its core business

comprising of lighting and steel tube products. The company has nearly four

decades of experience in the steel pipe industry and nearly three decades

experience in the lighting industry. The company is a reputable name in India and

also has presence in over more than 54 countries. It has recently forayed into Fans

and Appliances businesses.

Steel - The company is a leader in the steel pipe industry and is the largest G.I &

Hollow section Pipe manufacturer in India. It has the largest ERW pipe and cold

rolled strips mills at Bahadurgarh, Haryana. It also produces API pipes for India as

well as for export markets. The pipe division produces nearly 8 lakh MT per annum

in various sizes and specifications. The exports from the segment account for

~17% (`340cr) of total revenues.

Lighting

- The company is the second largest lighting company in India

commanding a market share in excess of 25%. The company’s existing range of

products includes LED lamps, CFL, Tube light, GLS, Luminaries and Accessories,

High Mast lighting Systems, Lighting Poles, etc.

Fans - The company has recently entered the Fans business with product offering

that includes ceiling, table, pedestal, wall mounted and exhaust fans.

Approximately, the Fans business accounts for ~`60cr of the overall revenues.

The company in FY2012 had set up a development (R&D) centre in Noida, which

is equipped with most advanced equipments for light measurement and optical

evaluation for conventional lighting as well as LED measurement. It is listed as one

of the best testing laboratories in India by BEE (Bureau of Energy Efficiency) for LED

lighting system.

Plant Locations

Exhibit 18: Plant Locations

Lighting Division

Steel Division

Kashipur, Uttaranchal

Malanpur, Madhya Pradesh

Malanpur, Madhya Pradesh

Bahadurgarh, Haryana

Source: Company

April 29, 2015

11

Initiating coverage | Surya Roshni

Profit and loss statement

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Total operating income

2,959

3,031

2,853

2,990

3,216

% chg

15.8

2.4

(5.9)

4.8

7.6

Net Raw Materials

2,251

2,266

2,064

2,169

2,323

% chg

15.4

0.7

(8.9)

5.1

7.1

Personnel

135

151

163

167

180

% chg

6.5

12.2

7.6

3.0

7.6

Other

337

380

397

406

437

% chg

19.6

12.8

4.3

2.4

7.6

Total Expenditure

2,722

2,797

2,623

2,743

2,940

EBITDA

237

234

230

247

276

% chg

20.8

(1.3)

(1.6)

7.6

11.7

(% of Net Sales)

8.0

7.7

8.1

8.3

8.6

Depreciation& Amortisation

57

56

58

62

65

EBIT

180

178

172

186

211

% chg

21.2

(1.2)

(3.6)

8.1

13.8

(% of Net Sales)

6.1

5.9

6.0

6.2

6.6

Interest & other Charges

110

114

111

103

98

(% of Net Sales)

3.7

3.8

3.9

3.4

3.1

Other Income

2

4

1

1

1

(% of Net Sales)

0.1

0.1

0.0

0.0

0.0

Recurring PBT

70

64

61

83

113

% chg

28.7

(9.8)

(4.7)

36.2

37.0

PBT (reported)

72

67

62

84

114

Tax

20

14

13

21

34

(% of PBT)

28.4

20.5

20.5

25.0

30.0

PAT (reported)

52

53

49

63

80

Extraordinary Expense/(Inc.)

-

-

-

-

-

ADJ. PAT

52

53

49

63

80

% chg

20.4

3.5

(7.9)

27.9

27.4

(% of Net Sales)

1.7

1.8

1.7

2.1

2.5

Basic EPS (`)

11.8

12.2

11.2

14.3

18.3

Fully Diluted EPS (`)

11.8

12.2

11.2

14.3

18.3

% chg

20.4

3.5

(7.9)

27.9

27.4

April 29, 2015

12

Initiating coverage | Surya Roshni

Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

SOURCES OF FUNDS

Equity Share Capital

44

44

44

44

44

Reserves& Surplus

502

551

595

652

727

Warrants

-

-

-

-

-

Shareholders’ Funds

546

595

639

696

771

Revaluation of Land

186

179

179

179

179

Total Loans

857

1,038

965

936

913

Other Long Term Liabilities

5

6

6

6

6

Long Term Provisions

18

17

17

17

17

Deferred Tax Liability

42

48

48

48

48

Total Liabilities

1,655

1,883

1,854

1,883

1,935

APPLICATION OF FUNDS

Gross Block

1,364

1,470

1,561

1,651

1,735

Less: Acc. Depreciation

511

558

616

678

743

Net Block

853

912

945

973

992

Capital Work-in-Progress

26

54

40

30

23

Investments

50

50

50

50

50

Current Assets

886

1,055

1,020

1,033

1,088

Cash

19

25

31

19

10

Loans & Advances

70

94

86

90

96

Inventory

380

433

429

443

473

Debtors

410

497

469

475

502

Other current assets

6

7

6

6

6

Current liabilities

161

188

201

203

217

Net Current Assets

725

867

819

830

870

Misc. Exp. not written off

-

-

-

-

-

Total Assets

1,655

1,883

1,854

1,883

1,935

April 29, 2015

13

Initiating coverage | Surya Roshni

Cash flow statement

Y/E March (` cr)

FY2013

FY2014

FY2015E FY2016E FY2017E

Profit before tax

72

67

62

84

114

Depreciation

57

56

58

62

65

Change in Working Capital

(50)

(136)

54

(22)

(50)

Direct taxes paid

(20)

(14)

(13)

(21)

(34)

Others

117

116

(1)

(1)

(1)

Cash Flow from Operations

175

89

160

101

94

(Inc.)/Dec. in Fixed Assets

(72)

(133)

(78)

(80)

(77)

(Inc.)/Dec. in Investments

0

0

-

-

-

(Incr)/Decr In LT loans & adv.

-

-

-

-

-

Others

(4)

(13)

1

1

1

Cash Flow from Investing

(77)

(146)

(77)

(78)

(75)

Issue of Equity

(15)

(7)

-

-

-

Inc./(Dec.) in loans

25

181

(73)

(29)

(23)

Dividend Paid (Incl. Tax)

(20)

(5)

(5)

(5)

(5)

Others

(89)

(106)

-

-

-

Cash Flow from Financing

(100)

63

(78)

(34)

(29)

Inc./(Dec.) in Cash

(2)

6

6

(11)

(10)

Opening Cash balances

21

19

25

31

19

Closing Cash balances

19

25

31

19

10

April 29, 2015

14

Initiating coverage | Surya Roshni

Key Ratios

Y/E March

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

9.3

9.0

9.8

7.6

6.0

P/CEPS

4.4

4.4

4.5

3.8

3.3

P/BV

0.9

0.8

0.8

0.7

0.6

EV/Net sales

0.4

0.5

0.5

0.5

0.4

EV/EBITDA

5.4

6.2

5.9

5.4

4.8

EV / Total Assets

0.8

0.8

0.7

0.7

0.7

Per Share Data (`)

EPS (Basic)

11.8

12.2

11.2

14.3

18.3

EPS (fully diluted)

11.8

12.2

11.2

14.3

18.3

Cash EPS

24.7

24.9

24.5

28.4

33.1

DPS

4.0

1.0

1.0

1.0

1.0

Book Value

124.6

135.6

145.7

158.8

176.0

DuPont Analysis

EBIT margin

6.1

5.9

6.0

6.2

6.6

Tax retention ratio

0.7

0.8

0.8

0.8

0.7

Asset turnover (x)

1.9

1.8

1.6

1.7

1.8

ROIC (Post-tax)

8.5

8.5

7.8

7.9

8.1

Cost of Debt (Post Tax)

9.3

9.6

8.8

8.1

7.4

Leverage (x)

1.4

1.6

1.4

1.2

1.1

Operating ROE

7.3

6.8

6.5

7.6

8.9

Returns (%)

ROCE (Pre-tax)

11.1

10.1

9.2

9.9

11.1

Angel ROIC (Pre-tax)

11.9

10.7

9.8

10.5

11.6

ROE

9.9

9.4

8.0

9.4

10.9

Turnover ratios (x)

Asset TO (Gross Block)

2.2

2.1

1.9

1.9

1.9

Inventory / Net sales (days)

47

49

55

53

52

Receivables (days)

46

55

60

58

57

Payables (days)

18

23

28

27

27

WC cycle (ex-cash) (days)

84

93

104

98

95

Solvency ratios (x)

Net debt to equity

1.4

1.6

1.4

1.2

1.1

Net debt to EBITDA

3.3

4.1

3.8

3.5

3.1

Int. Coverage (EBIT/ Int.)

1.6

1.6

1.5

1.8

2.2

April 29, 2015

15

Initiating coverage | Surya Roshni

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel has received in-principal approval

from SEBI for registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its associates

including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company covered by

Analyst. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of securities of

the company covered by Analyst during the past twelve months. Angel/analyst has not served as an officer, director or employee of

company covered by Analyst and has not been engaged in market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important 'Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Surya Roshni

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15

April 29, 2015

16