3QCY2016 Result Update | Pharmaceutical

November 10, 2016

Sanofi India

NEUTRAL

CMP

`4,277

Performance Highlights

Target Price

-

Investment Period

-

Y/E Dec. (` cr)

3QCY2016 2QCY2016

% chg (qoq) 3QCY2015

% chg (yoy)

Net sales

583

565

3.1

553

5.4

Stock Info

Other income

56

59

(4.9)

42

32.5

Sector

Pharmaceutical

Operating profit

104

103

0.7

109

(4.7)

Market Cap (` cr)

9,850

Adj. Net profit

81

85

(4.9)

73

11.9

Net debt (`

cr)

(239)

Source: Company, Angel Research

Beta

0.3

Sanofi India posted results and are below expectations on all fronts. The sales

52 Week High / Low

4,770/3,850

came in at `583cr vs. `600cr expected, posting a yoy growth of 5.4%. According

Avg. Daily Volume

2,410

to AIOCD, secondary sales, growth for Sanofi India was double digit. According

Face Value (`)

10

to AIOCD, regulatory actions will have negative one-time impact of ~2% on sales

BSE Sensex

27,591

of the company. We expect revenue growth to sustain in the coming quarters with

Nifty

8,544

improvement in volumes.On the operating front, the EBITDA margin came in at

Reuters Code

SANO.BO

17.8% vs. 19.0% expected and 19.7% in 3QCY2015. Consequently, the Adj. PAT

Bloomberg Code

SANL@IN

came in at `81cr vs. `73cr in 3QCY2015, a yoy growth of 11.9%. This was

against the expectations of `94cr. We maintain our Neutral rating on the stock.

Shareholding Pattern (%)

Lower -than-expected results; mainly on sales: Sanofi India posted results and are

Promoters

60.4

below expectations on all fronts. The sales came in at `583cr vs. `600cr

MF / Banks / Indian Fls

19.3

expected, posting a yoy growth of 5.4%. According to AIOCD, secondary sales,

FII / NRIs / OCBs

15.1

growth for Sanofi India was double digit. According to AIOCD, regulatory actions

Indian Public / Others

5.2

will have negative one-time impact of ~2% on sales of the company.On the

operating front, the EBITDA margin came in at 17.8% vs. 19.0% expected and

19.7% in 3QCY2015. Consequently, the Adj. PAT came in at `81cr vs. `73cr in

Abs. (%)

3m 1yr

3yr

3QCY2015, a yoy growth of 11.9%. This was against the expectations of `94cr.

Sensex

(2.1)

5.0

33.5

Outlook and valuation: We expect net sales to post a 12.6% CAGR to `2,597cr

Sanofi India

(4.6)

(0.8)

66.7

and EPS to register a 22.2% CAGR to `172.1 over CY2015-17. At current levels,

the stock is trading at 28.5x and 24.8x its CY2016E and CY2017E earnings,

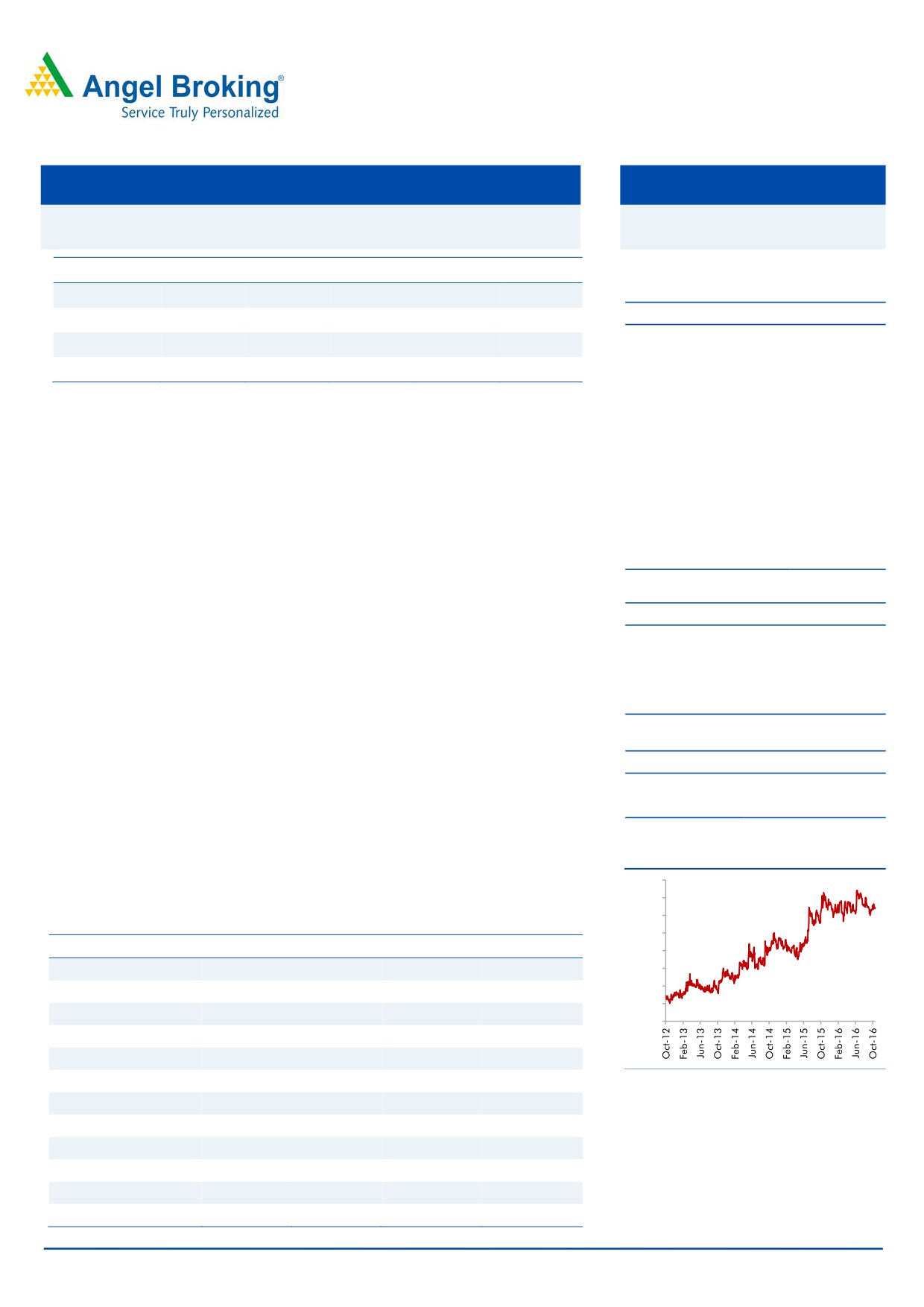

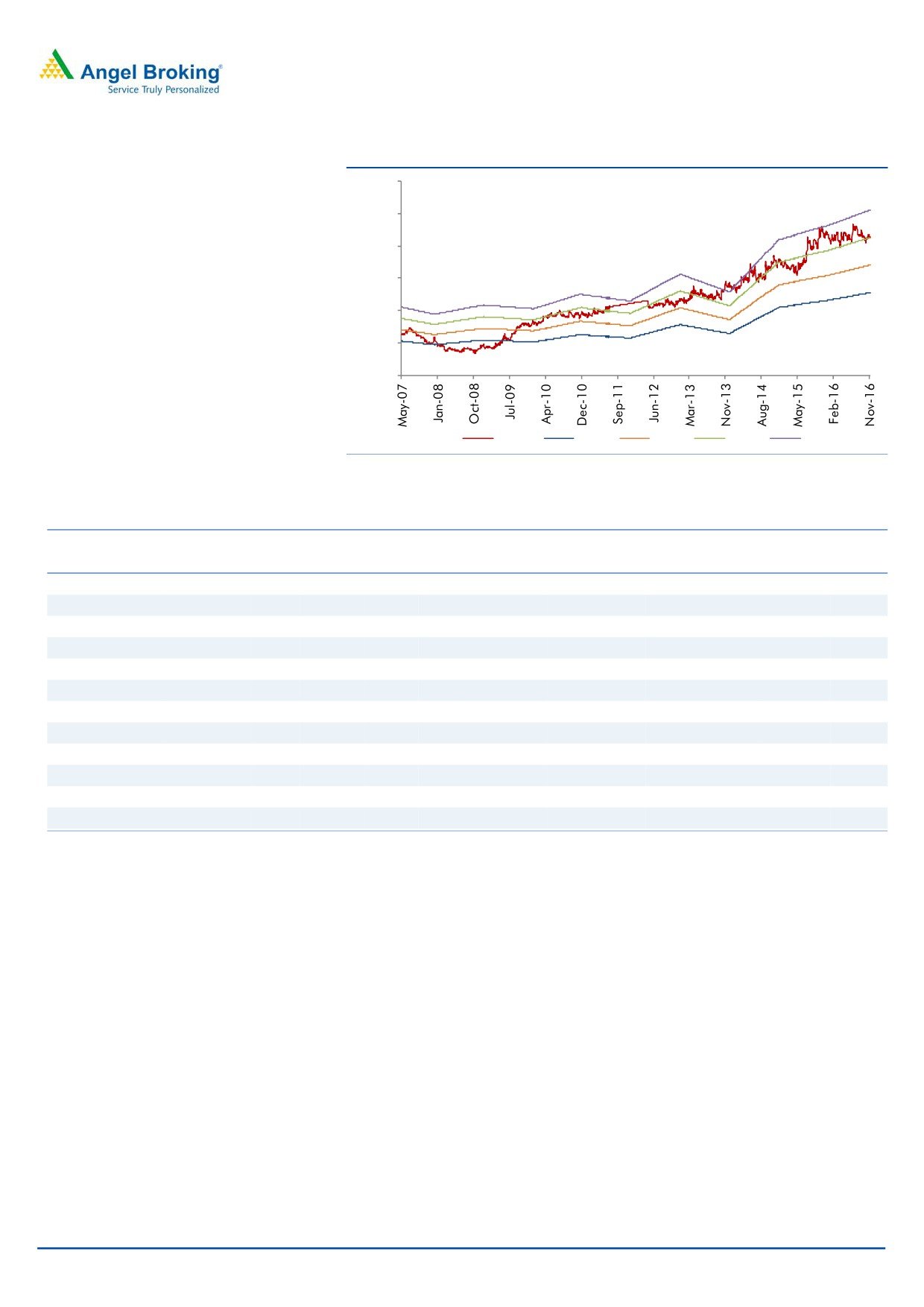

3-year price chart

respectively. Given the rich valuations, we recommend a Neutral rating on the

4,900

stock.

4,500

4,100

Key financials

3,700

Y E Dec (` cr)

CY2014

CY2015

CY2016E

CY2017E

3,300

Net Sales

1,875

2,049

2,277

2,597

2,900

2,500

% chg

9.9

9.3

11.1

14.1

2,100

Net Profit

197.1

264.9

343.7

395.5

1,700

% chg

(17.8)

34.4

29.8

15.1

EPS (`)

85.6

115.2

149.4

172.0

EBITDA(%)

12.6

15.4

17.3

18.3

Source: Company, Angel Research

P/E (x)

49.7

37.0

28.5

24.8

RoE (%)

14.4

19.3

25.1

28.8

RoCE (%)

10.2

14.8

19.9

25.6

P/BV (x)

6.6

6.0

4.7

3.8

Sarabjit Kour Nangra

EV/Sales (x)

5.0

4.5

4.0

3.2

+91 22 3935 7800 Ext: 6806

EV/EBITDA (x)

39.5

29.2

22.8

17.6

Source: Company, Angel Research; Note: CMP as of November 8, 2016

Please refer to important disclosures at the end of this report

1

Sanofi India | 3QCY2016 Result Update

Exhibit 1: 3QCY2016 performance

Y/E Dec (` cr)

3QCY2016

2QCY2016

% chg (qoq) 3QCY2015

% chg (yoy) 9MCY16 9MCY15

% chg yoy

Net sales

583

565

3.1

553

5.4

1,654

1,527

8.3

Other income

56

59

(4.9)

42

32.5

178

152

17.0

Total income

639

624

2.3

595

7.4

1,832

1,679

9.1

PBIDT

104

103

0.7

109

(4.7)

299

249

19.9

OPM (%)

17.8

18.2

19.7

18.0

16.3

Interest

0.3

0.7

0.1

1

0

Depreciation & amortisation

30

30

0.0

29

3.4

90

83

8.6

PBT & exceptional items

130

132

(1.4)

122

6.1

385

318

21.1

Less : Exceptional items

0

0

0

0

16

Profit before tax

130

132

(1.4)

122

6.1

385

302

27.5

Provision for taxation

49

46

5.2

50

(2.2)

139

116

19.6

Net profit

81

85

(4.9)

73

11.9

247

185

33.2

Adj net profit

81

85

(4.9)

73

11.9

247

169

45.9

EPS (`)

35.3

37.1

31.5

107.2

73.5

Source: Company, Angel Research

Exhibit 2: 3QCY2016 - Actual Vs Angel estimates

` cr

Actual

Estimates

Variation (%)

Net sales

583

600

(2.9)

Other income

56

60

(6.3)

Operating profit

104

114

(9.1)

Tax

49

51

(4.3)

Net profit

81

94

(14.0)

Source: Company, Angel Research

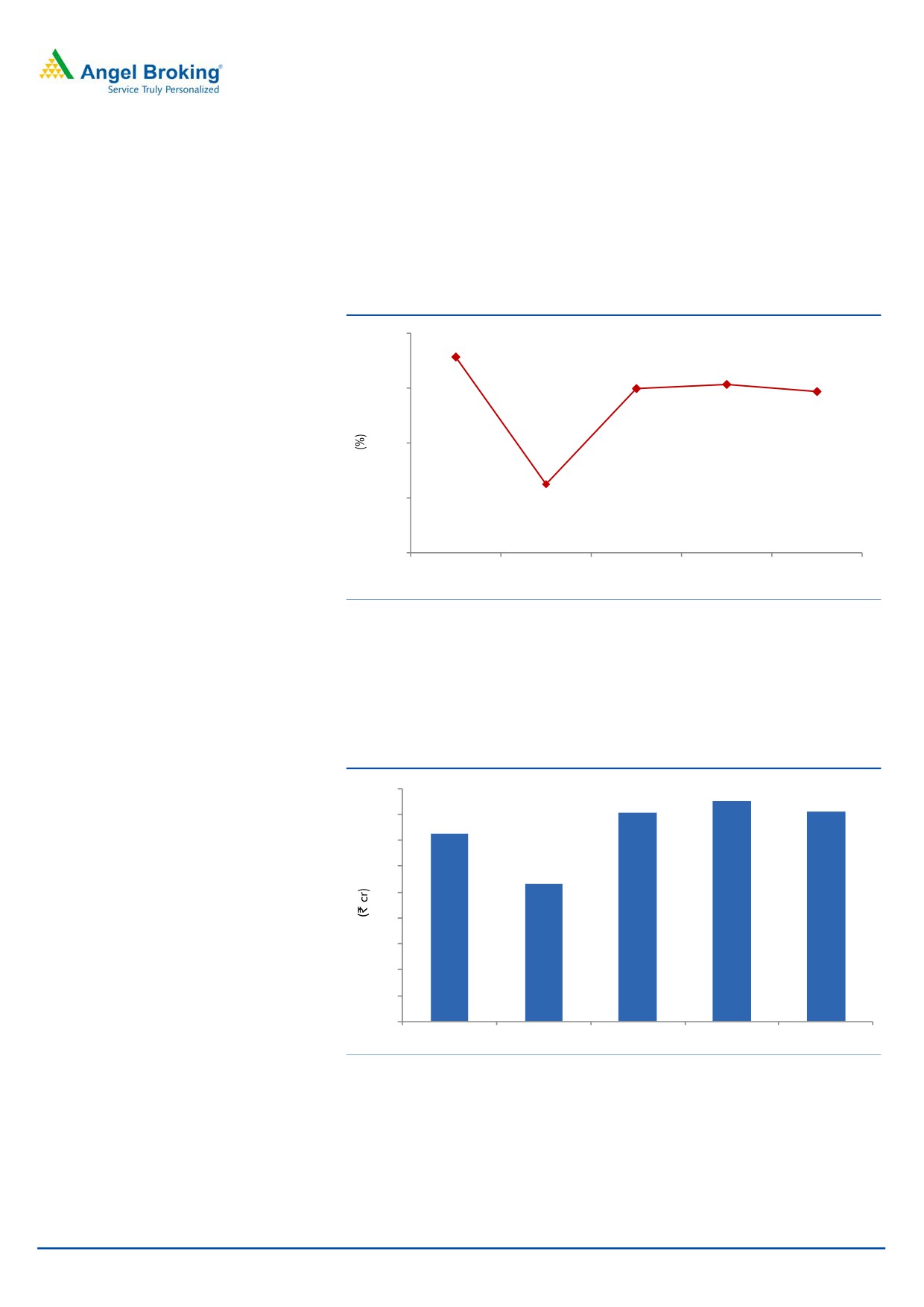

Revenue growth lower than expectation

The company posted sales of `583cr (vs. an expected `600cr), a yoy growth of

5.4%. According to AIOCD, secondary sales, growth for Sanofi India was double

digit. According to AIOCD, regulatory actions will have negative one-time impact

of ~2% on sales of the company. We expect revenue growth to sustain in the

coming quarters with improvement in volumes.

Exhibit 3: Sales trend

620

583

565

570

553

522

506

520

470

420

370

320

3QCY2015

4QCY2015

1QCY2016

2QCY2016

3QCY2016

Source: Company, Angel Research

November 10, 2016

2

Sanofi India | 3QCY2016 Result Update

OPM dips to 17.8%: On the operating front, the gross margin came in at 49.8%

vs. an expected 52.4% and vs. 52.0% in the corresponding period of last year. The

OPM came in at 17.8% vs. an expected 19.0% and vs. 19.7% in the corresponding

period of last year. Other expenses moved down by 5.4%, while employee

expenses moved up by 16.1% yoy during the quarter; thus leading dip in the

operating margins.

Exhibit 4: OPM trend

21.0

19.7

18.0

17.8

18.0

18.2

15.0

12.0

12.7

9.0

3QCY2015

4QCY2015

1QCY2016

2QCY2016

3QCY2016

Source: Company, Angel Research

Bottom-line lower than estimate: The PAT came in at `81cr (vs.an expected `94cr),

a yoy growth of 11.9%. The other income during the quarter came in at `56.5cr

vs. `42.4cr in 3QCY2015, while tax as a percentage of PBT was at 37.5% vs.

40.7% in 3QCY2015.

Exhibit 5: Adj. net profit trend

90

85

81

81

80

73

70

60

53

50

40

30

20

10

0

3QCY2015

4QCY2015

1QCY2016

2QCY2016

3QCY2016

Source: Company, Angel Research

November 10, 2016

3

Sanofi India | 3QCY2016 Result Update

Recommendation rationale

Focus on top-line growth: Sanofi recorded revenue CAGR of 9.1% to `1,494cr

over CY2006-12. The growth was impacted by a lower-than-expected growth in

domestic formulations and loss of distribution rights of Rabipur vaccine. Going

forward, to grow in line with the industry’s average growth rate in the domestic

segment, the company has rolled out a project - Prayas, an initiative to increase its

penetration in rural areas. Under the project, the company would launch low-

priced products in the anti-infective and NSAID therapeutic segments and increase

its field force. The project is expected to provide incremental revenue of `500cr

over the next five years.

Sanofi also plans to launch CVS and vaccine products in the domestic market post

the acquisition of Shantha Biotech by its parent company. Further, during CY2011,

the company acquired the nutraceutical business of Universal Medicare Pvt. Ltd,

which led the company’s foray into the nutarceutical business, thus aiding it in

diversifying and boosting overall growth of its domestic formulation business.

During 2HCY2014 the company’s sales were impacted by the July 2014 National

Pharmaceutical Pricing Authority (NPPA) order which has brought 80 formulations

pertaining to 50 drugs under price control. This severely impacted the company as

three of its major products have come under price control. The company is

estimated to suffer a value loss of `120cr on an annualized basis. However, on the

positive side the government has revoked the order, which should aid a recovery in

the domestic formulation sales of the company, going forward. We expect the

company’s net sales to log a 12.6% CAGR over CY2015-17, with domestic

formulation sales expected to post a yoy growth of around 14.3% during the

period.

Valuation: We expect net sales to post a 12.6% CAGR to `2,597cr and EPS to

register a 22.2% CAGR to `172.1 over CY2015-17. At current levels, the stock is

trading at 28.1x and 24.8x its CY2016E and CY2017E earnings, respectively. Given

the rich valuations, we recommend a Neutral rating on the stock.

Exhibit 6: Key assumptions

CY2016E

CY2017E

Net sales growth (%)

11.1

14.1

Domestic sales growth (%)

10.0

15.0

Export sales growth (%)

6.0

10.0

Growth in employee expenses (%)

11.1

14.1

Operating margins (%)

17.4

20.8

Net profit growth (%)

29.8

15.1

Capex (` cr)

30.0

30.0

Source: Company, Angel Research

November 10, 2016

4

Sanofi India | 3QCY2016 Result Update

Exhibit 7: One-year forward P/E

6,000

5,000

4,000

3,000

2,000

1,000

0

Price

10x

15x

20x

25x

Source: Company, Angel Research

Exhibit 8: Recommendation summary

Company

Reco.

CMP Tgt Price Upside

FY2018E

FY16-18E

FY2018E

(`)

(`)

(%) PE (x) EV/Sales (x) EV/EBITDA (x)

CAGR in EPS (%) RoCE (%) RoE (%)

Alembic Pharma

Neutral

655

-

-

21.6

2.9

13.5

(10.8)

27.5

25.3

Aurobindo Pharma Buy

757

877

15.9

16.0

2.6

11.1

18.1

22.5

26.1

Cadila Healthcare Buy

375

-

-

19.5

3.0

13.7

13.4

22.7

25.7

Cipla

Neutral

536

-

-

19.7

2.5

13.6

20.4

13.5

15.2

Dr Reddy's

Neutral

3,115

-

-

21.8

2.8

12.5

1.7

16.2

15.9

Dishman Pharma Neutral

237

-

-

21.0

2.3

10.3

3.1

10.3

10.9

GSK Pharma*

Neutral

2,719

-

-

44.7

6.8

32.8

17.3

35.3

32.1

Indoco Remedies Reduce

277

240

(13.4)

17.3

2.0

11.1

33.2

19.1

20.1

Ipca labs

Accumulate

572

613

7.2

29.0

2.0

13.1

36.5

8.8

9.4

Lupin

Buy

1,509

1,809

19.9

21.8

3.6

13.4

17.2

24.4

20.9

Sanofi India*

Neutral

4,277

-

-

24.9

3.3

17.8

22.2

24.9

28.8

Sun Pharma

Buy

635

944

48.6

19.4

3.8

12.2

22.0

33.1

18.9

Source: Company, Angel Research

Company Background

Sanofi, a leading global pharmaceutical company, operates in India through four

entities - Sanofi India, Sanofi-Synthelabo (India) Ltd, Sanofi Pasteur India Private

Ltd and Shantha Biotechnics. Sanofi India focuses its activities on seven major

therapeutic areas, namely

- Cardiovascular diseases, Metabolic Disorders,

Thrombosis, Oncology, Central Nervous System disorders, Internal Medicine and

Vaccines. Predominately a domestic company, the company exports to

semi-regulated markets; exports of ~`500cr, contributed around 26% of sales in

CY2014.

November 10, 2016

5

Sanofi India | 3QCY2016 Result Update

Profit & loss statement

Y/E Dec. (` cr)

CY12

CY3

CY14

CY15

CY16E

CY17E

Gross sales

1,534

1,746

1,915

2,097

2,329

2,653

Less: Excise duty

40

39

40

48

53

56

Net sales

1,494

1,707

1,875

2,049

2,277

2,597

Other operating income

91

102

103

144

144

144

Total operating income

1,585

1,809

1,978

2,193

2,420

2,741

% chg

20.5

14.1

9.3

10.9

10.4

13.2

Total expenditure

1,261

1,411

1,639

1,734

1,882

2,120

Net raw materials

735

820

974

1,012

1,079

1,205

Other mfg costs

74

82

93

106

118

135

Personnel

214

242

288

333

370

422

Other

238

267

283

283

314

358

EBITDA

233

296

236

315

395

477

% chg

32.2

27.0

7.3

8.3

9.3

10.3

(% of Net Sales)

15.6

17.3

12.6

15.4

17.3

18.3

Dep. & amortisation

90

92

97

113

123

125

EBIT

143

203

140

202

272

351

% chg

(1.5)

42.4

5.7

6.7

7.7

8.7

(% of Net Sales)

9.6

11.9

10.2

11.2

12.2

13.2

Interest & other charges

1

0

-

-

-

-

Other income

30

58

64

135

100

100

(% of PBT)

11.4

15.9

18.6

19.6

20.6

21.6

Share in profit of Asso.

-

-

-

-

-

-

Recurring PBT

262

363

307

481

516

595

% chg

(7.7)

38.7

3.8

4.8

5.8

6.8

Extraordinary Exp./(Inc.)

PBT (reported)

262

363

307

481

516

595

Tax

85.0

123.3

109.0

159.4

170.3

196.3

(% of PBT)

32.4

33.9

35.6

33.1

33.0

33.0

PAT (reported)

177

240

198

322

346

399

Extra-ordinary items

(0)

(25)

(67)

56

-

-

PAT after MI (reported)

177

266

264

321

344

396

ADJ. PAT

177

240

197

265

344

396

% chg

(7.4)

35.4

(17.8)

34.4

29.8

15.1

(% of Net Sales)

11.8

15.6

14.1

15.7

15.1

15.2

Basic EPS (`)

77

104

86

115

149

172

Fully Diluted EPS (`)

77

104

86

115

149

172

% chg

(7.4)

35.4

(17.8)

34.6

29.8

15.1

November 10, 2016

6

Sanofi India | 3QCY2016 Result Update

Balance sheet

Y/E Dec (` cr)

CY12

CY3 CY14 CY15 CY16E CY17E

SOURCES OF FUNDS

Equity share capital

23

23

23

23

23

23

Preference Capital

-

-

-

-

-

-

Reserves & surplus

1,181

1,324

1,463

1,604

2,051

2,551

Shareholders funds

1,204

1,347

1,486

1,627

2,074

2,574

Long term provisions

19

25

32

40

40

40

Other long term liabilities

-

-

-

-

-

-

Total loans

-

-

-

-

-

-

Total liabilities

1,223

1,372

1,518

1,668

2,117

2,617

APPLICATION OF FUNDS

Gross block

889

1,075

1,195

1,349

1,379

1,409

Less: Acc. depreciation

315

409

506

619

741

867

Net block

574

666

690

730

638

542

Goodwill

125

125

125

125

125

125

Capital Work-in-Progress

43

43

43

43

43

43

Long term loan and adv.

61

62

106

262

262

262

Investments

0.4

0.2

0.2

0.2

0.2

0.2

Current assets

827

947

1,263

1,245

1,832

2,521

Cash

429

264

469

572

792

1,427

Loans & advances

208

219

196

301

334

288

Other

191

464

598

373

706

806

Current liabilities

387

435

656

617

664

757

Net current assets

441

512

607

628

1,169

1,764

Deferred tax assets

(21)

(37)

(54)

(120)

(120)

(120)

Total assets

1,223

1,372

1,518

1,668

2,117

2,617

November 10, 2016

7

Sanofi India | 3QCY2016 Result Update

Cash flow statement

Y/E Dec. (` cr)

CY12 CY13 CY14 CY15 CY16E

CY17E

Profit before tax

282

285

291

292

293

294

Depreciation

90

92

97

113

123

125

(Inc)/Dec in Working Capital

(147)

236

(64)

73

321

(40)

Less: Other income

91

102

66

67

68

69

Direct taxes paid

93

91

93

94

95

96

Cash Flow from Operations

41

420

164

317

574

215

(Inc.)/Dec.in Fixed Assets

(67)

(186)

(120)

(154)

(30)

(30)

(Inc.)/Dec. in Investments

-

0

0

-

-

1

Other income

91

102

66

67

68

69

Cash Flow from Investing

24

(84)

41

42

43

44

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

-

-

-

-

-

-

Dividend Paid (Incl. Tax)

(88)

(104)

(104)

(104)

(104)

(104)

Others

218

(397)

102

(153)

(301)

519

Cash Flow from Financing

130

(501)

(1)

(257)

(404)

415

Inc./(Dec.) in Cash

195

(164)

204

103

213

675

Opening Cash balances

234

429

264

469

572

792

Closing Cash balances

429

264

469

572

792

1,427

November 10, 2016

8

Sanofi India | 3QCY2016 Result Update

Key ratios

Y/E Dec.

CY12

CY13

CY14

CY15

CY16E

CY17E

Valuation Ratio (x)

P/E (on FDEPS)

55.4

40.9

49.7

37.0

28.5

24.8

P/CEPS

36.7

27.4

27.2

22.6

21.0

18.8

P/BV

8.1

7.3

6.6

6.0

4.7

3.8

EV/Sales

6.3

5.6

5.0

4.5

4.0

3.2

EV/EBITDA

40.3

32.3

39.5

29.2

22.8

17.6

Per Share Data (`)

EPS (Basic)

76.9

104.1

85.6

115.2

149.4

172.0

EPS (fully diluted)

76.9

104.1

85.6

115.2

149.4

172.0

Cash EPS

115.9

155.4

156.7

188.7

202.8

226.5

DPS

33.0

33.0

33.0

33.0

33.0

33.0

Book Value

522.9

584.8

645.2

707.4

901.9

1,118.9

Returns (%)

RoCE (Pre-tax)

12.1

15.7

10.2

14.8

19.9

25.6

Angel ROIC (Pre-tax)

17.5

22.4

14.6

21.1

28.3

36.5

ROE

15.3

18.8

14.4

19.3

25.1

28.8

Turnover ratios (x)

Inventory / Sales (days)

61

31

28

26

23

21

Receivables (days)

23

9

8

7

7

6

Payables (days)

44

24

21

20

18

16

November 10, 2016

9

Sanofi India | 3QCY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Sanofi India

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 10, 2016

10