Initiating Coverage | NBFC

June 29, 2018

Shriram Transport Fin Co

BUY

CMP

`1,301

Uncontested leader in niche category

Target Price

`1,760

Shriram Transport Finance Company (SHTF) is a NBFC with differentiated

Investment Period

12 Months

business model. The company pioneers in financing used commercial vehicles

and had AUM of `95,306cr in FY18; it also focuses on small truck owners

Stock Info

(having less than 5 trucks). SHTF has presence in almost all regions of the country

Sector

NBFC

with 1,213 branches.

Market Cap (` cr)

29,532

Multiple AUM growth levers: CV and M&HCV sales grew 20% and 25.5% yoy,

Beta

1.0

respectively in FY18. We expect AUM growth momentum to continue led by (1)

52 Week High / Low

1670/898

macro-economic revival, vehicles typically change hands in three years in good

Avg. Daily Volume

70,755

economic environment and in five years in subdued economy, (2) business loans

Face Value (`)

10

are gaining traction (`2,600cr portfolio in FY18). The company started with

BSE Sensex

35,038

business loans from the South (Tamil Nadu), but is now expanding it to Karnataka

and Andhra Pradesh, (3) ramping up of rural distribution, which led to 49% yoy

Nifty

10,589

growth in rural AUM to `3,100cr. It has opened incremental branches (217) in

Reuters Code

SRTS.NS

rural areas in FY18.

Bloomberg Code

SHTF.IN

Stabilizing asset quality to lead to lower credit costs: SHTF recognized NPA on

180DPD basis till Q3FY16, but has gradually moved to 90DPD in Q4FY18. This

Shareholding Pattern (%)

has led to spike in GNPA (from 3.8% in FY15 to 9.15% in FY18) and credit cost

Promoters

26.1

(from 2.4 in FY15 to 3.8% in FY18). Credit cost over FY09-15 was in the range of

MF / Banks / Indian Fls

4.0

1.4-2.4% and due to a regulatory requirement; it reached 3.8% in Q4FY18. We

FII / NRIs / OCBs

51.2

expect credit cost to fall by 140bps over FY18-20E, which would drive RoA

Indian Public / Others

6.9

expansion.

Outlook & Valuation: We expect SHTF’s AUM to grow at CAGR of 20% over

FY18-20E led by stronger CV volume, macro recovery and improving rural

Abs.(%)

3m 1yr 3yr

market. The company’s return ratios are at decade low levels (RoA/RoE -

Sensex

5.6

13.2

26.7

1.9%/13% in FY18) primarily owing to higher credit cost, which we believe to

SHTF

(10.2)

31.6

49.8

normalize from FY19E onwards, which would propel RoA/RoE to 2.8%/20.7% in

FY20E. At CMP, the stock is trading at 2.1x FY20E ABV and 9x FY20E EPS. We

recommend a BUY on the stock with a target price of `1,760 (2.7x FY2020E

ABV).

3-year price chart

2000

Exhibit 1: Key Financials

1500

Y/E March (` cr)

FY16

FY17

FY18

FY19E

FY20E

1000

NII

5,052

5,561

6,771

8,042

9,702

500

YoY Growth (%)

32.0

10.1

21.8

18.8

20.6

0

PAT

1,178

1,257

1,569

2,315

3,284

YoY Growth (%)

-4.8

6.7

24.8

47.5

41.9

EPS

52

55

69

102

145

Source: Company, Angel Research

Adj Book Value

397

425

460

526

640

P/E

25

24

19

13

9

P/Adj.BV

3.3

3.1

2.9

2.5

2.1

Jaikishan J Parmar

ROE (%)

12.2

11.7

13.1

17.1

20.7

022 39357600, Extn: 6810

ROA (%)

1.9

1.8

1.9

2.4

2.8

Source: Company, Angel Research; Note: CMP as of June 28, 2018

Please refer to important disclosures at the end of this report

1

Shriram Transport Fin Co | Initiating Coverage

Company background

Shriram Transport Finance Company (SHTF) is a NBFC with differentiated business

model that pioneers in financing used commercial vehicles. The company also

focuses on small truck owners (having less than 5 trucks) with underdeveloped

banking habits. The company was established in 1979 and belongs to the

business conglomerate, Shriram Group. Started by financing pre-owned

commercial vehicles, the company has added ancillary services also to its portfolio.

As on date, SHTF has presence in almost all regions of the country with 1,213

branches. On the business operations front, its AUM reached `95,306cr and NIM

at 7.5% in FY18.

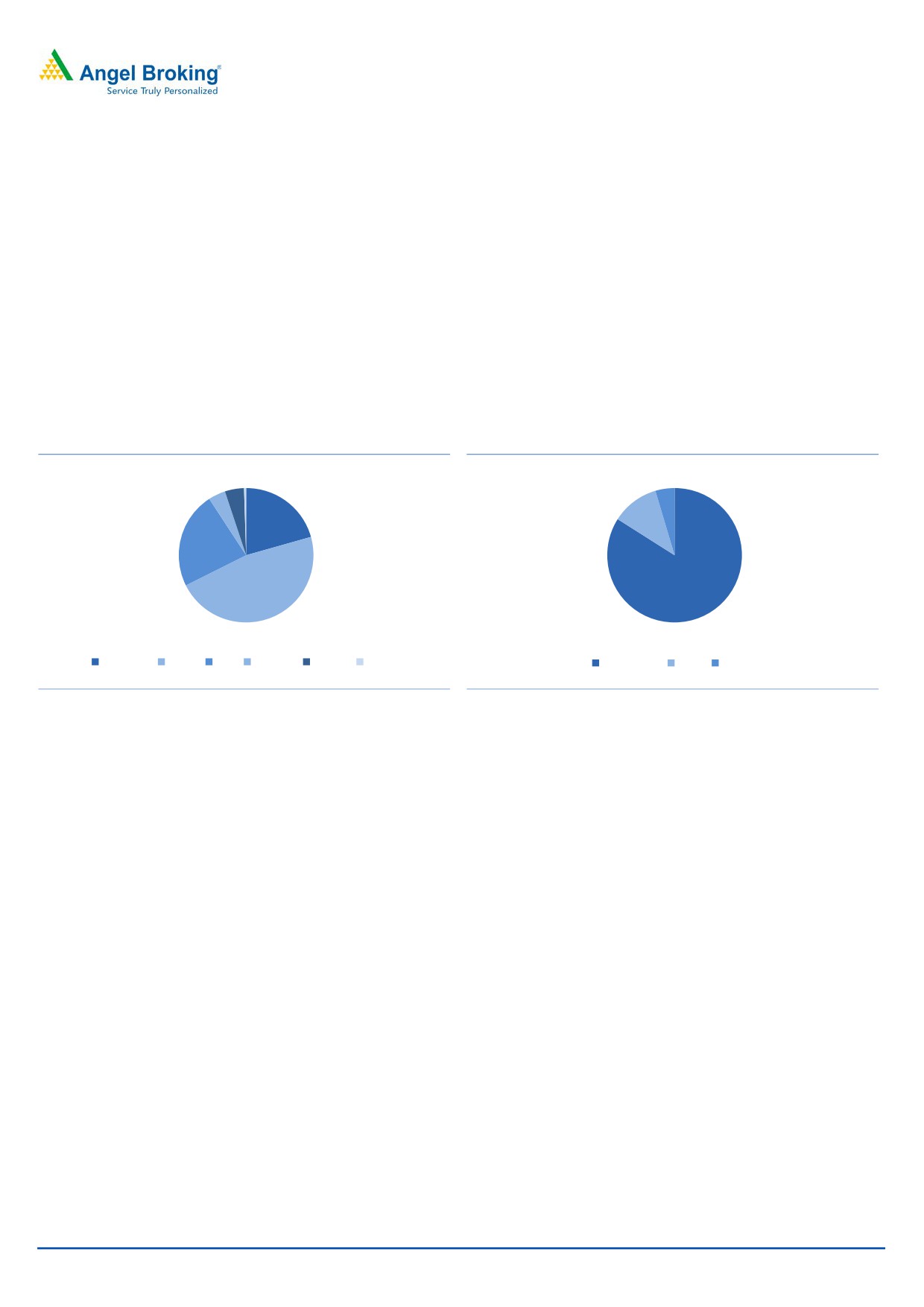

Exhibit 1: Loan Mix

Exhibit 2: Break Up of Used & New vehicles

1

4.6

5

4

21

11.4

23

47

84

M&LCVs

HCV

PV

Tractor

Other

Equipment

Pre Owned

New Other

Source: Company, Angel Research

Source: Company, Angel Research

Key Management Personnel

Mr. S. Lakshminarayan Chairman: Mr. Lakshminarayanan Subramanian is a non-

executive Director on the company’s Board. He holds Master’s degree in Science in

Chemistry and post graduate diploma from University of Manchester (U.K.) in

Advanced Social & Economic Studies.

Mr. Umesh Revankar MD & CEO: Mr. Umesh Govind Revankar holds a Bachelor’s

degree in business management from Mangalore University and a Master of

Business Administration (MBA) in finance. Mr. Revankar started his career with the

Shriram Group as an executive trainee in 1987. He has been associated with the

Shriram Group for the last 28 years and has extensive experience in the financial

services industry.

Mr. Parag Sharma CFO: Mr. Parag joined the company 1995 and now heads the

Finance functions of the company. He is a qualified Cost Accountant. He has over

27 years experience in finance industry.

June 29, 2018

2

Shriram Transport Fin Co | Initiating Coverage

Investment Argument

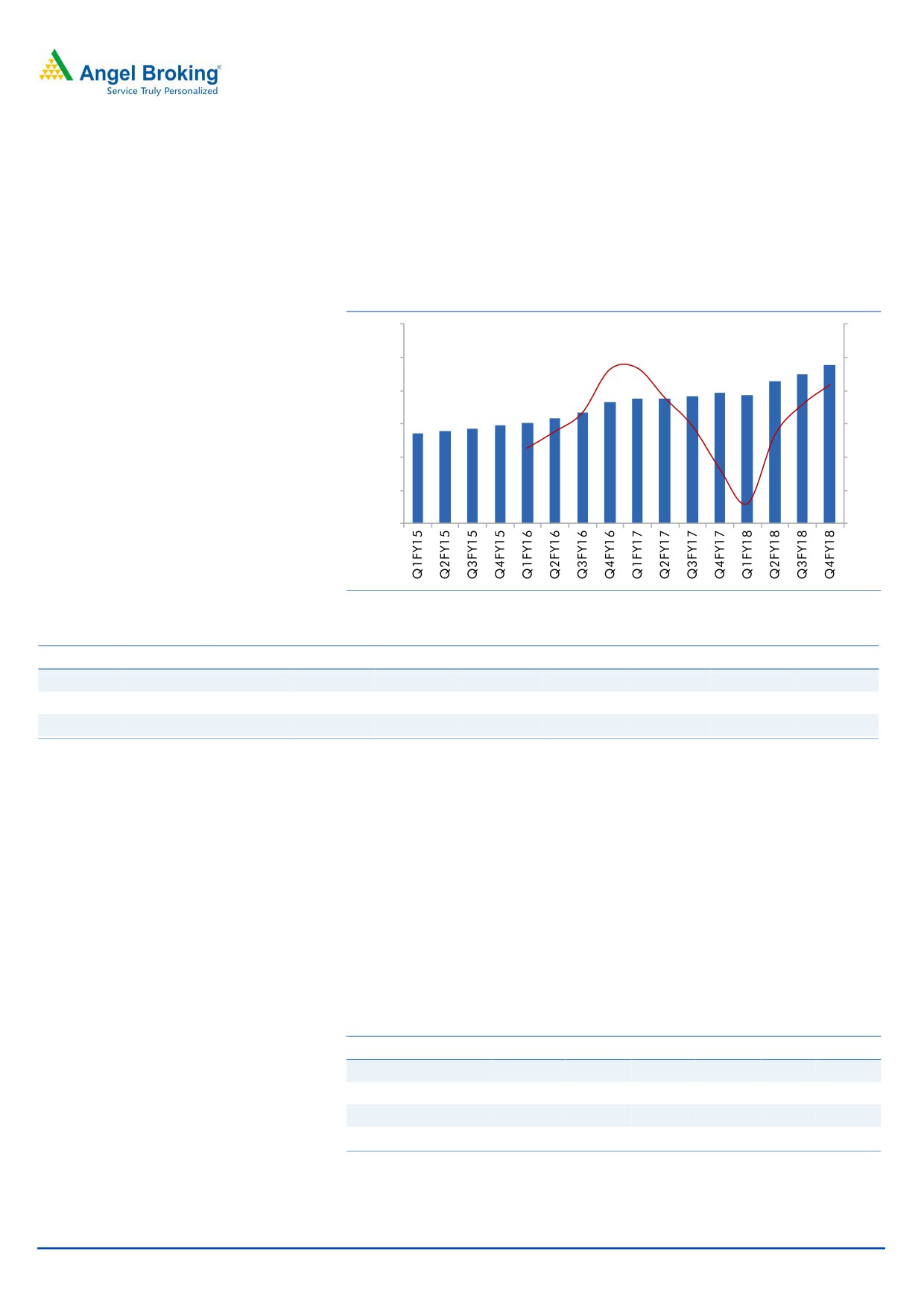

Multiple AUM growth levers: CV and M&HCV sales grew 20% and 25.5% yoy

respectively in FY18. We expect AUM growth momentum to continue led by

macro-economic revival; vehicles typically change hands in three years in good

economic environment and in five years in subdued economy.

Exhibit 3: AUM Trend (` in Cr)

12,000

30%

10,000

25%

8,000

20%

6,000

15%

4,000

10%

2,000

5%

0

0%

Source: Company

Exhibit 4: Vehicles Sold

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

LCV

2,87,777

3,61,846

4,60,831

5,24,887

4,32,233

3,82,206

3,83,307

4,11,703

5,16,140

MHCV

2,44,944

3,23,059

3,48,701

2,68,263

2,00,618

2,32,755

3,02,397

3,02,529

3,40,313

Total

5,32,721

6,84,905

8,09,532

7,93,150

6,32,851

6,14,961

6,85,704

7,14,232

8,56,453

Source: Company

The company’s business loans segment is also gaining traction and as on FY18 the

portfolio was ~`2,600cr. The business loans are given to existing customers who

have other business such as warehousing, petrol pump, workshop, crusher for the

bricks, etc. This strategy of the company would reduce NPA risks, as SHTF already

has the track record of the customers. Further, most of these people had been

borrowing from the local money lenders earlier, which provided SHTF an

opportunity to replace the money lenders’ loan with its business loans.

In FY18, company ramped up its rural distribution, which led to 49% yoy growth in

rural AUM (`3,100cr). In FY18, it opened 295 branches, higher than those added

in FY16/17. Out of 295 branches, 217 were opened in rural areas.

Exhibit 5: Branch & AUM distribution - Q4FY18 vs. Q4FY17

Branch

AUM (`cr)

Q4FY17

Q4FY18 % Change Q4FY17 Q4FY18 % Change

Rural

366

583

59%

208

310

49%

Urban

583

630

8%

580

643

11%

Total

949

1,213

28%

788

953

21%

Source: Company

June 29, 2018

3

Shriram Transport Fin Co | Initiating Coverage

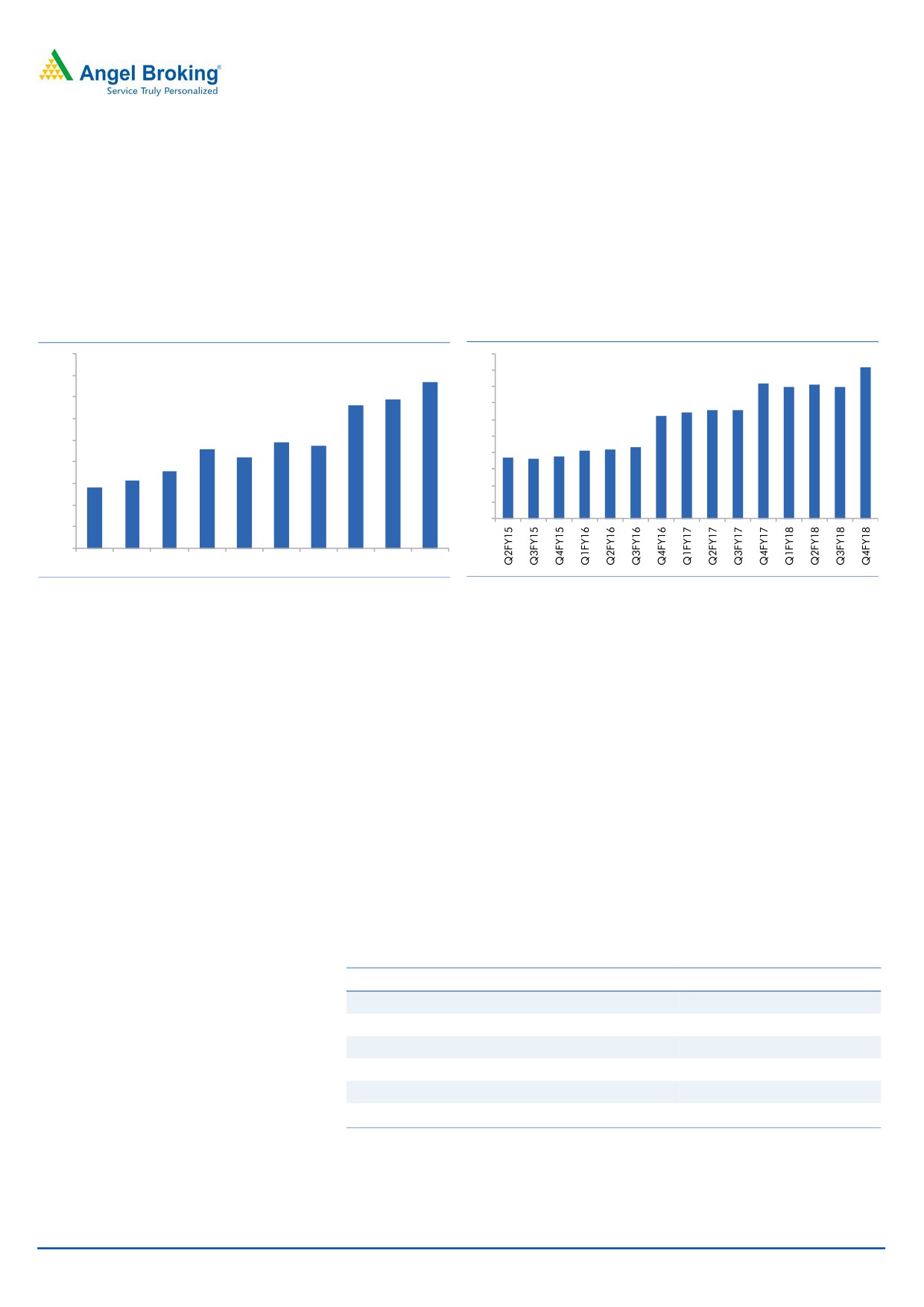

Stabilizing asset quality to lead to lower credit costs: SHTF recognized NPA on

180DPD basis till Q3FY16, but has gradually moved to 90DPD in Q4FY18. This

has led to spike in GNPA (from 3.8% in FY15 to 9.15% in FY18) and credit cost

(from 2.4 in FY15 to 3.8% in FY18). Credit cost over FY09-15 was in the range of

1.4-2.4% and due to a regulatory requirement; it reached 3.8% in Q4FY18. We

expect credit cost to fall by 140bps over FY18-20E, which would drive RoA

expansion.

Exhibit 6: Credit cost (%)

Exhibit 7: Jump in GNPA due to transition to 90DPD (%)

4.5

10

9.2

3.8

9

8.2

8

8.1

8

4.0

3.4

8

3.3

3.5

6.4

6.6

6.6

7

6.2

3.0

6

2.4

2.4

2.5

2.3

5

4.1

4.2

4.3

2.1

3.7

3.6

3.8

4

2.0

1.8

1.6

3

1.4

1.5

2

1.0

1

0

0.5

-

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

Source: Company, Angel Research

Source: Company, Angel Research

Since Q4FY16, SHTF GNPA and credit cost have been increasing primarily owing

to regulatory requirement (transition from 180DPD to 90DPD). Demonetization

and GST added further stress to the increasing GNPA. However, with improving

macros, fresh slippages should slow from Q1FY19 onwards.

NIM to remain stable: Going forward, we expect limited pressure on NIM despite

increase in bond yield.

Low competitive pressure in niche used CV market.

Recent effort to penetrate rural area would help to increase high yield assets.

Cost of borrowing, which is coming for repricing in FY19, is around 8.5% and

current G-sec yield is 8.8%. Hence, incremental cost of fund would be

minimal.

Exhibit 8: Borrowing Profile

Particular

(%)

NCD

39

Term Loan Bank

30

Fixed Deposit

16

Term loan Corporate

4

Working cap Loan

5

Subordinate Debt

7

Source: Company

June 29, 2018

4

Shriram Transport Fin Co | Initiating Coverage

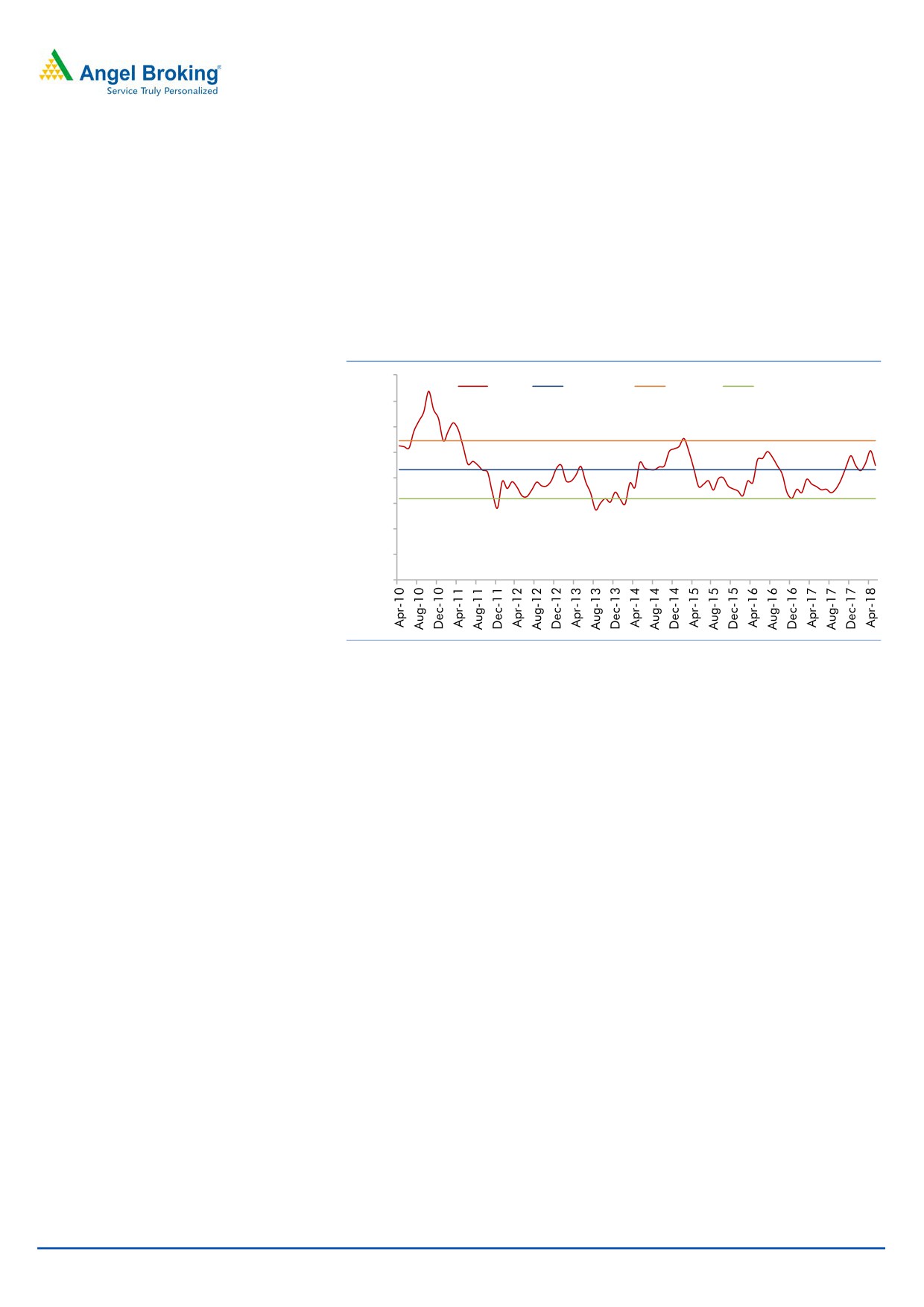

Outlook & Valuation: We expect SHTF’s AUM to grow at CAGR of 20% over FY18-

20E led by stronger CV volume, macro recovery and improving rural market. The

company’s return ration are at decade low levels (RoA/RoE - 1.9%/13% in FY18)

primarily owing to higher credit cost, which we believe to normalize FY19E

onwards, which would propel RoA/RoE to 2.8%/20.7% in FY20E. At CMP, the stock

is trading at 2.1x FY20E ABV and 9x FY20E EPS. We recommend a BUY on the

stock with a target price of `1,760 (2.7x FY2020E ABV).

Exhibit 9: P/BV chart

4.00

P/BV

Avg. P/BV

STD+1

STD-1

3.50

3.00

2.73

2.50

2.15

2.00

2.23

1.50

1.58

1.00

0.50

0.00

Source: Company, Angel Research

Risk

Sale of used CV is mostly linked to economic activity. Hence, any slowdown in

economy activity would impact the company’s AUM growth.

Any sudden spike in interest rate cycle may adversely impact the company’s NIM.

June 29, 2018

5

Shriram Transport Fin Co | Initiating Coverage

Income Statement

Y/E March ( `cr)

FY15

FY16

FY17

FY18

FY19E

FY20E

NII

3,827

5,052

5,561

6,771

8,042

9,702

- YoY Growth (%)

9.5

32.0

10.1

21.8

18.8

20.6

Other Income

428

184

82

248

134

160

- YoY Growth (%)

(6.9)

(57)

(55.5)

202.9

(46.1)

19.7

Operating Income

4,255

5,236

5,643

7,019

8,176

9,862

- YoY Growth (%)

7.6

23.1

7.8

24.4

16.5

20.6

Operating Expenses

1,123

1,347

1,275

1,524

1,764

2,113

- YoY Growth (%)

14.7

20.0

(5.4)

19.6

15.7

19.8

Pre - Provision Profit

3,132

3,888

4,368

5,495

6,412

7,749

- YoY Growth (%)

5.2

24.2

12.3

25.8

16.7

20.9

Prov. & Cont.

1,289

2,107

2,444

3,122

2,905

2,773

- YoY Growth (%)

12.2

63.4

16.0

27.7

(7)

(4.5)

Profit Before Tax

1,842

1,781

1,924

2,373

3,507

4,976

- YoY Growth (%)

0.8

(3.3)

8.0

23.3

47.8

41.9

Prov. for Taxation

605

603

667

804

1,192

1,692

- as a % of PBT

32.8

33.9

34.6

33.9

34.0

34.0

PAT

1,238

1,178

1,257

1,569

2,315

3,284

- YoY Growth (%)

(2.1)

(4.8)

6.7

24.8

47.5

41.9

Source: Company

Balance Sheet

Y/E March ( ` cr)

FY15

FY16

FY17

FY18

FY19E

FY20E

Share Capital

227

227

227

227

227

227

Reserve & Surplus

9,011

9,927

11,075

12,345

14,292

17,053

Networth

9,238

10,154

11,302

12,572

14,519

17,280

Borrowing

44,276

49,791

53,110

63,320

75,494

90,007

- YoY Growth (%)

23.2

12.5

6.7

19.2

19.2

19.2

Other Liab. & Prov.

5,813

8,018

9,998

12,578

15,183

18,629

Total Liabilities

59,327

67,963

74,410

88,470

1,05,195

1,25,917

Investment

3,327

1,356

1,549

1,480

1,480

1,480

Cash

4,723

2,364

4,441

3,638

3,944

4,733

Advance

49,227

61,878

65,463

79,673

95,608

1,14,729

- YoY Growth (%)

34.9

25.7

5.8

21.7

20.0

20.0

Fixed Asset

101

101

84

120

144

151

Other Assets

1,949

2,264

2,874

3,560

4,020

4,824

Total Asset

59,327

67,963

74,410

88,470

1,05,195

1,25,917

Growth (%)

20.5

14.6

9.5

18.9

18.9

19.7

Source: Company

June 29, 2018

6

Shriram Transport Fin Co | Initiating Coverage

Key Ratio

Y/E March

FY15

FY16

FY17

FY18

FY19E

FY20E

Profitability ratios (%)

NIMs

8.3

8.7

8.5

9.1

9.0

9.1

Cost to Income Ratio

26.4

25.7

22.6

21.7

21.6

21.4

RoA

2.3

1.9

1.8

1.9

2.4

2.8

RoE

14.1

12.2

11.7

13.1

17.1

20.7

Asset Quality (%)

Gross NPAs (%)

3.80

6.20

8.20

9.15

9.0

8.0

GNPA Amt

1,894

3,870

5,408

7,376

8,605

9,178

Net NPAs

0.8

1.9

2.7

2.83

2.7

2.4

NPA Amt

379

1,144

1,659

2,131

2,581

2,753

Provision Coverage

78.9

69.4

67.1

69.1

70.0

70.0

Credit Cost

2.4

3.3

3.4

3.8

3.0

2.4

Per Share Data (`)

EPS

55

52

55

69

102

145

ABVPS

390

397

425

460

526

640

DPS

8

10

10

11

16

23

BVPS

407

448

498

554

640

762

Valuation Ratios (x)

PER

24.1

25.4

23.8

19.0

12.9

9.1

P/ABVPS

3.4

3.3

3.1

2.9

2.5

2.1

P/BVPS

3.2

2.9

2.6

2.4

2.1

1.7

Dividend Yield (%)

0.6

0.8

0.8

0.8

1.2

1.7

Note - Valuation done on closing price of 28/06/2018

June 29, 2018

7

Shriram Transport Fin Co | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER:

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India

Limited, Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository

Participant with CDSL and Portfolio Manager and Investment Adviser with SEBI. It also has registration with AMFI as a Mutual

Fund Distributor. Angel Broking Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research

Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not been debarred/ suspended

by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its associates/analyst has not

received any compensation / managed or co-managed public offering of securities of the company covered by Analyst during

the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any

investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this

document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in

the securities of the companies referred to in this document (including the merits and risks involved), and should consult their

own advisors to determine the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions

and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a

company's fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our

website to evaluate the contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other

reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as

such, as this document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall

not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the

information contained in this report. Angel Broking Pvt. Limited has not independently verified all the information contained

within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the

accuracy, contents or data contained within this document. While Angel Broking Pvt. Limited endeavors to update on a

reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent

us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be

reproduced, redistributed or passed on, directly or indirectly.

Disclosure of Interest Statement

Shriram Transport Fin

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

June 29, 2018

8