IPO Note | Chemicals

October 27, 2015

S H Kelkar and Company

AVOID

Issue Open: October 28, 2015

IPO Note - Valuation expensive

Issue Close: October 30, 2015

S H Kelkar & Company Ltd (SHKCL) is the largest fragrance and flavour company

Issue Details

in India by revenue, with a market share of approximately 12.0%. The company

has four manufacturing facilities, three of which are located in India and one in

Face Value: `10

The Netherlands, with a total installed manufacturing capacity of over 19,819

Present Eq. Paid up Capital: `133.0cr

tonne annually.

Offer Sale:1.7cr Shares

Established Market Leadership: The company has established brands like SHK,

Cobra and Keva, which enjoy leadership positions in their respective categories

Post Eq. Paid up Capital: `144.6cr

and draw substantial brand equity in India. For the year ended December 31,

Market Lot: 80 Shares

2013, SHKCL had a market share of 12.0% in the Indian fragrance and flavour

(F&F) industry. On bifurcating, the company’s market share stood at 20.5% in the

Fresh Issue (amount): `210cr

fragrance industry and 2.0% in the flavour industry.

Price Band: `173-180

Comprehensive Product Offering and Diverse Customer Base: SHKCL has a wide

Post-issue implied mkt. cap `2,502cr*-

portfolio of offerings with over 9,700 fragrances, ingredients and flavour products

2,603cr**

and a large library of product formulations created over the past 90 years. The

Note:*at Lower price band and **Upper price band

company enjoys a competitive advantage over its peers on the back of its wide

product portfolio. It has a deep understanding of its customers’ requirements and

preferences and has over 4,100 customers, including leading national and

Book Building

multi-national FMCG companies, blenders of fragrances and flavours, and

QIBs

50%

fragrance and flavour producers.

Non-Institutional

15%

Outlook and Valuation: SHKCL is valued at a P/E multiple of 40.4x its FY2015

EPS. In terms of P/BV, the company is valued at 5.1x its pre-IPO and 3.2x its post-

Retail

35%

IPO at the upper end of the price band. In our view, the valuation is expensive,

considering its low ROE numbers (around 12-13%) and considering that they are

expected to continue to remain in the same range. Further, the domestic F&F industry is

Post Issue Shareholding Pattern(%)

not a high growth industry, expected to grow at a subtle rate of 9-10% going forward.

Promoters Group

56.7

The company’s global peers Givaudan S.A. and International Flavors &

MF/Banks/Indian

Fragrances Inc trade at 28.1x and 20.1x their CY2014 earnings, respectively.

FIs/FIIs/Public & Others

43.3

Givaudan S.A. and International Flavors & Fragrances Inc have strong market

shares in the global market of ~21% and ~12%, respectively, and deliver higher

RoEs. On the other hand, SHKCL has negligible market share at the global level.

Thus, SHKCL’s valuation looks expensive vis-a-vis these companies.

Hence, we recommend an “Avoid” on the issue. Investors having conviction in the

long term growth prospects of the company and the emerging consumption story in

India, and wanting to enter the stock to tap this perceived opportunity, could consider

waiting for a possible correction in the stock price post the listing of the IPO.

Key Financials

Y/E March (` cr)

FY2013

FY2014

FY2015E

1QFY16E

Net Sales

666

761

837

222

% chg

16.9

14.3

9.9

-

Net Profit

58

79

64

21

% chg

31.0

46.6

(18.6)

-

OPM (%)

17.7

18.0

14.3

17.3

EPS (`)

4.1

6.0

4.8

1.6

P/E (x)

44.3

30.2

37.2

-

P/BV (x)

5.0

5.0

4.7

-

RoE (%)

12.3

16.4

12.6

Amarjeet S Maurya

EV/Sales (x)

3.7

3.3

3.0

-

+91 22 3935 7800 Ext: 6831

EV/EBITDA (x)

20.8

18.5

21.2

-

Source: Company, Angel Research; Note:*EPS and other valuation parameters is based on Pre IPO

outstanding shares at upper price band

Please refer to important disclosures at the end of this report

1

S H Kelkar and Company | IPO Note

Company background

SHKCL is the largest F&F company in India by revenue, with a market share of

approximately 12.0%. The company initiated business in 1922 as a manufacturer

of industrial perfumes in British India. It now has four manufacturing facilities,

three of which are located in India and one in The Netherlands, with a total

installed manufacturing capacity of over 19,819 tonne annually.

Last year, the company manufactured and supplied over 6,300 fragrances. The

offerings included fragrance ingredients and flavours for the personal and home

care products industry and the food and beverage industry, either in the form of

compounds or individual ingredients. The company has a large and diverse mix of

over 3,500 customers, including leading national and multi-national FMCG

companies, blenders of F&F, and F&F producers.

The flavour products produced by the company are used as a raw material by

producers of baked goods, dairy products, beverages and pharmaceutical

products. The company has over 300 customers for its flavour products and a

dedicated research team of 18 scientists. The research team has developed 12

molecules over the last three years, of which, the company has filed patent

applications for three.

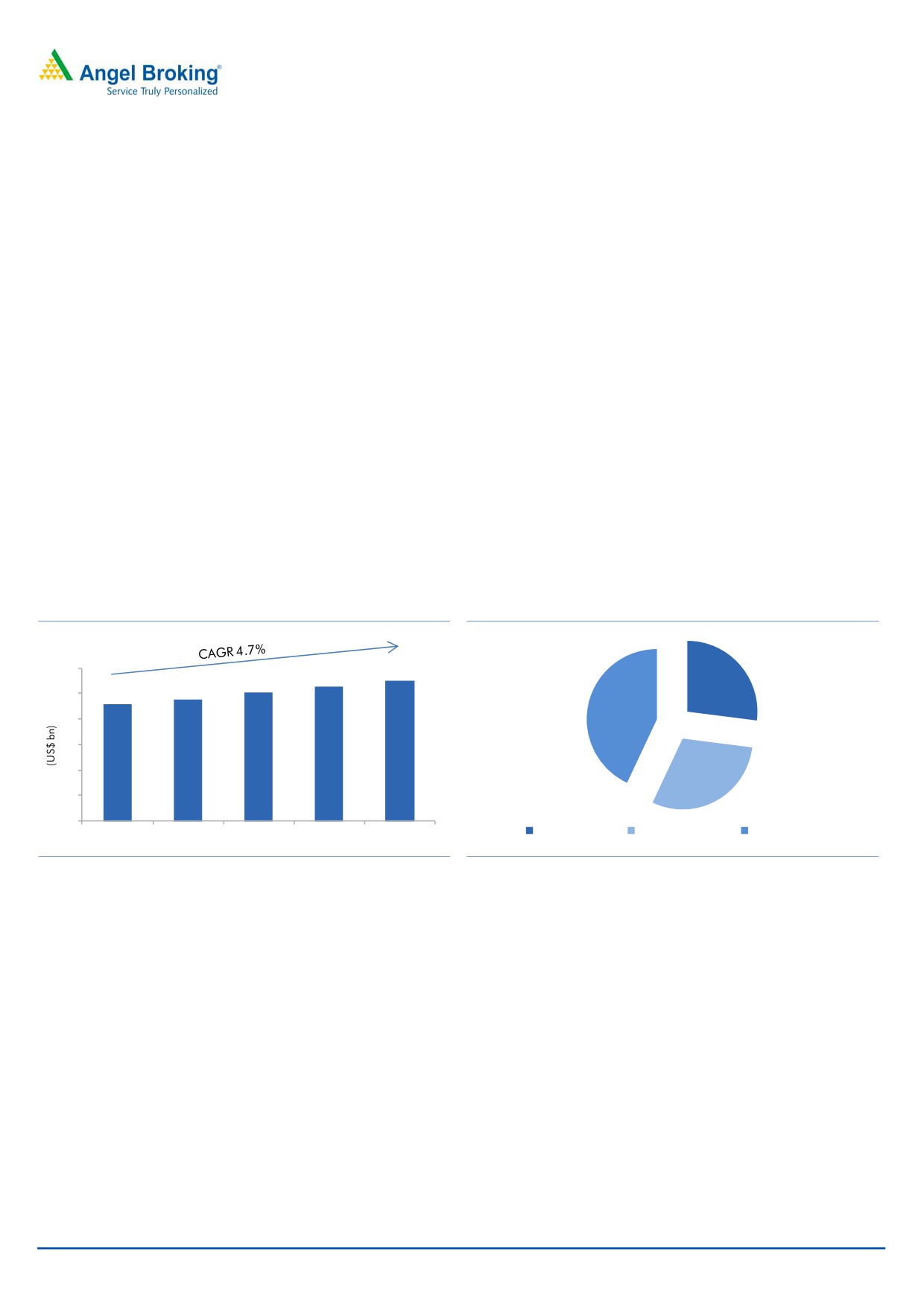

Exhibit 1: Global fragrance and flavour industry

Exhibit 2: Geographic revenue break-up for FY13

30

27.5

26.3

25.2

27%

23.9

25

22.9

43%

20

15

10

30%

5

0

North American

Western European

Rest of the world

CY2012

CY2013

CY2014

CY2015

CY2016

Source: RHP

Source: RHP

October 27, 2015

2

S H Kelkar and Company | IPO Note

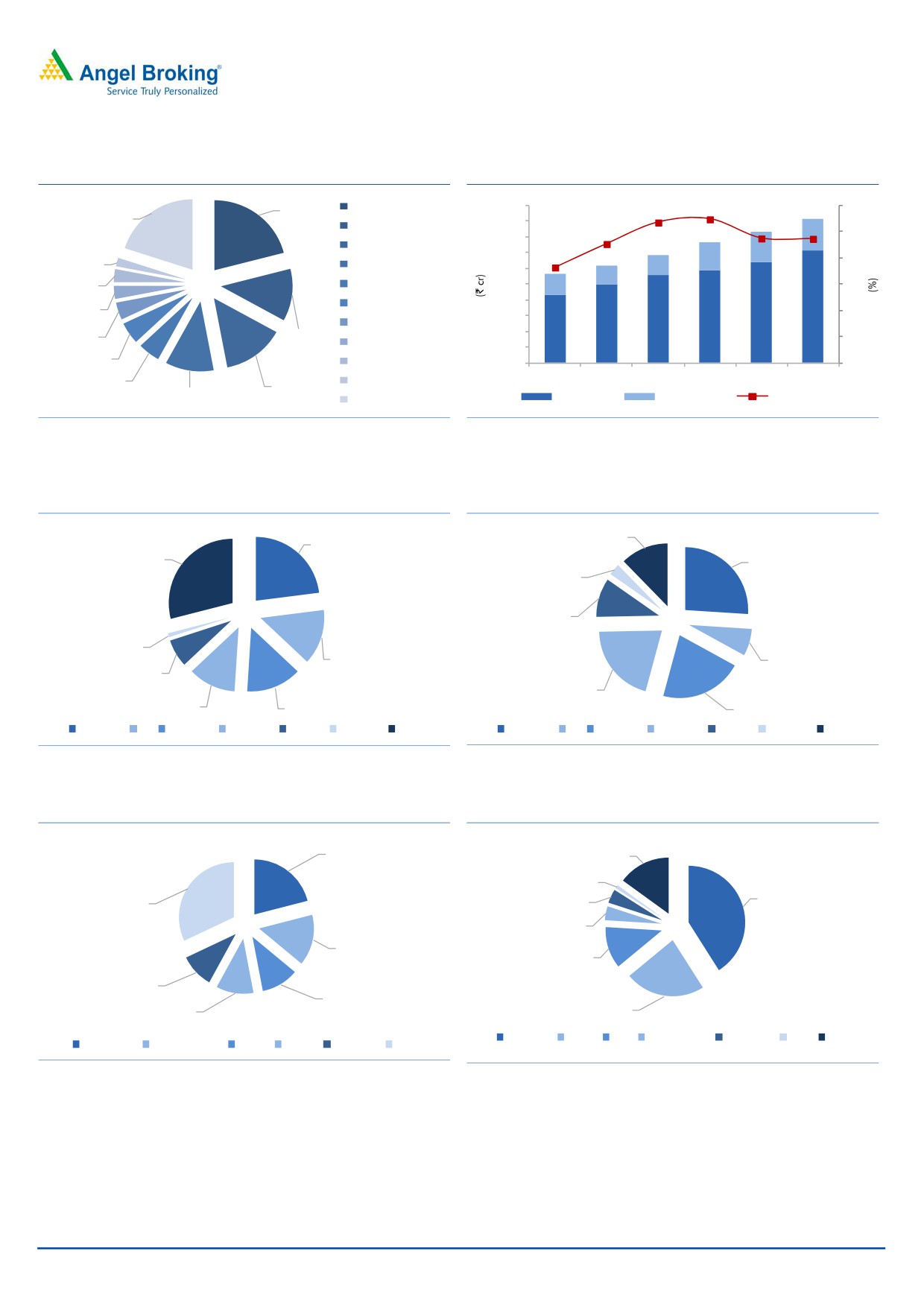

Exhibit 3: Market shares of the top 10 players in the

Exhibit 4: Organised and unorganised Indian

global fragrance and flavour industry

fragrance and flavour industry trend.

21.0%

Givaudan

5,000

10.7

11.0

12

20.0%

4,500

9.5

IFF

9.1

10

4,000

1,014

Firmenich

967

9.5

3,500

7.3

2.0%

879

8

Symrise

654

3,000

601

3.0%

Takasago

2,500

672

6

Wild Flavors

2,000

3.0%

3,548

1,500

3,200

4

Mane SA

2,775

2,926

12.0%

2,496

4.0%

1,000

2,167

Frutarom

2

500

5.0%

Sensient Flavors

-

0

5.0%

Robertet SA

CY2011

CY2012

CY2013

CY2014

CY2015

CY2016

14.0%

11.0%

Organised

Unorganised

yoy growth (%)

Others

Source: RHP

Source: RHP

Exhibit 5: Market share in Indian F&F

industry

Exhibit 6: Market share in Indian Fragrance industry

`34.29bn

`18.8bn

12.3%

23%

29%

26.0%

3.0%

10.0%

1%

14%

7.0%

7%

20.5%

12%

14%

21.2%

Givaudan IFF Firmenich SH Kelkar Symrise Goldfield Others

Givaudan IFF Firmenich SH Kelkar Symrise Goldfield Others

Source: RHP

Source: RHP

Exhibit 7: End user industry for fragrances

Exhibit 8: End user industry for Flavours

21%

15%

1%

41%

32%

4%

4%

15%

12%

10%

11%

11%

23%

Beverages Bakery Oral Confectionery Salty snack Dairy Others

Home care Personal wash Fabric Beauty Hair care

Others

Source: Company, Angel Research

Source: Company, Angel Research

October 27, 2015

3

S H Kelkar and Company | IPO Note

Issue details

The company’s `210cr IPO comprises of a fresh issue/Offer for Sale of upto

1.66cr shares, in which Blackstone PE Fund is selling ~10% share and the

promoter is selling ~2.5% share of the total pre-IPO outstanding shares. Shares

could be subscribed to in the price band of `173-180 (face value of shares: `10/-

each) via the book building route. The fresh issue of shares will constitute ~8% (at

the upper end of the price band) of the post-issue paid-up equity share capital of

the company.

Exhibit 9: Shareholding pattern

Particulars

Pre-Issue

Post-Issue

No. of shares

(%)

No. of shares

(%)

Promoter group

853,52,000

64.2

820,14,414

56.7

Others

476,02,135

35.8

626,06,388

43.3

Total

1329,54,135

100.0

1446,20,802

100.0

Source: Company, Angel Research Note: calculation is based on upper price band

Objects of the Fresh Issue are as below

Repayment/pre-payment in full or in part of certain loans availed by the

company - `126cr

Investment in its subsidiary K.V. Arochem Pvt Ltd (KVA) and for

repayment/prepayment of certain loans availed by KVA in full or in part -

`32cr.

The balance would be utilized towards general corporate purposes.

October 27, 2015

4

S H Kelkar and Company | IPO Note

Key investment rational

Established Market Leadership

The company has established brands like SHK, Cobra and Keva which enjoy

leadership positions in their respective categories, and have substantial brand

equity in India. For the year ended December 31, 2013, SHKCL had a market

share of 12.0% in the Indian F&F industry. For the same period, the company had

a market share of 20.5% in the Indian fragrance industry and 2.0% in the Indian

flavour industry. (Source: “Market Study on Fragrances and Flavours” by Nielsen,

March 22, 2015). The company is the largest domestic fragrance producer in

India, while it also exports fragrance products to over 52 countries.

Comprehensive Product Offering and Diverse Customer Base

SHKCL has a wide product portfolio with over 9,700 fragrances, ingredients and

flavour products and a large library of product formulations created over 90 years.

The company enjoys a competitive advantage over its peers on the back of its wide

product portfolio. It has a deep understanding of its customers’ requirements and

preferences and has over 4,100 customers, including leading national and multi-

national FMCG companies, blenders of fragrances and flavours, and fragrance

and flavour producers. The company enjoys long term relationships with several

customers for its F&F products spanning over 15 years. Its diversified and

comprehensive product portfolio and large customer base, spread across several

countries and customer categories, mitigates concentration risk.

Research and development skills

SHKCL has a strong research & development (R&D) team, which has contributed to

the company’s growth over the past several years. The company currently

employs 18 scientists; over the last three years the R&D team has developed

12 molecules, of which, patent applications have been filed for three

molecules by the company. As in FY2015, the company had 12 perfumers and

2 flavourists in its

5 creation and development centres. The company

developed over 502 new fragrance and flavour compounds during the year,

which it sold commercially.

Experienced Promoters and Management Team

SHKCL is led by a qualified and experienced management team that has the

expertise and vision to manage and grow business. Its Promoters have an

experience of over 50 years in the fragrance industry and of over 15 years in the

flavour industry. Its senior and mid-level management teams are also very

experienced, having worked in large multi-national companies, in the F&F and

FMCG industries, with an average experience of over 20 years. The knowledge

and experience of its Promoters, senior and middle-management, and its team of

R&D personnel and perfumers provides the company a significant competitive

advantage as it seeks to expand in its existing markets and enter new geographic

markets.

October 27, 2015

5

S H Kelkar and Company | IPO Note

Valuation

SHKCL is valued at a P/E multiple of 40.4x its FY2015 EPS. In terms of P/BV, the

company is valued at 5.1x its pre-IPO and 3.2x its post-IPO at the upper end of the

price band. In our view, the valuation is expensive, considering its low ROE numbers

(around 12-13%) and considering that they are expected to continue to remain in the

same range. Further, the domestic F&F industry is not a high growth industry, expected to

grow at a subtle rate of 9-10% going forward.

The company’s global peers Givaudan S.A. and International Flavors &

Fragrances Inc trade at 28.1x and 20.1x their CY2014 earnings, respectively.

Givaudan S.A. and International Flavors & Fragrances Inc have strong market

shares in the global market of ~21% and ~12%, respectively, and deliver higher

RoEs. On the other hand, SHKCL has negligible market share at the global level.

Thus, SHKCL’s valuation looks expensive vis-a-vis these companies.

Hence, we recommend an “Avoid” on the issue. Investors having conviction in the

long term growth prospects of the company and the emerging consumption story in

India, and wanting to enter the stock to tap this perceived opportunity, could consider

waiting for a possible correction in the stock price post the listing of the IPO.

Exhibit 10: Valuation table

Year

Currency

Net Sales

EBITDA

Margin (%)

PAT

PE

ROE

*S H Kelkar & Company

FY2015

` cr

837

119

14.3

64

40.4

12.6

Givaudan S.A.

CY2014

CHF mn

4,404

760

17.3

563

28.1

16.5

International Flavors & Fragrances Inc

CY2014

US$ mn

3,089

601

19.5

449

20.1

29.5

Source: Company, Angel Research, Note: * EPS and other valuation parameters is based on Post IPO outstanding shares at upper price band

Risks to upside

Higher than expected growth in the FMCG industry and launches of strong

brands by the company would be a risk to our recommendation.

Decline in input costs for the company could increase the profitability of the

company.

October 27, 2015

6

S H Kelkar and Company | IPO Note

Consolidated Profit & Loss Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

1QFY16

Total operating income

666

761

837

222

% chg

16.9

14.3

9.9

Total Expenditure

548

624

718

184

Raw Materials Costs

351

399

466

125

Personnel Expenses

89

103

115

26

Others Expenses

108

122

137

33

EBITDA

118

137

119

39

% chg

13.1

16.1

(12.9)

-

(% of Net Sales)

17.7

18.0

14.3

17.3

Depreciation& Amortisation

17

19

29

7

EBIT

101

118

90

31

% chg

15.7

17.4

(23.9)

(% of Net Sales)

15.1

15.5

10.8

14.1

Interest & other Charges

22

18

19

5

Other Income

2

8

23

2

(% of PBT)

1.9

7.2

24.6

6.4

Share in profit of Associates

-

-

-

-

Recurring PBT

80

109

95

28

% chg

(74.0)

34.8

(12.7)

Prior Period & Extraordinary Exp./(Inc.)

(2)

-

-

-

PBT (reported)

83

109

95

28

Tax

24

29

30

8

(% of PBT)

29.3

27.1

32.1

26.7

PAT (reported)

58

79

64

21

Less: Minority interest (MI)

-

-

0

-

PAT after MI (reported)

58

79

64

21

% chg

31.0

46.6

(18.6)

-

(% of Net Sales)

8.8

10.4

7.7

9.3

Basic EPS (`)

4.1

6.0

4.8

1.6

Note: *EPS calculation is based on Pre IPO outstanding shares

October 27, 2015

7

S H Kelkar and Company | IPO Note

Consolidated Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

1QFY16

SOURCES OF FUNDS

Equity Share Capital

12

14

141

141

Reserves& Surplus

412

467

369

397

Equity Application Money

52

-

-

-

Shareholders Funds

477

481

510

538

Minority Interest

-

-

-

-

Total Loans

133

184

214

176

Deferred Tax Liability

6

6

5

5

Total Liabilities

616

671

728

719

APPLICATION OF FUNDS

Net Block

140

169

196

192

Capital Work-in-Progress

43

50

10

15

Goodwill

71

83

78

83

Investments

41

0

0

0

Current Assets

480

557

650

629

Inventories

225

279

318

308

Sundry Debtors

172

179

195

215

Cash

33

42

76

40

Loans & Advances

47

56

56

60

Other Assets

2

2

5

7

Current liabilities

164

196

216

212

Net Current Assets

316

361

434

417

Deferred Tax Asset

5

8

10

12

Mis. Exp. not written off

-

-

-

-

Total Assets

616

671

728

719

October 27, 2015

8

S H Kelkar and Company | IPO Note

Consolidated Cash Flow Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

1QFY16

Profit before tax

78

109

95

28

Depreciation

17

19

29

7

Change in Working Capital

11

(73)

(38)

(13)

Interest / Dividend (Net)

0

(1)

(0)

(0)

Direct taxes paid

(26)

(34)

(28)

(12)

Others

23

13

5

6

Cash Flow from Operations

103

32

62

16

(Inc.)/ Dec. in Fixed Assets

(26)

(105)

(18)

(6)

(Inc.)/ Dec. in Investments

(8)

41

0

-

Cash Flow from Investing

(33)

(64)

(17)

(6)

Issue of Equity

1

-

-

-

Inc./(Dec.) in loans

(79)

52

32

(41)

Dividend Paid (Incl. Tax)

(11)

-

(18)

-

Interest / Dividend (Net)

28

(16)

(22)

(7)

Cash Flow from Financing

(61)

36

(7)

(48)

Inc./(Dec.) in Cash

9

4

37

(38)

Opening Cash balances

19

29

35

72

Effect of exch. rate changes

0

2

1

1

on cash & bank bal.

Closing Cash balances

29

35

72

36

October 27, 2015

9

S H Kelkar and Company | IPO Note

Key Ratios

Y/E March

FY2013E

FY2014

FY2015

Valuation Ratio (x)

P/E (on FDEPS)

44.3

30.2

37.2

P/CEPS

33.6

24.4

25.6

P/BV

5.0

5.0

4.7

EV/Sales

3.7

3.3

3.0

EV/EBITDA

20.8

18.5

21.2

EV / Total Assets

3.1

2.9

2.7

Per Share Data (`)

EPS (Basic)

4.1

6.0

4.8

EPS (fully diluted)

4.1

6.0

4.8

Cash EPS

5.4

7.4

7.0

Book Value

35.9

36.2

38.4

Returns (%)

ROCE

16.5

17.8

12.4

Angel ROIC (Pre-tax)

18.8

19.0

13.9

ROE

12.3

16.4

12.6

Turnover ratios (x)

Inventory / Sales (days)

123

134

138

Receivables (days)

94

86

85

Payables (days)

40

42

15

WC cycle (ex-cash) (days)

177

178

208

Note:*EPS and other valuation parameters is based on Pre IPO outstanding shares at upper price

band

October 27, 2015

10

S H Kelkar and Company | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

October 27, 2015

11