IPO Note | Financials

Oct 24, 2017

SUBSCRIBE

Reliance Nippon Life Asset Management Ltd

sue Open: Oct 25, 2017

Is

Issue Close: Oct 27, 2017

Reliance Nippon Life Asset Management Ltd (RNAM) is the third largest Asset

Management Company (AMC) in terms of quarterly average AUM (QAAUM) with

11.4% market share and is ranked second most profitable AMC. RNAM managed

Issue Details

`3,84,061cr as on August 2017, which includes Mutual Fund (`2,28,329cr),

Face Value: `10

Managed Account

(`1,53,509cr) and offshore funds & advisory mandates

Present Eq. Paid up Capital: `41.5cr

(`2,223cr). It is also the second largest AMC among retail investors (market share

of 13.6%), having 7.01 million investor folios, of which 6.72 million retail folios.

Offer for Sale: **3.67cr Shares

Huge potential for growth (Industry) in Mutual Fund AUM: In the past three years,

Fresh issue: `617cr

equity assets under management for Indian MF industry have increased three-

fold, from ` 2 lakh cr to `7 lakh cr. Overall AUM has nearly doubled from `10

Post Eq. Paid up Capital: `66cr

lakh cr to `20 lakh cr. Moreover, the industry is receiving about `5,000cr per

Issue size (amount): *`1,512cr -

month through SIP (Systematic Investment Plan). We believe that this trend would

**1,542 cr

continue in the coming years owing to (1) Continuation of black money crack

down;

(2) Lower fixed deposit rates;

(3) Increase in awareness;

(4) Low

Price Band: `247 - 252

penetration (AUM/GDP -13% v/s. +50% in developed market).

Lot Size: 59 shares and in multiple

thereafter

Wide distribution network with strong focus on retail investors: RNAM has a pan-

Post-issue implied mkt. cap:

India network of 171 branches, of which 132 branches are located in B15

*`15,116cr - **`15,422cr

(Beyond top 15 Cities) locations. Distributors contributed 54% and Direct 46% of

Promoters holding Pre-Issue: 96%

monthly average AUM on June 2017. Retail contribution to total AAAUM has

increased by 1600bps to 26.5% from FY2013 to FY2017. Its MF AUM has grown

Promoters holding Post-Issue: 86%

at healthy CAGR of 26% over FY2013-17. PAN India presence & superior fund

*Calculated on lower price band

performance would continue to help them to garner big chunk of new flow.

** Calculated on upper price band

Healthy financials to support higher dividend payout: Revenue/EBITDA has grown

Book Building

at healthy CAGR of 21%/28% over FY2013-17. Return on equity (ROE) for

FY2017 was 21.3% and last 5 years average ROE was 20%. For FY2017, RNAM

QIBs

50% of issue

made dividend payout of 61% and it has maintain dividend payout of 55% on an

Non-Institutional

15% of issue

average for last 5 years.

Retail

35% of issue

Outlook & Valuation: At the upper end of the IPO price band it is offered at 37x

its FY2017 EPS and 8x its FY2017 book value (Pre-IPO), demanding `15,442cr

market cap, which is 6.8% of the MF AUM (`2,28,329cr for the month of August

Post Issue Shareholding Patter

2017). Considering that RNAM is the third largest AMC coupled with huge

Promoters

86%

potential of MF industry to grow, strong return ratios, asset light business, higher

dividend payout ratio and track record of superior investment performance, we

Others

14%

are positive on this IPO and rate it as SUBSCRIBE.

Key Financials

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

Net Sales

609

676

847

1,200

1,307

% chg

11.0

25.4

41.6

9.0

Net Profit

230

271

354

396

403

% chg

17.5

31.0

11.8

1.6

EBITDA (%)

29

36

43

34

36

EPS (Rs)

4

5

6

7

7

P/E (x)

64

55

42

37

37

P/BV (x)

10

10

10

8

8

Jaikishan J Parmar

ROE (%)

16

17

23

22

21

+022 39357600, Extn: 6810

ROA (%)

15

16

21

21

20

Source: RHP, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

Please refer to important disclosures at the end of this report

1

Reliance Nippon Life Asset Management Ltd | IPO Note

Company background

Reliance Nippon Life Asset Management Ltd is a joint venture between Reliance

ADAG and Nippon Life of Japan (formerly Reliance Capital Asset Management

Limited). It began mutual fund operations in 1995 as the asset manager for

Reliance Mutual Fund, managed QAAUM of

`2,22,964cr and 7.01 million

investor folios, as of June 30, 2017. It is managing 55 open-ended mutual fund

schemes including 16 ETFs and 174 closed ended schemes for Reliance Mutual

Fund as of June 30, 2017. RNAM has a pan-India network of 171 branches and

approximately 58,000 distributors including banks, financial institutions, national

distributors and independent financial advisors (“IFAs”), as of June 30, 2017.

The company is involved in managing

Mutual Funds (Including EFTs)

Managed account, including portfolio management services (PMS), alternative

investment funds (AIF) and Pension funds

Offshore funds and advisory mandates

Exhibit 1: fund wise information on mutual fund AUM

2015

2016

2017

Q1FY18

% of total

% of total

% of total

% of total

` in Cr

` in Cr

` in Cr

` in Cr

QAAUM

QAAUM

QAAUM

QAAUM

Debt

5,74,936

46

70,151

46

93,888

50

1,02,840

46

Equity

3,59,510

29

48,981

32

53,360

28

64,410

29

Debt - Liquid

2,90,011

23

32,299

21

36,216

19

41,564

19

Gold

17,232

1

1,369

1

1,953

1

2,674

1

ETF

3,379

0.3

453

0.3

3,744

2

11,475

5

12,45,068

100

1,53,251

100

1,89,161

100

2,22,964

100

Source: RHP

Oct 24, 2017

2

Reliance Nippon Life Asset Management Ltd | IPO Note

Issue details

The IPO of Reliance Nippon Life AMC, a joint venture of Reliance group (ADAG)

and Japan’s Nippon Life, aims to raise `1,542cr through mix of Offer for sale and

fresh issue. The issue would constitute fresh issue worth of `617cr and Offer for

sale worth of `925cr. The company would divest 10% of its shareholding. While

Nippon Life would divest 5%, Reliance Capital will divest 1.5%, the balance being

issue of fresh shares.

Exhibit 2: Exhibit 2: Pre and Post-IPO shareholding pattern

No of shares

No of shares

%

%

(Pre-issue)

(Post-issue)

Promoter

56,15,10,000

96

52,47,90,000

86

Investor/Public

2,60,10,000

4

8,72,10,000

14

58,75,20,000

100

61,20,00,000

100

Source: RHP, Note: Calculated on upper price band

Objects of the offer

Setting up new branches and relocating certain existing branches (`38.3cr)

Upgrading the IT system (`40.6cr)

Advertising, marketing and brand building activities (`72cr)

Lending to our Subsidiary (Reliance AIF) for investment as continuing interest in

the new AIF schemes managed by Reliance AIF (`125cr)

Investing towards our continuing interest in new mutual fund schemes

managed by us (`100)

Funding inorganic growth and other strategic initiatives (`165)

Meeting expenses towards general corporate purposes

Key Management

Mr. Sundeep Sikka, is an Executive Director and Chief Executive Officer of the

Company (a nominee of Reliance Capital). He holds a Master’s degree in

Business Administration from the University of Pune. Prior to joining the

Company, he had also worked with ICICI Bank Ltd for more than four years.

Mr. Prateek Jain is the Chief Financial Officer of the Company. He cleared the

final examinations held by ICWAI in 1994 and by ICAI and ICSI in 1996. He

has, in the past, also worked with Pine Bridge Investments Asset Management

Company Private Ltd as CFO & Head - Risk Management.

Mr. Manish Gunwani is the CIO - Equity Investments of the Company. He has

been associated with the Company since September 5, 2017. He holds a

bachelor’s degree in technology from IIT, Madras and a post-graduate

diploma in management from IIM, Bangalore. Prior to joining the Company,

he had also worked with ICICI Prudential Asset Management Company

Limited.

Oct 24, 2017

3

Reliance Nippon Life Asset Management Ltd | IPO Note

Investment Rationale

Huge potential for growth in (Industry) MF AUM: In the past three years, equity

assets under management (AUM) for the Indian MF industry have increased three-

fold from `2 lakh cr to `7 lakh cr. Overall AUM has nearly doubled from `10 lakh

cr to ` 20 lakh cr. The AUM has grown from ₹3.26 lakh cr as on 31st March,

2007 to ₹20 lakh cr as on 30th September, 2017, more than six-fold increase in a

span of about 10 and half years. Moreover, the industry is receiving about

`5,000cr per month through SIP (Systematic Investment plan).

We believe this trend would continue in the coming years owing to

(1)

Continuation of black money crack down; (2) Lower fixed deposit rate; (3) Increase

in awareness; (4) Low penetration (AUM/GDP -13% V/s +50% in developed

market).

Exhibit 3: Trend in AUM/GDP across economies

Equity AUM to GDP

Debt AUM to GDP

Total AUM/GDP

Australia

51

85

136

USA

66

38

104

Germany

35

24

59

Brazil

14

42

56

Global

30

25

55

UK

29

25

54

South Africa

12

34

46

India

7

3

10

Source: RHP,FY16 Data

Mutual Fund industry in India still has very huge potential to grow. Mutual fund’s

AUM/GDP in the US is around 104%, 59% in Germany, above 55% in Brazil,

while in India it is still around 11%. Despite the increase, the share of mutual fund

savings continues to remain a small proportion. As on FY2016, mutual fund as %

of net financial savings was just 2.94%. This clearly indicates the penetration level

is very low.

Exhibit 4: Mutual fund penetration

3.5

41.5

45

36.5

36.1

40

3

32.9

31.1

35

2.94

2.5

30

2

1.8

25

1.53

1.32

20

1.5

1.12

15

1

10

0.5

5

0

0

FY12

FY13

FY14

FY15

FY16

Mutual Fund % of Net Financial Saving

Net Fiancial Saving % as house hold saving

Source: RHP

Oct 24, 2017

4

Reliance Nippon Life Asset Management Ltd | IPO Note

Wide distribution network with strong focus on retail investors: RNAM has a pan-

India network of 171 branches, of which 132 branches are located in B15

locations. Distributors contributed 54% and Direct 46% of monthly average AUM

on June 2017. Retail contribution to total AAAUM has increased by 1600bps to

26.5% from FY2013 to FY2017. Its MF AUM has grown at healthy CAGR of 26%

over FY2013-17. PAN India presence & superior fund performance would continue

to garner big chunk of new flow.

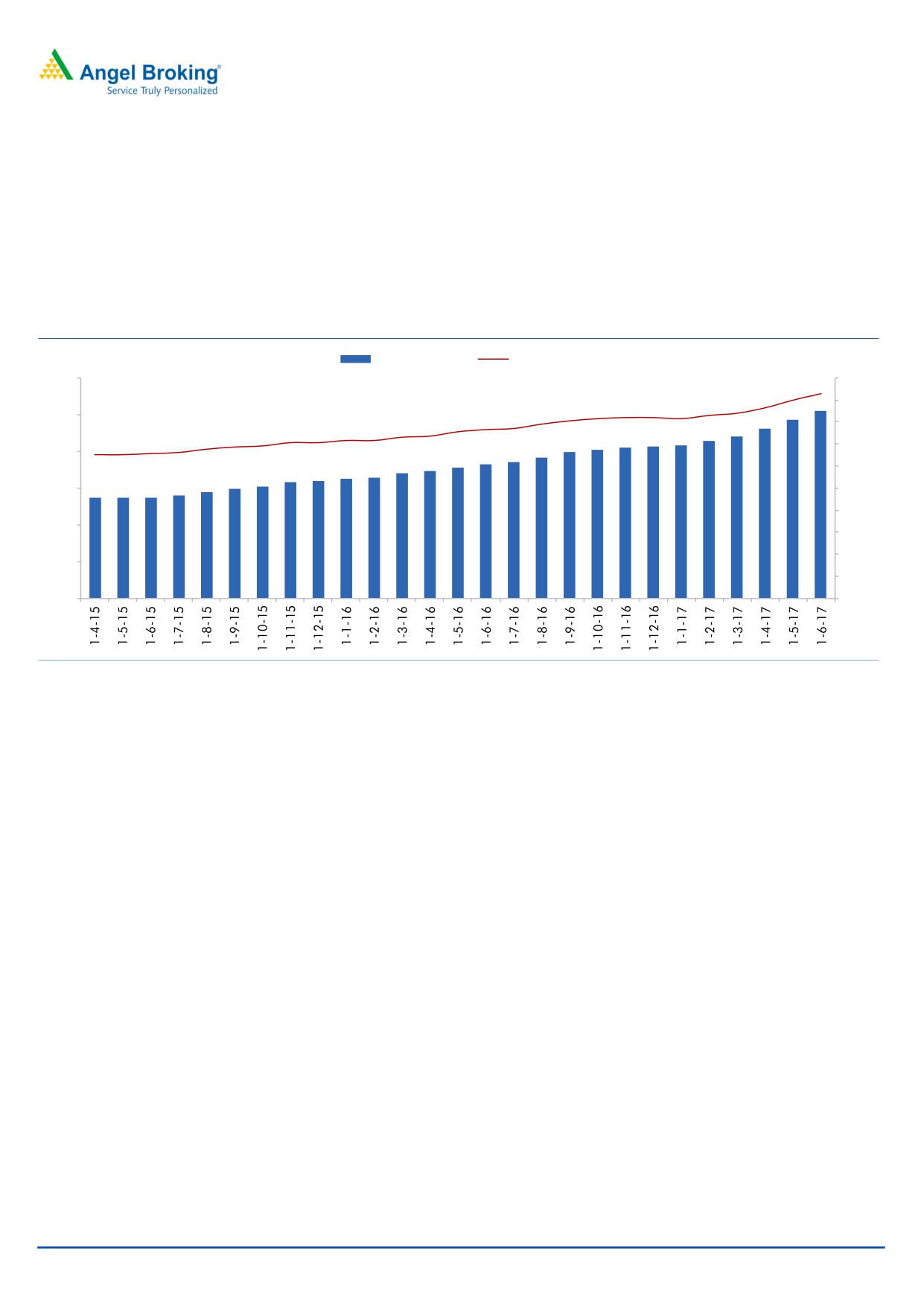

Exhibit 5: RNAM’s growing SIP Book

SIP Book (in bn)

SIP Count (mn)

6.0

1.9

2.0

1.8

1.7

1.6

1.6

1.6

1.6

1.7

1.7

1.8

1.6

1.6

4.9

5.1

5.0

1.5

1.5

1.5

4.6

1.5

1.5

1.4

1.4

1.4

1.4

4.4

1.6

1.4

1.4

4.3

1.4

4.1

4.1

4.2

1.3

1.3

1.3

1.3

4.0

4.0

3.8

1.4

4.0

3.6

3.7

3.5

3.6

3.2

3.3

3.3

3.4

1.2

3.0

3.1

2.9

3.0

2.7

2.7

2.7

2.8

3.0

1.0

0.8

2.0

0.6

0.4

1.0

0.2

-

-

Source: RHP

SIP Highlights

RNAM is sourcing INR 5.1 Bn of monthly flow through 1.86 mn SIP accounts

(as of Jun‟17)

In the last 2 years:

Total SIP count and monthly inflow have increased by

43% and 86%

respectively

Incremental (New) SIP count has doubled and New SIP Book amount (inflow)

has almost tripled (3x)

Average Ticket Size has increased from ~INR 2,102 (June 2015) to INR 2,745

(June 2017)

As of June 30, 2017, 77% of new SIPs have a tenure of over 5 years

High tenure implies continuity and sustainability in inflows

Oct 24, 2017

5

Reliance Nippon Life Asset Management Ltd | IPO Note

Robust Investment Process

The company has very strong team consisting of 28 senior members having an

average investment management experience of approximately 19 years. Equity

team is headed by Mr. Manish Gunwani and Debt team is headed by Mr. Amit

Tripathi. Reliance growth fund/ Reliance equity opportunity fund has given stellar

return of 23.75%/18.82% since inception.

Exhibit 6: Investment (Equity Scheme) performance

Compounded Annual Yield Period Ended August 31, 2017 (%)

MAAUM as

of August

Equity Funds

Since Inception

1 year

3 Years

5 years

31, 2017

(` in cr)

Reliance Equity Opportunities

9,715

18.82

12.33

10.56

17.7

S&P BSE 100

14

14.34

8.76

14.45

S&P BSE Sensex

13.58

11.52

5.98

12.72

Reliance Tax Saver (ELSS)

8,914

16.24

20.58

14.95

23.43

S&P BSE 100

12.17

14.34

8.76

14.45

S&P BSE Sensex

11.67

11.52

5.98

12.72

Reliance Regular Savings Fund (Balanced)

8,159

14.53

17.95

14.25

18.35

S&P BSE Sensex

13.33

11.52

5.98

12.72

Reliance Growth Fund

6,538

23.75

18.91

16.78

20.5

S&P BSE Sensex

10.4

11.52

5.98

12.72

Reliance Top 200 Fund*

4,148

11.6

17.47

13.49

19.15

S&P BSE 200

8.71

15.02

10.22

15.32

S&P BSE Sensex

7.51

11.52

5.98

12.72

Source: RHP

Growth Strategy

For next stage of growth, apart from MF, the company is developing alternative

investment fund and is open for inorganic growth through strategic acquisitions.

Reliance AIF launched its first AIF in 2014 and is currently managing six schemes

of which, four are closed for subscription. As of June 30, 2017, Reliance AIF was

raising funds in three alternative investment schemes across asset classes in

categories including long only equity, sector agnostic credit and high yield real

estate structured debt. The total capital commitment raised across these schemes

as of June 30, 2017 was `13,36.7cr. Reliance AIF intends to introduce and launch

various offerings to capitalize on market opportunities.

Reliance AIF intends to launch 6 to 10 new schemes (Category II and Category III)

over the next three financial years (“Proposed Schemes”) and utilize `1,25cr from

the net proceeds towards such continuing interest at or above the minimum level

prescribed by law for the Proposed Schemes.

Oct 24, 2017

6

Reliance Nippon Life Asset Management Ltd | IPO Note

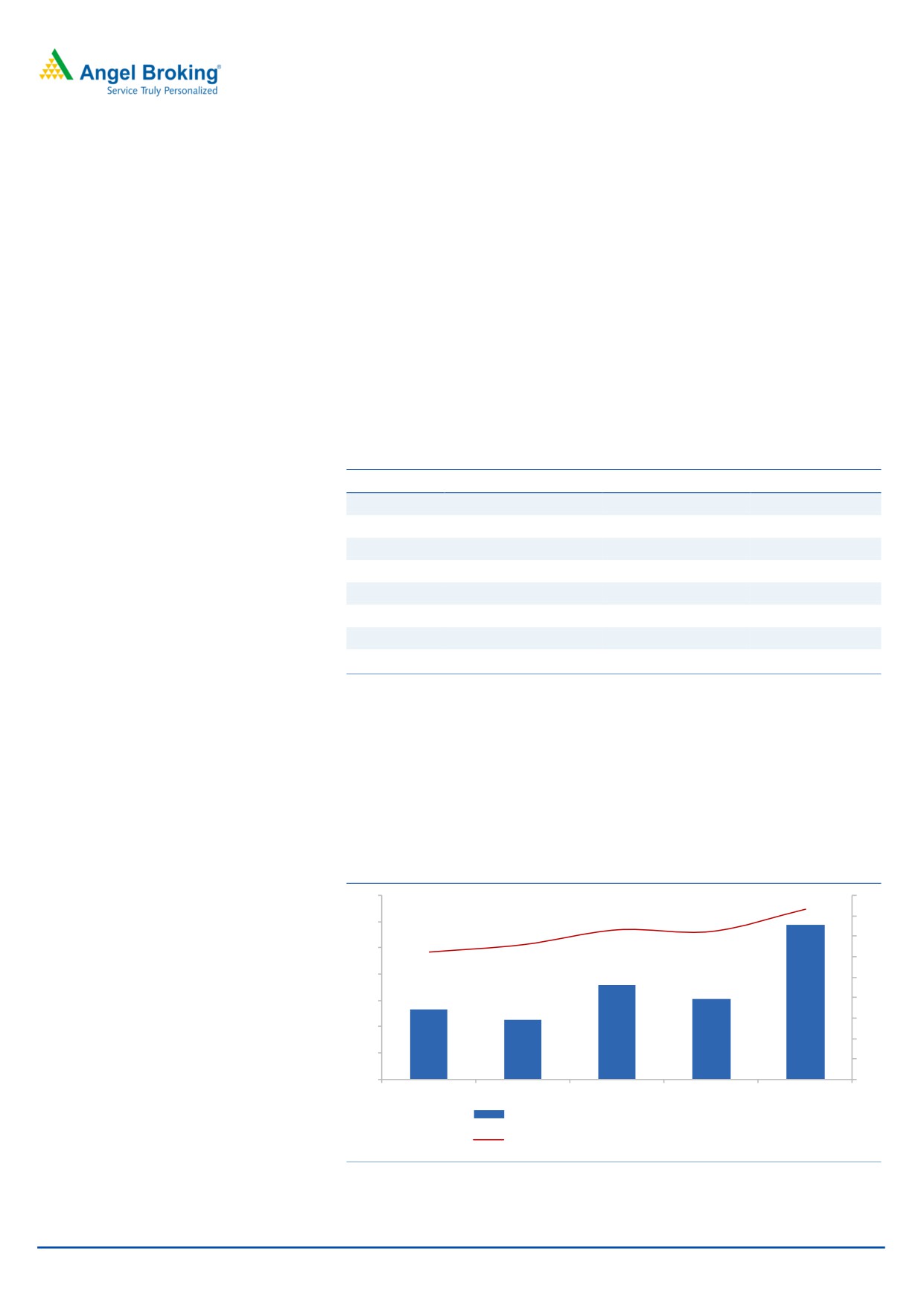

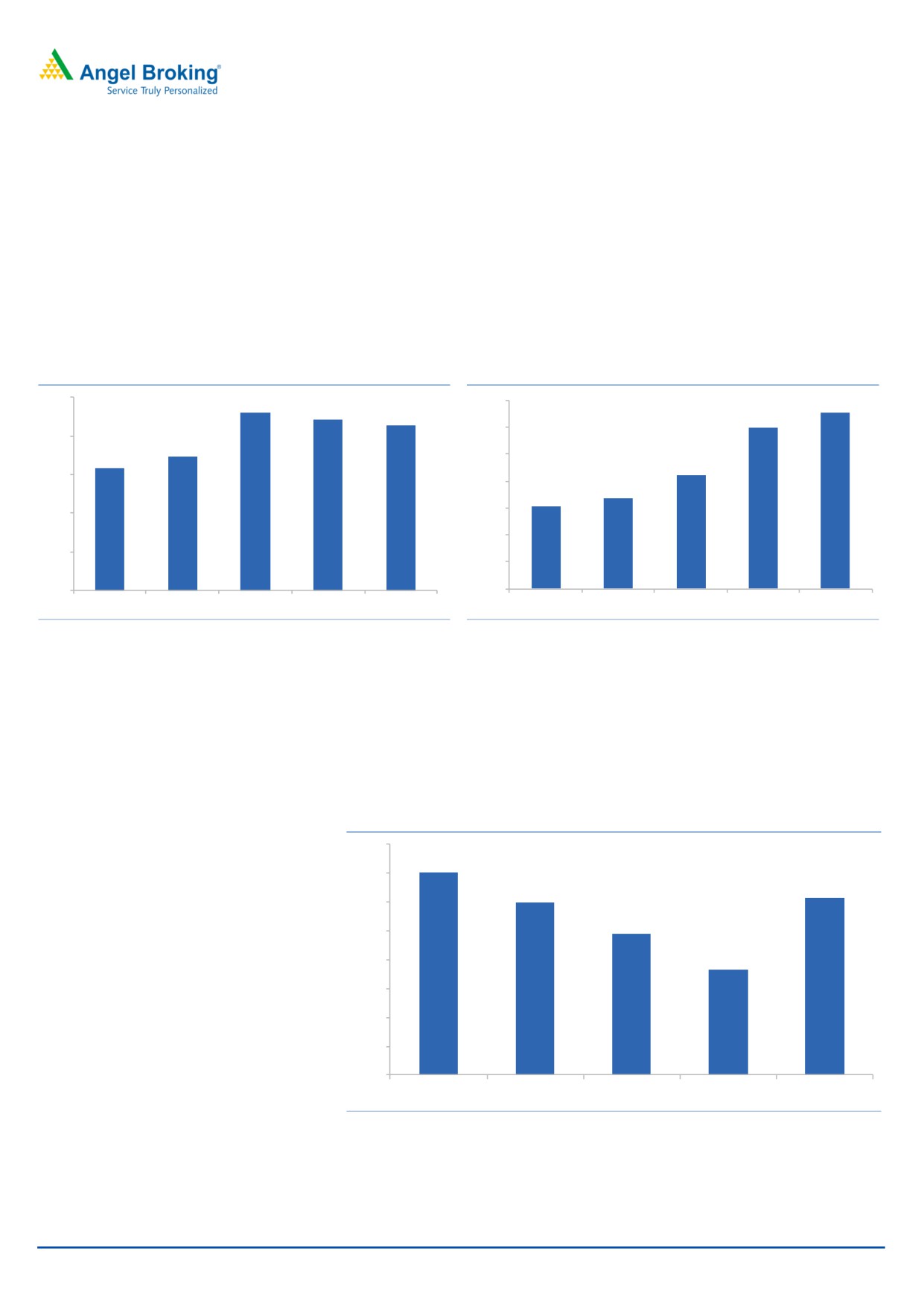

Healthy financials to support higher dividend payout: Revenue/EBITDA has grown

at healthy CAGR of 21%/28% over FY2013-17. Return on equity (ROE) for FY2017

was 21.3% and last 5 years average ROE was 20%. For FY2017, RNAM had made

dividend payout of 61% and it has maintained dividend payout of 55% on an

average for last 5 years.

Exhibit 7: ROE trend (%)

Exhibit 8: Revenue trend (`in cr)

25

1400

1307

23

22

21

1200

1200

20

17

16

1000

847

15

800

676

609

600

10

400

5

200

-

0

FY13

FY14

FY15

FY16

FY17

FY13

FY14

FY15

FY16

FY17

Source: RHP

Source: RHP

At upper end of the IPO price band dividend yield is 1.7%. We believe RNAM

would continue to maintain higher dividend payout ratio. As AMC business is

capital light business and company is debt free, so company would remain with

healthy free cash flow to distribute as dividend to the shareholder of the company.

Exhibit 9: History of dividend payout ratio (%)

80%

70%

70%

61%

60%

60%

49%

50%

40%

36%

30%

20%

10%

0%

FY13

FY14

FY15

FY16

FY17

Source: RHP

Oct 24, 2017

7

Reliance Nippon Life Asset Management Ltd | IPO Note

Outlook & Valuation: At the upper end of the IPO price band it is offered at 37x its

FY2017 EPS and 8x its FY2017 book value (Pre-IPO), demanding `15,442cr

market cap, which is 6.8% of the MF AUM (`2,28,329cr for the month of August

2017). Considering that RNAM is the third largest AMC coupled with huge

potential of MF industry to grow, strong return ratios, asset light business, higher

dividend payout ratio and track record of superior investment performance, we are

positive on this IPO and rate it as SUBSCRIBE.

Key Risk

Overall underperformance of investment would adversely affect new

investment flow and could lead to redemption of exiting investment.

Correction in the stock market would impact revenue and profitability of the

company.

Any step taken by SEBI to further reduce management fees would impact

revenue very sharply.

Oct 24, 2017

8

Reliance Nippon Life Asset Management Ltd | IPO Note

Income Statement

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

Revenues from Operations

609

676

847

1200

1307

- YoY Growth (%)

11.0

25.4

41.6

9.0

Employee Expenses

160

151

161

192

196

- YoY Growth (%)

-5.6

6.7

19.2

1.8

Other Expenses

273

283

323

595

641

- YoY Growth (%)

3.9

14.0

84.1

7.8

Total Expenses

433

435

484

787

837

- YoY Growth (%)

0.4

11.4

62.5

6.3

EBITDA

176

241

363

413

471

- YoY Growth (%)

37.1

50.4

13.8

14.0

Depreciation

9

14

7

4

18

- YoY Growth (%)

68.0

(52)

(37)

316

Other Income

126

103

108

114

128

- YoY Growth (%)

-18.3

4.9

5.4

12.9

Profit Before Tax

293

330

464

522

581

- YoY Growth (%)

12.5

40.6

12.6

11.3

Exceptional Items

0.0

0.0

0.0

0.0

0.0

PBT After Exceptional Item

293

330

464

522

581

Prov. for Taxation

62.8

59.1

109.4

126.0

178.6

- as a % of PBT

PAT

230

271

354

396

403

- YoY Growth (%)

17.5

31.0

11.8

1.6

Balance sheet

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

Share Capital

11

11

41

42

42

Reserve & Surplus

1446

1543

1495

1750

1851

Net Worth

1458

1554

1536

1792

1893

Minority Interest

3.8

3.8

8.9

8.9

0.0

Other Long Term Liabilities

2.9

2.5

3.3

7.5

11.6

Total Current Liabilities

96.6

148.5

153.4

122.5

147.1

Total Liabilities

1561

1709

1702

1931

2051

Total Fixed Assets

16.3

11.6

4.4

8.5

8.7

Total Non Current Assets

796

141

317

398

402

Investments

308

289

403

527

589

Cash & Cash equivalents

55.2

65.2

60.2

79.5

39.7

Other Current Assets

385.0

1202.9

917.5

917.7

1011.0

Total Assets

1561

1709

1702

1931

2051

Growth YoY

9.5%

-0.4%

13.5%

6.2%

Oct 24, 2017

9

Reliance Nippon Life Asset Management Ltd | IPO Note

Cash Flow Statement

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

Profit before tax

293

330

464

522

581

Depreciation

9

14

7

4

18

Change in Working Capital

107

256

57

361

715

Interest / Dividend (Net)

(86)

(72)

(70)

(41)

(70)

Direct taxes paid

(59)

(79)

(99)

(143)

(158)

Others

216

272

401

485

529

Cash Flow from Operations

48

177

(42)

218

556

(Inc.)/ Dec. in Fixed Assets

(8)

(3)

(5)

(9)

(257)

(Inc.)/ Dec. in Investments

173

17

449

(19)

(37)

Cash Flow from Investing

164

14

445

(28)

(294)

Issue of Equity

-

(0)

-

-

-

Inc./(Dec.) in loans

-

-

-

-

-

Others

(187)

(189)

(404)

(174)

(300)

Cash Flow from Financing

(187)

(189)

(404)

(174)

(300)

Effect of exchange fluctuation

5

7

(3)

3

(2)

Inc./(Dec.) in Cash

30

10

(5)

19

(40)

Opening Cash balances

25

55

65

60

79

Closing Cash balances

55

65

60

79

40

Key Ratio

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

Per Share Data

EPS

3.9

4.6

6.0

6.7

6.9

BVPS

24.8

26.5

26.1

30.5

32.2

DPS

2.7

2.7

2.9

2.5

4.2

Valuation Ratio (x)

P/E

64.4

54.8

41.8

37.4

36.8

P/BV

10.2

9.5

9.6

8.3

7.8

EV/EBITDA

83.9

60.6

40.0

34.9

30.7

EV/Sales

24.3

21.6

17.1

12.0

11.0

Dividend Yield (%)

1.1

1.1

1.2

1.0

1.7

Profitability Ratios (%)

ROE

15.8

17.4

23.1

22.1

21.3

ROA

14.7

15.8

20.8

20.5

19.6

PAT/AAUM

0.25

0.26

0.25

0.25

0.19

EBITDA

28.9

35.7

42.8

34.4

36.0

PAT

37.9

40.0

41.8

33.0

30.8

Source: RHP, Note: ratios are Calculated on upper price band

Oct 24, 2017

10

Reliance Nippon Life Asset Management Ltd | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager and investment advisor with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Oct 24, 2017

11