2QFY2017 Result Update | Agrichemical

November 3, 2016

Rallis India

NEUTRAL

CMP

`221

Performance Highlights

Target Price

-

Y/E March (` cr)

2QFY2017 1QFY2017

% chg (qoq) 2QFY2016

% chg (yoy)

Investment Period

-

Net sales

540

445

21.4

447

20.8

Stock Info

Other income

12

7

75.2

5

136.6

Sector

Agrichemical

Gross profit

210

202

4.2

234

(10.3)

Market Cap (` cr)

4,295

Operating profit

96

70

36.5

86

11.2

Net debt (` cr)

126

Adj. Net profit

67

49

35.1

51

31.0

Beta

0.9

Source: Company, Angel Research

52 Week High / Low

246/142

Avg. Daily Volume

88,414

For 2QFY2017, Rallis India (Rallis) reported a yoy growth of 20.8% in sales to

Face Value (`)

1

`540cr (vs. `447cr in 2QFY2016). On the operating front, the gross margin

BSE Sensex

27,877

came in at 38.9% (vs. 52.4% in 2QFY2016), which along with sales growth aided

Nifty

7,502

the OPM to come in at 17.7% (V/s 19.2% in 2QFY2016). Aided by sales growth,

Reuters Code

RALL.BO

a good operating performance and surge in other income (`12cr vs. `5cr in

Bloomberg Code

RALI@IN

2QFY2016), the Adj. Net profit grew by 31.0% yoy to `67cr (vs. `51cr in

2QFY2016). We maintain our Neutral view on the stock.

Shareholding Pattern (%)

Robust numbers mainly aided by robust growth: For 2QFY2017, the company

Promoters

50.1

reported a yoy growth of 20.8% in sales to `540cr (vs. `447cr in 2QFY2016).

MF / Banks / Indian Fls

19.8

On the operating front, the gross margin came in at 38.9% (vs. 52.4% in

FII / NRIs / OCBs

6.4

2QFY2016), which along with sales growth aided the OPM to come in at 17.7%

Indian Public / Others

23.7

(vs. 19.2% in 2QFY2016). Aided by sales growth, a good operating performance

and surge in other income (`12cr V/s `5cr in 2QFY2016), the Adj. Net profit

grew by 31.0% yoy to `67cr (vs. `51cr in 2QFY2016).

Abs. (%)

3m

1yr

3yr

Sensex

(0.5)

4.6

31.5

Outlook and valuation: For FY2016-18E, we expect a CAGR of 15.0% and

Rallis India

0.0

6.9

40.5

22.3% in net sales and profit, respectively, with recovery expected in FY2017. At

the current levels, the stock is trading at a fair valuation of 20.5x its FY2018E EPS.

3-year price chart

Hence, we maintain our Neutral view on the stock.

400

350

Key financials (Consolidated)

300

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

250

200

Net Sales

1,822

1,637

1,937

2,164

150

% chg

4.3

(10.1)

18.3

11.7

100

50

Adj.Net Profit

157

143

167

214

0

% chg

3.5

(9.0)

16.6

28.2

EBITDA %

14.2

13.3

14.3

14.3

Source: Company, Angel Research

FDEPS (`)

8.1

7.4

8.6

11.0

P/E (x)

27.8

30.6

26.2

20.5

P/BV (x)

5.4

4.9

3.9

3.5

RoE (%)

20.5

16.7

16.5

18.0

RoACE (%)

24.7

19.2

20.9

20.3

Sarabjit Kour Nangra

EV/Sales (x)

2.3

2.6

2.1

1.9

+91-22-39357800 ext. 6806

EV/EBITDA (x)

16.4

19.5

14.9

13.0

Source: Company, Angel Research; Note: CMP as of November 1, 2016

Please refer to important disclosures at the end of this report

1

Rallis India | 2QFY2017 Result Update

Exhibit 1: 2QFY2017 performance (Consolidated)

Y/E March (` cr)

2QFY2017

1QFY2017

% chg (QoQ) 2QFY2016

% chg (YoY) 1HFY2017 1HFY2016

% chg

Net sales

540

445

21.4

447

20.8

985

862

14.2

Other income

12

7

75.2

5

136.6

178

10

1679.7

Total income

553

452

22.3

453

22.1

1,163

872

33.3

Gross profit

210

202

4.2

234

(10.3)

412

390

5.6

Gross margin (%)

38.9

45.4

52.4

41.8

45.3

EBDITA

96

70

36.5

86

11.2

166

142

16.6

EBDITA margin (%)

17.7

15.8

19.2

16.8

16.5

Financial cost

1

2

(51.1)

3

(60.4)

3

7

(50.4)

Depreciation

11

12

(11.2)

13

(13.6)

23

24

(3.2)

PBT

96

62

53.6

76

26.8

317

121

161.8

Provision for taxation

29

47

(37.1)

25

18.2

76

28

173.4

PAT Before Exc. And MI

67

16

320.7

51

31.0

241

93

158.4

Minority

0

0

0

0

0

-

Exceptional

0

158

0

120

0

Reported PAT

67

174

(61.8)

51

31.0

241

93

158.4

Adjusted PAT

67

49

35.1

51

31.0

120

93

29.1

EPS (`)

3.4

2.5

2.6

6.2

4.8

Source: Company, Angel Research

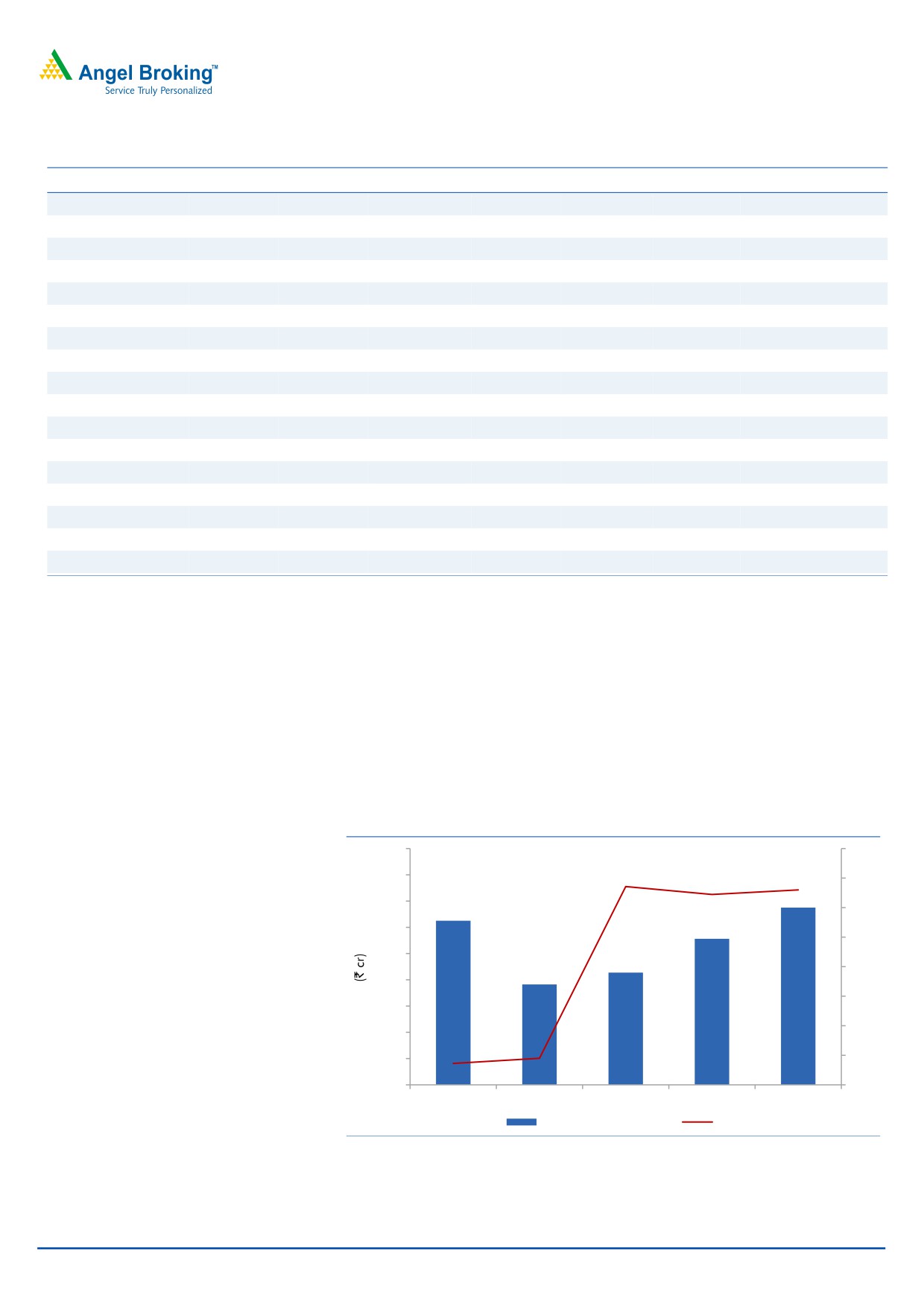

Sales rose by 20.8% yoy

For 2QFY2017, the company’s sales rose by 20.8% yoy to `540cr (vs. `447cr in

2QFY2016). Monsoon 2016 ended on a positive note with rainfall for the season

at 97% of LPA against interim fears of below normal monsoons. Rainfall was

muted at the start of the season with 89% of LPA in June but gained pace during

the crucial period with 107% of LPA in July. The subsidiary business (Metahelix), on

the other hand, witnessed growth of 66% yoy albeit on a lower base. Subsidiaries

sales for the quarter came in at `45cr.

Exhibit 2: Revenue performance

720

15

640

540

10

560

500

5

480

445

0

400

342

306

(5)

320

(10)

240

(15)

160

80

(20)

0

(25)

2QFY2016

3QFY2016

4QFY2016

1QFY2017

2QFY2017

Total Revenue

% YoY

Source: Company, Angel Research

November 3, 2016

2

Rallis India | 2QFY2017 Result Update

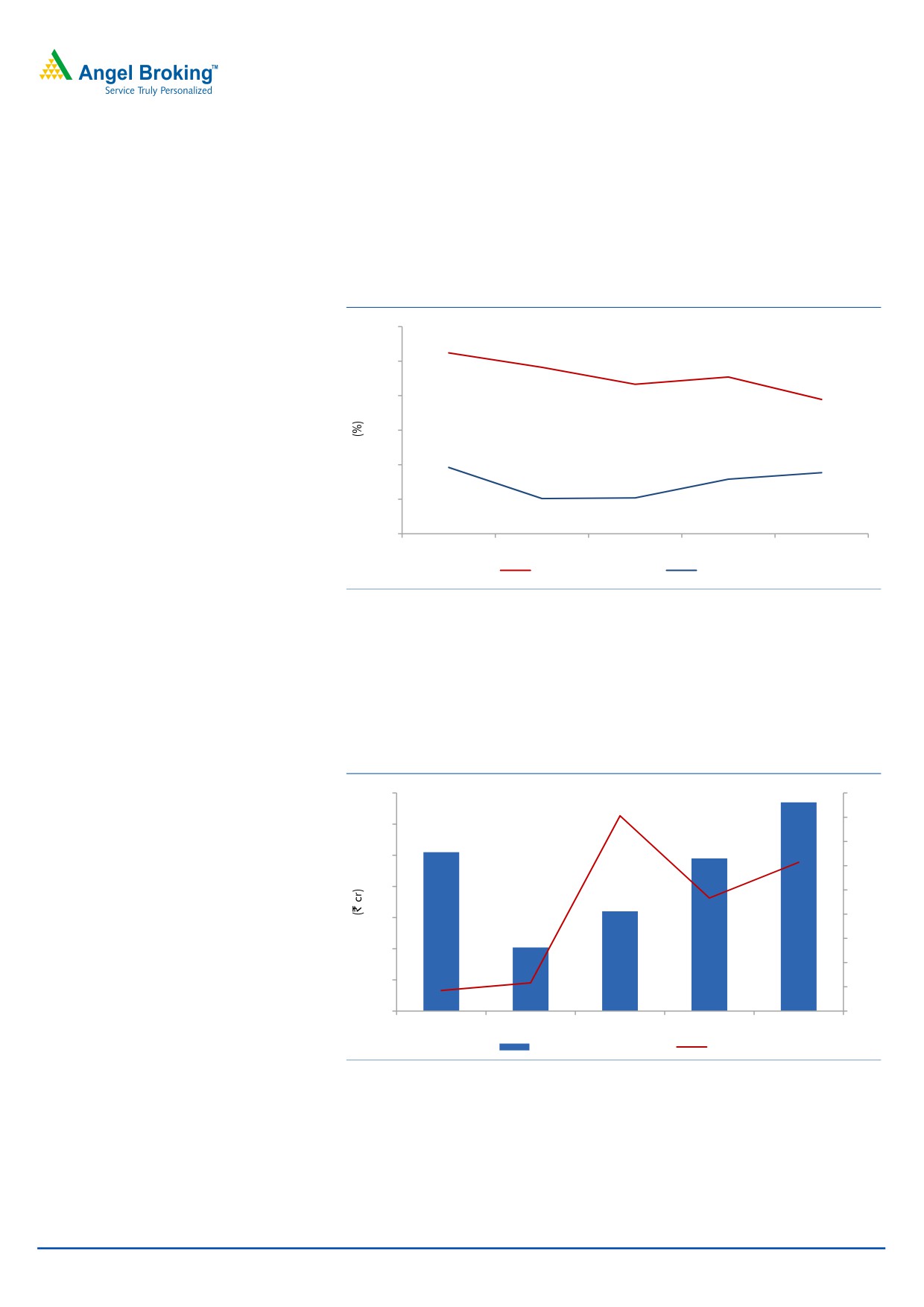

OPM dips yoy

On the operating front, the gross margin came in at 38.9% (vs. 52.4% in

2QFY2016), a yoy dip of 13.5%. Inspite of this, the OPM came in at 17.7% (vs.

19.2% in 2QFY2016). This was mainly on back of only 10.8% yoy rise in

employee expenses and 8.6% yoy dip in other expenses.

Exhibit 3: Margin trend (%)

60.0

52.4

48.2

50.0

45.4

43.3

38.9

40.0

30.0

20.0

19.2

17.7

10.0

15.8

10.2

10.4

0.0

2QFY2016

3QFY2016

4QFY2016

1QFY2017

2QFY2017

Gross margin

EBITDA margin

Source: Company, Angel Research

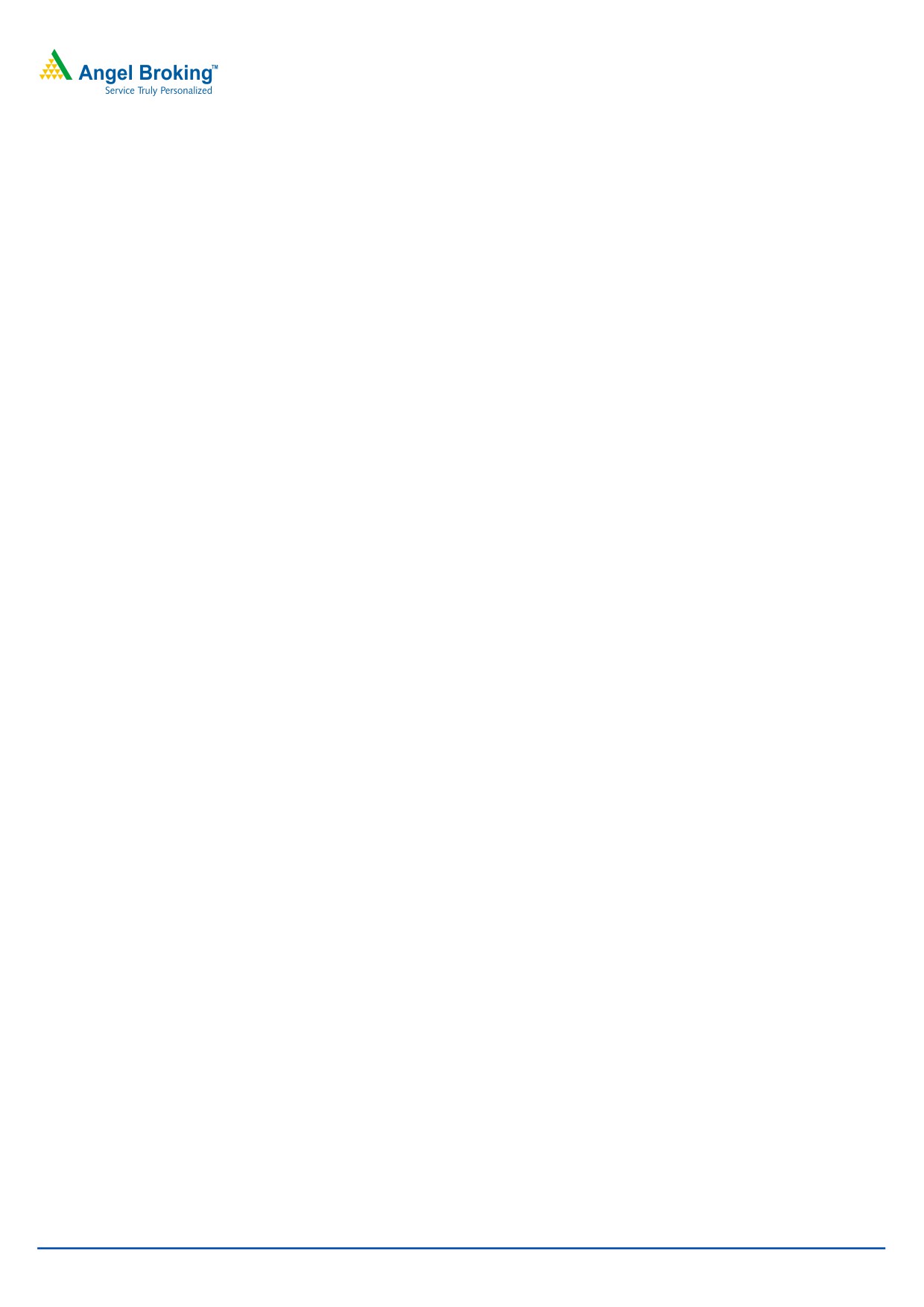

Earnings rise 31% yoy

Aided by sales growth, a good operating performance and surge in other income

(`12cr vs. `5cr in 2QFY2016), the Adj. Net profit grew 31.0% yoy to `67cr

(vs. `51cr in 2QFY2016).

Exhibit 4: Adjusted PAT trend

70

67

60

50

60

51

40

49

50

30

40

20

32

30

10

20

0

20

(10)

10

(20)

0

(30)

2QFY2016

3QFY2016

4QFY2016

1QFY2017

2QFY2017

Adj PAT

% YoY

Source: Company, Angel Research

November 3, 2016

3

Rallis India | 2QFY2017 Result Update

Investment arguments

The company set to seize rising opportunities in the domestic crop protection

market: India's overall pesticide consumption is one of the lowest in the world and

has a huge potential to grow. We believe Rallis is well placed to seize this

opportunity on the back of its wide distribution network, strong brands, and a

robust new-product pipeline. According to industry estimates, the unorganized

market accounts for

50% of the industry. Nonetheless, we believe Rallis is in a

position to wrest market share as well as charge a premium for its products.

FY2016 has been challenging on back of poor monsoons but the outlook for

FY2017 is favorable and should bode well for domestic sales growth. A lower base

would result in 17.3% CAGR in the domestic business during FY2016-18E.

Exports under pressure: Although a late entrant, the company has been enhancing

its focus in the exports market, which is now turning out to be its main growth

driver. Overall exports formed ~30% of sales in FY2016. In FY2016, the global

weakness in the agrochemical industry put pressure on Rallis’ exports business,

where the revenues dropped by 20% yoy to `400cr. The company’s primary export

market is Brazil where a sluggish demand environment, currency volatility and

macro headwinds led to deferment/cancelation of many orders. However, export

orders saw a revival in 4QFY2016; still the management remains cautious on

recovery in Brazil, which could take more than a couple of quarters. This would

likely keep the exports business revenues under pressure. Going forward, the

segment will continue to post a 7.2% CAGR over FY2016-18E.

Seed business to augment the domestic portfolio: After the acquisition of

Metahelix’ seeds business in 2010, the seeds business forms a major part of the

domestic business of the company. During FY2016, Rallis’ seed business, under

Metahelix reported a decent growth of 8% yoy to `334cr (almost 23% of the

domestic business) on back of increased market share and despite significant

reduction in acreages for some of the key crops such as paddy and corn. The

company is also strengthening its cotton portfolio and will be launching a new

product to take on the market leaders in this crop. The management remains

confident of Metahelix achieving 12-14% margin in a good monsoon year. During

FY2016, the company increased its stake in Metahelix to 100%.

Contract manufacturing ramping up slowly: Rallis plans to focus on contract

manufacturing for exports and selectively target top players. To facilitate the same,

the company has set up a plant at Dahej, which in FY2013 was working at full

capacity and contributed significantly to the overall growth of the company. The

company has bagged two CRAMS projects on a pilot basis during the year. The

management expects to convert these pilot projects into full commercial contracts

in FY2017 and contribute to earnings growth from FY2018-2019.

Outlook and valuation

Over FY2016-18E, we expect the company to post a CAGR of 15.0% and 22.3%

in net sales and profit, respectively, with recovery expected in FY2017 driven by

above normal monsoons. At the current level, the stock is trading at a fair

valuation of 20.5x its FY2018E EPS. Hence, we maintain our Neutral view on the

stock.

November 3, 2016

4

Rallis India | 2QFY2017 Result Update

Exhibit 5: Key assumptions

Particulars (%)

FY2017E

FY2018E

Domestic growth

24.0

11.0

Export growth

5.0

15.0

Total revenue growth

18.3

11.7

EBITDA margin

14.3

14.3

Capex (` cr)

70

70

Source: Company, Angel Research

Exhibit 6: Peer valuation

Company Reco

Mcap CMP TP Upside

P/E (x)

EV/Sales (x)

EV/EBITDA (x)

RoE (%)

CAGR (%)

(` cr)

(`)

(`)

(%) FY17E FY18E FY17E FY18E FY17E FY18E FY17E FY18E Sales PAT

Rallis

Neutral

4,377

221

-

-

26.2

20.5

2.1

1.9

14.9

13.0

16.5

18.0

15.0

22.3

UPL

Neutral

35,259

696

-

-

16.1

13.5

1.8

1.5

9.6

8.0

21.4

21.2

16.0

18.9

Source: Company, Angel Research, Bloomberg

Company background

Rallis is one of the oldest and second largest pesticide agrichemical companies in

the country with a market share of around 13% and belongs to the Tata Group.

The company also has a credible presence in the international market.

Contribution from the domestic business stands at ~70%, while exports account

for the balance.

November 3, 2016

5

Rallis India | 2QFY2017 Result Update

Profit & loss (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

Gross sales

1,535

1,840

1,922

1,730

2,059

2,302

Less: Excise duty

95

114

121

119

147

164

Net Sales

1,440

1,726

1,801

1,612

1,911

2,138

Other operating income

18

21

21

26

26

26

Total operating income

1,458

1,747

1,822

1,637

1,937

2,164

% chg

14.4

19.8

4.3

(10.1)

18.3

11.7

Total Expenditure

1,241

1,485

1,545

1,398

1,637

1,832

Net Raw Materials

823

1,008

995

839

1,110

1,242

Other Mfg costs

304

342

341

404

363

406

Personnel

94

111

129

132

137

154

Other

20

24

25

22

27

30

EBITDA

199

240

256

214

274

306

% chg

3.9

20.8

6.5

(16.5)

27.9

11.9

(% of Net Sales)

13.8

13.9

14.2

13.3

14.3

14.3

Depreciation & Amort.

32

41

50

45

56

61

EBIT

186

221

228

195

244

271

% chg

(1.5)

18.9

3.1

(14.3)

24.8

11.3

(% of Net Sales)

12.9

12.8

12.6

12.1

12.7

12.7

Interest & other Charges

21

13

10

14

9

8

Other Income

5

6

4

4

4

4

(% of PBT)

3

3

2

2

2

2

Share in profit of Asso.

-

-

-

-

-

-

Recurring PBT

170

214

222

186

238

267

% chg

(3.5)

26.3

3.4

(16.2)

28.4

12.1

Extraordinary Exp./(Inc.)

3

-

-

-

(120)

-

PBT (reported)

172

214

222

186

358

267

Tax

53

62

62

39

72

53

(% of PBT)

31.0

28.8

27.9

21.0

20.0

20.0

Minority Interest

(0)

0.8

2.6

3.7

3.7

3.7

PAT (reported)

119

152

157

143

287

214

ADJ. PAT

114

152

157

143

167

214

% chg

4.6

32.9

3.5

(9.0)

16.6

28.2

(% of Net Sales)

7.9

8.8

8.7

8.9

8.7

10.0

Basic EPS (`)

5.9

7.8

8.1

7.4

8.6

11.0

Fully Diluted EPS (`)

5.9

7.8

8.1

7.4

8.6

11.0

% chg

4.6

32.9

3.5

(9.0)

16.6

28.2

November 3, 2016

6

Rallis India | 2QFY2017 Result Update

Balance sheet (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

SOURCES OF FUNDS

Equity Share Capital

19

19

19

19

19

19

Preference Capital

-

-

-

-

-

-

Reserves & Surplus

601

699

795

880

1,098

1,243

Shareholders Funds

621

718

815

899

1,117

1,263

Minority Interest

5

10

10

4

4

4

Total Loans

131

75

111

75

110

50

Other Long Term Liabilities

6

4

4

4

4

4

Long Term provisions

30

15

19

18

18

18

Deferred Tax Liability

28

32

36

39

39

39

Total Liabilities

821

853

993

1,038

1,295

1,380

APPLICATION OF FUNDS

Gross Block

581

651

687

764

834

904

Less: Acc. Depreciation

195

233

282

327

383

444

Net Block

386

418

405

437

451

460

Capital Work-in-Progress

35

21

21

21

21

21

Goodwill

169

186

196

259

259

259

Investments

20

25

24

28

28

28

Long Term Loans and Adv.

92

98

110

110

109

122

Current Assets

488

549

680

650

889

1,006

Cash

26

9

7

8

136

164

Loans & Advances

28

40

28

35

69

77

Other

435

500

645

607

684

765

Current liabilities

368

445

443

467

462

517

Net Current Assets

120

104

237

183

427

490

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

821

853

993

1,038

1,295

1,380

November 3, 2016

7

Rallis India | 2QFY2017 Result Update

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Profit before tax

172

214

222

186

358

267

Depreciation

32

41

50

45

56

61

(Inc)/Dec in Working Capital

(61)

(7)

(147)

55

(115)

(47)

Direct taxes paid

(53)

(62)

(62)

(39)

(72)

(53)

Cash Flow from Operations

150

186

63

246

228

227

(Inc.)/ Dec. in Fixed Assets

(5)

(56)

(36)

(76)

(70)

(70)

(Inc.)/ Dec. in Investments

3

(5)

1

(4)

-

-

Inc./ (Dec.) in loans and adv.

-

-

-

-

-

-

Cash Flow from Investing

(2)

(61)

(35)

(80)

(70)

(70)

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

(6)

(73)

40

(36)

35

(60)

Dividend Paid (Incl. Tax)

(50)

(55)

(68)

(68)

(68)

(68)

Others

(78)

(14)

(1)

-

-

(1)

Cash Flow from Financing

(134)

(142)

(29)

(165)

(29)

(129)

Inc./(Dec.) in Cash

15

(17)

(2)

1

128

28

Opening Cash balances

11

26

9

7

8

136

Closing Cash balances

26

9

7

8

136

164

November 3, 2016

8

Rallis India | 2QFY2017 Result Update

Key ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

38.3

28.8

27.8

30.6

26.2

20.5

P/CEPS

29.1

22.7

21.2

23.3

12.8

15.9

P/BV

7.0

6.1

5.4

4.9

3.9

3.5

Dividend yield (%)

0.9

0.9

0.9

1.3

1.8

2.2

EV/Sales

2.9

2.4

2.3

2.6

2.1

1.9

EV/EBITDA

21.3

17.4

16.4

19.5

14.9

13.0

EV / Total Assets

5.2

4.9

4.2

4.0

3.1

2.9

Per Share Data (`)

EPS (Basic)

5.9

7.8

8.1

7.4

8.6

11.0

EPS (fully diluted)

5.9

7.8

8.1

7.4

8.6

11.0

Cash EPS

7.7

9.9

10.6

9.6

17.6

14.1

DPS

2.0

2.0

2.0

3.0

4.0

5.0

Book Value

31.9

36.9

41.9

46.2

57.5

64.9

Dupont Analysis

EBIT margin

12.9

12.8

12.6

12.1

12.7

12.7

Tax retention ratio

69.0

71.2

72.1

79.0

80.0

80.0

Asset turnover (x)

1.9

2.1

2.0

1.6

1.7

1.6

ROIC (Post-tax)

16.6

19.0

18.0

15.4

16.9

16.4

Cost of Debt (Post Tax)

10.1

8.7

7.9

11.6

8.0

8.0

Leverage (x)

0.2

0.2

0.2

0.2

(0.0)

(0.0)

Operating ROE

18.0

20.6

19.6

16.1

16.8

16.2

Returns (%)

ROCE (Pre-tax)

23.8

26.4

24.7

19.2

20.9

20.3

Angel ROIC (Pre-tax)

33.7

35.9

32.4

25.7

29.9

29.9

ROE

19.5

22.7

20.5

16.7

16.5

18.0

Turnover ratios (x)

Asset Turnover (Gross Block)

2.6

2.8

2.7

2.3

2.4

2.5

Inventory / Sales (days)

67

62

74

89

87

96

Receivables (days)

34

35

37

44

43

48

Payables (days)

111

98

105

119

103

97

WC cycle (ex-cash) (days)

16

20

33

46

45

53

Solvency ratios (x)

Net debt to equity

0.2

0.1

0.2

0.1

(0.0)

(0.1)

Net debt to EBITDA

0.7

0.3

0.5

0.4

(0.0)

(0.3)

Interest Coverage (EBIT / Int.)

9.0

17.5

22.5

14.4

26.4

33.9

November 3, 2016

9

Rallis India | 2QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Rallis India

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 3, 2016

10