2QFY2016 Result Update | Agrichemical

November 4, 2015

Rallis India

NEUTRAL

CMP

`206

Performance Highlights

Target Price

-

Y/E March (` cr)

2QFY2016 1QFY2016

% chg (qoq) 2QFY2015

% chg (yoy)

Investment Period

-

Net sales

500

464

7.8

636

(21.4)

Other income

5

6

(19.6)

7

(31.3)

Stock Info

Gross profit

233

243

(4.1)

245

(4.8)

Sector

Agrichemical

Operating profit

95

52

82.7

116

(18.4)

Market Cap (` cr)

4,010

Adj. Net profit

57

33

73.1

73

(22.0)

Net debt (` cr)

126

Source: Company, Angel Research

Beta

0.8

Rallis India (Rallis) posted disappointing results for 2QFY2016. Sales for the

52 Week High / Low

299/201

quarter came in at `499.7cr V/s `635.9cr in 2QFY2015, a dip of 21.4% yoy.

Avg. Daily Volume

47,701

Sales were adversely impacted due to poor monsoon in India, while the

Face Value (`)

1

international market also faced pressure with Brazil (a key market for the

BSE Sensex

26,591

company) witnessing a severe drought. In USA, low crop commodity prices

Nifty

8,061

along with higher inventory prices impacted consumption. On the operating

Reuters Code

RALL.BO

front, the gross margins came in at 46.7% V/s 38.5% in 2QFY2015, which lead

Bloomberg Code

RALI@IN

the OPM to come in at 18.9% V/s 18.2% in 2QFY2015. The PAT came in at

`57cr V/s `73cr in 2QFY2015, a yoy dip of 22.0%. We remain Neutral on the

stock.

Shareholding Pattern (%)

Promoters

50.1

Disappointing sales: For 2QFY2016, sales came in at `499.7cr V/s `635.9cr in

MF / Banks / Indian Fls

14.5

in 2QFY2015, a dip of 21.4% yoy. Sales were adversely impacted due to poor

FII / NRIs / OCBs

13.6

monsoon in India, while the international market also faced pressure with Brazil

(a key market for the company) witnessing a severe drought. In USA, low crop

Indian Public / Others

21.7

commodity prices along with higher inventory prices impacted consumption. On

the operating front, the gross margins came in at 46.7% V/s 38.5% in

Abs. (%)

3m 1yr 3yr

2QFY2015, which lead the OPM to come in at 18.9% V/s 18.2% in 2QFY2015.

Sensex

(5.7)

(4.6)

41.8

The PAT came in at `57cr V/s `73cr in 2QFY2015, a yoy dip of 22.0%.

Rallis India

(3.4)

(9.9)

46.0

Outlook and valuation: The Management is confident about the long-term

prospects of the agrochemicals industry. We expect Rallis to register a CAGR of

15.1% and 16.7% in net sales and profit, respectively, over FY2015-17E. At the

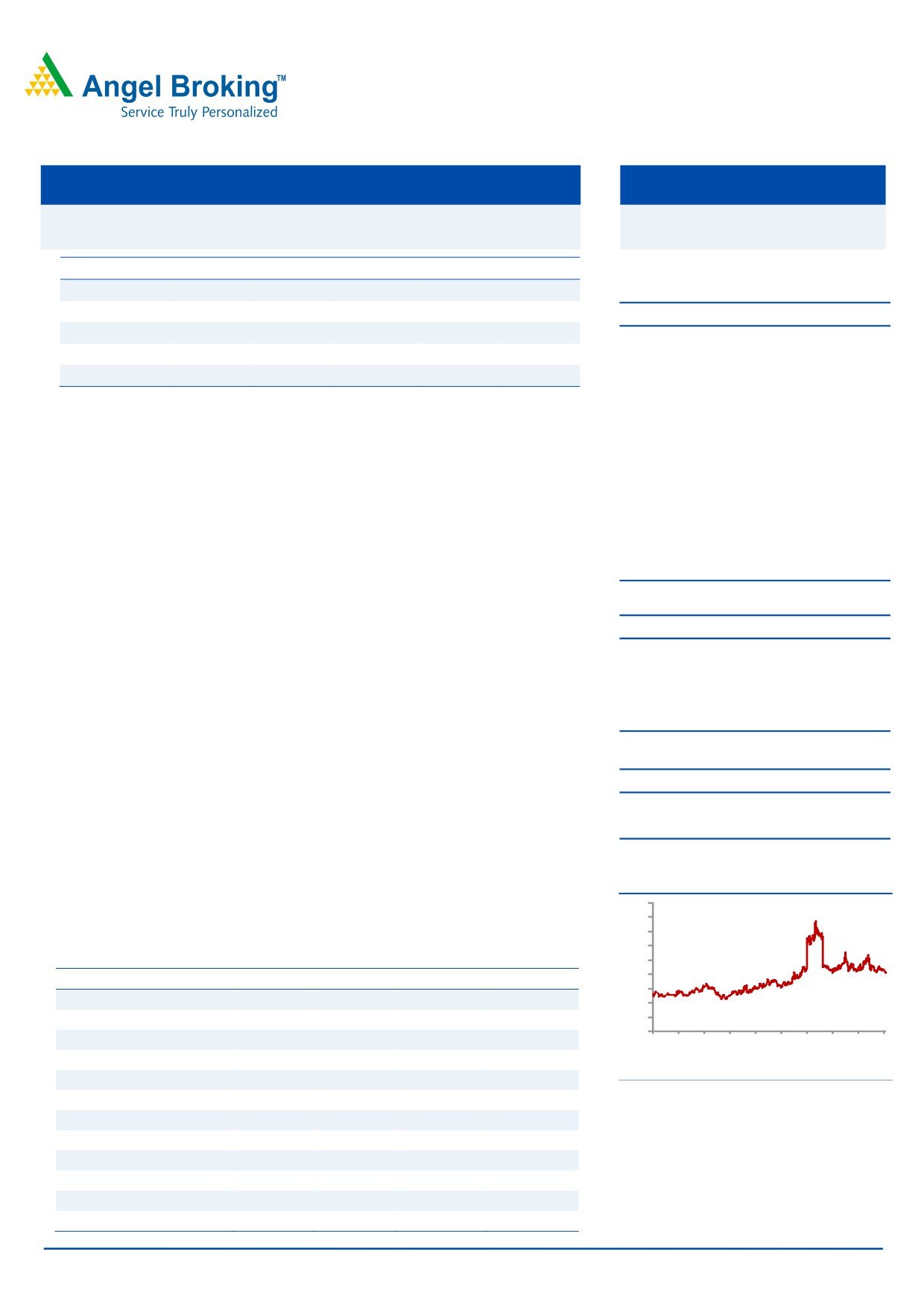

3-year price chart

450

current levels, the stock is trading at a fair valuation of 18.7x its FY2017E EPS.

400

Hence, we maintain our Neutral recommendation on the stock.

350

300

Key financials (Consolidated)

250

200

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

150

Net Sales

1,747

1,822

2,097

2,415

100

50

% chg

19.8

4.3

15.1

15.2

0

Adj.Net Profit

152

157

184

214

2

2

2

3

3

4

4

4

5

5

1

1

1

1

1

1

1

1

1

1

n

n

v

r

p

b

-

c

y

ŧ

% chg

32.9

3.5

16.9

16.4

a

u

o

p

e

e

uJ

e

a

c

J

J

N

A

S

F

D

M

O

EBITDA %

13.9

14.2

14.4

14.4

Source: Company, Angel Research

FDEPS (`)

7.8

8.1

9.5

11.0

P/E (x)

26.4

25.5

21.8

18.7

P/BV (x)

5.6

4.9

4.3

3.7

RoE (%)

22.7

20.5

21.1

21.3

RoACE (%)

26.4

24.7

25.6

26.6

Sarabjit Kour Nangra

EV/Sales (x)

2.4

2.3

2.0

1.7

+91-22-39357800 ext. 6806

EV/EBITDA (x)

17.4

16.4

14.0

11.9

Source: Company, Angel Research; Note: CMP as of November 3, 2015

Please refer to important disclosures at the end of this report

1

Rallis India | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance (Consolidated)

Y/E March (` cr)

2QFY2016

1QFY2016

% chg (qoq) 2QFY2015

% chg (yoy)

1HFY2016 1HFY2015

% chg

Net sales

500

464

7.8

636

(21.4)

963

1,101

(12.5)

Other income

5

6

(19.6)

7

(31.3)

11

13

(17.0)

Total income

505

470

7.4

643

(21.5)

974

1,114

(12.6)

Gross profit

233

243

(4.1)

245

(4.8)

477

479

(0.5)

Gross margin (%)

46.7

52.5

38.5

49.5

43.5

EBDITA

95

52

82.7

116

(18.4)

146

172

(14.9)

EBDITA margin (%)

18.9

11.2

18.2

15.2

15.6

Financial cost

3

4

(30.3)

3

(5.0)

7

5

38.8

Depreciation

13

12

10.9

13

0.0

25

24

3.0

PBT

84

42

99.2

107

(21.9)

126

156

(19.5)

Provision for taxation

28

2

1,386.1

34

(18.3)

30

40

(25.9)

PAT Before Exc. And MI

56

40

39.2

73

(23.6)

96

116

(17.3)

Minority

(1)

7

(1)

6

5

-

Exceptional

0

0

0

0

0

Reported PAT

57

33

73.1

73

(22.0)

90

110

(18.2)

Adjusted PAT

57

33

73.1

73

(22.0)

90

110

(18.2)

EPS (`)

2.9

1.7

3.8

4.6

5.7

Source: Company, Angel Research

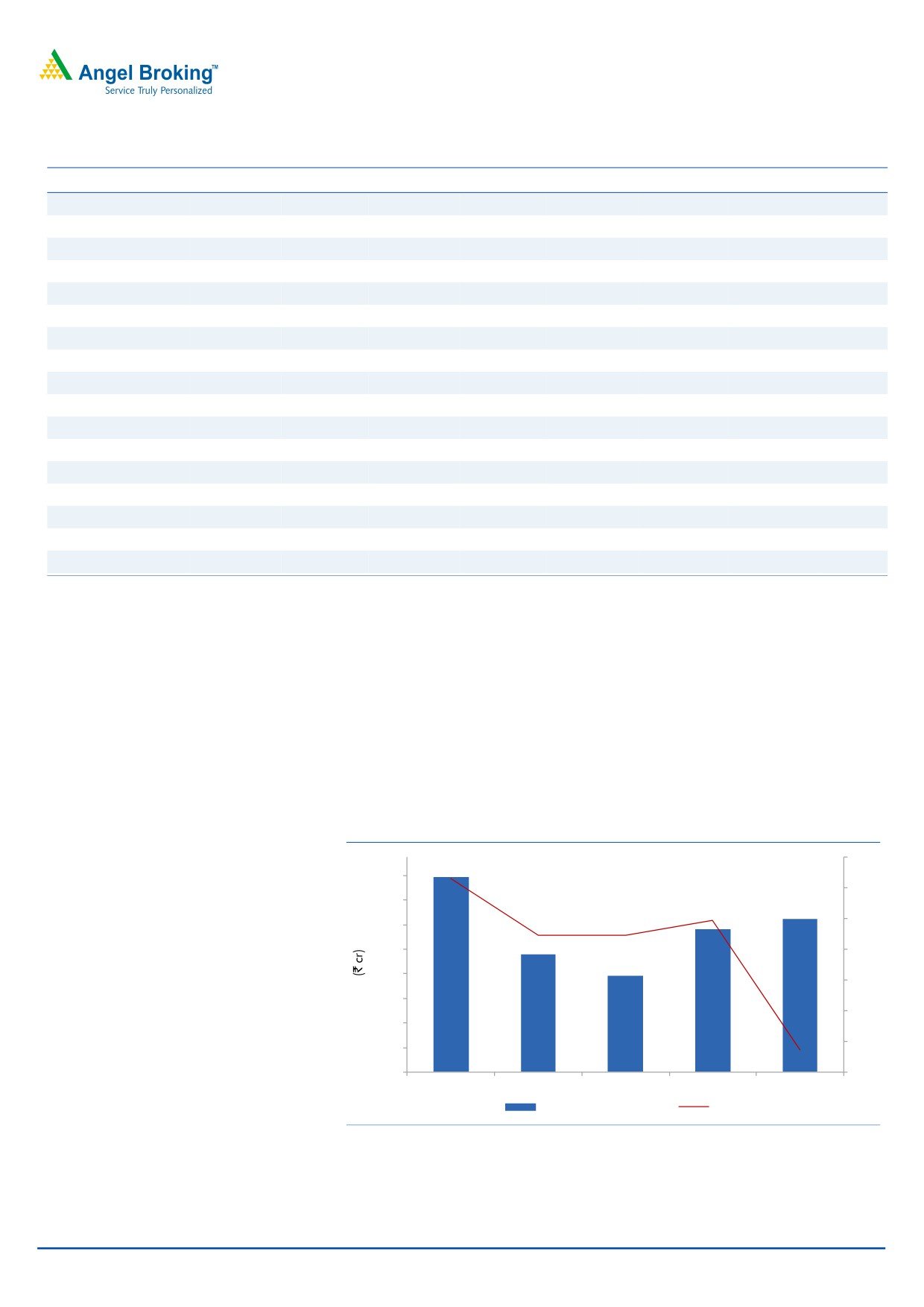

Sales de-grew by 21.4% yoy

For 2QFY2016, sales were adversely impacted due to poor monsoon in India,

while the international market also faced pressure with Brazil (a key market for the

company) witnessing a severe drought. In USA, low crop commodity prices along

with higher inventory prices impacted consumption. The company’s seed business

also posted a 35% yoy drop in sales due to lower purchases by the government

and shift in cropping pattern. On account of weak monsoon, the company’s

domestic business posted flat growth.

Exhibit 2: Total revenue performance

10

636

640

5

560

500

464

0

480

385

400

(5)

315

320

(10)

240

(15)

160

(20)

80

0

(25)

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

Total Revenue

% YoY

Source: Company, Angel Research

November 4, 2015

2

Rallis India | 2QFY2016 Result Update

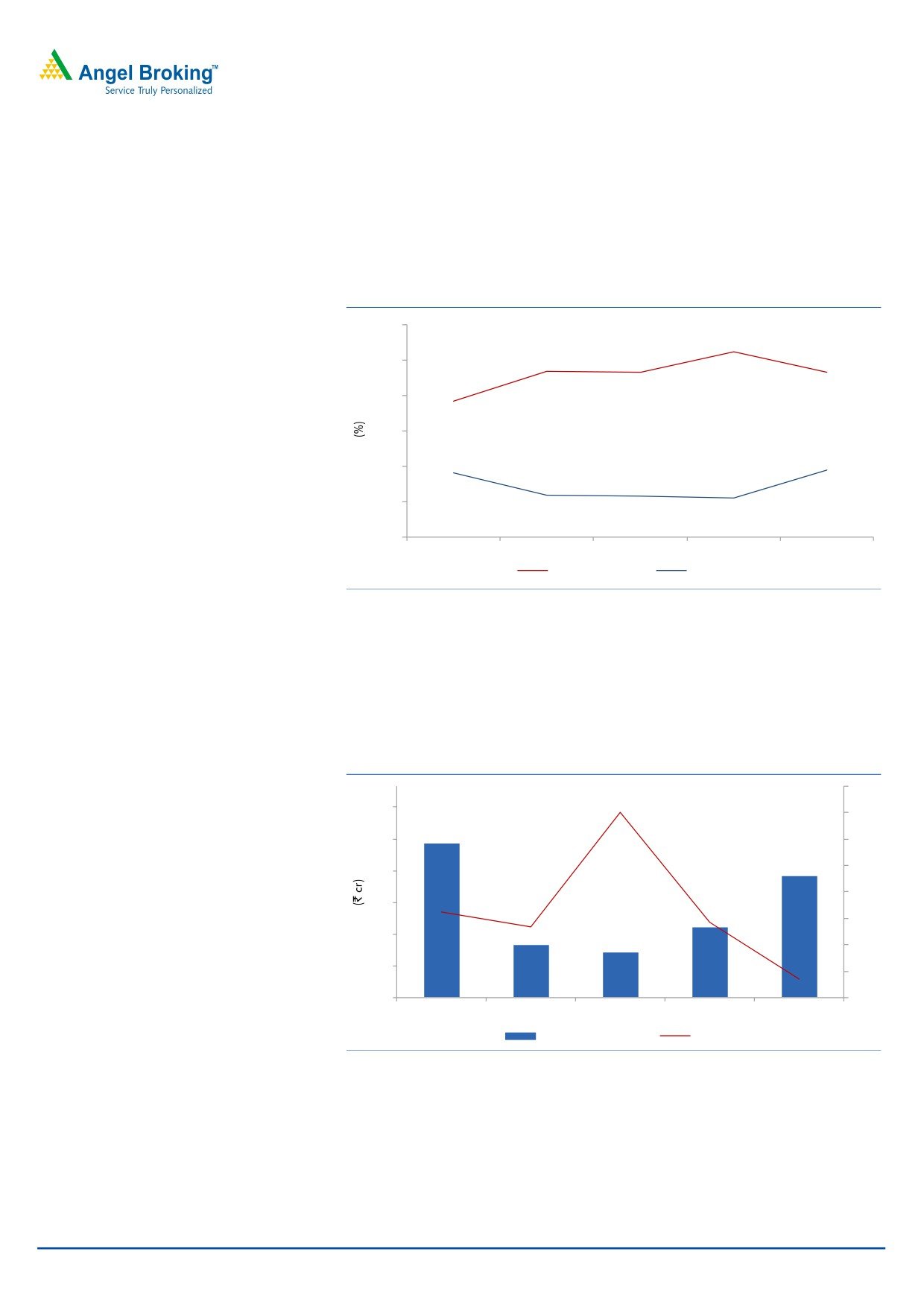

OPM dips yoy

On the operating front, the gross margin for the quarter came in at 46.7% V/s

38.5% in 2QFY2015, which led the OPM to come in at 18.9% V/s 18.2% in

2QFY2015. An 11% and 5.0% yoy rise in staff costs and other expenditure,

respectively, weighed down margins.

Exhibit 3: Margin trend (%)

60.0

52.5

46.8

46.6

46.7

50.0

38.5

40.0

30.0

20.0

18.2

18.9

10.0

11.9

11.7

11.2

0.0

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

Gross margin

EBITDA margin

Source: Company, Angel Research

Earnings decline

The PBT for the quarter posted a decline of 21.9% yoy owing to a 31.3% dip in

other income. The Adj. net profit declined by 22.0% yoy to ~`57cr. Tax expenses

during the quarter dipped by 18.3% to `28cr V/s `34cr in 2QFY2015.

Exhibit 4: Adjusted PAT trend

15

90

10

73

75

5

57

0

60

(5)

45

33

(10)

30

25

21

(15)

15

(20)

0

(25)

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

Adj PAT

% YoY

Source: Company, Angel Research

November 4, 2015

3

Rallis India | 2QFY2016 Result Update

Concall Highlights

The Management has maintained its cautious outlook for the ensuing Rabi

season as low ground water level remains a concern. Water in reservoirs is

lower by 20-25% compared to the average levels. However, rainfall in late

September, especially in the farming regions of Maharashtra and Karnataka,

has given some hope to farmers of a decent harvest.

The company has taken a decision to offer higher credit to its dealers /

distributors and bring it in line with the industry.

Investment arguments

Company set to seize rising opportunities in the domestic crop protection market:

India's overall pesticide consumption is one of the lowest in the world, and has a

huge potential to grow. We believe Rallis is well placed to seize this opportunity on

the back of its wide distribution network, strong brands, and a robust new-product

pipeline. According to industry estimates, the unorganized market accounts for

50% of the industry. Nonetheless, we believe Rallis is in a position to wrest market

share as well as charge a premium for its products. Further, the company has

enhanced focus on the non-pesticide side of the business, which is a high growth

segment, and now constitutes around 30% of its overall sales. Thus, we estimate

Rallis to post a13.0% CAGR in its domestic sales over FY2015-17E.

Exports to register steady growth: Although a late entrant, the company has been

enhancing its focus in the exports market, which is now turning out to be its main

growth driver. Overall exports formed ~30% of sales in FY2015. Going forward,

the segment will continue to post a 20% CAGR over FY2015-17E.

Contract manufacturing to be the next growth driver: Rallis plans to focus on

contract manufacturing for exports and selectively target top players. To facilitate

the same, the company has set up a plant at Dahej, which in FY2013 was working

at full capacity and contributed significantly to the overall growth of the company.

Overall, Rallis targets to achieve a cumulative revenue of `1,000cr over the next

five years from this segment alone. Currently, the company is working on 12-13

projects in the CRAMS business and expects this business to ramp up significantly

over the next few years

Outlook and valuation

The Management is confident of the prospects of key crops such as cotton and

paddy due to generally normal monsoons, which should aid continued healthy

growth in the agrochemicals industry. We expect Rallis to register a CAGR of

15.1% and 16.7% in net sales and profit respectively, over FY2015-17E. At the

current levels, the stock is trading at a fair valuation of 18.7x its FY2017E EPS.

Hence, we maintain our Neutral recommendation on the stock.

November 4, 2015

4

Rallis India | 2QFY2016 Result Update

Exhibit 5: Key assumptions

Particulars (%)

FY2016E

FY2017E

Domestic growth

13.0

13.0

Export growth

20.0

20.0

Total revenue growth

15.1

15.2

EBITDA margin

14.4

14.4

Capex (` cr)

50

70

Source: Company, Angel Research

Exhibit 6: Peer valuation

Company

Reco

Mcap CMP TP Upside

P/E (x)

EV/Sales (x)

EV/EBITDA (x)

RoE (%)

CAGR (%)

(` cr)

(`)

(`)

(%) FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E

Sales PAT

Rallis

Neutral

4,011

206

-

-

21.8

18.7

2.0

1.7

14.0

11.9

21.1

21.3

15.1

16.7

United Phosphorus Accumulate

19,347

451

510

13.1

14.0

11.6

1.8

1.5

10.3

8.6

21.4

21.3

15.0

20.0

Source: Company, Angel Research, Bloomberg

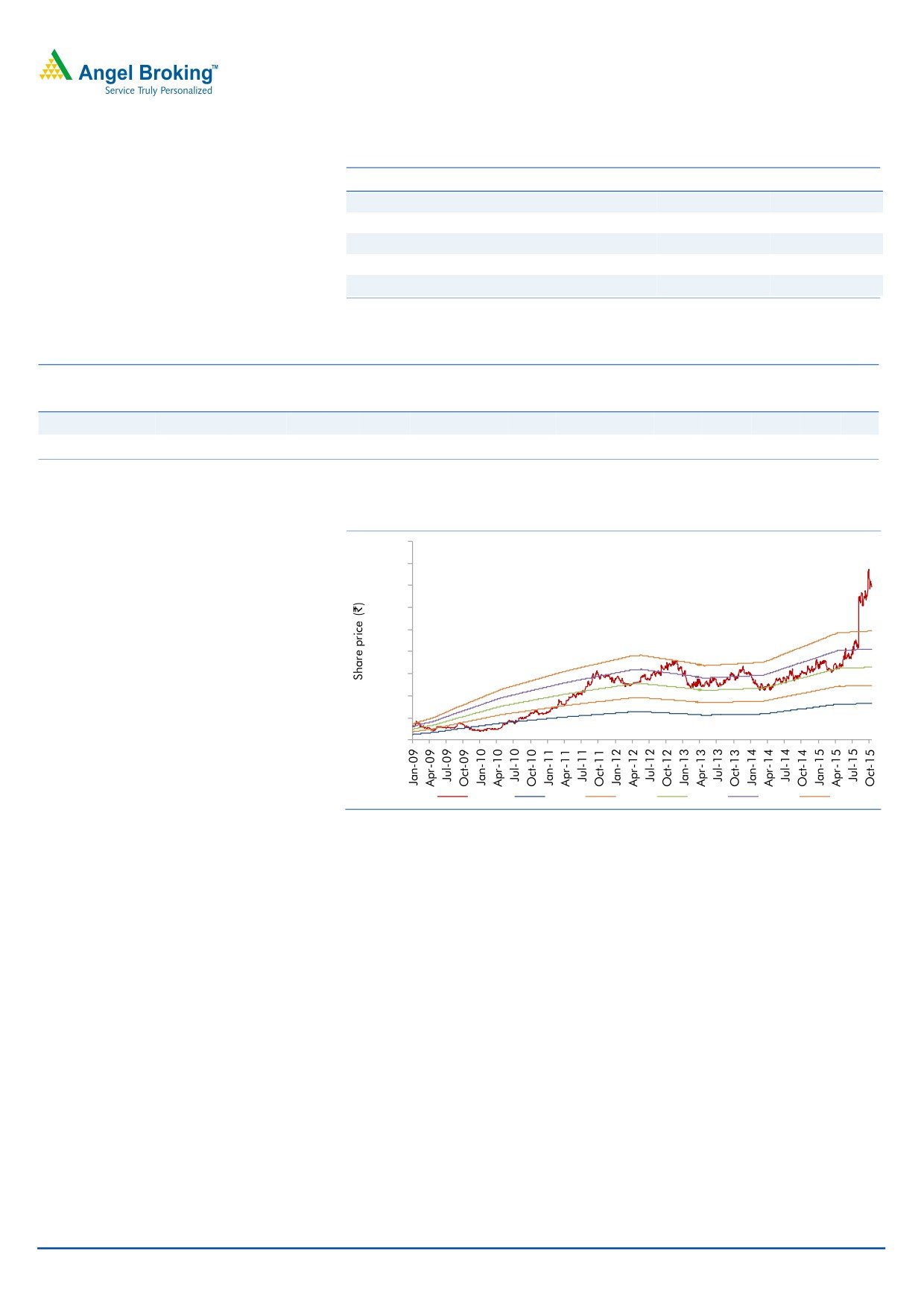

Exhibit 7: One-year forward P/E band

450.0

400.0

350.0

300.0

250.0

200.0

150.0

100.0

50.0

0.0

Price

10x

15x

20x

25x

30x

Source: C-line, Angel Research

Company Background

Rallis is one of the oldest and second largest pesticide agrichemical companies in

the country with a market share of around 13% and belongs to the Tata Group.

The company also has a credible presence in the international market. Pesticides

account for 97% of the company's total revenues, while plant nutrients, seeds and

leather chemicals contribute the balance. Contribution from the domestic business

stands at ~70%, while exports account for the balance.

November 4, 2015

5

Rallis India | 2QFY2016 Result Update

Profit & loss (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Gross sales

1,328

1,535

1,840

1,922

2,212

2,548

Less: Excise duty

79

95

114

121

136

154

Net Sales

1,249

1,440

1,726

1,801

2,075

2,394

Other operating income

25

18

21

21

21

21

Total operating income

1,275

1,458

1,747

1,822

2,097

2,415

% chg

17.4

14.4

19.8

4.3

15.1

15.2

Total Expenditure

1,058

1,241

1,485

1,545

1,777

2,050

Net Raw Materials

695

823

1,008

995

1,206

1,391

Other Mfg costs

255

304

342

341

393

454

Personnel

90

94

111

129

149

172

Other

18

20

24

25

29

33

EBITDA

192

199

240

256

298

344

% chg

10.0

3.9

20.8

6.5

16.5

15.3

(% of Net Sales)

15.3

13.8

13.9

14.2

14.4

14.4

Depreciation & Amortisation

29

32

41

50

50

54

EBIT

188

186

221

228

269

311

% chg

6.3

(1.5)

18.9

3.1

18.4

15.4

(% of Net Sales)

15.1

12.9

12.8

12.6

13.0

13.0

Interest & other Charges

17

21

13

10

11

10

Other Income

5

5

6

4

4

4

(% of PBT)

3

3

3

2

2

1

Share in profit of Associates

-

-

-

-

-

-

Recurring PBT

176

170

214

222

263

306

% chg

(4.2)

(3.5)

26.3

3.4

18.5

16.4

Extraordinary Expense/(Inc.)

(23)

3

-

-

-

-

PBT (reported)

153

172

214

222

263

306

Tax

49

53

62

62

79

92

(% of PBT)

31.8

31.0

28.8

27.9

30.0

30.0

Minority Interest

2

(0)

0.8

2.6

2.6

2.6

PAT (reported)

99

119

152

157

184

214

ADJ. PAT

109

114

152

157

184

214

% chg

(13.3)

4.6

32.9

3.5

16.9

16.4

(% of Net Sales)

8.7

7.9

8.8

8.7

8.9

8.9

Basic EPS (`)

5.6

5.9

7.8

8.1

9.5

11.0

Fully Diluted EPS (`)

5.6

5.9

7.8

8.1

9.5

11.0

% chg

(13.3)

4.6

32.9

3.5

16.9

16.4

November 4, 2015

6

Rallis India | 2QFY2016 Result Update

Balance sheet (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

SOURCES OF FUNDS

Equity Share Capital

19

19

19

19

19

19

Preference Capital

-

-

-

-

-

-

Reserves & Surplus

534

601

699

795

910

1,056

Shareholders Funds

553

621

718

815

930

1,075

Minority Interest

1

5

10

10

10

10

Total Loans

151

131

75

111

111

80

Other Long Term Liabilities

0

6

4

4

4

4

Long Term provisions

18

30

15

19

19

19

Deferred Tax Liability

13

28

32

36

36

36

Total Liabilities

736

821

853

993

1,113

1,227

APPLICATION OF FUNDS

Gross Block

551

581

651

687

737

807

Less: Acc. Depreciation

189

195

233

282

332

386

Net Block

362

386

418

405

405

421

Capital Work-in-Progress

60

35

21

21

21

21

Goodwill

155

169

186

196

196

196

Investments

23

20

25

24

24

24

Long Term Loans and Adv.

91

92

98

110

119

137

Current Assets

432

488

549

680

850

1,007

Cash

11

26

9

7

32

64

Loans & Advances

45

28

40

28

75

86

Other

375

435

500

645

743

857

Current liabilities

387

368

445

443

502

579

Net Current Assets

45

120

104

237

348

428

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

736

821

853

993

1,113

1,227

November 4, 2015

7

Rallis India | 2QFY2016 Result Update

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

Profit before tax

153

172

214

222

263

306

Depreciation

29

32

41

50

50

54

(Inc)/Dec in Working Capital

(28)

(61)

(7)

(147)

(94)

(67)

Direct taxes paid

(38)

(53)

(62)

(62)

(79)

(92)

Cash Flow from Operations

144

150

186

63

139

201

(Inc.)/ Dec. in Fixed Assets

(55)

(5)

(56)

(36)

(50)

(70)

(Inc.)/ Dec. in Investments

3

3

(5)

1

-

-

Inc./ (Dec.) in loans and adv.

-

-

-

-

-

-

Cash Flow from Investing

(52)

(2)

(61)

(35)

(50)

(70)

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

35

(6)

(73)

40

0

(31)

Dividend Paid (Incl. Tax)

(47)

(50)

(55)

(68)

(68)

(68)

Others

(82)

(78)

(14)

(1)

-

-

Cash Flow from Financing

(95)

(134)

(142)

(29)

(64)

(99)

Inc./(Dec.) in Cash

(3)

15

(17)

(2)

25

32

Opening Cash balances

15

11

26

9

7

32

Closing Cash balances

11

26

9

7

32

64

November 4, 2015

8

Rallis India | 2QFY2016 Result Update

Key ratios

Y/E March

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

36.7

35.1

26.4

25.5

21.8

18.7

P/CEPS

22.3

26.6

20.8

19.4

17.2

15.0

P/BV

7.3

6.5

5.6

4.9

4.3

3.7

Dividend yield (%)

1.0

1.0

1.0

1.0

1.5

1.9

EV/Sales

3.4

2.9

2.4

2.3

2.0

1.7

EV/EBITDA

22.3

21.3

17.4

16.4

14.0

11.9

EV / Total Assets

5.8

5.2

4.9

4.2

3.8

3.3

Per Share Data (`)

EPS (Basic)

5.6

5.9

7.8

8.1

9.5

11.0

EPS (fully diluted)

5.6

5.9

7.8

8.1

9.5

11.0

Cash EPS

9.3

7.7

9.9

10.6

12.0

13.8

DPS

2.0

2.0

2.0

2.0

3.0

4.0

Book Value

28.4

31.9

36.9

41.9

47.8

55.3

Dupont Analysis

EBIT margin

15.1

12.9

12.8

12.6

13.0

13.0

Tax retention ratio

68.2

69.0

71.2

72.1

70.0

70.0

Asset turnover (x)

1.8

1.9

2.1

2.0

2.0

2.1

ROIC (Post-tax)

19.0

16.6

19.0

18.0

18.1

18.8

Cost of Debt (Post Tax)

8.9

10.1

8.7

7.9

7.0

7.0

Leverage (x)

0.3

0.2

0.2

0.2

0.2

0.1

Operating ROE

22.4

18.0

20.6

19.7

19.8

19.8

Returns (%)

ROCE (Pre-tax)

27.3

23.8

26.4

24.7

25.6

26.6

Angel ROIC (Pre-tax)

44.1

33.7

35.9

32.4

33.0

34.4

ROE

20.6

19.5

22.7

20.5

21.1

21.3

Turnover ratios (x)

Asset Turnover (Gross Block)

2.7

2.6

2.8

2.7

2.9

3.1

Inventory / Sales (days)

72

67

62

74

80

84

Receivables (days)

30

34

35

37

40

42

Payables (days)

131

111

98

105

97

96

WC cycle (ex-cash) (days)

4

16

20

33

48

52

Solvency ratios (x)

Net debt to equity

0.3

0.2

0.1

0.2

0.1

0.0

Net debt to EBITDA

0.8

0.7

0.3

0.5

0.3

0.1

Interest Coverage (EBIT / Int.)

10.9

9.0

17.5

22.5

24.3

32.6

November 4, 2015

9

Rallis India | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay Stock

Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with CDSL and Portfolio Manager

with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a registered entity with SEBI for Research

Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not been debarred/

suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its associates including its relatives/analyst do

not hold any financial interest/beneficial ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not

received any compensation / managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months.

Angel/analyst has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity of

the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in

this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem

necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits

and risks involved), and should consult their own advisors to determine the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be

true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. Angel

Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person

from any inadvertent error in the information contained in this report. Angel Broking Pvt. Limited has not independently verified all the information

contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents

or data contained within this document. While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this

material, there may be regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or

passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection

with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the latest update on

respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may have investment positions in the

stocks recommended in this report.

Disclosure of Interest Statement

Rallis India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 4, 2015

10