Quick take | BANK

January 7, 2018

RBL Bank

BUY

CMP

`573

Target Price

`690

RBL Bank (RBL), formerly Ratnakar Bank, was founded in 1943 and is a 75-year

Investment Period

12 Months

old bank now. Post induction of Mr. Vishwavir Ahuja, RBL has transformed from

a small & regional bank to a new age bank with all the products and

technologies that any private bank has to offer. The bank’s advances have

Stock Info

registered healthy CAGR of 42% over FY2014-18. As of Q2FY2019, it has

Sector

Banking

branch network of 268 and CASA ratio of 24.5%; wholesale lending forms 59%

Market Cap (` cr)

24,122

of advances and retail 41%.

Beta

1.1

VISION 2020 - Well on track: In FY2016, RBL came up with an IPO and had set

52 Week High / Low

652/439

VISION 2020 with a target to grow advances at 30-35% CAGR, increase CASA

Avg. Daily Volume

73,296

by 75-100bps every year and elevate ROA to 1.5% by 2020. Since, then, the

Face Value (`)

10

bank has been progressing on the path to achieve this target. Advances grew at

BSE Sensex

35,850

healthy CAGR of 38% over FY2016-18 and CASA increased by 590bps to 24.5%

Nifty

10,771

in Q2FY2019. Further, cost control measures, improvement in core fee income

Reuters Code

RATB.NS

and stable asset quality has aided ROA improvement by 0.28bps to 1.26% in

Bloomberg Code

RBK.IN

Q2FY2019.

Impeccable asset quality: Despite growing the loan book aggressively, RBL

Bank’s asset quality has not deteriorated like that of other corporate lenders.

Shareholding Pattern (%)

RBL’s GNPA rose from 1% in FY2016 to 1.40% in Q2FY2019 however, other

Promoters

7.8

corporate lenders witnessed deterioration in asset quality by more than 400bps

MF / Banks / Indian Fls

20.7

during the same time. As on Q2FY2019, restructured assets are 0.7% of

FII / NRIs / OCBs

39.8

advances, exposure to IBC list I/II is negligible and in RBI annual review of Asset

Indian Public / Others

31.7

quality banks divergence was negligible, where RBI checks that all NPA are

disclosed as per norms. This clearly indicates strong risk management practice of

the bank.

Abs.(%)

3m 1yr

3yr

NIM to sustain: NIM has improved 120bps from FY2016 to 3.8% in Q2FY2019.

Sensex

(1.7)

6.1

-

Despite offering differential rates in SA deposits, NIM has been improving

RBL Bank

8.5

10.8

-

continuously, owing to rising share of high yielding retail loans and lower interest

reversals, as slippages remain under control. We expect that NIMs will remain

stable over FY2018-20E, as retail contribution is likely to grow and COF to

3-year price chart

remain moderate with rising CASA.

700

Outlook & valuation: RBL Bank currently trades at 2.9x its FY2020E book value,

600

500

which we believe is reasonable for a bank with focused management, high-

400

growth traction, improving CASA and prospects of improvement in NIM & return

300

ratio. Hence, we recommend Buy on the stock, with a Target Price of `690.

200

Exhibit 1: Key Financials

100

Y/E March (` cr)

FY16

FY17

FY18

FY19E

FY20E

0

NII

819

1,221

1,766

2,478

3,219

% chg

42

42

27

33

34

Net profit

292

446

635

914

1,195

Source: Company, Angel Research

% chg

41.2

52.5

42.3

44.0

30.7

NIM (%)

2.6

2.9

3.4

3.6

3.6

EPS ( `)

7.0

10.6

15.1

21.8

28.5

P/E (x)

75

49

35

24

18

Jaikishan Parmar

P/ABV (x)

7.5

5.2

3.4

3.0

2.7

Research Analyst

RoA (%)

0.9

1.0

1.1

1.3

1.3

022 - 3935 7800 Ext: 6810

RoE (%)

11.2

12.2

11.5

12.9

15.0

Source: Company CMP as on 07/01/2019

Please refer to important disclosures at the end of this report

1

RBL Bank

Key investment arguments

VISION 2020 - Well on track: In FY2016, RBL came up with an IPO and had set

VISION 2020 with a target to grow advances at 30-35% CAGR, increase CASA by

75-100bps every year and elevate ROA to 1.5% by 2020. Since, then, the bank

has been progressing on the path to achieve this target. Advances grew at healthy

CAGR of 38% over FY2016-18 and CASA increased by 590bps to 24.5% in

Q2FY2019. Further, cost control measures, improvement in core fee income and

stable asset quality has aided

ROA improvement by 0.28bps to 1.26% in

Q2FY2019.

Exhibit 1: Vision 2020 well on track

RBL Vision 2020

Actual 2QFY19

Particular

(Post IPO/Sept 2016)

FY16

FY17

FY18

1QFY19

2QFY19

Advances

30-35% CAGR

47

39

37

36

37

0.75 - 1% increase

CASA Ratio (%)

18.6

22

24.3

24.5

24.5

every year

Cost/Income ratio of

Operational Efficiency (%)

58.6

53.5

53

51.5

51.5

51% - 52% by 2020

Return Ratios (%)

~ 1.50% RoA by 2020

0.98

1.08

1.21

1.22

1.26

Other Income (%)

~ 1/3rd of Net Total Income

37

38

38

37

36

Source: Company

Retail business to drive growth: Since FY2012, RBL Bank has been focusing on

building the retail business and the retail book has been growing at healthy rate.

RBL has divided retail assets into three verticals viz. (1) Branch & Business Banking

(BBB), (2) Development Banking, and (3) Financial Inclusion (DB&FI) and Agri.

BBB segment offers LAP, business loans, personal loans, cards and other loans.

Exhibit 2: Retail loan book trend

Particular (`)

FY13

FY14

FY15

FY16

FY17

FY18

BBB

690

1630

2360

3465

5,370

8,891

yoy %

136

45

47

55

66

DB & FI

720

1320

2080

3,133

4,122

5,684

yoy %

83

58

51

32

38

Agri

210

620

1340

1756

2,109

1,940

yoy %

195

116

31

20

-8

Non-Wholesale

1,620

3,570

5,780

8,354

11,601

16,515

yoy %

120

62

45

39

42

Source: Company

RBL is gaining market share in credit cards:

RBL had tied up with Bajaj Finance (NBFC) in FY2017 to launch a series of co-

branded credit cards for Indian customers. With this partnership, RBL Bank is

strengthening its scale of operations in the credit cards business, while the

January 07, 2019

2

RBL Bank

partnership has also enabled Bajaj Finance to expand its EMI network, especially

in the consumer finance space.

The tie up with Bajaj Finance coupled with focused approach of the management

to build the credit card portfolio, has resulted into an increase in the market share

of RBL Bank, which has doubled over the last one year. Its share in outstanding

number of cards has increased from a minuscule 0.9% in March 2017 to 2.1% in

March 2018. The tie up has worked very well for RBL (refer Exhibit 4).

Exhibit 3: RBL has gained market share

Particulars (%)

Mar-16

Mar-17

Mar-18

Apr-18

May-18

Jun-18

Jul-18

Aug-18

HDFC Bank Ltd

29.7

28.6

28.5

28.6

28.5

28.4

28.3

28.2

State Bank Of India

14.8

15.3

16.7

16.8

16.8

16.8

16.7

16.7

ICICI Bank Ltd

14.9

14.3

13.3

13.3

13.4

13.4

13.4

13.4

Axis Bank Ltd

9.8

11.2

12.0

12.0

11.9

11.8

11.8

11.9

Citi Bank

9.8

8.5

7.1

6.7

6.7

6.7

6.6

6.5

Kotak Mahindra Bank Ltd

3.0

3.5

3.9

4.0

4.0

4.1

4.1

4.1

Standard Chartered Bank Ltd

4.1

3.7

3.3

3.4

3.3

3.3

3.2

3.2

American Express

3.4

3.4

3.2

3.2

3.2

3.1

3.1

3.1

Ratnakar Bank Limited

0.6

0.9

2.1

2.3

2.4

2.5

2.6

2.7

IndusInd Bank Ltd

1.8

2.0

2.1

2.1

2.1

2.1

2.1

2.1

Source: Company

Majority of the banks have incrementally added new credit cards in the range of

1.1x to 2x over FY2017-18, however, RBL has added 3.9x over the same time

period. RBL has not only added credit cards but has enhanced the the customer

base also, which has proved to be business accretive. The share in number of

transactions has increased & spending per card has been continuously rising. RBL’s

ticket size per transaction has improved steadily and it is amongst the top five in

the industry.

Exhibit 4: New credit card addition growth

Particular

Mar-17

Mar-18

YoY Growth

HDFC Bank Ltd

1,31,416

5,18,726

3.95

State Bank Of India

81,903

1,61,169

1.97

ICICI Bank Ltd

9,49,006

16,89,312

1.78

Axis Bank Ltd

12,63,028

21,41,655

1.70

Citi Bank

1,42,321

1,98,638

1.40

Kotak Mahindra Bank Ltd

3,17,195

4,18,078

1.32

Standard Chartered Bank Ltd

6,00,940

7,43,543

1.24

American Express

9,33,167

11,39,659

1.22

Ratnakar Bank Limited

1,28,434

1,46,069

1.14

IndusInd Bank Ltd

1,68,001

1,78,257

1.06

Source: Company

RBL is aiming to double the customer base in FY2019E and the bank has set a

target of 40 lakh card users (customers) by FY2021E, as it aims to become a

prominent player in the country. Bajaj Finance has customer base of over ~30

million, which will help RBL to achieve its target of becoming top player in the

January 07, 2019

3

RBL Bank

industry. Improvement in credit card business would help RBL to grow its retail loan

book and also aid to generate higher fee income.

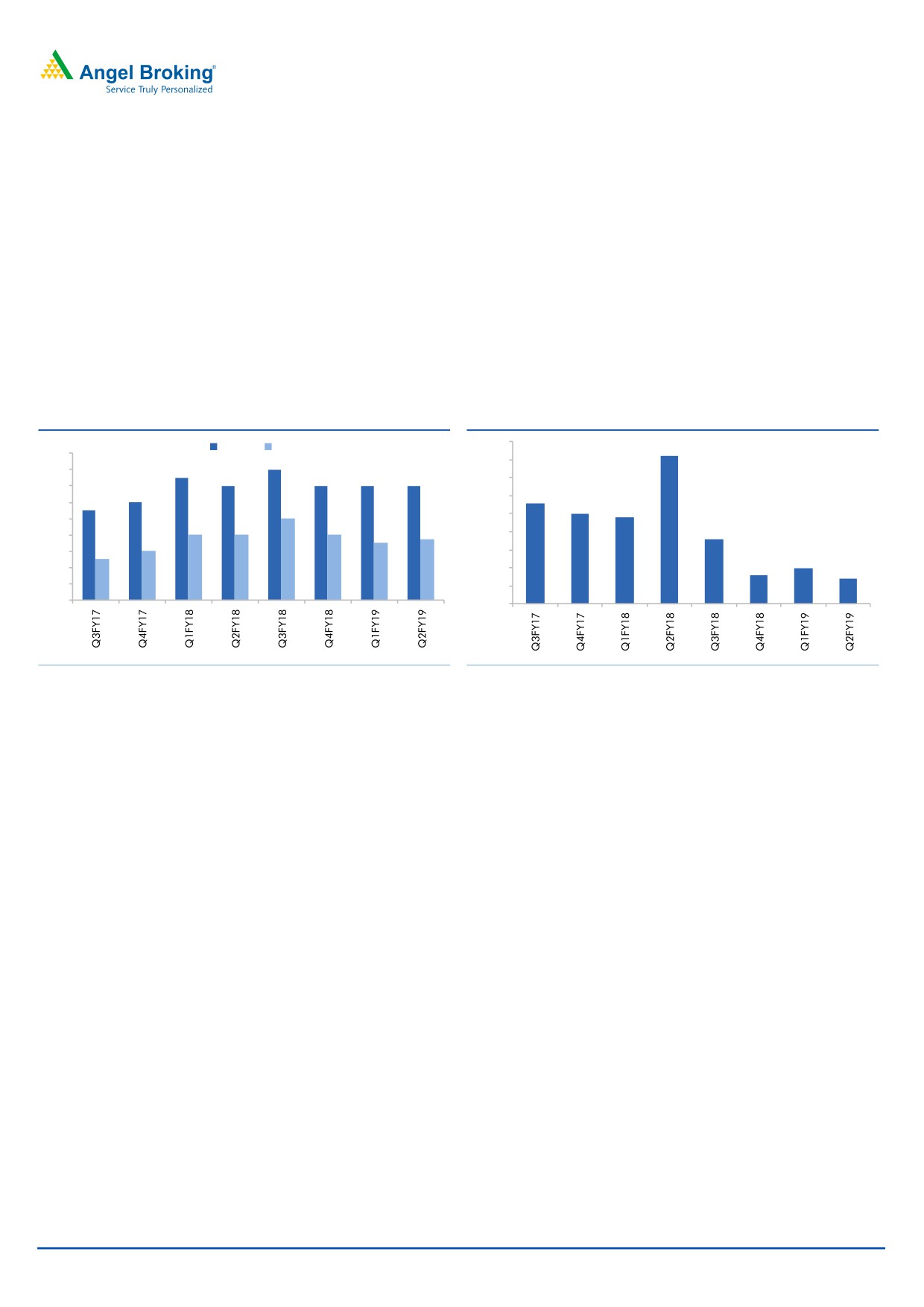

Impeccable asset quality: Most of the corporate lenders have witnessed jump

in GNPA largely owing to exposure to steel and power sectors, where lot of

projects have got stuck owing to delay in regulatory approvals and changes in

policy. Further, in RBI’s annual review of Asset quality, RBL’s divergence was

negligible, where RBI checks that all NPA are disclosed as per norms.

According to Divergence with the RBI during asset quality review (AQR) on

FY2016, the gross NPAs for RBL stood at 1.6% of FY2016 advances. For

FY2017, divergence further reduced and which is just 17bps of Q3FY18 loan

book. This clearly indicates that the bank is following strong credit risk

monitoring.

Exhibit 5: GNPA & NPA

Exhibit 6: Restructured assets as (%) of advance

GNPA% NPA%

0.45

0.41

1.8

1.6

0.40

1.5

1.6

1.4

1.4

1.4

1.4

0.35

1.4

1.2

0.28

1.1

0.30

1.2

0.25

1.0

0.24

0.25

1.0

0.8

0.8

0.8

0.7

0.18

0.7

0.20

0.8

0.6

0.6

0.5

0.15

0.10

0.08

0.4

0.10

0.07

0.2

0.05

0.0

0.00

Source: Company

Source: Company

Despite growing the loan book aggressively, RBL Bank’s asset quality has not

deteriorated like that of other corporate lenders. RBL’s GNPA rose from 1% in

FY2016 to 1.40% in Q2FY2019 however, other corporate lenders witnessed

deterioration in asset quality by more than 400bps during the same time. As on

Q2FY2019, restructured asset is 0.7% of advances, exposure to IBC list I/II is

negligible in RBI annual review of Asset quality banks divergence was negligible,

which clearly indicates strong risk management practices of the bank.

NIM to sustain: NIM has improved 120bps from FY2016 to 3.8% in Q2FY2019.

Despite offering differential rates in SA deposits, NIM has been improving

continuously, owing to rising share of high yielding retail loans and lower interest

reversals, as slippages remain under control. We expect that NIMs will remain

stable over FY2018-20E, as retail contribution is likely to grow and COF to remain

moderate with rising CASA.

January 07, 2019

4

RBL Bank

Outlook & valuation: RBL Bank currently trades at 2.9x its FY2020E book value,

which we believe is reasonable for a bank with focused management, high-growth

traction, improving CASA and prospects of improvement in NIM & return ratio.

Hence, we recommend Buy on the stock, with a Target Price of `690.

Exhibit 7: Comparative DuPont analysis

Du Pont (%)

RBL

HDFC ICICI

IndusInd

Yes

DCB

Federal

City Union

FY2018

Bank

Bank

Bank

Bank

Bank

Bank

Bank

Bank

NII

3.2

4.2

2.8

3.7

2.9

3.7

2.8

3.8

Non Interest Income

1.9

1.6

2.1

2.4

2.0

1.1

0.9

1.4

Total Revenues

5.1

5.7

4.9

6.1

4.9

4.8

3.7

5.2

Operating Cost

2.6

2.5

1.9

2.8

2.0

2.9

1.9

2.0

PPP

2.5

3.3

3.0

3.3

2.9

1.9

1.8

3.2

Total provisions

0.7

0.6

2.1

0.6

0.6

0.5

0.7

1.1

Pre-Tax Profit

1.8

2.7

0.9

2.7

2.3

1.4

1.1

2.1

Tax

0.7

1.0

0.1

0.9

0.7

0.5

0.4

0.5

ROA

1.1

1.7

0.8

1.8

1.6

0.9

0.7

1.6

Leverage

10.0

9.8

8.1

9.0

11.0

10.8

12.0

9.7

RoE (%)

11.5

16.8

6.6

16.2

17.7

9.8

8.3

15.3

Source: Company

Company background

RBL Bank (RBL), formerly Ratnakar Bank, was founded in 1943 and is a 75-year

old bank now. Post induction of Mr. Vishwavir Ahuja, RBL has transformed from a

small & regional bank to a new age bank with all the products and technologies

that any private bank has to offer. The bank’s advances have registered healthy

CAGR of 42% over FY2014-18. As of Q2FY2019, it has branch network of 268

and CASA ratio of 24.5%; wholesale lending forms 59% of advances and retail

41%.

Key risks to our estimates

Deterioration in asset quality, slowdown in growth and bloating up of costs are

the key risks.

Unsecured loan book resulting in higher than anticipated defaults and credit

costs.

January 07, 2019

5

RBL Bank

Income Statement

Y/E March (` cr)

FY16

FY17

FY18

FY19E

FY20E

Net Interest Income

819

1,221

1,766

2,478

3,219

- YoY Growth (%)

47

49

45

40

30

Other Income

491

755

1,068

1,372

1,852

- YoY Growth (%)

22

54

41

28

35

Operating Income

1,310

1,977

2,834

3,850

5,072

- YoY Growth (%)

36

51

43

36

32

Operating Expenses

767

1,056

1,504

1,975

2,601

- YoY Growth (%)

28

38

42

31

32

Pre - Provision Profit

542

920

1,331

1,874

2,470

- YoY Growth (%)

51

70

45

41

32

Prov. & Cont.

114

239

365

489

660

- YoY Growth (%)

90

109

53

34

35

Profit Before Tax

428

681

966

1,385

1,810

- YoY Growth (%)

43

59

42

43

31

Prov. for Taxation

136

235

331

471

615

- as a % of PBT

32

35

34

34

34

PAT

292

446

635

914

1,195

- YoY Growth (%)

41

53

42

44

31

Balance Sheet

Y/E March (` cr)

FY16

FY17

FY18

FY19E

FY20E

Equity

325

375

420

420

420

Reserve & Surplus

2,665

3,960

6,264

7,041

8,057

Networth

2,989

4,336

6,684

7,461

8,476

Deposits

24,349

34,588

43,902

58,325

78,303

- Growth (%)

42

42

27

33

34

Borrowings

10,536

7,980

9,261

12,410

16,630

Other Liab. & Prov.

1,330

1,785

2,003

3,851

3,854

Total Liabilities

39,204

48,689

61,851

82,047

1,07,263

Cash Balances

1,340

2,948

2,589

3,578

4,782

Bank Balances

1,110

1,246

1,695

2,045

2,733

Investments

14,436

13,482

15,448

19,934

23,910

Advances

21,229

29,449

40,268

54,362

73,388

- Growth (%)

47

39

37

35

35

Fixed Assets

177

259

334

460

615

Other Assets

912

1,306

1,517

1,669

1,836

Total Assets

39,204

48,689

61,851

82,047

1,07,263

January 07, 2019

6

RBL Bank

Key Ratio

Y/E March

FY16

FY17

FY18

FY19E

FY20E

Profitability ratios (%)

NIMs

2.6

2.9

3.4

3.6

3.6

Cost to Income Ratio

58.6

53.4

53.0

51.3

51.3

RoA

0.9

1.0

1.1

1.3

1.3

RoE

11.2

12.2

11.5

12.9

15.0

B/S ratios (%)

CASA Ratio

0.19

0.22

0.24

0.25

0.26

Credit/Deposit Ratio

0.9

0.9

0.9

0.9

0.9

Asset Quality (%)

Gross NPAs

0.98

1.21

1.41

1.33

1.25

Gross NPAs (Amt)

208.1

356.8

566.7

723.0

917.4

Net NPAs

0.59

0.64

0.78

0.73

0.73

Net NPAs (Amt)

124.4

189.9

314.0

396.8

535.7

Slippages

Credit Cost on Advance

0.54

0.81

0.91

0.90

0.90

Provision Coverage

60%

53%

55%

55%

58%

Per Share Data (`)

EPS

7.0

10.6

15.1

21.8

28.5

BV

71.2

103.3

159.3

177.8

202.0

ABVPS (75% cover.)

69.8

101.3

155.8

173.5

195.8

DPS

1.5

1.8

2.3

3.3

4.3

Valuation Ratios

PER (x)

81.9

53.7

37.7

26.2

20.1

P/BV

8.0

5.5

3.6

3.2

2.8

P/ABVPS (x)

8.2

5.6

3.7

3.3

2.9

Dividend Yield

0.3

0.3

0.4

0.6

0.7

Valuation done on closing price of 04/01/2019

January 07, 2019

7

RBL Bank

Research Team Tel: 022 - 39357800

DISCLAIMER:

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay

Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National Commodity &

Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and Investment Adviser with

SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered entity with SEBI for Research

Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its

associates/analyst has not received any compensation / managed or co-managed public offering of securities of the company covered

by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Disclosure of Interest Statement

RBL Bank

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)