2QFY2016 Result Update | Banking

November 13, 2015

Punjab National Bank

NEUTRAL

CMP

`134

Performance Highlights

Target Price

-

Particulars (` cr)

2QFY16 1QFY16

% chg (qoq) 2QFY15

% chg (yoy)

Investment Period

-

NII

4,322

4,102

5.4

4,151

4.1

Pre-prov. profit

2,939

3,132

(6.2)

2,876

2.2

PAT

621

721

(13.8)

575

7.9

Stock Info

Source: Company, Angel Research

Sector

Banking

Punjab National Bank (PNB) reported a mixed set of numbers for 2QFY2016 with

Market Cap (` cr)

28,263

subdued operating performance, while its asset quality improved marginally.

Beta

1.3

Loan growth remains modest; NIM improves qoq

52 Week High / Low

232/123

During 2QFY2016, advances and deposits grew by 6.7% and 14.0% yoy,

Avg. Daily Volume

5,003,957

respectively, with the CD ratio at 70.6%. Domestic advances growth was sluggish

Face Value (`)

2

at 6.3% yoy, while international advances saw a modest growth of 9.5% yoy. In

BSE Sensex

25,743

domestic advances, the retail loan book grew by 23.0% yoy, aided by 27.6% yoy

Nifty

7,783

growth in housing segment. Industry loans growth was modest at 7.6% yoy as the

Reuters Code

PNBK.NS

bank was cautious lending to the large industry segment.

Bloomberg Code

PNB@IN

CASA deposits grew by 13.4% yoy with Current deposits growing by 25.0% yoy.

The NIM improved by 7bp qoq to 2.97%, due to higher yields. Other income

Shareholding Pattern (%)

(excl. treasury) was weak witnessing a decline of 12.9% yoy due to a decline seen

Promoters

62.1

in both fee income and recoveries.

MF / Banks / Indian Fls

19.7

Asset quality improved for the second consecutive quarter as the Gross NPA ratio

FII / NRIs / OCBs

13.0

decreased by 11bp qoq to 6.36%, while the Net NPA also drifted downwards by

Indian Public / Others

5.3

6bp qoq to 3.99%. The bank reported the second quarter of consecutive

significant decline in slippages on a qoq basis to `2,613cr (annualized slippage

ratio stood at 2.8%) as compared to `3,382cr in 1QFY2016. Out of the total

Abs. (%)

3m 1yr

3yr

slippages, fresh slippage for the quarter was to the tune of `2,388cr while fresh

Sensex

(8.4)

(7.6)

37.9

restructuring during the quarter was lower at `216cr as against `676cr in 1QFY2016.

PNB

(16.0)

(27.5)

(13.4)

The outstanding restructured book stood at `38,261cr, 10.3% of the loan book.

Outlook and valuation: PNB has been witnessing improvement in asset quality

3-year price chart

since the past 2 quarters after severe asset quality pain over the previous several

250

quarters. In our view, we expect asset quality pressure to ease from here on given

200

the bank’s seasoned loan book and conservative lending approach followed by

150

the bank as compared to its peers. At the current market price, the stock trades at 0.6x

100

FY2017E ABV. However, given the stress in certain sectors of the economy and with PNB

50

having a meaningful exposure to these stressed sectors, we would follow a cautious

0

stance in the near-term. Hence, we recommend a Neutral rating on the stock.

Key financials

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

Source: Company, Angel Research

NII

16,146

16,556

17,101

19,343

% chg

8.7

2.5

3.3

13.1

Net profit

3,343

3,061

3,316

5,052

Vaibhav Agrawal

% chg

(29.6)

(8.4)

8.3

52.3

NIM (%)

3.2

2.9

2.8

2.8

022 - 3935 7800 Ext: 6808

EPS (`)

18.5

16.5

17.9

27.2

P/E (x)

7.4

8.3

7.7

5.0

P/ABV (x)

0.8

0.8

0.8

0.6

Chintan Shah

RoA (%)

0.6

0.5

0.5

0.7

022 - 3935 7800 Ext: 6839

RoE (%)

10.2

8.5

8.5

12.0

Source: Company, Angel Research; Note: CMP as of November10, 2015

Please refer to important disclosures at the end of this report

1

Punjab National Bank | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance

Particulars (` cr)

2QFY16

1QFY16

% chg (qoq)

2QFY15

% chg (yoy)

FY2015

FY2014

% chg

Interest earned

12,345

12,035

2.6

11,462

7.7

46,315

43,223

7.2

- on Advances / Bills

9,064

8,908

1.7

8,654

4.7

34,794

32,393

7.4

- on investments

3,029

2,906

4.2

2,609

16.1

10,600

10,266

3.3

- on balance with RBI & others

218

169

29.0

137

58.9

632

362

74.5

- on others

35

52

(33.0)

61

(43.6)

289

202

42.9

Interest Expended

8,023

7,932

1.1

7,311

9.7

29,760

27,077

9.9

Net Interest Income

4,322

4,102

5.4

4,151

4.1

16,556

16,146

2.5

Other income

1,357

1,397

(2.9)

1,558

(12.9)

5,891

4,577

28.7

Other income excl. treasury

1,019

1,159

(12.1)

1,330

(23.4)

4,529

3,843

17.9

- Fee Income

784

721

9

591

32.7

2,526

2,380

6.1

- Treasury Income incl. MF Div.

338

238

42.0

228

48.2

1,362

734

85.6

- Recov. from written off a/cs

236

217

8.8

483

(51.1)

1,018

514

98.1

- Others

(1)

221

(100.5)

256

(100.4)

985

949

3.8

Operating income

5,679

5,500

3.3

5,710

(0.5)

22,446

20,723

8.3

Operating expenses

2,740

2,368

15.7

2,834

(3.3)

10,492

9,338

12.4

- Employee expenses

1,878

1,550

21.2

2,034

(7.7)

7,337

6,510

12.7

- Other Opex

863

818

5.5

799

7.9

3,155

2,828

11.6

Pre-provision Profit

2,939

3,132

(6.2)

2,876

2.2

11,955

11,384

5.0

Provisions & contingencies

1,882

1,811

3.9

1,768

6.5

7,998

6,694

19.5

- Provisions for NPAs

2,031

1,291

57.3

1,638

24.0

7,978

4,518

76.6

- Other Provisions

(149)

520

(128.6)

130

(214.6)

20

1,394

(98.6)

PBT

1,056

1,321

(20.0)

1,108

(4.7)

3,957

4,691

(15.6)

Provision for Tax

435

600

(27.4)

533

(18.3)

896

1,348

(33.6)

PAT

621

721

(13.8)

575

7.9

3,062

3,343

(8.4)

Effective Tax Rate (%)

41.2

45.4

(421)bp

48.1

(686)bp

22.6

28.7

(610)bp

Source: Company, Angel Research

November 13, 2015

2

Punjab National Bank | 2QFY2016 Result Update

Exhibit 2: 2QFY2016 performance analysis

Particulars

2QFY16 1QFY16

% chg (qoq) 2QFY15

% chg (yoy)

Advances (` cr)

3,80,958

3,80,880

0.0

3,57,093

6.7

Deposits (` cr)

5,39,924

5,17,733

4.3

4,73,511

14.0

Credit-to-Deposit Ratio (%)

70.6

73.6

(301)bp

75.4

(486)bp

Current deposits (` cr)

36,863

31,938

15.4

29,497

25.0

Saving deposits (` cr)

1,57,683

1,49,555

5.4

1,42,079

11.0

CASA deposits (` cr)

1,94,546

1,81,493

7.2

1,71,576

13.4

Reported CASA ratio (%)

40.2

38.9

129bp

39.9

34bp

CAR (%)

12.2

12.1

12bp

11.8

41bp

Tier 1 CAR (%)

9.4

9.2

18bp

8.7

66bp

Profitability Ratios (%)

Cost of deposits

5.97

6.0

(2)bp

6.1

(17)bp

Yield on advances

9.66

9.56

10bp

9.9

(24)bp

Yield on investments

8.0

7.9

1bp

8.0

(4)bp

Yield on funds

7.68

7.69

(1)bp

8.0

(32)bp

Cost of funds

5.0

5.1

(4)bp

5.1

(7)bp

Reported NIM

2.97

2.9

7bp

3.2

(21)bp

Cost-to-income ratio

48.3

43.1

520bp

49.6

(137)bp

Asset quality

Gross NPAs (` cr)

24,945

25,397

(1.8)

20,752

20.2

Gross NPAs (%)

6.36

6.47

(11)bp

5.7

71bp

Net NPAs (` cr)

15,187

15,394

(1.3)

11,618

30.7

Net NPAs (%)

3.99

4.1

(6)bp

3.3

73bp

Provision Coverage Ratio (%)

61.4

59.3

203bp

59.1

225bp

Slippage ratio (%)

2.7

3.9

(113)bp

4.1

(134)bp

Credit cost (%)

1.4

0.9

47bp

1.2

13bp

Source: Company, Angel Research

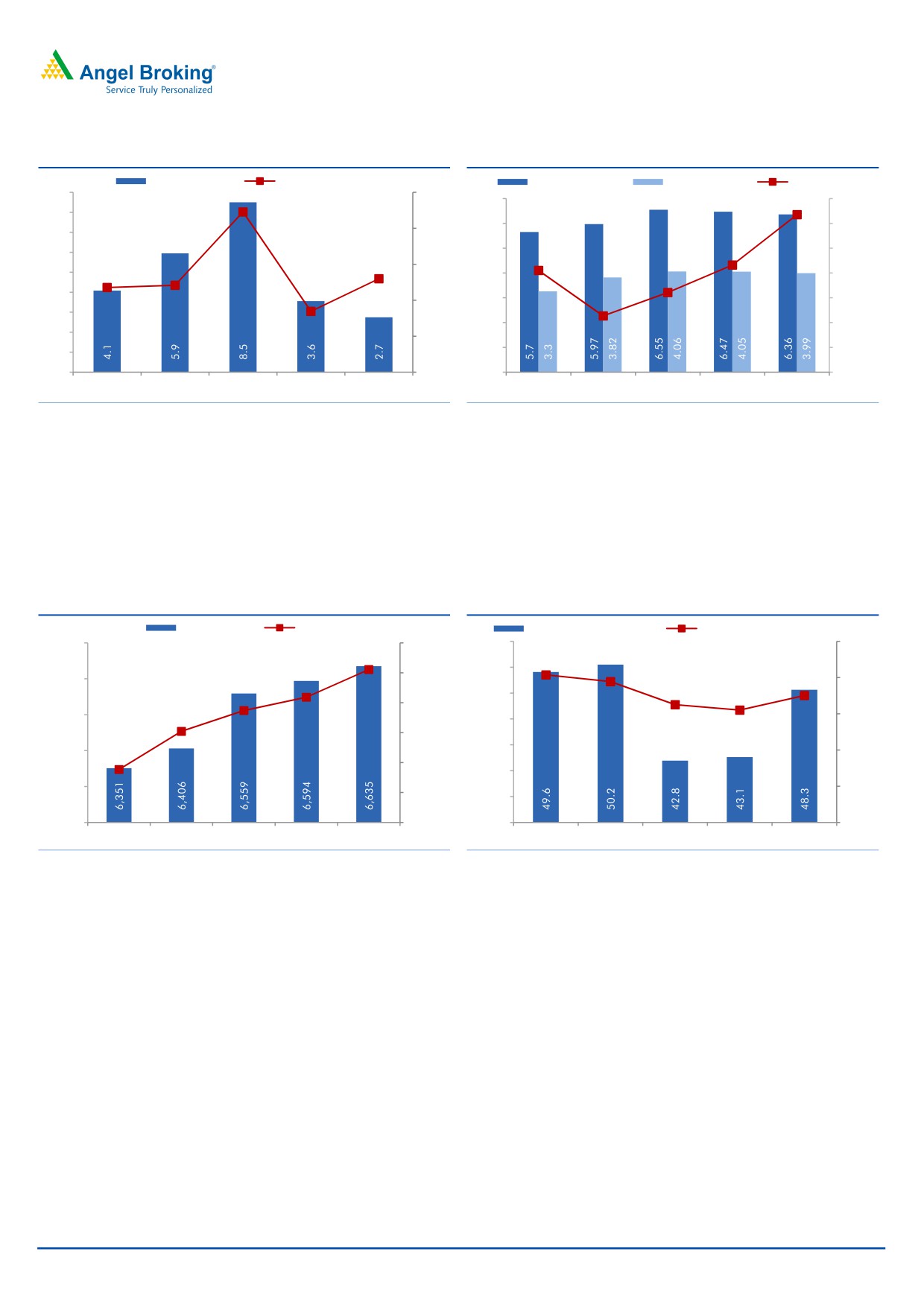

Loan book grows at modest pace; NIM improves qoq

During 2QFY2016, advances and deposits grew by

6.7% and

14.0% yoy,

respectively, with the CD ratio at 70.6%. Domestic advances growth was sluggish

at 6.3% yoy, while international advances saw a modest growth of 9.5% yoy. The

share of overseas advances to total advances constituted 14.1% as against 13.8%

in 2QFY2015. In domestic advances, the retail loan book grew by 23.0% yoy,

aided by 27.6% yoy growth in the housing segment. Growth in industry loans was

modest at 7.6% yoy yoy as the bank was cautious lending to the large industry

segment. CASA deposits grew by 13.4% yoy with Current deposits growing by

25.0% yoy. The Domestic CASA ratio jumped by 129bp qoq to 40.2%, due to the

spurt seen in term deposits. The NIM improved by 7bp qoq to 2.97%, due to

higher yields.

November 13, 2015

3

Punjab National Bank | 2QFY2016 Result Update

Exhibit 3: Cost of funds down by 4bp qoq; 7bp yoy

Exhibit 4: NIM increases by 7bp qoq; dips 21bp yoy

5.25

5.22

(%)

3.30

5.20

3.21

3.18

3.20

5.15

3.10

5.10

5.09

2.97

5.10

5.07

3.00

2.90

5.05

5.03

2.90

2.79

2.80

5.00

2.70

4.95

2.60

2.50

4.90

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Source: Company, Angel Research

Source: Company, Angel Research

Weak Non-interest income (excluding treasury)

Other income (excl. treasury) was weak witnessing a decline of 12.8% yoy due to a

decline seen in both fee income and recoveries. Treasury income surged by

33.7% yoy which provided a cushion to the other income to an extent.

Exhibit 5: Treasury aid non-interest income performance to an extent

Particulars (` cr)

2QFY16 1QFY16

% chg (qoq) 2QFY15

% chg (yoy)

Fee based Income

784

943

(16.9)

822

(4.6)

Treasury

337

237

42.2

252

33.7

Recoveries

236

217

8.8

483

(51.1)

Other income

1,357

1,397

(2.9)

1,557

(12.8)

Other income excl. treasury

1,020

1,160

(12.1)

1,305

(21.8)

Source: Company, Angel Research

Asset quality improves for second consecutive quarter

Asset quality improved consecutively for the second quarter as the Gross NPA ratio

decreased by 11bp to 6.36%, while the Net NPA also drifted downwards by 6bp to

3.99%. The bank reported a second consecutive quarter of significant decline in

slippages on a qoq basis to `2,613cr (annualized slippage ratio stood at 2.8%) as

compared to `3,382cr in 1QFY2016. Out of the total slippages, fresh slippage for

the quarter was to the tune of `2,388cr while fresh restructuring during the quarter

was lower at

`216cr as against

`676cr in 1QFY2016. The outstanding

restructured book stood at `38,261cr, 10.3% of the loan book.

November 13, 2015

4

Punjab National Bank | 2QFY2016 Result Update

Exhibit 6: Slippages ratio falls sharply qoq

Exhibit 7: ...resulting in lower Gross NPA ratio qoq

Slippages (%)

Credit cost (%, RHS)

Gross NPAs (%)

Net NPAs (%)

PCR (%, RHS)

9.0

2.2

2.5

7.0

61.4

62.0

8.0

6.0

61.0

7.0

2.0

5.0

59.3

60.0

6.0

59.1

1.3

1.5

1.2

1.2

5.0

4.0

58.2

59.0

4.0

0.8

1.0

3.0

57.3

58.0

3.0

2.0

57.0

2.0

0.5

1.0

56.0

1.0

-

-

-

55.0

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Source: Company, Angel Research

Source: Company, Angel Research;

Cost-to-income ratio improves

Operating expense was under control which declined 3.3% yoy marked by a

7.7% yoy decline in staff expenses. A lower opex and an improvement in NIM of

7bp enabled the bank to reduce cost/income ratio by 137bp yoy to 48.3% given

the fact that the bank also opened 41 new branches during the quarter.

Exhibit 8: Steady branch expansion continues

Exhibit 9: Cost to income ratio decreases yoy

Branches

ATMs (RHS)

Cost-to-income ratio (%)

Opex to average assets (%, RHS)

6,700

8,622

8,800

52.0

2.5

2.0

50.0

1.9

8,437

8,600

6,600

8,348

1.8

2.0

1.6

48.0

1.6

8,400

8,209

6,500

1.5

46.0

8,200

44.0

6,400

7,954

1.0

8,000

42.0

6,300

0.5

7,800

40.0

6,200

7,600

38.0

-

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Source: Company, Angel Research

Source: Company, Angel Research

Outlook and valuation

PNB has been witnessing improvement in asset quality since the past 2 quarters

after severe asset quality pain over the previous several quarters. In our view, we

expect asset quality pressure to ease from here on given the bank’s seasoned loan

book and conservative lending approach followed by the bank as compared to its

peers. At the current market price, the stock trades at 0.6x FY2017E ABV.

However, given the stress in certain sectors of the economy and with PNB having a

meaningful exposure to these stressed sectors, we would follow a cautious stance

in the near-term. Hence, we recommend a Neutral rating on the stock.

November 13, 2015

5

Punjab National Bank | 2QFY2016 Result Update

Exhibit 10: Recommendation summary

CMP

Tgt. Price

Upside

FY2017E

FY2017E

FY2017E

FY15-17E

FY2017E

FY2017E

Company

Reco.

(`)

(`)

(%)

P/ABV (x)

Tgt. P/ABV (x)

P/E (x)

EPS CAGR (%)

RoA (%)

RoE (%)

HDFCBk

Buy

1,054

1,262

19.7

3.2

3.8

17.3

22.4

1.9

19.7

ICICIBk*

Buy

262

348

32.5

1.8

2.0

10.4

15.3

1.6

15.2

YesBk

Buy

740

914

23.5

1.9

2.4

10.7

20.2

1.6

19.6

AxisBk

Buy

469

630

34.4

1.9

2.6

10.8

18.4

1.8

18.9

SBI*

Buy

241

283

17.3

1.2

1.2

9.9

17.8

0.7

12.8

FedBk

Neutral

54

-

-

1.0

1.0

8.6

3.1

1.0

11.9

SIB

Neutral

20

-

-

0.7

0.8

6.2

21.6

0.7

11.6

BOB

Neutral

173

-

-

0.9

0.9

8.2

17.5

0.6

10.6

PNB

Neutral

134

-

-

0.6

0.6

4.9

28.5

0.7

12.0

BOI

Neutral

132

-

-

0.3

0.8

4.0

14.0

0.3

7.6

IndBk

Neutral

127

-

-

0.4

0.4

4.2

19.4

0.7

9.3

Vijaya Bank

Neutral

34

-

-

0.5

0.5

5.1

14.1

0.4

8.8

OBC

Neutral

148

-

-

0.3

0.5

3.3

65.5

0.5

9.4

Allahabad Bank Neutral

77

-

-

0.3

0.3

3.0

53.5

0.6

10.9

UnionBk

Neutral

161

-

-

0.5

0.4

4.1

18.1

0.6

11.4

CanBk

Neutral

273

-

-

0.4

0.3

4.0

9.8

0.5

10.7

IDBI#

Neutral

77

-

-

0.3

0.4

3.0

53.5

0.6

10.9

DenaBk

Neutral

88

-

-

0.6

0.6

6.2

61.6

0.6

9.3

Source: Company, Angel Research; Note:*Target multiples=SOTP Target Price/ABV (including subsidiaries), #Without adjusting for SASF

November 13, 2015

6

Punjab National Bank | 2QFY2016 Result Update

Company Background

Punjab National Bank is the country's third-largest PSU bank, with a balance sheet

size of around `6.34lakh cr and a pan-India network of around 6,635 branches.

The bank's network is primarily spread across north India, ie in Punjab, Haryana

and Uttar Pradesh. Almost 64% of its branches are based in rural and semi-urban

hinterland, which results in a large legacy of low-cost CASA deposits.

November 13, 2015

7

Punjab National Bank | 2QFY2016 Result Update

Income statement

Y/E March (` cr)

FY12

FY13

FY14

FY15

FY16E

FY17E

Net Interest Income

13,414

14,857

16,146

16,556

17,101

19,343

- YoY Growth (%)

13.6

10.8

8.7

2.5

3.3

13.1

Other Income

4,203

4,216

4,577

5,891

6,537

7,213

- YoY Growth (%)

16.3

0.3

8.6

28.7

11.0

10.3

Operating Income

17,617

19,073

20,723

22,446

23,638

26,557

- YoY Growth (%)

14.2

8.3

8.7

8.3

5.3

12.3

Operating Expenses

7,003

8,165

9,338

10,492

10,544

11,598

- YoY Growth (%)

10.0

16.6

14.4

12.3

0.5

10.0

Pre - Provision Profit

10,614

10,908

11,384

11,955

13,094

14,958

- YoY Growth (%)

17.2

2.8

4.4

5.0

9.5

14.2

Prov. & Cont.

3,577

4,386

6,694

7,998

8,217

7,529

- YoY Growth (%)

43.6

22.6

52.6

19.5

2.7

(8.4)

Profit Before Tax

7,037

6,522

4,691

3,957

4,877

7,430

- YoY Growth (%)

7.2

(7.3)

(28.1)

(15.6)

23.3

52.3

Prov. for Taxation

2,153

1,774

1,348

895

1,561

2,378

- as a % of PBT

30.6

27.2

28.7

22.6

32.0

32.0

PAT

4,884

4,748

3,343

3,061

3,316

5,052

- YoY Growth (%)

10.2

(2.8)

(29.6)

(8.4)

8.3

52.3

Balance sheet

Y/E March (` cr)

FY12

FY13

FY14

FY15

FY16E

FY17E

Share Capital

339

354

362

371

371

371

Reserve & Surplus

27,476

32,323

35,533

38,707

41,286

45,231

Deposits

3,79,588

3,91,560

4,51,397

5,01,379

5,56,530

6,28,879

- Growth (%)

21.3

3.2

15.3

11.1

11.0

13.0

Borrowings

26,074

28,726

36,404

34,331

36,570

41,128

Tier 2 Capital

11,190

10,895

11,630

11,340

11,056

10,780

Other Liab. & Prov.

13,524

15,019

15,093

17,206

19,098

21,387

Total Liabilities

4,58,192

4,78,877

5,50,420

6,03,334

6,64,911

7,47,775

Cash Balances

18,493

17,886

22,246

24,225

27,827

31,444

Bank Balances

10,335

9,249

22,973

31,709

34,945

39,301

Investments

1,22,703

1,29,896

1,43,786

1,51,282

1,70,301

1,89,274

Advances

2,93,775

3,08,725

3,49,269

3,80,534

4,14,782

4,68,704

- Growth (%)

21.3

5.1

13.1

9.0

9.0

13.0

Fixed Assets

3,169

3,358

3,420

3,552

3,797

4,142

Other Assets

9,718

9,763

8,727

12,031

13,259

14,912

Total Assets

4,58,192

4,78,877

5,50,420

6,03,334

6,64,911

7,47,775

- Growth (%)

21.1

4.5

14.9

9.6

10.2

12.5

November 13, 2015

8

Punjab National Bank | 2QFY2016 Result Update

Ratio analysis

Y/E March

FY12

FY13

FY14

FY15

FY16E

FY17E

Profitability ratios (%)

NIMs

3.3

3.3

3.2

2.9

2.8

2.8

Cost to Income Ratio

39.8

42.8

45.1

46.7

44.6

43.7

RoA

1.2

1.0

0.6

0.5

0.5

0.7

RoE

21.1

16.5

10.2

8.5

8.5

12.0

B/S ratios (%)

CASA Ratio

35.3

39.2

38.3

36.7

37.0

37.3

Credit/Deposit Ratio

77.4

78.8

77.4

75.9

74.5

74.5

CAR

12.6

12.3

12.1

11.9

11.3

10.9

- Tier I

9.3

9.4

9.3

9.3

9.0

8.8

Asset Quality (%)

Gross NPAs

2.9

4.3

5.3

6.6

8.5

8.4

Net NPAs

1.5

2.3

2.8

4.0

4.5

3.5

Slippages

2.7

2.9

3.4

5.3

4.9

3.7

Loan Loss Prov. /Avg. Assets

0.6

0.7

0.9

1.4

1.3

1.0

Provision Coverage

62.7

58.8

59.1

57.5

60.0

67.5

Per Share Data (`)

EPS

28.8

26.9

18.5

16.5

17.9

27.2

ABVPS (75% cover.)

146.7

160.4

168.7

168.9

179.6

218.0

DPS

22.0

27.0

10.0

17.3

17.0

25.5

Valuation Ratios

PER (x)

4.8

5.1

7.4

8.3

7.7

5.0

P/ABVPS (x)

0.9

0.9

0.8

0.8

0.8

0.6

Dividend Yield

16.0

19.7

7.3

12.6

12.4

18.6

DuPont Analysis

NII

3.2

3.2

3.1

2.9

2.7

2.7

(-) Prov. Exp.

0.9

0.9

1.3

1.4

1.3

1.1

Adj. NII

2.4

2.2

1.8

1.5

1.4

1.7

Treasury

0.1

0.1

0.1

0.2

0.2

0.2

Int. Sens. Inc.

2.4

2.3

1.9

1.6

1.6

1.9

Other Inc.

0.9

0.8

0.8

0.9

0.8

0.8

Op. Inc.

3.4

3.1

2.7

2.5

2.4

2.7

Opex

1.7

1.7

1.8

1.8

1.7

1.6

PBT

1.7

1.4

0.9

0.7

0.8

1.1

Taxes

0.5

0.4

0.3

0.2

0.2

0.3

RoA

1.2

1.0

0.6

0.5

0.5

0.7

Leverage

18.0

16.3

15.7

16.0

16.3

16.7

RoE

21.1

16.5

10.2

8.5

8.5

12.0

November 13, 2015

9

Punjab National Bank | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Punjab National Bank

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

November 13, 2015

10