2QFY2016 Result Update | Oil&Gas

October 26, 2015

Petronet LNG

ACCUMULATE

CMP

`193

Utilisation improves; Expansion on-track

Target Price

`210

Investment Period

12 Months

Standalone (` cr)

2QFY16

2QFY15

yoy%

1QFY16

qoq%

Net revenue

7,545

10,980

(31.3)

8,377

(9.9)

EBITDA

467

519

(10.1)

361

29.3

Stock Info

Margin (%)

6.2

4.7

146bp

4.3

188bp

Sector

Oil&Gas

Reported PAT

249

263

(5.3)

248

0.5

Market Cap (` cr)

14,456

Source: Company, Angel Research

Net Debt (` cr)

2,310

For 2QFY2016, Petronet LNG (PLNG)’s EBITDA came in ahead of our expectation

Beta

0.7

at `467cr, as against our estimate of `389cr, led by higher-than-expected

52 Week High / Low

222/160

contribution margin. The EBITDA declined 10% yoy but was up 29% sequentially.

Avg. Daily Volume

7,75,154

Contribution margin for the quarter came in at `37.4/MMBTU as against

Face Value (`)

10

`42.0/MMBTU in the corresponding quarter last year and vs `35.7/MMBTU in the

BSE Sensex

27,471

sequential previous quarter. The better-than-expected contribution was on

Nifty

8,295

account of higher utilization at the Dahej terminal, which operated at ~121% of

Reuters Code

PLNG.BO

its capacity (as against ~98% utilisation in the sequential previous quarter),

Bloomberg Code

PLNG IN

processing 154TBTU during the quarter. The Management indicated that the

increase in utilisation was temporary and should be ~100% going forward.

Shareholding Pattern (%)

Blended realisation was lower at

`481/MMBTU as against

`637/MMBTU

Promoters

50.0

in 1QFY2016 and `730/MMBTU in 2QFY2015, on account of lower spot

MF / Banks / Indian Fls

5.1

LNG prices.

FII / NRIs / OCBs

22.5

Expansion plan remains on track: Expansion of capacity of the Dahej terminal

Indian Public / Others

22.5

from 10MMTPA to 15MMTPA is going on as per schedule and the Management

expects to complete the same by 2016-end. The company has also initiated the

process for selection of EPC contractors for further expansion of the Dahej

Abs. (%)

3m 1yr

3yr

terminal’s capacity to 17.50 MMTPA.

Sensex

(3.2)

2.3

46.8

PLNG

(3.6)

(2.4)

17.3

Outlook and valuation: PLNG is a direct play on the gas deficit story in India. The

company’s strong expansion plan makes it well positioned to benefit from the

demand supply gap. The stock currently trades at 15x and 14x its FY2016E and

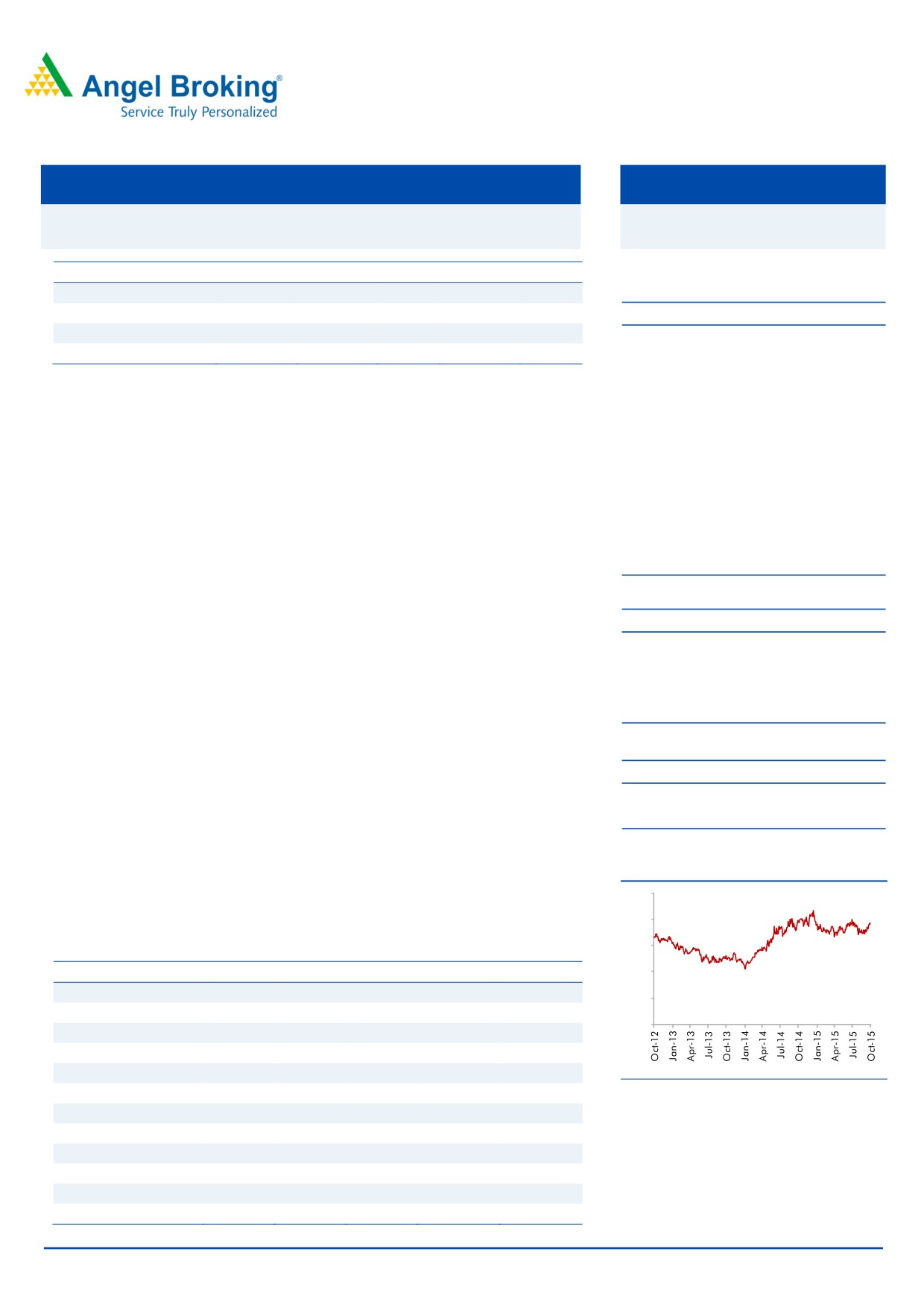

3-year price chart

250

FY2017E EPS. We use DCF to arrive at our target price of `210 and retain our

Accumulate rating on the stock.

200

150

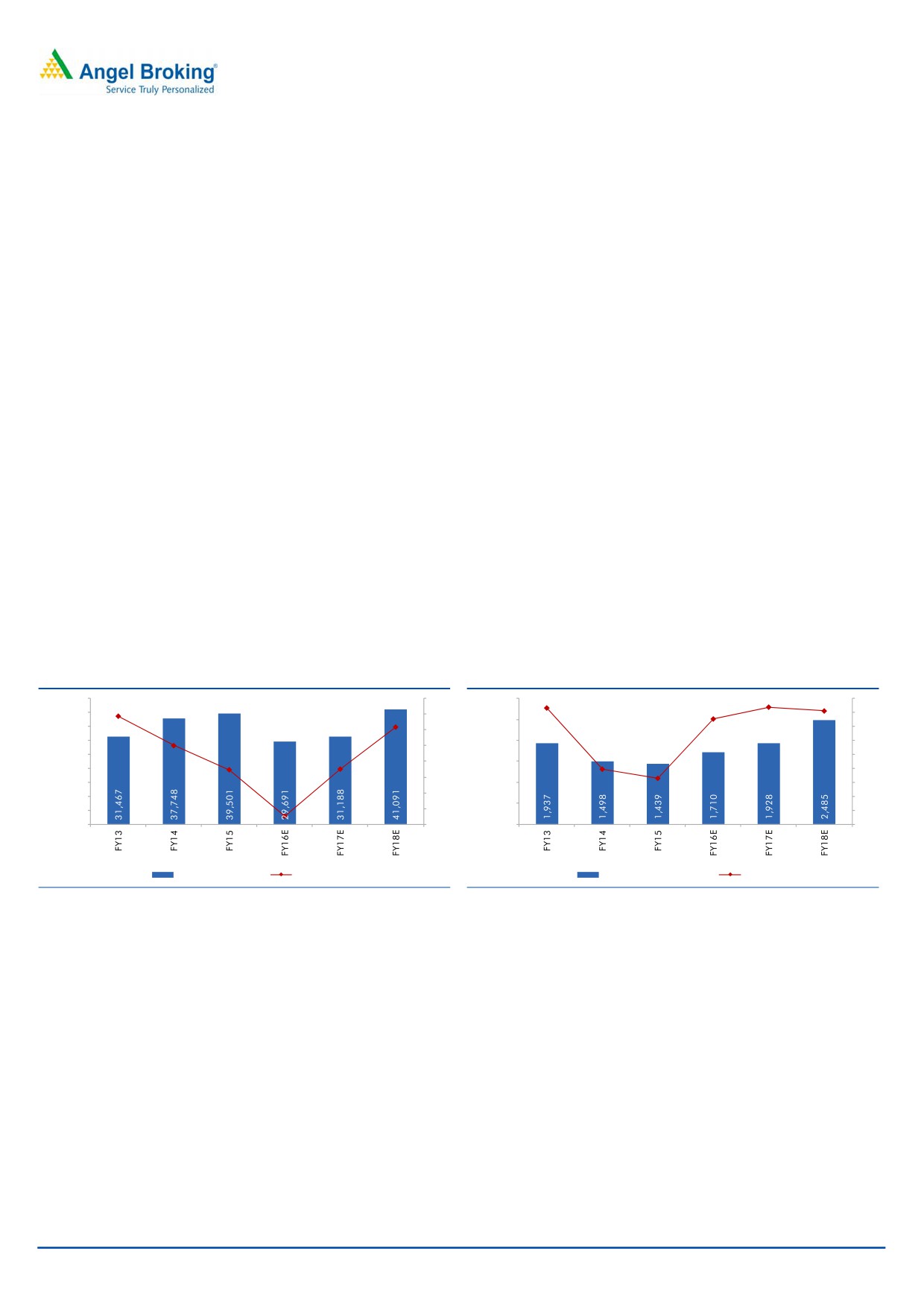

Key financials (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

100

Net sales

31,467

37,748

39,501

29,691

31,188

50

% chg

38.6

20.0

4.6

-24.8

5.0

0

Adj. net profit

1,149

712

883

959

1,007

% chg

8.7

(38.1)

24.0

8.6

5.0

Adj. EPS (`)

15.3

9.5

11.8

12.8

13.4

Source: Company, Angel Research

OPM (%)

6.2

4.0

3.6

5.8

6.2

P/E (x)

12.6

20.3

16.4

15.1

14.4

P/BV (x)

3.2

2.9

2.5

2.2

2.0

RoE (%)

28.8

15.1

16.5

15.8

14.8

RoCE (%)

24.5

15.1

13.5

15.7

15.8

Rahul Dholam

EV/Sales (x)

0.5

0.4

0.4

0.6

0.5

Tel: 022- 3935 7800 Ext: 6847

EV/EBIDTA

8.4

11.0

11.7

9.7

8.5

Source: Company, Angel Research: Note CMP as of October 23, 2015

Please refer to important disclosures at the end of this report

1

Petronet LNG | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance (Standalone)

(` cr)

2QFY16

2QFY15

yoy%

1QFY16

qoq%

FY2015

FY2014

yoy%

Net sales

7,545

10,980

(31.3)

8,377

(9.9)

39,501

37,748

4.6

Raw material

6,959

10,349

(32.8)

7,908

(12.0)

37,611

35,849

4.9

% of net sales

92.2

94.2

94.4

95.2

95.0

Gross Margin

586

631

(7.1)

469

25.0

1,890

1,898

(0.4)

Margin (%)

7.8

5.8

202bp

5.6

217bp

4.8

5.0

274bp

Employee Cost

14

11

30.6

15

(4.4)

57

47

22.5

% of net sales

0.2

0.1

0.2

0.1

0.1

Other expenditure

105

101

3.8

93

13.1

394

353

11.6

% of net sales

1.4

0.9

1.1

1.0

0.9

Total expenditure

7,078

10,461

(32.3)

8,016

(11.7)

38,062

36,249

5.0

% of net sales

93.8

95.3

95.7

96.4

96.0

EBITDA

467

519

(10.1)

361

29.3

1,439

1,498

(4.0)

Margin (%)

6.2

4.7

146bp

4.3

188bp

3.6

4.0

222bp

Interest

61

80

(23.5)

61

(0.0)

293

220

33.7

Depreciation

81

77

4.5

80

0.9

315

308

2.4

Other income

36

35

2.7

33

8.0

155

84

84.8

Exceptional items

0

0

0

0

0

Profit before tax

361

397

(9.1)

253

42.6

985

1,055

(70.1)

% of net sales

4.8

3.6

3.0

2.5

2.8

Tax

112

134

6

102

343

(70.1)

% of PBT

31.0

33.8

2.2

10.4

32.5

Adj. PAT

249

263

(5.3)

248

0.5

883

712

24.0

Source: Company, Angel Research

Result highlights

Better than expected volumes led by higher utilisation

PLNG reported a healthy contribution margin of `586cr, well ahead

of our

expectation, led by higher volumes at the Dahej terminal. Contribution margin

declined 7% yoy, but increased 25% on a sequential basis. Contribution margin

came in at `37.4/MMBTU as against `42.0/MMBTU in the corresponding quarter

last year and vs `35.7/MMBTU in the sequential previous quarter.

During the quarter, the Dahej terminal operated at ~121% of its capacity,

processing 154TBTU, as against ~98% utilisation in the sequential previous

quarter. The Management indicated that the increase in utilisation was temporary

and should be at ~100%, going forward. Volumes continued to remain low at the

Kochi terminal at 2.7TBTU (no reload sales) as against 6.11TBTU in 1QFY2016.

Total volumes at 156.7TBTU were well ahead of our expectation, increasing 23%

over the sequential previous quarter (127.9TBTU). Blended realisation was lower at

`481/MMBTU as against `637/MMBTU in 1QFY2016 and `730/MMBTU in

2QFY2015, on account of lower spot LNG prices.

October 26, 2015

2

Petronet LNG | 2QFY2016 Result Update

Exhibit 2: Strong volume growth

Exhibit 3: Revenue declines due to lower realisation

180

12,000

30

151

157

160

139

141

130

132

10,000

20

123

124

140

117

10

120

103

8,000

0

100

6,000

80

-10

60

4,000

-20

40

2,000

-30

20

0

0

-40

Regasification Volumes

Reload Volumes

Revenue (` cr)

yoy change (%)

Source: Company, Angel Research

Source: Company, Angel Research

The EBITDA for the quarter came in ahead of our expectation at `467cr, as against

our estimate of `389cr, led by higher-than-expected contribution margin. EBITDA

declined 10% yoy but was up 29% sequentially. Depreciation and finance expenses

were in line with our expectations. The Net profit declined 5% yoy to `249cr, but

remained flat on a sequential basis on account of tax reversals in 1QFY2015

pertaining to prior years under Section 80-IA of the Income Tax Act.

Exhibit 4: Quarterly Performance Trend

1QFY14

2QFY14

3QFY14

4QFY14

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Blended Realisation (`/MMBTU)

652

772

759

890

733

730

792

699

637

481

EBITDA (`/MMBTU)

31

30

28

33

26

34

24

22

27

30

Source: Company, Angel Research

Exhibit 5: 2QFY2016 Actual vs. Angel estimates

(` cr)

Actual

Estimates

Variation (%)

Net sales

7,545

7,866

(4.1)

EBITDA

467

389.2

19.9

EBITDA margin (%)

6.2

4.9

50bp

Source: Company, Angel Research

Exhibit 6: High Contribution margin

Exhibit 7: EBITDA margin improves ~150bp yoy

700

42.1

42.0

45

600

6.2

6.5

37.1

37.3

37.6

37.4

35.7

40

6.0

600

33.3

33.3

31.8

500

35

5.5

500

4.7

4.7

30

400

5.0

4.3

400

25

4.5

300

3.8

3.7

3.7

20

3.5

4.0

300

15

200

3.0

3.1

3.5

200

10

3.0

100

100

5

2.5

-

0

-

2.0

Contribution Margin (` cr)

(`/MMBTU)

EBITDA (` cr)

Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

October 26, 2015

3

Petronet LNG | 2QFY2016 Result Update

Conference Call Highlights

PLNG’s off-take volume from Ras Gas for 9MCY2015 stood at 68% of the

contracted long term volume as the current spot LNG price is significantly

lower than the contracted price. The Management remains positive with

regards to its negotiations with Ras Gas and expects to review the take-or-pay

contract by the year-end. The Management believes that there would be no

risk to the company on account of this take-or-pay contract, as off-takers will

have to pay for any volume shortfall.

Expansion of the Dahej terminal from 10MMTPA to 15MMTPA is going on as

per schedule and the Management expects to complete the capacity expansion

by 2016- end. The company has also initiated the process for selection of EPC

contractors for further expansion of the Dahej terminal’s capacity to

17.50MMTPA.

The Kochi terminal reported an EBITDA loss in the absence of reloading

revenue during the quarter.

Gorgon volumes are to start from mid CY2016 and will be processed at the

Kochi terminal, if the pipelines are ready. In case they are not, then the Dahej

terminal will get utilized.

PLNG once again reiterated that it is not giving any concessions to power

plants and its regas tariffs are based entirely on commercial considerations.

Exhibit 8: Revenue Growth to pick up going forward

Exhibit 9: Higher volumes to drive EBITDA margin

45,000

50

3,000

6.2

6.2

6.0

6.5

5.8

40,000

40

6.0

2,500

35,000

5.5

30

30,000

2,000

5.0

20

25,000

4.0

4.5

10

1,500

20,000

3.6

4.0

0

15,000

1,000

3.5

10,000

-10

3.0

500

5,000

-20

2.5

0

-30

0

2.0

Revenue (` cr)

yoy change (%)

EBITDA (` cr)

Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

October 26, 2015

4

Petronet LNG | 2QFY2016 Result Update

Investment arguments

Huge demand for gas at lower prices

The demand-supply gap for LNG is expected to increase from ~180mmscmd in

FY2015 to ~285mmscmd by FY2020. If crude prices remain at low levels, this gap

will increase even further. PLNG currently operates ~60% of the country’s LNG

import capacity and is expected to remain the leader over the next five years led by

its expansion at Dahej, which will position it well to benefit from the massive

demand for gas.

Capacity expansion remains on track

PLNG remains on track to expand the Dahej terminal capacity from 10MMTPA to

15MMTPA by the end of CY2016. A major portion of the expansion work is

complete and almost the entire capacity post expansion is already booked, which

would ensure a quick ramp-up in volumes, post commissioning.

High probability of RasGas contract being negotiated

Off-take volumes from RasGas have declined sharply as the LNG pricing formula

will need a long time to reflect the current spot prices (contract price linked to 60M

average oil price) in a low oil price scenario. The Management has clarified that

while the ‘take-or-pay’ provisions would apply, off-takers will have the option to

pay upfront and defer the off-take till the pricing formula reflects the lower prices.

RasGas may then have to refund the excess amount paid by the off-takers.

Deferment of off-take would not be in the interest of either parties and we believe

that RasGas’s Management will take a practical view of this situation and ensure

that the contract is renegotiated.

October 26, 2015

5

Petronet LNG | 2QFY2016 Result Update

Outlook and valuation

PLNG is a direct play on the gas deficit story in India. The company’s strong

expansion plan makes it well positioned to benefit from the demand-supply gap.

However, near term concerns such as declining off-take volumes from RasGas and

delays in the Kochi - Bangalore pipeline, which is critical for the ramp up at the

Kochi terminal, weigh on the stock. The stock currently trades at 15.1x and 14.5x

its FY2016E and FY2017E EPS.

We use DCF to arrive at our target price of `210 and retain our Accumulate rating

on the stock.

Exhibit 10: DCF valuation

(` cr)

WACC

11.5%

PV of forecast period FCF (till FY25)

8,495

Terminal Growth

2.5%

PV of Terminal Value

9,436

Enterprise Value

17,930

Less: Net Debt (FY16E)

2,216

Equity Value

15,715

Shares (cr)

75

Target Price

210

Source: Angel Research

Company background

Formed as a joint venture by the Government of India to import LNG and set up

LNG terminals in the country, PLNG was promoted by GAIL (India) Ltd (GAIL), Oil

& Natural Gas Corporation Limited (ONGC), Indian Oil Corporation Limited

(IOCL) and Bharat Petroleum Corporation Limited (BPCL). PLNG has set up India’s

first LNG receiving and regasification terminal at Dahej, Gujarat, and another

terminal at Kochi, Kerala. While the Dahej terminal has a nominal capacity of

10MMTPA [equivalent to 40mmscmd of natural gas], the Kochi terminal has a

capacity of 5MMTPA [equivalent to 20mmscmd of natural gas]. The company is in

the process to build a third terminal at Gangavaram, Andhra Pradesh.

October 26, 2015

6

Petronet LNG | 2QFY2016 Result Update

Profit & Loss Statement (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

Net Sales

31,297

37,545

39,093

28,900

30,357

Other operating income

170

203

408

791

830

Total operating income

31,467

37,748

39,501

29,691

31,188

% chg

38.6

20.0

4.6

(24.8)

5.0

Total Expenditure

29,531

36,249

38,062

27,981

29,259

Net Raw Materials

29,212

35,849

37,611

27,565

28,822

Other Mfg costs

282

353

394

354

372

Personnel

37

47

57

62

65

Other

-

-

-

-

-

EBITDA

1,937

1,498

1,439

1,710

1,928

% chg

5.9

(22.6)

(4.0)

18.9

12.7

(% of Net Sales)

6.2

4.0

3.6

5.8

6.2

Depreciation& Amortisation

187

308

315

322

394

EBIT

1,750

1,190

1,124

1,388

1,534

% chg

6.4

(32.0)

(5.6)

23.5

10.5

(% of Net Sales)

5.6

3.2

2.8

4.7

4.9

Interest & other Charges

118

220

293

245

244

Other Income

89

84

155

141

148

Share in profit of Associates

-

-

-

-

-

Recurring PBT

1,720

1,055

985

1,285

1,438

% chg

10.8

(38.7)

(6.6)

30.4

12.0

Extraordinary Inc/(Expense)

-

-

-

-

-

PBT (reported)

1,720

1,055

985

1,285

1,438

Tax

571

343

102

326

432

(% of PBT)

33.2

32.5

10.4

25.4

30.0

PAT (reported)

1,149

712

883

959

1,007

% chg

8.7

(38.1)

24.0

8.6

5.0

(% of Net Sales)

3.7

1.9

2.2

3.2

3.2

Basic EPS (`)

15.3

9.5

11.8

12.8

13.4

% chg

8.7

(38.1)

24.0

8.6

5.0

October 26, 2015

7

Petronet LNG | 2QFY2016 Result Update

Balance Sheet (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

750

750

750

750

750

Reserves & Surplus

3,700

4,236

4,939

5,678

6,465

Shareholders Funds

4,450

4,986

5,689

6,428

7,215

Total Loans

3,034

3,267

2,674

2,941

2,794

Deferred Tax Liability

391

553

727

922

1,181

Other Long term liabilities

3

304

604

604

604

Total Liabilities

7,878

9,110

9,694

10,896

11,795

APPLICATION OF FUNDS

Gross Block

3,580

7,795

7,954

8,114

11,584

Less: Acc. Depreciation

1,222

1,530

1,845

2,167

2,562

Net Block

2,358

6,265

6,110

5,946

9,023

Capital Work-in-Progress

4,331

880

1,580

2,671

250

Goodwill

0

0

0

0

0

Investments

140

140

90

90

90

Current Assets

4,137

4,376

2,665

2,654

2,998

Cash

1,269

1,233

364

725

844

Loans & Advances

1,037

956

883

691

726

Other

1,832

2,187

1,419

1,237

1,428

Current liabilities

3,205

2,803

1,425

1,139

1,239

Net Current Assets

933

1,573

1,240

1,515

1,759

Other Assets

117.3

252.0

673.9

673.9

673.9

Total Assets

7,878

9,110

9,694

10,896

11,795

October 26, 2015

8

Petronet LNG | 2QFY2016 Result Update

Cash flow statement (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

Profit before tax

1,720

1,055

985

1,285

1,438

Depreciation

187

308

315

322

394

Change in Working Capital

404

(353)

(536)

87

(125)

Others

51

146

48

0

0

Direct taxes paid

(539)

(193)

(102)

(130)

(173)

Cash Flow from Operations

1,823

964

710

1,563

1,535

(Inc.)/ Dec. in Fixed Assets

(841)

(876)

(860)

(1,250)

(1,050)

(Inc.)/ Dec. in Investments

-

11.6

49.9

-

-

Share of profit/ (loss) from asso.

72

62

0

0

0

Cash Flow from Investing

(769)

(803)

(810)

(1,250)

(1,050)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

(242)

205

(593)

267

(147)

Dividend Paid (Incl. Tax)

(218)

(219)

(176)

(219)

(219)

Others

(310)

(182)

-

-

-

Cash Flow from Financing

(770)

(197)

(769)

48

(367)

Inc./(Dec.) in Cash

285

(36)

(869)

361

119

Opening Cash balances

984

1,269

1,233

364

725

Closing Cash balances

1,269

1,233

364

725

844

October 26, 2015

9

Petronet LNG | 2QFY2016 Result Update

Key ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

Per Share Data (`)

Reported EPS

15.3

9.5

11.8

12.8

13.4

Cash EPS

17.8

13.6

16.0

17.1

18.7

DPS

2.5

2.0

2.5

2.5

2.5

Book Value

59.3

66.5

75.8

85.7

96.2

Valuation Ratio (x)

P/E (on FDEPS)

12.6

20.3

16.4

15.1

14.4

P/CEPS

10.8

14.2

12.1

11.3

10.3

P/BV

3.2

2.9

2.5

2.2

2.0

Dividend yield (%)

1.3

1.0

1.3

1.3

1.3

EV/Sales

0.5

0.4

0.4

0.6

0.5

EV/EBITDA

8.4

11.0

11.7

9.7

8.5

EV/Total Assets

2.1

1.8

1.7

1.5

1.4

Returns (%)

ROCE

24.5

15.1

13.5

15.7

15.8

ROE

28.8

15.1

16.5

15.8

14.8

Turnover ratios (x)

Asset Turnover (Gross Block)

8.8

6.6

5.0

3.7

3.2

Inventory (days)

10.1

9.6

8.5

9.7

8.3

Receivables (days)

17.3

17.9

15.5

15.5

14.9

Payables (days)

27.8

26.6

17.4

13.5

11.8

WC cycle (ex-cash) (days)

11.5

12.1

13.0

16.9

19.2

Solvency ratios (x)

Net debt to equity

0.4

0.4

0.4

0.3

0.3

Net debt to EBITDA

0.6

0.6

0.9

0.8

0.7

Interest Coverage (EBIT / Int.)

14.8

5.4

3.8

5.7

6.3

October 26, 2015

10

Petronet LNG | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Petronet LNG

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

October 26, 2015

11