2QFY2016 Result Update | Infrastructure

November 9, 2015

PNC Infratech

ACCUMULATE

CMP

`522

Performance Highlights

Target Price

`558

Quarterly highlights - Standalone

Investment Period

12 Months

Y/E March (` cr)

2QFY16 1QFY16

% chg (qoq) 2QFY15

% chg (yoy)

Net sales

463

426

8.5

319

45.1

Stock Info

EBITDA

54

52

3.8

39

38.7

Sector

Infrastructure

Reported PAT

30

26

16.6

21

43.4

Market Cap (` cr)

2,681

Source: Company, Angel Research

Net debt (` cr)

303

Beta

1.3

PNC Infratech (PNC) reported a top-line and bottom-line growth of 45.1% and

52 Week High / Low

538/346

43.4% yoy, respectively, for 2QFY2016. Top-line growth was driven by strong

Avg. Daily Volume

10,653

execution across Agra-Firozabad and other road projects. Higher dependency on

Face Value (`)

10

sub-contracting led PNC to report 50bp yoy decline in its EBITDA margin to

11.7%, for the quarter. A 38.7% yoy EBITDA growth coupled with 55.3% decline

BSE Sensex

26,565

in interest expenses led the PAT to grow by 43.4% yoy. PAT margin, at 6.6% for

Nifty

7,954

the quarter, was marginally down on a yoy basis.

Reuters Code

PNCI.BO

Bloomberg Code

PNCL@IN

PNC’s unexecuted order book as of 2QFY2016 stands at `3,578cr (order book

to LTM sales ratio stands at 2.1x).

One more BOT is expected to commence operation in FY2016 in addition to 3

Shareholding Pattern (%)

already started in YTDFY2016. Management has indicated that it does not intend

Promoters

56.1

to add any new BOT projects in FY2016 unless a lucrative project in north India

MF / Banks / Indian Fls

13.8

comes up within the ticket size of `500cr. As a result, we are of the view that

FII / NRIs / OCBs

6.4

PNC’s consolidated D/E ratio would peak out in FY2017E.

Indian Public / Others

23.7

Outlook and Valuation: Considering the strong uptick in roads and highways

EPC award activity especially in North India, where PNC has more comfort, and

Abs. (%)

3m 1yr 3yr

given its past track record and recent wins, we expect the standalone entity to

Sensex

(7.0)

(5.8)

39.0

report 21.1% and 28.5% top-line and bottom-line CAGR, respectively, over

PNC Infratech

11.2

NA NA

FY2015-2017E. This, coupled with the likelihood of 1 BOT project commencing

*NA as PNC listed on May 26, 2015

operation in FY2016E, leads us to estimate that the consolidated Balance Sheet

should peak from FY2017E onwards, which is comforting. Using SoTP based

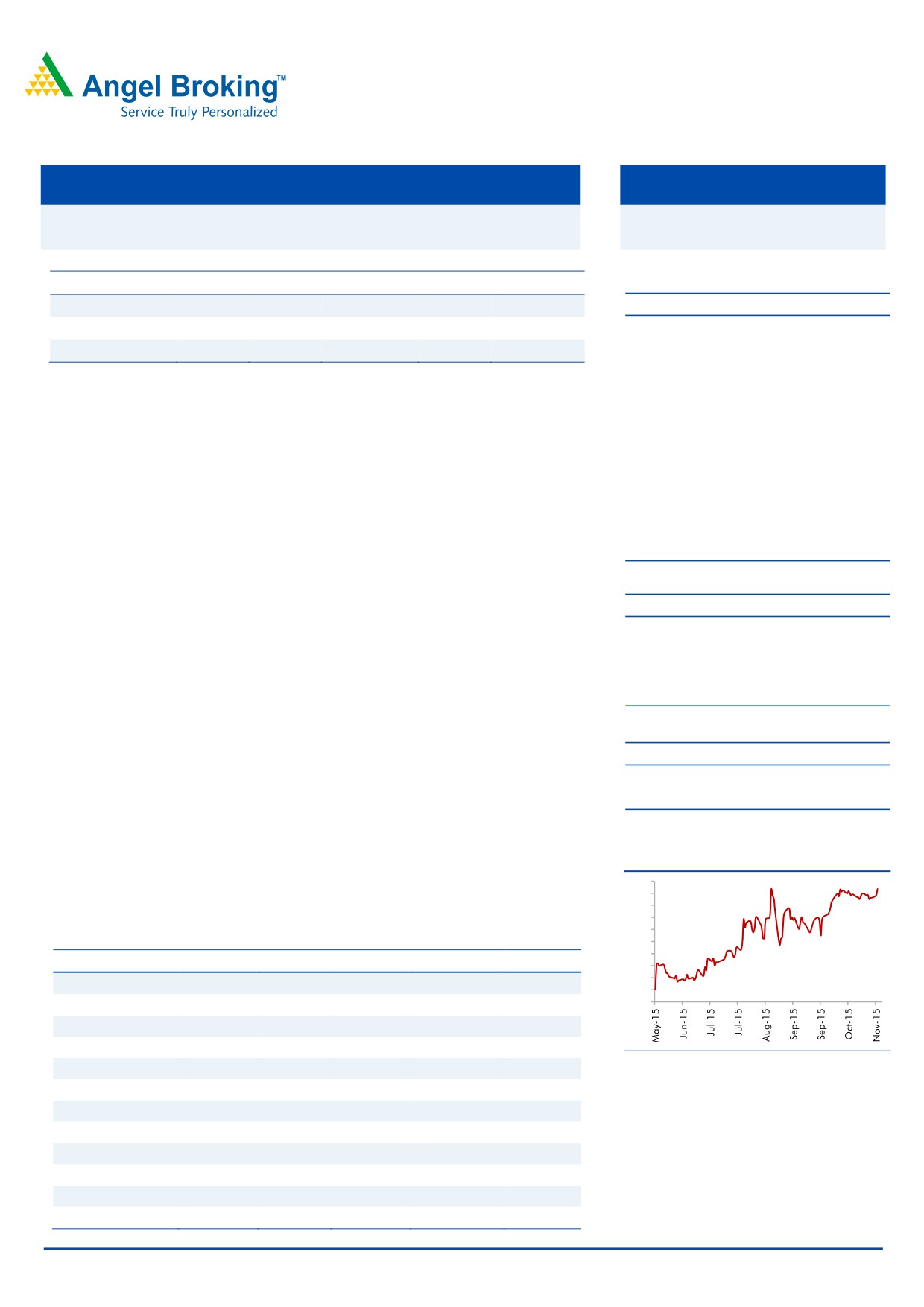

3-Year Daily Price Chart

valuation methodology we arrive at a FY2017E based price target of `558.

540

Given the 7% upside in the stock form the current levels, we maintain our

520

500

Accumulate rating on the stock.

480

460

Key financials (Standalone)

440

420

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

400

380

Net Sales

1,303

1,145

1,561

1,873

2,288

360

340

% chg

2.3

(12.1)

36.3

20.0

22.2

Net Profit

76

67

100

121

166

% chg

(3.3)

(12.6)

50.2

20.2

37.5

Source: Company, Angel Research

EBITDA (%)

11.9

12.2

13.9

13.2

13.5

EPS (`)

19

17

25

24

32

P/E (x)

27.2

31.1

20.7

22.2

16.2

P/BV (x)

3.7

3.3

2.9

2.1

1.9

RoE (%)

14.4

11.2

14.9

12.1

12.3

RoCE (%)

17.7

15.0

20.2

17.3

17.6

Yellapu Santosh

EV/Sales (x)

1.7

1.9

1.5

1.5

1.3

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

14.6

15.9

11.0

11.6

9.4

Source: Company, Angel Research; Note: CMP as of November 6, 2015

Please refer to important disclosures at the end of this report

1

PNC Infratech | 2QFY2016 Result Update

Exhibit 1: Quarterly Standalone Performance

Particulars (` cr)

2QFY16

1QFY16

% chg (qoq) 2QFY15

% chg (yoy) 1HFY16 1HFY15

% chg (yoy)

Net Sales

463

426

8.5

319

45.1

889

690

(53.8)

Total Expenditure

408

374

9.1

280

46.0

783

611

(54.2)

Cost of materials consumed

351

302

16.2

248

41.3

652

549

(54.8)

Changes in Inv. Of FG & WIP

(2)

15

nmf

(24)

nmf

12

(32)

nmf

Employee Benefits Expense

21

19

10.7

15

37.0

40

30

(48.9)

Other Expenses

39

39

0.7

40

(3.0)

78

64

(36.8)

EBITDA

54

52

3.8

39

38.7

106

79

(50.7)

EBIDTA %

11.7

12.2

12.2

12.0

11.5

Depreciation

12

12

5.9

10

20.5

24

17

(38.4)

EBIT

42

40

3.2

29

45.3

82

62

(54.0)

Interest and Financial Charges

6

10

(42.5)

13

(55.3)

16

21

(35.8)

Other Income

10

10

4.2

15

(32.0)

20

23

(35.1)

PBT before Exceptional Items

46

40

15.3

30

50.8

86

65

(53.0)

Exceptional Items

0

0

0

0

0

PBT after Exceptional Items

46

40

15.3

30

50.8

86

65

(53.0)

Tax

16

14

12.8

9

67.7

29

21

(55.8)

% of PBT

33.8

34.5

30.4

34.1

32.3

PAT

30

26

16.6

21

43.4

57

44

(51.7)

PAT %

6.6

6.1

6.7

6.4

6.4

Dil. EPS (after extra-ord. Items)

5.93

5.79

2.4

5.33

11.3

11.72

11.04

(51.7)

Source: Company, Angel Research

Standalone Business Review

Strong execution seen during the quarter

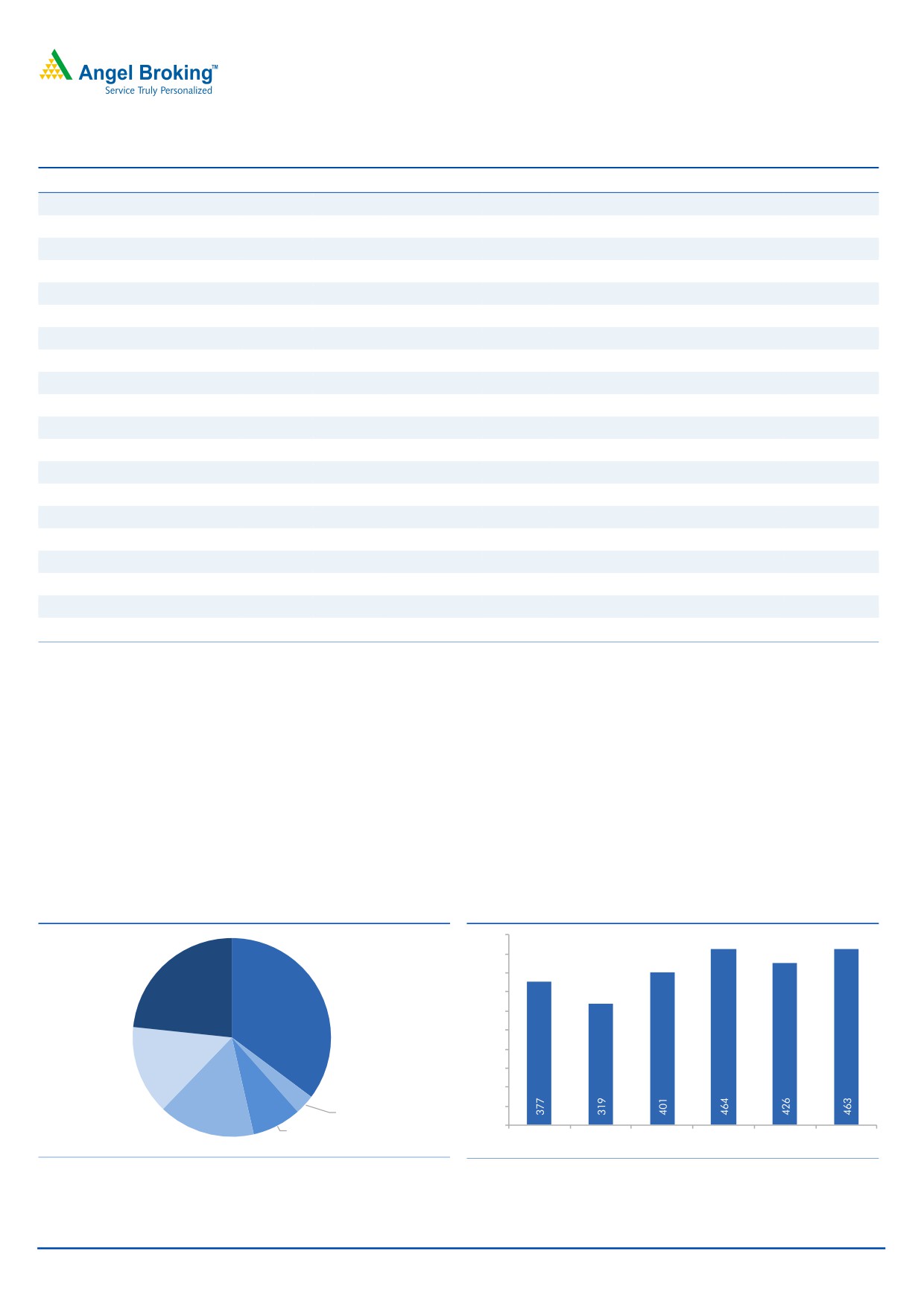

PNC witnessed strong execution during 2QFY2016. The company reported a top-

line growth of 45.1% yoy to `463cr (ahead of our estimate of `378cr). 69.8% of

the 2QFY2016 revenues were booked from external road EPC projects, inclusive of

Agra-Firozabad (35.2%), Sonauli-Gorakhpur (3.2%) and Barabanki-Jarwal (8.0%)

projects. EPC works from captive BOT projects (1) Bareilly-Almora (14.5%) and

(2) Rae-Bareli-Jaunpur (15.8%), also contributed to the quarter’s top-line numbers.

Exhibit 2: 2QFY2016 Revenue-Mix (in %)

Exhibit 3: Quarterly Revenue performance

500

450

400

350

Other Projects,

Agra-

23.3

Firozabad,

300

35.2

250

Bareily-

200

Almora, 14.5

150

100

Raibareli-

Sonauli-

Jaunpur, 15.8

Gorakhpur,

50

Barabanki-

3.2

0

Jarwal, 8.0

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Source: Company, Angel Research

Source: Company, Angel Research

November 9, 2015

2

PNC Infratech | 2QFY2016 Result Update

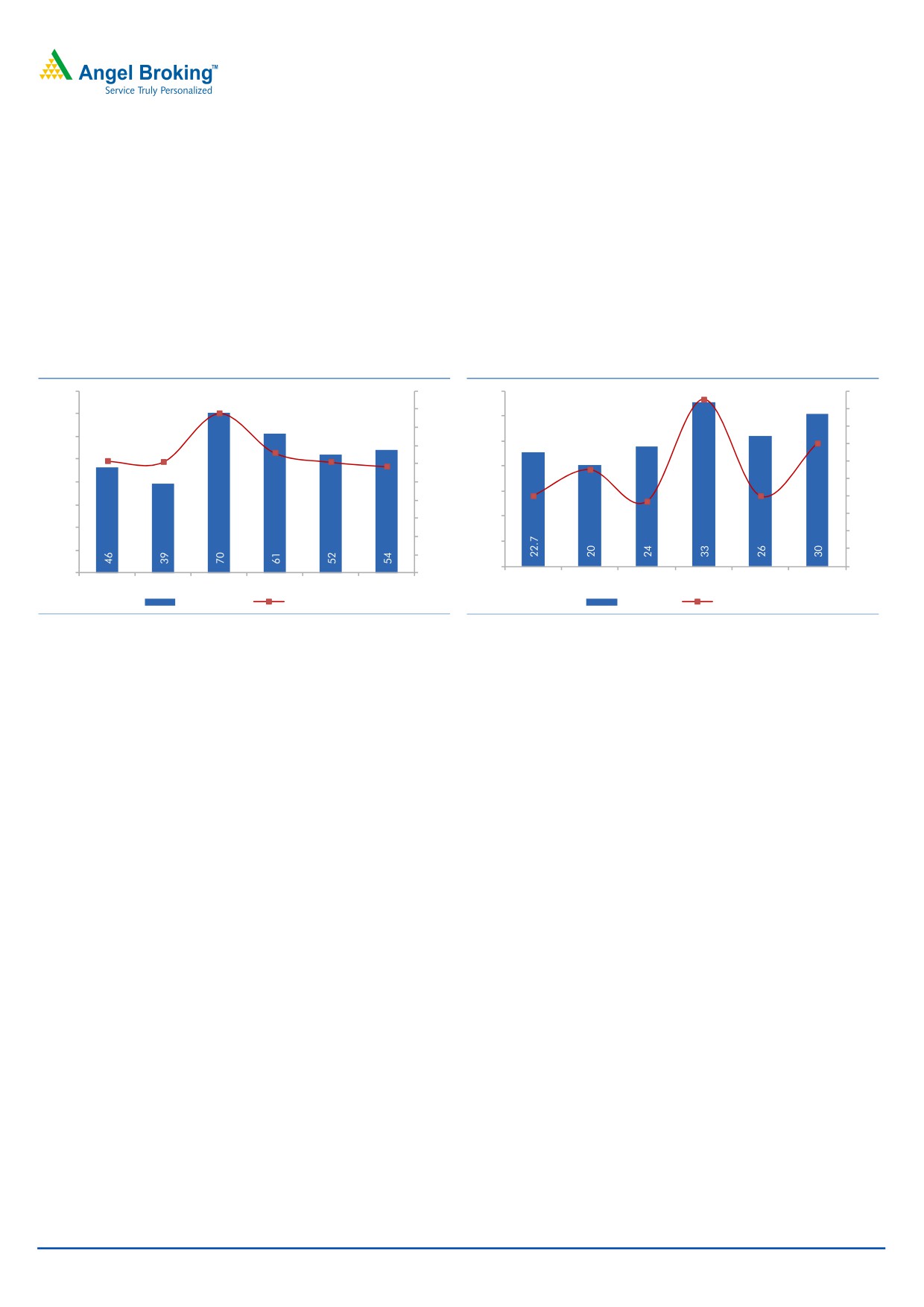

EBITDA margin declines during the quarter

On the operating front, PNC reported an EBITDA of `54cr, ahead of our estimate

of `47cr. Reported EBITDA margin of the company was at 11.7%, lower than the

year ago and sequential previous quarter’s EBITDA margin of 12.2%. Decline in

EBITDA margin on a yoy basis is on account of (1) 37.0% yoy increase in employee

expenses to `21cr, and (2) 41.3% increase in raw material expenses to `351cr.

The decline in yoy EBITDA margin is attributable to higher sub-contracting

expenses, as well.

Exhibit 4: EBITDA margin declines to 11.7%

Exhibit 5: PAT Margin flat at 6.1% for the quarter

80

17.5

20

35

7.1

7.2

18

7.0

70

30

16

6.6

6.8

13.2

60

12.2

12.3

12.2

14

25

6.6

11.7

6.3

50

6.4

12

20

6.0

5.9

6.2

40

10

6.0

15

8

6.0

30

6

10

5.8

20

5.6

4

5

10

5.4

2

0

5.2

0

0

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

EBITDA (` cr)

EBITDA Margins (%)

PAT (` cr)

PAT Margins (%)

Source: Company, Angel Research

Source: Company, Angel Research

PAT margin declines a bit on a yoy basis

PNC reported a PAT of `30cr, ahead of our expectations of `23cr. Reported PAT

margin of the company was at 6.6% during the quarter, marginally lower than

6.7% in the corresponding quarter a year ago and vs 6.1% in the sequential

previous quarter. PAT margin on a yoy basis was impacted due to (1) 20.5%

increase in depreciation expenses to `12cr (reflecting impact of new equipment

purchases), and (2) 55.3% decline in interest expenses to `6cr (on the back of

decline in yoy debt to `211cr).

November 9, 2015

3

PNC Infratech | 2QFY2016 Result Update

Order Inflows continue to grow…

In FY2015, PNC reported net order inflow of `1,618cr (55.5km stretch connecting

Agra-Firozabad Green Expressway project). In YTDFY2016, PNC has either won/is

L1 for projects worth `1,743cr.

2 projects are currently at L1 stage - (1) resurfacing/ strengthening of Runway at

Air Force Station, Kanpur (worth `167cr), and (2) Aligarh-Moradabad EPC project

(worth `645cr).

Exhibit 6: YTD Order Inflows stand at `1,743cr

Exhibit 7: Order Book gives strong revenue visibility

3,500

6,000

0.31x

0.3x

0.3x

0.31x

3,000

5,000

0.31x

2,500

4,000

0.31x

2,000

0.30x

3,000

1,500

0.3x

0.30x

2,000

0.30x

1,000

0.30x

1,000

500

0.30x

0

0

0.29x

FY2015

YTDFY2016

FY2016E

FY2017E

FY15

FY16E

FY17E

OI (` cr)

OB (` cr)

Execution Rate (x)

Source: Company, Angel Research

Source: Company, Angel Research

Management expects the company to benefit from an uptick in NHAI & MoRTH’s

award activity and has maintained its order inflow guidance of ~`2,500cr-3,000cr

for FY2016E. The guidance is backed by strong bid pipeline emerging from NHAI

& MoRTH side (projects to be awarded are from Uttar Pradesh., Punjab, Madhya

Pradesh, Chattisgarh).

PNC’s unexecuted order book (inc. L1 order wins) as of 2QFY2016 stands at

`3,578cr (order book to LTM ratio stands at 2.1x). The Roads & Highways vertical

continues to dominate the order book mix.

Exhibit 8: Top 5-projects as % of total Order Book

Exhibit 9: Details of Top-5 projects being executed

O/s Total Project

Project details

Value (` cr)

Agra-Firozabad

1,408

17%

Bhojpur-Buxar

477

Koilwar-Bhojpur

454

83%

Sonauli-Gorakhpur

408

Barabanki-Jarwal

218

Top 5-projects

2,965

Top 5 projects

Other Projects

Source: Company, Angel Research

Source: Company, Angel Research

November 9, 2015

4

PNC Infratech | 2QFY2016 Result Update

Update on BOT projects

PNC currently has 8 BOT/OMT assets which are at different stages of execution.

Of these, 1 is a BOT-Annuity project, 1 is an industrial estate maintenance project

(BOT-Annuity + Fee model), 1 is an OMT project, and the remaining 5 are BOT-

Toll projects. Notably, all 8 BOT projects are Uttar Pradesh (UP) or Central/North

India based. 5 of these BOT projects have been won on Viability Gap Funding

(VGF) basis, amidst competition. The Management highlighted that equity IRRs for

these BOT projects are in the range of 16-18%.

Currently 6 of the 7 BOT projects are operational and the remaining 1 (Rae Bareli-

Jaunpur BOT projects) is likely to be operational by December-2015 (ahead of its

scheduled CoD of June-2016). On such early completion, the company claims that

it would be eligible for single annuity (worth `64.3cr) as bonus amount.

Exhibit 10: BOT Projects Status (at 2QFY2016-end)

PNC

Length

PNC Equity

BOT projects

Proj. Type

Status

TPC

Stake (%)

(kms)

Invested to-date

Ghaziabad-Aligarh

Toll

35%

Operational

125

2,000

68

Kanpur-Kabrai

Toll

100%

Operational

123

458

68

Gwalior-Bhind

Toll

100%

Operational

108

340

78

Bareilly-Almora

Toll

100%

Operational

54

604

75

Jaora-Nayagaon

Toll

9%

Operational

128

907

24

Rae Bareli-Jaunpur

Annuity

100%

Under Const.

166

837

140

Narela Industrial Estate

Annuity + Fee

100%

Operational

NA

175

35

OMT projects

Kanpur-Ayodhya

Toll

100%

Operational

217

0

0

Source: Company, Angel Research

With `65cr (from the IPO proceeds) having been infused by PNC towards the

Raebareli-Jaunpur BOT project, it now does not have any more equity

commitments pending towards the BOT projects.

Kanpur-Kabrai BOT project witnessed ~11.4% yoy increase in its per-day toll

collections for the quarter at `59.09lakh/day.

Kanpur-Ayodhya OMT project during 2QFY2016 collected `54cr of gross toll

income, which in our estimate is an 8% yoy increase.

For Ghaziabad-Aligarh BOT project, the company reported a sequential decline in

toll income from ~`36lakh/day (`32.4cr for the quarter) to ~`40lakh/day (`36cr

for the quarter) in 2QFY2016. The Management expects tolling from this BOT to

catch-up in the next 3-6 months, (1) once the entire road stretch gets operational

(currently does only partial tolling; tolling could potentially increase by `17lakh/

day), and (2) on implementation of over-loading charges (tolling could potentially

increase by `7lakh/ day).

November 9, 2015

5

PNC Infratech | 2QFY2016 Result Update

Risks & Concerns

Delay in order wins could pose as a risk to our estimates.

Roads & Highways account for a substantial chunk of the order book.

Slowdown in orders from NHAI

/ State governments could affect the

company’s order inflow adversely.

PNC's order book comes majorly from North India. Any slowdown in orders

from this region may impact our order inflow assumption for the company.

November 9, 2015

6

PNC Infratech | 2QFY2016 Result Update

Outlook & Valuation

Considering strong execution trends exhibited by PNC, uptick in the NHAI and

MoRTH awarding momentum, when coupled with recent NHAI announcements,

we expect further uptick in the execution from here-on. Accordingly, we revise

upwards our revenue estimates for FY2016/FY2017E to

`1,873/2,288cr,

respectively (revenue CAGR of 21.1% over FY2015-17E). We maintain our EBITDA

margin assumption for FY2016 and FY2017 at 13.2% and 13.5%, respectively. In

addition to EBITDA growth, on fine-tuning our estimates, we expect PNC

(standalone entity) to report 28.5% PAT CAGR during FY2015-17E to `166cr.

Exhibit 11: Earnings Revision

FY2016E

FY2017E

Y/E March (` cr)

Old

New Change (%)

Old

New Change (%)

Net Sales

1,798

1,873

4.2

2,132

2,288

7.3

EBITDA

237

247

4.2

288

309

7.3

EBITDA Margins (%)

13.2

13.2

13.5

13.5

PAT

114

121

6.1

153

166

8.5

PAT Margins (%)

6.3

6.4

7.2

7.2

Source: Angel Research

We have valued PNC using the Sum-Of-The-Parts method. The company’s EPC

business (under standalone entity) has been valued using FY2017E P/E multiple,

whereas BOT projects are valued using the Book Value/ Free Cash flow to Equity

holders method.

Value of Core EPC business

Considering the growth prospects of the EPC segment (given the expected uptick in

Roads and Highways award activity environment), we have valued PNC’s core EPC

business (standalone entity) on P/E of 14.0x its revised FY2017E EPS of `32,

resulting in a value of `452 per share.

November 9, 2015

7

PNC Infratech | 2QFY2016 Result Update

Exhibit 12: Sum-of-the-Parts based Valuation Table

FY17E Std. PAT

Target

Target Value

Value/ share

% of

Particulars

Segment

Basis

(` cr)

Multiple

(` cr)

(`)

SoTP

PNC's EPC business

Construction

166

14.0

2,321

452

81 P/E of 14x

Total

2,321

452

81

Adj. Equity

Equity Invested/

Project

Invested/ Disc.

Value/ share

% of

Particulars

Proj. Type

Disc. FCFE

Basis

Stake

FCFE

(`)

SoTP

(` cr)

(` cr)

Road BOT projects

Ghaziabad-Aligarh

Toll

194

35%

68

13

2

BV/share- 1.0x

Kanpur-Kabrai

Toll

68

100%

81

16

3

BV/share- 1.2x

Gwalior-Bhind

Toll

78

100%

78

15

3

BV/share- 1.0x

Bareilly-Almora

Toll

75

100%

75

15

3

BV/share- 1.0x

Jaora-Nayagaon

Toll

287

9%

24

5

1

BV/share- 1.0x

Rae Bareli-Jaunpur

Annuity

140

100%

140

27

5

BV/share- 1.0x

Narela Industrial Estate

Annuity+Fee

35

100%

39

8

1

BV/share- 1.1x

Kanpur Ayodhya

OMT

37

100%

37

7

1

FCFE, discount rate at 14%

Total

913

541

105

19

Grand Total

2,862

558

100

Upside

7%

CMP

522

Source: Company, Angel Research

Value of BOT projects

BOT projects have been valued using Book Value/ Free Cash flow to Equity

holder’s method. Our value for all the 8 BOT projects comes to `105/share, which

is 19% of the overall SOTP value for the company.

On combining the value of EPC business BOT projects, we arrive at a combined

business value of `558/share, reflecting 7% upside in stock price from the current

levels. Given the upside, we maintain our ACCUMULATE rating on the stock.

November 9, 2015

8

PNC Infratech | 2QFY2016 Result Update

Investment arguments

Strong order inflows to lead to better execution: PNC, a north focused EPC

player, should gain from a sharp revival in NHAI and MoRTH award activity,

in-turn translating into strong order inflows over the next 12 months. We

expect PNC to report order inflows of

`2,800/3,000cr during

FY2016E/2017E, which should further lead to uptick in execution. Accordingly,

we expect PNC (on standalone basis) to report strong 21.1% top-line CAGR

during FY2015-17E.

28.5% PAT CAGR during FY2015-17E: Stronger execution, benefits of lower

raw material prices and absorption of fixed costs, should help PNC

(standalone entity) report 19.4% EBITDA CAGR during FY2015-17E. EBITDA

growth coupled with decline in interest expenses (from `46cr in FY2015 to

`25cr in FY2017E) should help the standalone entity report 28.5% PAT CAGR

during the same period.

BOT projects nearing completion: PNC has a portfolio of 8 BOT projects, of

which 7 are operational. 3 of the BOT projects (Ghazaibad-Aligarh, Bareilly

Almora and Kanpur-Kabrai) commenced tolling in FY2016. Also, 1 of the

remaining project would commence operations in FY2016E itself. With

commencement of 4 BOT projects in FY2016E, we can expect possible ease in

consolidated balance sheet stress from FY2017E onwards.

Comfortable consol. D/E ratio: PNC entered the BOT space in FY2012 and

OMT space in FY2014. As a result, the consolidated debt of the company

increased from 0.2x in FY2011 to 1.9x in FY2015 (consolidated debt at

`1,635cr). The Management commented that they do not intend to build the

BOT portfolio unless (1) BOT project gives an estimated 16-18% equity IRR, (2)

the project’s ticket size is within `500cr as the Management intends equity

funding for new BOTs to be done through internal accruals, and (3) the

project is based within North India/ UP. With 1 pending BOT project likely to

get operational in the next 3 months, and PNC’s focus to reduce additions to

BOT projects portfolio, we expect the consolidated D/E ratio levels of the

company to peak-out in FY2017E.

Company background

PNC Infratech Ltd (PNC), incorporated in 1999, is an Agra based infra player

mainly focused on Roads & Highways construction. PNC, in FY2012, diversified

into BOT-Toll & Annuity projects and in FY2014 into OMT projects. Currently, PNC

is executing 20 Engineering Procurement Construction (EPC) projects (1 through JV

route), 7 BOT projects (including 2 Annuity projects) and 1 OMT project.

November 9, 2015

9

PNC Infratech | 2QFY2016 Result Update

Profit and Loss Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Net Sales

1,303

1,145

1,561

1,873

2,288

% Chg

2.3

(12.1)

36.3

20.0

22.2

Total Expenditure

1,148

1,005

1,344

1,626

1,979

Cost of Raw Materials Consumed

367

372

1,196

760

915

Change in Inventories of WIP

2

10

(60)

(37)

(34)

Employee benefits Expense

47

58

74

90

108

Other Expenses

732

566

135

813

991

EBITDA

156

140

217

247

309

% Chg

1.0

(10.0)

54.6

14.1

25.0

EBIDTA %

11.9

12.2

13.9

13.2

13.5

Depreciation

23

25

36

43

47

EBIT

133

115

180

205

261

% Chg

(1.7)

(13.3)

56.3

13.6

27.7

Interest and Financial Charges

23

23

46

34

25

Other Income

4

11

14

14

16

PBT

114

102

148

184

253

Tax

37

36

47

64

87

% of PBT

32.7

34.8

32.1

34.5

34.4

PAT before Exceptional item

76

67

100

121

166

Exceptional item

0

0

0

0

0

PAT

76

67

100

121

166

% Chg

(3.3)

(12.6)

50.2

20.2

37.5

PAT %

5.9

5.8

6.4

6.4

7.2

Diluted EPS

19

17

25

24

32

% Chg

(3.3)

(12.6)

50.2

(6.8)

37.5

November 9, 2015

10

PNC Infratech | 2QFY2016 Result Update

Balance Sheet (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Sources of Funds

Equity Capital

40

40

40

51

51

Reserves Total

527

590

679

1,219

1,375

Networth

566

630

718

1,270

1,426

Total Debt

234

248

324

215

235

Other Long-term Liabilities

99

178

250

234

234

Deferred Tax Liability

0

3

0

0

0

Total Liabilities

900

1,058

1,293

1,719

1,895

Application of Funds

Gross Block

225

287

387

431

494

Accumulated Depreciation

111

134

171

213

261

Net Block

114

153

217

218

234

Capital WIP

12

2

1

1

1

Investments

271

351

424

699

699

Current Assets

Inventories

105

105

223

260

305

Sundry Debtors

398

344

367

468

572

Cash and Bank Balance

38

100

21

25

25

Loans, Advances & Deposits

75

127

214

255

308

Other Current Asset

2

1

1

2

2

Current Liabilities

218

223

285

343

407

Net Current Assets

401

455

541

666

805

Other Assets

102

98

111

135

158

Total Assets

900

1,058

1,293

1,719

1,895

November 9, 2015

11

PNC Infratech | 2QFY2016 Result Update

Cash Flow Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Profit before tax

114

103

148

184

253

Dep. & Other Non-cash Charges

22

28

28

32

38

Change in Working Capital

59

74

(105)

(162)

(161)

Interest & Financial Charges

23

23

46

34

25

Direct taxes paid

(39)

(33)

(50)

(63)

(86)

Cash Flow from Operations

179

195

67

26

68

(Inc)/ Dec in Fixed Assets

(33)

(54)

(100)

(44)

(63)

(Inc)/ Dec in Investments

(104)

(80)

(73)

(275)

0

Cash Flow from Investing

(137)

(133)

(172)

(319)

(63)

Issue/ (Buy Back) of Equity

0

0

0

435

0

Inc./ (Dec.) in Loans

(17)

21

76

(109)

20

Dividend Paid (Incl. Tax)

(3)

(3)

(7)

(7)

(10)

Net Interest Expenses

(21)

(17)

(42)

(22)

(16)

Cash Flow from Financing

(42)

0

27

297

(6)

Inc./(Dec.) in Cash

0

62

(79)

4

(0)

Opening Cash balances

38

38

100

21

25

Closing Cash balances

38

100

21

25

25

November 9, 2015

12

PNC Infratech | 2QFY2016 Result Update

Key Ratios (Standalone)

Y/E March

FY13

FY14

FY15P

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

27.2

31.1

20.7

22.2

16.2

P/CEPS

20.9

22.7

15.2

16.4

12.6

Dividend yield (%)

17.5

17.5

8.7

8.7

6.3

EV/Sales

1.7

1.9

1.5

1.5

1.3

EV/EBITDA

14.6

15.9

11.0

11.6

9.4

EV / Total Assets

2.0

1.7

1.5

1.4

1.3

Per Share Data (`)

EPS (fully diluted)

19.2

16.8

25.2

23.5

32.3

Cash EPS

24.9

23.0

34.3

31.8

41.6

DPS

0.8

0.8

1.5

1.2

1.6

Book Value

142

158

180

247

278

Returns (%)

RoCE (Pre-tax)

17.7

15.0

20.2

17.3

17.6

Angel RoIC (Pre-tax)

18.8

16.5

21.6

17.6

17.9

RoE

14.4

11.2

14.9

12.1

12.3

Turnover ratios (x)

Asset Turnover (Gross Block) (X)

6.1

4.5

4.6

4.6

4.9

Inventory / Sales (days)

35

33

38

47

45

Receivables (days)

114

118

83

81

83

Payables (days)

61

80

69

71

69

WC (days)

88

72

52

58

59

Leverage Ratios (x)

D/E ratio (x)

0.4

0.4

0.5

0.2

0.2

Interest Coverage Ratio (x)

5.8

5.4

4.2

6.3

11.2

November 9, 2015

13

PNC Infratech | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

PNC Infratech

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

November 9, 2015

14