IPO Note | Financial Services

October 21, 2016

PNB Housing Finance Limited

SUBSCRIBE

Issue Open: October 25, 2016

All set to grow

Issue Close: October 27, 2016

PNB Housing Finance (PNBH) has been one of the fastest growing Housing

Finance Company and is currently the 5th largest player in India. Strong Brand

Issue Details

name of PNB & efficient management has helped in growing the business much

Face Value: `10

ahead of industry. With 49% stake being held by Pvt Equity Major Carlyle group,

PNBH is all set to scale up its operations.

Present Eq. Paid up Capital: `126.9cr

Strong management with fresh capital should help maintaining the growth: Mr.

Fresh Issue*: 3.9 cr Shares amounting to `3000crs

Sanjay Gupta was appointed as the MD of PNBH in 2010. Having worked with

MNCs like AIG, ABN Amro Bank & HDFC Ltd, he along with the newly hired

Offer for sale: -cr Shares amounting to -

professionals from pvt sector has been the key behind the growth. PNBH has

Post Eq. Paid up Capital: `165.63crs

delivered a phenomenal ~61% CAGR in loan book over FY12-16, which has

resulted in 43% CAGR in PAT growth. The IPO proceeds will enable the company

Market Lot: 19 Shares

maintaining the growth momentum albeit with a lower rate.

Fresh Issue (amount): `3000cr

Higher LTV/ ticket size & multiple products offerings have helped the growth:

PNBH’s average ticket size at `32 lakh is highest among the HFCs (HDFC `22

Price Band: `750-775

lakh, LICH `21 lakh). It also offers higher LTV of 66% vs 47%-LIC, 53%-DHFL,

Post-issue implied mkt. cap `12837cr*

65%-HDFC. Higher ticket size backed by high LTV also seems to have backed the

growth. PNBH has a well diversified portfolio (Home loans-61%, LAP-18%, Builder

Note:*Upper price band

Loans 13% & others 12%).The management intends to maintain similar portfolio

concentration going ahead.

Best in class asset quality despite aggressive growth: Despite aggressive loan

Book Building

growth, PNBH has managed strong asset quality, with GNPAs/NNPAs at

QIBs

50%

0.22%/0.14%, respectively (one of the best in industry) & better than large pvt

Non-Institutional

15%

players. However, the company has expanded its loan book in the last few years

and hence the book is not seasoned, so the possibility of rise in NPAs can be seen

Retail

35%

in the coming years. Nevertheless, we believe PNBH will be able to control its

credit cost and have NPAs at par with other Pvt Sector players.

Access to low cost funds and reduction in cost should be RoE accretive: PNBH has

Pre Issue Shareholding Pattern(%)

access to funds at a competitive rate, due to strong parentage & management

Promoter & Promoter group

51.0

(PNB & Carlyle group). Loans from banks now account for just 6% vs 34% in

FY12, while NCD+CP form 59% vs 43% of the total borrowings. The cost/income

Other

49.0

of 30% for PNBH is higher than others (LICH 15%, DHFL 30%). Higher share of

business from DSA and recent brand building initiatives have resulted in the

increase in cost. Ability to reduce cost and access to low cost funds going ahead

should be RoE accretive.

Outlook Valuation: PNBH has delivered RoE of 17.6% on the pre issue net worth.

While the IPO will result in RoE compression, this will give the much required fund

for growth. At the upper price band, the issue is offered at 4.6x its FY16 BV.

However at the post issue BV of `311, it is offered at 2.5x. PNBH is all geared up

for its next leg of growth and has the potential to become a significant player in

the Indian mortgage business. Looking at the quality of management, which can

drive the growth, we recommend a SUBSCRIBE to the issue.

Key Financials

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

NII

173

254

406

684

% chg

33.7

47.3

59.6

68.4

Net profit

93

130

194

328

% chg

19.9

39.7

49.6

68.8

NIM (%)

2.8

2.7

2.5

2.5

Book Value (`)

123.6

142.2

152.0

169.0

Siddharth Purohit

P/ABV (x)

6.3

5.5

5.1

4.6

RoA (%)

1.5

1.4

1.3

1.3

+91 22 39357800 Ext: 6872

RoE (%)

18.2

16.7

15.4

17.6

Source: Company, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

Please refer to important disclosures at the end of this report

1

PNB Housing Finance | IPO Note

Company background

PNB Housing Finance (PNBH) has been one of the fastest growing Housing

Finance Company in the last few years and is currently the 5th largest HFC in India.

Strong Brand name of PNB & management skill set of Pvt Sector has helped in

growing the business much ahead of industry. With 49% stake being held by Pvt

Equity Major Carlyle group, PNBH is all set to scale up its operations.

Key Management Personnel

Ms. Usha Ananthasubramanian (Chairperson): She holds a bachelor’s degree in

science and a master’s degree in statistics from the University of Madras and a

master’s degree in arts from the University of Mumbai. She has significant

experience in the fields of banking and financial services. She has been the

Managing Director and Chief Executive Officer of Punjab National Bank since

August 14, 2015

Mr. Sanjaya Gupta (MD): He has significant experience in the mortgage industry in

both retail and corporate assets. Prior to joining PNB Housing Finance he worked

with AIG United Guaranty as the country head and Chief Executive Officer of the

prospective mortgage guaranty business in India. He also worked with ABN Amro

Bank N.V. as the National Product Head, Mortgages- Consumer Banking and with

ABN AMRO Central Enterprise Services Private Limited as the VP, Mortgages. Prior

to that he worked with HDFC Limited.

Issue details

The company is raising `3000cr through fresh issue of equity shares in the price

band of `750-775. The fresh issue will constitute 23.37% of the post-issue paid-up

equity share capital of the company assuming the issue is subscribed at the upper

end of the price band.

Objects of the offer

To augment the bank’s tier-I capital base to meet its future capital

requirements due to expected growth of the company’s assets.

The listing will also enhance the visibility and brand name of the company

among existing and potential customers.

October 21, 2016

2

PNB Housing Finance | IPO Note

Investment rationale

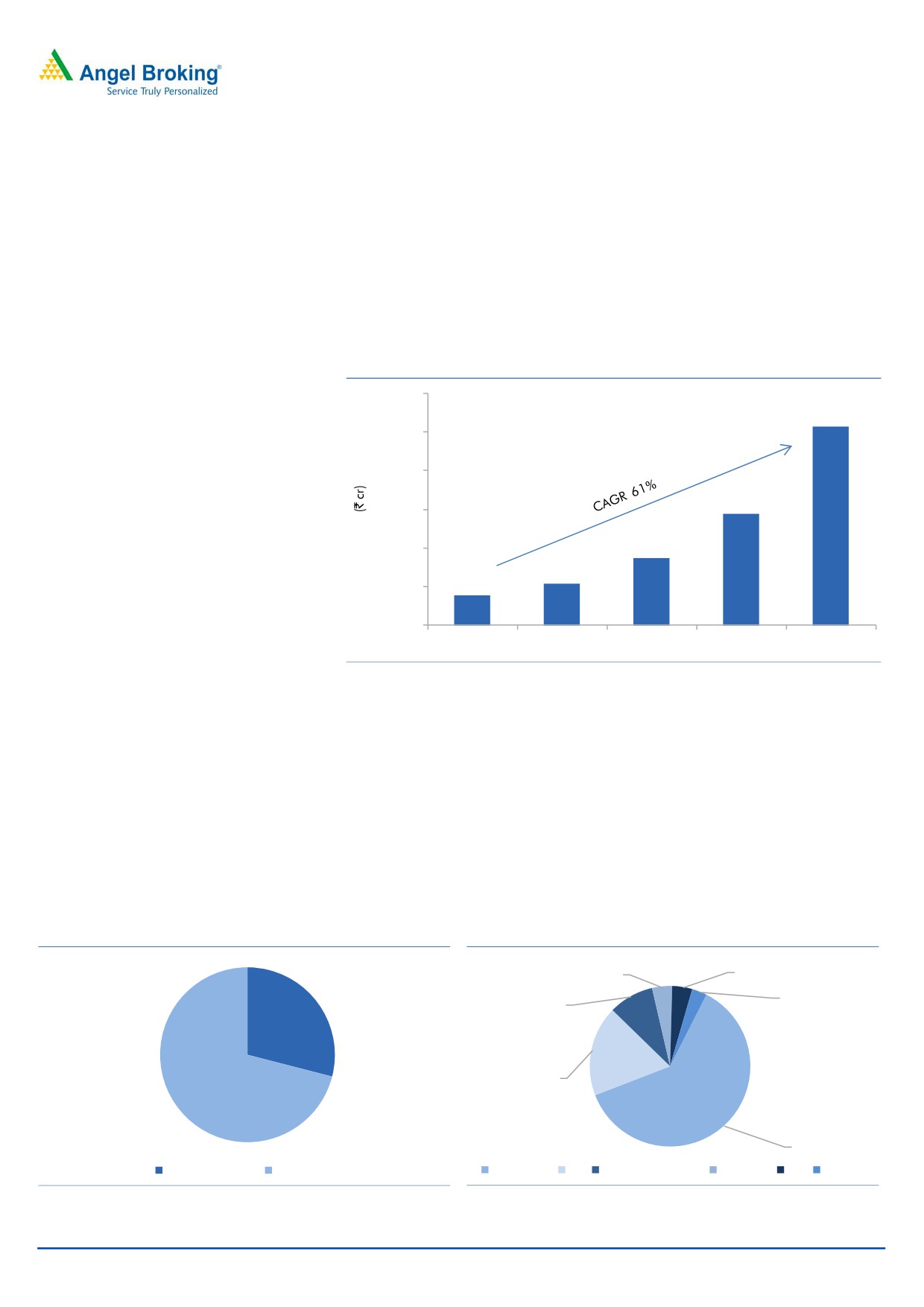

Strong management with fresh capital should help maintaining the growth:

Mr. Sanjay Gupta was appointed as the MD of PNBH in 2010. Having worked with

MNCs like AIG, ABN Amro Bank & HDFC Ltd, he along with the newly hired

professionals from pvt sector has been the key behind the growth. PNBH has

delivered a phenomenal ~61% CAGR in loan book over FY12-16, which has

resulted in 43% CAGR in PAT growth. The IPO proceeds will enable the company

maintaining the growth momentum albeit with a lower rate.

Exhibit 1: Strong growth in loan book

30,000

25,641

25,000

20,000

14,400

15,000

10,000

8,649

5,399

3,781

5,000

-

FY12

FY13

FY14

FY15

FY16

Source: RHP, Angel Research

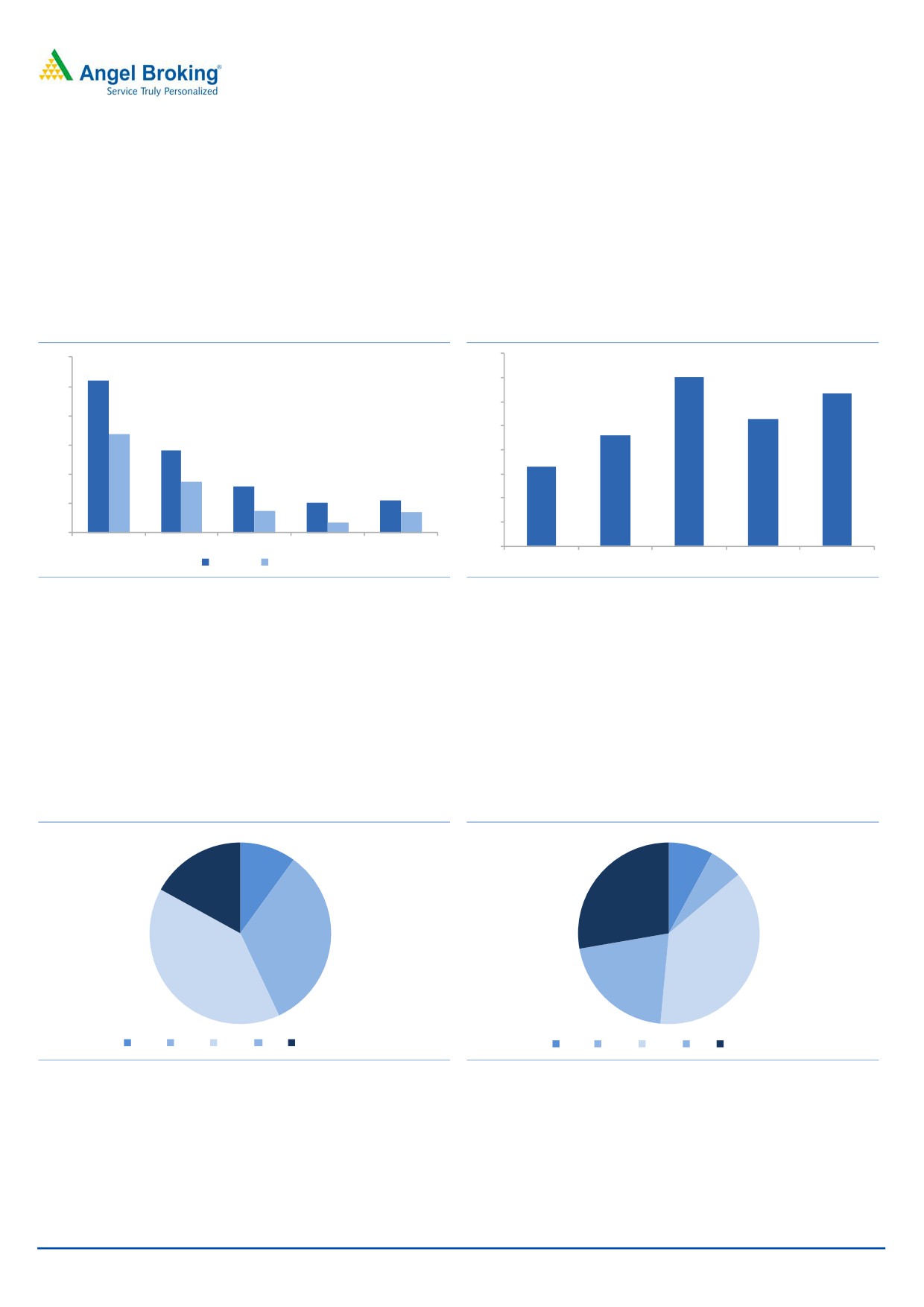

PNBH’s retail loan share is lower than peers, but growth from both retail as well

non retail remains strong: Housing loan constitutes ~70% of the loan book, while

non housing loans constitute the balance of the portfolio. The non housing loans

normally generates higher yield; hence, we believe over the long run, PNB

Housing will be able to scale up its yield and in turn return ratios. PNBH has a well

diversified portfolio where in home loans form -61%, LAP-18%, and builder loans

13% of the total book. The company also offers loans for non residential premises

and lease discounting rental loans, which together forms ~12% of the portfolio.

The management intends to maintain similar portfolio concentration going ahead.

Exhibit 2: Loan mix - Housing - Non-housing

Exhibit 3: Portfolio distribution

4%

4%

3%

9%

29

18%

71

61%

Non Housing Loans Housing Loans

Home Loans LAP Construction Finance NRP Loans LRD Corp Loans

Source: RHP, Angel Research

Source: RHP, Angel Research

October 21, 2016

3

PNB Housing Finance | IPO Note

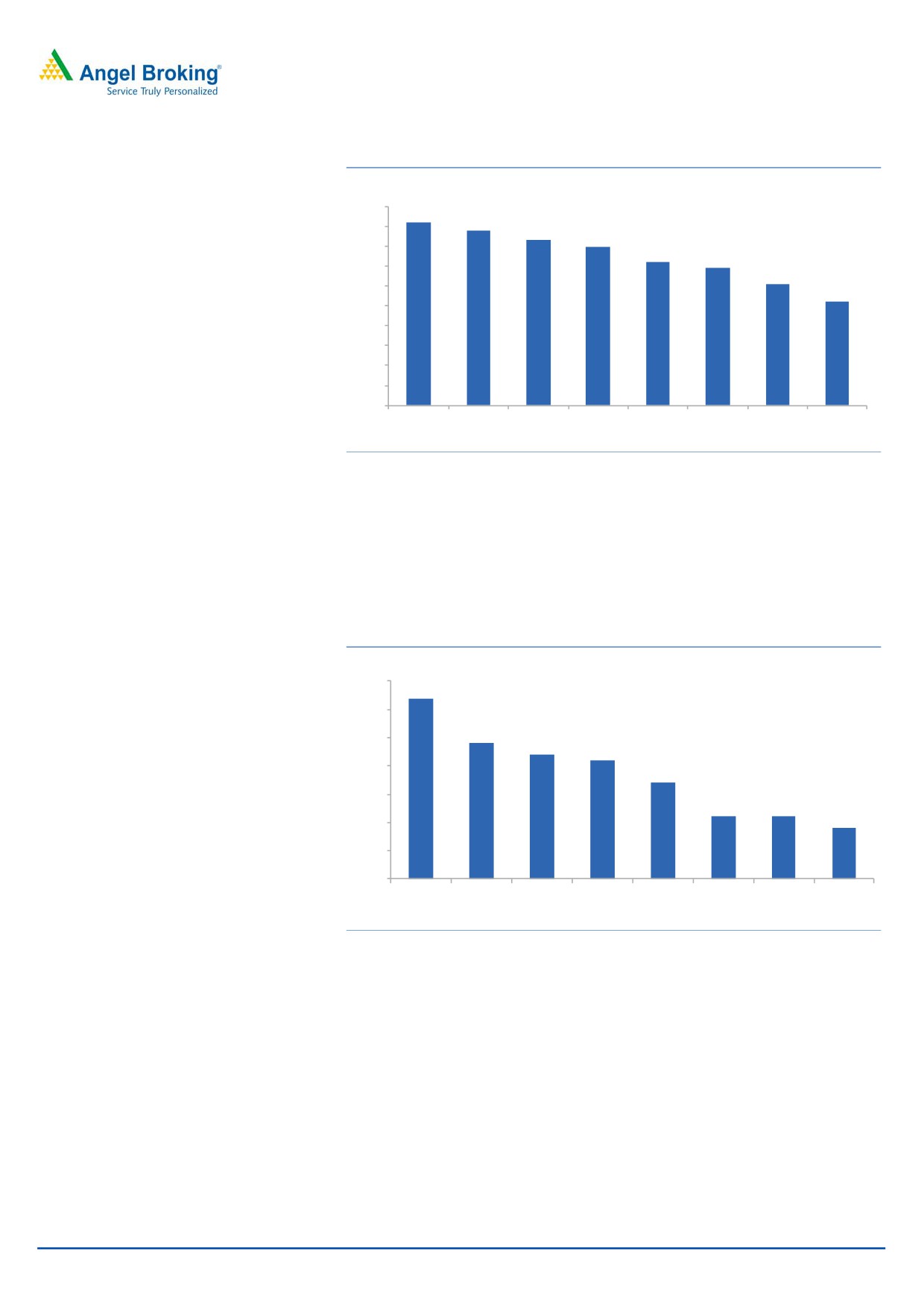

Exhibit 4: Comparative Retail Loan Mix

(%)

100

92

88

90

83

80

80

72

69

70

61

60

52

50

40

30

20

10

0

GRUH

LIC

Can Fin REPCO DHFL

HDFC

PNB India Bulls

Finance Housing Homes

Housing Housing

Source: RHP, Angel Research

Higher average ticket size, together with higher LTV have also contributed to

growth: PNBH’s average ticket size at `32 lakh is highest among the listed Housing

Finance Companies (HDFC `22 lakh, LICH `21 lakh, DHFL `11 lakh).It also offers

higher LTV of 66% vs 47%-LIC, 53%-DHFL, 65%-HDFC. Higher ticket size backed

by high LTV also seems to have backed the growth.

Exhibit 5: Comparative Average Ticket Size

(` lakhs)

35

32

30

24

25

22

21

20

17

15

11

11

9

10

5

0

PNB

India Bulls HDFC

LIC

Can Fin REPCO DHFL

GRUH

Housing Housing

Housing Homes

Source: RHP, Angel Research

While the blended LTV of PNBH looks high, the LTV differs according to the loan

types like in a retail housing loan for a salaried person would be ~69% and for a

self-employed person would be ~60%. While the LTV in case of non housing loans

for both the segments would be ~45-46%. PNBH’s relatively high LTV as well as

high ticket size is also partly due to the fact that it has been so far largely present

in the urban areas. Whereas some of the mid and large players have much wider

network, where the ticket size can be low.

October 21, 2016

4

PNB Housing Finance | IPO Note

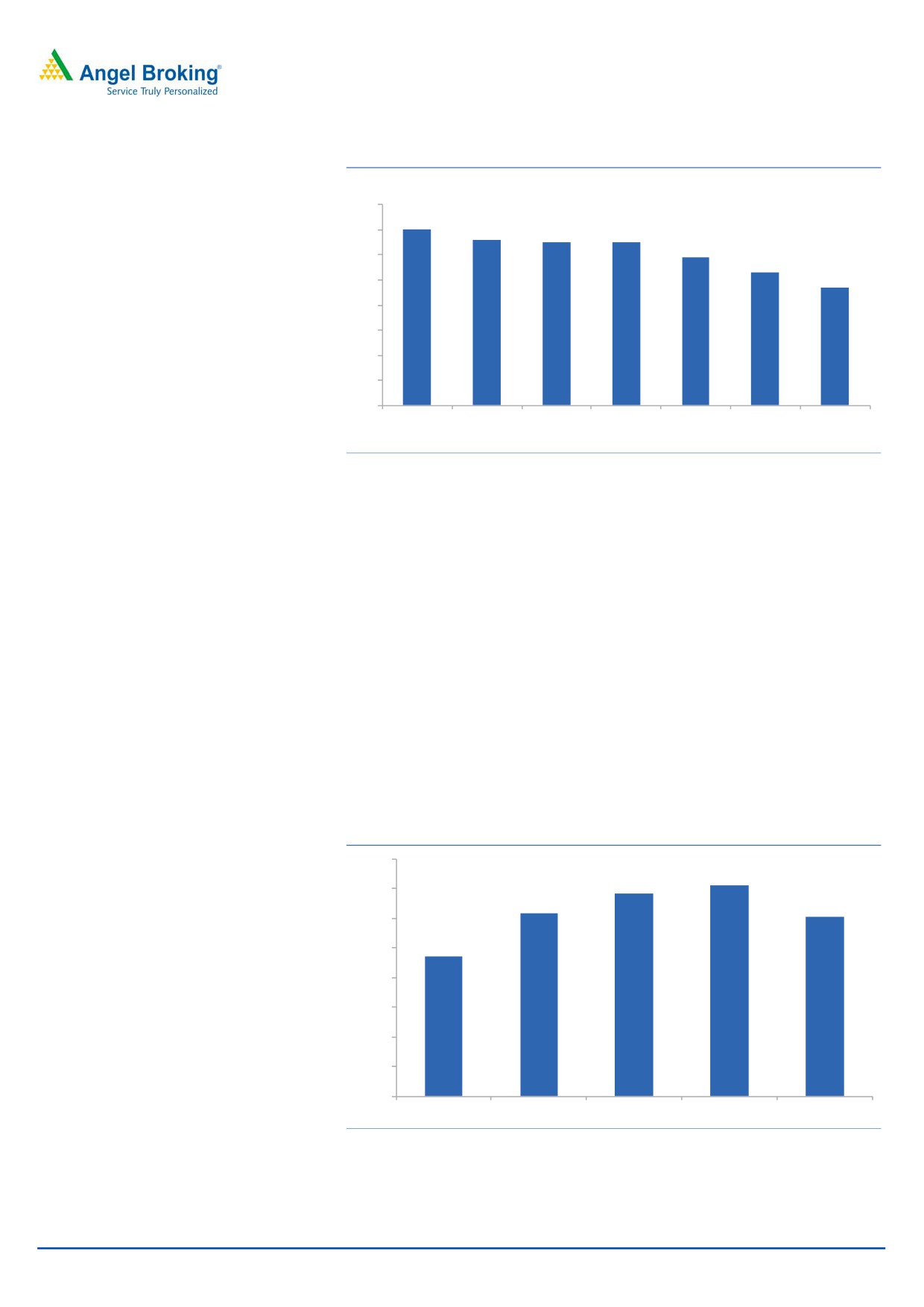

Exhibit 6: Average LTV of HFCs in India

(%)

80

70

70

66

65

65

59

60

53

47

50

40

30

20

10

0

India Bulls

PNB

REPCO

HDFC

GRUH

DHFL LIC Housing

Housing Housing

Source: RHP, Angel Research

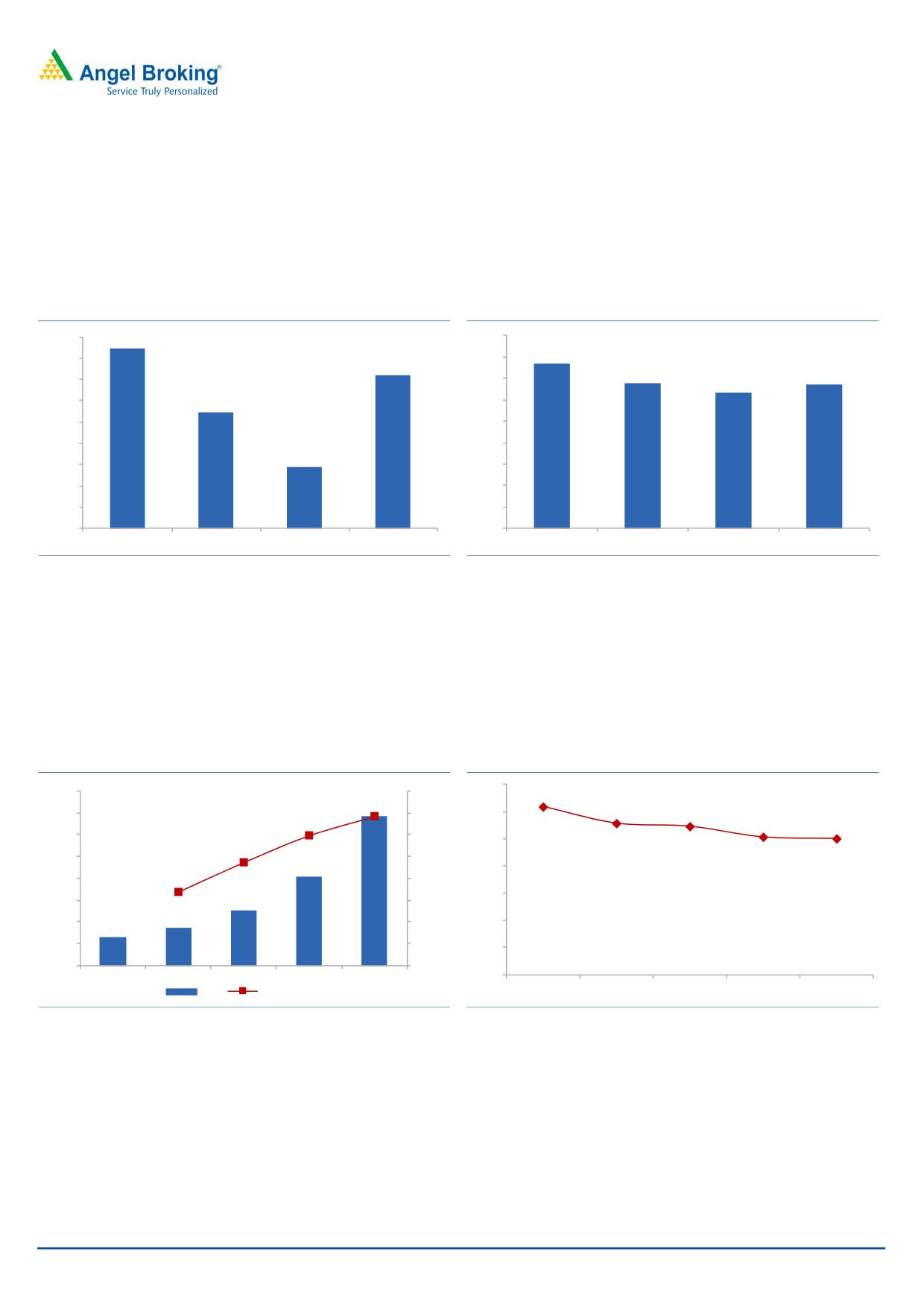

Enough scope for a decline in cost/income ratio: The operating cost of PNBH is

relatively higher and remains one of the highest among the HFCs. Higher share of

business sourced from other channels like DSA and brand building cost has led to

the higher cost structure. However, we believe there is enough scope in the cost to

come down. We have seen this happening in case of mid-sized housing finance

companies in the recent years.

Business sourcing from direct sales agents still forms a large part of the total book,

~45%. Though it has come down from 53%, ability to generate higher business

from own sources could reduce the overall operating expenses. Further, over the

last few years, the company has undertaken several steps to improve the brand

visibility. The cost/income of 30% for PNBH is higher than others (LICH 15%, DHFL

30%). Hence, we expect going ahead there would be enough scope for cost

rationalization.

Exhibit 7: Cost/Income Ratio (%) likely to come down

40.0

35.5

34.3

35.0

30.9

30.2

30.0

23.7

25.0

20.0

15.0

10.0

5.0

-

FY12

FY13

FY14

FY15

FY16

Source: RHP, Angel Research

October 21, 2016

5

PNB Housing Finance | IPO Note

Best in class asset quality despite aggressive growth: Despite aggressive loan

growth, PNBH has managed strong asset quality, with GNPAs/NNPAs at

0.22%/0.14%, respectively (one of the best in industry) & better than large pvt

players. However, the company has expanded its loan book in the last few years

and hence the book is not seasoned, so the possibility of rise in NPAs can be seen

in the coming years. Nevertheless, we believe PNBH will be able to control its

credit cost and have NPAs at par with other pvt sector players.

Exhibit 8: GNPAs and NNPAs trend

Exhibit 9: Credit Cost (%)

1.2

0.40

0.35

1.0

0.35

0.32

1.0

0.30

0.26

0.8

0.7

0.25

0.23

0.6

0.6

0.20

0.17

0.4

0.4

0.3

0.15

0.2

0.2

0.2

0.1

0.10

0.2

0.1

0.05

0.0

FY12

FY13

FY14

FY15

FY16

0.00

GNPAs % NNPAs %

FY12

FY13

FY14

FY15

FY16

Source: RHP, Angel Research

Source: RHP, Angel Research

Strong parentage & management bandwidth with stable credit rating has allowed

access to low cost funds: PNBH is able to raise funds from the money markets at a

competitive rate, largely due to strong parentage (PNB & Carlyle group). Over the

last 4 years, PNBH has reduced its dependence on bank funding substantially and

has been able to raise funds via NCD, CP as well as public deposits. Bank funding

in total funds has been reduced to 6% by FY16 from a high of 34% in FY12. PNBH

is the 2nd largest deposit taking HFC in India.

Exhibit 10: Sources of Funding FY2014

Exhibit 11: Sources of Funding FY2016

10

8

17

6

0

28

33

38

40

21

NHB Bank NCD CP Deposits & ECB

NHB Bank NCD CP Deposits & ECB

Source: RHP, Angel Research

Source: RHP, Angel Research

October 21, 2016

6

PNB Housing Finance | IPO Note

Scope for improvement in ROE & ROA profile: PNBH has delivered RoE of 17.6%

on the pre issue net worth. While the IPO will result in RoE compression, this will

give the much required fund for growth. Though PNBH has product offerings

across various segments and the RoE & RoA is little lower than some of the large

HFCs. However, we believe as the business scales up the operating cost structure

would also get reduced.

Exhibit 12: ROE

Exhibit 13: ROA

18.5

18.2

1.80

1.54

18.0

1.60

17.6

1.35

1.35

17.5

1.40

1.27

17.0

16.7

1.20

16.5

1.00

16.0

0.80

15.4

15.5

0.60

15.0

0.40

14.5

0.20

14.0

0.00

FY13

FY14

FY15

FY16

FY13

FY14

FY15

FY16

Source: RHP, Angel Research

Source: RHP, Angel Research

NIM likely to see improvement post fund raising: While NIM remains moderately

lower than large HFCs, higher operating cost has resulted in RoE being lower.

However, we believe the unique blend of portfolio will enable PNB housing to

optimize its RoE in the long run. Post dilution, we expect RoE to drop to ~14.5% by

FY18. However, we believe it will be able to bounce back to its existing RoE levels

post that.

Exhibit 14: NII trend

Exhibit 15: NIM trend

3.50

800

80.0%

3.09

684

2.79

700

68.4%

70.0%

3.00

2.73

59.6%

2.54

2.51

600

60.0%

2.50

47.3%

500

50.0%

406

2.00

400

33.7%

40.0%

1.50

300

254

30.0%

173

200

20.0%

1.00

129

100

10.0%

0.50

-

0.0%

0.00

FY12

FY13

FY14

FY15

FY16

NII

% Growth YoY

FY12

FY13

FY14

FY15

FY16

Source: RHP, Angel Research

Source: RHP, Angel Research

October 21, 2016

7

PNB Housing Finance | IPO Note

IPO will enable improved Capital Adequacy

PNBH’s capital adequacy at the end of 1QFY2017 stood at 13.04% and looking at

the high growth, which the company has been delivering, capital raising was a

must. We believe the current fund raising via the IPO should meet the company’s

capital requirement in the near term.

Exhibit 16: Capital adequacy

20.0

17.2

18.0

16.0

13.6

13.3

14.0

12.6

12.7

12.0

10.9

9.9

9.5

10.0

9.0

9.0

8.0

6.0

4.0

2.0

0.0

FY12

FY13

FY14

FY15

FY16

CAR % Tier I

Source: RHP, Angel Research

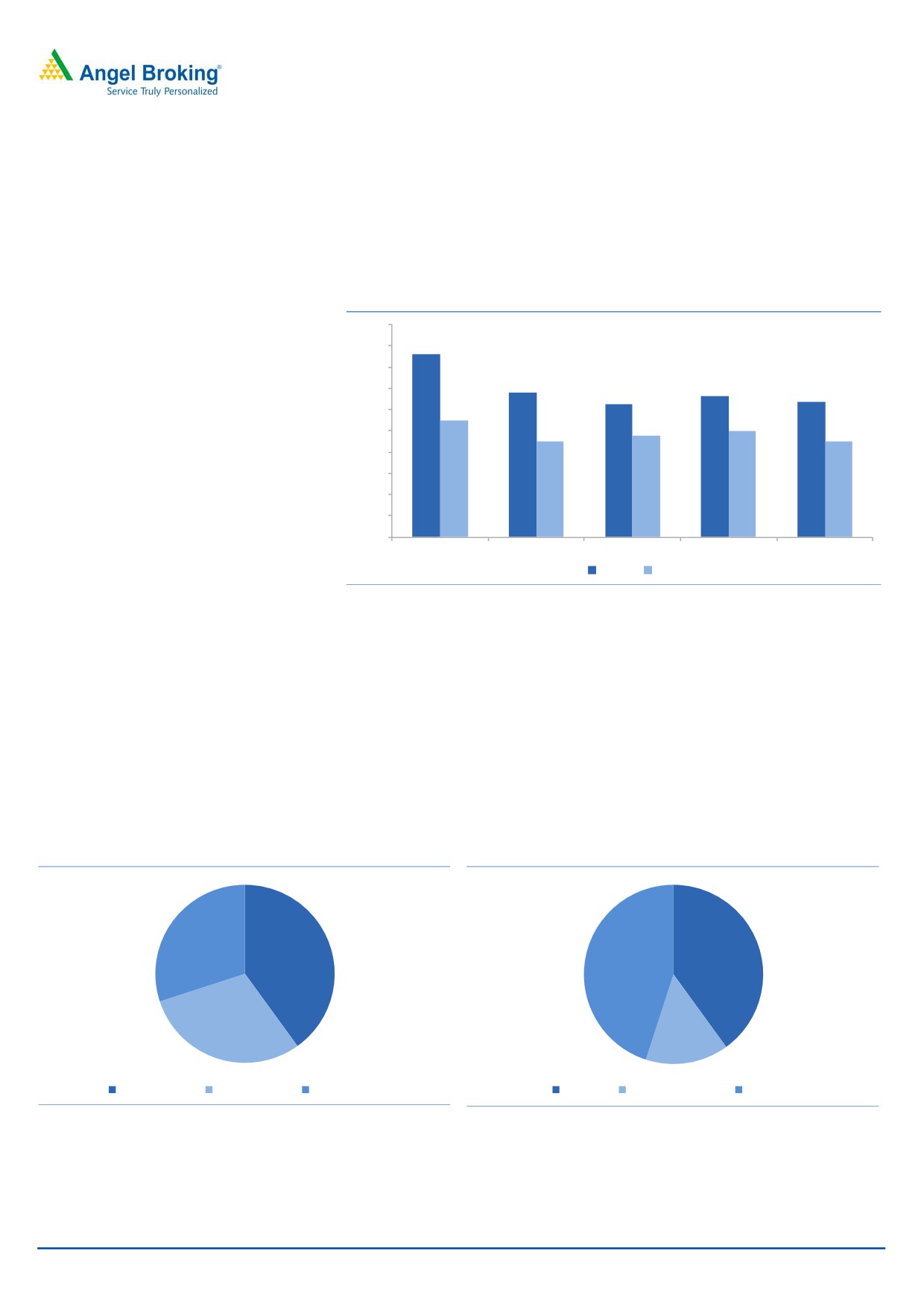

Well diversified geographical and customer mix

PNBH has a high presence in the northern part of India. However, off late the

company has also expanded into other geographies. North accounted for 40% of

the outstanding loans, while west and south accounted for 30% each of the loan

book in India. Based on customer profile again the loan book seems well

balanced with 45% of the outstanding loans to self employed persons. While

salaried customers accounted for ~40% of the loans, the balance 15% loan was

towards corporate.

Exhibit 17: Geographical Mix of Loan (%)

Exhibit 18: Loan mix by customer

30

40

40

45

30

15

Northern region

Southern region

Western region

Salaried

Loan to corporates

Self employed

Source: RHP, Angel Research

Source: RHP, Angel Research

October 21, 2016

8

PNB Housing Finance | IPO Note

Outlook & Valuation: PNBH has delivered RoE of 17.6% on the pre issue net

worth. While the IPO will result in RoE compression, this will give the much

required fund for growth. At the upper price band, the issue is offered at 4.6x its

FY16 BV. However at the post issue BV of `311, it is offered at 2.5x. PNBH is all

geared up for its next leg of growth and has the potential to become a significant

player in the Indian mortgage business. Looking at the quality of management,

which can drive the growth, we recommend a SUBSCRIBE to the issue.

Comparative tables

Exhibit 19: Comparative Performance Balance sheet

Cost/

Loan Book Retail Others

GNPAs % CAR%

Income

LIC Housing

125,173

88

12

0.45

17.0

14.7

DHFL

62,295

72

28

0.93

16.7

30.1

India Bulls Housing

67,800

77

23

0.84

20.5

14.3

PNB Housing

25,641

61

39

0.22

12.7

30.2

Can Fin Homes

10,643

99

1

0.19

20.7

18.7

REPCO

7,691

80

20

1.20

20.8

19.3

GRUH Finance

11,115

92

8

0.30

17.8

18.0

Source: RHP, Company, Angel Research

Exhibit 20: Comparative - Asset Quality & Capital Adequacy

4 year CAGR

BV ( FY18E

NII Loan PAT NIM % RoE %

P/ BV*

CMP

Consensus)

LIC Housing

20.6

18.7

16.0

2.5

19.6

252.8

2.4

600

DHFL

30.3

25.1

27.5

3.0

15.1

217.2

1.5

332

India Bulls Housing

26.2

25.3

74.0

4.7

27.0

312.2

2.8

879

PNB Housing**

51.7

61.4

43.4

2.9

17.6

386.5

2.0

775

Can Fin Homes

37.7

41.2

37.4

3.2

17.9

480.7

3.8

1830

REPCO

31.0

28.6

25.8

4.4

16.4

213.2

3.7

790

GRUH Finance

24.4

28.6

19.3

4.2

31.5

35.1

9.7

339

Source: RHP, Company, Angel Research; Note: CMP as of October 21, 2016; * Bloomberg

Consensus; ** Angel Estimates; CAGR FY2012-16

October 21, 2016

9

PNB Housing Finance | IPO Note

Income statement

Y/E March (` cr)

FY13

FY14

FY15

FY16

NII

173

254

406

684

- YoY Growth (%)

33.7

47.3

59.6

68.4

Other Income

32

64

110

155

- YoY Growth (%)

81.0

103.2

70.1

41.9

Operating Income

204

319

516

839

- YoY Growth (%)

39.4

56.0

61.8

62.8

Operating Expenses

63

109

183

254

- YoY Growth (%)

81.9

73.1

67.4

38.7

Pre - Provision Profit

141

209

333

585

- YoY Growth (%)

26.2

48.3

58.8

76.0

Prov. & Cont.

12

30

38

81

- YoY Growth (%)

98.7

144.1

25.2

112.9

Profit Before Tax

129

179

294

504

- YoY Growth (%)

21.9

39.0

64.5

71.3

Prov. for Taxation

36

49

100

177

- as a % of PBT

27.9

27.5

34.1

35.0

PAT

93

130

194

328

- YoY Growth (%)

19.9

39.7

49.6

68.8

Balance sheet

Y/E March (` cr)

FY13

FY14

FY15

FY16

Share Capital

50

66

104

127

Reserve & Surplus

568

868

1,475

2,018

NetWorth

618

934

1,579

2,144

Borrowings

5,535

8,396

14,552

24,095

- YoY Growth (%)

98.2

51.7

73.3

65.6

Provisions & Others

65

106

197

337

Other Liabilities

1,437

2,103

2,707

3,096

Total Liabilities

7,655

11,540

19,035

29,672

Cash and Bal With RBI

128

138

293

249

Investments

777

645

1,586

1,622

Advances

5,399

8,649

14,400

25,641

- Growth (%)

42.8

60.2

66.5

78.1

Fixed Assets

18

29

58

62

Deferred Tax Assets

14

15

-

-

Other Assets

1,319

2,062

2,698

2,099

Total Assets

7,655

11,540

19,035

29,672

October 21, 2016

10

PNB Housing Finance | IPO Note

Ratio analysis

Y/E March

FY13

FY14

FY15

FY16

Profitability ratios (%)

NIMs

2.8

2.7

2.5

2.5

RoA

1.5

1.4

1.3

1.3

RoE

18.2

16.7

15.4

17.6

Asset Quality (%)

Gross NPAs

0.6

0.3

0.2

0.2

Net NPAs

0.4

0.2

0.1

0.1

Per Share Data (`)

EPS

18.6

19.7

18.7

25.8

BV

123.6

142.2

152.0

169.0

Valuation Ratios

PER (x)

41.7

39.3

41.5

30.0

P/BVPS (x)

6.3

5.5

5.1

4.6

DuPont Analysis

Net Interest Income

10.5

11.0

10.9

10.4

Non Interest Income

7.6

8.4

8.3

7.6

Total Revenues

2.9

2.6

2.7

2.8

Operating Cost

1.0

1.1

1.2

1.0

PPP

2.3

2.2

2.2

2.4

Total Provisions

0.2

0.3

0.2

0.3

PreTax Profit

2.1

1.9

1.9

2.1

Tax

0.6

0.5

0.7

0.7

ROA

1.5

1.4

1.3

1.3

Leverage

11.9

12.4

12.2

13.1

RoE (%)

18.2

16.7

15.4

17.6

October 21, 2016

11

PNB Housing Finance | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

October 21, 2016

12