Initiating Coverage | Education

November 18, 2015

Navneet Education

ACCUMULATE

CMP

`88

A stable business model

Target Price

`97

Navneet Education’s is primarily engaged in the business of publishing educational

Investment Period

12 Months

material, in both print and digital formats. The company also manufactures paper and

non-paper stationary products.

Stock Info

Investment Arguments

Sector

Education

Business expansion to mitigate cyclical risk: NEL’s Publication business is seasonal in

Market Cap (` cr)

2,092

nature and any strong growth is dependent on major changes in the syllabus of

Maharashtra (market share of 60%) and Gujarat boards (market share of 65%). Now,

Net Debt (` cr)

138

the company is attempting to increase its revenues through business expansion in

Beta

0.5

different segments. It is taking initiatives like

52 Week High / Low

120 / 87

(a) Content publication for CBSE syllabus: Apart from Maharashtra and Gujarat, NEL

Avg. Daily Volume

20,049

is targeting to grow its presence in other states through its CBSE content business. It is

Face Value (`)

2

anticipated that the growth may continue to be strong in the segment on account of a

BSE Sensex

25,864

syllabus change and also with more schools in different states adopting CBSE curriculum.

Nifty

7,838

(b) Selling supplementary books to government: NEL takes orders to sell

Reuters Code

NAVN.BO

supplementary books to Maharashtra government, which get distributed to students in

Bloomberg Code

NELI@IN

government schools. In FY2013, NEL generated ~`27cr through this business. But in

FY2014, there were no government orders after many controversies arose related to

the issue of tenders. The tenders issue then got resolved and in FY2015 the company

Shareholding Pattern (%)

generated a revenue of around `25cr. Going forward, we expect the company to

achieve strong revenue from this segment.

Promoters

61.8

MF / Banks / Indian Fls

15.2

Higher exports to drive stationary growth business: In the Stationary segment, we

expect the company to report healthy growth in coming financial years on back of

FII / NRIs / OCBs

2.5

higher growth in exports. The company mainly exports to USA and Africa. Also, the

Indian Public / Others

20.5

company is looking to tap newer geographies like the Middle East. In FY2015, exports

in the segment reported a yoy growth of ~33% to ~`170cr. In FY2016, the company

Abs. (%)

3m 1yr

3yr

expects around `200cr from export sales. On the margin front, the company is

expecting a margin improvement by 30-40bp, benefitting from economies of scale.

Sensex

(7.8)

(1.7)

41.3

NEL

(12.2)

(10.8)

58.0

Outlook and Valuation: Given the company’s proven track record, its strong brand,

consistent performance of Government projects and E-Learning (Digital) segments,

and with it tapping new segments like CBSE across India, we expect it to report a

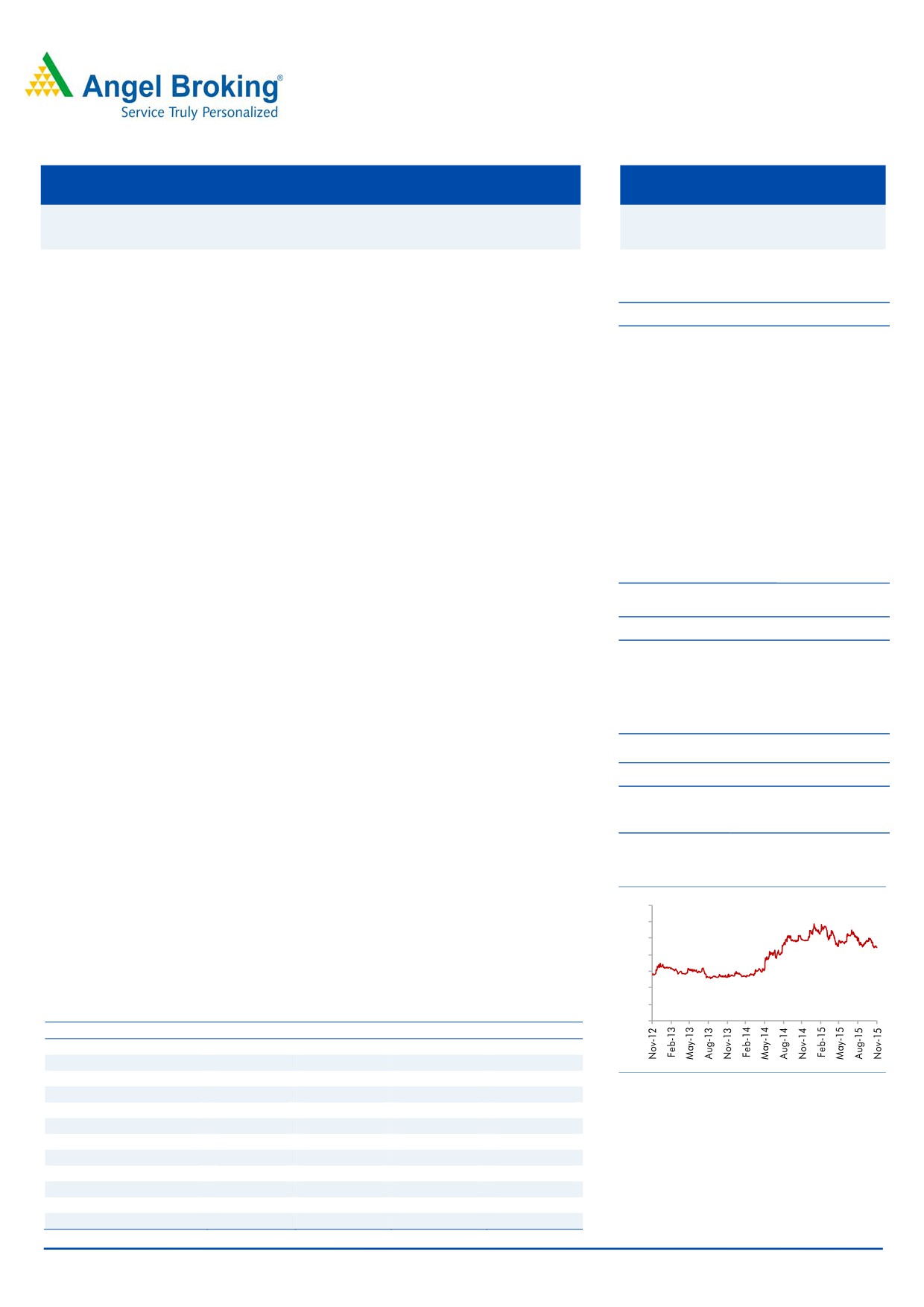

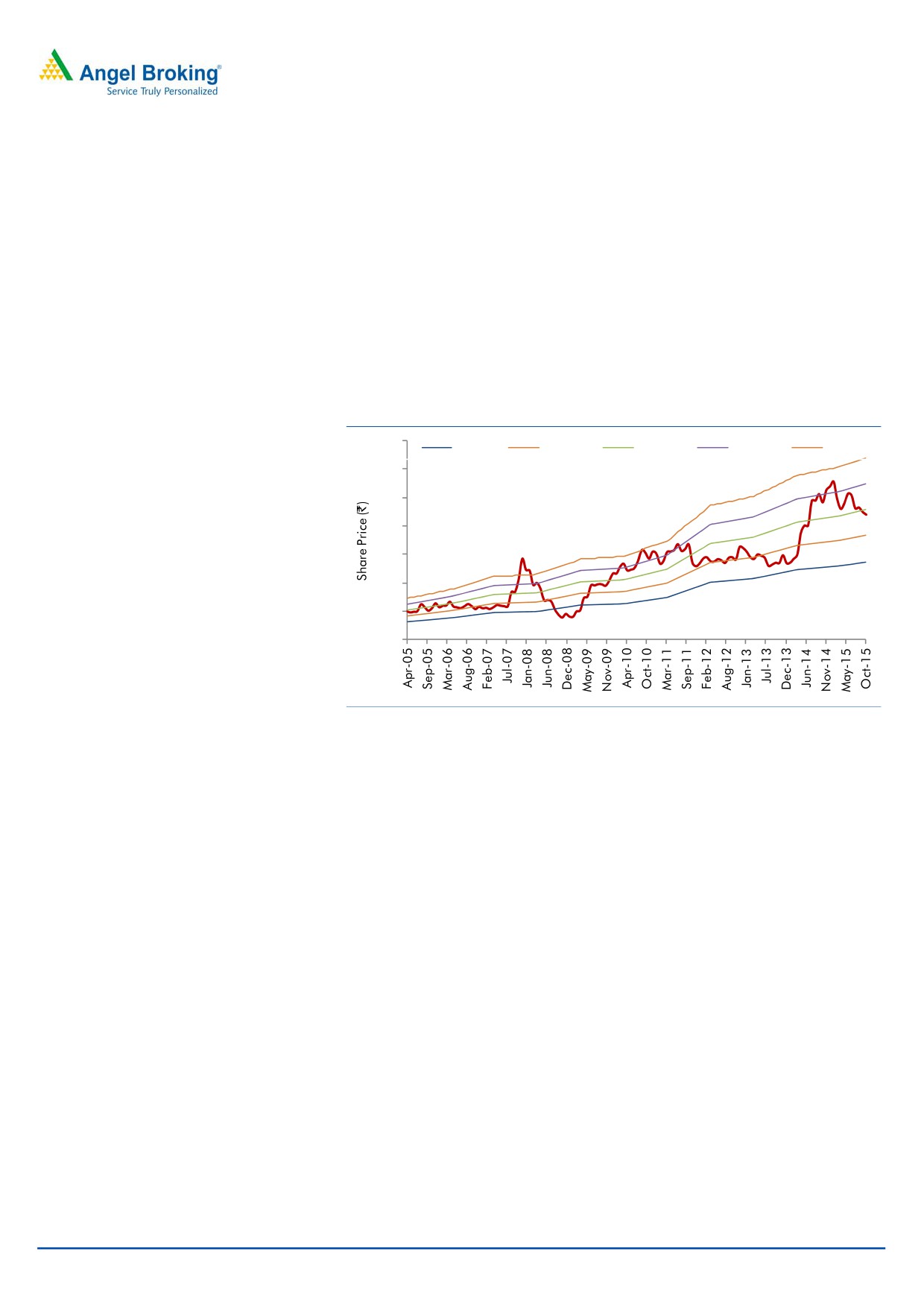

3 years - share price chart

healthy top-line and bottom-line CAGR of 4.1% and 5.5%, respectively, over FY2015-

17E. Moreover, NEL has repaid the `90cr loan which will lead to significant saving in

140

120

interest cost in the coming financial years. At the current market price, the stock trades

100

at a P/E of 14.4x its FY2017E EPS. We initiate coverage on the stock with an

80

Accumulate recommendation and target price of `97 (16x FY2017E EPS), indicating

60

an upside of ~11% in the stock price from the present levels.

40

20

Key financials

0

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

Net sales

882

979

998

1,062

% chg

9.5

11.0

1.9

6.4

Net profit

115

130

137

145

Source: Company, Angel Research

% chg

8.0

13.1

5.1

5.9

EBITDA margin (%)

23.6

24.2

24.1

24.0

EPS (`)

4.8

5.5

5.8

6.1

P/E (x)

18.2

16.1

15.3

14.4

P/BV (x)

4.4

3.9

3.4

3.0

RoE (%)

24.1

24.0

22.0

20.5

RoCE (%)

25.6

30.1

26.9

25.7

Amarjeet S Maurya

EV/Sales (x)

2.6

2.2

2.2

2.0

022-39357800 Ext: 6831

EV/EBITDA (x)

10.9

9.2

9.1

8.5

Source: Company, Angel Research, Note: CMP as of November 17, 2015

Please refer to important disclosures at the end of this report

1

Navneet Education | Education

Investment Arguments

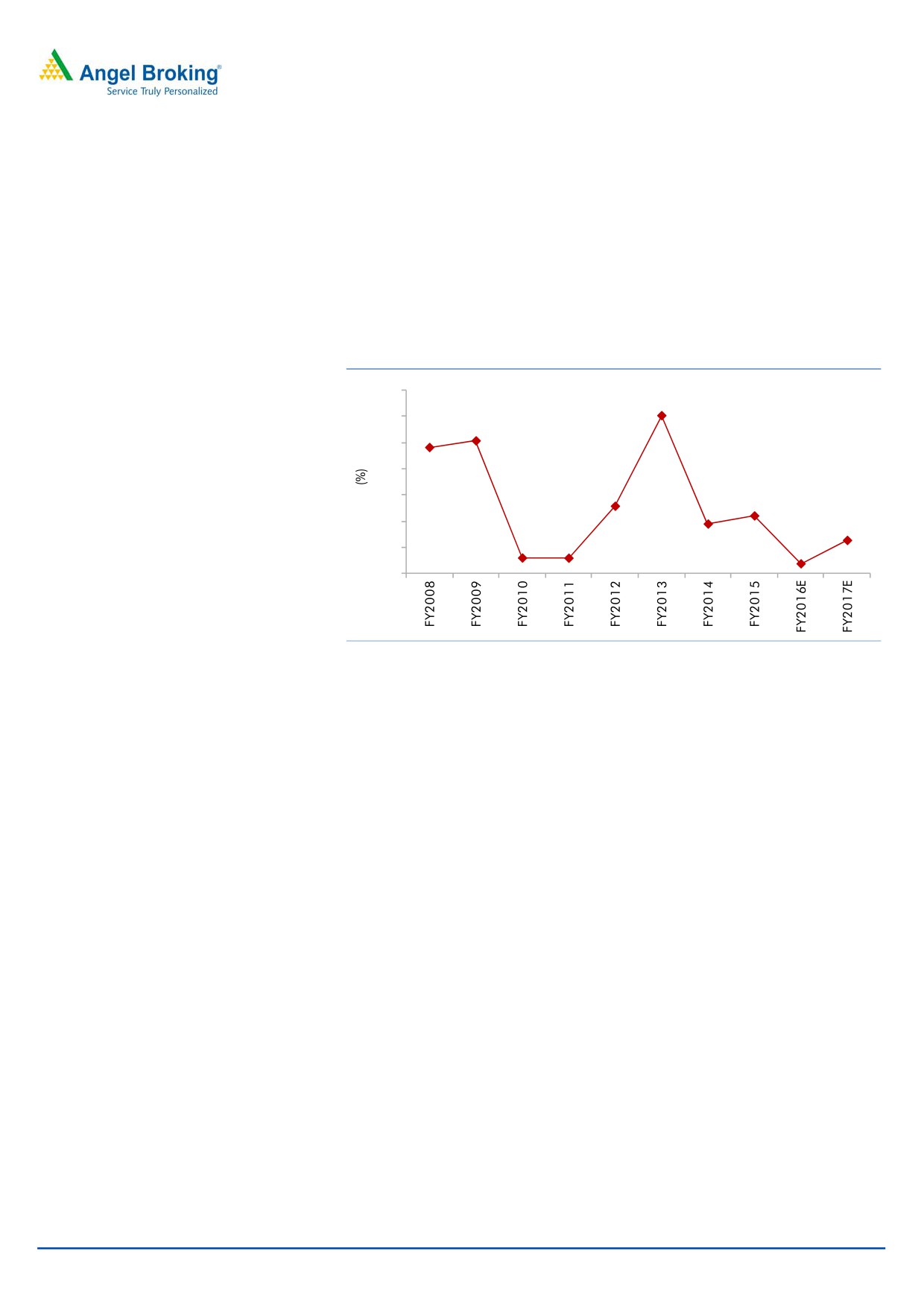

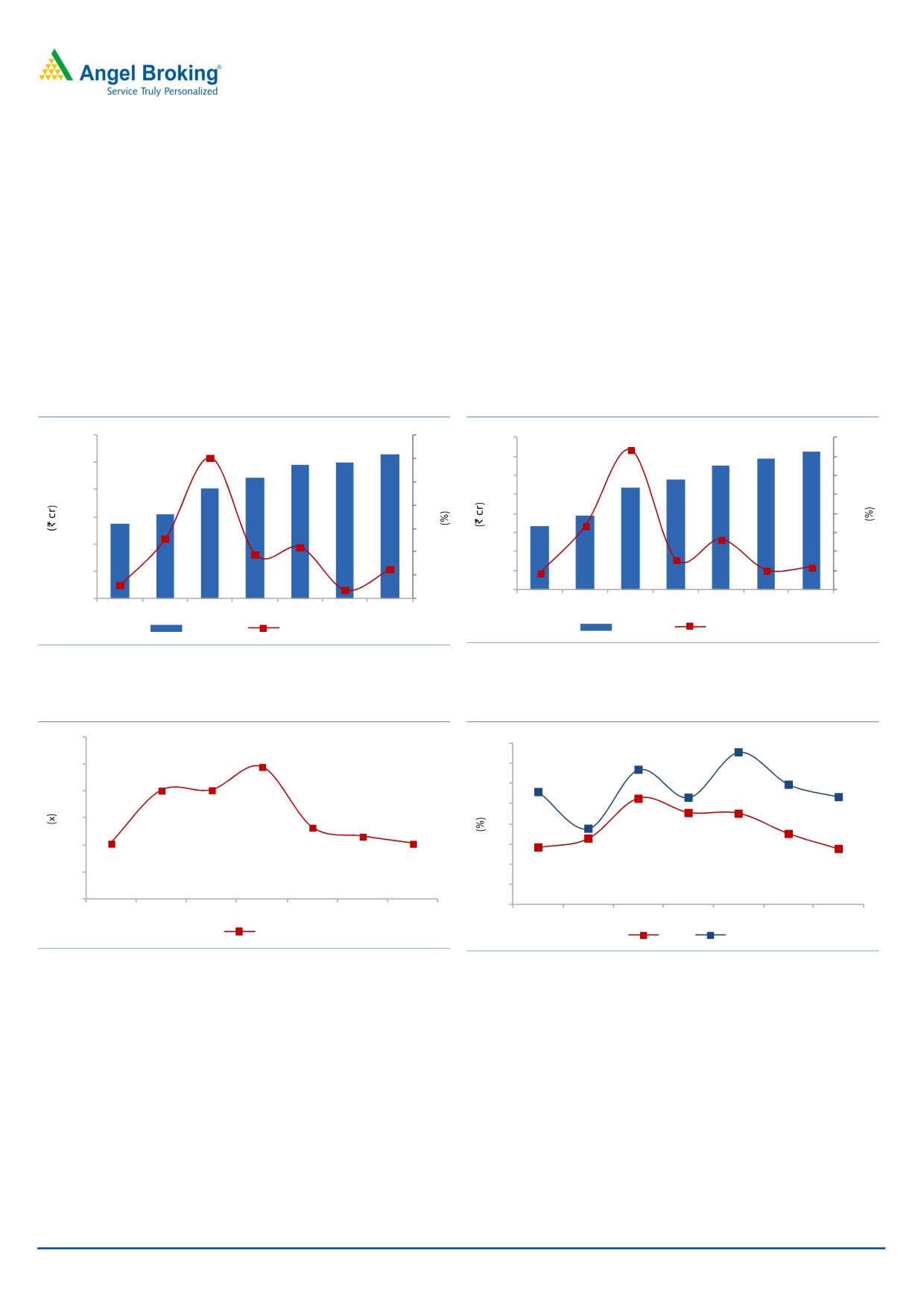

Top-line to report 4.1% CAGR over FY2015-17E

The company’s business mainly comprises of Publication, Stationary and

e-Learning segments. In the past, whenever there has been a major change in the

syllabuses of Maharashtra and Gujarat boards, NEL has reported a strong double

digit revenue growth. Going forward, in FY2016 and FY2017, there would be no

major change in syllabus.

Exhibit 1: Top-line performance tracking change in syllabus

35

30.2

30

25.4

24.1

25

Going forward, in FY2016 and FY2017,

20

there would be no major change in

12.9

15

11.0

syllabus

9.5

10

6.4

3.0

3.0

5

1.9

0

Source: Company, Angel Research

November 18, 2015

2

Navneet Education | Education

Exhibit 2: Syllabus change expected for FY16 & FY17

Academic

Maharashtra

Gujrat

Year

Std. Subject

Std.

Subject

I

All Subjects (All Mediums)

VI

All Subjects (English & Hindi Mediums)

II

All Subjects (All Mediums) VII All Subjects (English & Hindi Mediums)

All Languages

VIII

All Subjects (English & Hindi Mediums)

FY2014

X History & Political Science

Geography & Economics

Science - Environment

III

All Subjects (All Mediums)

I

All Subjects (Gujrati Medium)

IV

All Subjects (All Mediums)

II

All Subjects (Gujrati Medium)

FY2015

III

All Subjects (Gujrati Medium)

IV

All Subjects (Gujrati Medium)

V All Subjects (Gujrati Medium)

V

All Subjects (All Mediums)

I

All Subjects (English & Hindi Mediums)

VI

All Subjects (All Mediums)

II

All Subjects (English & Hindi Mediums)

FY2016

III

All Subjects (English & Hindi Mediums)

IV

All Subjects (English & Hindi Mediums)

V All Subjects (English & Hindi Mediums)

VII

All Subjects (All Mediums)

IX

All Subjects (All Mediums)

FY2017

VIII

All Subjects (All Mediums)

XI

All Commerce Subjects (All Mediums)

Source: Company, Angel Research

We expect healthy growth going forward, owing to the following reasons

(a) Adoption of CBSE syllabus on the rise across India: Apart from Maharashtra

and Gujarat, NEL is targeting to grow its presence in other states through its

CBSE content business. It is anticipated that the growth may continue to be in

double digits in the segment with more number of schools in different states

adopting CBSE curriculum.

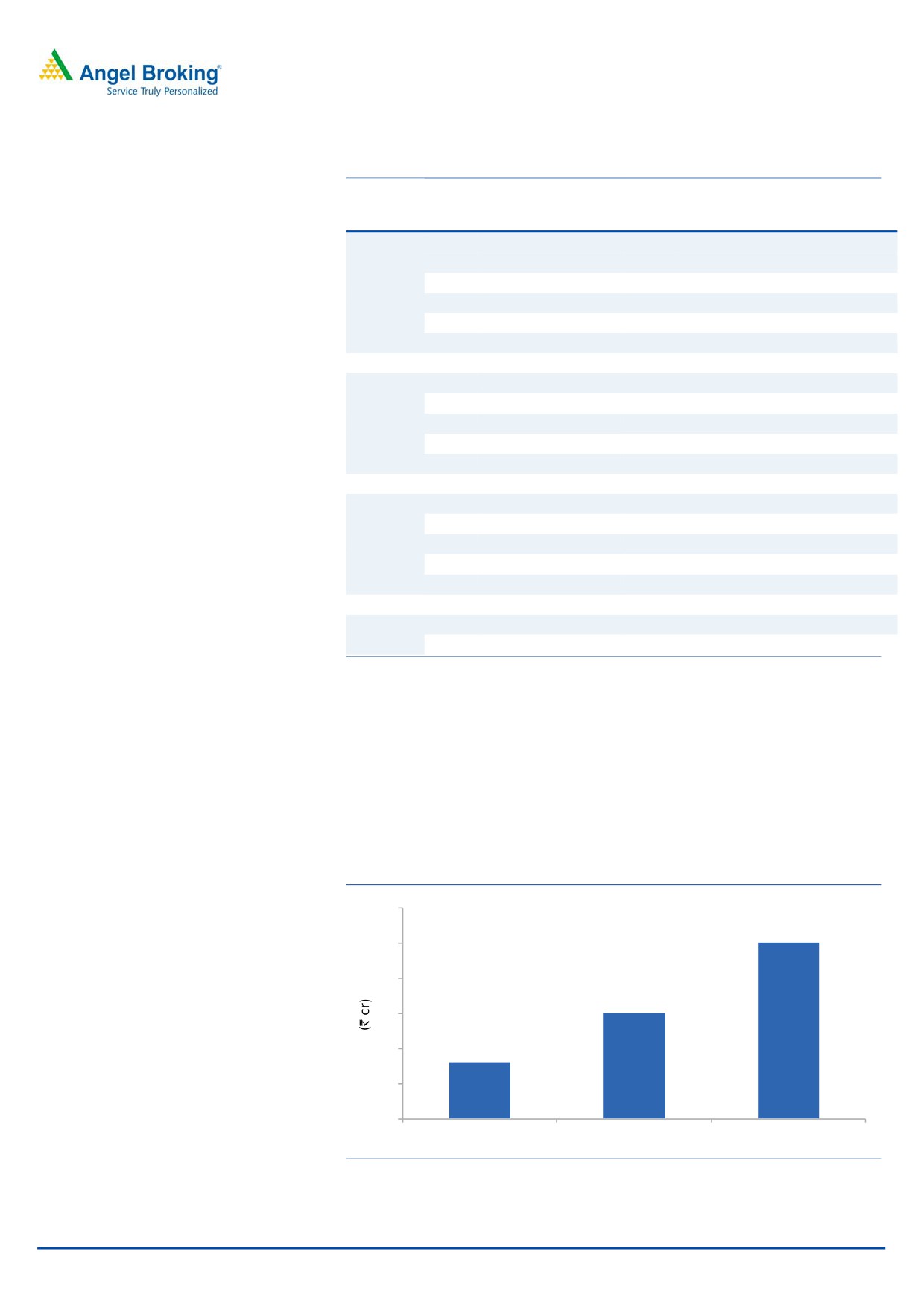

Exhibit 3: CBSE segment’s expected revenue trend

60

In the CBSE segments, NEL expect

50

revenue of `30cr in FY16 & `50cr in

50

FY17

40

30

30

20

16

10

0

FY2015

FY2016E

FY2017E

Source: Company, Angel Research

November 18, 2015

3

Navneet Education | Education

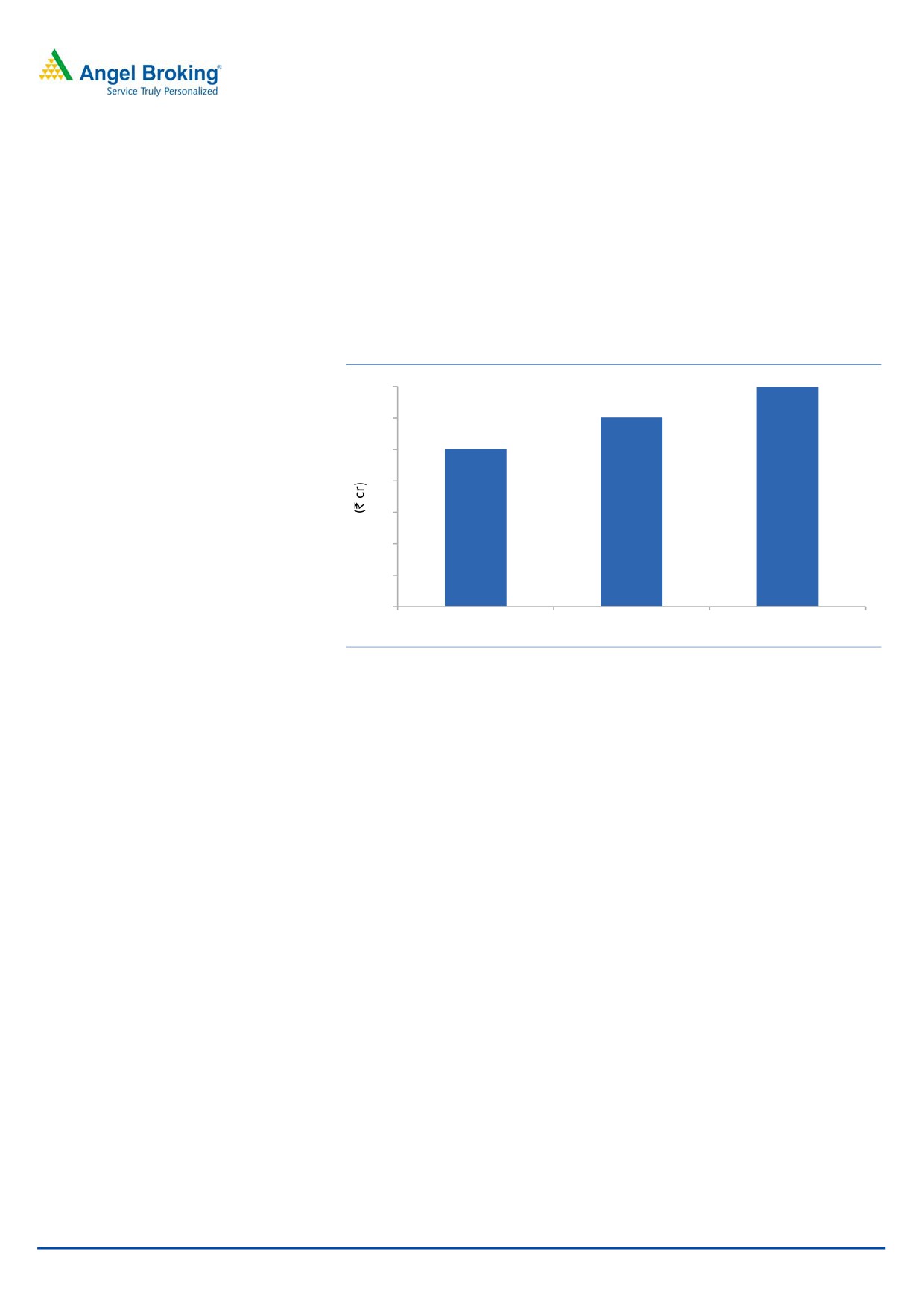

(b) Government Projects: NEL takes orders to sell supplementary books to

Maharashtra government, which get distributed to students in government

schools. In FY2013, NEL generated

~`27cr through the Government

segment. But in FY2014, there were no government orders after many

controversies arose related to the issue of tenders. The tenders issue then got

resolved and in FY2015 the company generated revenue of around `25cr.

Going forward, we expect the company to achieve strong revenue from this

segment.

Exhibit 4: Government orders’ expected revenue trend

35

35

30

30

25

25

20

15

10

5

0

FY2015

FY2016E

FY2017E

Source: Company, Angel Research

(c) E-Learning segment: In this segment, NEL is targeting products such as

e-learning tablets, cloud based interactive exams, application based audio

visuals and also B2B products such as ‘Top Class’ provided to educational

institutions. In FY2015, the company has generated a revenue of `20cr from

this segment. Going ahead, we expect decent growth from this segment.

Expect healthy growth in Stationary business

In the Stationary segment, we expect the company to report healthy growth in

coming financial years on back of higher growth in exports. The company mainly

NEL is looking to tap newer

exports to USA and Africa. Also, the company is looking to tap newer geographies

geographies like the Middle East &

like the Middle East. In FY2015, the company has reported ~33% growth. In

expects around

`200cr from export

FY2016, the company expects around `200cr from export sales. On the margin

sales in FY16

front, the company is expecting an improvement by 30-40bp, benefitting from

economies of scale.

November 18, 2015

4

Navneet Education | Education

Financial outlook

Going ahead, we expect NEL to report

Going ahead, we expect NEL to report a top-line CAGR of 4.1% over FY2015-17E

a top-line CAGR of

~4.1% over

to ~`1,062cr owing to healthy growth in Publication as well as Stationery

FY2015-17E to ~`1,062cr

businesses. In the Publication business, we expect double-digit growth, driven by

growth in CBSE school, Government projects and E-Learning (Digital) segments.

On the bottom-line front, we expect the

On the bottom-line front, we expect the company to report a 5.5% CAGR over

company to report a 5.5% CAGR over

FY2015-17E on account of healthy top-line growth and operating margin.

FY2015-17E

Moreover, NEL has repaid the `90cr loan which will lead to significant saving in

interest costs in the coming financial years.

Exhibit 5: Projected Net Sales growth trend

Exhibit 6: Projected Net Profit growth trend

1,200

35

36.8

30.2

1,062

160

145

40

979

998

137

30

140

130

35

1,000

882

115

806

120

107

30

25

800

100

25

619

20

78

548

80

67

20

600

12.9

13.2

11.0

15

60

15

9.5

16.8

400

7.9

6.4

10

40

5.1

5.9

10

4.4

200

3.0

20

5

1.9

5

0

0

-

0

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

FY2011

FY2012

FY2013

FY2014

FY2015 FY2016E FY2017E

Net Sales

yoy growth (%)

Net Profit

yoy growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 7: Debt/Equity trend

Exhibit 8: ROE and ROCE trend

30.1

0.6

31

0.5

28.4

0.5

29

26.9

0.4

0.4

26.2

27

25.6

25.7

0.4

25

0.3

22.5

0.3

25.5

0.2

23

0.2

0.2

24.1

24.0

0.2

21

22.0

21.6

19

20.7

20.5

0.1

17

0.0

15

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

D/E

ROE

ROCE

Source: Company, Angel Research

Source: Company, Angel Research

November 18, 2015

5

Navneet Education | Education

Outlook and Valuation

Given the company’s proven track record, its strong brand, consistent performance of

Government projects and E-Learning (Digital) segments, and with it tapping new

segments like CBSE across India, we expect it to report a healthy top-line and bottom-

line CAGR of 4.1% and 5.5%, respectively, over FY2015-17E. Moreover, NEL has

repaid the `90cr loan which will lead to significant saving in interest cost in the coming

financial years. At the current market price, the stock trades at a P/E of 14.4x its

FY2017E EPS. We initiate coverage on the stock with an Accumulate recommendation

and target price of `97 (16x FY2017E EPS), indicating an upside of ~11% in the stock

price from the present levels.

Exhibit 9: One year PE forward chart

140

9x

12x

15x

18x

21x

120

100

80

60

40

20

0

Source: Company, Angel Research

Downside risks to our estimates include 1) adverse volatility in currency exchange

rates could impact company’s profitability as

17% of the company’s total

consolidated revenue comes from exports sales (2) the company’s Publication

business is largely present in Maharashtra and Gujarat, which exposes the

company to concentration risk.

November 18, 2015

6

Navneet Education | Education

Company Background

Navneet Education Ltd, formerly Navneet Publication (India) Ltd, is in the business

of publication of knowledge based information in educational and general books

form as well as in electronic media, and manufacturing of paper and other

stationery products. The company’s segments include Publication and Stationery.

The company's products are sold under the brand names - Navneet, Vikas, Gala,

FfUuNn and Boss. The company’s portfolio of education based books includes

supplementary books like digests (guide) and workbooks, which are published in

five languages: English, Gujarati, Hindi, Marathi, and Urdu. The company also

publishes various titles in the children and general books category, which are not

based on syllabus, such as coloring and activity books, board books, story books

and books on health and hygiene, art and artist, cooking, mehendi, and

embroidery.

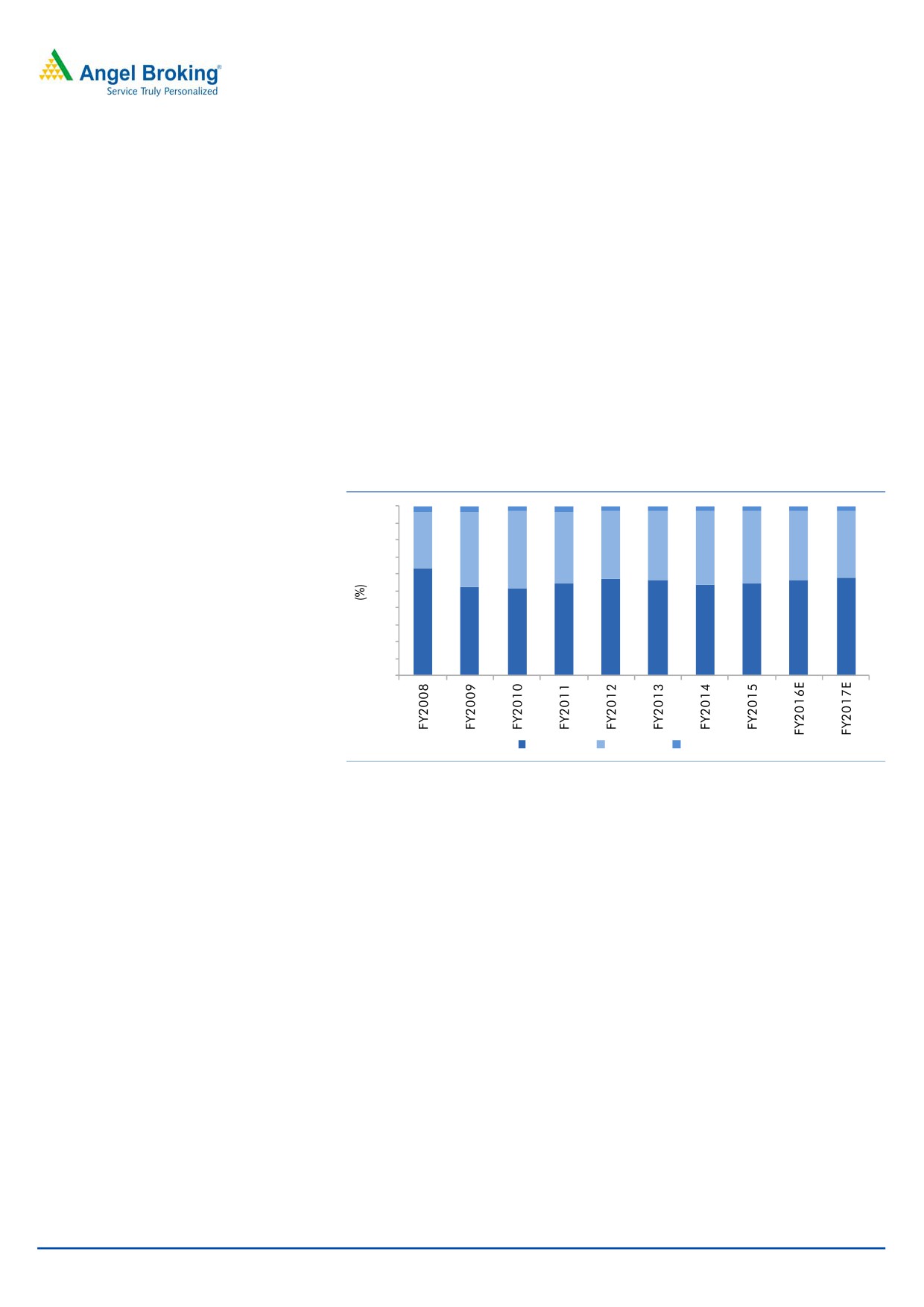

Exhibit 10: Segment wise revenue break-up of NEL

100

3

3

3

3

3

3

3

3

3

3

90

80

33

40

40

41

40

44

45

42

43

43

70

60

50

40

30

64

55

57

57

54

57

58

52

52

54

20

10

0

Publishing Stationery

Others

Source: Company, Angel Research

November 18, 2015

7

Navneet Education | Education

Consolidated Profit & Loss Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Total operating income

806

882

979

998

1,062

% chg

30.2

9.5

11.0

1.9

6.4

Total Expenditure

616

674

742

758

807

Raw Materials

387

434

464

474

505

Personnel Expenses

69

74

87

92

100

Others Expenses

160

167

191

192

202

EBITDA

190

208

237

241

255

% chg

44.7

9.5

14.0

1.4

5.9

(% of Net Sales)

23.6

23.6

24.2

24.1

24.0

Depreciation& Amortisation

23

26

31

35

36

EBIT

167

182

206

206

218

% chg

45.8

9.4

13.3

(0.2)

6.0

(% of Net Sales)

20.7

20.7

21.1

20.6

20.6

Interest & other Charges

8

10

9

7

7

Other Income

4

4

2

12

12

(% of PBT)

2.2

2.0

1.1

5.7

5.4

Share in profit of Associates

-

-

-

-

-

Recurring PBT

162

176

200

211

223

% chg

35.6

8.2

13.6

5.6

5.9

Prior Period & Extraord. Exp./(Inc.)

-

-

-

-

-

PBT (reported)

162

176

200

211

223

Tax

55

60

69

74

78

(% of PBT)

33.9

34.4

34.7

35.0

35.0

PAT (reported)

107

115

130

137

145

Less: Minority interest (MI)

1

(0)

0

0

0

PAT after MI (reported)

107

115

130

137

145

ADJ. PAT

107

115

130

137

145

% chg

36.8

8.0

13.1

5.1

5.9

(% of Net Sales)

13.2

13.1

13.3

13.7

13.7

Basic EPS (`)

4.5

4.8

5.5

5.8

6.1

Fully Diluted EPS (`)

4.5

4.8

5.5

5.8

6.1

% chg

36.8

7.9

13.2

5.1

5.9

November 18, 2015

8

Navneet Education | Education

Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

48

48

48

48

48

Reserves& Surplus

370

430

495

574

658

Shareholders Funds

418

478

542

622

706

Minority Interest

0

0

0

0

0

Total Loans

169

234

144

144

145

Deferred Tax Liability

6

7

5

5

5

Total Liabilities

594

719

691

771

856

APPLICATION OF FUNDS

Gross Block

332

365

374

394

414

Less: Acc. Depreciation

157

178

204

239

275

Net Block

174

187

170

155

139

Capital Work-in-Progress

6

5

4

4

4

Investments

31

47

49

49

49

Current Assets

498

604

599

681

779

Inventories

275

334

348

383

413

Sundry Debtors

166

196

189

205

233

Cash

4

7

6

13

17

Loans & Advances

35

47

38

50

69

Other Assets

19

20

19

30

48

Current liabilities

117

126

132

120

116

Net Current Assets

381

478

467

561

663

Deferred Tax Asset

2

1

1

1

1

Mis. Exp. not written off

-

-

-

-

-

Total Assets

594

719

691

771

856

November 18, 2015

9

Navneet Education | Education

Cashflow Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Profit before tax

164

176

200

211

223

Depreciation

23

26

31

35

36

Change in Working Capital

(118)

(89)

(10)

(87)

(98)

Interest / Dividend (Net)

5

8

7

7

7

Direct taxes paid

-

(61)

(65)

(74)

(78)

Others

(0)

(0)

(0)

-

-

Cash Flow from Operations

74

59

162

92

91

(Inc.)/ Dec. in Fixed Assets

(39)

(45)

(6)

(20)

(20)

(Inc.)/ Dec. in Investments

(30)

(16)

(2)

-

-

Cash Flow from Investing

(70)

(62)

(8)

(20)

(20)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

(22)

(50)

(56)

0

1

Dividend Paid (Incl. Tax)

(43)

(48)

(53)

(58)

(61)

Interest / Dividend (Net)

59

104

(46)

(7)

(7)

Cash Flow from Financing

(6)

6

(156)

(64)

(67)

Inc./(Dec.) in Cash

(2)

3

(1)

8

3

Opening Cash balances

5

4

7

6

13

Closing Cash balances

4

7

6

13

17

November 18, 2015

10

Navneet Education | Education

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

19.6

18.2

16.1

15.3

14.4

P/CEPS

16.0

14.9

13.0

12.2

11.6

P/BV

5.0

4.4

3.9

3.4

3.0

Dividend yield (%)

2.0

2.3

2.5

2.7

2.9

EV/Sales

2.8

2.6

2.2

2.2

2.0

EV/EBITDA

11.7

10.9

9.2

9.1

8.5

EV / Total Assets

3.1

2.7

2.7

2.4

2.2

Per Share Data (`)

EPS (Basic)

4.5

4.8

5.5

5.8

6.1

EPS (fully diluted)

4.5

4.8

5.5

5.8

6.1

Cash EPS

5.5

5.9

6.8

7.2

7.6

DPS

1.8

2.0

2.2

2.4

2.6

Book Value

17.6

20.1

22.8

26.1

29.6

Returns (%)

ROCE

28.4

25.6

30.1

26.9

25.7

Angel ROIC (Pre-tax)

30.1

27.7

32.7

29.3

27.8

ROE

25.5

24.1

24.0

22.0

20.5

Turnover ratios (x)

Asset Turnover (Gross Block)

2.4

2.4

2.6

2.5

2.6

Inventory / Sales (days)

125

138

130

140

142

Receivables (days)

75

81

70

75

80

Payables (days)

13

9

7

5

4

WC cycle (ex-cash) (days)

187

210

193

210

218

November 18, 2015

11

Navneet Education | Education

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Navneet Education

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 18, 2015

12