Initiating coverage | Chemical

March 27, 2017

Navin Fluorine International

BUY

CMP

`2,957

The unique chemistry of growth

Target Price

`3,650

Navin Fluorine (NFIL), part of the Arvind Mafatlal group, is a leader in fluorine

Investment Period

12 Months

based chemicals in India. It operates mainly in four segments i.e. Refrigerant,

Organic Fluoride, Specialty Chemicals and CRAMs. While Refrigerant segment

Stock Info

will continue to generate strong cash flows, the incremental focus of the company

is the high margin and scalable specialty chemicals and CRAMs business. While

Sector

Commodity Chemicals

the contribution from the JV with Piramal group is expected to commence from

Market Cap (` cr)

2,900

FY2018 onwards, NFIL has also entered into supply and technology licenses

Beta

0.9

agreement with Honeywell to produce next generation automobile refrigerant.

52 Week High / Low

3012/1592

Judicious capital allocation has been a key differentiator of NFIL: NFIL received

Avg. Daily Volume

5,475

~`400cr from sales of carbon credit over FY2011-13, while part of that was used

Face Value (`)

10

to repay debt & one-time dividend, the management chose to diversify the

BSE Sensex

29,421

remaining funds in valued added business like CRAMs. This gave an entry to NFIL to

Nifty

9,108

global Pharma and Agro chemical companies. With gradual phase out of Refrigerant,

the move was in right direction which is paying off now in the form of high growth.

Reuters Code

NAFL.BO

Increasing share of high valued added business like Speciality Chemicals &

Bloomberg Code

NFIL@IN

CRAMS should be margin accretive: NFIL’s business mix has changed favorably

over the last few years and share of value added products, specialty chemicals

and CRAMs has gone up from 41% in FY2013 to 51% in FY2016, we expect this

Shareholding Pattern (%)

to further go up to 60% by FY2019, which we believe will be margin accretive for

Promoters

38.7

the company. Its EBITDA margin has increased from 13% in FY2013 to 18.5% in

MF / Banks / Indian Fls

21.9

FY2016 and we believe this has further scope to improve to 22% by FY2019.

FII / NRIs / OCBs

11.8

JV with Piramal Enterprises a win-win situation for both: NFIL (49%) & Piramal

Indian Public / Others

27.7

Enterprises

(51%) entered into a JV in 2014 to manufacture Specialty Fluorine

Chemicals targeted at healthcare segment. The JV with an investment of `140cr is

likely to start contributing from FY2018 onwards. The JV with Piramal is a

Abs.(%)

3m 1yr 3yr

testimony to NFIL’s capability of handling the complex fluorine molecules, while

Sensex

12.6

15.8

34.8

being strategically fit it is a win-win situation for both the players.

NFIL

15.9

68.0

910.0

Improvement in RoCE a result of low debt and strong cash flows: NFIL has been

generating strong cash flows, as a result, which it is able to fund its capex via

internal accruals (negligible debt equity) leading to strong return ratios. The RoCE

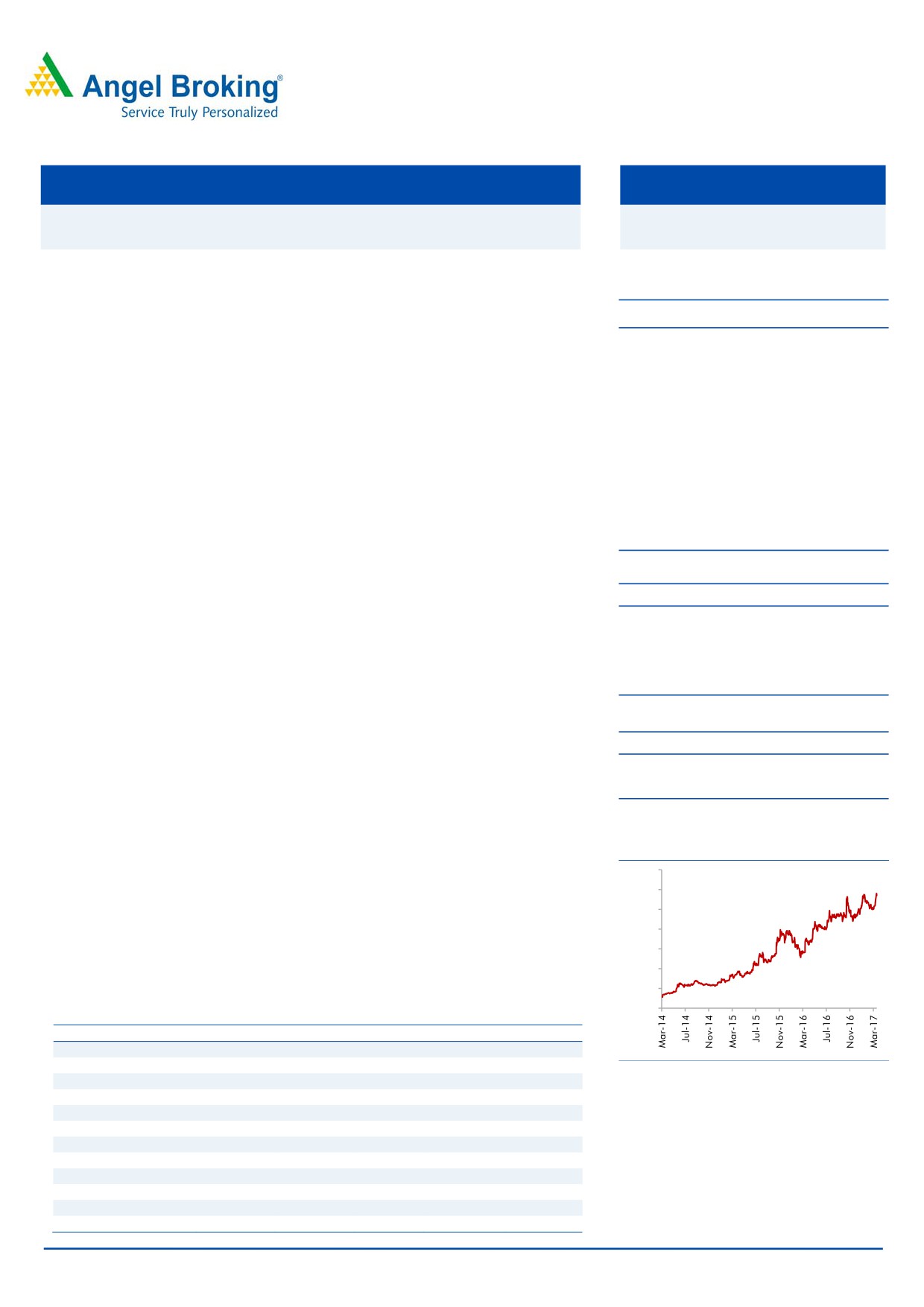

3-year price chart

has improved from 9.9% in FY2013 to 14.1% by FY2016 and with increasing

3,500

share of value added products we expect this to touch 22.7% by FY2019.

3,000

Outlook and Valuation: NFIL’s presence in the high margin, scalable business

2,500

with strong entry barriers makes it a unique player in the Indian specialty

2,000

chemical industry. At the CMP, the stock is trading at 17x its FY2019E EPS and

1,500

10.1x EV/EBITDA. We believe NFIL would continue to attract premium valuations

1,000

due to the long term growth visibility. We have valued the stock at 21x its FY2019E

500

EPS and recommend BUY on the stock with 12 months target price of `3,650.

0

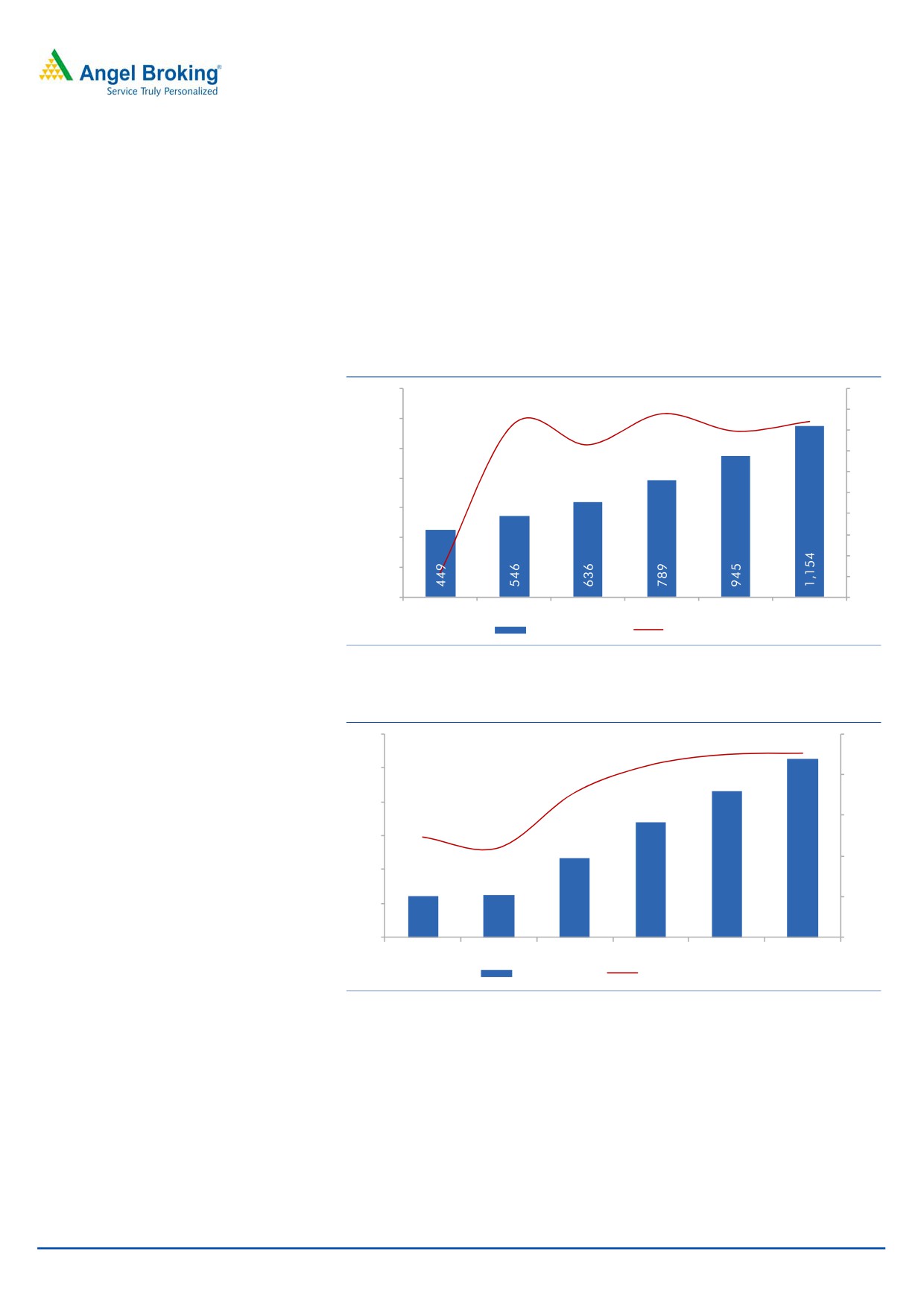

Key Financials (Consolidated)

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

Net Sales

546

636

789

945

1,154

% chg

21.6

16.5

24.0

19.8

22.1

Source: Company, Angel Research

Net Profit

49

86

118

140

170

% chg

(2.5)

75.1

35.9

19.4

21.2

OPM (%)

11.0

17.8

21.1

22.4

22.6

EPS (`)

50.6

88.4

120.1

143.4

173.8

P/E (x)

58.4

33.5

24.6

20.6

17.0

P/BV (x)

5.1

4.6

4.0

3.4

2.9

RoE (%)

8.9

14.4

17.2

17.8

18.5

RoCE (%)

7.0

14.1

19.3

21.3

22.7

Siddharth Purohit

EV/Sales (x)

5.3

4.6

3.6

2.9

2.3

022 - 3935 7800 Ext: 6872

EV/EBITDA (x)

46.1

25.0

16.7

12.9

10.1

Source: Company, Angel Research; Note: CMP as of March 24, 2017

Please refer to important disclosures at the end of this report

1

Initiating coverage | Navin Fluroine

Company background

Navin Fluorine International Ltd (NFIL), part of the Arvind Mafatlal Group is one of

the largest manufacturers of Specialty Fluorochemicals in India. With nearly

5 decades of expertise NFIL has evolved over the years and has now got into high

margin and scalable business like specialty chemicals and CRAMs. The company’s

manufacturing facilities are located at Surat in Gujarat and Dewas in Madhya

Pradesh. The primary business of the company can be dividend into the following

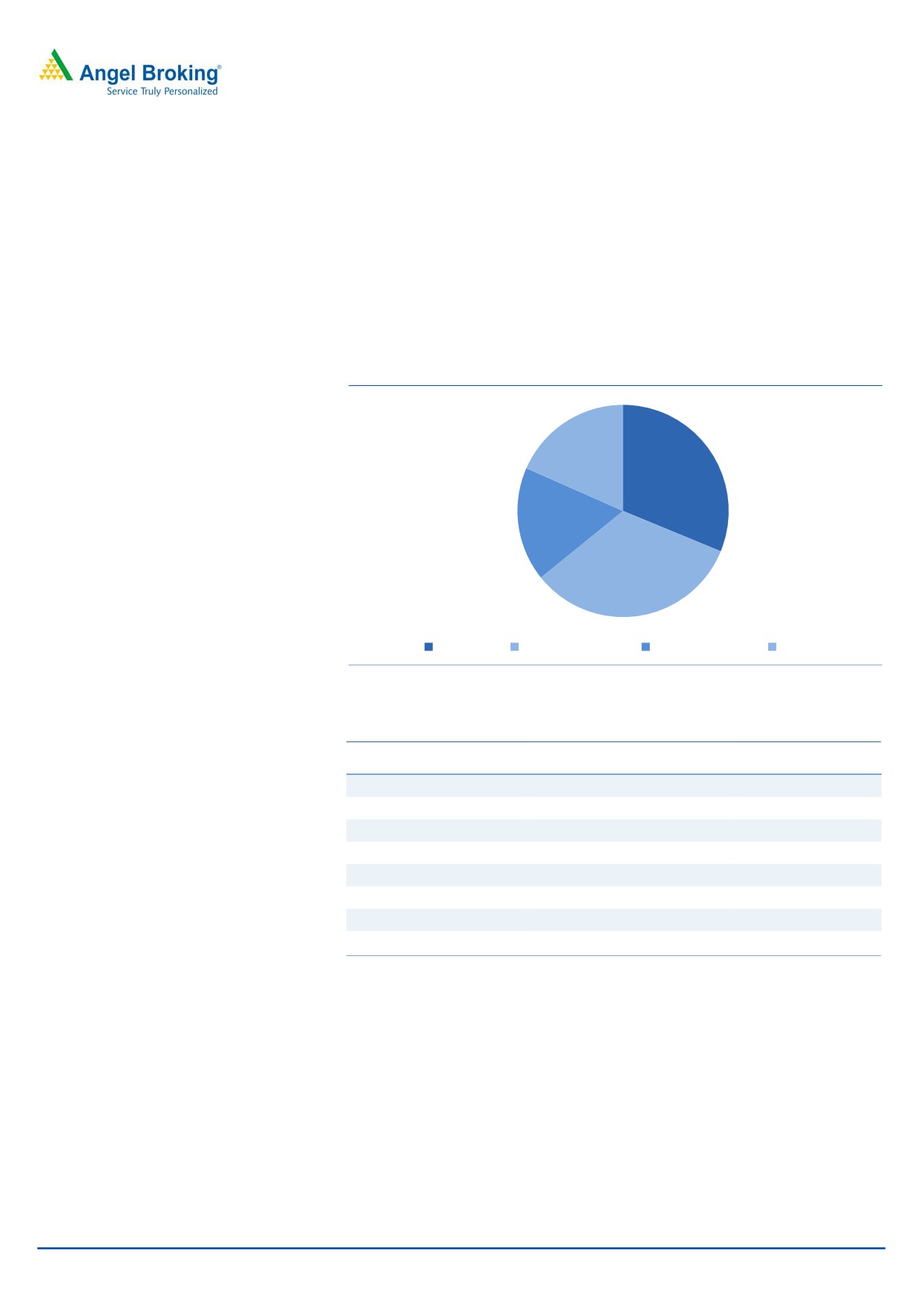

four segments - Refrigerant, Specialty Chemicals, Inorganic Fluoride, and CRAMs.

Exhibit 1: Segmental Revenue Contribution (%)

18

31

17

33

Refrigerent

Speacity Chemicals

Inorganic Flouride

CRAMs

Source: Company, Angel Research

Exhibit 2: Marquee Client Base

Specialty Chemicals &

Pharma Segment

Refrigerant Segment

Agro Chemicals

SUN Pharmaceuticals

CLRIANT

SAMSUNG

LUPIN

BAYER

VOLTAS

Orchid Pharma

SYNGENTA

BLUE STAR

HETERO

BAYER Crop Science

CARRIER

NOVARTIS

DUPONT

LG

Dr Reddy's

BASF

ROCHE

Aurobindo

Source: Company, Angel Research

Key management Personnel:

Mr Shekhar S Khanolkar - Managing Director -Mr Khanolkar has been the MD of

NFIL, since Jan,2011. He served as President of Fluorochemicals segment at NFIL

from Nov-2008 to Jan-2011. Backed by strong qualifications, BE -Chemical and

Masters from Harvard Business School, he has been instrumental behind the

growth of the company.

March 27, 2017

2

Initiating coverage | Navin Fluroine

Exhibit 3: Business Segment

Refrigerant

Specialty Chemicals

Inorganic Fluorides

CRAMs

Fluorine based

Key Products Refrigerant Gas- Viz

Aluminum Fluoride

Contract Research &

Intermediates

Manufacturing of

R-22,R-22 (PTFE Grade),

Ammonium Bi-Fluoride

fluorine based compounds

HFC-134a

Anhydrous Hydrofluoric

Air Conditioning and

Pharmaceutical &

User Industry

Pharma & Agrochemicals

Steel, Aluminum, Glass

Refrigeration

Agro Chem companies

Entry Barriers High

Very High

Low

Very High

Profitability

High

High

Low

Very High

Lowering of Quota and

Longer than expected slowdown

Prolonged slowdown in

Delayed off take

Risk

Early Phase out R-22 gas

in global agrochem business

user industry

from clients

Source: Company, Angel Research

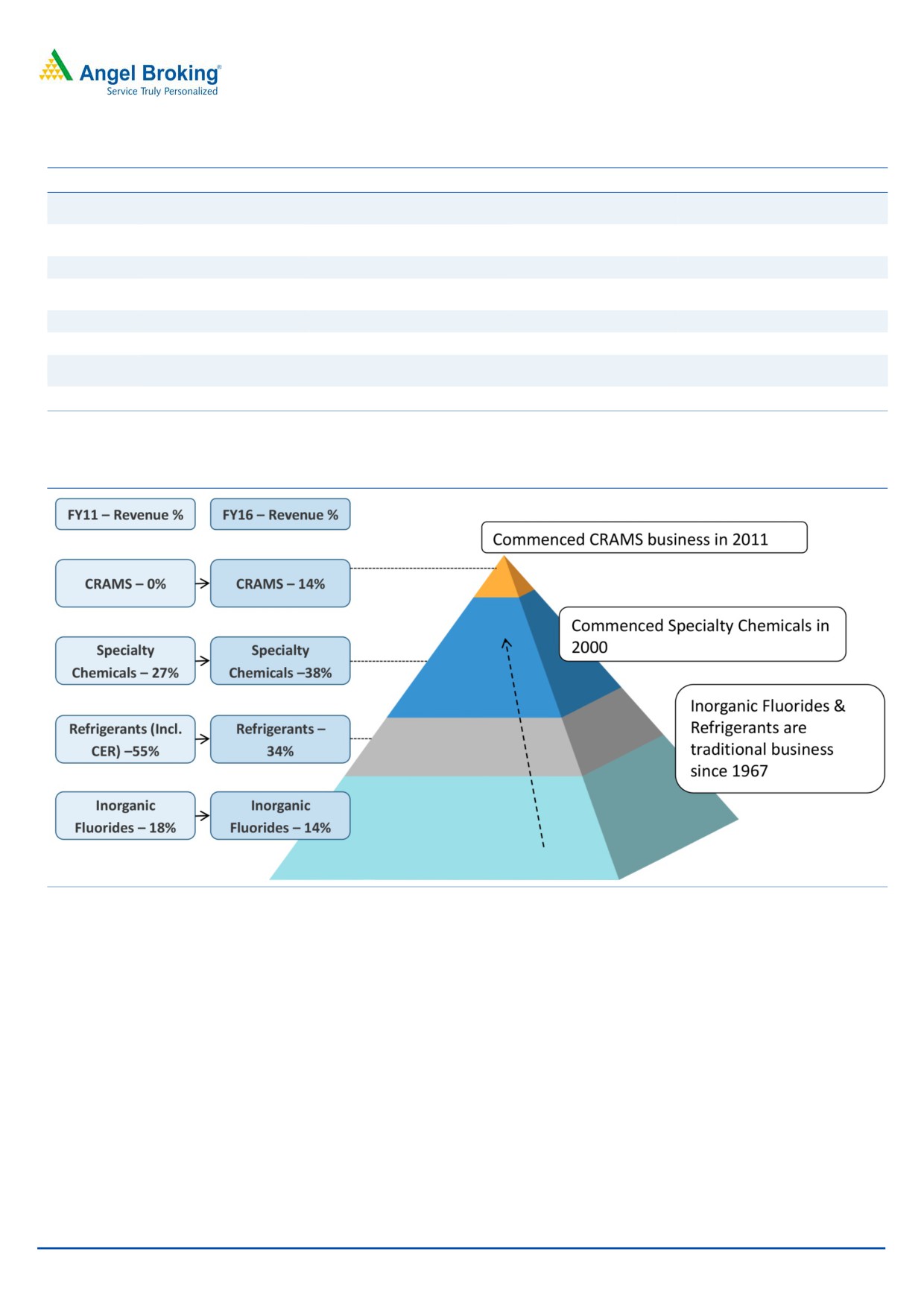

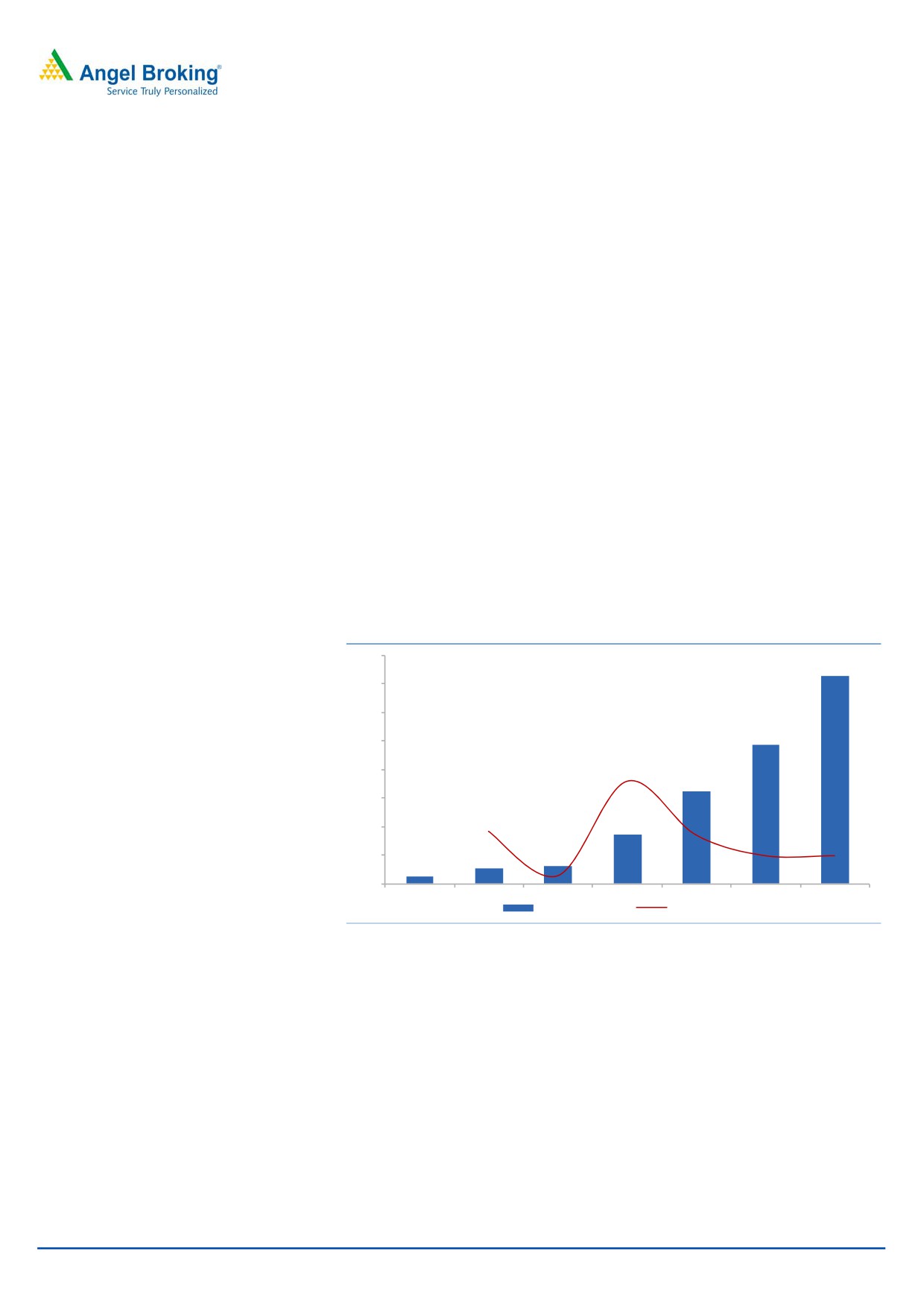

Exhibit 4: Higher Incremental business from valued added segment

Source: Company, Angel Research

March 27, 2017

3

Initiating coverage | Navin Fluroine

Investment Rationale

Judicious capital allocation has been a key differentiator of NFIL: NFIL received

~`400cr from sales of carbon credit over FY2011-13, and taking a proactive

decision the management chose to diversify by deploying funds in in valued added

business like CRAMs. This gave an entry to NFIL to global Pharma and Agro

chemical companies. With gradual phase out of Refrigerant, the move was in right

direction which is paying off now in the form of high growth. While there are other

players also in the Fluorinated chemical business, they do also have sizeable

operations in segments which are not necessarily related to each other. While in

case of NFIL all the segments of business are related to fluorine based molecules

and it has not gone into unrelated diversification. Further the organizations

strategy is to focus and deploy more incremental capital towards the high value

added segment.

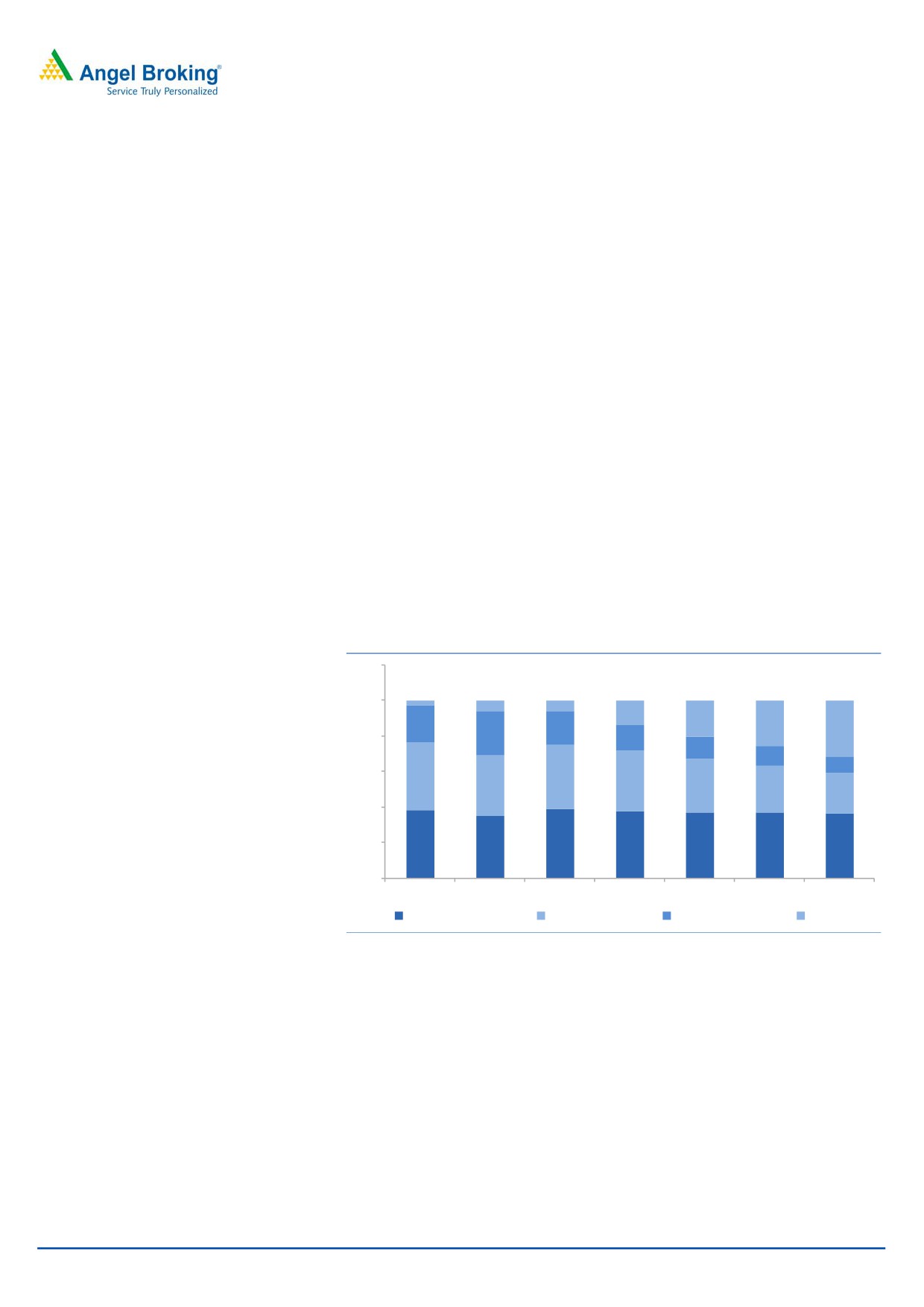

Increasing share of high valued added business should be margin accretive:

NFIL’s business mix has changed favorably over the last few years and share of

value added products, specialty chemicals and CRAMs has gone up from 41% in

FY2013 to 51% in FY2016, we expect this to further go up to 60% by FY2019,

which we believe will be margin accretive for the company. Its EBITDA margin has

increased from 13% in FY2013 to 18.5% in FY2016 and we believe this has

further scope to improve to 22% by FY2019.

Exhibit 5: Favourable change in business mix

120

100

3

6

6

14

21

21

26

19

32

80

25

15

13

11

9

60

38

36

34

34

30

26

23

40

20

38

35

39

38

37

37

36

0

FY13

FY14

FY15

FY16

FY17E

FY18E

FY19E

Speciality Chemicals

Refrigrant Gases

Inorganic Flouride

CRAMS

Source: Company, Angel Research

March 27, 2017

4

Initiating coverage | Navin Fluroine

Joint Venture with Piramal Enterprises a win-win situation for

both

NFIL and Piramal Group entered into a JV in 2014 in which NFIL holds 49% and

Piramal holds 51%. The JV will focus exclusively on Specialty Fluorine Chemicals

targeted at healthcare segment. The JV will invest `140cr and the project is on

schedule and is likely to start contributing from FY2018 onwards. The JV with

Piramal is a testimony to NFIL’s capability of handling the complex fluorine

molecules. We believe the JV is strategically fit and a win-win situation for both the

players, as NFIL will focus on the production and is assured of 100% product off

take by Piramal Enterprises. The Greenfield plant is being set up at NFIL’s land at

Dahej, which the company has leased out to the JV.

Exhibit 6: Key Highlights of the Joint Venture

Piramal Enterprises - 51% stake

Navin Fluorine -49% stake

JV Entered in 2014, to start commercial production by FY18

Investment of JV- `140 cr

Piramal’s pharma arm to buy out the entire output from the JV

NFIL to supply raw materials to the JV at arm lengths price

Source: Company, Angel Research

Recent partnership with Honeywell is another testimony of NFIL’s

ability to handle complex fluorine chemistry:

Recently, NFIL entered into a supply agreement and technology license with

Honeywell to produce Honeywell Solastice yf, an automobile refrigerant with a

lower global warming quality. Under the agreement, Honeywell will license its

proprietary process technologies to produce the refrigerant to Navin Flourine,

which will manufacture Solastice yf in India, exclusively for Honeywell.

Solastice yf, also known as HFO-1234yf is a next generation hydrofluro-olefin

(HFO) refrigerant that is a near drop in replacement for R-134a. R-134a is a HFC

with a global warming potential of 1300, which is used in vehicle air-condition

systems globally. Solastice yf is also being used in a growing number of stationary

air conditioning and commercial refrigeration applications.

March 27, 2017

5

Initiating coverage | Navin Fluroine

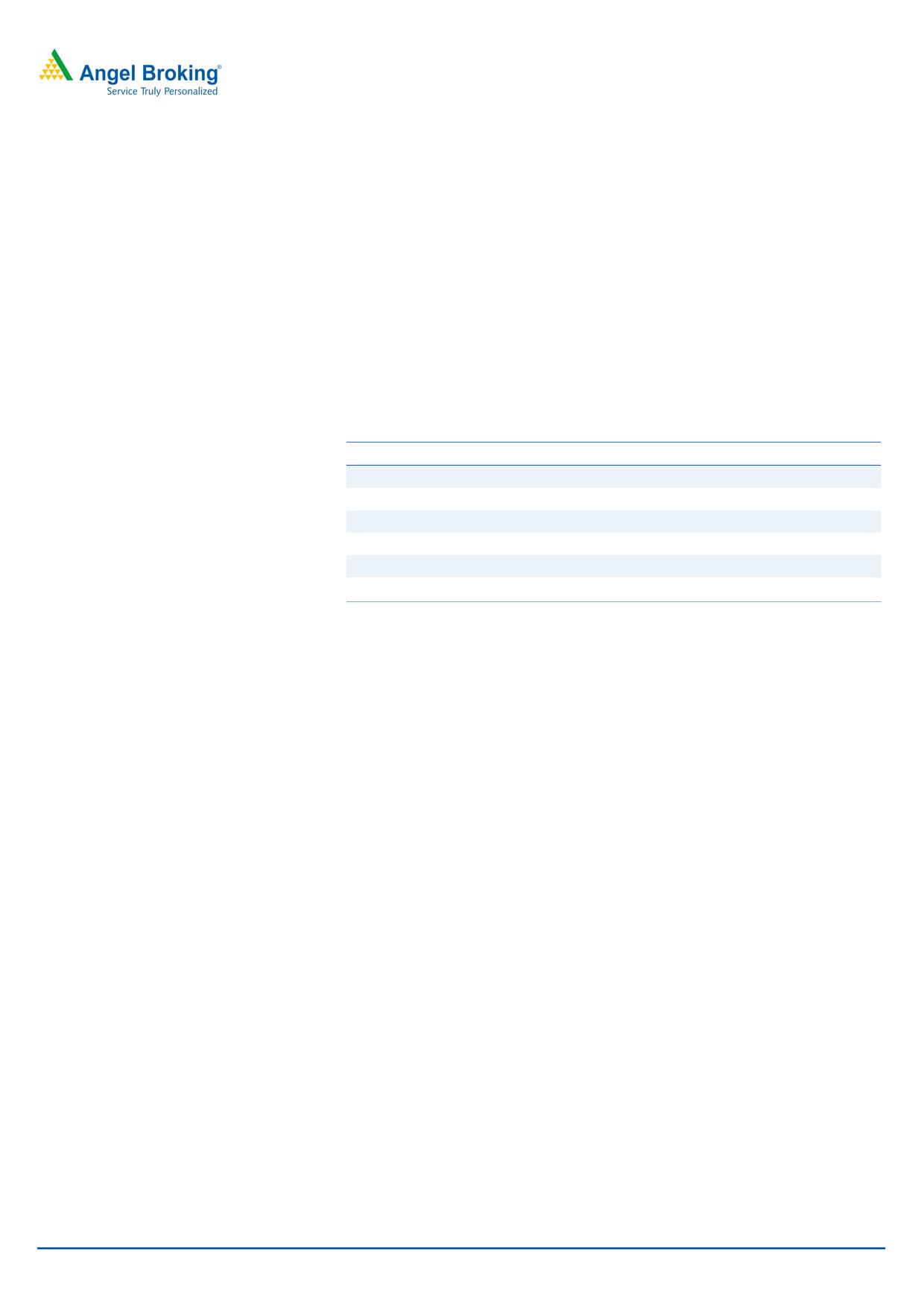

Refrigerant business unlikely to see de-growth in the near term

NFIL started the refrigerant business in

1967 and has a fully integrated

manufacturing facility for developing R22 gas. A backward integrated facility to

produce critical intermediaries like Sulphuric acid and Hydrofluoric acid has

ensured uninterrupted production of the refrigerant gas. NFIL sells its refrigerant

under the brand name of Mafron, which has become a generic name for

refrigerant in India over the years.

Exhibit 7: Steady revenue from refrigerant segment

300

30

26

25

250

20

15

200

11

10

10

150

5

5

5

0

100

(5)

(10)

50

(13)

(15)

177

154

194

215

237

248

261

0

(20)

FY13

FY14

FY15

FY16

FY17E

FY18E

FY19E

Refrigrant Gases (` cr)

% YoY Growth

Source: Company, Angel Research

As per the Montreal protocol, the phase out of HFC refrigerants of which R22 is the

most important has begun. In Europe, the phase out of R22 has already been

accomplished while the US will stop using R22 in 2020. In developing countries

the phase out had started in 2015 and will get over in 2030. With strict quota

restriction, we don’t expect any volume growth to come from the refrigerant

segment for NFIL. However, production cut down and effective demand supply

mismatch will ensure better price realization, and hence, the segment is likely to

remain steady cash flow for multiple years now. While R22 is being phased out for

refrigeration, there is no restriction on its use in Pharma sector as a feed stock and

this should compensate the decline in volume from other segments.

Exhibit 8: Geographical bifurcation of Refrigerant business

120

100

32

32

32

30

80

38

60

40

68

68

68

70

62

20

0

FY13

FY14

FY15

FY16

9mFY17

Domestic (%)

Exports (%)

Source: Company, Angel Research

March 27, 2017

6

Initiating coverage | Navin Fluroine

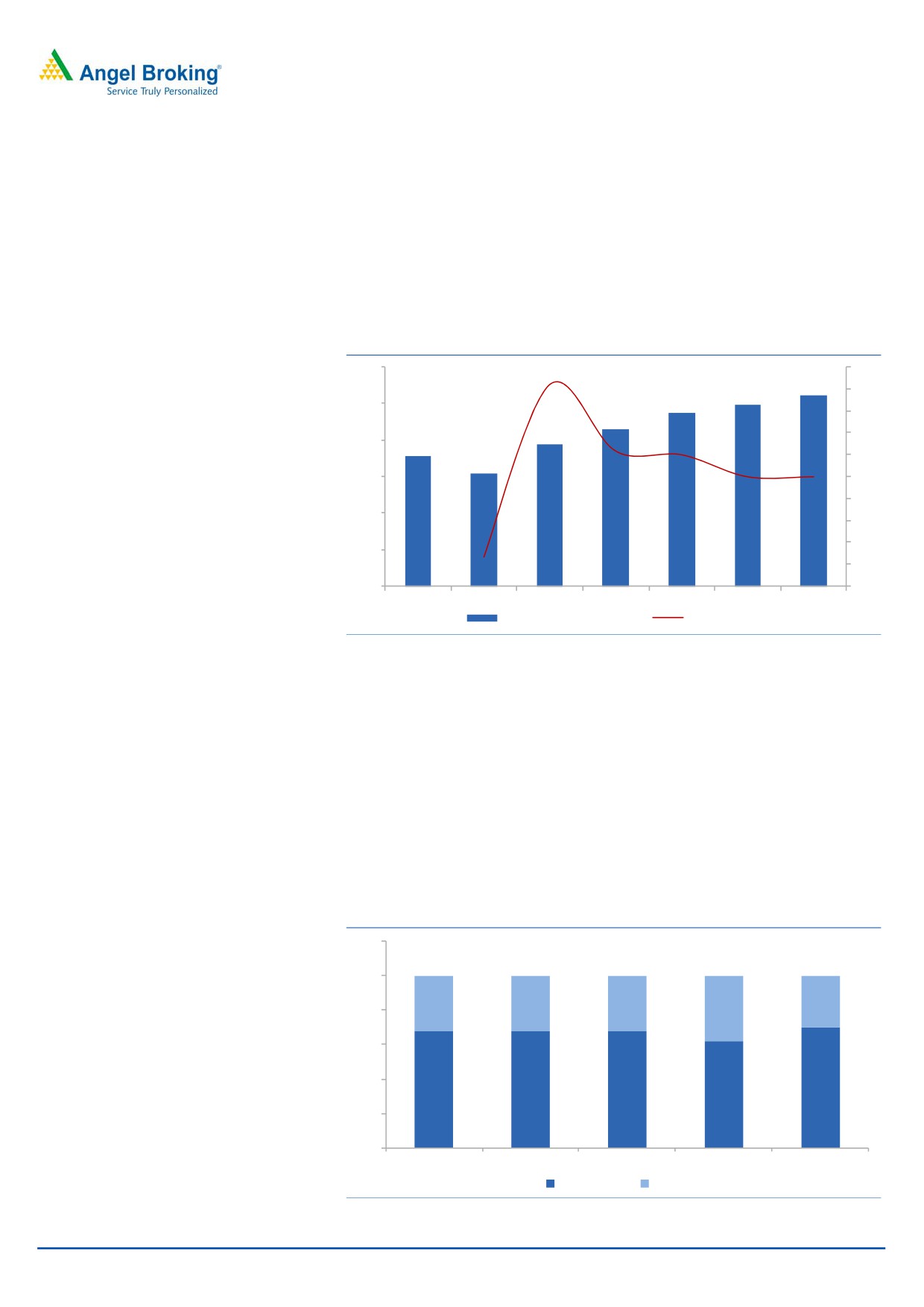

Specialty chemicals will continue to see increased traction: NFIL entered into

specialty chemicals business in 2000. This segment offers high scalability with

significant entry barriers. NFIL has dedicated multipurpose plants to process multi

step products and intermediates, which are high in the value chain. In this

segment, NFIL primarily supplies to the Pharmaceutical and Agrochemical

companies. In addition to the above industries, NFIL’s specialty chemicals also find

application in the Hydrocarbon and Fragrance segments to some extent.

Exhibit 9: Sustainable growth in Speciality Chemical segment

450

50

400

37.8

40

350

22.0

30

300

250

11.2

20

20.0

20.0

200

10

150

0

100

-12.09

(10)

50

177

156

215

239

292

350

420

0

(20)

FY13

FY14

FY15

FY16

FY17E

FY18E

FY19E

Speciality Chemicals (` cr)

% YoY Growth

Source: Company, Angel Research

The Specialty Chemicals supplied by NFIL are of low volume but high value in

nature. Although as a percentage of total input cost it might be low for the user,

but carries high importance, and that is the major reason for strong client

relationship of high repute for NFIL. The revenue from this segment has reported a

10.4% CAGR over FY2013-16. With global agrochemical industry going through a

phase of slow down the growth for NFIL has also been moderate. However, there

is trend of higher contribution from the exports business, which should be margin

accretive for the company.

Exhibit 10: Increasing share of exports in Speciality Chemicals

120

100

36

32

80

43

46

60

40

64

68

54

57

20

0

FY14

FY15

FY16

9mFY17

Domestic (%)

Exports (%)

Source: Company, Angel Research

March 27, 2017

7

Initiating coverage | Navin Fluroine

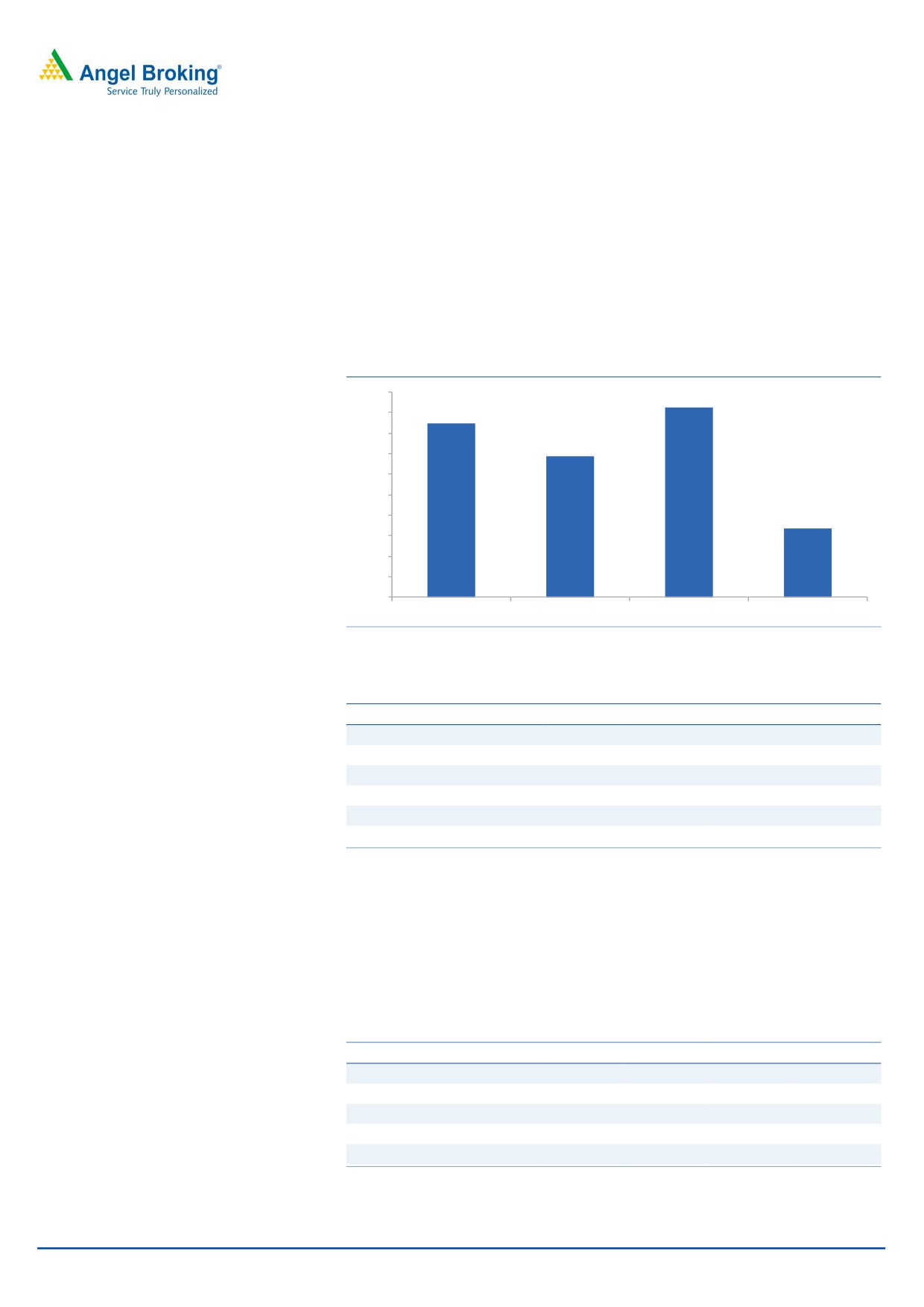

Inorganic fluoride segments growth will depend on the user

industries like Aluminum & Steel

The various inorganic fluorides like - Ammonium BiFluoride, Potassium Fluoride,

Sodium Fluoride supplied by NFIL find application in sectors like Aluminum Steel

and Glass production. Due to slow down in the user industry, the revenue from this

segment has remained muted over the years. These set of products being

commoditized in nature generally have relatively lower margins v/s. other products

of the company.

Exhibit 11: Subdued growth in Inorganic Fluoride ( Revenues ` cr)

120

113

109

105

104

98

99

100

94

80

60

40

20

0

FY13

FY14

FY15

FY16

FY17E

FY18E

FY19E

Source: Company, Angel Research

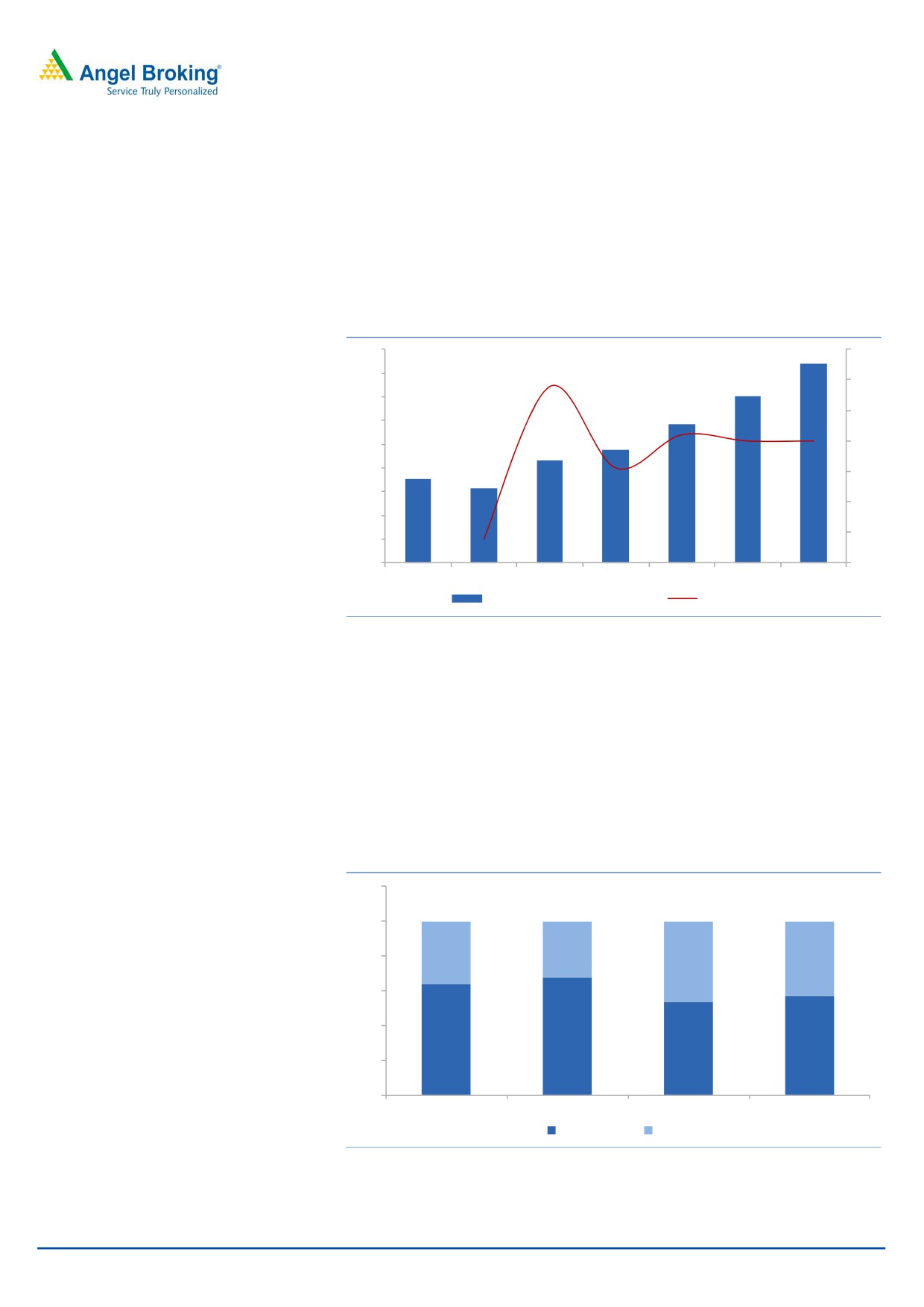

NFIL has been upgrading itself via continuous focus on R&D

While the traditional business of NFIL like Refrigerant and Inorganic Fluoride are

high volume business and doesn’t need major R&D. The new areas of business

which NFIL is actively pursuing are Specialty Chemicals and CRAMs, which need a

lot of R&D, hence NFIL has been spending higher amount on it every year.

Exhibit 12: Increasing share of R&D Expenses

25

4

3.0

3

20

2.3

3

15

1.8

2

1.6

2

10

1

5

1

8.2

7.2

12.4

19.2

0

0

FY13

FY14

FY15

FY16

R&D Expenses

R&D Expenses as % of Total Revenues

Source: Company, Angel Research

March 27, 2017

8

Initiating coverage | Navin Fluroine

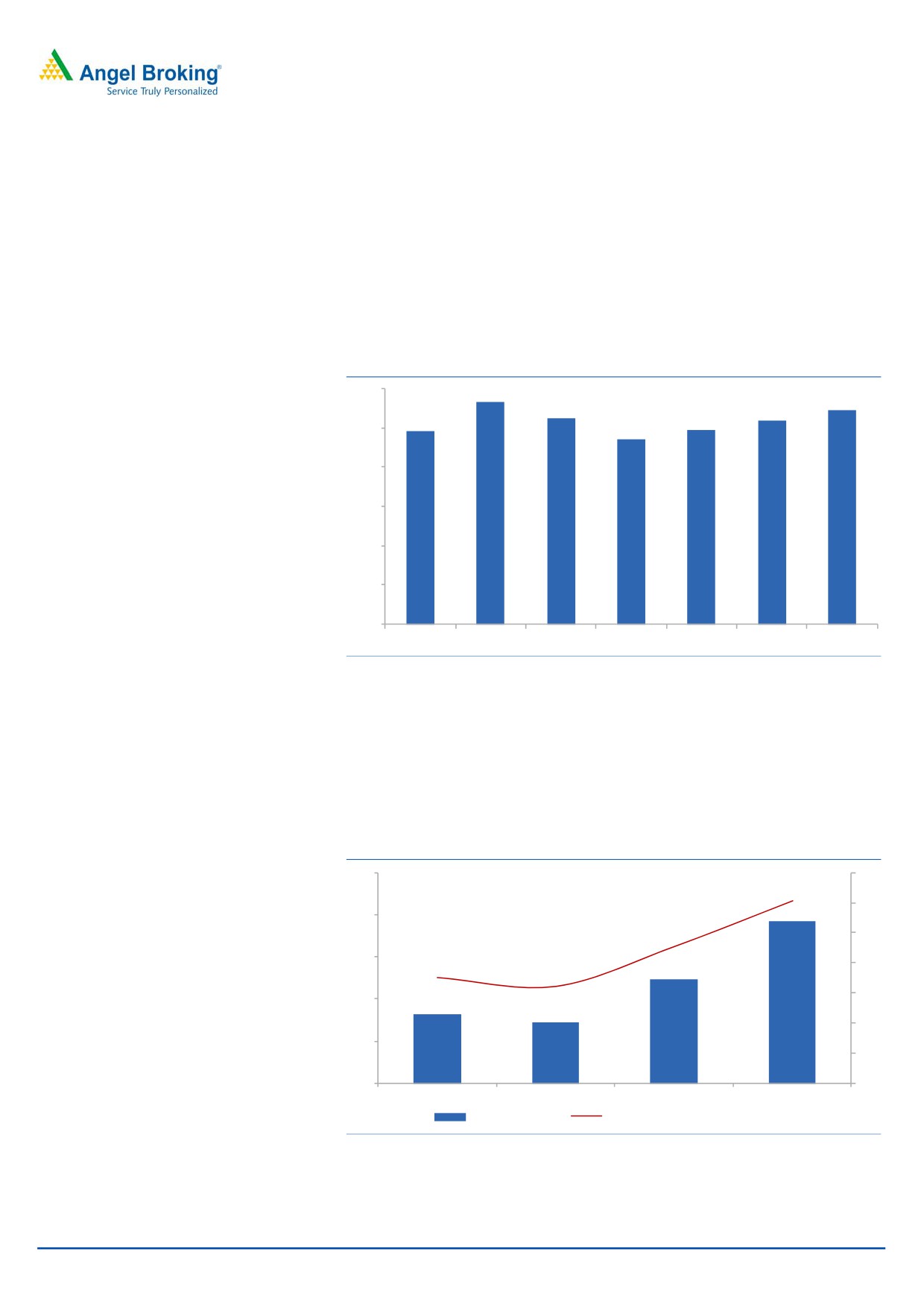

CRAMs will be the growth engine, Dewas plant to have high

asset turn over:

NFIL got a windfall gain of ~`400cr via sale of carbon credit and part of this was

used for starting the high margin and scalable Contract Research and

Manufacturing Services business. In order to make its presence felt in the global

markets the company acquired 51% stake in the UK based Manchester Orgaincs

Ltd, though small in size MOL is a highly specialized chemical research company.

The Company invested `65cr to set up a multipurpose plant. The plant with high

efficiency can operate at 2.5x-3x asset turn over at the peak level. After going

through various phases of customer audits, the plant started commercial

production in FY2016. Being the first cGMP compliant pilot plant for developing

high pressure fluorination, NFIL got access to global innovative Pharma companies

via this plant. The Dewas plant will help in growing the CRAMs business in the

years to come.

NFIL started the CRAMs business in 2011 and within a span of 5 years the share of

CRAMs in total business has gone up to 14% in FY2016. With increasing clients

mining, we expect the share of this increase upto 30% by FY2019. CRAMs is high

margin business with high entry barriers, but it also takes time to go through

various approval processes and build a scalable business.

Exhibit 13: High growth in CRAMS segment

400

365

350

300

243

250

200

162

181

150

87

100

93

86

50

27

31

50

50

14

15

0

CRAMS (` cr)

% YoY Growth

Source: Company, Angel Research

March 27, 2017

9

Initiating coverage | Navin Fluroine

Efforts for securing long term raw material sourcing to reduce

margin volatility:

NFIL’s margin is highly dependent on the movement of the raw material prices.

However, with higher contribution from the new business segments like Specialty

Chemicals and CRMAs, the correlation of price movement of input costs and

margins will reduce gradually. In the last few quarters, the cost of key raw

materials like Sulphur, Fluorspar, Chloroform & Boric Acid have seen downward

trend.

Exhibit 14: Raw materials as % of sales

48.0

47.6

47.5

47.2

47.0

46.4

46.5

46.0

45.5

45.0

44.7

44.5

44.0

43.5

43.0

FY13

FY14

FY15

FY16

Source: Company, Angel Research

Exhibit 15: Mix of Various Raw materials

As % of Total Raw materials

FY13

FY14

FY15

FY16

Fluorspar

36%

35%

26%

22%

Chloromethanes

11%

7%

14%

13%

Spor 11

7%

7%

5%

6%

Sulphur

6%

6%

7%

5%

Others

41%

44%

47%

54%

Total

100%

100%

100%

100%

Source: Company, Angel Research

Fluorspar is one of the key raw materials for the company, which is imported from

diverse regions. However, in order to secure long term availability of this key raw

material, the company has entered into a JV with GMDC in which NFIL holds 25%

stake. The JV is expected to supply fluorspar ore for further beneficiation from GMDC

mines. The JV is likely to start commercial production from FY2018 onwards.

Exhibit 16: Raw materials Mix

(` Cr)

FY13

FY14

FY15

FY16

Imported

184

140

174

173

Indigenous

63

69

110

87

Total

248

209

284

260

Imported

74%

67%

61%

67%

Indigenous

26%

33%

39%

33%

Source: Company, Angel Research

March 27, 2017

10

Initiating coverage | Navin Fluroine

Expect Revenues /EBITDA / PAT to report 20%/30%/24% CAGR

over FY2016-19

NFIL reported a 16.8% growth in revenues in FY16, which has gained further

momentum during the year and we expect it to end FY17 with 24% YoY growth.

Over FY16-19the revenue CAGR is expected to be 22%, with large part of the

incremental growth being driven by the high margin specialty chemical and

CRAMs business. We expect EBITDA to report 31% CAGR over the same period on

the back of higher contribution from CRAMs segment, having better margins.

Exhibit 17: Revenue Growth

1,400

30

24.0

21.6

22.1

25

19.8

1,200

16.5

20

1,000

15

10

800

5

600

(14.4)

0

400

(5)

(10)

200

(15)

-

(20)

FY14

FY15

FY16

FY17E

FY18E

FY19E

Net Sales (` cr)

% Growth YoY

Source: Company, Angel Research

Exhibit 18: EBITDA & EBITDA Margin % Trend

300

22.4

22.6

25.0

21.1

264

250

17.8

215

20.0

200

170

15.0

12.3

11.0

150

116

10.0

100

61

63

5.0

50

0

0.0

FY14

FY15

FY16

FY17E

FY18E

FY19E

EBITDA (` cr)

EBITDA Margin (%)

Source: Company, Angel Research

March 27, 2017

11

Initiating coverage | Navin Fluroine

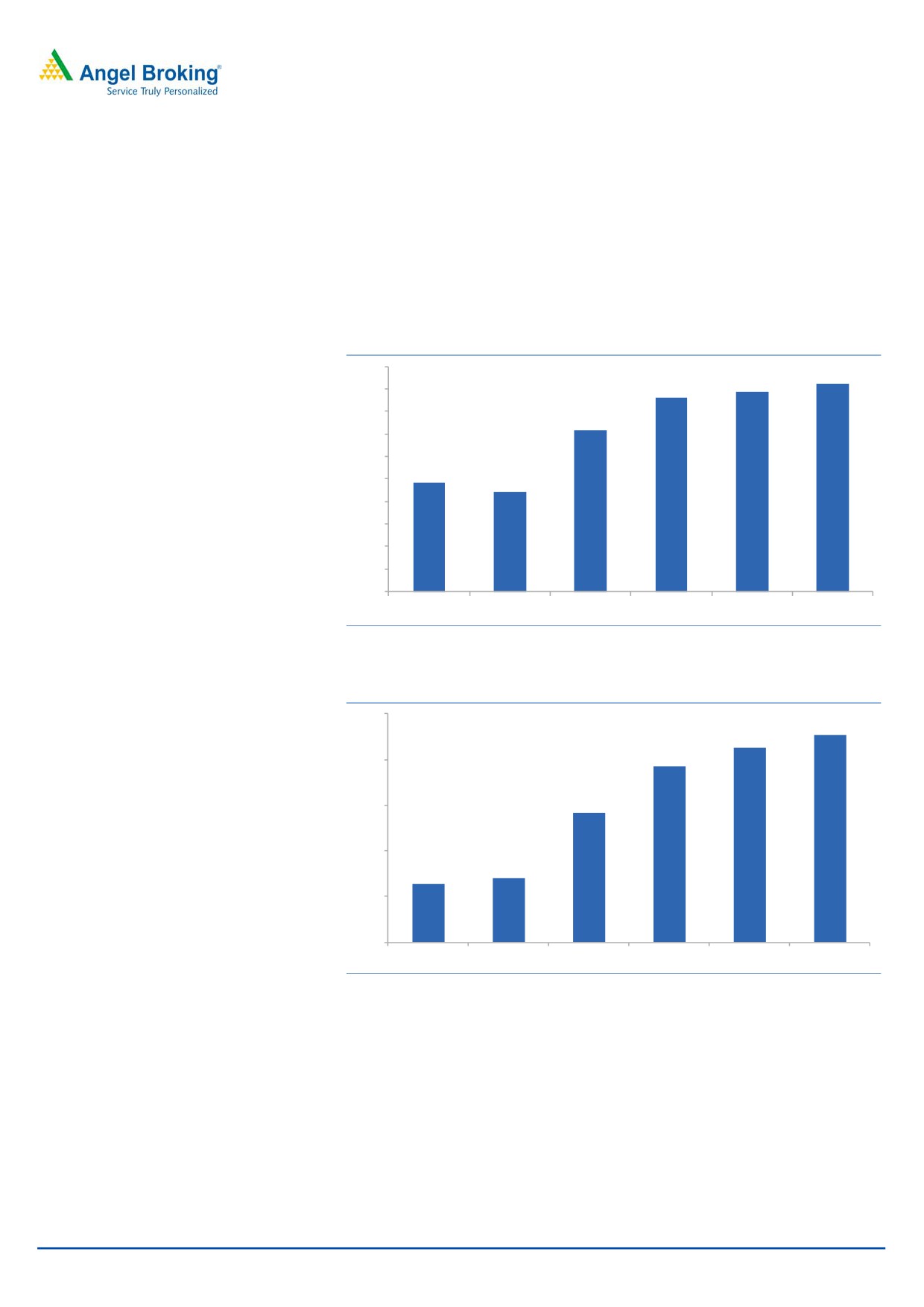

Low debt and strong cash flows has resulted in sharp

improvement in RoCE

NFIL has been generating strong cash flows, as a result of which it is able to fund

its capex via internal accruals, and hence the debt equity is at 0.2x, leading to

strong return ratios. The RoCE has improved from 9.9% in FY2013 to 14.1% by

FY2016 and with increasing share of value added products we expect this to touch

22.7% by FY2019.

Exhibit 19: ROE% has been improving

20.0

18.5

17.8

17.2

18.0

16.0

14.4

14.0

12.0

9.6

10.0

8.9

8.0

6.0

4.0

2.0

0.0

FY14

FY15

FY16

FY17E

FY18E

FY19E

Source: Company, Angel Research

Exhibit 20: See further improvement in ROCE %

25.0

22.7

21.3

19.3

20.0

14.1

15.0

10.0

7.0

6.4

5.0

0.0

FY14

FY15

FY16

FY17E

FY18E

FY19E

Source: Company, Angel Research

March 27, 2017

12

Initiating coverage | Navin Fluroine

Exhibit 21: Key Assumptions

Segmental Revenues (` Cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

FY19E

Specialty Chemicals

177

156

215

239

292

350

420

Refrigerant Gases

177

154

194

215

237

248

261

Inorganic Fluoride

98

113

105

94

99

104

109

CRAMS

14

27

31

87

162

243

365

Total

467

450

545

635

789

945

1,154

Overall Growth % YoY

-

(4)

21

17

24

20

22

Segmental Growth % YoY

Specialty Chemicals

-

(12)

38

11

22

20

20

Refrigerant Gases

-

(13)

26

11

10

5

5

Inorganic Fluoride

-

15

(7)

(10)

5

5

5

CRAMS

-

93

15

181

100

50

50

Revenue Contribution %

Specialty Chemicals

38

35

39

38

37

37

36

Refrigerant Gases

38

34

36

34

30

26

23

Inorganic Fluoride

21

25

19

15

13

11

9

CRAMS

3

6

6

14

21

26

32

Source: Company, Angel Research

Exhibit 22: Favourable Change in Business Mix

Business Segment

Refrigerant

Sp -Chemicals

In- Fluorides CRAMs

Revenue Contribution ( FY11)

55%

27%

18%

0%

Revenue Contribution ( FY16)

34%

38%

14%

14%

Revenue Contribution (FY19E)

25%

32%

13%

30%

Geographic Distribution ( 9MFY17)

Domestic

70%

57%

93%

Exports

30%

43%

7%

100%

CAGR

FY13-16

6%

10%

(1.4%)

84%

FY16-19E

10%

14%

5%

61%

Source: Company, Angel Research

March 27, 2017

13

Initiating coverage | Navin Fluroine

Outlook and Valuation

NFIL’s presence in the high margin, scalable business with strong entry barriers

makes it a unique player in the Indian specialty chemical industry. While other

players like SRF Ltd and Gujarat Fluorochemicals Ltd are also present in the

Fluorine based specialty chemicals, they also do have many other divisions of

operations and this makes NFIL the only company to focus solely on Fluorine

based business. Thus, we believe NFIL will continue to attract premium valuations

due to the long term growth visibility and focused business model. At the CMP, the

stock is trading at 17x its FY2019E EPS and 10.1x EV/EBITDA. We have valued the

stock at 21x its FY2019E EPS and recommend BUY on the stock with 12 months

target price of `3,650.

Key Risks & Concerns

NFIL still derives ~33% of its total revenues from the refrigerant business. The

phase out of R-22 Refrigerant gas for developing countries had started in

2015 and is likely to be phased out completely by 2030. Earlier than expected

and aggressive phase out of the same could impact the business of NFIL.

CRAMs is a high margin business, but the company has to go through multiple

audits and approvals before it gets sizeable business. And any delay in off

take from the customer’s end can result in slow down in business growth.

Growth of the specialty chemicals division depends on growth of the user

industry like Pharma & Agrochemicals. The global Agrochemicals industry is

going through a phase of slow down due to drought in multiple geographies.

Longer than expected delay in recovery could impact the volumes and in turn

margins of NFIL

The company imports nearly 2/3rd of its raw materials from overseas markets

and any adverse movement in raw material prices could hit the profitability.

March 27, 2017

14

Initiating coverage | Navin Fluroine

Consolidated Profit & Loss Account

Y/E March (` cr)

Mar-15

Mar-16

Mar-17E

Mar-18E

Mar-19E

Total Net Sales

546

636

789

945

1,154

% Change

21.6

16.5

24.0

19.8

22.1

Total Raw materials

272

292

333

404

515

Staff costs

61

66

73

81

87

Other Expenditure

150

162

213

246

288

Total Expenditure

483

520

619

730

890

EBITDA

63

116

170

215

264

% Change

4.3

83.4

46.3

26.5

22.6

EBITDA Margin %

11.6

18.3

21.5

22.7

22.8

Depreciation

19

21

26

34

41

EBIT

45

95

144

181

223

% Change

11.2

113.1

50.9

25.9

23.1

EBIT Margin %

8.2

15.0

18.2

19.1

19.3

Interest

3

3

3

3

3

Other Income

27

25

25

20

20

( as % of PBT)

39

21

15

10

8

PBT

68

117

166

198

240

Tax

19

30

48

57

69

Tax Rate %

27

26

29

29

29

APAT

49

86

118

140

170

% Change

(2.5)

75.1

35.9

19.4

21.2

March 27, 2017

15

Initiating coverage | Navin Fluroine

Balance Sheet ( Consolidated)

Y/E March (` cr)

Mar-15

Mar-16

Mar-17E

Mar-18E

Mar-19E

Share Capital

10

10

10

10

10

Reserves & Surplus

561

624

721

838

983

Net Worth

571

634

731

848

993

Total Loan funds

45

30

27

24

22

Deferred Tax Liability

32

36

36

36

36

Capital Employed

648

699

793

908

1,050

Gross Block

422

430

445

460

475

Less: Depreciation

152

163

189

223

264

Net Block

270

267

256

237

211

Investments

234

266

295

328

364

Sundry Debtors

110

138

166

199

239

Cash & Bank Bal

14

15

82

155

253

Loans & Advances

95

81

88

95

103

Inventory

66

63

73

84

98

Other Current Assets

3

3

3

4

5

Total Current Assets

287

300

412

537

697

Current Liabilities

124

125

144

165

190

Sundry Creditors

88

92

106

122

140

Other Creditors

36

33

37

43

50

Provision

20

24

27

29

32

Curr Liab & Prov

144

149

170

194

222

Net Current Assets

143

151

242

343

475

Total Assets

648

699

793

908

1,050

March 27, 2017

16

Initiating coverage | Navin Fluroine

Cash Flow Statement ( Consolidated)

Y/E March (` cr)

Mar-15

Mar-16

Mar-17E Mar-18E Mar-19E

PBT

68

117

166

198

240

Depreciation & Amortization

19

11

26

34

41

Provision for Taxes

(19)

(30)

(48)

(57)

(69)

Chg in Deferred tax

(1)

4

-

-

-

Chg in Working cap

(17)

(7)

(24)

(28)

(34)

Cash flow from operations

50

95

120

146

177

Chg in Gross Block

(58)

(9)

(14)

(15)

(15)

Chg in Investments

28

(32)

(29)

(32)

(36)

Chg in WIP

-

(14)

14

-

-

Cash flow from investing

(29)

(54)

(30)

(47)

(51)

Chg in debt

(12)

(15)

(3)

(3)

(2)

Chg in Net Worth

(2)

(4)

(0)

0

(0)

Dividend

(18)

(20)

(21)

(23)

(25)

Cash flow from financing

Chg in cash

(11)

1

67

73

98

Cash at start

25

14

15

82

155

Cash at end

14

15

82

155

253

March 27, 2017

17

Initiating coverage | Navin Fluroine

Key Ratios

Financial Ratios

2015

2016

2017E

2018E

2019E

Growth (%)

Net Sales

21.6

16.5

24.0

19.8

22.1

EBITDA

4.3

83.4

46.3

26.5

22.6

APAT

(2.5)

75.1

35.9

19.4

21.2

Profitability (%)

EBITDA Margin

11.0

17.8

21.1

22.4

22.6

Adj. PAT Margin

9.0

13.6

14.9

14.9

14.7

ROCE

7.0

14.1

19.3

21.3

22.7

ROE

8.9

14.4

17.2

17.8

18.5

Angel (ROIC)

7.4

14.7

21.3

25.2

29.2

Per Share Data (`)

Adj. EPS

51

88

120

143

174

Adj. CEPS

70

113

147

178

215

BVPS

585

647

747

867

1015

Valuations (X)

PER

58.4

33.5

24.6

20.6

17.0

P/BV

5.1

4.6

4.0

3.4

2.9

EV / EBITDA

46.1

25.0

16.7

12.9

10.1

EV / Net sales

5.3

4.6

3.6

2.9

2.3

Dividend Yield (%)

0.5

0.6

0.6

0.7

0.7

Turnover Days

Asset Turnover ( Gross Block)

1.3

1.5

1.8

2.1

2.4

Inventory days

88

78

80

76

69

Debtors days

74

79

77

77

76

Creditors days

119

115

116

110

100

Working Capital Days

43

42

40

43

45

Gearing Ratio

Total Debt to Equity

0

0

0

0

0

March 27, 2017

18

Initiating coverage | Navin Fluroine

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Navin Fluroine

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

March 27, 2017

19