Initiating coverage | Pharma

March 9, 2017

Natco Pharma

BUY

CMP

`786

Top league player

Target Price

`926

Natco Pharma is a Hyderabad based pharma company with focus on limited

Investment Period

12 Months

competition and high margin products. It has presence in domestic and global

markets and has two main business segments i.e. API and Formulations.

Stock Info

Sector

Pharma

Niche therapeutic play in domestic formulations: In the domestic formulations

business

(57% of revenues), Natco focuses on oncology and Hepatitis C

Market Cap (` cr)

13,397

segments. The oncology segment continues do as market dynamics favor while

Net Debt (` cr)

98

Hepatitis C franchisee is expected to grow by ~20% rate over next couple of years

Beta

0.6

due to huge cost advantage. Owing to this, we expect 24% CAGR in domestic

52 Week High / Low

830/390

formulations over FY16-FY19E.

Avg. Daily Volume

52,582

Export formulations to grow 4.0x in next two years: Natco’s export formulations

Face Value (`)

2

revenue is set to grow at a CAGR of 64% over FY16-FY19E. The company has

BSE Sensex

29,000

already monetized some niche ANDAs in FY17E and a few more ANDAs are due

Nifty

8,947

for launches over next two years. This is expected to see 4.0x growth in export

Reuters Code

NATP NS

formulations by FY19E.

Bloomberg Code

NTCPH IN

Copaxone approval remains a near term trigger: Natco and its marketing partner

Mylan believe that they are the FTF filers on multiple sclerosis drug Copaxone

Shareholding Pattern (%)

40mg (annual sales of $3.3bn). The US District Court has already invalidated

Promoters

51.2

several patents on this drug. The verdict on one of the patents is due by May

2017. A favorable verdict will raise hopes of launching generic Copaxone 40mg.

MF / Banks / Indian Fls

12.2

We believe that Copaxone 40mg is a ~`400-500cr revenues opportunity during

FII / NRIs / OCBs

17.4

180-day period for Natco Pharma.

Indian Public / Others

19.3

Revlimid opportunity significantly big: Natco has settled litigation regarding

multiple myeloma drug Revlimid (US sales of $4.4bn) with its innovator Celgene.

Abs. (%)

3m 1yr 3yr

The company will be able to launch this drug in 2022 and it will certainly be a

Sensex

8.4

17.8

32.2

large opportunity considering the size of the drug.

Natco Pharma

28.4

58.2

349.3

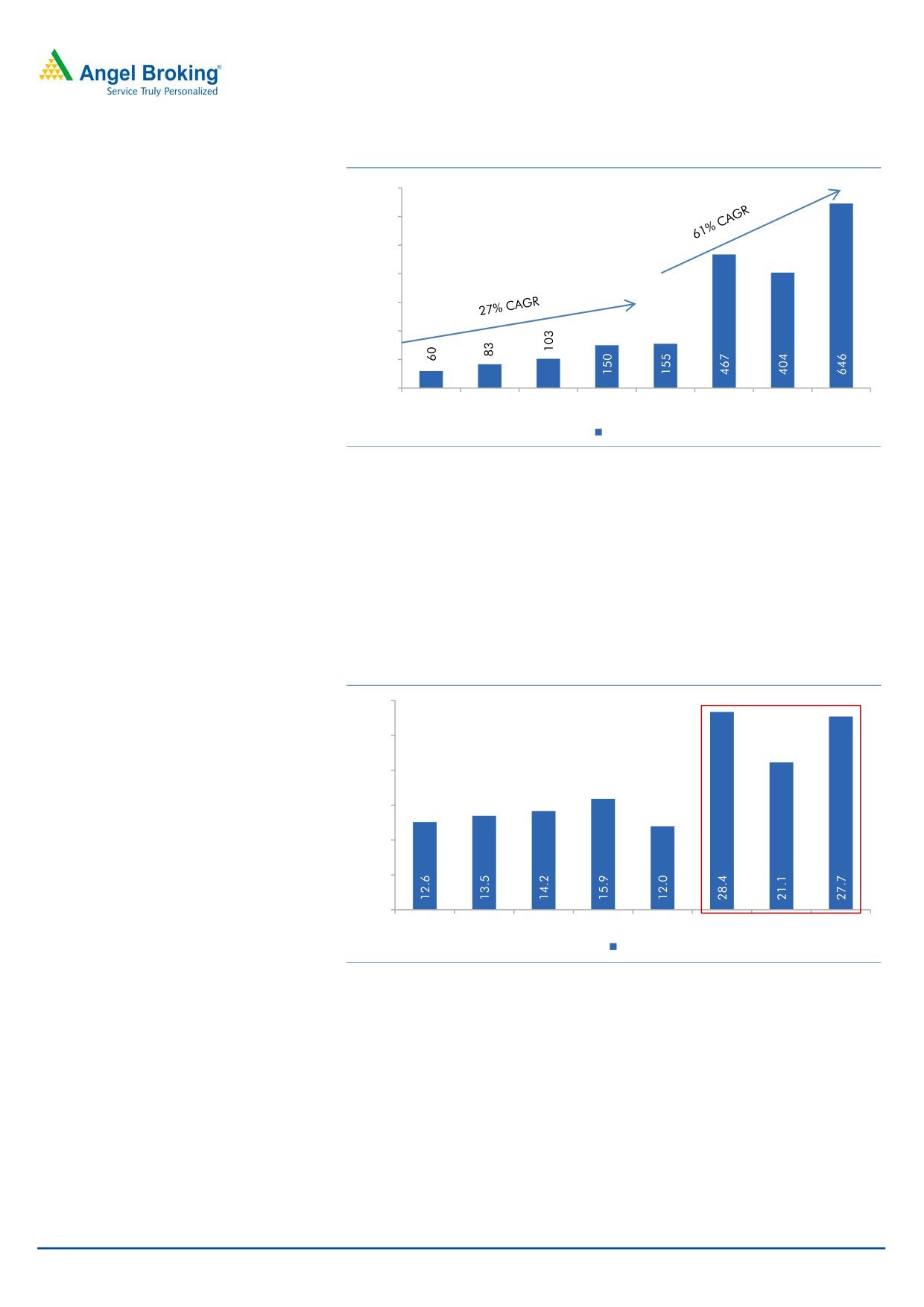

Outlook and Valuation: Natco’s topline and bottomline is set to grow at 36%

and 61% CAGR over FY16-FY19E due to 1) strong performance of domestic

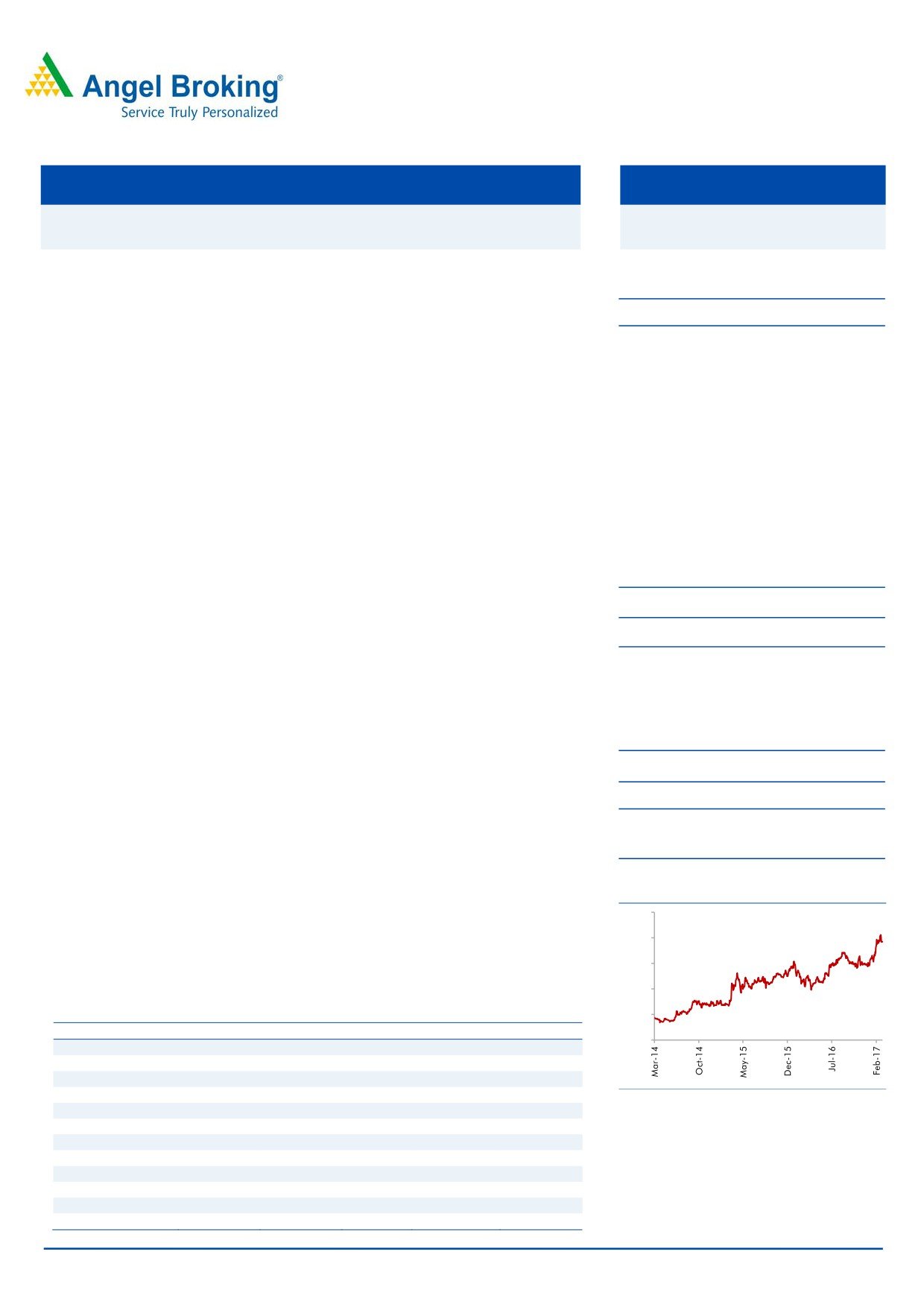

Price Chart

formulations and 2) monetization of high value ANDAs. The stock at the CMP of

1,000

`769 is trading at P/E of 21.2x of FY2019E EPS of `37. This is 15% discount to its

800

3 year average P/E multiple of 26x. We initiate coverage on Natco Pharma with

buy rating and SOTP value of `926 (`890 base on 24xFY19E EPS + Revlimid

600

NPV at `37. ) implying 18% upside from current level.

400

Key Financials (Consolidated)

200

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

0

Net Sales

825

1,142

2,090

2,335

2,869

% chg

11.7

38.3

83.1

11.7

22.9

Net Profit

213

270

670

622

972

% chg

19.0

26.4

148.4

(7.2)

56.3

Source: Company, Angel Research

OPM (%)

25.9

23.6

32.1

26.6

33.9

EPS (`)

8.1

8.9

26.8

23.2

37.1

P/E (x)

94.9

86.3

28.6

33.2

20.7

P/BV (x)

15.1

10.3

8.1

7.0

5.7

RoE (%)

15.9

12.0

28.4

21.1

27.7

RoCE (%)

14.3

15.5

33.5

25.8

34.5

Shrikant Akolkar

EV/Sales (x)

16.6

11.8

6.5

5.8

4.6

022 - 3935 7800 Ext: 6846

EV/EBITDA (x)

64.2

49.9

20.2

21.7

13.7

Source: Company, Angel Research; Note: CMP as of March 7, 2017

Please refer to important disclosures at the end of this report

1

Initiating coverage | Natco Pharma

Company background

Natco Pharma is a Hyderabad based R&D driven organization. The company has

presence in domestic as well as global markets, and has two main business

segments i.e. API and Formulations. It has seven manufacturing facilities, which

are approved by various drug regulatory authorities, and the prominent ones

include USFDA, WHO GMP, ANVISA. Natco’s logistics network in India is well-knit

with about 150 marketing personnel and distributors at strategic points to ensure

product availability pan-India.

The company mainly operates in the niche therapeutic segments i.e. Oncology and

Hepatitis C. Natco was earlier a pure oncology player in the domestic market,

however in 2015, the company forayed in the Hepatitis C segment, diversifying its

domestic operations. Further in 2017, company has forayed in Diabetology and

Cardiology. In the domestic markets, company mainly focuses on limited

competition products with high margin. Natco is ranked among leaders in

oncology segment, while in Hepatitis C; it has been able to grow faster than its

competitors due to the early mover’s advantage. In the overseas markets,

company is present in US, Canada, Europe, Australia, Brazil, etc In the US,

company focuses on limited competition products and has partnered with several

Indian as well as overseas partners, which help it mitigate risk and launch

products.

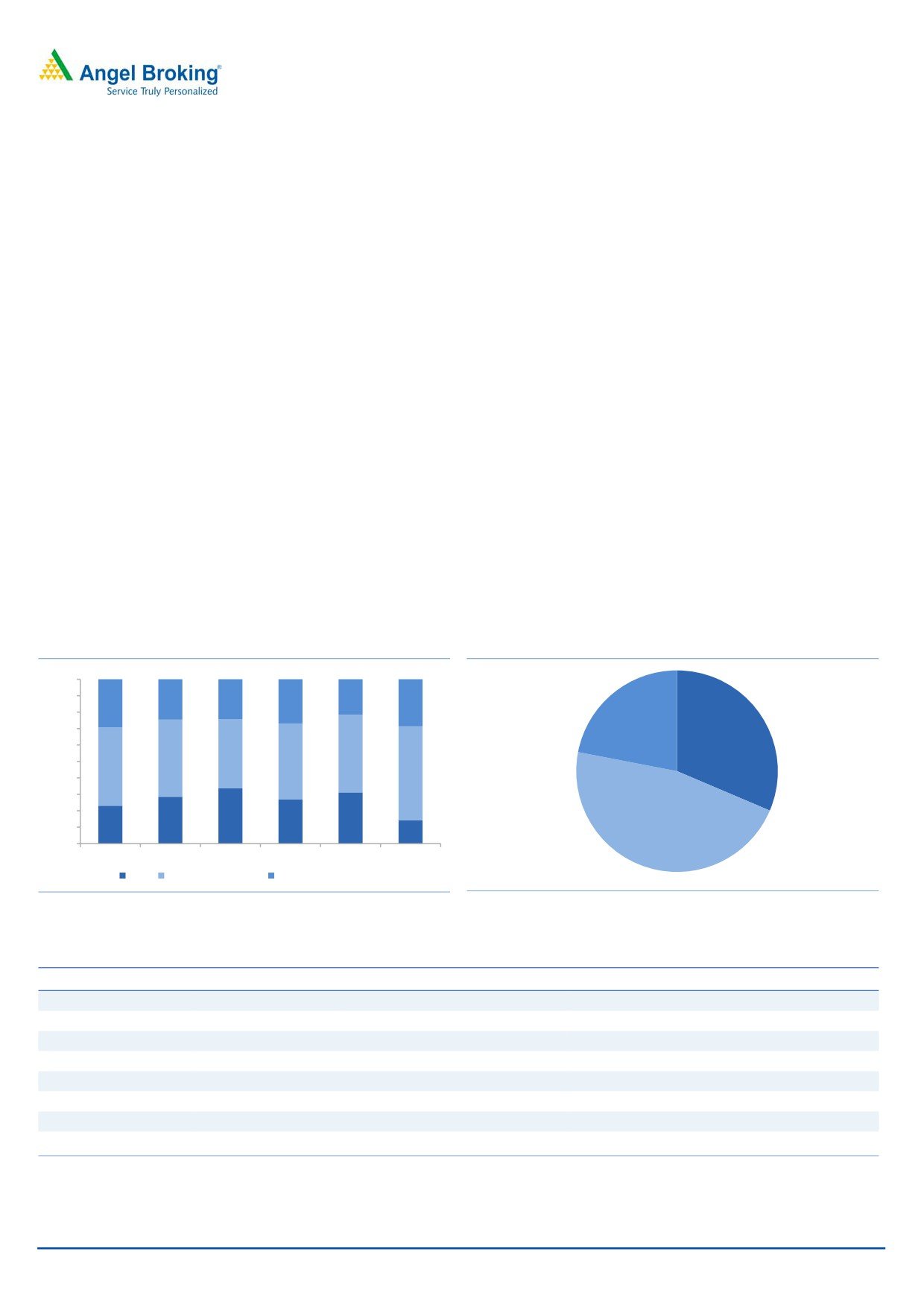

Exhibit 1: Evolution of business mix (%)

Exhibit 2: Domestic business mix

100%

90%

24%

22%

29%

25%

27%

29%

80%

70%

Others, 22%

Oncology,

60%

31%

42%

47%

50%

47%

46%

48%

57%

40%

30%

20%

28%

34%

31%

23%

27%

Hepatitis C,

10%

14%

47%

0%

FY11

FY12

FY13

FY14

FY15

FY16

API

Domestic business

Formulations exports

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 3: Manufacturing facilities

Facility

Segment

Regulatory Approvals

Therapeutic capability

*Kothur

Formulations

USFDA, WHO GMP, ANVISA

Oncology, Gastroenterology CNS, Cardiology

Visakhapatnam

Formulations

Under construction

Oncology, CNS, Cardiology, Diabetology,

Mekaguda

Chemical API

USFDA, WHO GMP

API

Chennai

Chemical API

WHO GMP

API

Nagarjuna Sagar

Formulations

WHO GMP

Oncology, Antibiotics, Antiviral

Dehradun Unit 6

Formulations

WHO GMP

Oncology & Antiviral

Dehradun Unit 7

Formulations

WHO GMP, EU GMP

Oncology

Guwahati

Formulations

GMP

Gastroenterology

Source: Company, Angel Research, *Kothur facility was audited by USFDA in January 2017 and has received 6 observations

March 9, 2017

2

Initiating coverage | Natco Pharma

Investment Rationale

Natco is a top league player in the domestic formulations market: Natco, over the

last decade has emerged as a top league player in the niche therapeutic segments

in the domestic market. The company was present in multiple therapeutic segments

earlier, however, due to its poor financial performance; it sold its domestic finished

formulations business to Sun Pharma in 1988. Further, in 1999, the company had

taken to recourse to debt restructuring post which company focused to improve the

financial health of the company by reducing the debt and raising equity. This has

helped the company to become viable in long term.

Its fortunes changed in FY2003 with the launch of generics of Imatinib Mesylate,

Zoledronic Acid and Letrozole - drugs used in cancer therapy. Natco was the first

company to launch these medicines at affordable prices in India, which quickly

helped it to become a leader in the oncology therapy segment.

Further in FY2015, company expanded its therapeutic reach by launching Hepatitis

C drugs in India at affordable prices. Here too, company was first one to bring

affordable quality Hepatitis C medicines in India. This clearly proved to be a

successful move and company quickly grabbed the number one position in the

Hepatitis C segment.

Natco’s story has been of the specialty drugs instead of me-too drugs. Company

now has total ~28 brands in its portfolio, which has limited competition and

healthy margins. These complex drugs have enabled the company to gain the

market share and drive its top-line growth. This can clearly be seen in

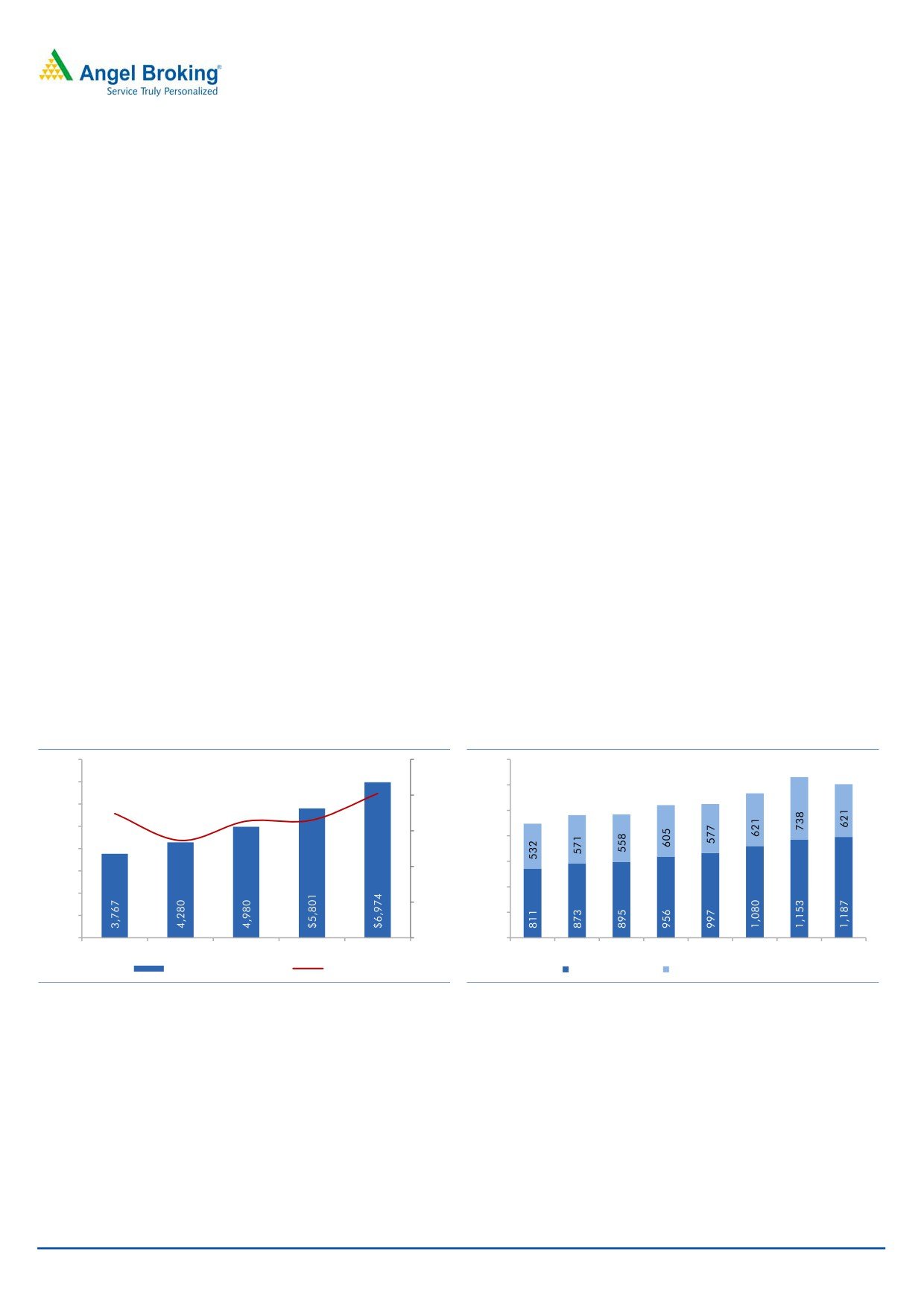

its domestic revenue performance, which has grown at a CAGR of 24% over

FY2011-16.

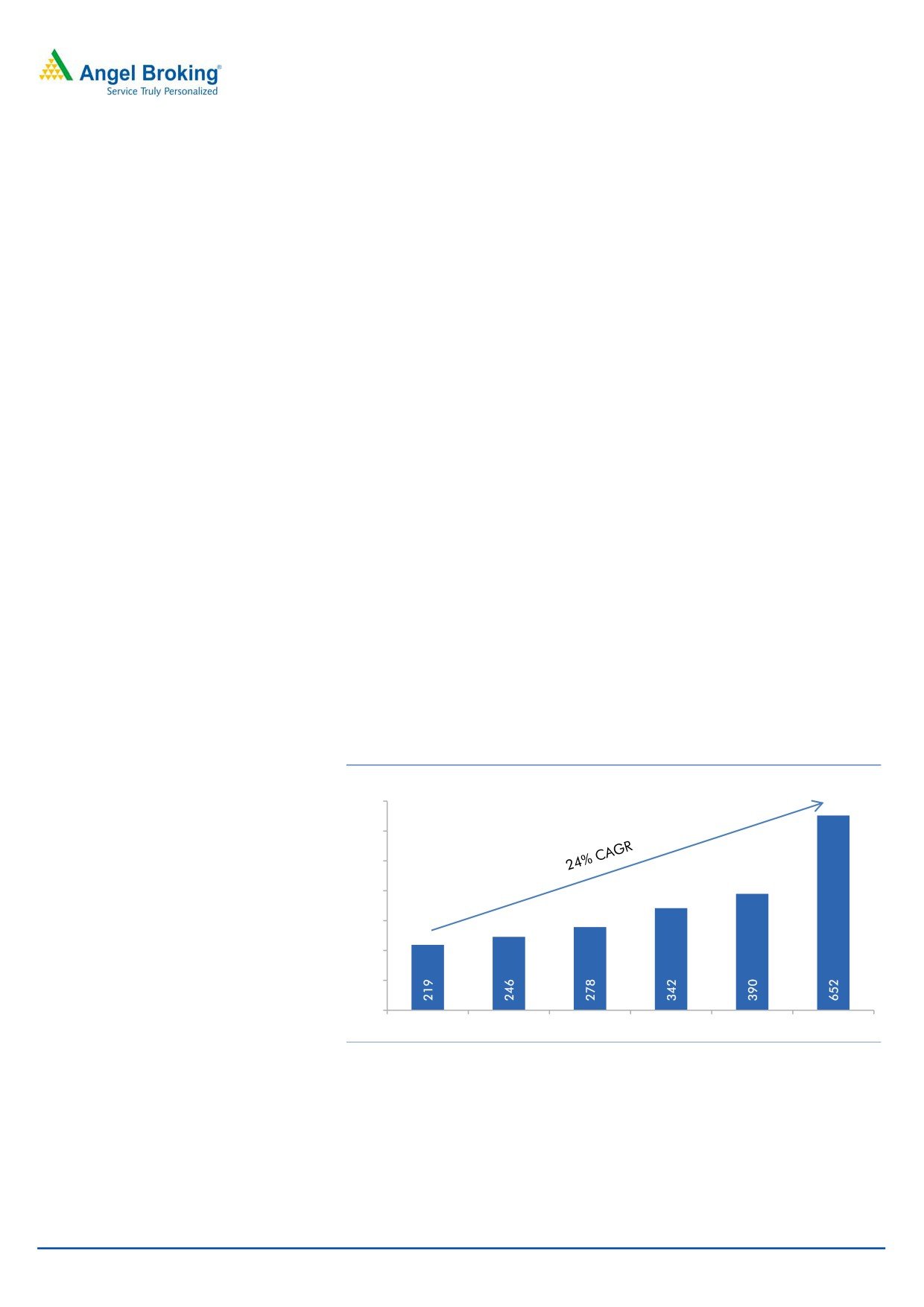

Exhibit 4: Domestic formulations has grown at 24% CAGR (FY11-FY16)

(` cr)

700

600

500

400

300

200

100

0

FY11

FY12

FY13

FY14

FY15

FY16

Source: Company, Angel Research

Oncology segment - Strong growth drivers in place: Oncology is one of the

leading therapeutic segments in the domestic markets as well as globally. Total

number of cancer cases in India is estimated to be 25 lakhs, while every year ~10

lakh new cases are registered. This burden is expected to increase to ~21 lakh

new cases by 2025 indicating that the demand for anti-cancer drugs would

increase going ahead. The domestic oncology market in value terms was

March 9, 2017

3

Initiating coverage | Natco Pharma

~`2,000cr in FY2013, which is expected to grow at ~18% CAGR to reach

~`3,800cr in FY2017.

The rising cancer coverage by insurance companies, increasing affordability of the

cancer medicines, rise in the specialty hospitals, etc. are the major growth drivers

for the anti-cancer medicine in India.

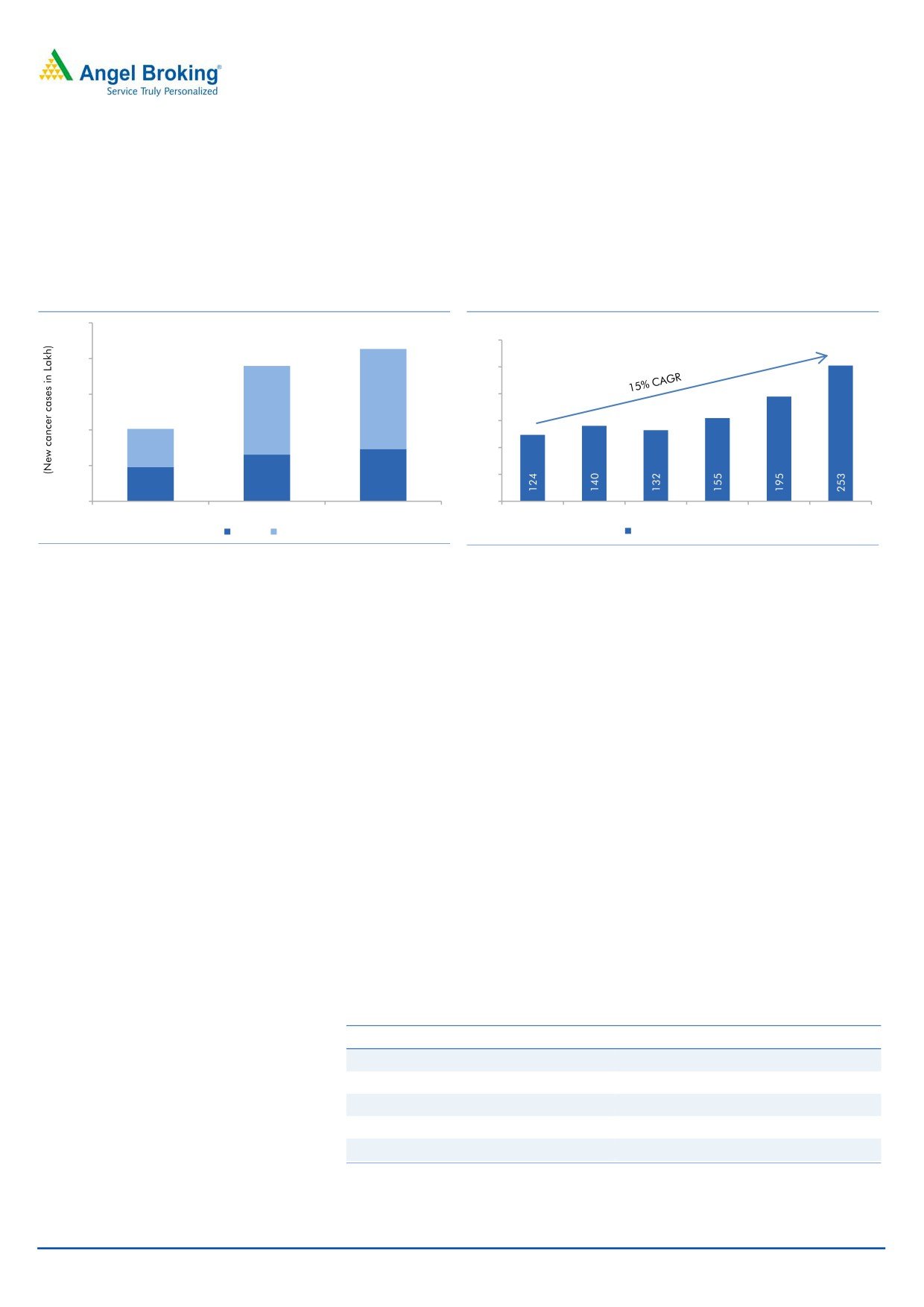

Exhibit 5: India - Growing cancer burden

Exhibit 6: Natco has scaled up its oncology business

25.0

(` cr)

300

20.0

250

15.0

200

14.0

12.4

150

10.0

5.4

100

5.0

7.3

50

6.5

4.8

0.0

0

2012

2020E

2025E

FY11

FY12

FY13

FY14

FY15

FY16

Male

Female

Oncology revenues

Source: GLOBOCAN 2012, Angel Research

Source: Company, Angel Research

Natco holds ~30% market share in targeted cancer therapies: Broadly, cancer

therapies can be classified in several subtypes i.e. 1) Radiation, 2) Chemotherapy,

3) Targeted Therapies, 4) Surgery, and 5) Biologics. Natco competes in targeted

anti-cancer therapies segment, which is pegged to have a size of ~`800cr. Of this,

Natco holds ~30% market share.

The domestic anti-cancer market is fragmented in nature and has several players.

Chemotherapy was the preferred route for cancer treatment earlier, however

combination therapies are on rise due to their effectiveness, and targeted therapy

has found a good application in this. Targeted therapies are economical and

come with lesser side effects, hence, gaining traction in India. While the use of

biologics is expected to increase in future, at the current juncture biologics are not

affordable for the masses.

Over last few years, India has adopted a compulsory license route to bring the life

saving medicines in India. Natco was the first company to receive a compulsory

license for Bayer HealthCare AG’s lung cancer drug Nexavar (Sorafenib) in India.

Natco currently has a product basket of more than 25 drugs in Oncology segment.

This segment has grown at a 5 year CAGR of 15.4% to reach `253cr in FY2016.

Exhibit 7: Natco's `10cr anti-cancer brands

Product

Therapeutic segment

Geftinat

Lung cancer

Erlonat

Lung cancer

Veenat

Chronic Myeloid Leukemia

Sorafenat

Liver and kidney cancer

Lenalid

Multiple Myeloma

Source: Company, Angel Research

March 9, 2017

4

Initiating coverage | Natco Pharma

Exhibit 8: Natco holds 30% market share in its targeted Onco therapies

Domestic cancer

drugs market in

FY16 ~ `2,700cr,

growing by 18% p.a.

Of this 24% is

targeted cancer

therapies' market

~`800 crore

Natco's FY16

revenues of

`253 crore gives

it ~30% market

share

Source: Company, Angel Research

Hepatitis C franchisee has witnessed rapid growth: To diversify its business in

other therapeutic segments, Natco forayed into Hepatitis C segment by launching

three drugs namely 1) Hepcinat (generic Sofosbuvir), 2) Hepcinat LP (generic of

Sofosbuvir+Ledipasvir combination), and 3) Natdac (generic Daclatasvir). For

Hepcinat, Natco received a license from Gilead Sciences while for Natdac it has a

license from Bristol-Myers Squibb This proved successful, as Natco reported

revenue of `340cr from this franchisee in FY2016. In the first full year of

operations, Hepatitis C franchisee outsized the revenue from Oncology segment,

indicating strong future potential. Company is also expected to launch generics of

another blockbuster Hepatitis- C drug Epclusa, which has better cure rate.

Natco has grown despite competition in Hepatitis C: Gilead Sciences has signed a

non-exclusive licensing agreement with several generic pharma companies in

2015 to manufacture and market generics of Sofosbuvir and Ledipasvir in more

than 100 countries. Gilead will receive royalty payment on these sales of these

products. For Daclatasvir too, the innovator company (Bristol-Myers Squibb) has

signed an agreement with several generic pharma companies including Natco to

market and sell generic of Daclatasvir in 112 countries. Despite this competition,

Natco has emerged the biggest beneficiary due to its front end capabilities, first

mover’s advantage and strong brand name.

Why we think Hepatitis C has robust future? Hepatitis C is a liver disease caused

by the Hepatitis C virus (HCV). Globally, ~150 million people are believed to be

infected by HCV and every year ~7 lakh people die due to this disease. While

antiviral medicines have high cure rates (as high as ~90%) against HCV infection,

the access to treatment is a major concern area. HCV is found worldwide, however

Africa and Central and East Asia are the most affected areas.

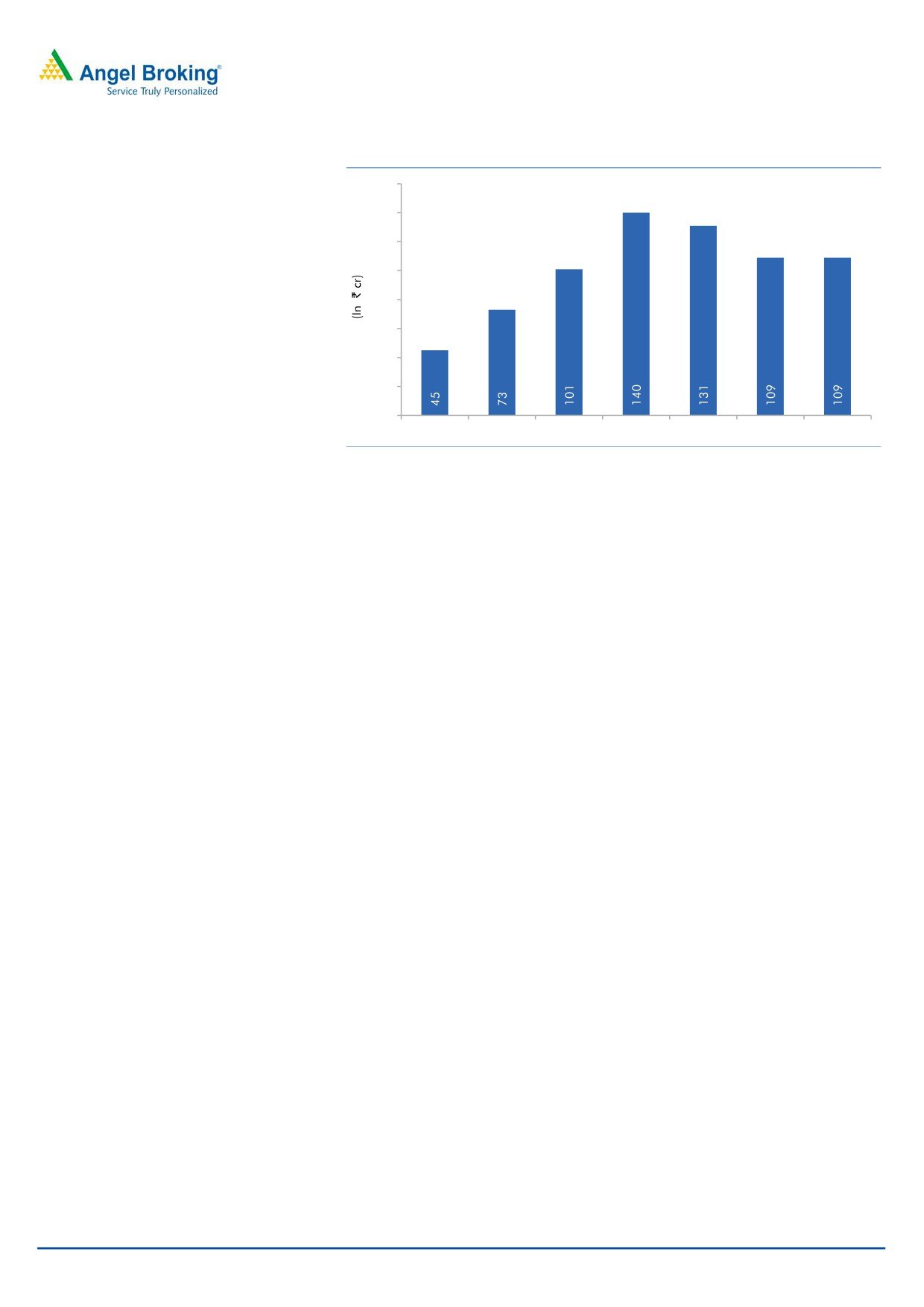

In the domestic market, the growth in Natco’s Hepatitis C franchisee revenue has

been positively surprising. During the first 9 months of FY2017, Hepatitis C

branded formulations have grown to `359cr, surpassing FY2016 full year revenue

of `340cr. The company believes that the franchisee is likely to be `600cr-700cr in

the next two years, implying 2.0x revenue potential from this segment going ahead.

March 9, 2017

5

Initiating coverage | Natco Pharma

Exhibit 9: Natco has seen fast ramp up in Hepatitis C franchisee

160

140

120

100

80

60

40

20

0

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Source: Company, Angel Research

The existing Hepatitis C drugs launched by innovators such as Gilead’s Sovaldi

and Harvoni and Bristol-Myers Squibb’s Daclatasvir (Daklinza) cost

$84,600,

$94,500 and $63,000 respectively for full treatment in the United States. The

generics of these products are available at almost 99% discount to the innovator’s

costs. This is very promising for Natco Pharma, which has already showcased its

capabilities to manufacture and market Hepatitis C drugs. It has required license

for generics of Sofosbuvir / Ledipasvir / Daclatasvir and is in the process to take

the drug to 10-12 countries. Worldwide, Hepatitis C market was estimated to be

~$11.81bn in 2015, which is expected to grow at a CAGR of 15% to reach

~$27.63bn by 2021. This indicates that Hepatitis C franchisee has a very strong

future going ahead.

Launch of cardio and diabetology divisions to give more upside in revenues:

Recently, company has launched two new divisions i.e. Cardiology and

Diabetology. It aims to launch first time generics in this portfolio over the next

18 months, which we believe would be limited competition products that would

help to bring a sizable contribution in the domestic business mix. Company has

indicated that it has 7-8 products in sight and a proper execution of these products

would give additional revenues of `150-200cr annually (~20% of FY2017E

domestic business mix). This will be strongly positive for its domestic portfolio.

Domestic formulations set to cross `1,000cr mark in FY2018E: We believe that

domestic formulations business is likely to cross `1,000cr mark in FY2018E owing

to strong sales from Hepatitis C and Oncology segments. In the first nine months

of FY2017, company reported `664cr of domestic revenue v/s. FY2016 domestic

revenue of `652cr. We expect a CAGR of 21% and 26% in oncology and Hepatitis

C revenues respectively over FY2016-19E period indicating strong domestic

revenues going ahead.

March 9, 2017

6

Initiating coverage | Natco Pharma

Export formulations to thrive with monetization of R&D pipeline:

Natco has been able to grow its export formulations business from `24cr in

FY2010 to `231cr in FY2016. This translates in revenue CAGR of 46% during this

period. Within this, US formulation is the major part of its exports revenues. In the

US, the company has filed a pipeline of complex products, which has limited

competition and high revenue potential. This pipeline is at an interesting point with

few drugs nearing monetization, indicating that its formulations exports are

expected to receive a strong upward thrust in the next two years.

Natco, realizing the importance of niche products, started to file low competition

(Abbreviated New Drug Applications) ANDAs in 2004. Currently it has ANDA

pipeline of 40 ANDAs by 3QFY2017, which does not look rich in volumes

compared its larger peers. However, this pipeline is one of the best in the industry

in value terms (~$16.3bn). This is due to its continued focus on complex products

with limited competition. The company has total 19 Para IVs, which represents

sales of ~$13.4bn of innovator’s brands, indicating an opportunity to grab huge

revenues going ahead.

Exhibit 10: Natco’s pipeline is nearing monetisation over next 3-4 years

Innovator brand name

Size in $ bn

Patent expiry / Launch

Entocort

370

Launched

Nuvugil

482

Launched

Tracleer

487.5

Patent expired, not launched yet

Vidaza

240

2017

Doxil

200

2017

Zortress

60

2017

Copaxone

4300

2018

Gleevec

2,533

2019

Gilenya

1800

2019

Tarceva

564

2020

Tykerb

74

2021

Jevtana

137

2021

Nexavar

300

2022

Fosrenol

118

2024

Treanda

710

2026

Revlimid

6,800

2027

Source: Company, Angel Research

Copaxone 40mg likely to be launched in FY2018: Copaxone (glatiramer acetate

injection) is an immunomodulator drug (acts on immune system) used to treat

multiple sclerosis. This is a blockbuster product of Israeli pharma company Teva,

and had annual sales of ~$4.3bn in 2016. This drug was earlier available in

20mg formulations, which lost the patent in 2015 after which generic drug -

Glatopa was launched by Sandoz/Momenta in June

2015. However, Teva

received approval for its 40mg formulation in 2014 and was able to move 80-85%

patients from Copaxone-20mg to Copaxone-40 mg prescription. This has reduced

the size for Copaxone-20mg drastically. Natco along with its US partner Mylan

believe that they have a FTF on Copaxone 40mg. The drug is protected by five

method of use patents.

March 9, 2017

7

Initiating coverage | Natco Pharma

The 40mg formulation is yet to go off patent and Teva is fiercely trying to keep the

generics away from entering in Copaxone-40mg. Its efforts were, however, wasted

after the United States District Court for the District of Delaware has issued a

decision that 3 out of 4 patents on Copaxone 40m are unpatentable. The ruling

on the fourth patent is expected on May 16, 2017. The fourth patent is expected to

expire in 2030. A positive verdict on May-2017 is likely to see generic companies

(most possibly Natco/Mylan) launch Copaxone 40mg in the US markets without

waiting for expiry of 5th patent (at risk launch) and thereby monetizing its FTF

opportunity. The precursor for this is an approval for Copaxone 20mg ANDA, which

company is optimistic to receive very soon. The fifth patent is also a method of use

patent and invalidation of four patents will boost the confidence of generic

companies to launch the drug at risk.

If Natco is able to launch Copaxone 40mg, it will be Natco’s biggest launch so far.

Just to give a glimpse of this opportunity, Natco Natco reported `277cr quarterly

revenues in US from its recently launched generic of Tamiflu. This revenue was

higher than its full year export revenue in FY2016. The innovator’s drug recorded

sales of ~$400mn in US. By this comparison, Copaxone 40mg is a much larger

drug. We believe that the company would be able to launch Copaxone 40mg in

FY2018E and would be a massive opportunity for the company, as it will scale up

its business significantly.

Exhibit 11: Copaxone journey so far

Dec 1996

May 2017

•Approal and launch of

•Verdict on four of five

Copaxone 20mg

Copaxone 40mg

patent expected

Jan 2014

Dec 2016

•Teva receives USFDA

•US district court rejects

approval for

three Copaxone 40

Copaxone 40mg

mg patents

May 2014

June 2015

•Copaxone 20mg loses

•Sandoz/Momenta

patent

launch Glatopa

(generic Copaxone

20mg)

Source: Company, Angel Research

Revlimid - Natco’s most promising generic: Natco Pharma had challenged certain

patents of a blockbuster multiple myeloma drug Revlimid (lenalidomide), which is

manufactured by a US company Celgene. The case, however, got settled in

December 2015 with Celgene allowing Natco to sell unlimited quantity of generic

Revlimid from April 2027. Additionally Natco has also received a volume limited

license to sell generic Revlimid from March 2022. The company would be able to

sell mid-single-digit percentage of the total lenalidomide capsules dispensed in the

United States during the first full year of entry. Gradually, company can increase

volumes until March 2025 but should not exceed 1/3rd of the total lenalidomide

capsules dispensed in the U.S. in the final year of the volume-limited license under

March 9, 2017

8

Initiating coverage | Natco Pharma

this agreement. From January 31st 2026, Natco can sell unlimited quantities of

generic Revlimid.

Revlimid is one of the most expensive drugs with a single pill priced at ~$634 and

full treatment cost running more than $100,000 per patient. The company has

also an immense pricing power and the pill has seen 1.6x increase in price since

2008. Revlimid holds dominant market share in the multiple myeloma treatment

(~50%). This has resulted in Revlimid’s annual sales surging by 17% to reach

$6.8bn in 2016. This blockbuster drug is likely to lose patent in 2026.

Why Revlimid is a promising opportunity for Natco? Revlimid, by its sheer size, is

one of the top ten best selling drugs in the US. The drug is expected to clock more

than $10bn in its peak revenues. Worldwide this drug has reported total sales of

$6.9bn in 2016, of which $4.4bn came from US alone. The Revlimid sales are

increasing at a CAGR of ~17%, indicating that US sales of Revlimid will cross

$7bn-$8bn making this even bigger opportunity for the generic players like Natco.

This indicates huge windfall gains for Natco once it starts selling generic of

Revlimid in 2022. At 7% market share and 70% price erosion, Natco will be able

to generate annual Revlimid sale of ~`1100cr.

Natco believes that the drug could be launched early if more companies file for the

lenalidomide ANDA. Dr. Reddy’s Laboratories has already filed an ANDA for

Revlimid, however, Natco has FTF for this drug. Revlimid is a complex biologic with

an orphan drug status. The complex biologic means that making the copy of this

drug is very difficult. This is very positive for Natco Pharma, as after losing patents,

lenalidomide may still remain a limited competition drug giving strong revenue

contribution.

Exhibit 12: Revlimid is a $7bn drug...

Exhibit 13: ...and US alone contributes ~2/3rd of sales

8,000

25.0

2,100

20.2

7,000

1,800

17.4

20.0

6,000

16.3

16.5

1,500

5,000

13.6

15.0

1,200

4,000

900

10.0

3,000

600

2,000

5.0

1,000

300

0

0.0

0

2012

2013

2014

2015

2016

Q1-15

Q2-15

Q3-15

Q4-15

Q1-16

Q2-16

Q3-16

Q4-16

Revlimid Sales in $ mn

Growth

US sales ($ mn)

International sales ($ mn)

Source: Company, Angel Research

Source: Company, Angel Research

Differentiated R&D strategy: Natco has adopted a different approach in its

research than its peers. While the Indian companies were busy in entering me-too

products in domestic markets and growing their ANDA pipeline, Natco decided to

focus on niche, limited competition products. In the domestic markets, it focused

on oncology products first and then entered the Hepatitis C drugs. In the

international markets, where one needs 1) strong front end capabilities and

2) ability to take risk, company adopted a strategy to partner with bigger generic

companies. This has helped Natco in minimizing the legal risk. Company has

collaboration with companies, such as, Mylan, Breckenridge, Alvogen, Actavis and Lupin.

March 9, 2017

9

Initiating coverage | Natco Pharma

Natco has currently total 43 ANDAs and the pipeline is not big compared to its

peers, however, of its 43 ANDAs, 19 are the Para-IVs which have addressable size

of ~$13.4bn, which speaks about its differentiated approach. We believe that

Natco’s US formulations business has multifold growth opportunity going ahead,

as between FY2018 and FY2022, lot of products are likely to be launched.

Exhibit 14: Natco’s marketing partners

Innovator brand

Size in $ mn

Marketing partner

*Tamiflu

403

Alvogen

Doxil

200

Dr. Reddy's lab

Copaxone

4300

Mylan

Tykerb

74

Lupin

Fosrenol

118

Lupin

Revlimid

6,800

Watson

Source: Company, Angel Research, *already launched

Natco’s other business: Natco has operations in Europe, Canada, Brazil, etc.

which together contributed ~15% of the total revenues. This business is growing at

~6% CAGR over the period of FY2011-16. The company has indicated of

continuing its strategy of focusing on the US business as its ANDA pipeline is

expected to fire up in next three to four years.

In the US business, Natco had earlier acquired retail pharmacies as a preferred

option to grow US business. However, with the change in strategy, company has

sold two retail pharmacies in the US. With this, the contribution of pharmacies in

total revenues has come down from ~12% in FY2016 to <5% in FY2017. This is

expected to go down further with stronger contribution from the formulations

business.

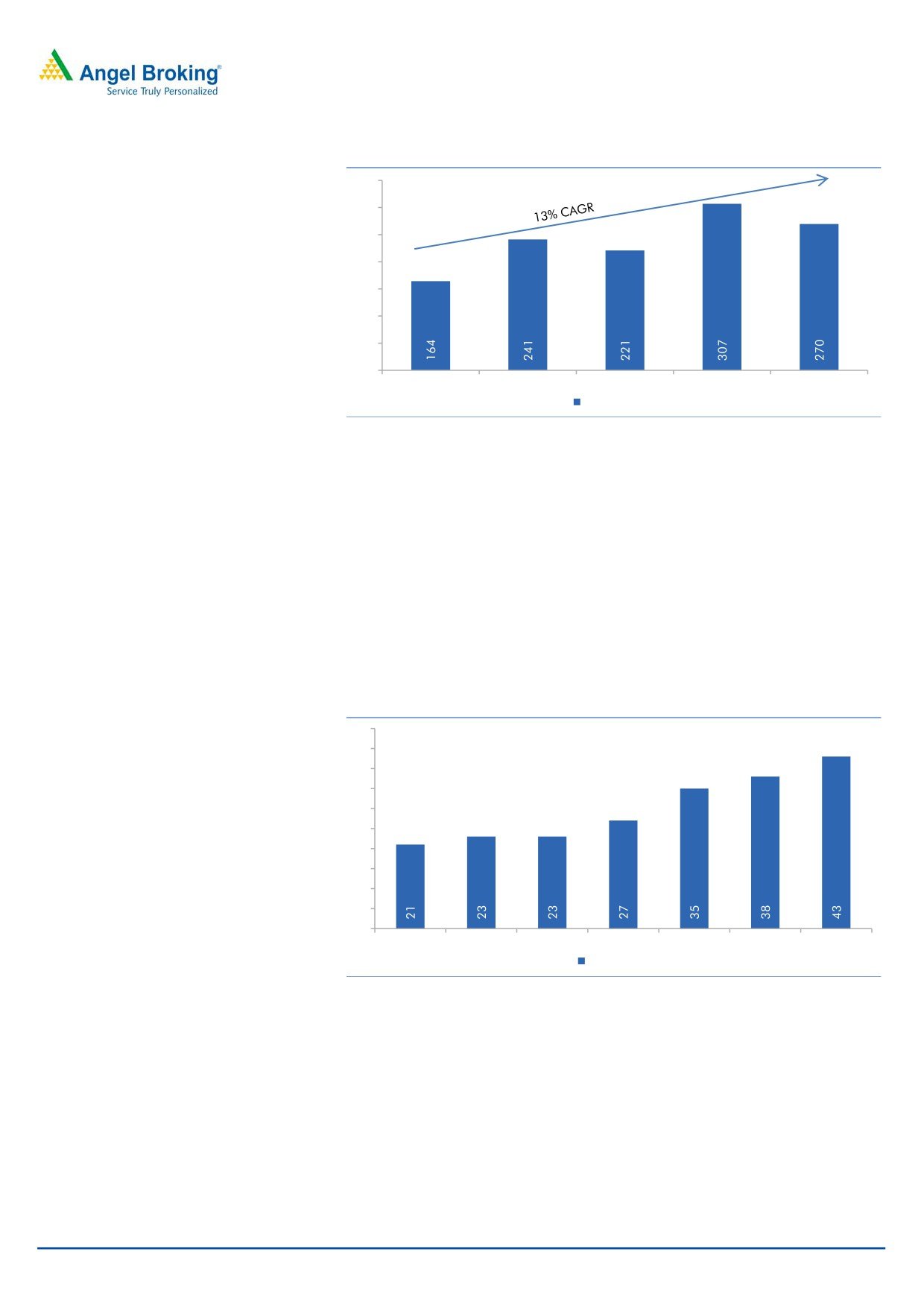

Capacity augmentation in API business: Natco has an API business, which

contributed 23% of its revenues in FY2016. Company uses APIs for domestic

consumption as well as to supply to its domestic and international customers. The

80-90% of the API turnover is generated through exports, while rest comes from

the domestic customers. In FY2013, API business contributed 36% of its total

revenues, however, with remarkable growth in the formulation business;

contribution of API has come down gradually. By 9MFY2017, API business

contributed ~ 9% of the total revenues. We believe that this trend is likely to

continue with launch of two new therapeutic divisions in India and launches of high

value generics in the US.

Natco’s management believes that its API business has a strong potential, as it fits

in its value chain by means of backward integration for its formulations business.

With the new product launches over next few years, company is augmenting its API

manufacturing capacity at its Manali & Mekaguda locations which will continue to

supply APIs to its formulations business as well as for third party sales to external

customers.

March 9, 2017

10

Initiating coverage | Natco Pharma

Exhibit 15: API revenues have grown at 13% CAGR

350

300

250

200

150

100

50

0

FY12

FY13

FY14

FY15

FY16

API sales in ` Cr

Source: Company, Angel Research

Addition of new formulations capacity to boost ANDA pipeline: Natco Pharma is

setting up a new formulations facility at Visakhapatnam (Vizag). This facility is

expected to be operational in June 2017. This facility holds key for Natco’s

incremental fillings going ahead. This is a major capacity expansion program for

the company aimed to support its growing US business. Management has

indicated that it will start filling ANDAs from this facility in early 2017.

The company, during the period of FY2011-9MFY2017, made only 22 filings and

expects to file more than 10 ANDAs per year once Vizag capacity is ready. So this

facility is extremely important to support Natco’s growing US business.

Exhibit 16: Natco filed only 22 ANDAs between FY11-9MFY17

50

45

40

35

30

25

20

15

10

5

0

FY11

FY12

FY13

FY14

FY16

FY16

9MFY17

ANDA pipeline

Source: Company, Angel Research

Expansion of Dehradun and Guwahati facilities to enable incremental product

launches: Natco is also in process of upgrading its existing formulations facilities at

Dehradun and Guwahati. Once completed, these upgraded capacities will support

its domestic formulations business. The augmentation of the Dehradun and

Guwahati capacities will support its entry in the diabetology and cardiology

divisions. The total capex on these facilities is expected to be ~`40cr.

Track record of compliant facilities - We observe that the recently issued 483s on

its facilities had minor observations and has not escalated to warning alert. In

March 2016, USFDA issued observations on two of its facilities i.e. Manali (API)

March 9, 2017

11

Initiating coverage | Natco Pharma

and Kothur (Formulations). The inspections at these facilities were triggered due to

generic of Doxil. Both facilities received EIR however Kothur facility was again

inspected (GMP purpose) in January-2017 and received 6 observations. Company

has indicated that these observations are correctable in nature (no data integrity

issues) and hence, escalation is not expected. Company has indicated that it is not

expecting any USFDA inspection on formulations side, except for Vizag. On API

side, there could be inspection this year.

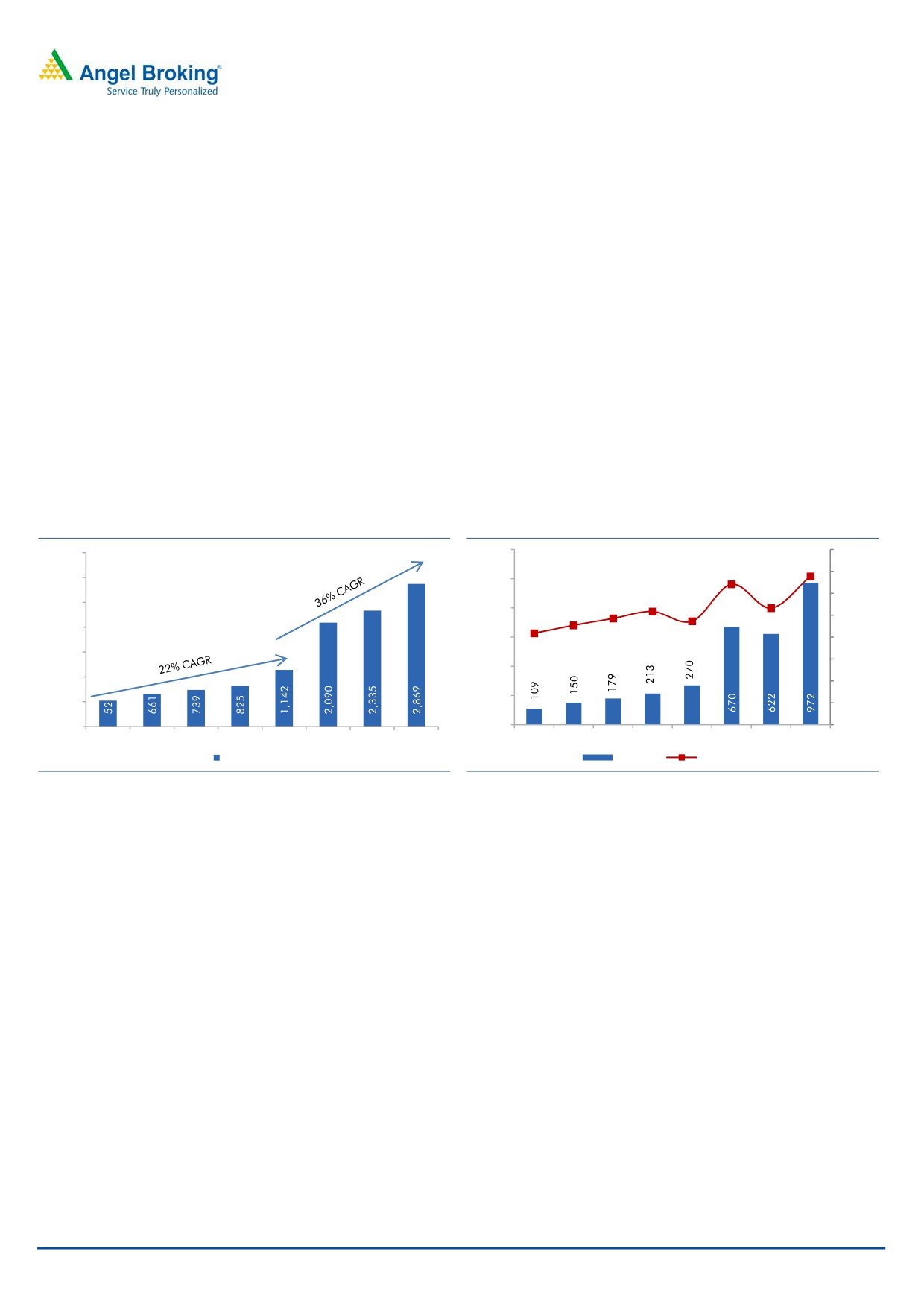

Financial performance: Over the last 5 years (FY2012-16), company has seen

2.2x growth in its top-line, which exhibits a healthy 21.5% CAGR. During this

period, Natco has also seen strong improvement in its EBITDA margins due to

1) focus on niche therapeutic segments, 2) improving product mix, and 3) growing

domestic branded business. Owing to this, its operating margins have increased

from 20.9% in FY2012 to 23.6% in FY2016. With the addition of the two new

franchisees, the margins are likely to go up from here as well. During the

FY2012-16 period, its bottom-line has seen 2.6x growth, which works out to be an

attractive 27.5% CAGR.

Exhibit 17: Revenue to grow at 36% over FY16-FY19E

Exhibit 18: Operating margins set to improve

3,500

1,200

40.0

33.9

32.1

35.0

3,000

1,000

26.6

30.0

25.9

23.6

2,500

24.3

800

22.7

20.9

25.0

2,000

600

20.0

1,500

15.0

400

1,000

10.0

200

500

5.0

-

-

-

FY12

FY13

FY14

FY15

FY16

FY17E FY18E FY19E

FY12

FY13

FY14

FY15

FY16

Revenue (` cr)

EBITDA

(% of Net Sales)

Source: Company, Angel Research

Source: Company, Angel Research

We believe that due to the favorable dynamics, Natco’s growth rates are likely to

accelerate even higher with export formulations seeing huge 64% CAGR in

revenues over FY16-19E. This will mainly be due to launch of Copaxone 20 mg

and 40 mg which are likely to see high revenue contribution in FY18E and FY19E.

The FY17E revenue has already seen huge growth due to the contribution of export

formulations (mainly due to generic Tamiflu). We have also incorporated revenues

from generic Entocort and generic Nuvugil which already have been launched. We

also expect generic Vidaza and generic Doxil revenues in FY18E.

March 9, 2017

12

Initiating coverage | Natco Pharma

Exhibit 19: PAT to grow at 61% over FY16-FY19E

700

600

500

400

300

200

100

-

FY12

FY13

FY14

FY15

FY16

FY17E

FY18E

FY19E

PAT (` cr)

Source: Company, Angel Research

Healthy balance sheet, RoE profile to improve: Since FY13, the company has been

able to strengthen its balance sheet with repayment of debt. The debt to equity

ratio which stood at 0.63x in FY13 has come down to almost nil in FY16. The

continues to maintain conservative approach to keep lower debt to equity. In FY15,

company raised `350cr through QIP route to augment its capacities. While this led

to equity dilution and declined its RoE, the substantial growth in next few years is

expected to boost its RoE profile.

Exhibit 20: Healthy RoE expansion over FY17E-FY19E

30.0

25.0

20.0

15.0

10.0

5.0

0.0

FY12

FY13

FY14

FY15

*FY16

FY17E

FY18E

FY19E

ROE (%)

Source: Company, Angel Research

March 9, 2017

13

Initiating coverage | Natco Pharma

Outlook and Valuation

Natco’s topline and bottomline is set to grow at 36% and 61% CAGR over

FY16-FY19E due to

1) strong performance of domestic formulations and

2) monetization of high value ANDAs. We believe that Natco is also set to see

margin expansion on the back of improving product mix (higher hepatitis sales in

domestic business) and launch of high value, low competition ANDAs. We expect

FY19E revenue at `2,869cr and PAT of `644cr.

The stock at the CMP of `786 is trading at P/E of 21.2x of FY2019E EPS of `37.

This is ~15% discount to its 3 year average P/E multiple of 26x. We value Natco

based on SOTP approach, which yields a total value of Natco’s shares to be `926

(base business `890 + Revlimid opportunity `37). Our valuations stems from

below rationale:

1) We value Natco’s base at ` 890 (24.0x of its FY19E EPS of `37) assuming

1) Natco receives final approval for its Copaxone 20mg ANDA, 2) Teva’s final

patent on Copaxone

40mg is rejected by the Patent Office,

3) Natco receives final approval for its Copaxone

40mg ANDA, and

4) Natco’s marketing partner, Mylan launches generic Copaxone 20mg and

40 mg in the US in FY18E. We also consider Natco’s 1) Niche segment

focused domestic business, 2) strong track record of execution of strategy,

3) high growth rates going during the forecast period, 4) improving RoE

profile, and 5) ANDA pipeline focusing on low competition/high margin

products.

2) We have also considered generic Revlimid in valuation, as Natco’s agreement

with Celgene indicates that Natco has secured a significant big opportunity

between FY2022E-27E. We derive generic Revlimid NPV to be `37 applying

60% probability of discount. From our interaction with the company, we

understand that there is also a probability of Natco launching this drug earlier

in the market if more companies file Revlimid ANDAs. Dr. Reddy’s have filed

ANDA of Revlimid. Entry of more competitors in Revlimid ANDA may trigger

early launch by Natco.

March 9, 2017

14

Initiating coverage | Natco Pharma

Risks to Our Estimates

An unfavorable facility inspection from USFDA or other major regulatory body,

leading to significant delay of product exports.

Failure to get USFDA approval for Copaxone (20mg and 40 mg) and Revlimid

would lead to decline in its financial performance and stock valuation.

Company has indicate of at-risk launch if dynamics favor, however an

unsuccessful at-risk launch of Copaxone would severely erode its financial

performance at it would involve a litigation and possible penalty payment to

the innovator.

Decline in Hepatitis C revenues due to increased competition in the domestic

markets.

March 9, 2017

15

Initiating coverage | Natco Pharma

Income statement

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

FY19E

Total operating income

739

825

1,142

2,090

2,335

2,869

% chg

11.9

11.7

38.3

83.1

11.7

22.9

Total Expenditure

560

612

872

1,420

1,713

1,897

Cost of Materials

233

242

341

651

746

844

Personnel

113

137

187

229

296

353

Others Expenses

214

233

344

541

672

700

EBITDA

179

213

270

670

622

972

% chg

19.6

19.0

26.4

148.4

(7.2)

56.3

(% of Net Sales)

24.3

25.9

23.6

32.1

26.6

33.9

Depreciation& Amort.

30

47

51

58

82

105

EBIT

149

166

219

612

540

867

% chg

16.5

11.6

31.7

179.9

(11.9)

60.5

(% of Net Sales)

20.2

20.1

19.2

29.3

23.1

30.2

Interest & other Charges

37

32

23

16

20

20

Other Income

17

15

11

20

24

24

(% of PBT)

13.0

10.0

5.2

3.3

4.4

2.8

Share in profit of Ass.

-

-

-

-

-

-

Recurring PBT

129

149

207

617

544

871

% chg

26.1

4.1

53.9

198.4

(11.8)

60.1

Prior Period & Extra. Exp.

-

15

-

-

-

-

PBT (reported)

129

134

207

617

544

871

Tax

31

4

53

151

141

226

(% of PBT)

23.9

2.9

25.6

24.4

26.0

26.0

PAT (reported)

98

130

154

466

402

644

Add: Share of earnings of ass.

Less: Minority interest (MI)

(5)

(4)

(1)

(1)

(1)

(1)

PAT after MI (reported)

103

135

155

467

404

646

ADJ. PAT

103

150

155

467

404

646

% chg

23.1

45.8

3.6

201.2

(13.6)

59.9

(% of Net Sales)

13.9

18.1

13.6

22.4

17.3

22.5

Basic EPS (`)

31.1

8.1

8.9

26.8

23.2

37.1

Fully Diluted EPS (`)

31.1

8.1

8.9

26.8

23.2

37.1

% chg

23.1

45.8

3.6

201.2

(13.6)

59.9

March 9, 2017

16

Initiating coverage | Natco Pharma

Balance sheet

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

FY19E

SOURCES OF FUNDS

Equity Share Capital

33

33

35

35

35

35

Reserves& Surplus

693

813

1,263

1,613

1,876

2,295

Shareholders’ Funds

726

846

1,298

1,648

1,911

2,330

Minority Interest

7

5

5

5

5

5

Total Loans

240

312

113

183

183

183

Deferred Tax Liability

43

12

14

14

14

14

Other long term liabilities

1

1

1

1

1

1

Long-term provisions

11

9

12

12

12

12

Total Liabilities

1,028

1,185

1,443

1,863

2,126

2,545

APPLICATION OF FUNDS

Gross Block

781

886

972

1,202

1,721

2,037

Less: Acc. Depreciation

168

222

268

325

407

512

Net Block

613

664

705

877

1,314

1,524

Intangible assets

32

46

9

9

9

9

Capital work-in-progress

124

129

212

262

(0)

(0)

Non-current investments

2

2

0

0

0

0

Long-term loans and adv.

54

57

62

62

62

62

Other non-current assets

3

4

4

4

4

4

Current Assets

368

483

832

1,296

1,388

1,731

Inventories

181

220

357

573

608

707

Sundry Debtors

119

192

262

481

512

629

Cash

11

13

45

51

61

152

Loans & Advances

54

55

104

136

152

186

Other Assets

3

2

64

56

56

56

Current liabilities

167

199

380

647

651

785

Net Current Assets

201

284

452

649

737

946

Deferred Tax Asset

-

-

-

-

-

-

Misc. Exp. not written off

-

-

-

-

-

-

Total Assets

1,028

1,185

1,443

1,863

2,126

2,545

March 9, 2017

17

Initiating coverage | Natco Pharma

Cash flow statement

Y/E March (` cr)

FY14

FY15

FY16

FY17E FY18E FY19E

Profit before tax

129

134

207

617

544

871

Depreciation

30

47

51

58

82

105

Change in Working Capital

(16)

(86)

(150)

(192)

(78)

(118)

Interest / Dividend (Net)

35

30

21

16

20

20

Direct taxes paid

(35)

(24)

(46)

(151)

(141)

(226)

Others

1

(9)

20

-

-

-

Cash Flow from Operations

144

93

102

348

427

652

(Inc.)/ Dec. in Fixed Assets

(106)

(117)

(157)

(280)

(257)

(316)

(Inc.)/ Dec. in Investments

(3)

2

2

(0)

-

-

Cash Flow from Investing

(109)

(115)

(155)

(280)

(257)

(316)

Issue of Equity

109

-

334

-

-

-

Inc./(Dec.) in loans

(91)

71

(199)

70

-

-

Interest paid

(34)

(30)

(25)

(16)

(20)

(20)

Dividend Paid (Incl. Tax)

(18)

(12)

(25)

(116)

(140)

(225)

Effect of currency

0

(5)

(1)

0

0

0

translation adjustment

Cash Flow from Financing

(35)

24

85

(62)

(160)

(245)

Inc./(Dec.) in Cash

0

2

32

6

10

91

Opening Cash balances

11

11

13

45

51

61

Closing Cash balances

11

13

45

51

61

152

March 9, 2017

18

Initiating coverage | Natco Pharma

Key Ratios

Y/E March

FY14

FY15

FY16

FY17E

FY18E

FY19E

Valuation Ratio (x)

P/E (on FDEPS)

25.3

97.0

88.2

29.3

33.9

21.2

P/CEPS

19.5

71.8

66.4

26.1

28.2

18.2

P/BV

3.6

15.4

10.5

8.3

7.2

5.9

Dividend yield (%)

0.7

0.2

0.2

0.9

1.0

1.7

EV/Sales

18.8

17.0

12.1

6.6

5.9

4.8

EV/EBITDA

77.6

65.6

51.0

20.6

22.2

14.1

EV / Total Assets

13.5

11.8

9.5

7.4

6.5

5.4

Per Share Data (`)

EPS (Basic)

31.1

8.1

8.9

26.8

23.2

37.1

EPS (fully diluted)

31.1

8.1

8.9

26.8

23.2

37.1

Cash EPS

40.3

10.9

11.8

30.1

27.9

43.1

DPS

5.9

1.2

1.5

6.8

8.1

13.0

Book Value

219.5

50.9

74.5

94.6

109.7

133.8

Dupont Analysis

EBIT margin

20.2

20.1

19.2

29.3

23.1

30.2

Tax retention ratio

0.8

1.0

0.7

0.8

0.7

0.7

Asset turnover (x)

0.8

0.7

0.8

1.2

1.1

1.2

ROIC (Post-tax)

11.9

14.1

11.9

26.0

19.7

27.2

Cost of Debt (Post Tax)

0.12

0.10

0.15

0.07

0.08

0.08

Leverage (x)

0.3

0.4

0.1

0.1

0.1

0.0

Operating ROE

15.6

19.0

12.5

28.1

20.9

27.5

Returns (%)

ROCE

15.4

14.3

15.5

33.5

25.8

34.5

Angel ROIC (Pre-tax)

15.6

14.5

16.0

34.4

26.6

36.7

ROE

14.2

15.9

12.0

28.4

21.1

27.7

Turnover ratios (x)

Asset Turnover (Gross Block)

0.9

0.9

1.2

1.7

1.4

1.4

Inventory / Sales (days)

89

97

114

100

95

90

Receivables (days)

59

85

84

84

80

80

Payables (days)

54

55

88

80

70

70

WC cycle (ex-cash) (days)

94

127

110

104

105

100

Solvency ratios (x)

Net debt to equity

0.3

0.4

0.1

0.1

0.1

0.0

Net debt to EBITDA

1.3

1.4

0.2

0.2

0.2

0.0

Interest Coverage (EBIT / Int.)

4.1

5.2

9.6

37.7

26.9

43.2

March 9, 2017

19

Initiating coverage | Natco Pharma

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Natco Pharma

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

March 9, 2017

20