4QFY2017 Result Update | Pharma

June 5, 2017

Natco Pharma

ACCUMULATE

CMP

`968

Performance Highlights

Target Price

`1,060

Y/E March (` cr)

4QFY17 4QFY16 % chg (yoy) FY17

FY16

% chg (yoy)

Investment Period

12 Months

Net Sales

578

394

46.5

2,065

1,080

91.2

EBITDA

241

93

158.7

683

266

157.3

Stock Info

EBITDA Margin (%)

41.7

23.6

1809 bp

33.1

24.6

850 bp

Sector

Pharma

Adj. PAT

176

63

178.6

486

155

213.8

Market Cap (` cr)

16,865

Source: Company, Angel Research

Net Debt (` cr)

187

Tamiflu lifts 4Q numbers: Natco reported strong earnings in 4QFY17 owing to

Beta

0.6

strong sales of generic Tamiflu during the quarter. Company reported 47% yoy

52 Week High / Low

1,015/480

growth in its top line to `578cr. EBITDA in the quarter came in at `241cr, vs.

Avg. Daily Volume

46,541

`93cr in 4QFY16 and `195cr in 3QFY7. EBITDA margin was at 41.7%, up by

Face Value (`)

2

more than 1800bss on yoy basis due to the higher sales and profit sharing of

BSE Sensex

31,309

gTamiflu. Company during the quarter reported yoy 2.8x jump in the PAT from

Nifty

9,675

`63cr to 176cr. Employee cost increased 49% during the quarter mainly due to

Reuters Code

NATP NS

the ESOP and bonus to employees. From the conference call, we understand that

Bloomberg Code

NTCPH IN

the company is almost launch ready for gCopaxone however the final decision to

launch the drug lies with Mylan. gCopaxone launch is expected to significantly

Shareholding Pattern (%)

boost its top line and bottom line due to the limited competition and complex

Promoters

51.2

nature of the drug. Besides, company is also expected to benefit from

MF / Banks / Indian Fls

20.5

observations on facility of Momenta, the existing generic manufacturer in 20mg.

FII / NRIs / OCBs

6.3

Outlook and valuation: The bumper earnings in 4QFY17 were mostly expected

Indian Public / Others

22.1

and there was no surprise element. We however believe that company is almost

launch ready for gCopaxone in June-2017. We gain significant confidence that

Mylan/Natco are most likely to launch the drug soon which is the most important

Abs. (%)

3m 1yr 3yr

trigger for the Natco at the moment. Company has responded all the queries on

Sensex

8.6

16.6

26.0

gCopaxone and from the commentary in the conference call, it’s just a matter of

Natco Pharma

26.1

102.5

544.0

time before the company launches this gCopaxone 20mg and 40mg. We value

Natco’s base business at 24x of its FY19E EPS to 587 per share and add NPV of

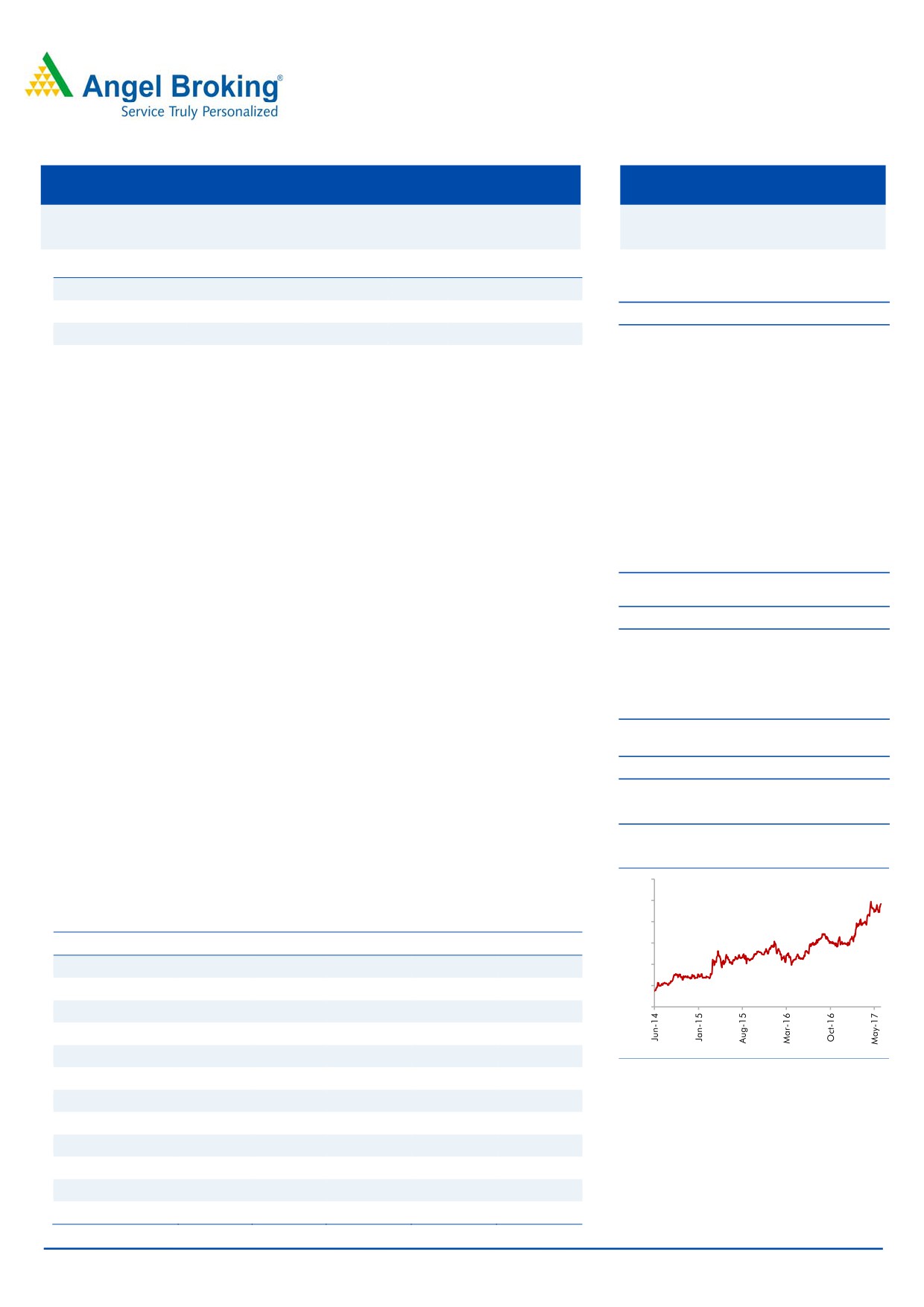

3-year price chart

R&D pipeline of `471 to derive new price target of `1,060. Our target indicates

1,200

10% upside from the CMP of `968.

1,000

Key financials (Consolidated)

800

Y/E March (` cr)

FY15

FY16

FY17

FY18E

FY19E

600

Net Sales

825

1,080

2,065

1,988

2,131

400

200

% chg

11.7

30.9

91.2

(3.7)

7.2

0

Net Profit

213

266

683

670

653

% chg

19.0

24.5

157.3

(2.0)

(2.5)

OPM (%)

25.9

24.6

33.1

33.7

30.7

Source: Company, Angel Research

EPS (`)

8.1

8.9

27.9

25.7

24.5

P/E (x)

119.4

108.8

34.7

37.6

39.5

P/BV (x)

19.0

13.0

10.1

8.6

7.5

RoE (%)

15.9

11.9

29.2

22.9

19.1

RoCE (%)

14.3

15.2

33.1

27.5

23.3

Shrikant Akolkar

EV/Sales (x)

20.8

15.7

8.3

8.3

7.8

022-3935 7800 Ext: 6846

EV/EBITDA (x)

80.4

63.8

25.0

24.7

25.3

Source: Company, Angel Research; Note: CMP as of June 05, 2017

Please refer to important disclosures at the end of this report

1

Natco Pharma |4QFY2017 Result Update

Exhibit 1: Quarterly financial performance

Y/E March (` cr)

4QFY17

4QFY16

% chg (yoy)

3QFY17

% chg (qoq)

FY17

FY16

% chg (yoy)

Net sales

578

394

46.5

679

(14.9)

2,065

1,080

91.2

Consumption of RM

117

100

17.4

206

(43.0)

599

271

121.4

(% of Sales)

20.3

25.3

30.3

29.0

25.1

Staff costs

80

53

49.3

61

31.1

243

180

35.3

(% of Sales)

13.8

13.5

8.9

11.8

16.6

Other expenses

140

148

(5.5)

153

(8.4)

539

364

48.1

(% of Sales)

24.2

37.6

22.5

26.1

33.7

Total Expenditure

337

301

11.8

419

(19.6)

1,382

815

69.6

Operating Profit

241

93

158.7

260

(7.3)

683

266

157.3

OPM

41.73

23.63

1809 bp

38.3

342 bp

33.1

24.6

850 bp

Depreciation

14

12

9.8

14

(1.5)

54

51

7.1

Other income

(1)

0

(250.0)

6

(109.8)

14

10

44.8

Finance cost

6

4

77.8

5

39.1

19

23

(19.2)

PBT (excl. Extr. Items)

221

78

183.9

248

(11.0)

624

202

209.9

Extr. Income/(Expense)

0

0

0

0

0

PBT (incl. Extr. Items)

221

78

183.9

248

(11.0)

624

202

209.9

(% of Sales)

38.2

19.7

1847 bp

36.5

166 bp

30.2

18.7

1158 bp

Tax

44

14

213.5

53

(16.8)

140

48

191.2

(% of PBT)

20.0

18.1

21.4

22.3

23.8

Reported PAT

176

64

177.4

195

(9.4)

485

154

215.7

Minority interest and Associate Company

(0)

(0)

(25.0)

(0)

50.0

(1)

(1)

(15.4)

Adj PAT

176

63

178.6

195

(9.5)

486

155

213.8

Adj. PATM

30.5

16.0

28.7

23.5

14.3

Equity capital (cr)

35

35

35

35

35

Adjusted EPS (`)

10

4

177.1

11

(9.4)

28

9

213.8

Source: Company, Angel Research

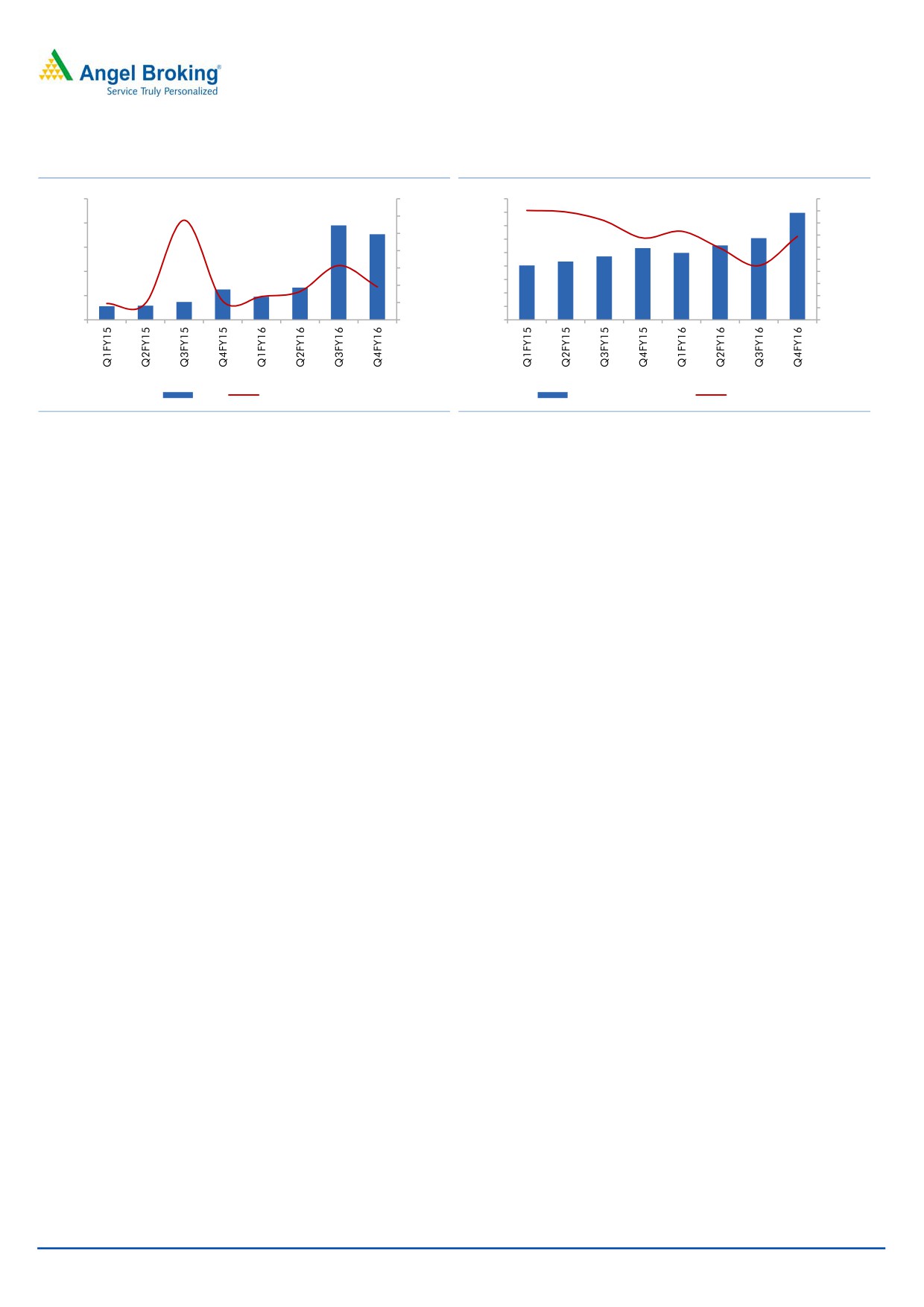

Exhibit 2: Tamiflu inspires strong Topline growth

Exhibit 3: Operating margins improve significantly

300

50

800

136

160

250

700

140

40

600

96

120

200

93

30

500

100

52

47

150

400

9

80

5

20

47

300

60

100

200

40

50

10

100

20

0

0

0

0

Net sales (`cr)

yoy growth (%)

Operating profit

Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

February 14, 2017

2

Natco Pharma |4QFY2017 Result Update

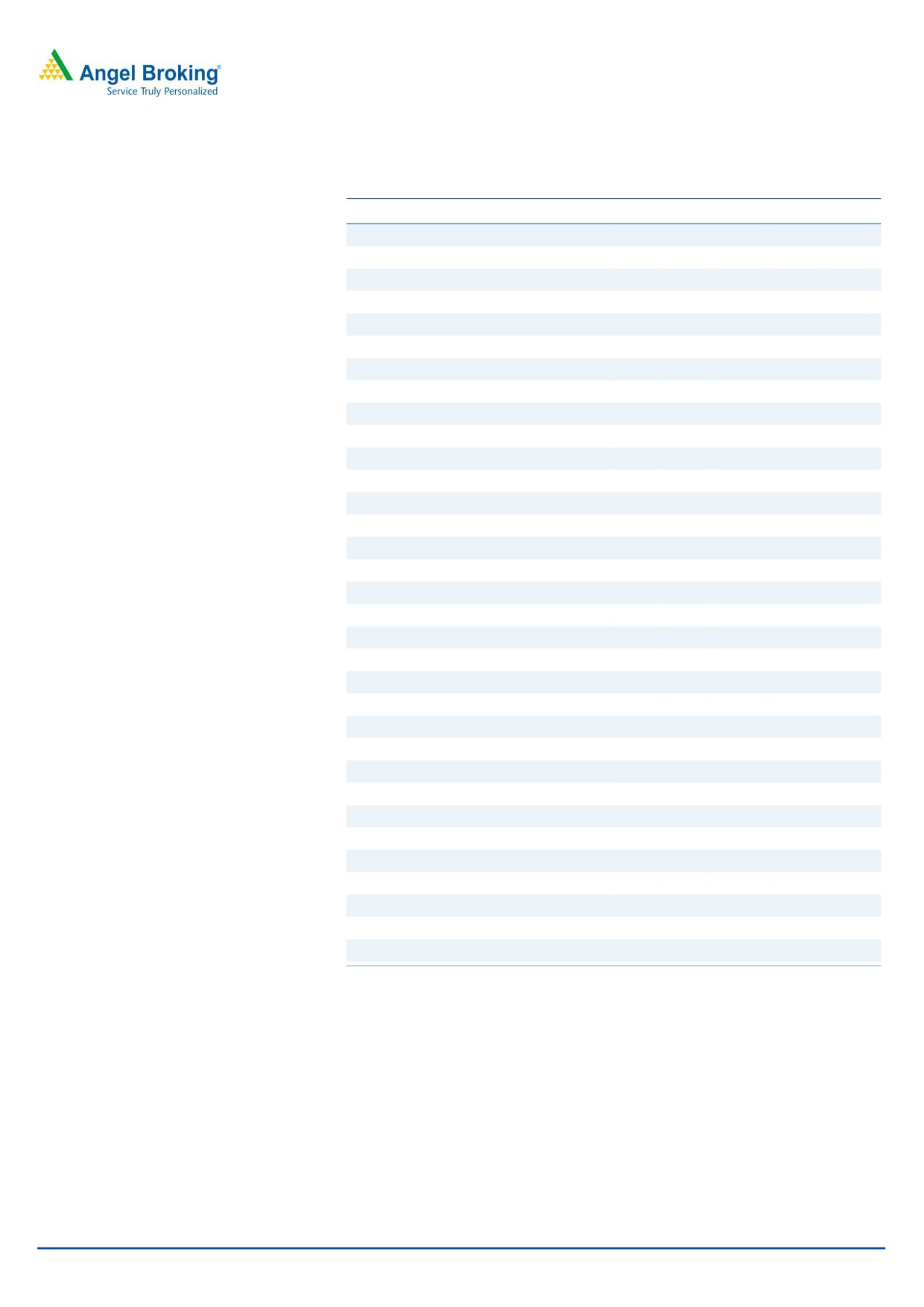

Exhibit 4: ~2.8x yoy growth in PAT

Exhibit 5: Employee costs soars on one off payments

250

1,200

90

20.0

80

18.0

1,000

200

70

16.0

800

14.0

60

150

12.0

600

50

10.0

400

40

100

8.0

200

30

6.0

50

20

4.0

0

10

2.0

0

-200

0

0.0

PAT

yoy growth (%)

Employee cost

as % of sales

Source: Company, Angel Research

Source: Company, Angel Research

Conference call - Key highlights

Company has indicated of tough business environment due to the pricing

pressure in the US.

Natco will focus more on the domestic business and will be selective of low

competition products in the US. The higher free cash flow earned this year will

be used for debt repayment.

gCopaxone launch is almost certain in FY18. Company has said that there is

not much price erosion expected at the moment in gCopaxone franchisee.

gTamiflu sales in FY17 were `705cr which included `404 in profit sharing.

HepC business during the quarter done well and company expects 20-25%

growth in FY18. Onco revenue during FY17 was `322cr.

1QFY18 revenue will also see some positive effect of gTamiflu sales.

Company has filed for suspension of gTamiflu.

Company expects a conservative `1,700cr revenue in FY18 (ex-Copaxone)

with `420cr in PAT. This estimate includes new product launches in India.

Capex for FY18E would be `350cr.

Company is planning to add another line in Guwahati and invest in API

capacity.

Vizag capacity will be ready soon and has not filling from there as of now.

Rest all plants of Natco are current with USFDA.

Company has said that the domestic drug regulator has increased scrutiny of

manufacturing plants and has made plant inspection mandatory for new drug

approvals.

Total debt at the end of the quarter was `80cr and cash position is `230cr.

February 14, 2017

3

Natco Pharma |4QFY2017 Result Update

Investment arguments

Niche therapeutic player in domestic formulations: Natco is a niche

therapeutic segment player in the domestic formulations business (57% of

revenues). It mainly focuses on oncology and Hepatitis C segments. The

oncology segment continues to grow as market dynamics favor while Hepatitis

C franchisee is expected to grow by 20-25% rate over next couple of years due

to huge cost advantage and limited competition. Owing to this, we expect 25%

CAGR in domestic formulations over FY16-FY19E.

Copaxone approval remains a near term trigger: Natco and its marketing

partner Mylan believe that they are the FTF filers on multiple sclerosis drug

Copaxone 40mg. The US District Court has already invalidated several

patents on this drug and Natco/Mylan have successfully addressed all queries

on this drug to the regulator. Additionally the generic manufacturer of 20mg

version, Momenta, has received form 483 on its manufacturing facility which

will delay Teva/Momenta’s gCompaxone 40mg copy. With the June-17 as

mostly likely launch month of gCopaxone 40mg and 20mg, Natco/Mylan are

expected to emerge as the biggest beneficiary from this.

Revlimid opportunity significantly big: Natco has several low competition drugs

in its pipeline which includes gVidara, gDoxil, gForsenol, etc. We believe that

Natco has a significant large opportunity in another limited competition

multiple myeloma drug gRevlimid. Natco has settled litigation regarding

Revlimid (US sales of $4.4bn) with its innovator Celgene and will be able to

launch this drug in 2022E. This will be a very large opportunity considering

the size and growth rate of this drug.

Proven track record in execution and regulatory compliance: Natco has been

able to keep its facilities USFDA compliant since beginning, this is especially

good when several India drug makers have seen adverse regulatory action on

their manufacturing sites. Natco is also going through a period of

extraordinary growth and USFDA compliance is paramount at this stage. We

believe that Natco is a big league player with ability to manufacture limited

competition niche drugs and partner with big companies to sell them.

Outlook and valuation

The bumper earnings in 4QFY17 were mostly expected and there was no surprise

element. We however believe that company is almost launch ready for gCopaxone

in June-2017. We gain significant confidence that Mylan/Natco are most likely to

launch the drug soon which is the most important trigger for the Natco at the

moment. Company has responded all the queries on gCopaxone and from the

commentary in the conference call, it’s just a matter of time before the company

launches this gCopaxone 20mg and 40mg. We value Natco’s base business at

24x of its FY19E EPS to 587 per share and add NPV of R&D pipeline of `471 to

derive new price target of `1,060. Our target indicates 10% upside from the CMP

of `968.

February 14, 2017

4

Natco Pharma |4QFY2017 Result Update

Company background

Natco pharma is a Hyderabad based R&D driven organization. The company has

presence in domestic and global markets and has two main business segments i.e.

API and Formulations. It has seven manufacturing facilities which are approved by

various medical regulatory authorities and prominent ones include US FDA, WHO

GMP, ANVISA. The company mainly operates in the niche therapeutic segments

I.e. Oncology and Hepatitis-C. Natco was earlier pure oncology play in the

domestic market however in 2015; company forayed in the Hepatitis C segment,

diversifying its domestic operations. Further in 2017, company has forayed in

Diabetology and cardiology. In the overseas markets, company is present in US,

Canada, Europe, Australia, Brazil etc. The company mainly focuses on limited

competition products with high margin. In the domestic markets, company is

ranked as #1 in oncology segment while in Hepatitis-C; it has been able to grow

faster than the competition due to early mover’s advantage. IN the US, company

focuses on limited competition products and has partnered with several Indian as

well as overseas partners which helps it mitigate risk and launch products. Natco’s

logistics network in India is well-knit with about 150 marketing personnel and

distributors at strategic points to ensure product availability pan-India.

February 14, 2017

5

Natco Pharma |4QFY2017 Result Update

Profit and loss statement

Y/E March (` cr)

FY15

FY16

FY17

FY18E

FY19E

Total operating income

825

1,080

2,065

1,988

2,131

% chg

11.7

30.9

91.2

(3.7)

7.2

Total Expenditure

612

815

1,382

1,318

1,478

Cost of Materials

242

271

599

537

586

Personnel

137

180

243

304

380

Others Expenses

233

364

539

477

511

EBITDA

213

266

683

670

653

% chg

19.0

24.5

157.3

(2.0)

(2.5)

(% of Net Sales)

25.9

24.6

33.1

33.7

30.7

Depreciation& Amortisation

47

51

54

67

78

EBIT

166

215

629

603

576

% chg

11.6

29.3

192.8

(4.1)

(4.6)

(% of Net Sales)

20.1

19.9

30.5

30.3

27.0

Interest & other Charges

32

23

19

24

24

Other Income

15

10

14

24

24

(% of PBT)

10.0

4.8

2.2

4.0

4.2

Share in profit of Ass.

-

-

-

-

-

Recurring PBT

149

202

624

604

576

% chg

4.1

50.1

209.9

(3.3)

(4.6)

Prior Period & Extra. Exp.

15

-

-

-

-

PBT (reported)

134

202

624

604

576

Tax

4

48

140

157

150

(% of PBT)

2.9

23.8

22.3

26.0

26.0

PAT (reported)

130

154

485

447

426

Add: Share of earnings of ass.

Less: Minority interest (MI)

(4)

(1)

(1)

(1)

(1)

PAT after MI (reported)

135

155

486

448

427

ADJ. PAT

150

155

486

448

427

% chg

45.8

3.4

213.8

(7.8)

(4.6)

(% of Net Sales)

18.1

14.3

23.5

22.5

20.1

Basic EPS (`)

8.1

8.9

27.9

25.7

24.5

Fully Diluted EPS (`)

8.1

8.9

27.9

25.7

24.5

% chg

45.8

3.4

213.8

(7.8)

(4.6)

February 14, 2017

6

Natco Pharma |4QFY2017 Result Update

Balance Sheet Statement

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

SOURCES OF FUNDS

Equity Share Capital

33

35

35

35

35

Reserves& Surplus

813

1,263

1,632

1,923

2,201

Shareholders’ Funds

846

1,298

1,667

1,958

2,236

Minority Interest

5

5

4

4

4

Total Loans

312

113

236

236

236

Deferred Tax Liability

12

14

15

15

15

Other long term liabilities

1

1

1

1

1

Long-term provisions

9

12

12

12

12

Total Liabilities

1,185

1,443

1,935

2,226

2,504

APPLICATION OF FUNDS

Gross Block

886

972

1,149

1,228

1,548

Less: Acc. Depreciation

222

268

322

389

466

Net Block

664

705

827

839

1,081

Intangible assets

46

9

6

6

6

Capital work-in-progress

129

212

363

313

263

Non-current investments

2

0

0

0

0

Long-term loans and advances

57

62

62

62

62

Other non-current assets

4

4

4

4

4

Current Assets

483

832

1,063

1,527

1,650

Inventories

220

357

351

381

409

Sundry Debtors

192

262

475

436

467

Cash

13

45

47

524

579

Loans & Advances

55

104

134

129

139

Other Assets

2

64

56

56

56

Current liabilities

199

380

391

525

563

Net Current Assets

284

452

672

1,001

1,087

Deferred Tax Asset

-

-

-

-

-

Mis. Exp. not written off

-

-

-

-

-

Total Assets

1,185

1,443

1,935

2,226

2,504

Note: Cash includes cash with scheduled banks on dividend current accounts

February 14, 2017

7

Natco Pharma |4QFY2017 Result Update

Cash flow statement

Y/E March (`cr)

FY15

FY16

FY17E

FY18E

FY19E

Profit before tax

134

207

624

604

576

Depreciation

47

51

54

67

78

Change in Working Capital

(86)

(150)

(219)

149

(31)

Interest / Dividend (Net)

30

21

19

24

24

Direct taxes paid

(24)

(46)

(139)

(157)

(150)

Others

(9)

20

-

-

-

Cash Flow from Operations

93

102

340

685

497

(Inc.)/ Dec. in Fixed Assets

(117)

(157)

(328)

(29)

(270)

(Inc.)/ Dec. in Investments

2

2

3

-

-

Cash Flow from Investing

(115)

(155)

(325)

(29)

(270)

Issue of Equity

-

334

0

-

-

Inc./(Dec.) in loans

71

(199)

123

-

-

Interest paid

(30)

(25)

(19)

(24)

(24)

Dividend Paid (Incl. Tax)

(12)

(25)

(117)

(156)

(148)

Effect of currency translation adjustment

(5)

(1)

0

0

0

Cash Flow from Financing

24

85

(13)

(179)

(172)

Inc./(Dec.) in Cash

2

32

1

478

55

Opening Cash balances

11

13

45

47

524

Closing Cash balances

13

45

47

524

579

February 14, 2017

8

Natco Pharma |4QFY2017 Result Update

Key ratios

Y/E March

FY15

FY16

FY17E

FY18E

FY19E

Valuation Ratio (x)

P/E (on FDEPS)

119.4

108.8

34.7

37.6

39.5

P/CEPS

88.4

81.9

31.2

32.8

33.4

P/BV

19.0

13.0

10.1

8.6

7.5

Dividend yield (%)

0.1

0.2

0.7

0.9

0.9

EV/Sales

20.8

15.7

8.3

8.3

7.8

EV/EBITDA

80.4

63.8

25.0

24.7

25.3

EV / Total Assets

14.5

11.7

8.8

7.4

6.6

Per Share Data (`)

EPS (Basic)

8.1

8.9

27.9

25.7

24.5

EPS (fully diluted)

8.1

8.9

27.9

25.7

24.5

Cash EPS

10.9

11.8

31.0

29.5

29.0

DPS

1.2

1.5

6.8

9.0

8.6

Book Value

50.9

74.5

95.7

112.4

128.3

Dupont Analysis

EBIT margin

20.1

19.9

30.5

30.3

27.0

Tax retention ratio

1.0

0.8

0.8

0.7

0.7

Asset turnover (x)

0.7

0.8

1.1

1.2

1.1

ROIC (Post-tax)

14.1

12.0

26.3

26.8

22.5

Cost of Debt (Post Tax)

0.10

0.16

0.06

0.07

0.07

Leverage (x)

0.4

0.1

0.1

(0.1)

(0.2)

Operating ROE

19.0

12.6

29.3

22.8

19.1

Returns (%)

ROCE

14.3

15.2

33.1

27.5

23.3

Angel ROIC (Pre-tax)

14.5

15.7

33.9

36.2

30.4

ROE

15.9

11.9

29.2

22.9

19.1

Turnover ratios (x)

Asset Turnover (Gross Block)

0.9

1.1

1.8

1.6

1.4

Inventory / Sales (days)

97

121

62

70

70

Receivables (days)

85

88

84

80

80

Payables (days)

55

93

46

70

70

WC cycle (ex-cash) (days)

127

116

100

80

80

Solvency ratios (x)

Net debt to equity

0.4

0.1

0.1

(0.1)

(0.2)

Net debt to EBITDA

1.4

0.3

0.3

(0.4)

(0.5)

Interest Coverage (EBIT / Interest)

5.2

9.4

34.0

25.6

24.4

February 14, 2017

9

Natco Pharma |4QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Natco Pharma

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 14, 2017

10