4QFY2016 Result Update | Infrastructure

May 19, 2016

NBCC

ACCUMULATE

CMP

`984

Performance Highlights

Target Price

`1,098

Quarterly Highlights - Consolidated

Investment Period

12 Months

Y/E March (` cr)

4QFY16 4QFY15 3QFY16

% chg (yoy)

% chg (qoq)

Net sales

2,251

1,622

1,358

38.8

65.8

Stock Info

Sector

Infrastructure

EBITDA

120

139

56

(13.7)

115

Net profit

141

134

57

5.9

147

Market Cap (` cr)

11,805

Source: Company, Angel Research;

Net Debt (` cr)

(1,160)

Beta

1.1

National Building Construction Corporation (NBCC) reported a strong 38.8% yoy

52 Week High / Low

1,215/707

increase in revenue for 4QFY2016 to `2,251cr, which is above our estimate of

Avg. Daily Volume

212,239

`2,130cr. Revenue growth during the quarter was on account of 45.6% yoy

Face Value (`)

10

increase in the PMC segment revenue to `2,068cr. The segment accounted for

BSE Sensex

25,705

92% of the company’s 4QFY2016 revenues. Despite strong execution, NBCC

Nifty

7,870

however disappointed us on the margin front; the EBITDA margin for the quarter

Reuters Code

NATO.NS

came in at 5.3%, lower by 324bps on a yoy basis. The miss in the operating

performance percolated down to the PAT level. The PAT at `141cr is lower than

Bloomberg Code

NBCC@IN

our expectation of `186cr while the reported PAT margin declined 196bp yoy to

6.3% for 4QFY2016.

Shareholding Pattern (%)

NBCC‘s order book stands at `37,000cr as of 4QFY2016, indicating an increase

Promoters

90.0

of over 100% on a yoy basis. The current order book to Last Twelve Month (LTM)

MF / Banks / Indian Fls

3.4

sales ratio stands at 6.3x.

FII / NRIs / OCBs

0.0

Indian Public / Others

6.6

Outlook and valuation: Considering the reviving award activity environment, we

expect NBCC to report ~`20,000cr of order inflows each year for FY2017-18E.

Also, emerging opportunities in the redevelopment space, the government’s

Abs. (%)

3m 1yr

3yr

initiative of developing ‘Smart Cities’ and the company’s cash rich status should

Sensex

8.4

(7.0)

30.7

aid its growth. We expect the company to report 27.9% and 45.5% top-line and

NBCC

14.6

21.3

594.7

bottom-line CAGR during FY2016-18E, respectively. Given the bid pipeline and

the company’s huge order book, we are convinced about the company’s earnings

growth prospects over the next few years. Accordingly, we have assigned 20.0x

3-year price chart

P/E multiple to our FY2018E EPS of `55/share to arrive at a price target of

1400

`1,098. Given the 12% upside potential in the stock from the current level, we

1200

maintain our Accumulate rating on the stock.

1000

800

Key Financials (Consolidated)

600

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

400

Net Sales

4,070

4,674

5,838

7,428

9,549

200

% chg

14.8

24.9

27.2

28.5

0

Net Profit

257

278

311

490

659

% chg

8.1

11.8

57.5

34.4

EBITDA (%)

5.9

6.2

6.0

7.9

8.6

Source: Company, Angel Research

EPS (`)

21

23

26

41

55

P/E (x)

45.8

42.4

37.9

24.1

17.9

P/BV (x)

10.4

8.8

7.8

6.2

4.8

RoE (%)

22.6

22.5

21.9

28.8

30.4

RoCE (%)

36.2

39.3

39.4

50.8

50.2

Santosh Yellapu

EV/Sales (x)

2.6

2.3

1.8

1.3

1.0

022-39357800 Ext: 6811

EV/EBITDA (x)

44.1

36.8

29.7

16.4

11.0

Source: Company, Angel Research; Note: CMP as of May 18, 2016

Please refer to important disclosures at the end of this report

1

NBCC | 4QFY2016 Result Update

Exhibit 1: Quarterly Performance (Consolidated)

Particulars (` cr)

4QFY16

3QFY16

% chg (qoq)

4QFY15

% chg (yoy)

FY2016

FY2015

% chg

Net Sales

2,251

1,358

65.8

1,622

38.8

5,760

4,359

32.1

Total Expenditure

2,131

1,302

63.7

1,483

43.7

5,487

4,112

33.5

Cost of materials consumed

188

13

1,393.1

108

74.8

233

180

29.5

Changes in Inv. of FG & WIP

(240)

(42)

nmf

(96)

nmf

(301)

(155)

nmf

Employee Benefits Expense

53

54

(1.6)

47

13.0

226

195

15.6

Other Expenses

40

17

130.0

16

154.9

79

57

38.7

Work & Consultancy Expenses

2,089

1,260

65.8

1,408

48.4

5,251

3,835

36.9

EBITDA

120

56

115.0

139

(13.7)

273

247

10.4

EBIDTA %

5.3

4.1

8.6

4.7

5.7

Depreciation

1

1

15.3

0

36.0

2

2

(4.7)

EBIT

119

55

115.9

139

(13.9)

271

245

10.6

Interest and Financial Charges

14

10

41.0

9

60.6

37

40

(8.6)

Other Income

94

38

146.7

62

53.6

207

188

10.1

PBT before Exceptional Items

200

84

138.9

191

4.4

441

393

12.3

Exceptional Items

0

0

0

0

0

PBT after Exceptional Items

200

84

138.9

191

4.4

441

393

12.3

Tax

58

26

121.2

58

1.1

130

115

13.7

% of PBT

29.2

31.5

30.2

29.5

29.2

PAT bef. Minority Interest

141

57

147.0

134

5.9

311

278

11.8

Minority Interest

(0)

(0)

0

(0)

0

PAT

141

57

147.0

134

5.9

311

278

11.8

PAT %

6.3

4.2

8.2

5.4

6.4

Dil. EPS (after extra-ord. Items)

2.36

0.95

148.4

2.23

5.8

5.19

4.64

11.9

Source: Company, Angel Research; Note: nmf- Not Meaningful

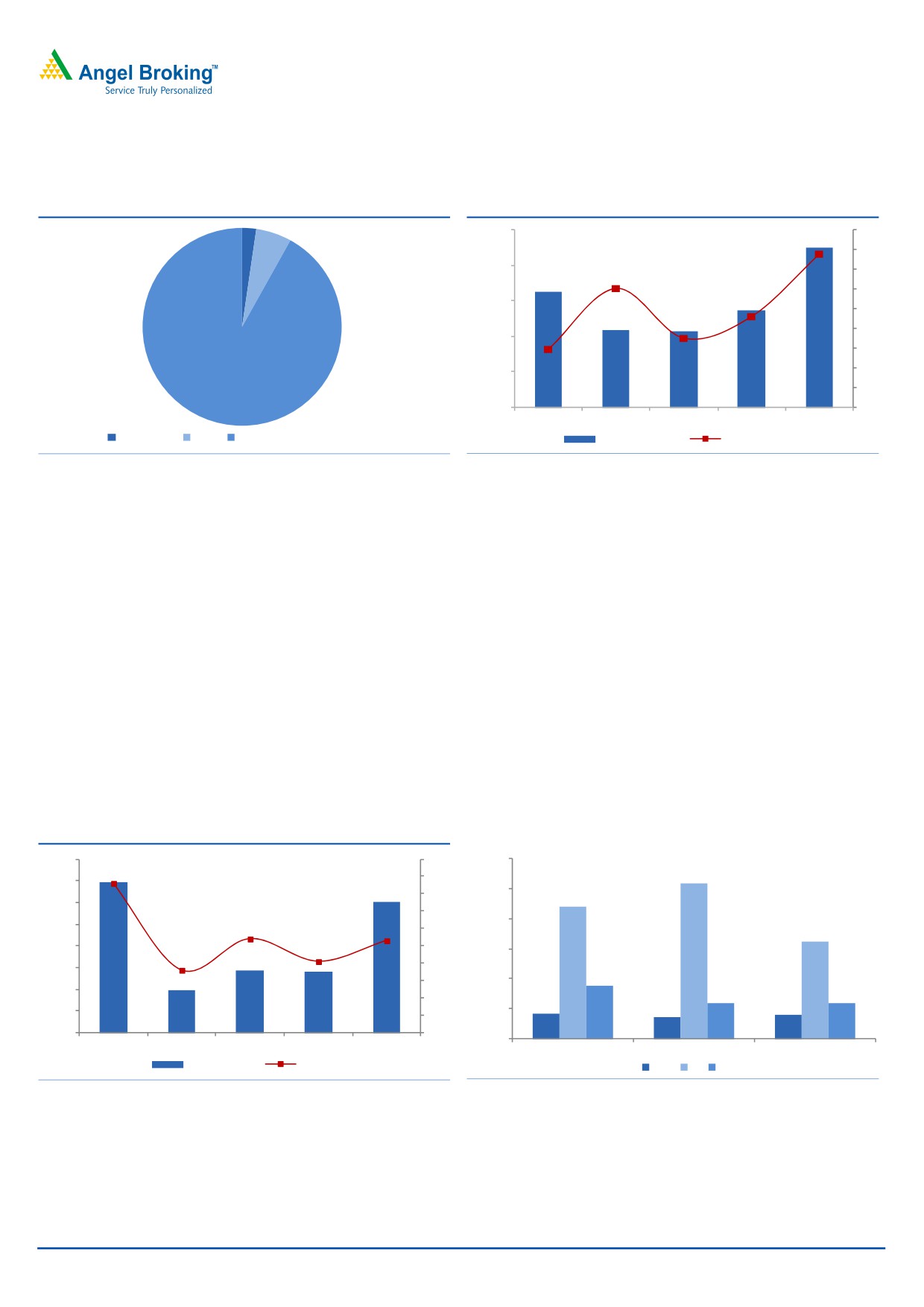

Strong revenue growth driven by PMC segment

NBCC reported a strong 38.8% yoy increase in revenue for 4QFY2016 to

`2,251cr, which is ahead of our estimate of `2,130cr. Revenue growth during the

quarter was led by a 45.6% yoy increase in the PMC segment’s revenue to

`2,068cr; the segment accounted for 92% of the company’s 4QFY2016 revenues.

Further, a 54.0% yoy decline in the Real Estate segment’s revenue was offset by a

46.9% yoy increase in the EPC segment’s revenues. The East Kidwainagar

redevelopment project (reported under the PMC segment) contributed ~`300cr to

the company’s revenues for the quarter.

NBCC reported a 32.1% yoy increase in its FY2016 revenues to `5,760cr. The

surge is owing to a 32.2% yoy increase in the PMC segment’s revenues which

accounted for 90% of the company’s FY2016 revenues.

May 19, 2016

2

NBCC | 4QFY2016 Result Update

Exhibit 2: Revenue bifurcation - 4QFY2016

Exhibit 3: Quarterly revenue trend

2,500

45

2,251

2

6

40

2,000

35

30.1

38.8

1,622

30

1,500

1,358

25

1,089

1,062

14.7

23.0

20

1,000

17.5

15

10

500

5

92

0

0

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

Real Estate

EPC

PMC (inc. Redevelopment works)

Revenue (` cr)

yoy growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

EBITDA margin declines yoy

For 4QFY2016, NBCC disappointed on the margin front with the EBITDA margin

coming in at 5.3%, 324bp lower yoy. The decline in mainly attributable to (1)

74.8% increase in raw material costs, (2) 48.4% increase in work & consultancy

expenses, and (3) 154.9% increase in other expenses. The EBITDA margin for the

quarter was also impacted by a 13.0% yoy increase in employee expenses, which

is mainly on account of (1) higher provision towards post-retirement employee

medical benefits (based on actuarial valuation) and (2) one-time remuneration

made to employees on account of the company attaining Navratna status. The

Management highlighted that these 2 developments are one-time in nature.

Also, all the segments reported a decline in EBIT margins on a yoy basis. The

prime PMC segment reported a 54bp yoy decline in EBIT margin for the quarter to

7.9%.

Exhibit 4: EBITDA margin declines to 5.3%

Exhibit 5: EBITDA margin across business segments decline

160

10

60.0

8.6

51.8

140

9

5.3

50.0

8

44.1

120

7

5.4

4.1

40.0

100

32.5

6

80

5

30.0

3.6

60

4

17.6

3

20.0

40

11.9

12.0

2

8.5

7.3

7.9

20

10.0

1

139

39

58

56

120

0

0

0.0

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

4QFY2015

3QFY2016

4QFY2016

EBITDA (` cr)

EBITDA (%)

PMC RE EPC

Source: Company, Angel Research

Source: Company, Angel Research

For the full year FY2016, the EBITDA margin declined 93bp yoy to 4.7%. The

decline is attributable to a 38.7% and 36.9% increase in other expenses and work

& consultancy expenses, respectively.

May 19, 2016

3

NBCC | 4QFY2016 Result Update

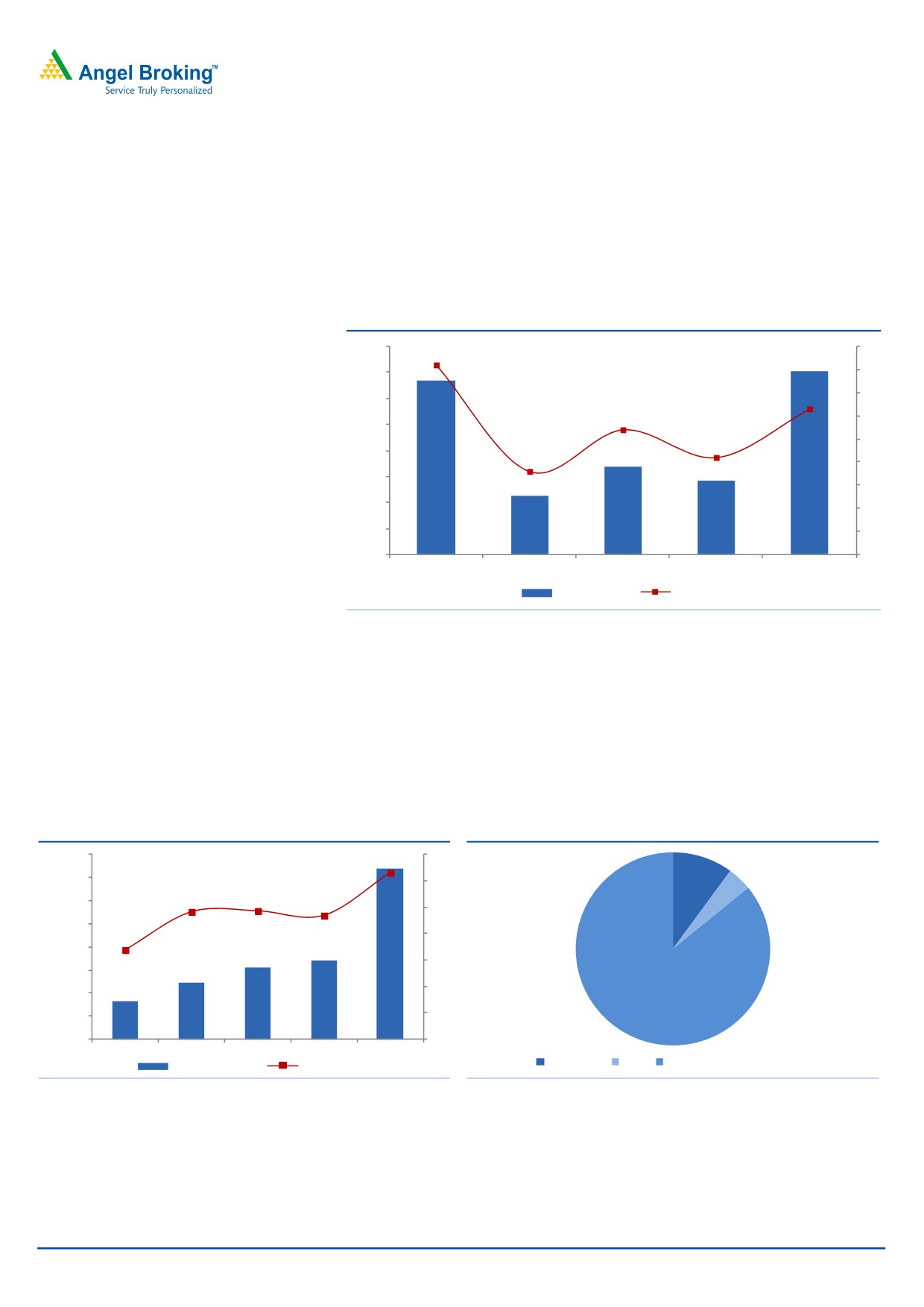

The miss on the EBITDA margin percolated down to the PAT level. The company

reported a PAT of `141cr for the quarter against our expectation of `186cr, while

the reported PAT margin declined 196bp yoy to 6.3%. Further, the company

benefitted from a 53.6% yoy increase in other income to `94cr on the back of

`16cr of provision reversal made towards payments to contractors in the previous

year.

Exhibit 6: PAT margin declines to 6.3%

160

9

8.2

6.3

140

8

7

120

5.4

6

100

4.2

5

80

3.6

4

60

3

40

2

20

1

134

45

67

57

141

0

0

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

PAT (` cr)

PAT (%)

Source: Company, Angel Research

In-line with the EBITDA margin, the PAT margin for FY2016 declined 98bp yoy to

5.4%.

Order book analysis

NBCC reported over `25,000cr of order inflows in FY2016, indicating an over

300% yoy increase.

Exhibit 7: Order book stands at `37,000cr

Exhibit 8: PMC contributes 85% of Order Book

40,000

7

6.3

10

35,000

6

4

4.8

4.9

30,000

37,000

5

25,000

3.4

4.7

4

20,000

17,000

15,427

3

15,000

12,163

8,162

2

10,000

1

5,000

85

0

0

FY2012

FY2013

FY2014

FY2015

FY2016E

Real Estate

EPC

PMC (inc. Redevelopment works)

Order Book (` cr)

OB/ LTM (x)

Source: Company, Angel Research

Source: Company, Angel Research

The company’s order book stands at `37,000cr as of 4QFY2016, indicating over

100% yoy increase. A majority of the order wins were in the PMC segment, which

contributes ~85% of the total order book. The current order book to Last Twelve

Month (LTM) sales ratio stands at 6.3x.

May 19, 2016

4

NBCC | 4QFY2016 Result Update

The Management sounded optimistic in its concall interaction towards the

company being awarded 3 Delhi Re-development projects (at Sarojini Nagar,

Netaji Nagar and Nauroji Nagar) worth `25,000cr in the next 2 months, given the

recent developments and government approvals in place.

Concall Notes & Management Guidance

The company’s Board has withdrawn its earlier proposed follow-on public offer

(FPO), where the proceeds were expected to be used towards the 3 redevelopment

projects. Now the company expects to deploy internal accruals towards these 3

redevelopment projects. Initial equity requirement towards these redevelopment

projects would be in the range of `300-500cr, which in 6-12 months time period,

will be taken back from the project’s cash flows.

No major progress is seen across any works originating from Air India. Works

across 2-3 Bengaluru Waqf Board properties should start sooner and Detailed

Project Report (DPR) is being prepared for newly identified projects.

Drawings are made and DPR is being prepared for DDA and AIIMS projects.

Works for AIIMS projects would start in the next 6 months, whereas, works at DDA

would start in 4QFY2017.

Design works and DPR is being prepared for the Sanjay Lake View & Karkardooma

projects. Works are expected to start by 4QFY2017. Similarly once local bodies

approve (post design works are submitted), works across Chroma Centre project

(PMC project) would start. The Management expects this project to start by

Sep/Oct-2016.

East Kidwainagar re-development project is expected to report 8-10% margins.

The entire outstanding construction works worth `3,500cr would get completed in

the next 2-3 years. After handing over, NBCC would look after the O&M works of

this project for the next 30 years, where the billing across this duration is expected

in the range of `250cr (5% of `5,000cr). The Management has guided that they

are entitled to 20% margins on all the actual expenses incurred.

The company’s Management indicated that it would complete 51% stake purchase

of Hindustan Steelworks for ~`120-150cr in the next few months. The entire debt

outstanding of Hindustan Steelworks would be taken over by the Government of

India. The company would get access to ~`8,000cr of order book, a 7% EBITDA

margin business, and a few land parcels in addition to the existing business.

On the back of strong order inflows and current order book, the company’s

Management has guided for a 30% top-line and 20-25% bottom-line growth for

FY2017E.

The Management expects the company to report FY2017E EBITDA margins

(includes other income) in the range of 8-9%.

May 19, 2016

5

NBCC | 4QFY2016 Result Update

Revision of Estimates

On taking into consideration the company’s FY2016 results and the Management

commentary in the concall interaction, we are fine-tuning our FY2017-18E

estimates.

Exhibit 9: Revision of Estimates

FY2017E

FY2018E

Old

New change %

Old

New change %

Revenues

7,382

7,428

0.6%

9,506

9,549

0.5%

EBITDA

568

584

2.7%

818

825

0.9%

EBITDA %

7.7%

7.9%

8.6%

8.6%

PAT

478

490

2.5%

653

659

0.9%

PAT %

6.5%

6.6%

6.9%

6.9%

Source: Company, Angel Research

Outlook and Valuation

Considering the reviving award activity environment, we expect NBCC to report

~`20,000cr of order inflows each year for FY2017-18E. Post the Management’s

guidance in the recent concall interaction, we expect NBCC to report a 27.9%

top-line CAGR during FY2016-18E to `9,549cr. With expected shift in business

mix towards the high margin re-development works, we expect EBITDA margins to

improve from 6.0% in FY2016 to 8.6% in FY2018E. On back of the better

operating performance coupled with higher other income (given the cash rich

status of the company), we expect PAT margin to also improve from 5.3% in

FY2016 to 6.9% in FY2018E.

We maintain Accumulate with price target of `1,098

We have a strong positive view on NBCC, given its growth prospects as reflected

by its strong order book of `37,000cr (6.3x LTM revenues). Also, emerging

opportunities in the redevelopment space, the government’s initiative of developing

‘Smart Cities’, and the company’s cash rich status, should aid its growth. Given the

bid pipeline and huge order book, we are convinced about the strong earnings

growth potential of the company for the next few years. Accordingly, we have

conservatively assigned 20.0x P/E multiple to our FY2018E EPS of `55/share; we

arrive at a price target of `1,098. Given the 12% upside potential in the stock from

the current level, we maintain our Accumulate rating on the stock.

Company background

National Buildings Construction Corporation (NBCC) is a Navratna PSU company

engaged in the business of Project Management Consultancy (PMC), Engineering

Procurement & Construction (EPC) and Real Estate development.

The PMC business contributed ~90% of FY2016 sales and ~90% of FY2016 EBIT.

NBCC works on the entire project cycle, right from concept stage to commissioning

to civil construction works. It gets PMC contracts on nomination basis, as it is

notified as a Public Work Organization under revised Rule 126 (2) of General

Financial Rules (GFR). The real estate business involves development of residential

and commercial projects on Government/PSU land bank, through the joint

development or land bank development model.

May 19, 2016

6

NBCC | 4QFY2016 Result Update

Profit & loss statement (Consolidated)

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

Net Sales

4,070

4,674

5,838

7,428

9,549

% Chg

14.8

24.9

27.2

28.5

Total Expenditure

3,831

4,386

5,487

6,844

8,724

Land & Materials Consumed

426

299

-68

502

646

Work and Consultancy Expenses

3,169

3,835

5,251

5,944

7,593

Employee benefits Expense

182

195

226

310

380

Other Expenses

55

57

79

89

105

EBITDA

239

288

351

584

825

% Chg

20.8

21.8

66.3

41.2

EBIDTA %

5.9

6.2

6.0

7.9

8.6

Depreciation

1

2

2

3

3

EBIT

237

286

349

581

822

% Chg

20.5

22.1

66.4

41.5

Interest and Financial Charges

22

40

37

50

53

Other Income

134

147

129

169

172

PBT

349

393

441

700

941

Tax

92

115

130

210

282

% of PBT

26.3

29.2

29.5

30.0

30.0

PAT before Extraordinary item

257

278

311

490

659

Extraordinary item

0

0

0

0

0

PAT before Minority Interest

257

278

311

490

659

Minority Interest

0

0

(0)

(0)

0

Share of Profit/ (Loss) of Asso.

0

0

0

0

0

PAT after MI, profit share from Asso.

257

278

311

490

659

% Chg

8.1

11.8

57.5

34.4

PAT %

6.3

6.0

5.3

6.6

6.9

Diluted EPS

21

23

26

41

55

% Chg

8.1

11.8

57.5

34.4

May 19, 2016

7

NBCC | 4QFY2016 Result Update

Balance sheet (Consolidated)

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

Sources of Funds

Equity Capital

120

120

120

120

120

Reserves Total

1,021

1,218

1,385

1,776

2,320

Networth

1,141

1,338

1,505

1,896

2,440

Minority Interest

0

0

(0)

(0)

0

Total Debt

0

0

0

0

0

Long-term Liabilities

53

45

61

54

56

Total Liabilities

1,194

1,383

1,566

1,950

2,496

Application of Funds

Gross Block

35

42

49

53

56

Accumulated Depreciation

13

15

18

22

25

Net Block

23

26

31

31

31

Capital WIP

0

0

31

22

16

Investments

100

146

219

161

161

Goodwill

0

0

0

0

0

Current Assets

Inventories

1,020

1,173

1,443

1,536

2,030

Sundry Debtors

1,315

1,704

2,006

2,080

2,707

Cash and Bank Balance

1,201

1,067

1,160

2,059

2,548

Loans & Advances

515

612

616

662

860

Other Current Asset

11

16

8

17

18

Current Liabilities

3,013

3,381

3,978

4,650

5,908

Net Current Assets

1,047

1,192

1,255

1,704

2,257

Deferred Tax Asset

23

20

31

31

31

Total Assets

1,194

1,383

1,566

1,950

2,496

May 19, 2016

8

NBCC | 4QFY2016 Result Update

Cash flow statement (Consolidated)

Y/E March (` cr)

FY14 FY15 FY16E FY17E FY18E

Profit before tax

334

391

441

700

941

Depreciation & Amortisation Exp.

1

2

2

3

3

Other non-Cash Expenses

(122)

(158)

(158)

(171)

(177)

Change in Working Capital & Oth. Adj.

(619)

(342)

(7)

497

(5)

Cash Generated from Operations

(407)

(107)

278

1,030

762

Direct taxes paid

(32)

(47)

(143)

(225)

(300)

Net Cash Flow from Operations

(439)

(154)

135

805

462

(Inc)/ Dec in Fixed Assets

0

(7)

(8)

(4)

(3)

(Inc)/ Dec in Investments

718

(140)

(131)

8

(70)

(Inc)/ Dec in Other Investing Cash Flows

101

142

129

139

145

Cash Flow from Investing

818

(5)

(10)

143

72

Issue/ (Buy Back) of Equity

0

0

0

0

0

Inc./ (Dec.) in Loans

0

0

0

0

0

Dividend Paid (Incl. Tax)

(53)

(70)

(87)

(99)

(115)

Other Financing Cash Flows

0

0

0

0

0

Cash Flow from Financing

(53)

(70)

(87)

(99)

(115)

Inc./(Dec.) in Cash

327

(229)

38

849

419

Opening Cash balance & Oth. Adj.

569

896

667

705

1,554

Closing Cash balances

896

667

705

1,554

1,973

May 19, 2016

9

NBCC | 4QFY2016 Result Update

Key ratios

Y/E March

FY14

FY15

FY16

FY17E

FY18E

Valuation Ratio (x)

P/E (on FDEPS)

45.8

42.4

37.9

24.1

17.9

P/CEPS

45.6

42.1

37.7

23.9

17.8

Dividend yield (%)

0.5

0.6

0.6

0.7

0.8

EV/Sales

2.6

2.3

1.8

1.3

1.0

EV/EBITDA

44.1

36.8

29.7

16.4

11.0

EV / Total Assets

8.8

7.7

6.7

4.9

3.6

Per Share Data (`)

EPS (fully diluted)

21.5

23.2

25.9

40.8

54.9

Cash EPS

45.6

42.1

37.7

23.9

17.8

DPS

5.0

5.5

6.2

7.0

8.1

Book Value

95

112

125

158

203

Returns (%)

RoCE (Pre-tax)

36.2

39.3

39.4

50.8

50.2

Angel RoIC (Pre-tax)

32.6

32.4

31.8

39.5

40.7

RoE

22.6

22.5

21.9

28.8

30.4

Turnover ratios (x)

Inventory / Sales (days)

91

86

82

73

68

Receivables (days)

118

118

116

100

91

Payables (days)

287

266

245

230

221

Leverage Ratios (x)

D/E ratio (x)

0.0

0.0

0.0

0.0

0.0

Interest Coverage Ratio (x)

10.6

7.1

9.5

11.7

15.7

May 19, 2016

10

NBCC | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

NBCC

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

May 19, 2016

11