Initiating Coverage | Auto Ancillary

July 21, 2015

Minda Industries

BUY

CMP

` 525

Outpacing industry on product & customer consolidation

Target Price

` 652

Minda Industries Ltd (MIL) is a diversified auto ancillary supplier, manufacturing

Investment Period

12 Months

products such as switches, horns, lights, fuel caps, and cylinder valves. It is the

market leader in the switch segment with a market share of 67%, and also the

horn segment where it has a market share of 47%.

Stock Info

Sector

Auto Ancillary

New product introductions and increased sourcing from clients

to enable company outpace the automotive industry

Market Cap (` cr)

833

MIL has historically outpaced the automotive industry growth by consistently

Net Debt (` cr)

180

introducing new high value products which enhance the kit value per vehicle. The

Beta

0.9

company has forged alliances with global technology players and has also taken

52 Week High / Low

655 / 283

the acquisition route to introduce high value products. Given its focus on

innovation and its varied product range, the company has gained access to new

Avg. Daily Volume

1,176

platforms of clients, thus enabling it to gain market share. Over the next two

Face Value (`)

10

years, MIL aims to introduce alloy wheels in JV with Kosei, launch electronic

BSE Sensex

28,182

horns, and manufacture batteries with Panasonic as its technology partner, in the

domestic market. This will enable it to further move up the value chain and

Nifty

8,529

enhance the content per vehicle to the customers. Also, MIL aims to enhance

Reuters Code

MINDA.BO

supplies to its existing clientele such as Hero Motocorp, Honda Motorcycles and

Bloomberg Code

MINDA@IN

Scooters India (HMSI) and Hyundai India by securing supply contracts for their

new platforms. We believe MIL is well poised to outgrow the automotive industry

and expect it to post a CAGR of 14% in revenue over FY2015-17.

Shareholding Pattern (%)

Subsidiaries’ turnaround and better capacity utilization to

Promoters

70.9

augment margins

MF / Banks / Indian Fls

11.0

MIL is aiming to enhance its subsidiaries’ profitability, which account for about

35% of the consolidated turnover. FY2015 marked a turnaround in its

FII / NRIs / OCBs

8.6

subsidiaries’ performance, with them reporting a profit of `5cr as against a loss

Indian Public / Others

9.5

of `19cr in FY2014. Going ahead, better capacity utilization coupled with

increased sourcing from low cost domestic units will help its key subsidiaries -

Clarton Horns and Minda Kyoraku - to post an improvement in margins. Similarly,

operating leverage on back of double digit top-line growth would also enhance overall

Abs. (%)

3m 1yr 3yr

margins. We estimate MIL’s margins to improve by 140bp over the next two years.

Sensex

1.8

9.6

64.2

Outlook and valuation: MIL has evolved from being a switch player to an

Minda

(5.1)

52.2

224.1

ancillary supplier having a diverse product range viz switches, horns, lightings,

fuel caps, and cylinder valves. The company is aiming to further enhance the

product range and move up the value chain by introducing new products like

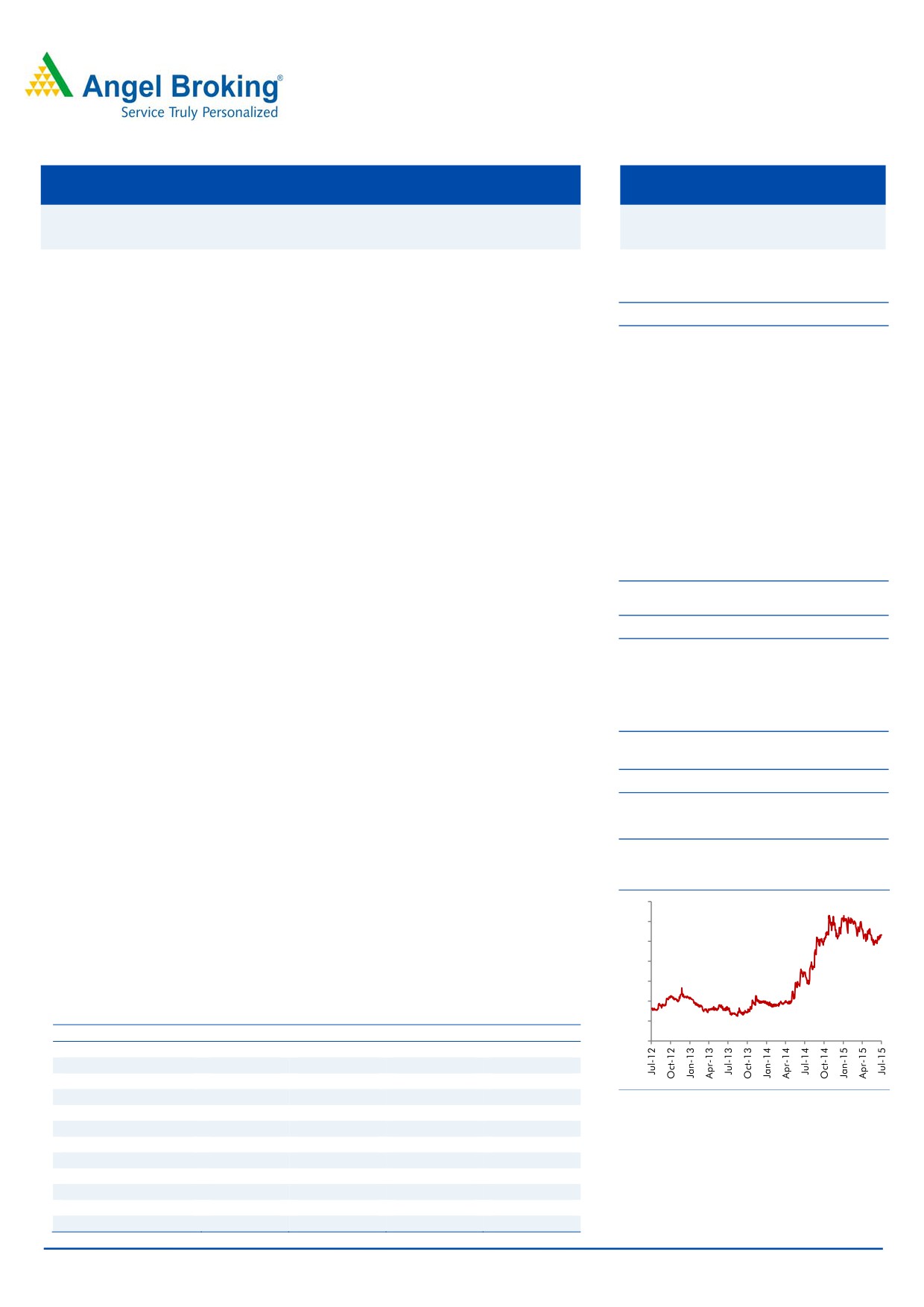

3-Year Daily price chart

alloy wheels and electronic horns. We expect MIL to clock a robust 14% top-line

700

growth over the next two years. Further, operating leverage and improvement

600

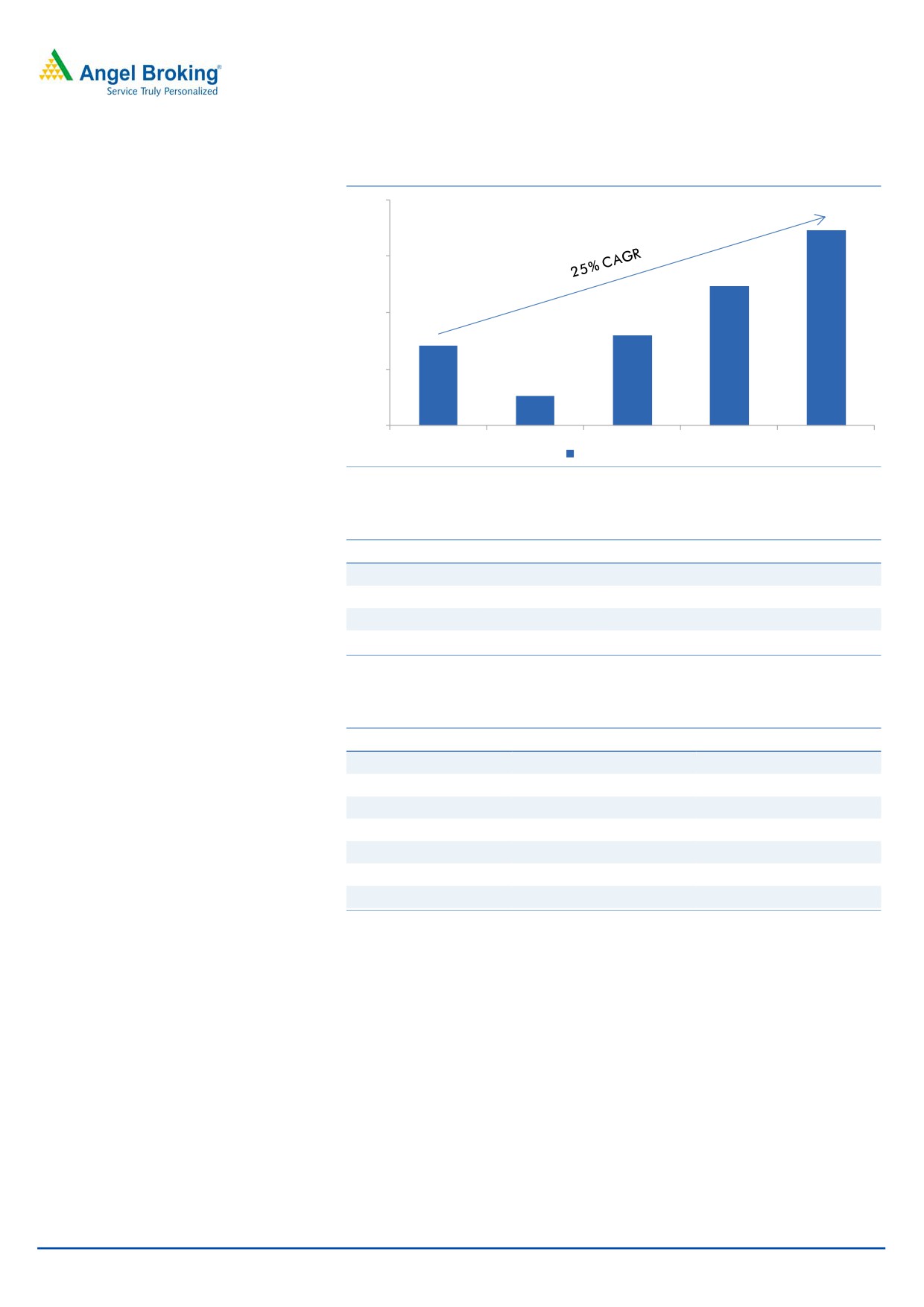

in margin of subsidiaries would lead to a CAGR of 25% in earnings over

500

FY2015-17. MIL is a well diversified Tier 1 ancillary player, available at an

400

attractive valuation. We initiate coverage on the stock with a Buy recommendation

300

and target price of `652 (based on 12x FY2017 earnings).

200

Key financials

100

Y/E March (` cr)

FY2014

FY2015E

FY2016E

FY2017E

0

Net sales

1,706

2,227

2,500

2,889

% chg

27.3

30.5

12.3

15.5

Net profit (Adj.)

6

56

62

86

% chg

(77.0)

762.9

12.5

38.0

Source: Company, Angel Research

EBITDA margin (%)

4.6

6.9

7.6

8.3

EPS (`)

4.1

35.0

39.4

54.3

P/E (x)

129.4

15.0

13.3

9.7

P/BV (x)

2.7

2.2

1.9

1.6

RoE (%)

2.1

14.6

14.1

16.3

RoCE (%)

5.7

14.7

15.0

18.4

Bharat Gianani

EV/Sales (x)

0.6

0.5

0.4

0.4

022-39357800 Ext: 6817

EV/EBITDA (x)

13.9

6.6

5.7

4.3

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Minda Industries | Initiating Coverage

Investment Arguments

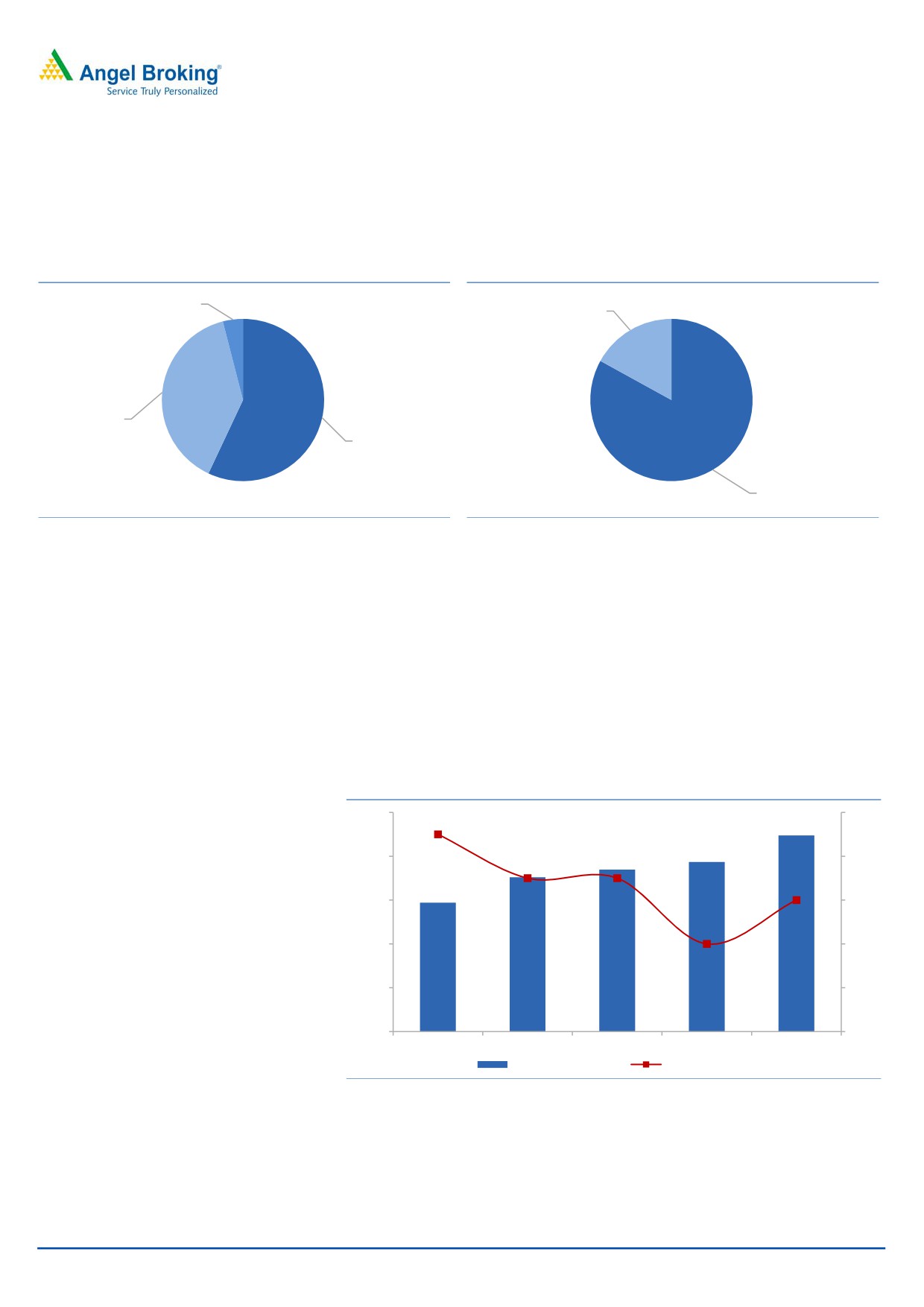

Diversified product profile with leadership position in switches

and horns

Over the years, MIL has successfully evolved from being a switch player to an auto

ancillary supplier dealing in multiple products. Today, MIL manufactures a broad

array of products viz switches, horns, lighting equipments and a host of other

products viz blow moulds, die casts, fuel caps and alternative fuel kits. The

company has forged technical agreements with global majors and has also made

acquisitions in order to enhance its product offerings.

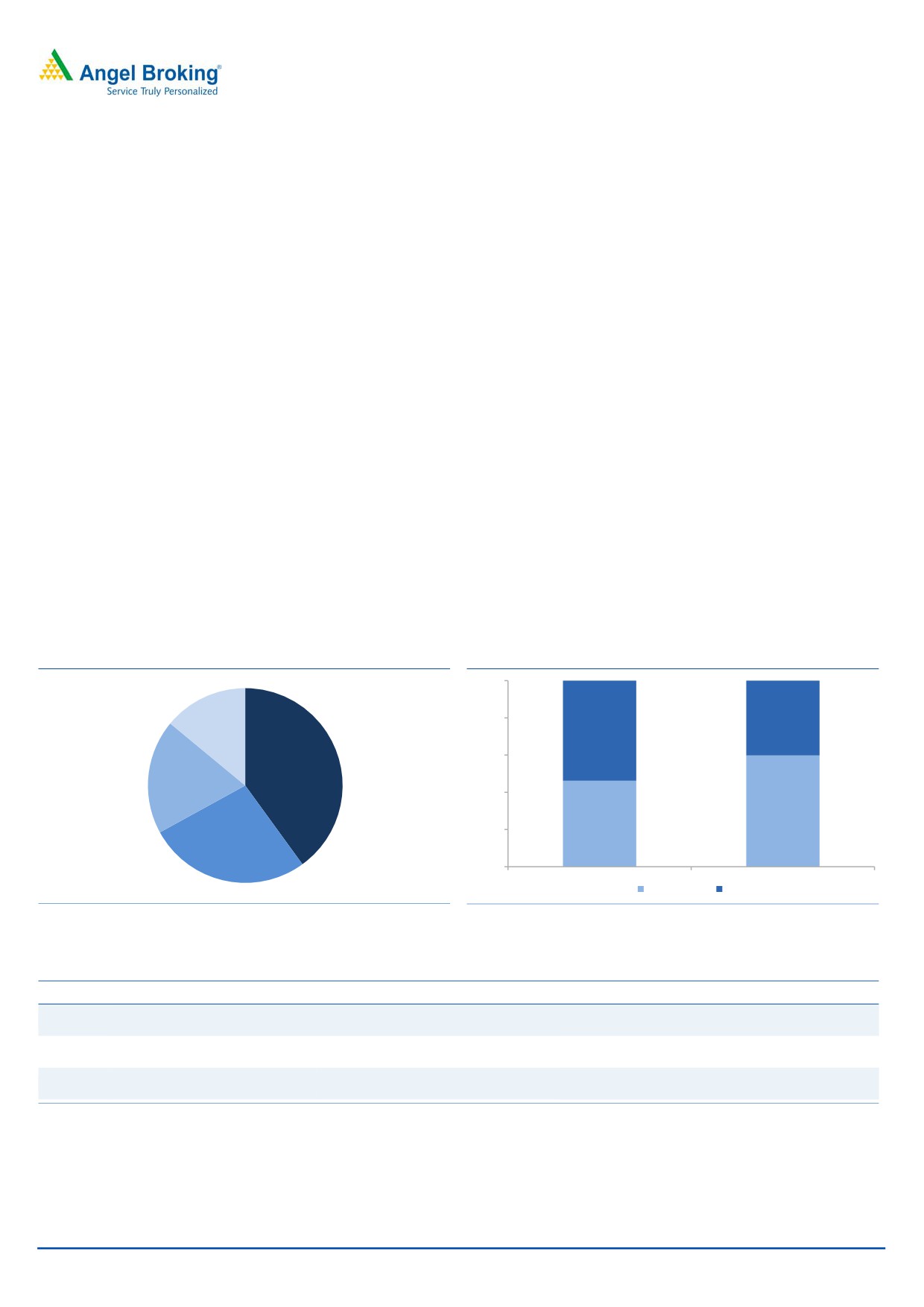

MIL is the market leader in the switch segment, commanding a share of 67%.

Further, with the acquisition of Clarton Horns, MIL has emerged as the second

largest horn player globally and leader in the domestic market with a share of

47%. MIL’s revenue mix is pretty diversified with switch and horn segments

contributing 40% and 27%, respectively, to overall revenues. The lighting segment

and others segments (comprising of blow moulds, die casts and fuel caps) account

for 19% and 14% of revenues, respectively. MIL has successfully leveraged its

strong OEM relationship to continuously broaden its product profile, thereby

enabling it to improve the kit value per vehicle. Further, MIL has manufacturing

presence in all the major automotive hubs across Northern, Western and Southern

regions of the country, which facilitates close proximity to the customers.

Exhibit 1: Segmentwise breakup (Consolidated)

Exhibit 2: Categorywise breakup

100%

40%

80%

Others, 14%

54%

60%

Switches, 40%

Lighting, 19%

40%

60%

46%

20%

Horns, 27%

0%

FY11

FY15

Non switch

Switch

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 3: Manufacturing footprint

Zone

Location

2W client

4W client

Haridwar, Pantnagar, Manesar,

Hero Motocorp, Honda Motorcycles

Maruti Suzuki, M&M, Tata Motors, Honda India,

Northern

Sonepat, Bawal

& Scooters India , Yamaha India

Eicher, Swaraj Mazda, Escorts, Swaraj Mazda

Volkswagen India, Tata Motors, M&M,

Western

Pune, Aurangabad

Bajaj Auto

General Motors, Fiat

Nissan, Renault, Hyundai India, Ford, Tata Motors,

Southern

Bangalore, Hosur, Chennai

TVS Motors, Royal Enfield

Toyota, Tata Motors, Ashok Leyland

Source: Company, Angel Research

July 21, 2015

2

Minda Industries | Initiating Coverage

Exhibit 4: MIL milestones

Foundation of UNO MINDA, NK

Blow Molding Manufacturing Starts in

1958

Minda Group

2008

Bangalore

Started with Ammeter Manufacturing

Design & Development of Alt Fuel Kits

Manufacturing of Automotive Switches

2009

1960

Die Casting Mfg

Manufacturing of Automotive Lighting

2010

1980

Products

Blow Molding Manufacturing starts in

2011

Bawal

Started Horn Manufacturing

Started production of Wheel Cover

1993

Manufacturing of Automotive 4 W

Started production of Fuel Cap

1995

Switches and Heater Control Panels

2012

Acquisition of Clarton Horns, Spain

Switch Manufacturing in Pune

2013

Incorporation of Trading Company in

2001

Kit Integration of CNG/LPG Kits

Brazil

Set Up of Manufacturing facility in

Entered into JV with Panasonic for

2005

Indonesia

2014

battery division

Started Battery Manufacturing

Entered into JV with Kosei Group for

2007

2015

Alloy Wheel

1958-2007

2008-2015

Source: Company, Angel Research

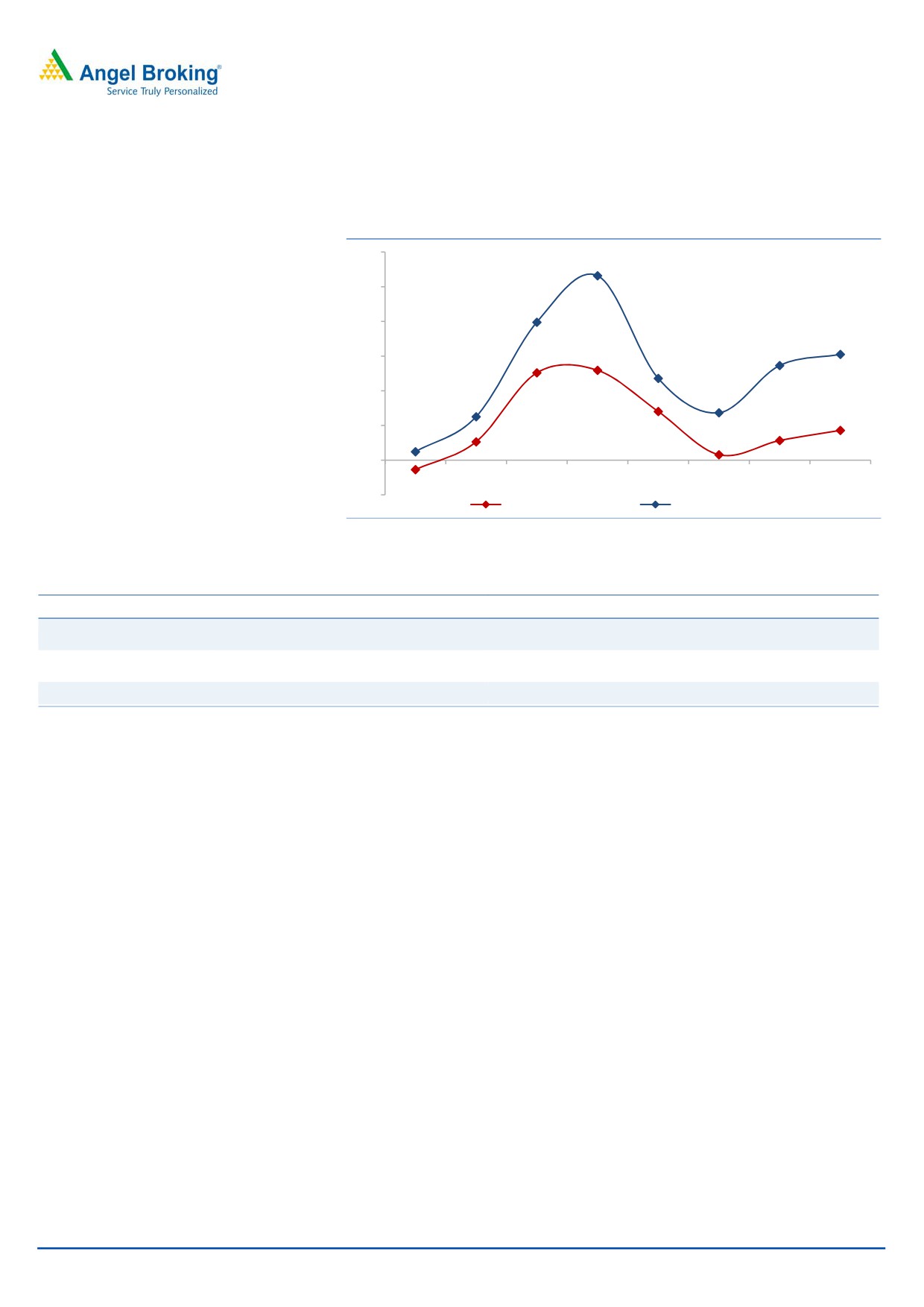

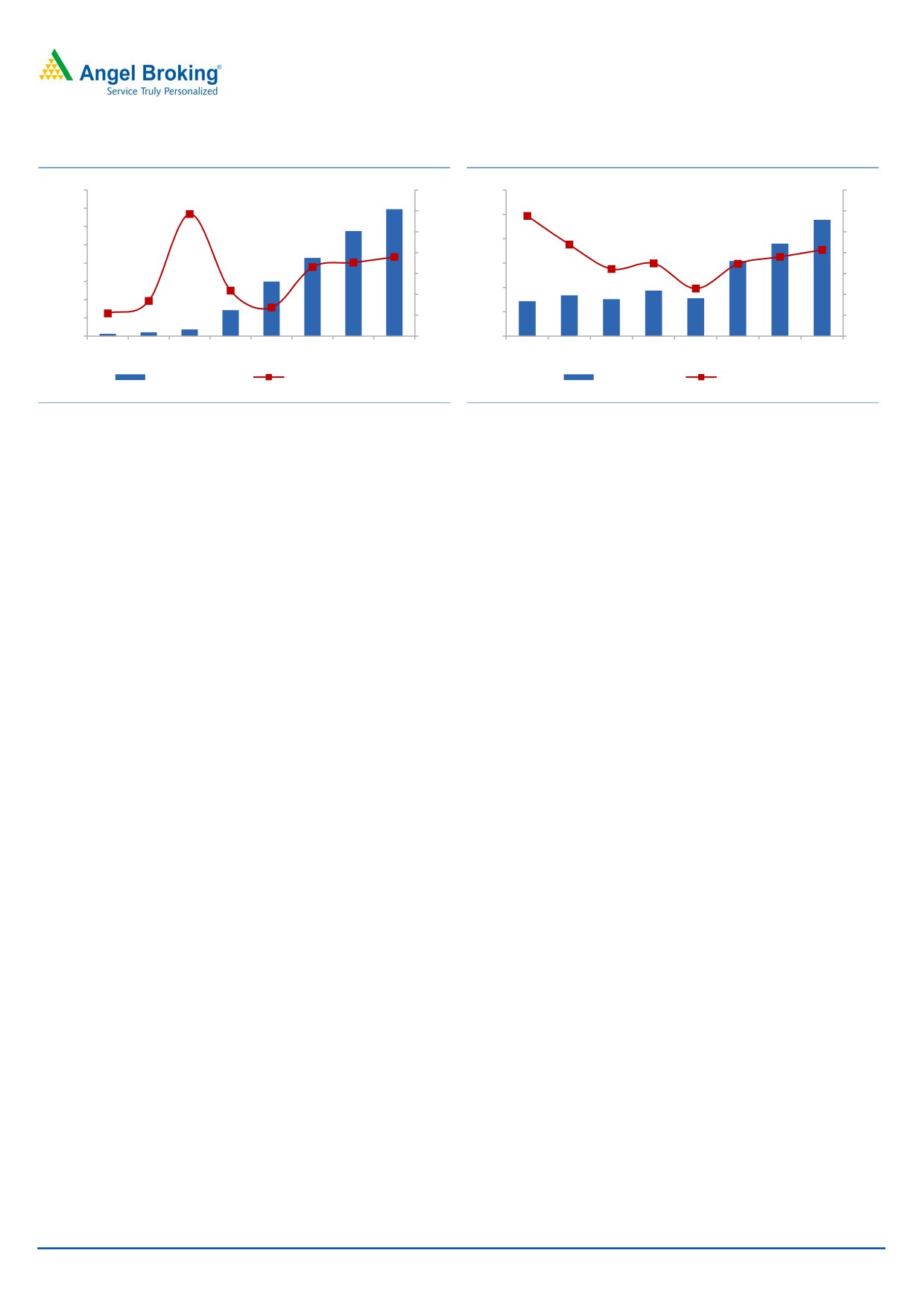

New product introductions help company to outpace industry

New product introductions have enabled MIL to consistently outgrow the

automotive industry. During FY2007-FY2015, the automotive industry has grown

at a CAGR of 10% while MIL’s revenues have grown at a CAGR of 25% over the

same period. MIL has focused on moving up the value chain and has evolved from

being a switch supplier. Over the last few years, it has introduced high value and

high margin products such as head lamps, tail lamps and brake lights within the

lighting division. With the acquisition of Clarton Horns, MIL has acquired the

business of high value electronic horning systems (Clarton Horns supplies to luxury

car makers - Mercedes, BMW, Porsche, Bentley). Also, MIL introduced fuel caps

and cylinder valves in its product portfolio, which further enrich its profile.

Technology and innovation are at the forefront of the company’s strategy. MIL

currently has 95 patented products which has led to it emerging as a leading

diversified ancillary player. MIL has successfully leveraged its strong OEM

relationship to supply new products and enhance the kit per vehicle. In order to

maintain the outperformance, MIL would be venturing into manufacturing alloy

wheels in joint venture with Kosei; it has already secured orders from Maruti and

M&M. The production is expected to commence in 2HFY2017 and is expected to

boost the top-line. Further, MIL has also entered into a technological agreement

July 21, 2015

3

Minda Industries | Initiating Coverage

with Panasonic, Japan for manufacture of automotive batteries. Batteries would be

sold to the existing clients and the production is likely to commence in 2QFY2016.

Exhibit 5: MIL has historically outpaced automotive industry

60

50

40

30

20

10

0

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

(10)

Auto industry growth

Minda Industries growth

Source: Company, Angel Research

Exhibit 6: New products planned

Product

Technology Partner

Prospective clientele

All 4W customers. Has already received confirmed orders

Alloy wheels

Kosei, Japan

from Maruti Suzuki and M&M

All 4W customers. Has already commenced supplies

Electronic Horns

Acquired post Clarton acquisition

to Hyundai India

Battery

Panasonic, Japan

All 2W and 4W customers

Source: Company, Angel Research

July 21, 2015

4

Minda Industries | Initiating Coverage

Increased supplies to customers and new customer acquisitions

drive growth

MIL has been successful in penetrating new platforms of its customers. Product

innovation coupled with broader product offerings has enabled MIL to increase its

share of supplies. OEM players are looking for vendor consolidation which bodes

well for suppliers like MIL who are constantly adding new high value products to

their portfolios. Further, MIL also follows the acquisition route in order to gain

access to new customers.

Post the split of Hero Honda, MIL has increased supplies to both Hero Motocorp as

well as Honda Motorcycles and Scooters India. Hero as well as HMSI currently

contribute about 4% of MIL’s standalone revenues as compared to less than 1% in

FY2010. Further, post the acquisition of Clarton Horns, MIL has now gained

access to new premium OEMs such as Mercedes, BMW, Porsche and Bentley. MIL

has also commenced horn supplies to Hyundai India post the Clarton Horns

acquisition. Also the proposed merger of Indonesia based PT Minda Asean

Automotive and Vietnam based SAM Global PTE would enable MIL to tap new

platforms of premium Japanese two-wheeler customers namely Yamaha, Suzuki

and Kawasaki.

Exhibit 7: Customer contribution

Customers

% of stdl rev FY11

% of stdl rev FY15

Honda Motorcycles & Scooters India

less than 1%

10%

Hero Motocorp

less than 1%

4%

M&M

2%

4%

Royal Enfield

less than 1%

4%

Source: Company, Angel Research

Subsidiaries’ margin improvement coupled with better capacity

utilization to improve margins

MIL’s subsidiaries witnessed a marked improvement in their profitability in FY2015.

After posting cumulative losses of `19.6cr in FY2014, the subsidiaries contributed

`5cr to profits in FY2015. The subsidiaries contribute by about 35% to the

consolidated revenues of MIL. The company’s Spain based subsidiary turned

around in FY2015, reporting a PBT of `1.8cr as compared to a loss of `11.4cr in

the previous year. Similarly other subsidiaries, MJ Casting (die casting

manufacturer) and Minda Kyoraku (makes blow mould products) reported reduced

losses during the year.

MIL is focusing on further improvement in margins of its subsidiaries. MIL

subsidiary Clarton aims to source parts from the Indian plants. Low cost domestic

manufacturing would reduce the costs for Clarton Horns, resulting in margin

improvement. Also, its other subsidiaries Minda Kyoraku and MJ Casting, are

estimated to turnaround in FY2016 on account of operating leverage and cost

control initiatives. Improving capacity utilization in new facilities at Hosur (for switch

segment) and Manesar (for lighting segment) would further enhance the

profitability of MIL. On back of better capacity utilization due to recovery in the

automotive segment, and operating leverage, MIL is targeting double-digit margin

over the next two to three years as against current margins of 7%. We estimate

MIL’s margins to improve from 6.9% in FY2015 to 8.3% in FY2017.

July 21, 2015

5

Minda Industries | Initiating Coverage

Exhibit 8: Subsidiaries financial performance

Exhibit 9: EBIDTA Margin trend

1,600

8

300

14

1,400

6

12

250

1,200

4

10

200

1,000

2

8

800

150

0

6

600

100

(2)

4

400

50

200

(4)

2

0

(6)

0

0

FY10

FY11

FY12

FY13

FY14

FY15

FY16E FY17E

FY10

FY11

FY12

FY13

FY14

FY15

FY16E FY17E

Revenues (` cr)

PAT Margins (%)

EBIDTA (` cr)

Margins (%)

Source: Company, Angel Research

Source: Company, Angel Research

July 21, 2015

6

Minda Industries | Initiating Coverage

Outlook and Valuation

MIL has evolved from being a switch player to an ancillary supplier having a

diverse product range viz switches, horns, lightings, fuel caps, and cylinder valves.

The company is aiming to further enhance the product range and move up the

value chain by introducing new products like alloy wheels and electronic horns. We

expect MIL to clock a robust 14% top-line growth over the next two years.

Further, operating leverage and improvement in margin of subsidiaries would lead

to a CAGR of 25% in earnings over FY2015-17. MIL is a well diversified Tier 1

ancillary player, available at an attractive valuation. We initiate coverage on the

stock with a Buy recommendation and target price of `652 (based on 12x FY2017

earnings).

Exhibit 10: One-year forward P/E band

1,000

800

600

400

200

0

Price (`)

4x

8x

12x

16x

20x

Source: Company, Angel Research

Company Background

Minda Industries Ltd (MIL) is the flagship company of the Uno Minda Group. Uno

Minda is a leading Tier 1 supplier of Proprietary Automotive Solutions to OEMs

having 37 manufacturing plants spread across India, Indonesia, Vietnam & Spain.

Further it has design centers in Taiwan and Japan, and sales offices in USA,

Europe and Vietnam. The Uno Minda Group has a diversified product portfolio

which includes switches, handle bar assemblies, electronics & sensors, automotive

lamps, automotive horns, alternate fuel systems and CNG-LPG kits, automotive

batteries, blow molding components, seat belts, alloy wheels, wheel covers, air

filtration systems, die casting components, src, cylinders, fuel caps, body sealing,

car infotainment systems, air brakes, clutch actuation systems and automatic gear

shifters. Innovation is the key thrust area for the group and it currently holds 95

registered patents and 127 design registrations.

MIL has a well diversified portfolio with 40% of the revenues accruing from the

switch division. The horn segment is the second largest contributor accounting for

27% of the revenues. The lighting segment constitutes about 19% of the revenues

while the other segment (consisting of fuel caps, CNG kits and batteries) forms

about 14% of the top-line.

July 21, 2015

7

Minda Industries | Initiating Coverage

The two-wheeler segment contributes the bulk of the revenues (approximately 57%)

for MIL. Passenger car is the next big segment constituting 39% of the top-line.

MIL’s supplies are largely OEM driven, which form 83% of sales, while the rest is

contributed by the replacement segment.

Exhibit 11: Segmentwise breakup

Exhibit 12: Categorywise breakup

Others, 4%

Aftermarket,

17%

Passenger

cars, 39%

Two wheelers,

57%

OEM , 83%

Source: Company, Angel Research

Source: Company, Angel Research

Business segment information

Switch segment

Switch is the oldest and the largest segment for MIL. MIL is the market leader in

switches commanding a market share of 67%. The segment reported a CAGR of

11% over FY2011-FY2015. Switches are supplied to two-wheeler customers.

Within the switch segment, Bajaj Auto is the largest client contributing about 46%

of revenues. HMSI, TVS Motor and Hero Motocorp contribute 11%, 10% and 6% of

revenues, respectively.

Exhibit 13: Switch division revenue and margin trend

1,000

14%

800

12%

600

10%

400

8%

200

6%

0

4%

FY11

FY12

FY13

FY14

FY15

Revenues (` cr)

EBIDTA Margin (%)

Source: Company, Angel Research

Lighting segment

Lighting division forms 19% of MIL’s top-line. The segment reported a CAGR of

16% over FY2011-FY2015. The 4W segment is the biggest customer for lighting

(contributes 85% of revenues). Within the lighting divison, Maruti Suzuki is the

July 21, 2015

8

Minda Industries | Initiating Coverage

largest client contributing about 37% of sales. M&M and Volkswagen India form

about 12% and 9% of sales, respectively. HMSI and Royal Enfield form 6% and 5%

of sales, respectively.

Exhibit 14: Lighting division revenue and margin trend

500

14%

400

12%

300

10%

200

8%

100

6%

0

4%

FY11

FY12

FY13

FY14

FY15

Revenues (` cr)

EBIDTA Margin (%)

Source: Company, Angel Research

Horns segment

The division currently contributes about 27% of the revenues of MIL. MIL is the

largest Indian horn manufacturing company with a 47% market share. Horn

segment revenues have leapfrogged post the acquisition of Clarton Horns, Spain.

Top-line has grown from `140cr in FY2011 to about `534cr in FY2015. 4W

customers contribute bulk of the revenues (83%) of the division.

Exhibit 15: Horn divison revenue and margin trend

600

16%

14%

500

12%

400

10%

300

8%

6%

200

4%

100

2%

0

0%

FY11

FY12

FY13

FY14

FY15

Revenues (` cr)

EBIDTA Margin (%)

Source: Company, Angel Research

Others

Other products of MIL include fuel caps, blow moulds, die casting, CNG/LPG kits

and automotive batteries. The division has clocked robust CAGR of 25% over the

last four years. 4W and 2W players contribute equally to the division’s revenues.

July 21, 2015

9

Minda Industries | Initiating Coverage

Exhibit 16: Other segment growth trend

400

300

200

100

0

FY11

FY12

FY13

FY14

FY15

Revenues (` cr)

Source: Company, Angel Research

Exhibit 17: Divisionwise break-up

Segment

% of consol rev

Key clientile

Switch

40%

Bajaj Auto, HMSI, TVS Motors

Lighting

19%

Maruti Suzuki, M&M, Volkswagen India

Horns

27%

Bajaj Auto, FIAMM, HMSI

Others

14%

Source: Company, Angel Research

Exhibit 18: Clientwise break-up

OEM mix

% of cons rev FY11

% of cons rev FY15

Bajaj Auto

35%

20%

Maruti Suzuki

12%

6%

TVS Motors

7%

5%

M&M

2%

2%

HMSI

less than1%

6%

Royal Enfield

less than1%

2%

Hero Motocorp

less than1%

2%

Source: Company, Angel Research

July 21, 2015

10

Minda Industries | Initiating Coverage

Profit & Loss Statement

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Total operating income

1,179

1,340

1,706

2,227

2,500

2,889

% chg

23.6

13.7

27.3

30.5

12.3

15.5

Total Expenditure

1,103

1,247

1,628

2,072

2,311

2,650

Net Raw Materials

813

941

1,171

1,478

1,648

1,903

Personnel

134

144

225

288

322

366

Other

156

162

232

307

341

381

EBITDA

76

93

78

154

190

239

% chg

(9.4)

23.2

(16.7)

98.3

23.0

25.8

(% of Net Sales)

6.4

7.0

4.6

6.9

7.6

8.3

Depreciation & Amort.

40

46

59

83

97

104

EBIT

52

58

36

94

115

157

% chg

(18.9)

11.8

(38.8)

163.3

22.6

36.9

(% of Net Sales)

4.4

4.3

2.1

4.2

4.6

5.4

Interest & other Charges

20

19

24

25

31

29

Other Income

16

11

17

23

22

23

PBT (recurring)

32

39

11

69

84

128

% chg

(32.5)

21.3

(70.8)

501.5

22.6

52.1

Extraordinary Exp./(Inc.)

(8)

0

1

16

-

-

PBT (reported)

25

39

13

85

84

128

Tax

0

11

8

19

20

38

(% of PBT)

1.3

28.0

58.7

22.9

24.0

30.0

Minority interest

0

(1)

(1)

(0)

4

7

Associate cos share

4

(1)

1

2

3

4

Pref dividend

0

0

0

0

0

0

PAT (reported)

28

28

7

68

62

86

ADJ. PAT

36

28

6

56

62

86

% chg

5.9

(21.7)

(77.0)

762.9

12.5

38.0

(% of Net Sales)

3.0

2.1

0.4

2.5

2.5

3.0

Basic EPS (`)

22.5

17.6

4.1

35.0

39.4

54.3

Fully Diluted EPS (`)

22.5

17.6

4.1

35.0

39.4

54.3

% chg

5.9

(21.7)

(77.0)

762.9

12.5

38.0

July 21, 2015

11

Minda Industries | Initiating Coverage

Balance sheet statement

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

19

19

19

19

19

19

Reserves& Surplus

267

289

292

360

422

508

Shareholders Funds

286

309

311

379

442

528

Total Loans

160

170

278

210

262

250

Deferred Tax Liability

1

-

-

-

-

-

Other long term liab.

1

7

2

2

3

3

Long term provisions

16

18

24

31

35

40

Total Liabilities

474

516

629

639

765

856

APPLICATION OF FUNDS

Gross Block

518

606

1,073

1,165

1,390

1,470

Less: Acc. Dep.

243

288

673

756

854

958

Net Block

275

319

401

409

536

512

Capital WIP

5

42

22

20

20

20

Investments

23

22

47

29

27

35

Loans and adv.

22

22

21

29

33

38

Current Assets

391

395

481

592

639

813

Cash

67

39

28

30

8

56

Other

324

356

453

562

631

757

Current liabilities

242

290

352

451

503

577

Net Current Assets

149

105

129

141

136

236

Total Assets

474

516

629

639

765

856

July 21, 2015

12

Minda Industries | Initiating Coverage

Cash flow statement

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015E FY2016E FY2017E

Profit before tax

25

39

13

85

84

128

Depreciation

91

44

385

83

97

104

Change in Working Capital

(29)

16

(35)

(10)

(17)

(52)

Others

(1)

4

(3)

6

2

4

Direct taxes paid

(0)

(11)

(8)

(19)

(20)

(38)

Cash Flow from Operations

84

92

353

145

146

146

(Inc.)/ Dec. in Fixed Assets

(113)

(125)

(447)

(90)

(225)

(80)

(Inc.)/ Dec. in Investments

(4)

1

(26)

18

2

(8)

(Inc.)/ Dec. in Loans & Adv

(8)

(1)

2

(8)

(4)

(5)

Cash Flow from Investing

(125)

(125)

(471)

(80)

(227)

(93)

Issue of Equity

(37)

0

0

0

0

0

Inc./(Dec.) in loans

10

10

108

(68)

52

(12)

Dividend Paid (Incl. Tax)

(7)

(6)

(6)

(6)

(6)

(6)

Others

119

1

4

10

12

13

Cash Flow from Financing

85

5

107

(63)

58

(5)

Inc./(Dec.) in Cash

44

(28)

(11)

2

(22)

48

Opening Cash balances

23

67

39

28

30

8

Closing Cash balances

67

39

28

30

8

56

July 21, 2015

13

Minda Industries | Initiating Coverage

Key ratios

Y/E March

FY2012

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

23.3

29.8

129.4

15.0

13.3

9.7

P/CEPS

11.0

11.2

12.7

6.0

5.2

4.4

P/BV

2.9

2.7

2.7

2.2

1.9

1.6

Dividend yield (%)

0.6

0.6

0.6

0.7

0.7

0.8

EV/Sales

0.8

0.7

0.6

0.5

0.4

0.4

EV/EBITDA

12.2

10.3

13.9

6.6

5.7

4.3

EV / Total Assets

2.0

1.9

1.7

1.6

1.4

1.2

Per Share Data (`)

EPS (Basic)

22.5

17.6

4.1

35.0

39.4

54.3

EPS (fully diluted)

22.5

17.6

4.1

35.0

39.4

54.3

Cash EPS

47.8

46.8

41.3

87.6

100.7

120.1

DPS

3.0

3.0

3.0

3.5

3.5

4.0

Book Value

180.4

194.6

196.2

239.0

278.4

332.7

Dupont Analysis

EBIT margin

4.4

4.3

2.1

4.2

4.6

5.4

Tax retention ratio

1.0

0.7

0.4

0.8

0.8

0.7

Asset turnover (x)

2.9

2.8

2.8

3.7

3.3

3.6

ROIC (Post-tax)

12.6

8.8

2.4

11.9

11.5

13.8

Cost of Debt (Post Tax)

12.2

8.1

3.6

9.2

8.9

8.2

Leverage (x)

0.3

0.4

0.8

0.5

0.6

0.4

Operating ROE

12.7

9.1

1.5

13.2

13.1

15.8

Returns (%)

ROCE (Pre-tax)

11.0

11.3

5.7

14.7

15.0

18.4

Angel ROIC (Pre-tax)

12.8

12.2

5.9

15.4

15.2

19.7

ROE

12.5

9.1

2.1

14.6

14.1

16.3

Turnover ratios (x)

Asset Turnover (Gross Block)

2.3

2.2

1.6

1.9

1.8

2.0

Inventory / Sales (days)

25.0

24.4

26.7

26.0

26.0

26.0

Receivables (days)

60.7

59.2

55.8

52.0

52.0

55.0

Payables (days)

75.0

78.9

75.3

74.0

73.5

72.9

WC cycle (ex-cash) (days)

25.4

18.1

21.6

18.2

18.7

22.7

Solvency ratios (x)

Net debt to equity

0.3

0.4

0.8

0.5

0.6

0.4

Net debt to EBITDA

1.2

1.4

3.2

1.2

1.3

0.8

Interest Coverage (EBIT / Int.)

2.6

3.1

1.5

3.7

3.7

5.4

July 21, 2015

14

Minda Industries | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Minda Industries

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

July 21, 2015

15